Core services inflation dished up bad head fakes last time we had this mess in 1966-1982. Mention of a rate hike crops up in a Fed speech.

By Wolf Richter for WOLF STREET.

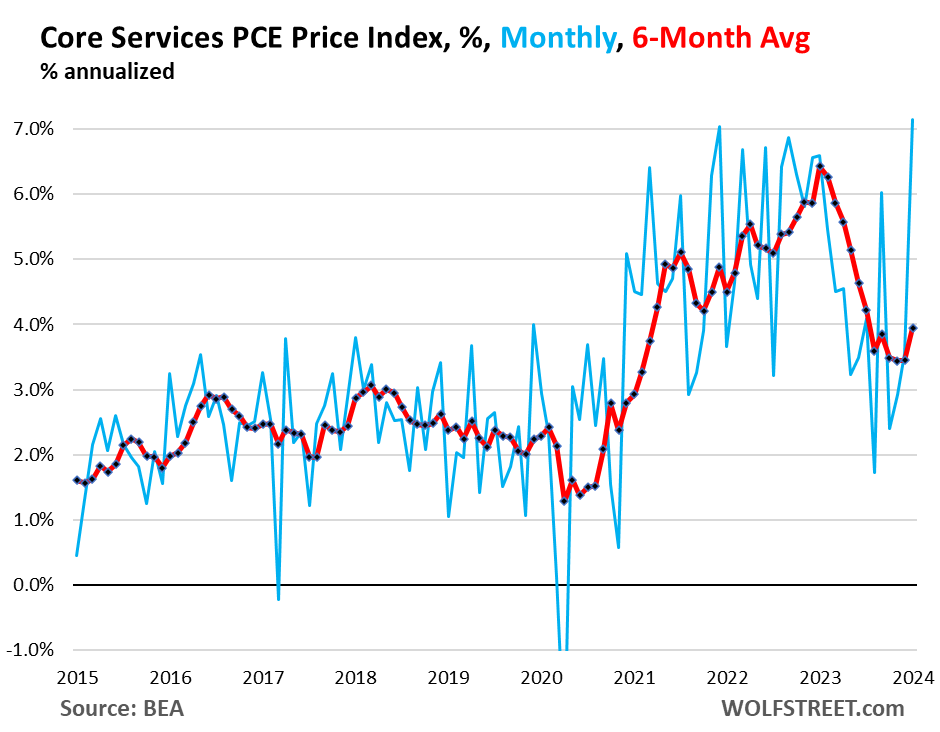

Over the past year or so, the Fed has been intensely discussing inflation in “core services,” which is where inflation had shifted to in 2022, from goods inflation which had spiked into mid-2022 but then cooled dramatically. So “core services” is where it’s at. Core services is where consumers spend the majority of their money. Core services are all services except energy services. Core services inflation has been behaving badly for months, and in January, it spiked out the wazoo.

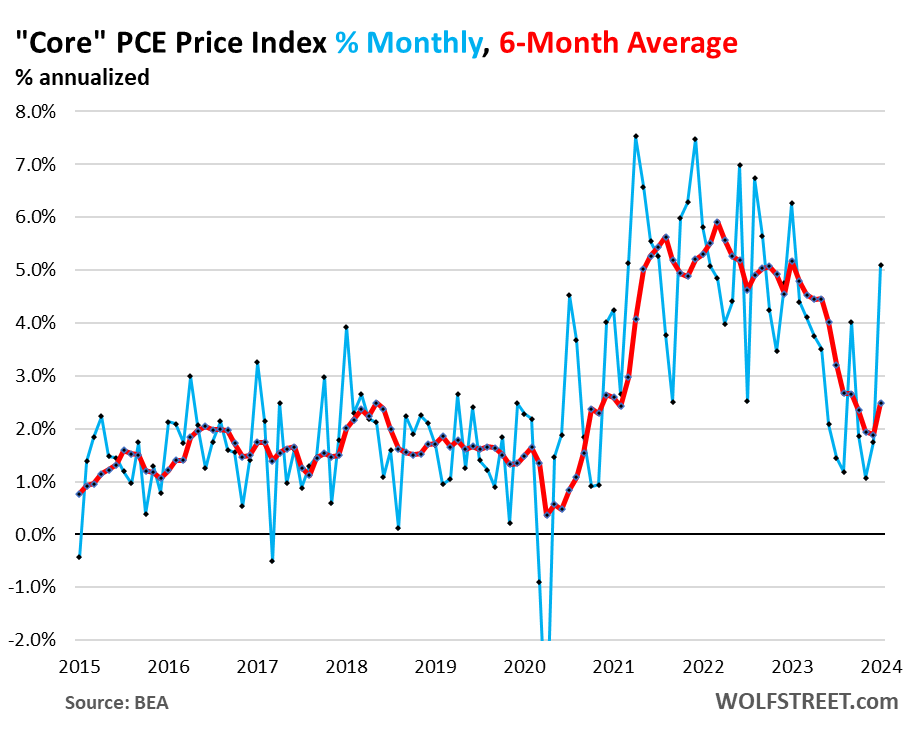

The “core services” PCE price index spiked to 7.15% annualized in January from December, the worst month-to-month jump in 22 years (blue line), according to index data released today by the Bureau of Economic Analysis. Drivers of the spike were non-housing measures as well as housing inflation. More on each category in a moment.

The six-month moving average, which irons out the month-to-month volatility, accelerated to 3.95% annualized, the worst since July, after having gotten stuck at the 3.5% level for three months in a row (red).

The bad behavior of core services inflation that we have been lamenting since June – and which was confirmed earlier this month by the nasty surprise in the CPI – is why Fed governors have said this year in near unison that they’re in no hurry to cut rates, but have taken a wait-and-see approach. And now the concept of rate hikes is cropping up in their speeches again.

For example, Fed governor Michelle Bowman said in the speech yesterday, that she was “willing to raise the federal funds rate at a future meeting should the incoming data indicate that progress on inflation has stalled or reversed.”

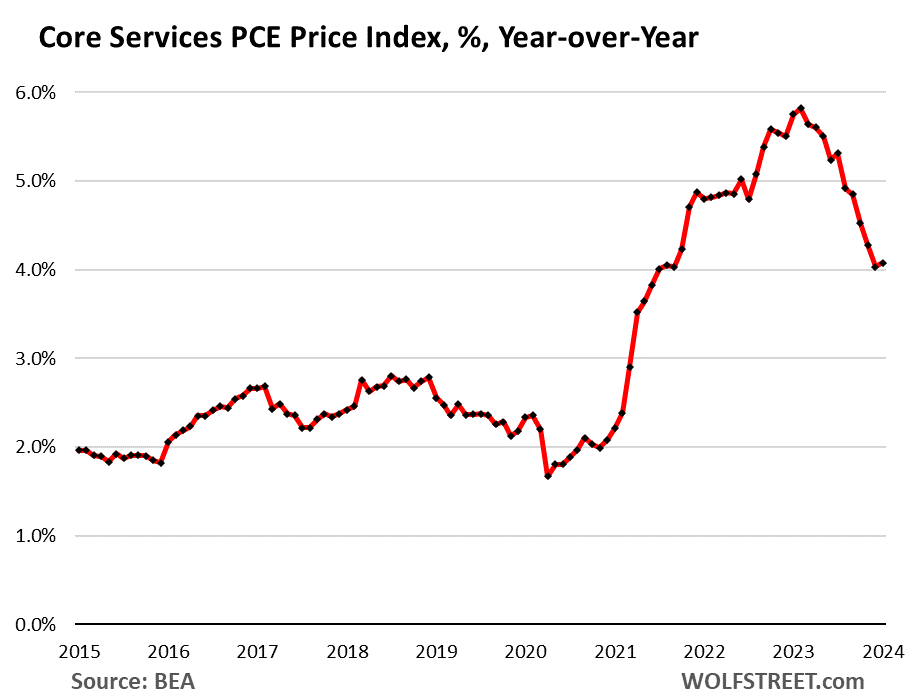

Even year-over-year, core services inflation has now reversed and accelerated to 4.1%.

The 7 Core Services Categories.

Core services – services without energy services, such as electricity – are grouped into seven PCE price indices, and we’ll look at them individually.

This is where consumers do the majority of their spending. The month-to-month data in these categories of core services can be crazy volatile (blue in the charts below), so we’ll focus on the six-month moving average, which irons out this volatility and shows the recent trends (red in the charts below).

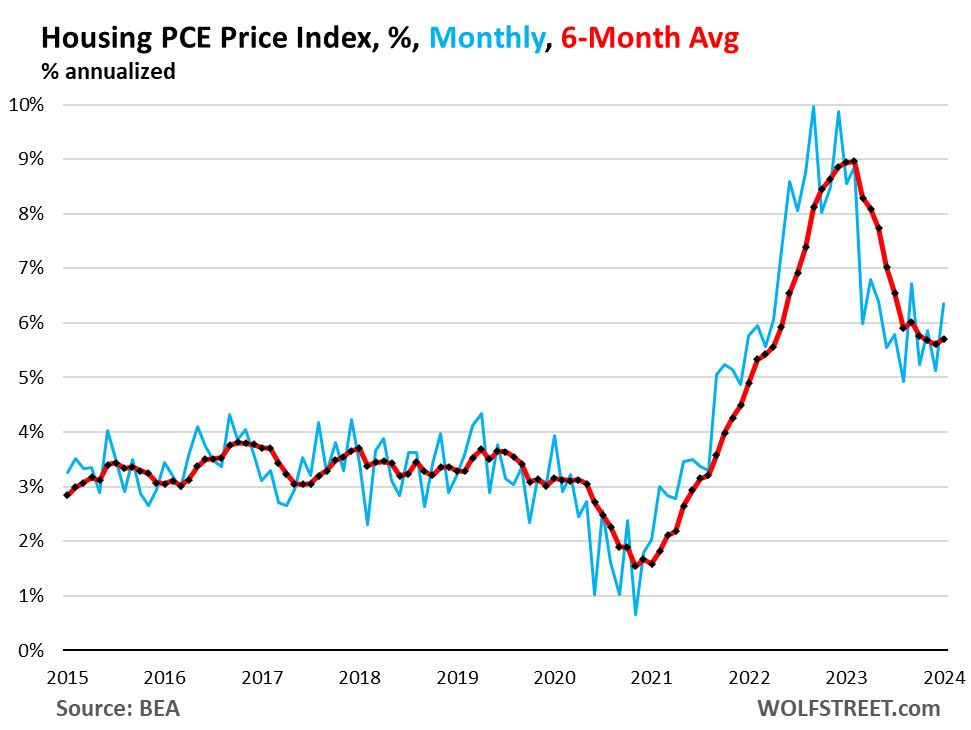

Housing inflation is hot. The PCE price index for housing accelerated to 6.4% annualized in January from December, the worst since September (blue).

The six-month moving average, which irons out the month-to-month volatility but still shows the more recent trends, accelerated to 5.7% annualized, having now been in the same range since August (red).

Housing inflation has backed off from the crazy spike in 2022 and through February 2023. But then it just got stuck at this hot level of 5.5%-plus, and has refused to cool further and seems to be re-accelerating now.

The housing index is broad-based and includes factors for rent in tenant-occupied dwellings; imputed rent for owner-occupied housing, group housing, and rental value of farm dwellings.

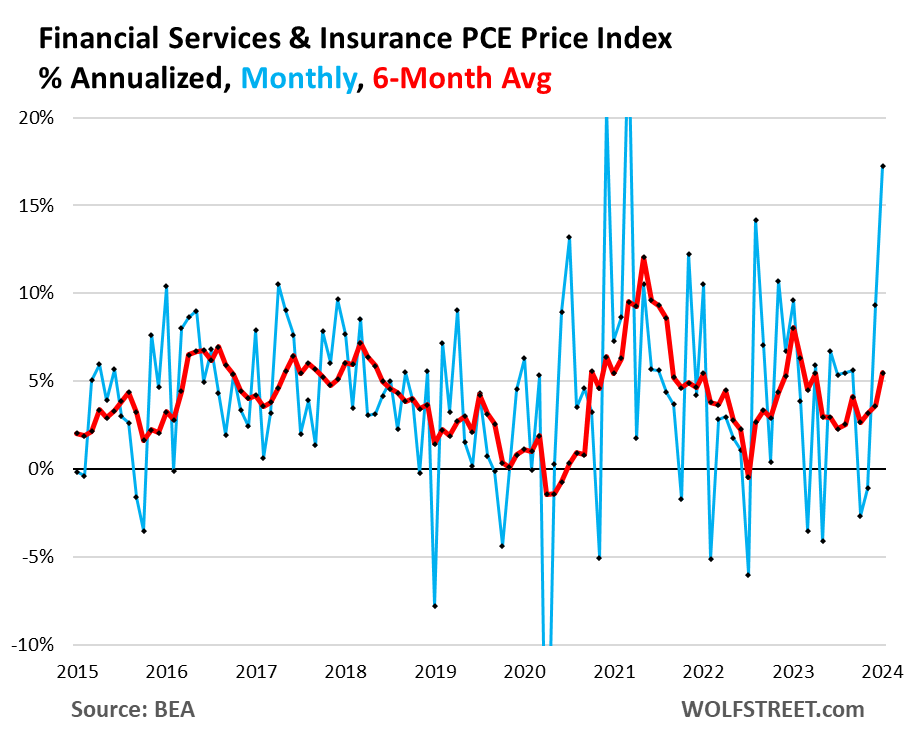

Financial Services and Insurance: +17.2% month-to-month annualized (blue); +5.5% six-month moving average annualized; third month in a row of acceleration (red):

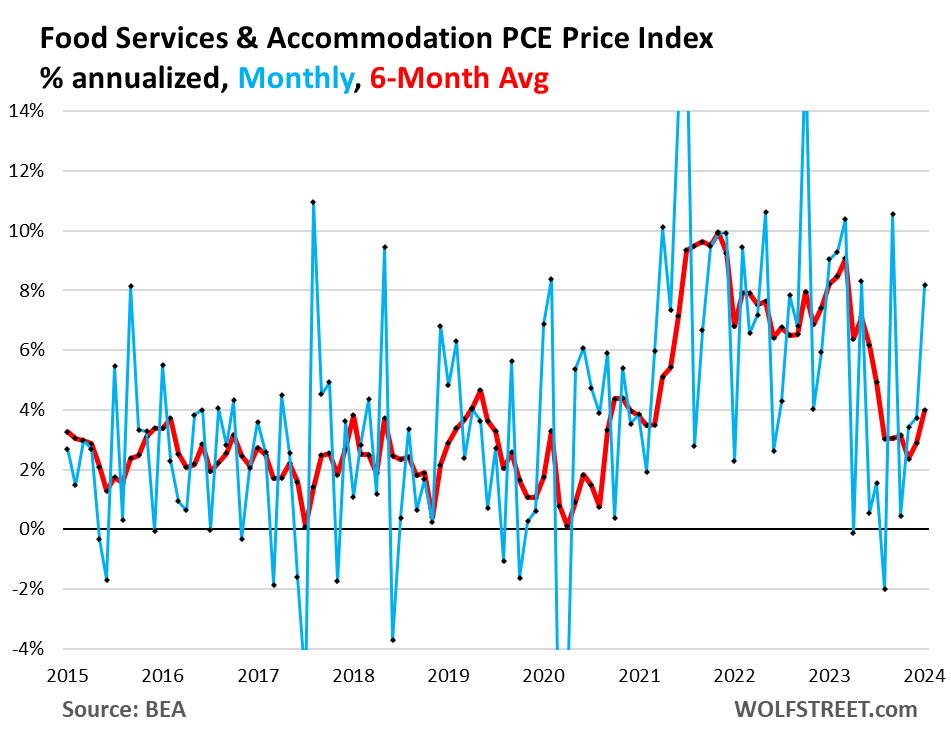

Food services and accommodation: +8.25 month-to-month annualized (blue); +4.0% six-month moving average annualized; second month of acceleration (red):

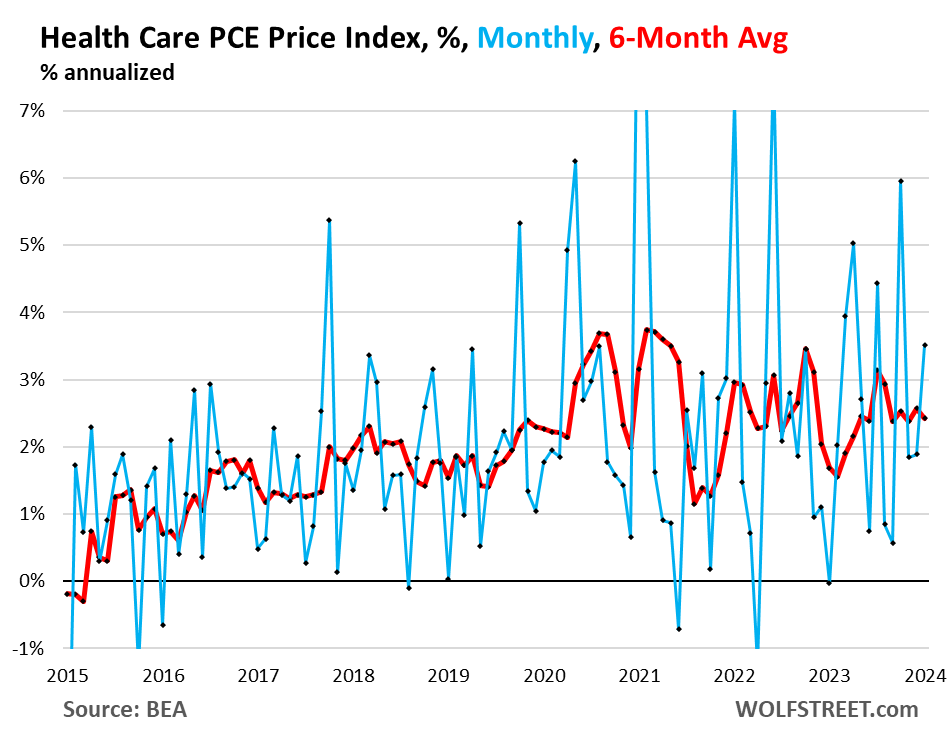

Health Care: +3.5% month-to-month annualized (blue), +2.4% six-month moving average annualized, roughly stable at this rate for the past five months (red).

Transportation services: +0.4% month-to-month annualized (blue), +3.2% six-month moving average annualized (red).

Includes motor vehicle services, such as maintenance and repair, car and truck rental and leasing, parking fees, tolls, and public transportation from airline fares to bus fares.

![]()

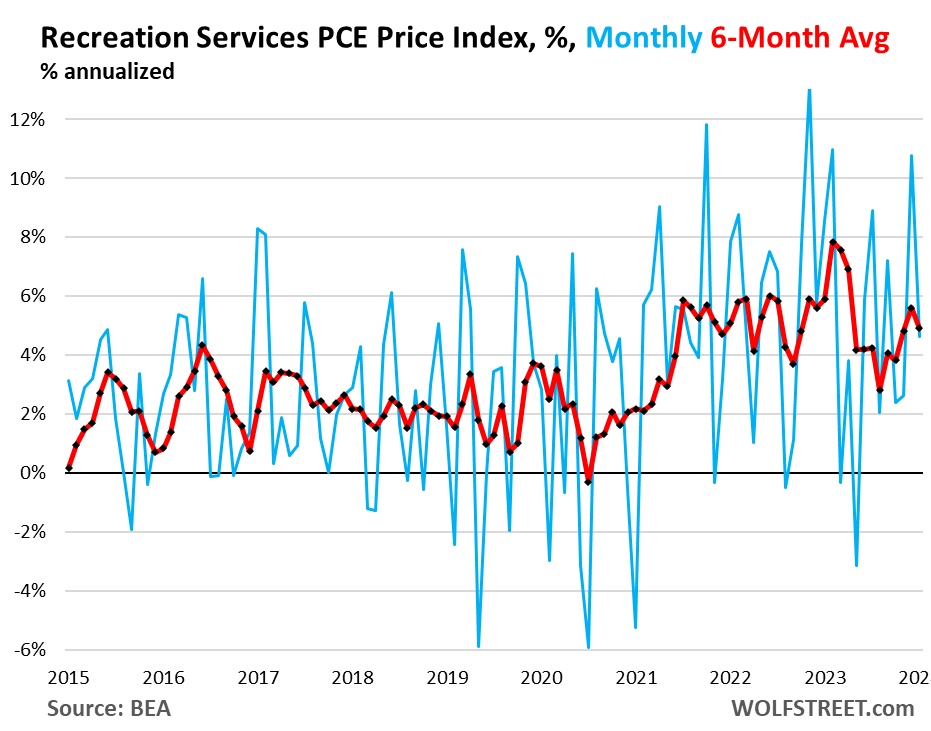

Recreation services: +4.6% month-to-month annualized (blue), +4.9% six-month moving average annualized (red).

Includes cable, satellite TV and radio, streaming, concerts, sports, movies, gambling, vet services, package tours, repair and rental of audiovisual and other equipment, maintenance and repair of recreational vehicles, etc.

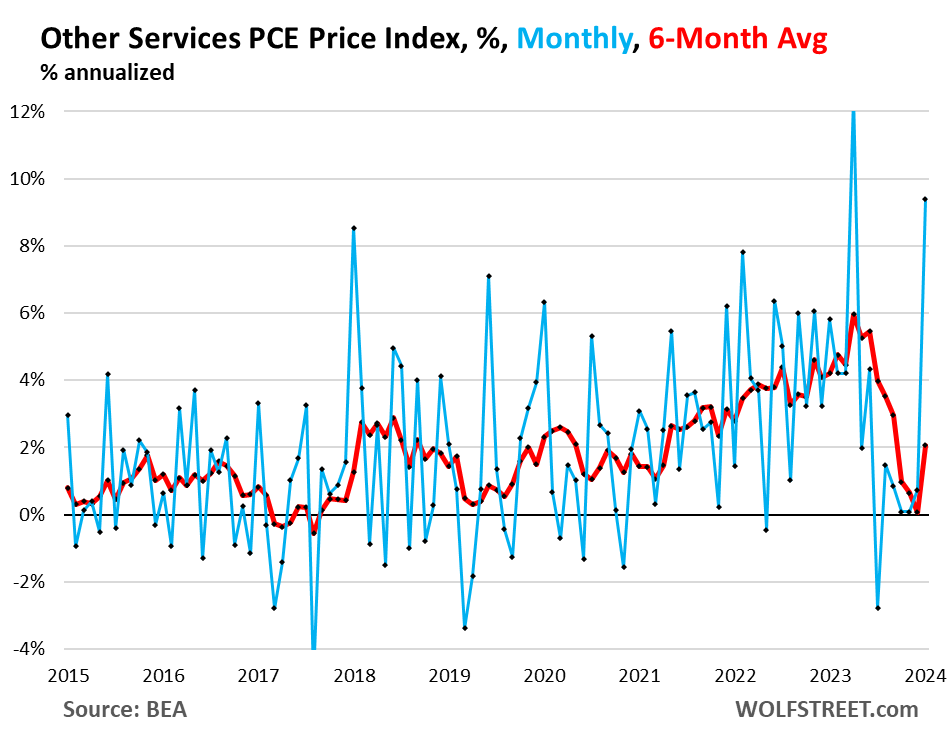

Other services: +9.4% month-to-month annualized (blue), +2.1% six-month moving average annualized (red).

A vast collection of other services where people spend lots of money on, including broadband, cellphone, and other communications; delivery; household maintenance and repair; moving and storage; education and training across the board; professional services, such as legal, accounting, and tax services; union dues, professional associations dues; funeral and burial services; personal care and clothing services; social services such as homes for the elderly and rehab services, etc.

And so the Core PCE price index…

So the Core PCE price index, which includes core services plus non-energy goods, accelerated month-to-month to 5.1% annualized, the worst in 12 months (blue). The six-month moving average accelerated to 2.5% annualized (red).

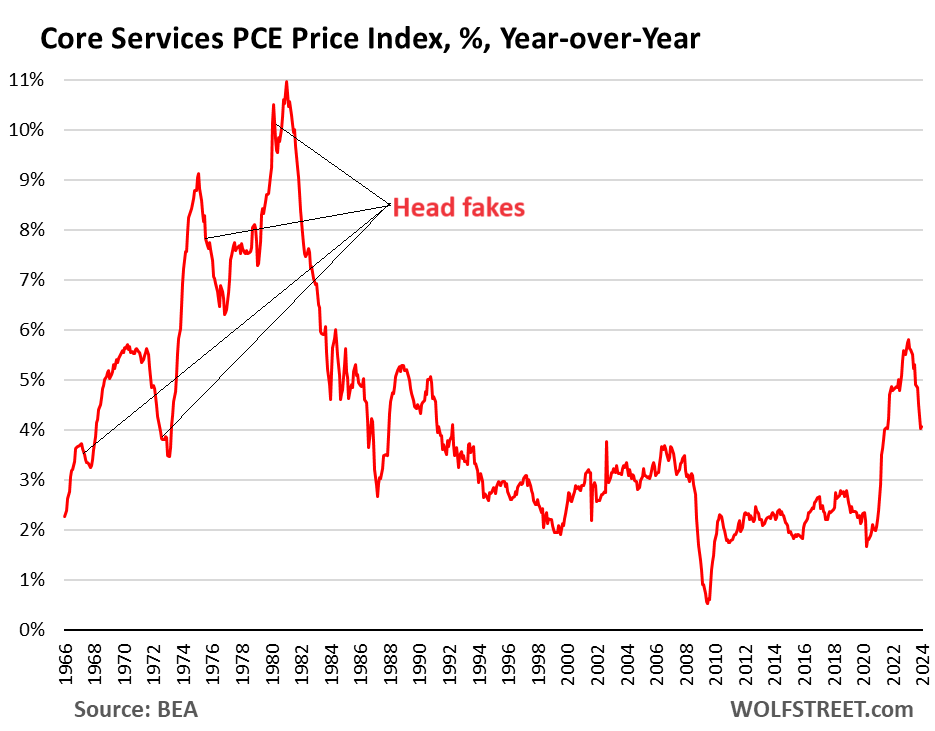

The head-fakes last time.

Inflation in core services is tough to beat, and it can dish up big head-fakes – a fact that Powell has mentioned a few times, hence the Fed’s wait-and-see approach.

Last time this type of core-services inflation occurred – in the 1970s and 1980s – there were clear signs that inflation was cooling sharply, and we thought repeatedly that the high interest rates at the time had beaten inflation back down, which caused the Fed to ease, only to find out that we’d fallen for an inflation head-fake, and then the Fed jacked up rates even further.

The head fakes occurred over the 15 years between 1966 and when core services inflation finally peaked at 11% in 1981. So this is the “core services” PCE price index which excludes energy and the oil-price shocks at the time.

And here is Fed Chair Jerome Powell’s reaction when he saw the inflation resurging in core services, as captured by cartoonist Marco Ricolli for WOLF STREET:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

There is another word in economics that means the opposite of inflation: deflation.

It would be strange and wondrous indeed to live in a deflationary world. Your paycheck would shrink. Products would shave quarters off their prices on a regular basis. Politicians would be desperate for a way to kickstart “inflation” again.

There was deflation during the Great Depression, and supposedly deflation is worse than inflation — although it is questionable whether it is worse than RAMPANT inflation.

The best situation would be to go into a deflationary environment with sacks of money (or liquid assets) and then buy up prime properties around you with your now-inflated cash assets. Just a tip, should you ever find yourself in a Second Great Depression.

My expectation is inflation in cost for the things we buy, deflation in value for the things we own.

GrassRanger,

+100

Excellent summation of how things feel to us too!

I’m stealing that line VBG

how about a “transient” bout of deflation?

Transitory….

Deflation means your purchasing power is increasing as time goes by, all other things being equal. Despite ‘increased purchasing power’ sounding like a great thing, deflation is considered worse than inflation because deflation encourages saving and less consumption (“the stuff I was thinking of buying today will be cheaper tomorrow, why buy today?”) and less work at the expense of more work (“since my paycheck is buying more stuff than it was last week, I can reduce my hours a bit and relax more”).

More saving and less consumption means fewer sales and fewer sales means fewer employed. For those who are employed, they feel less need to work as much, and so productivity falls. In short, deflation brings about less consumption and less productivity.

By contrast, a little bit of inflation is considered optimal because it encourages consumption and incentivises work (increased productivity).

“By contrast, a little bit of inflation is considered optimal because it encourages consumption and incentivises work (increased productivity).”

LOL!!!

If people have to work more for necessities, they will have less time to innovate. Innovation is where real gains in productivity come from.

This is why eCONomics is, and will ALWAYS be a social science, not a hard science.

“If people have to work more for necessities, they will have less time to innovate.”

I don’t think people who need to work more for necessities are giant producers of innovation on a meaningful scale. As you said, LOL!!

“This is why eCONomics is, and will ALWAYS be a social science, not a hard science.”

The CON caps are quite unbecoming.

Comprehension isn’t your strong suit. That’s EXACTLY what I said. People who are working just to get by, cannot innovate. Thanks for supporting the thesis (although you clearly didn’t understand).

LOL indeed!

Wonder when we will “innovate” and get VAGRANCY LAWS?

Man! That will sure surprise the MAGA bunch!!!!!!

Ever see a pic of those 7 cent flophouses from the Gilded Age? Or poor houses in our corp-government model England?

Deflation is awful. Look how it has destroyed the computer industry. Why buy a 1TB SSD when you know you’ll be able to get a 2TB SSD for the same price in a couple months. My first Macintosh, the lowest-priced model, cost $2,700, and today you can buy a new Mac with 100 times the performance but Apple can only get $499 for it.

Are you kidding?

Computers for everyone, and better computers every year for everyone.

It’s about as close as taste as we can get to a post-scarcity society. Deflation is wonderful.

And don’t pity the poor tech companies. Computer stocks are at an all time high – Dell just surged 25%. Deflation forces companies to innovate to stay ahead rather than rest on their laurels and rent seek.

Imagine if the same thing happened to real estate. Realtors and house scalpers would weep and gnash their teeth, and young people could actually afford a place to live – both positive changes for society.

Deflation changes the world for the better.

Carlos, Colinsky was being sarcastic…

How do you “know” government numbers are a joke? Have you studied and recreated the methodology over decades to prove it? Or do you just buy into ‘i could do everything better than the government’ meme & extrapolate memorable anecdotes from your own life to be equal to methodical study?

Most people do the latter.

The government publishes “Consumer Price Indexes” with consistent, disclosed methodology. It’s sampled data so it cannot be perfect, but it is the best anyone has come up with so far to describe how an “average” american experiences the cost of living. And this “average” cost of living is chosen to represent overall price inflation.

If you or anyone else could come up with a better methodology for price indexing, go ahead publish it and win a nobel prize.

Lol, you sound pretty butthurt that people don’t buy into the lies. That’s just too damn bad. As far as methodology, how about listing the revisions to their methodology over the last 20-40 years? Should be a short list right? LMAO!

And the whole notion of the fed changing what it supposedly cares about every few years just adds to the joke that they are. Cpi, core cpi, core services cpi, pce, super core, super duper gigundo core with a twist is probably the next thing they’ll emphasize. All signs we’ve gone full idiocracy and the Empire is in its terminal phase.

Great tip.. be sure to have sacks of money..

Yep, deflation is good for savers. Inflation is good for borrowers. And we all know America and Americans are heavy borrowers. Sad thing is that we’ve been told that slow and steady wins the race and that gamblers can’t win long term. But endless bailouts and money printing have been screwing the conservative investor and encouraging risky bets for decades.

Ever think of what would happen to all those colossal debts ($35 trillion and, now, an extra $1 Trillion every three months) in a Deflationary environment?

p.s. – you can’t deflate in near-wartime situation.

I’m not sure there is much more to say except.

Lol.

Until FRB can stop bailing out because they fear systemic issues, the moment investors won’t be front-running bailout, thus easing financial conditions and fuelling inflation.

Couldn’t agree more. There is an ultra-bull market. FED showed that its hand is weak last year. I think Pow will have a lot of cows in this market. Bulls are in full charge now and buying in full speed. They are not afraid of high rates, QT, geo risks, anything at all. Bulls have the upper hand for more than a decade and now more than ever.

They have the upper hand only because they have created this cognitive dissonance that inflation will go away on its own.

Folks! A secondary inflation bounce is normal. You all know that. Buy on all market dips.

They have the upper hand because the Fed doesn’t have the stomach to take it away from them. And they know it.

Pea Sea, I guess that’s the $64k (which will only buy a loaf of bread soon) question.

Long term, the Fed can protect markets or they can protect the dollar, but they can’t do both. And if we lose the reserve currency status (and no, I don’t buy the cleanest dirty shirt argument), their power is all over.

Sam

You are the problem. Can’t wait for it to implode. Wall Street needs to disappear. Go visit CNBC where you belong.

Since 2020, the Personal consumption expenditures: Services: Housing and utilities, has soared and it’s still soaring! In my opinion this particular index is of prime importance, given the sharp increases in house prices and gas and electric utility bills.

There are now the Have All and Have Nothings. Rent, insurance, utilities, and food costs take everything. Inflation is now making the lower income grovel for daily life.

Government is the cause. Yet they all keep being voted back into office year after year. Enjoy.

When the markets reach this level of bullishness & animal spirits, it’s pretty hard to stop without an earnings recession, or a full-blown economic recession alongside less-than-expected rate easing.

Greenspan had to raise rates all the way to 6.5% in 2000 (with inflation running around 3%) to pop the first internet bubble. From 1995 to 1999 the markets just shrugged everything off, including the 1997 Asian financial crisis & a secondary rate hiking cycle from 1998-2000.

I’m not sure about that. It’ll stop quickly if it starts dropping, even a little bit (say 5%) and the Fed doesn’t come to the rescue, as it has for the past 15 years.

Yup.

Go and look at when housing started to accerlate in 2023 and it is right in line with when the Fed and Gov’t started bailing out banks.

Now people are buying assets to get ahead of the super growth that is coming when the Fed cuts rates and goes back to QE…

JPOW, if they do that, you can either watch yields at the long end of the bond market blow out or you can watch the dollar go goodbye.

No one would be willing to buy 30 year treasuries at 4% if they thought 6-8% inflation per year was coming back.

…how do you think the TLT got from 160 to 90???

Howdy Jpow. You should pull a Greenspan and drop in March, then raise in June, then raise again or maybe drop again. A perfect tool to use …. Then we should really be having some fun.

Correct, remember all wars are bankers wars.

Excellent work Wolf. You have been ahead of the curve on the very important Inflation analysis

Agreed!

Agreed.

Why did the 10 Year Treasury still drop after this latest release ?

Wondering the same. It pumped then popped.

The headline CPI numbers were inline with expectations, so markets had adjusted rates earlier based on expectations. It probably dropped because the markets were relieved the CPI numbers were not worse. The markets do this kind of stuff all the time. The markets are basically nuts.

Don’t read too much into intraday movements. Zoom out and look at the longer-term trend.

Expectations for future economic activity and inflation.

The post-hoc, hand-waving explanations are always hilarious to me. Notice those explanations are never provided beforehand as predictions.

I prefer the simple explanation. The 10 year falls because the so-called ‘smart money’ is hedging, to some degree or another, for a recession or weaker anticipated future economic growth. They know, as I’m sure you do, that in general a recession, or a long slowdown, will bring rates and inflation down from wherever they were before with a slow down will come moves to ‘safe’ assets.

An increase in yield would mean that on net the market expects increased economic activity and inflation.

I don’t know why these are called smart money.

In the last 3l4 years these folks trading long bonds lost lot of money.

I know you know this but… many people who trade bonds do not sit on unhedged long positions. I am always amazed when I read these stories of banks losing billions because they didn’t hedge their bond portfolio even as Fed rates were at a historic low and inflation was starting to rear its ugly head. What did they think was going to happen?

The same sideways movements. Until Yellen adjusts issuance across the curve, the long end seems to be fairly stuck. Everything main stream harps on rate cuts–who ultimately cares if they’re running a $1.7T deficit. That level of issuance is going to keep rates afloat higher for longer. The question is, if the Treasury adjusts and issues more on the long end of the curve, what to 10-20-30’s look like then? And what do mortgage rates look like then?

I wonder how much of this is driven by churn in the labor market? I’m booked solid for months and turning down work. Many of my clients can’t fill positions and have lost experience in key positions since covid.

I am curious. What type of industry? Construction, High Tech, ?

This is why I love Wolf Street. Everybody else “Inflation is under control and we are on schedule for a June rate cut” Then we get the real data from Mr Richter. Its unreal how much BS the spin doctors come out with on CPI and PCE days.

No one that lives in the real economy believes inflation is declining.

The government has so contorted the measurements of inflation even they probably do not know the real situation.

I doubt Jerome Powell has any concern. He is rich and insulated from his own mismanagement.

I’m just giddy to see what happens to the price of oil once the Houthis step over that line and force us to engage with Iran directly.

That’ll kick inflation into high gear. With each month that passes, rate hikes become more & more likely. Higher for much, much longer than the street wants to admit.

The labor market remains extremely buoyant for the Fed to lower rates. It’s nowhere near that scenario. Continuing claims will have to rise at least another 300K for that to begin to filter into reality.

The US is the largest oil producer in the world, and a net exporter. If there is even a brief spike in global oil prices, US frackers are going to ramp up production and that’s the end of the spike. Profit is a huge motive to over-produce in the US of A, which will cause the price to collapse again.

The situation in the Red Sea affects Europe much more than the USA.

U.S. response to death of personnel IN SYRIA signals it’ll be very reluctant to escalate before the election

Agree 100%, enough so that I am going to continue to keep a lot of cash parked in T Bills of 4-week to 13-week maturity and thereby enjoy risk-free interest rates of 5.4% or more, free of state tax. The Wall Street Journal ran articles this week about the need to lock in rates for the long-term and about the growth of long-term bond ETF funds because the Fed is going to bring rates down soon. How many months in a row are the people at the WSJ going to run stories about the imminent drop in interest rates before they hold themselves accountable for bad reporting and analysis?

Agree with Steelers Fan, that is. With due respect to michael, my feeling about Powell is somewhat less negative than michael’s.

WSJ, Thomas.

Free bad advice can come at a very high price.

Well said. Never forget – WSJ publishes the news that people want to read. There are a lot of banks sitting on unrealized losses in their bond portfolio. They are desperate for the Fed to start lowering rates so that it will unwind some of that perceived risk. I am with you – I have been rolling over cash in 13wk TBills for almost a year now. Equities are too frothy for me at the moment. I would rather WSJ write an article titled “When are banks going to learn how to hedge their bond portfolios?”

Core CPI month-to-month is 5.1% annualized. Average annual 1971-2022 was 3.90%. Average Fed funds rate for the same time period was 4.86%, a little below current level. My point is core cpi, based on this month’s data, is through the roof historically. If Fed funds rate has any impact on core cpi, it has to go much higher. Doing a little math: (4.86/3.90)*5.1= 6.4%. So core CPI at 5.1% should have an associated Fed funds rate of 6.4% historically. Higher is needed to slow core inflation, if it has an impact at all. Of course this is just one month of core CPI data, but it is . . . interesting.

You can’t just annualize the monthly figure, because inflation data is noisy & volatile, and inflation is seasonal. January inflation historically tends to be high as the holiday discounts are unwound. The month over month inflation readings are seasonally adjusted, but it seems like the adjustments aren’t enough to completely offset this effect, at least in recent years.

I can do whatever I want. Sure, annualizing a one month figure is risky, but so is any prediction. We will have to wait a few months to see if there are some convincing trends in core PCE and core CPI.

If it doesn’t rain where you live tomorrow does that mean you must be living in a desert?

There’s a reason why it’s sensible to look at periods of time and averages rather than individual data points…

Not asking for financial advice, just a general inquiry about the way things work- if someone paid an early withdrawal penalty on a bank CD, can that penalty be used to offset income/capital gains taxes in the same manner as a capital loss from selling stocks? I read that it can, but specifically can the penalty be used as a Capital Loss Carryover for any tax year in the future like with capital loss from stock sales, or can it only be used for the tax year in which the penalty occurred? Also more specifically (lol) is there a difference if the CD was closed several months after opening it vs. a CD that was closed early a year or more after opening? Thanks in advance for any responses.

Don’t the banks usually just deduct the amount of the penalty from your interest when you do an early withdrawal?

See Schedule 1, line 18. That is where you put any early withdrawal penalties.

That sort of helps but does not quite answer the question of whether the withdrawal penalty can be carried over indefinitely into future tax years the same way as a Capital Loss Carryover from a stock sale

I don’t think the early withdrawal penalty is considered a capital gain or loss. If it was, it would be somewhere in Schedule D or Schedule D instructions. Just as interest on savings is not considered a capital gain (I wish it was, because interest is treated like normal income, which can be in a much higher tax bracket). Of course, I am not a tax adviser so I could be wrong. You can always consult with a financial advisor or phone the IRS if you want to risk an incorrect answer to your question.

As a heads up, before you buy a CD you must completely understand their early withdrawal penalty rules. They vary tremendously from one bank to another.

I would guess no. That early withdrawal penalty is probably a fee in the eyes of the bank. Same category as e.g. an overdraft charge.

If you bought a bond and sold it for a loss before maturity, that would be a cap loss.

When I type, ”cd early withdrawal penalty tax deduction” into google, the first answer says, ”You can deduct the amount you withdraw from your penalty, which may offset how much you pay in taxes on any interest earned, according to the IRS. So, if you earned $70 in interest, but you paid an early withdrawal penalty of $30, the full $30 can be deducted on taxes.Apr 22, 2023.”

The only thing I cannot for the life of me find an answer to is whether I can carry over the penalty to a future tax year instead of the tax year in which the penalty occurred.

Don’t have a cow CD but a “future tax year” might be wishful thinking. Good luck

The way I read it, the need to carry over the penalty would be a very unlikely scenario. In the case you quote, the penalty is deducted from the taxable interest, ie. taking the taxable interest from $70 to $40. The carry over scenario would only apply if the penalty exceeded the amount of interest earned.

I don’t think I would purchase a CD with that type of penalty.

So you might be able to deduct it from your other interest income, but that’s still different than capital gains which are taxed differently.

Doubtful that you can carry it into another year. Same thing with cap gains, that’s why tax loss selling at the end of the year is a thing.

Not to sound judgy, but I generally recommend only committing to fixed income products like bonds & CDs if you’re confident you can hold them till maturity.

It’s an above the line deduction. I don’t think the concept of carryover exists because it would be extremely unusual (potentially impossible) to have a penalty that exceeded interest and dividend income for a year. Can the penalty ever exceed the interest? I don’t deal with CDs often.

C,

The penalty can feasibly exceed the interest income if, for example, the CD is closed in January after very little interest is earned for that tax year. CD interest is taxed annually regardless if you receive the interest, so interest earned in the prior year will already have been taxed.

CD Capital loss carryover ?,

I copied the following from the IRS website:

“Instructions for Forms 1099-INT and 1099-OID (01/2024)

….

Box 2. Early Withdrawal Penalty

Enter interest or principal forfeited because of an early withdrawal of time deposits, such as an early withdrawal from a certificate of deposit (CD), that is deductible from gross income by the recipient. Do not reduce the amount reported in box 1 by the amount of the forfeiture. For detailed instructions for determining the amount of forfeiture deductible by the depositor, see Rev. Ruls. 75-20, 1975-1 C.B. 29, and 75-21, 1975-1 C.B. 367.”

Me again. Since an early withdrawal penalty is deductible against gross income there is no need for a carryover. I imagine it is exceedingly rare for the penalty to exceed a taxpayer’s total gross income. Capital losses are granted a carryover because of the $3,000 cap on deductibility. No such cap applies to early withdrawal penalties since interest is treated as ordinary income. That said, consult your tax advisor.

An early withdrawal penalty is not considered a capital loss. It is considered a reduction in your interest income – and is not reported on your taxes since you receive the net interest income from the CD issuer. Put differently, it’s like the CD issuer says “I will pay you x% interest… BUT if you hold your CD for a minimum of 24 months, I will pay you x% interest PLUS an early withdrawal fee (that you never used)”. Does that make sense?

I see services inflation at double digits right now. Look at homeowners and auto insurance rates for starters. Up 20% and 44% respectively. Wouldn’t be surprised to see Core Services PCE spike further. There will be no rate cuts this year. More likely is a rate increase. The only thing that will change this is severe recession.

Pure price gouging in the insurance sector. There was built-up pressure in the markets (both services and goods) after years of 2% inflation but 44% is simply out of this world.

New vehicle prices are up 20%, the value of their float in bonds is down 40%, there are more drivers, more accidents, and, on top of it all, more natural disasters. The industry is getting absolutely hammered on all fronts. The profit margins of public insurance companies like Progressive are about the same as they were pre-pandemic.

Just received USAA home insurance bill for new year: 1800 annual now 2600! Dropped ‘em for farm bureau and saved 600. After 25 years, they have lost all our accounts: banking, business, and rental policies.

They don’t care of course, but it’s all I can do and if everyone did the same….?

Exactly. I am seeing the same thing. That is why a 5% treasury does not cut it and I am not content with that type of return. I need higher yields on my investments.

I read Hotel revenue per rooms are 5.9% YOY. That also tells you that inflation is not low as low as advertised. Average room is now $153 / night. in 2010 it was $96.

ru82,

1. You said “exactly” but didn’t even read what Pilotdoc wrote. Pilotdoc wrote that they switched insurers because their insurance company jacked up the asking rate. So Pilotdoc is now paying LESS. That’s not inflation. It’s a lesson on how to deal with price increases; and you chose to not read the lesson because it doesn’t fit your narrative.

2. “I read Hotel revenue per rooms are 5.9% YOY. That also tells you that inflation is not low as low as advertised.”

This the kind of uninformed inflation nonsense just drives me up the wall. Revenue per room is a factor of the amount per room AND the occupancy rate. So hotels could cut room rates (deflation) and therefore increase occupancy rates, and revenues per room would increase.

Inflation discussions bring out the most uninformed BS. I block a lot of this BS because I’m tired of dumb shit and I don’t want to waste my time shooting it down. This crap belongs on X, not here.

These are broadly in-line with replacement costs so it shouldn’t really be a surprise.

Hell, food prices are absolutely raging. Every dam thing is higher now at each visit to the store. Milk, eggs, etc. The inflation figures from the gov are bullshit.

Inflation was good and the “risk on” mood set in because PCE was “as expected”. Just the same trick, lower earnings estimates and let every company beat them. Increase the inflation estimates so results as bad as expected turn become great.

This column is worth another Wolfstreet donation.

Powell Burns destroyed the price stability and the welfare of the people.

Fed is a total failure.

What a mess for the workers, savers and retirees.

Don’t forget about us wannabe homebuyers. We’ve been screwed for years, just looking for a window of time to buy without destroying our financial future.

“That’s why they call it the American Dream, because you have to be asleep to believe it.”

In the UK it isn’t a cow but kittens. Interesting visual and equally confusing to cows.

Not much reaction other than “just as we expected” it seems with most sources.

I remember those times in the 70’s and 80’s well: Nixon’s attempts at wage and price freezes, Ford’s “whip inflation now” [WIN] buttons, and Carter wearing a sweater around the White House. Carter possibly sacrificed his chances at a second term by dumping the then Fed Chair into the Treasury Dept and appointing Volker as the new Fed Chair to finally get a handle on inflation. If they takes 15 years to get a handle on it this time, I won’t be around to see the end of it.

The military had an attempted rescue in progress for the Iranian held hostages, a “SNAFU” occurred , or didn’t occur. Had the hostages been freed, Carter would have won re-election.

The Great Kahn! The moral equivalent of war. The malaise. Thank goodness U.S. is net exporter now.

Wolf, if you were the Fed Chair, what would you do right now? In terms of FF rate, balance sheet, BTFP, whatever.

Thanks

Howdy Peter G. If that were the case, he would have been assassinated before one word left his lips.

I’m not Wolf but I really don’t think the constant chatter about rate cuts coming from FOMC members is helping matters. This morning, as the stock market turned negative, Raphael Bostic said he still expected rate cuts could begin this summer, and markets rebounded.

At this point, Wall Street doesn’t even care about “higher for longer,” as the delay in rate cut expectations from March to June wasn’t accompanied by any significant selloff. Earnings growth, AI mania, the resilient economy, and pent-up investor demand have been driving up animal spirits on Wall Street, with or without rate cuts. All rate cut chatter does is pour more fuel on the fire, and in a worst-case inflation rebound scenario further erodes the Federal Reserve’s credibility.

They need to stop talking period, whether about cuts or hikes.

The Fed just needs to do its job as a truly independent body and STFU.

My personal belief though is that they’ve become so addicted to the power and attention that they can’t stop parading themselves in front of TV cameras.

The Fed is not a “truly independent” body. When you realize this, you can somewhat understand the strange and apparently stupid things they do. There is no such thing as an independent body. Everyone is a reflection of their environment and how that environment changes. Powell is a political appointee. I am sure his lawyers own plenty of stock for him.

The most common occupation for FOMC governors after leaving public service is going on the Wall Street speaking circuit. Janet Yellen did this in the years between leading the Federal Reserve & U.S. Treasury, making tens of millions giving speeches to Goldman, UBS, etc. It’s an easy way for them to make quick money without being technically going through the revolving door & actually working for the same firms they previously regulated. It’s for this reason they’re constantly yapping to the media.

The second most common occupation, of course, is actually working for a financial services or fintech company, eg Ben Bernanke & Richard Clarida are now PIMCO managing directors despite their academic backgrounds. The optics look worse, which is why they usually wait for their names to fall out of the news cycle before signing on.

Howdy Jackson Y. Research what Greenspan did after her left. I think you will find that interesting also.

Jackson Y, yes. I personally think these people are traitors who belong in detention camps, but at the very least, they should be prohibited from speaking publicly.

Jackson Y-

It seems the occupational shift you describe is mighty close to that which is commonly referred to as “the oldest profession in the world.”

The revolving door between banking, academia and DC has the whiff of the brothel to it…

I think the Fed is scared to death of all the 10x leverage out there, and that’s why they telegraph everything out so far into the future. Of course, this behavior will just lead to 15x leverage down the road, but they can’t think about that right now! Lol!

As of October 2023, “Leverage at the largest funds was significantly higher, with the average on-balance-sheet leverage of the top 15 hedge funds by gross asset value rising in the first quarter of 2023 to about 17-to-1”, from the Federal Reserve financial stability report. Leverage hasn’t been just 10-1 sincr 2016. My bad.

The problem the “markets” have is that rate cuts to 4% over the next few years aren’t enough to justify current valuations.

They need rates to drop back to 0, and I see no evidence this will happen anytime soon.

Anytime soon???

I feel “never” may be more like it.

Bostic must have bought call options before the speech and then sold it after the speech.

All the FED members are front running the market and making money.

All the rate cut chatter is there for a reason.

The peasants need to understand the game.

Bostic repeated what he has been saying for months: if inflation continues to go down, 2

hikescuts in the second half, no hurry.But inflation may not continue to go down, as we can see.

Wolf, but this raises the question, why is Bostic positing these conditionals at all? If he’s going to lay out hypotheticals as to what would lead to a rate cut, why not lay out hypotheticals as to what would lead to a rate hike?

It’s becoming harder and harder to believe that they’re doing anything other than trying to jawbone the market up.

@Wolf – I think you meant “cuts”

yes.

The first thing to do is take the rate cuts off the table for 2024 to get some breathing room. But the Fed chair isn’t a dictator. The members of the rate-setting committee vote. So Fed chairs alone cannot do much of anything. They have to schmooze and persuade the other FOMC members of their point of view.

Also, there is this political reality where certain members of Congress scream at Fed chairs, and even Presidents do, for being too tight in their policies. Politicians love free money for their vote-buying schemes. And so Fed chairs have to walk that tightrope.

So it’s a good idea to let the inflation data pile up, and when everyone can see that inflation is re-heating, and people hate it and get pissed off at the President over it, then there’s political backing to crack down further. Maybe I would just sit here, twiddle my thumbs, grin dumbly, and say wait-and-see over and over again until inflation is bad enough that politicians, now fearing for their jobs, would want me to crack down.

Thank god I don’t have that job!

Clearly the right way of handling it is confusion so the Fed has more months to look at the data before reacting. Powell gives another dovish statement about good progress and a likely rate cut by the end of the year. But the dot plot will show almost half the voting members wanting 2 rate HIKES, with the median being a single cut in 2024. That will confuse everyone and allow the media to keep up the misinformation.

Completely agree!

Thank you wolf!

Wolf,

Do you have any insights on why the bond market isn’t reacting to this (yet)?

My feeling is that for the last 40 years, interest rates have been on a downward trend, which combined with a generally upward sloping yield curve, allowed for bonds to provide substantial capital gains as well as interest payments.

This has caused the bond market traders to become dumber than a granite countertop, since there were 2 independent mutually reinforcing sources of capital gains (especially the normal yield curve, which caused long bonds to always become more valuable as they moved to the short end of the curve). Plus, as a bonus, during recessions bond prices went up.

Bill Gross even talked about being a beneficiary of these effects in his pioneering of a “total return bond fund”, and how a lot of his success was being in the right place at the right time.

The question becomes what could shake things up and cause the bond vigilantes to make a comeback– it took about 4 to 5 years during the Great Inflation, and we are almost 4 years into this now.

Do you see this reversing anytime soon, or do you think we will actually need a full on inflationary recession to bust through this complacency?

Thoughts?

“why the bond market isn’t reacting to this (yet)?”

The bond market has already reacted — a little. The 1-year yield is back over 5%, the 10-year yield is at 4.28%, up from 3.80% in December, mortgage rates are back over 7%, etc.

Looks like the 10 yr Treasury yield did a head-fake from 5.1% to 3.8% — mimicking the head-fake in CPI — and has now rebounded to 4.2%. Trading the bond market squiggles is a fruitless game, as far as I’m concerned.

For the 10 year note, the primary trend (up for yields/down for prices) appears to be intact, but time will tell…

If and as rates rise, I will slowly expand my maturity horizon, expecting that some future Fed in some future year, reacting to some future crisis, will throw what caution remains to the winds. I’ll vote with my portfolio duration.

In the world of authoritative monetary manipulation, some things are more predictable than others.

Waiting to crash with stocks in a few weeks.

Gotta sucker everybody in first!

The Treasury has been skewing new issuance towards bills to avoid too much supply and long rates rising too quickly. However they have since increased coupon issuance somewhat per the last quarterly refunding announcement.

I also bet that any significant stock mkt crash would cause a flight to safety, putting a floor on bond prices.

That said, I still think long rates will eventually climb above the Fed’s policy rates.

I think you hit the nail on the head. Likely the turn will have to come when tax receipts continue to drop to a level where coupon issuance needs to rise to meet funding needs.

If the Fed cuts rates, it might trigger a move higher in longer term rates with these inflation readings (meaning fewer bond investors willing to invest).

Do you have any thoughts on timing?

“Not as quickly as most WR commenters would like” would be a pretty good bet.

Right. The Treasury doesn’t like to keep more than 20% of outstanding debt in bills.

I’ve been thinking about another potential ceiling on bill issuance. While bill demand is somewhat inelastic (being equivalent to cash), I wonder if large bill issuance could suck too many reserves from the banking system.

This could be one of the implications of the RRP going to zero. As long as the RRP bal is >0, there’s enough excess liquidity to absorb more bills. But once that’s back to zero, new bill issuance will resume competing with banks for reserves.

“If the Fed cuts rates, it might trigger a move higher in longer term rates”

100% agree and I think I’ve commented the same thing recently.

The Fed cutting policy rates could trigger a significant bear-steepening and a loss of control over long rates as bond traders lose confidence in the Fed’s inflation fight.

However, I think Powell & co are very aware of this. No Fed chair wants a treasury mkt meltdown on their watch – and I think this scares them much more than a stock mkt or asset price crash.

Bill Gross is a grifter of the worse kind. I was his neighbor in Corona Del Mar for a while. Very odd bird, and not very neighborly…

Where you the neighbor he sued?

Bond vigilantes only exist in a tight-credit environment.

“Ample reserves regime” means no bond vigilantes.

Where are taxes accounted for in the CPI?

Here in Washington State we are experiencing record setting tax increase on gas, real estate, utilities, sales, capital gains, etc from our one-party (D) legislature.

Its like Clownifornia but without the sunshine!

DaveB/NYg – or a state income tax, like we have in CA. (…gotta find that revenue for expected services for all those folks somewhere…). (…and, NY, why the hostility? You sound like another jilted lover whose sojourn in CA didn’t match their expectations (damn surf music, and the Summer of Love, anyway! Didn’t you ever hear of Woody Guthrie’s ‘Do-Re-Mi’ warning from decades earlier?). Happy you’ve found your bliss in the Empire State…).

may we all find a better day.

Left almost 20 years ago, one of the best decisions of my life. And you’re not getting much in services, you’re paying for those huuuge pensions and millions of illegals. I looked around years ago, assessed the situation and gtfo’d. I’ve learned few can or want to accept reality. Sounds like you’re in the many camp.

Thank you for leaving California. Please don’t come back ❤️

Wow some people have the nerve… You don’t have income tax, so to pay all the freaking public services something had to give…, enjoy your property price appreciation…..

In NH, we have neither income nor sales nor gas taxes.

But we have lots of prop taxes…

We all pay what’s needed, one way or the other.

Two things in life are certain: death and taxes.

“We all pay what’s needed” … but in some states they pay for a lot more, and don’t get it.

Howdy Folks. So glad ZIRP is dead and more glader I found truth from

THE LONE WOLF

THANKS. Been waiting all day and was not disappointed .

Core PCE peaked in February 2022 and its trailing-12-month annualized rate has declined for 16 consecutive months. This is making market bulls euphoric as any elevated month-over-month reading like January’s is seen as a speed bump rather than a break in the trend.

1) At what point do we start getting difficult comps that would make the annualized rate move higher if inflation stays around where it’s been in recent months?

2) At what point does durable goods disinflation & deflation that’s worked so well to mask hot services prices begin to fall out of the 12-month window?

@Jackson Y,

Difficult comps likely coming soon…within months. Look at energy prices for starters. Bottomed in December, trending higher since. Should see $90 crude by the summer.

Rate hikes also coming by summer. Prior to this latest piece from Wolf, felt like I was the only one saying this…but I’m a nobody. Still wonder what in the world long duration Treasury buyers have been inhaling.

Here is the thing, though: you can’t actually eat NVDA stock.

Any time these meme stocks take off, hold on to your wallet. Remember the first NVDA head-fake during the pandemic when the price was being fueled by cypto miners? NVDA had to pay a $5.5 million fine to the SEC for failing to disclose the extent to which crypto mining was a “significant element of its material revenue growth”. My take was more aggressive – they not only failed to disclose, they DENIED the importance. In less than a year NVDA tumbled from $329 to $112 (2022). And now it is being pumped again. 69 P/E ratio? Yikes!

Reading other financial websites’ articles or looking at the market, one would not believe the numbers the way you presented even if true.

Looking at 1970’s Vs 2023’s, we have huge differences:

1. We were a manufacturing hub then. Now, China, after having invested in manufacturing so much (you yourself highlighted the cost of automation Vs their labor), they have no choice but to keep supplying us and gift us with their deflation and hence our numbers are not going to go to 1970’s level. Yes, I know service accounts 70% of our GDP but they don’t have much leverage.

2. Some 60% of our population don’t care about inflation as long as the stock market and housing market is kept up by the big FED balance sheet.

3. Speaking of FED loans, using your own graph, FED

https://wolfstreet.com/wp-content/uploads/2024/02/US-Fed-Balance-sheet-2024-02-01-total-assets-detail-768×589.png

took their assets from $4.5T to $9T and so got some useless or non-performing papers in return for newly minted money. That new money is creating havoc with new bubbles everywhere (bitcoin at 60K). But now FED is like a person holding a tiger by it’s tail, afraid to speed up the draining of that money lest they will crash everything. There is even talk (by FED officials) on how to reduce that number in case our economy slows down.

So, like a Red Vs Blue, we are seeing a bifurcation — two different economies and two different economic groups. Only time would tell.

I agree with all of this except for #2. It’s nowhere near 60%. If it was, then the current administration’s economic approval rating wouldn’t be in the toilet as it is.

At best, it’s probably like 15-25%.

I am LoLing at #2.

White house want to smoke what you are smoking .

Have you seen Bidens approval rating on economy ??

It’s pretty bad .

RE #1, China

I recall hearing a certain politician saying tariffs should be 60% on China and 10% on absolutely everyone else.

I do not think this would be helpful for containing inflation.

Any comments for 18 months from now if this happens?

That would pay for that guy’s tax cuts. I mean, consumers would pay. China has a $12,000 electric car. What we have is a manipulated car market by inefficient colluding protected cartels throwing hugely overbuilt products at us, with a whole segment of choices barred from us. Hence the vast hikes in insurance on the back of that. Those who can barely pay this hidden tax, have no choice. New serfdom, better than the old, for who? But the alternative is not costless either.

DEPFG-

The “tiger-by-the-tail” comment in your #3:

“But, as it is, we have the wolf by the ear, and we can neither hold him, nor safely let him go.”

—Thomas Jefferson, from a letter to John Holmes, April 22, 1820, discussing slavery and the Missouri question, but perhaps more appropriate to Fed’s price control attempts.

Here is the thing, though: you can’t actually eat NVDA stock.

Why is none of those experts on CNBC are talking about services inflation? They are all bulls, all are saying inflation is heading in the right direction and the Fed will cut and doesn’t really matter when exactly.

They all own stock and they all want stock prices to go up. I quit watching MSM financial commentary.

The problem is that stock isn’t really going up. It’s just that the dollar is going down.

People have so little faith in the dollar they’re willing to pay for stocks that return 1.5% in dividends.

Yep. Ulterior Motives, much like the rest of what passes for “news” these days.

1. They aren’t really experts on CNBC. They are talking heads.

2. They aren’t there to inform you, they are there to entertain you. People aren’t entertained by having to learn the intricacies of goods versus services inflation. They like simple, easy to digest stories.

3. They provide a platform for wall street types. Wall Street generally loves cheap and easy money.

Another great column.

It really is amazing to read MSM, fintwit, etc. with their spin, then read the exact opposite from Wolfstreet.

Howdy Grimp. Same here for a year. MSM is my comic section, news is the Lone Wolf.

Here is WR’s headline:

Worst Monthly Spike of “Core Services” PCE Inflation in 22 Years, and Not Just Housing: Powell’s Gonna Have Another Cow

Here CNN headline:

The Fed’s favored inflation gauge eases to slowest pace in more than two years

The sad part is: FED officials believe in what CNN and other MSM writes.

What is written in MSM moves the market and moves the FED.

“The sad part is: FED officials believe in what CNN and other MSM writes.”

Nonsense. The other way around. The Fed doesn’t even look at that CNBC crap. They look at the data and their own reports, and Powell has been talking about core services inflation for a year. But CNBC isn’t listening to Powell because it doesn’t fit their hype.

I have posted some of the charts that Powell showed in a presentation maybe a year ago, with core services inflation acting up already, and him being worried about it already.

If Fed really believes the data you are showing then they would come out with hawkish tone but we don’t see that. Otherwise the market would have reacted very differently as well .

Would Powell and his minions come out and say that inflation is high and financial conditions ayve become too lose making feds job harder..

“… come out and say that inflation is high and financial conditions ayve become too lose making feds job harder..”

They’re saying exactly that. And they’re also saying that fiscal stimulus is fueling inflation. You’re just not listening to them because you don’t want to hear it because it doesn’t fit your narrative. You’re listening to CNBC.

OMG, I saw the inflation numbers and the News was making the bad inflation numbers sound Good. I went and sold my stocks and bought more T-Bills. This country is in denial.

Nobody that moves the market gives 2 dumps about msm or cnn.

People are just riding a high off last year and when it turns….

He who panics first panics best is how it goes I believe

A lot of people are panicking for last 10 years or so for asset markets of all kind and they have missed out big time .

Download the M2 data and total government debt outstanding charts. Then use curve fitting software (Cricket graph, Excel, Igor, etc.) to fit the data;

The equation that fits the M2 data is “y = (2.4×10^11) + (151,650x)^2.79”, where y is money supply in billions of $, and x is months going back to 1959.

The equation that fits the outstanding debt is “y = 59,662 + (0.19x)^2.879”, where y is debt in millions and x is months going back to 1966.

Monetary policy is STILL VERY ACCOMMODATING!!!!!

Higher for much, much, longer!!!!

Don’t need to do that. keep it simple. Look at gbp and consumer spending and you know monetary policy is very accommodative…

Powell said his and the Federal Reserve’s favorite gauge was PCE inflation, but he never said he was going to do anything about it. Sounds more like a matter of personal taste.

It’s preposterous to think an inflection point has come about, but hotter PCE, short term yields bouncing higher, Yen differential fizzing and foaming, global recession pressures and everyone’s grandma speculating on crypto and AI — naw, everything is fine and normal.

Wolf – great info as always and very much appreciated.

I’m lost on the headline/articles today like this one at Yahoo:

“RPT-US STOCKS-S&P, Nasdaq end at records as inflation data supports rate cut view”

Says inflation in line with expectations etc etc

…what am I missing here ?

I have no idea what that article says. I don’t waste my time looking at that stuff. I look at the data.

Federal Reserve:

Turn-ons: Weak, timid legislative men who let me do whatever I want.

Turn-offs: Any kind of public scrutiny or performance metrics.

This unfortunate sticky inflation crap may actually make the equities market look obscenely overvalued versus amazingly ridiculous. It’s almost worth pondering the safety of a boring money market fund, that provides actual income.

Btw: “According to the CME FedWatch Tool, money markets see nearly 80% chance of no rate cut in May, and a 35% chance of another rate hold in June.”

Wolf, again great reporting. I still believe actual inflation continues to be under reported, like you have pointed out on health care cost. What I see on increases in infrastructure construction cost the last 3 years is through the roof, and is not slowing down here in North Carolina.

The PCE price index was never designed to be a measure of actual consumer price inflation. That’s the job of the CPI. And the CPI is generally higher than the PCE. The PCE price index is essentially a tool for economists to see broad underlying inflation trends. The PCE price index includes many items that are not sold to consumers.

I wonder when the market will exhausted from the constant rate cut narrative. At some point even coke stops working.

How do you think CPI performs as a measure of actual consumer price inflation? Critiques and criticisms? Defenses and merits?

I’ve noted your dissatisfaction on the way the medical services imputations have been handled, and agree myself. I’m curious to know if you had a clean slate and were designing a KPI to track actual consumer price inflation how would you go about it? Would it be fundamentally CPI like with a few tweaks, or something very different than what we have?

Just to clarify: this article here discusses PCE price index, not CPI.

But CPI is pretty good, it uses a broad mix of data, including in recent years a lot of private-sector data that have improved the index – I’m thinking about the new and used vehicle CPIs. I discussed the changes a few years ago when they switched to data from JD Power. Those vehicle CPIs were bad a decade ago and produced illogical results until they made the changes. So I was happy to see that. The changes were one reason why the CPI picked up the huge price spikes in 2020-2022 so well. It wouldn’t have done that before.

But CPI still has some flaws, for example how it measures health insurance. I don’t know how to fix the health insurance measurement. I would throw it out, but I don’t know how to replace it. Health insurance in the US is so complex because every state is different, and every plan is different, and there are a million components to each plan (what’s covered, what is not, the formulary, etc.), and documenting premium changes in relation to coverage changes across the US is a nightmare. But my feeling is that they’re now working on a real fix. What the health insurance CPI did in 2021-2024 is just embarrassing. It totally blew up during the distortions brought on by the pandemic. And they know it. They tweaked it a little, I think temporarily, and they will come out with a better method, just like they did with vehicles.

Shadowstats is pure lies; anyone who can do basic compounding math can prove that it’s a lie, and I have done that here before a few times.

Who else here is looking forward to seeing the updated dot plot at the Fed’s March meeting?

Howdy Shocka I am. Learn from the Lone Wolf about the dot plot.

I think the Fed should discontinue the dot plot.

Howdy MM. They seem to be following the dots they plotted.

…mebbe they’re just ‘dotty’…(pardon the ellipsis pun).

may we all find a better day.

Why?

Because its almost imediately outdatted, and stays that way for another 2.5 months.

March dots will almost certainly show fewer cuts this year / maybe a hike. But the stupid fed funds futs mkt keeps implying that all these cuts are still happening, and then all these traders keep bidding up stocks, RE etc.

If mkt participants can’t use the info the Fed is giving them, then the Fed should take that info away. Like a child that isn’t playing with a toy correctly.

I don’t think it would change that much. Bostic, Goolsbee, Mester and several other committee members who spoke this week continue to see 3 cuts as their most likely forecast.

Headlines all saying PCE was in line with expectations and not to worry. Burn it down. It’s not worth saving.

Howdy Desert Rat. Hang in there. Old folks made it through the 70s 80s.

Wolf, does the Financial Services and Insurance category give any breakdown of the +17.2% in terms of one (financial services) vs. the other (insurance)?

That is a massive number.

I wonder if the insurance side is contributing more than the financial services one. As an anecdotal example, my home insurance premium increased substantially recently, seemingly out of the blue. When I asked the provider about it, they basically shrugged and said it was something they had done across the board; all of their clients experienced the hike. The hikes suck, but you can see why they would have to do it. If the cost to repair stuff has gone up (materials and labor), then they have to eventually hike their insurance rates to catch up.

1. The PCE price index covers more than just items that consumers pay for; it’s far broader. The CPI covers only consumer inflation only.

2. The pusher was the Financial services PCE index. It alone is very very volatile. It spiked by 29% MoM, the biggest MoM jump since March 2021, when it spiked by 40%. But it also drops into the negative on a regular basis. These numbers need to be looked at on a 6-month moving average basis (red lines), not month-to-month (blue lines).

Most media outlets are saying that Core PCE inflation reduced to 2.8% on an annualized basis (down from 2.9% in December). How can it be going down if January 2024 was up? Is the answer base effect (i.e. January of 2023 coming off the book, which had a higher monthly reading than January 2024)?

You need to read more than the headlines.

“2.8%” was NOT “annualized” anything. That was the year-over-year change of the index, from January 2023 to January 2024.

here we are talking month-to-month and 6-month moving average, both annualized. That shows the recent trend. While two-thirds of year-over-year is a reflection of things that happened a year to six months ago.

Thank, Wolf. Appreciate the clarification.

Thanks for the reply (I posted my initial question in the wrong spot).

And wow are those are huge spikes in a category I clearly did not predict to see it in, no less.

The next question would be why the heck is the financial services category so volatile!? But that’s probably getting too far into the weeds (i.e. fine print).

Sorry, I am confused. Every news outlet including bea.gov is saying that yoy change is 2.8%. Isn’t that the same as saying that inflation has been 2.8%? Have I been misunderstanding what they report every month? Does the CPI report differently (I know the CPI is comprised differently, but I mean the yoy and mom figures)? I was always under the impression that the figure that they post was price changes from the prior year. I read what you posted and your responses but I still don’t get it. Thank you for clarifying!

1. You’re confusing CPI and PCE (the article here is about PCE, not CPI). CPI is not 2.8% year-over-year. CPI = 3.1% YoY. Core CPI = 3.9% year-over-year. Core Services CPI = 5.4% year-over-year.

2. Since you insist on CPI, I’ll stick to CPI, but PCE works the same way. They’re both indexes of monthly numbers, like a monthly S&P 500, This is what the CPI looks like:

The change of these numbers indicates “inflation” or “deflation.” When the numbers go up = inflation; when the numbers go down = deflation.

Then you can figure the percentage changes of these numbers. You can figure month to month % change, and then you can average three months or six months into moving averages to get the most recent trends; and you can “annualize” those moving averages to come with a figure what this would be for the 12 month period if it continues at this rate (there is a formula for that). This is what I did here, to show you the current trends.

You can also figure % change of the index from a year ago, or from two years ago, or from 20 years ago.

What you’re talking about, that 2.8% that’s PCE, not CPI, and is year-over-year, and two thirds of this figure is composed of what happened in January 2023, and what happened through June 2023. One third of the change reflects what has happened over the past few months. So if you want current trends, the year-over-year figure will not tell you, and you will be in the dark, and you are in the dark.

So we watch as wages keep getting pushed up by essential services inflation, and we do … nothing.

Looks like they can’t even pass a minimal cut in Federal spending and are getting ready to pass another continuing resolution. We now have a completely disfunctional government here in Washington DC. The Congress and Executive branches are incapable of doing anything to bring down spending. Look for more inflation as far as the eye can see. ENJOY!

Howdy Swamp C. Unfortunately you are probably correct. 70s 80s inflation was wild and so were the interest rates.

As was the disco music

Our hardly working Congress has managed to kick the can down the road for a FULL WEEK this time around!

Howdy SoCal B D A rumor floated that 100 Billion in cuts were on the table. HEE HEE

DM: The most valuable car in the world: 1955 Mercedes 300 SLR Uhlenhaut Coupe sold for £115 MILLION in 2022

RM Sotheby’s confirmed in 2022 that it had sold a 1955 Mercedes-Benz 300 SLR Uhlenhaut Coupes for £115million, making it the most expensive car ever.

It was sold to a private collector at a top-secret auction hosted at Mercedes’ museum in Germany on 5 May that year and exceeded the previous record amount paid for a motor vehicle at the time by a staggering £63million.

Experts say the car, which is one of two created in 1955, has ‘always been regarded as one of the great jewels of motoring history’ and its sale is a monumental moment with few ever imagining that it would be offered to a private buyer by the German manufacturer.

Nasdaq Composite posts first record close in over 2 years

Fisker seeks deal with another carmaker to remain afloat, ‘going concern’ warning on the horizon

It needs to go bankrupt. It’s one of my worst Imploded Stocks.

Well, Fiskar seems to have experience in bankruptcy court. Like “going home again”?

Somewhere I read that their successor firm name was Karma Automotive.

Karma, one definition:

“Fate or destiny resulting from one’s previous actions.”

Could it be?? How many new investors get a cleansing in bankruptcy court this time around?

I’m a great fan of your Imploded Stocks and consensual hallucination theory.

“Somewhere I read that their successor firm name was Karma Automotive.”

Including in Aug 2023: “Fisker [FSR], SPAC merger October 2020, preceded by Fisker Automotive which made the Fisker Karma. Now $5.93. From peak: -81%.”

https://wolfstreet.com/2023/08/09/the-collapse-of-the-ev-spacs-another-one-goes-bankrupt-others-on-the-verge/

Hey Wolf random question, but having done extraordinary research and self-educating, are you ever tempted to place some big bets on markets?

Or do your insights tell you not to play a game that doesn’t make sense?

He’d be a fool not to take reasonable steps in light of what seems to be happening.

and yet..

despite this ‘worst spike in 22 years’..

coupled with congress kicking the proverbial can down the road for another WEEK to avoid a shutdown..

AND vladimir putin once again warning of a potential nuclear conflict if NATO directly involves itself in ukraine,

there is little to no market volatility whatsoever.

in fact, the dow, s&p, and nasdaq were all up solidly on the day.

i think this confirms that the markets and society in general are living in one gigantic DELUSION, for which there is no remedy except for an absolute and total collapse of the current way of life.

yep. And it will come suddenly by surprise. Reality is too scary to think about anymore so we have YOLO since the future is bleak. Unprecedented greed has led to total blindness. Psychology turns on a dime. This time a penny.

Agree that we are living in fantasyland and borrowing heavily from the future. However I would not wish a total collapse. No one is a winner in that scenario.

I think the Fed should be given credit for preventing a (possible) total societal collapse during the pandemic when everything was shut down. Granted that they perhaps overdid it but I shudder at the thought of what could have happened if they underdid it. It looks like they are trying to do a job and correct their mistakes but it takes time. However the problem is that society has come to expect them to rescue always and that notion will take time to go away. What we are seeing is a delusion from a flawed policy that went on too long.

Let us hope that we escape this debt fueled binge with a little bit of pain and remind ourselves that hard work, ingenuity and thrift made this country great and that path isn’t completely lost, just a bit forgotten.

The cold hard truth is that society at large has become rude, ignorant, and largely disconnected from the natural world. The laws of physics and thermodynamics rule, and ultimate decide who lives/dies, but try explaining physics to a population where the average person can’t do basic math. It should be no surprise why the world is returning to a feudal system. It’s human nature.

@Aman: You’re probably young since you talk only about what the Fed did during the pandemic.

However, the irresponsibility of the Fed started in the 70’s when we went off the gold standard. This got tamped down due to high inflation in the late 70’s and 80’s. Then came back under with a vengeance under Greenspan who reveled in low interest rates and the so-called Wealth Effect to blow up stock and housing market bubbles in the 90’s.

Bernanke, Yellen, and the earlier years of Powell saw the continuation of loose monetary policy well beyond what the GFC required.

In summary, if you think the pandemic was the reason for the Fed’s loose policy, you’re absolutely mistaken IMO.

They want to run the economy hot because it is beneficial to the political class, the banksters, and the 1%-ers.

The fact that a significant amount of the population gets impacted with asset inflation especially housing, and the chaos of retrenchment after the bubbles implode is just collateral damage in their elitist plans.

Remember the stagflationists? “Rethink 2%”

Sean,

I think maybe you are young because your historical memory does not embrace the crises of the 20th century (in systems without this banking flex) which led to the Russian Revolution, World Wars and Chinese Revolution, and the millions of fatalities. The Fed in its worst excesses and its slow inflationary drag isn’t even in the same ballpark, or planet. It is hard to show someone the counter-factual, what happens if that dog did, or DOES bark: roll the dice hard on a new boss, better than the old boss? That almost never works. The USA because of this shallow historical perspective strikes me as full of various political shades of crybabies.

@phleep: “Things could be worse…they are not as bad as the 20th century or the 19th century or the 18th century” is not a good argument for looking at issues in the recent past and seeing how they can be mitigated.

That way, there will never be any improvement whatsoever.

Phleep,

My historical memory embraces the Russian Revolution, World Wars, and the Chinese Revolution, and I must say I never viewed those events as resulting from crises precipitated by systems with a lack of “banking flex.” The Czar really blew it I guess, he just needed to let the central bank off its leash.

Seriously though, implying “banking flex” in the United States avoided enormous evils such as those seen in the first half of the 20th century seems like a really big stretch to me. Reasonable people can debate Fed policy without trying to shut down the conversation by comparing alternatives to some of the most horrific events in human history.

@Aman: You said ” I am not trying to absolve Greenspan, Bernanke and Yellen of their misdeeds and crazy monetary policy. All three are idiots in my book.”

I would submit that they are not idiots and that they are intelligent people who do the bidding of the political class, the powerful, and the affluent – which is to run the economy as hot as possible consequences be damned. In fact, there are no consequences except for the folks at lower rungs of society.

This is by design. No system can make “mistakes” for 50+ years.

Aman-

Not sure I can buy the statement that “no one is a winner” in a market collapse. Winning, in a collapse, means that someone retains a relative advantage in the division of societal wealth and wealth generating ability, and that comparison takes place at economic lows just as it does at economic highs. Some will retain relative wealth, many will lose everything.

Two infamous collapses (Currency collapse in Germany and Great Depression in the US) left some family empires and employed persons with massive “wealth” after these two general disasters.

I don’t wish for a collapse, but economic manipulation through bond market tinkering ends in currency chaos. Historically, that chaos can develop slowly or quickly.

The cold waters of collapse might just revive the senses of the investing (and voting) public. In that respect, you might forgive the commenter who expresses eagerness to get the adjustment over with….

Respectfully.

Also-

Look into the magnitude of the Great Influenza pandemic (1918-1920) including the mortality tables, and then examine the Federal Reserve System response. The economic world survived.

Your pandemic counterfactual is debatable, IMHO.

John,

Wealth definitely continues to concentrate. I have no hope that anything can really right the ship especially as to your reference about voters. Both sides have slightly different approaches but in the end arriving at a place where affordable housing, education, health care, employment are basic human rights we are stuck. Wealth will continue to concentrate and the more it continues the more bubbles it continues to create. Even really wealthy people in our country where we can’t fathom the wealth are poor in comparison to the super wealthy. Nothing is turning this in the other direction.

@John H @Sean Shasta I am not trying to absolve Greenspan, Bernanke and Yellen of their misdeeds and crazy monetary policy. All three are idiots in my book.

My comment was mostly related to the pandemic response by the Fed. I have no doubt in my mind that I would have done the same. Wealth concentration and inflation are small prices to pay for what otherwise could have been looting in the streets.

The Spanish Flu pandemic cannot be used as a counterfactual because the nature of the economy back then and now. Economies were largely local at the time not greased by intercontinental movement of money.

Agree that wealth collapse would be good to reset to a new normal. The collapse I don’t want is that to the productive machinery, the real economy. Fed haters can take joy in the deflation of the asset bubble in that scenario but that is hardly a victory. Everyone is worse off if the economy collapses.

I would wish for a peaceful redistribution of wealth and deflation of the asset bubble with a mild to bad recession from which we can emerge stronger. I hope we all agree on that.

Ehh, that’s a gross exaggeration. I see no evidence that there would have been looting in the streets if we hadn’t handed out $5 trillion in free money.

In fact, the summer of 2020 did see looting in spite of it.

It’s the “The world would have ended if we didn’t print $5 trillion, so you should kiss the ground Powell walks on” nonsense that got us into this mess in the first place. No one is willing to challenge the core theses of the past 20 years.

“My comment was mostly related to the pandemic response by the Fed. I have no doubt in my mind that I would have done the same. Wealth concentration and inflation are small prices to pay for what otherwise could have been looting in the streets. ”

You would have continued to spray gasoline onto a raging economic fire between the summer of 2020 and the summer of 2022, despite every piece of data telling you that you had gone way, way, way too far?

Well this is about the most ridiculous thing I’ve read today.

@Pea Sea

I think even the Fed would admit (maybe not publicly) that they should have stopped QE towards the end of 2020 when the vaccines were on the way. So you can guess where I stand.

Actions taken by the Fed in 2008 crisis and in the pandemic were the right ones. Of course they were responsible for blowing the bubble and being asleep at the wheel while the leverage was building. But economies and finance are complex and often it is impossible to predict…which is why these things happen frequently.

Where they went badly wrong was not unwinding the monetary stimulus after the crisis had passed. Bernanke made the mistake and Yellen compounded it. J Powell tried to unwind but failed in 2019. Now he is trying to do the right thing. But the markets no longer care. They just firmly believe that the Fed will ALWAYS bail them out. And therefore any risk is acceptable. Time will tell if this assumption is correct or not.

I guess my views are controversial. I don’t like the Fed myself. I think they have been a drag on the US economy since Greenspan arrived and a major contributor to several social ills of today. But I also see them realizing their mistake and show willingness to correct. But their desire to fix is in conflict with a certain geriatric’s desire to extend his stay in a nice house in Washington.

Will the Fed do more foolish things in the future….certainly. Will they repeat the same foolish things they have done in the past….I really doubt it.

Aman-

The Fed, as a DC institution, is dedicated to it’s own survival. It’s constituency is the banking industry and the ruling elite in Washington. The federal government appoints some Fed leadership, while the banking industry appoints the remainder. The Fed is subject to congressional oversight, and it’s profits are disbursed to member banks and then to the treasury.

As a hybrid institution dedicated to its own survival, the Fed has grown its balance sheet, employment ranks, and toolbox EVERY decade since it’s inception, alway during or in close proximity to a perceived crisis.

You imply that the Fed has only been a problem “since Greenspan arrived,” but this ignores the gigantic expansion of Fed powers and scope that occurred between 1914 and 1987. For an elaborate discussion of one such expansion (1918 to 1935), read Banking and the Business Cycle, Phillips, McManus, Nelson, 1937. (I know you are a reader, and I hope that the age of this post-mortem of the Great Depression won’t deter you from exploring it. Very clearly written, and you can read it for free on Mises site.)

Similar expansions in scope and size occurred in each decade since then, responding to the perceived threats of the day (many of which were the results of Fed’s prior actions!).

The result is the bloated, money-losing, fumbling behemoth that manipulates our credit markets today. As such, your apology for the Fed IS indeed controversial for some.

Respectfully

i never said anything about wishing..

the issue is that the giant game of ‘pretending’ has no other remedy EXCEPT FOR that outcome.