A big milestone for Quantitative Tightening in the euro area.

By Wolf Richter for WOLF STREET.

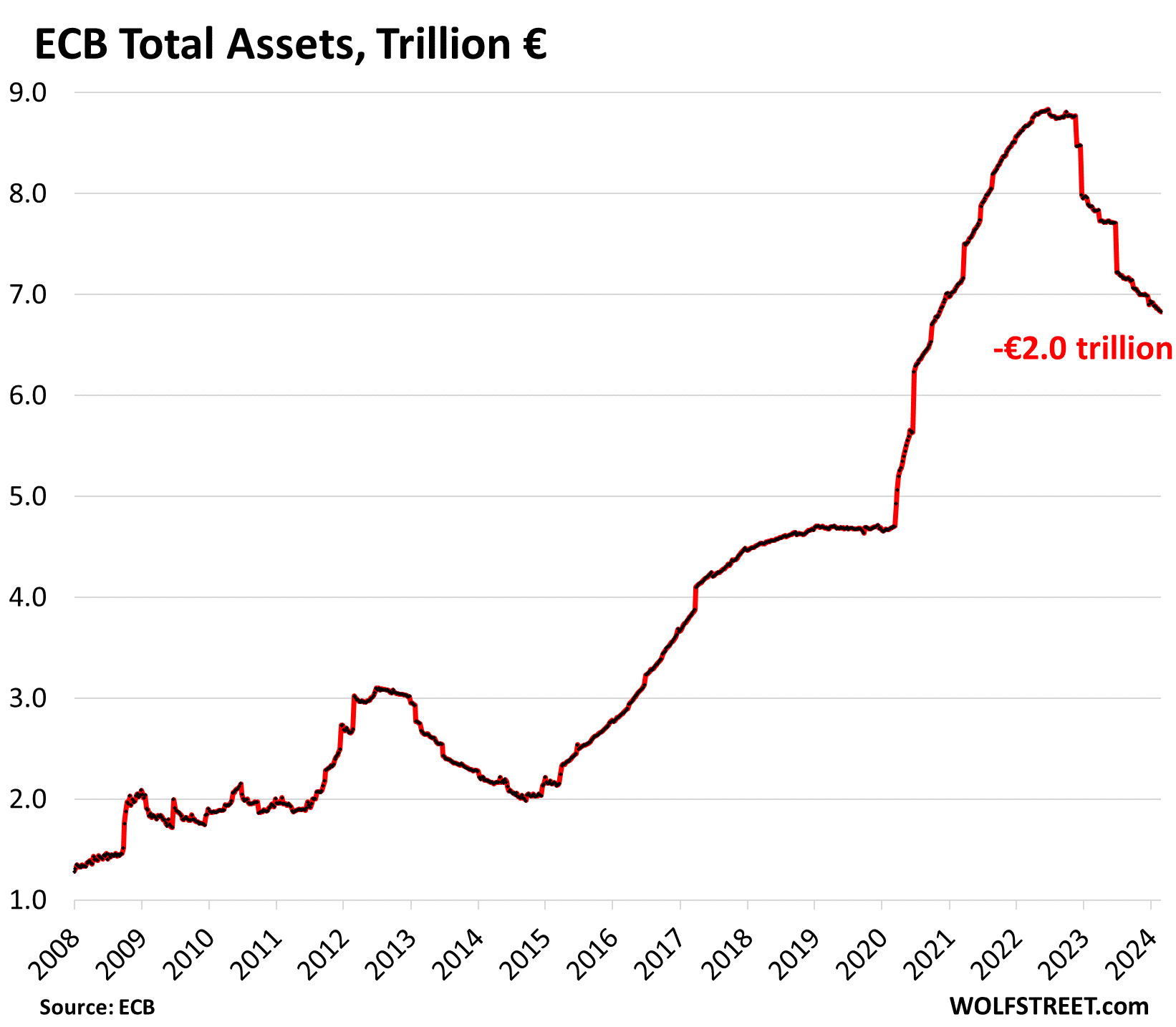

The ECB has shed €2.0 trillion of its assets since QT began, as of the latest weekly balance sheet. Its total assets are now down to €6.83 trillion, the lowest since November 2020.

In USD, the ECB has shed $2.17 trillion in assets at the current exchange rate, while the Fed has shed $1.34 trillion in assets.

During the pandemic QE, the ECB added €4.15 trillion in assets, a crazy huge amount; it has now shed 48% of that pile.

During QE, the ECB had piled up two very different types of assets, and both are getting unwound, but at a very different pace:

- It offered loans under very favorable conditions (free money) to banks, and it was up to the banks to deploy this cash.

- It purchased government bonds, corporate bonds, covered bonds, and asset-backed securities, thereby handing the financial markets this cash, under two programs: APP (asset purchase programme) and PEPP (pandemic emergency purchase programme).

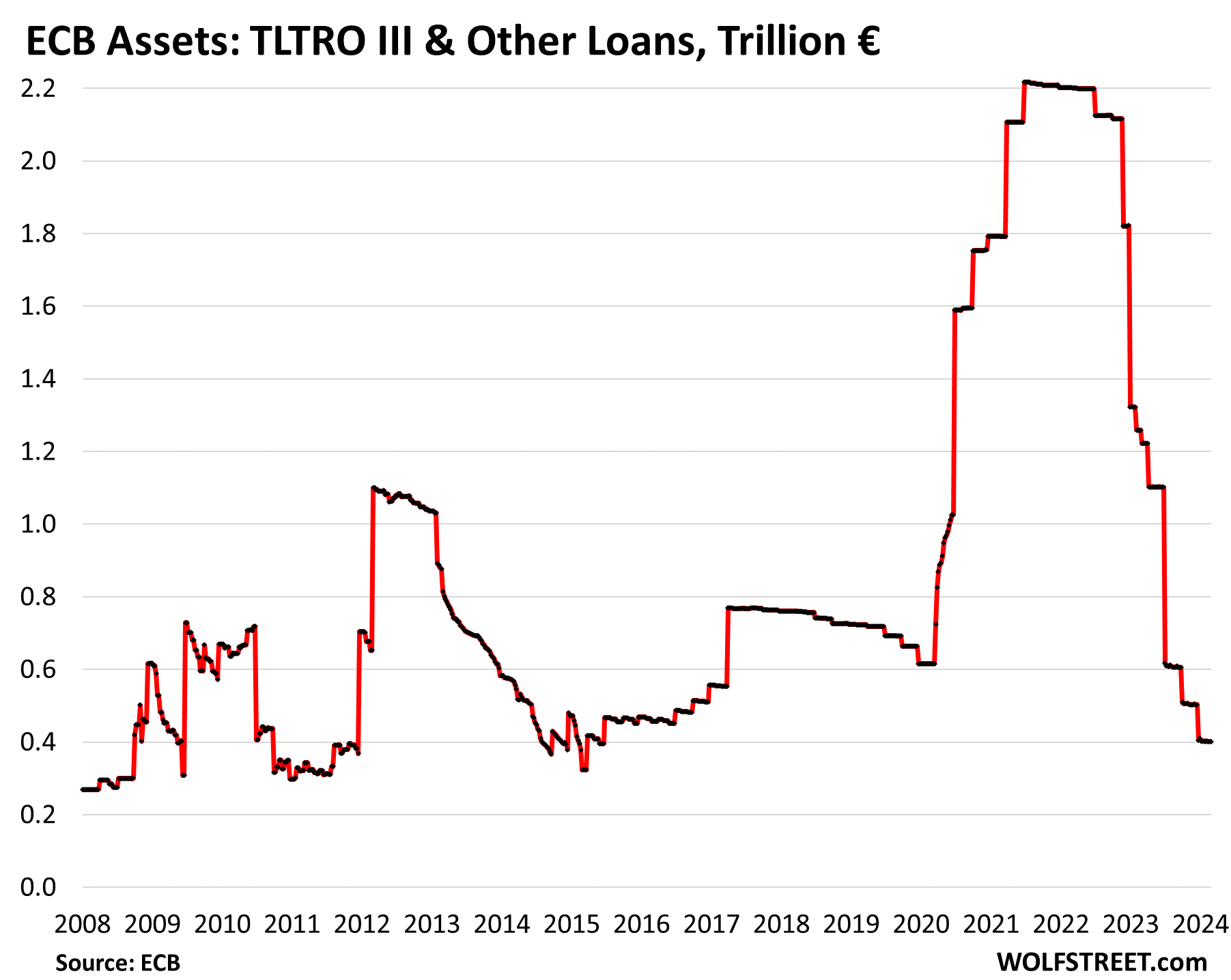

Loan QT: -€1.80 trillion

QT was announced in October 2022. As the first step, the ECB made loan terms unattractive, and it opened more windows for banks to pay back those loans, which banks did in big waves, which removed liquidity from the financial system via the banks.

By now, banks have paid back €1.80 trillion in loans since the peak, and only €401 billion in loans remain on the balance sheet, the lowest since 2015.

The ECB has always handled QE via waves of loans, at first during the Financial Crisis, then the Euro Debt Crisis, then the period of no-crisis, and finally the pandemic. The waves had names: Longer-Term Refinancing Operations (LTRO), and then Targeted Longer-Term Refinancing Operations (TLTRO); and the waves were numbered. During the pandemic, the ECB’s lending operations were called TLTRO III.

TLTRO III loans amounted to €1.6 trillion at the peak, on top of the still outstanding prior loans, for a total of €2.2 trillion at the peak between June 2021 and June 2022, now down to €401 billion.

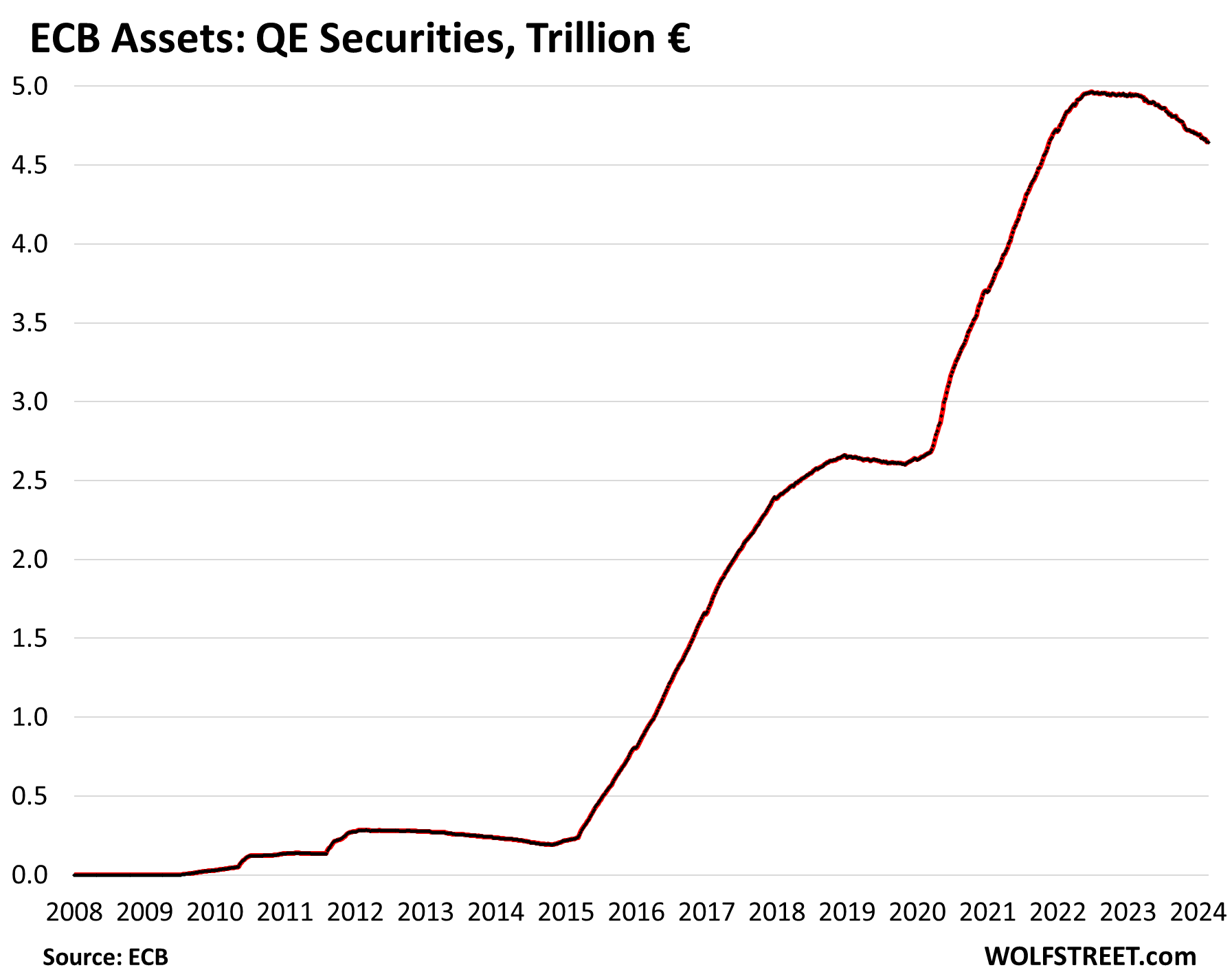

Bond QT: -€319 billion

The ECB had bought bonds under two programs: APP (since 2014) and PEPP (since March 2020). Bond QT started slowly in March 2023 and has since accelerated, and further accelerations have been announced.

The initial roll-off of APP bonds in 2023 was capped, but the cap was removed in July, and APP bonds have been rolling off without cap. Whatever matures, rolls off. In January, €33 billion in APP bonds matured and rolled off, in February €25 billion will mature and roll off; in March, €31 billion will mature and roll off.

Since the peak, €319 billion in bonds rolled off – all of them APP bonds. PEPP bonds won’t start rolling off until July 2024.

The entire bond portfolio is now down to €4.64 trillion, the lowest since November 2021:

Years of QT to control inflation with moderate interest rates.

QT is designed to run for years without fanfare on automatic pilot in the back ground, just calmly removing liquidity in a predictable manner, so liquidity can still flow to where it’s needed, attracted by the higher yields that those who need liquidity are willing to pay.

The interest rate decisions get all the media attention. But QT is complicated, and people don’t really understand it, and their eyes glaze over and they don’t click on the articles, and so it gets little media attention, and that’s how central banks want it.

The expectation is that removing this liquidity methodically from the markets in bits and pieces over the years, it will remove fuel from the inflationary fire, allowing central banks to not lift rates as high as in the past, but keep them at moderate levels.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The TLTRO and other Loans balance has effectively been zeroed. Commendable.

But the Bond Assets have only been marginally reduced. It is imperative that balance get reduced at the suggested accelerated rate or the cumulative effect would be more accommodating.

That really doesn’t make any difference at all.

IMO, its zero sum. Less or slower QT is relatively ccommodating

Would the ECB have a baseline balance sheet floor like the Fed that they won’t go below?

Yes, but I have not done my homework on it and cannot give you any thoughts on it.

I’m really looking forward to the next Fed QT update. Not sure why – maybe just to see if they “will”. Based on previous articles here it seems like they will bottom out at 5 or 6 trillion.

My next Fed QT update will come on Thursday, March 7, when the Feb 29 Treasury roll-off is included in the weekly balance sheet. I don’t expect any surprises, roughly -$80 billion for February.

I may eventually discuss the Treasury maturity schedule separately. It’s pretty interesting. Under the current program settings, they can go at the current pace of roll-off until mid-2025, and then the Treasury roll-off will decline naturally as fewer Treasuries mature each month as the remaining pile of Treasuries is getting smaller, and they’ll run out of T-bills in June 2025 to fill the gap.

But they could tweak the program before then.

I’m surprised they idea of letting excess-of-cap treasuries roll off and replace this excess with bills (to be at the cap still for the month), which can be used later when they can’t hit the cap with treasuries. Unless they’re guessing that they’re going to lower the cap anyway, or are happy being under the cap after their bill pile runs out.

Either way, the added flexibility might be advantageous.

Yes, there are some good ways to teak this. During the last QT, they did something like that. When they slowed and then ended QT, they continued to let all MBS roll off (via passthrough principal payments) and replaced them with Treasuries. QT ended in August 2019; MBS continued to roll off at the cap until March 2020.

So you also see in the minutes that they talked about slowing the Treasury roll off eventually. There was no word about slowing the MBS roll-off. So that may continue until the MBS are gone. The Fed really doesn’t like the MBS on their balance sheet (unpredictable, complicated to administer, showing preference for one type of private-sector debt).

Just today a Fed speaker indicated “I’d like to see MBS go to zero”. I suppose they could just quarantine these holdings and let them roll off as they are paid off and not actually count towards the “active QE”? Seem like it’s never going to be more than maybe $20B a month anyway.

The Fed should never have gotten into the mortgage business in 2009 and doubely not again in 2020. Housing is so screwed up right now that it could take a decade to seem normal again. How long will the remaining MBS take to disappear naturally? I still think at least one component mortgage will go the full 30-year distance and not be retired until early 2052.

That last chart is the tell. I would love to see the government debt for all EU governments overlaid on that chart. Same thing for the Federal reserve and U.S. government debt.

Great reporting as always, Wolf. Thank you for all that you do.

From my perspective the third chart, “ECB Assets: QE Securities, Trillion Euros”, speaks volumes about the shenanigans within the ECB that commenced with Mario Draghi, and will probably never end. When the GFC kicked off in 2008, central banks around the world engaged in a massive fraudulent money printing to “Save the World”. China, U.S.A., Japan, EU, all of them. This will never be unwound as it’s an impossibility that would collapse everything if attempted. Pure, unadulterated fraud. Central Banks are a pox on the people.

At the moment the ECB is doing much better than the Fed!

Let’s see how long.

You are a fool too puke out your angst that the ECB is doing better than the Fed which is patently not correct, mathematically. Which is the basis of human existence.

The ECB is pretending that it was not their irresponsible monetary experiment is still an inflationary problem. The ancient European aristocracy has found it’s way to naive America.

Yah, whatever dude. Make some sense with your comment. I’ll go back to my “Burpee Complete Gardner” book (copyright 1995). I’ve got better books, but this one sometimes yields a gem.

My understanding of the definition of a fool is someone who is super suspicious, always whining and distrustful, kind of like you!

Where else but WolfStreet can you get such great reporting on this wide of a variety of topics. I mean it would seriously never have even occurred to me to go LOOK at how the ECB is handling QT if this article didn’t get posted!

Yes, Wolf is a talented raconteur indeed. It takes years of effort to advance a website like this; years of hard work and sweat of the brow as you hunch over a keyboard. We all owe you a debt of thanks, Wolf.

The reason the Great Crash of late Oct 1929 turned into the Great Depression was there was, in effect, no central bank. The Fed just sat on its hands as the economy withered away. Politicians in both parties supported a balanced budget via tightening.

Cash disappeared. Things ground steadily down until by 1934 the economy had seized up. Corn and wheat could not afford their storage or rail shipping to customers and was often dumped on the ground. US Steel production dropped to 10 percent of 1928.

Ten thousand banks went under, with no deposit insurance like we have now from the FDIC arm of the evil ‘administrative state’.

In its master piece of irresponsibility the Federal Reserve Banks themselves ceased banking operations.

No doubt politicians today have abused the Keynesian theory of counter- cyclic central banking and instead run endless deficits to distribute goodies. Keynes said the CB should run a deficit in recessions and a SURPLUS in good times, balancing the budget.

Anyway, we’ve had one 10 year spell of no central bank intervention and it wasn’t pretty.

The reason was overvaluation in the stock market but the difference then was the stock market wasn’t rigged like today.

That’s the reason for the 29 Crash. It didn’t have to turn into a 10 year depression.

This btw is not just my opinion.

Wolf how did the ECB decide which sovereign Euro denominated bonds to buy (and now to sell)?

Does this have any affect on debt financing of countries within the Euro zone? Naturally not all EU countries are equally creditworthy.

Thanks in advance

Generally they bought everything that was at least investment-grade rated and above*. The purchasing strategy was not official as to not to influence the market**, but very likely it was more or less weighted by the bond’s share of the total market. I tried to look for fraudulent activity back in the day regarding CSPP (whether the ECB is picking favorite bonds), but it appears that was not the case. However, it might have worked the other way around: those countries and corporations that wanted to benefit more from QE focused on bonds as their primary mean of financing. LVMH, Kering and German auto manufacturers are prime examples, they launched dozens of new bonds around 2015-2018.

*This means that Greek bonds were completely off the table, the ECB’s reasoning was that risky bonds will benefit through the yield spread.

**The ISIN code of bonds bought by ECB was public, but the volumes were not.

Larceny lurks even in the hearts of a million lovers.

I am going to have to disagree with Wolf’s last paragraph. The U.S. Federal Reserve may be using QT as a slow and steady means of draining liquidity from the market… but there was nothing predictable (or moderate) about how the ECB did it. To see those loans to banks repaid as fast as they were looks like a precipitous plunge to me. I would be curious to see how the European inflation rates (and ECB interest rates) differ from America’s considering the two approaches.

Spencer:

IMO the Eurozone has a handful of problems that the US doesn’t have. They’re basically in/ teetering on recession.

They have a greater demographic problem (the US fills the need from the southern border: and CHEAP too!).

There’s a lot of social programs, including healthcare.

They are generally all energy dependent and food dependent/ as seen by the “war premium” effects.

The size of the economy is less, as is the number of “globally dominant” companies.

No idea how it all plays out? Stagflation is what I see in the US. Global depression/ deflation is the top clickbait headline (since the first rate hike), and we all could actually use a mild recession.

“They have a greater demographic problem (the US fills the need from the southern border: and CHEAP too!).”

Overpopulation is not a problem now, I see. As everything else in the stupefied mind, facts flip-flop between good and bad according to the argumentative needs of the preestablished belief.

SS:

Personally I have never believed overpopulation is a problem (I have felt it, and been taught that: but that’s a feeling and agenda).

It’s a convenient thing to sell people to legalize suicide (MAIDS in Canada, suicide booths in the Netherlands, other examples in California and beyond).

There’s plenty of room and resources, but it’s a challenge for humans to share nicely.

An imbalance of demographics means that young must care for old, and that productivity increases are required to offset those imbalances.

Instead we have a huge generation of unproductive influencers, sharing the wisdom of inexperience.

It’s quite possible those bank loans were very unproductive and didn’t make much difference. Repaying them may have been painless with minimal knock-on effects.

The way the ECB did that is it changed the terms of the loans, and they were no longer free money, and banks voluntarily returned that cash in big waves. So this is a little different than the ECB forcefully sucking out cash. The effect may be similar, but banks had time to prepare, and when they were ready to return portions of that cash, they did. So far, nothing in the Eurozone blew up, knock on wood. But I agree, €2 trillion in 14 months is pretty fast.

The last Federal Open Market Committee (FOMC) minutes mentioned the Committee beginning discussions on tapering QT and deciding on the level of assets to hold.

Suggested reading:

https://wolfstreet.com/2024/02/22/the-fed-wants-to-drive-qt-as-far-as-possible-without-blowing-stuff-up-and-its-working-on-a-plan-fomc-minutes/

It is fitting that you have shined the spotlight on the toothless tiger, the ECB.

I came to that impression today when I realized that cute Italy was paying over 1% less for their risky 10 years than Uncle Sam’s paper. Obviously, that is absurd according to rational economic thought.

The worldwide monetary environment is inflationary which is bad news for the everyday person, who will work all of their lives to attain grace and never was or became graceful.

The annual rate of inflation in Italy has dropped below 1%. That is part of the reason for the lower yields. The economy in euroland is slowing down, with mild recessions in some corners. The US economy is running hot, and core inflation started to accelerated again in recent months.

The ECB has an impossible task, imposing a common currency on a culturally diverse mega population who have yet, physically opposed the rise of the potentially, fascist governments.

Thank God for the little people who are paying for the military protection for the business interests of American billionaires.

Wolf, is there a relationship between leading economic indicators, coincident economic indicators and balance sheets (and is there an equivalent of those measures with Euro Zone)?

Do you also ever write specifically about leading or coincident economic indicators and how they’re composed, evolution of them,, and meanings etc?

Thanks as always!

1. Leading economic indicators are ridiculous fiction. They’re not related to anything. They’re just wrong:

https://wolfstreet.com/2023/11/20/leading-economic-index-predicts-recession-for-early-2024-after-having-predicted-a-recession-for-late-2022-early-2023-mid-2023-late-2023/

2. The balance sheet is related to a lot of things, mainly asset prices, but also inflation, but it’s not in lockstep.

Wolf,

Similarly can we call our or question FED’s staff forecasts/predictions?

All FED PhD Economists were predicting the Recessions like LEI. Finally they gave up on that tactic.

I remember Senator Warren using those FED staff forecasts to grill Powell saying 2 Millions jobs will be lost. How can he lead FED.. blah blah blah.

Post Pandemic economy taught many people one thing for sure.. humility about their forecasting abilities.

No one can consistently accurately forecast — except by luck — what GDP growth down to the first decimal will be next year. if you forecast 2.9% growth for next year, and then it comes in at 3.4% growth, your forecast failed.

The Leading Economic Indicators (LEI) has been forecasting a recession every month for almost two years in a row, and they’re still doing it, and that’s just BS.

The Fed’s Summary of Economic Projections (SEP… the dot plot, released four times a year) didn’t forecast a recession at all, but forecast slower GDP growth than what we got; so it was less far off target than the LEI.

In the Fed meeting minutes, we read ONE time (March 2023?) that staff economists projected a mild recession (by late 2023? I can’t remember the dates). But the SEP never picked that up and stuck with its no-recession projections.

Cant wait for the Wolf Street break down of the PCE data today.

Seems like all these central banks work together.

SRK-

“All FED PhD Economists were predicting the Recessions…”

That comment of your reminded me of a favorite quote from my stats class back in the 1970’s:

“If you torture the data long enough, it will confess to anything.”

—Darrell Huff, How to Lie With Statistics (1954)

The Fed, like the rest of us, promote it’s chosen narrative…

It takes a lot of time for the ECB to wind down their balance sheet at a pace as other central banks do, and the reason for that is the ECB have a higher portfolio duration with 5 years plus X.

Here the PSPP: https://www.ecb.europa.eu/mopo/implement/app/html/index.en.html

Here the PEPP:

https://www.ecb.europa.eu/mopo/implement/pepp/html/index.en.html

Faster QT will come from the TLTRO´s which mature completley in 2024, starting with the biggest outstanding amount of 215 billion Euro at the end of march. In June 2024 aamount of 53 billion, in September 84 billion, and in December 38 billion euro will mature.

Its weird but in the UK there are some people who think leaving the Eurozone was a mistake.

The ECB having printed the money is now not paying interest on deposits. The ECB is effectively captured by highly indebted countries such as Italy which would face probably impossibly high borrowing costs without the subsidy.

Germany is no longer a powerhouse and the Germans are waking up to a fleecing and they don’t like it.

More and more the peasantry are starting to point out that being in the euro is a bad idea.

Look out below!

No one is innocent in the EU. The German manufacturing machine did quite well selling their products to countries/people who could not afford their products, but that were extended credit by the financier class. The financier class has increased their wealth by several orders of magnitude as a result.

What’s that old saying? If the bank loans me $100 and I don’t pay it back, that’s my problem, but if the bank loans me $1,000,000,000,000 and I don’t pay it back then it’s the bank’s problem…

Just digits on a screen right?

I think you may be confused. The UK was never part of the EU monetary system. The UK left the “political union” in 2020.

Making loans to banks (in other words, making deposits in banks) is an understandable method of “flooding the system with liquidity”. The ECB absorbs the flood by withdrawing the deposits.

I’ve never understood the strange mechanisms used by the US central bank.

Canada missed the boat on basic economics and is ended QT this April in an effort to reflate one of the biggest housing bubbles in the world.

Nonsense. No bonds matured in December and January. Below is the maturity schedule for the next few months. And those bonds will roll off in March and April. And QT won’t end in April. The BOC said it might end it in late 2024 to mid 2025. It already shed about 57% of its pandemic QE bonds. By the end of 2024, it will have shed 70% of its pandemic bonds as another $54 billion will come off this year. If QT goes into mid-2025, the pandemic QT pile will be largely gone.

You forgot to mention that the ECB has now joined the club of insolvent Central banks, having recorded a loss of 1.3 billion Euros in 2023. The first loss since its inception. And it expects further losses as far as the eye can see.

So has, by the way, the Bundesbank.

But of course that doesn’t matter. I know.

Until it does.

Since modern central banks create their own money, they can neither be insolvent nor illiquid. But they can destroy their currency (see BOJ).

Ha,

The biggest wrong assed trade in the currency markets right now is being short the yen.

The yen hardly been destroyed.

The yen has crashed 30% against the hated USD, on top of the 10% loss in purchasing power that the USD experienced over this time. So when Japanese people come to the US, they see their purchasing power cut by 40% compared to 2 years ago. That is the definition of destruction of a currency. And the BOJ is quite happy with it. Shorting the yen was a great trade over those two years.

Maybe you could say the same thing about the Australian dollar then too.

It is now trading at 65 cents or so to the US dollar. Some years ago it was well over parity.

Did RBA also destroy the Australian dollar?

Or maybe on both of these cases it was actually the US Fed and their interest rate policy that did most of the damage especially in regard to the yen and the huge carry trade that resulted.

And regarding Japan and their currency….

You have to compare the inflation over a longer period of time than a year or so.

When comparing relative inflation over 5 , 10, or even 30 years the US comes out way worse.

And finally cherry picking out an example of using foreign travel to examine the case of “currency destruction” is too simplistic and disingenuous.

Come back in a year and the yen will probably be the best performing currency against the US dollar.

Howdy Lone Wolf This article is a bit over my head. Hope you are working on that inflation thingy that came out today.