These double-tops are weird. Prices coming off the second top. Only Miami home prices hit new high.

By Wolf Richter for WOLF STREET.

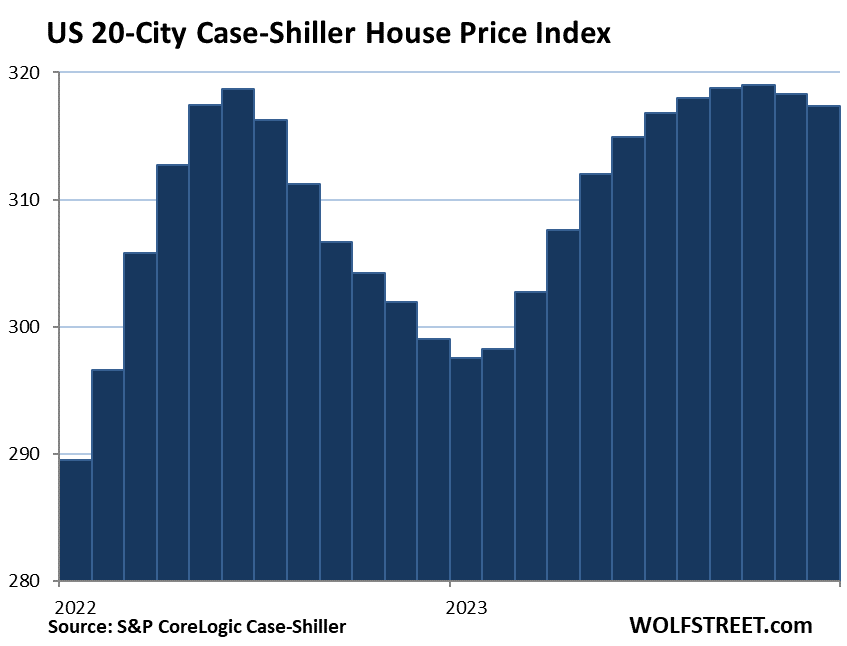

The overall home price index for the 20 metros that today’s S&P CoreLogic Case-Shiller Home Price Index covers declined by 0.6% from the prior month, the second month in a row of declines.

The index formed a double-top with the first peak in June 2022 and the second peak in October 2023. The close-up of the 20-Cities index shows the double-top, and now the beginnings of the downward slope off the second top:

Today’s S&P CoreLogic Case-Shiller Home Price Index for “December” is a three-month moving average of home prices whose sales were entered into public records in October, November, and December. It lags, but it uses the “sales-pairs method,” comparing the sales price of the same house over time, thereby eliminating the issues associated with median prices and average prices (see “Methodology” toward the end of the article).

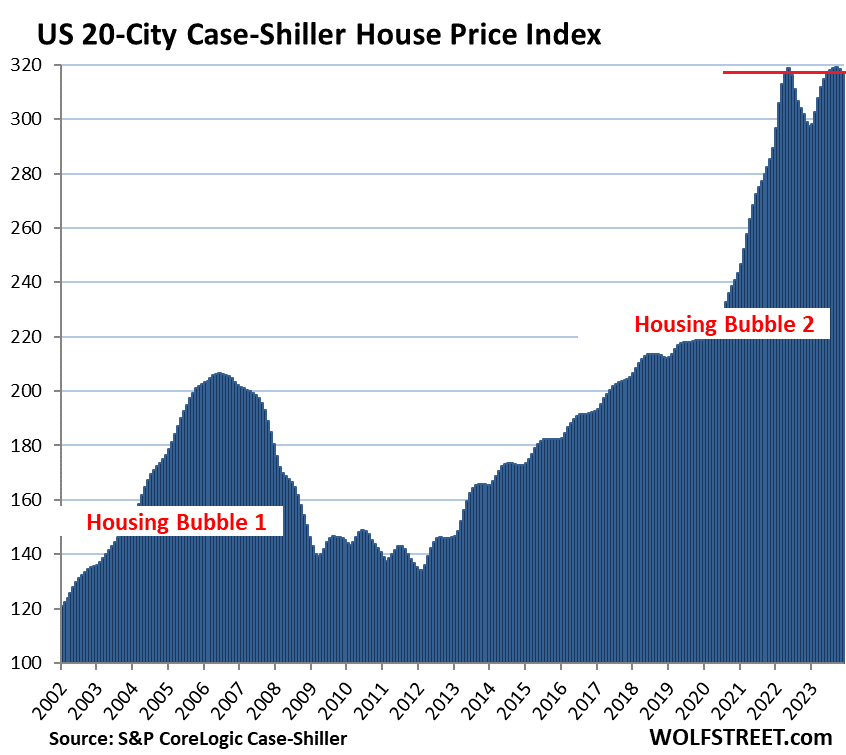

The long view of the 20-Cities Index shows the mind-blowing surge over the past few years: This kind of head-scratcher double-top has never occurred in the history of the index

Prices were below their 2022 peaks in 9 metros of the 20 metros in the Case-Shiller index (% from their respective peak in 2022, month of peak):

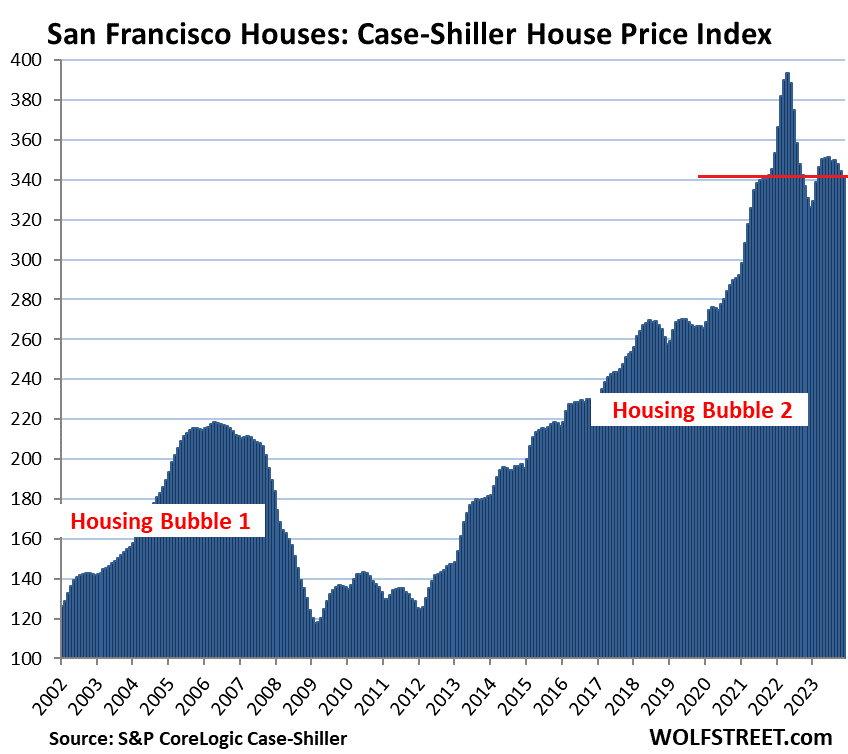

- San Francisco Bay Area: -13.4% (May 2022)

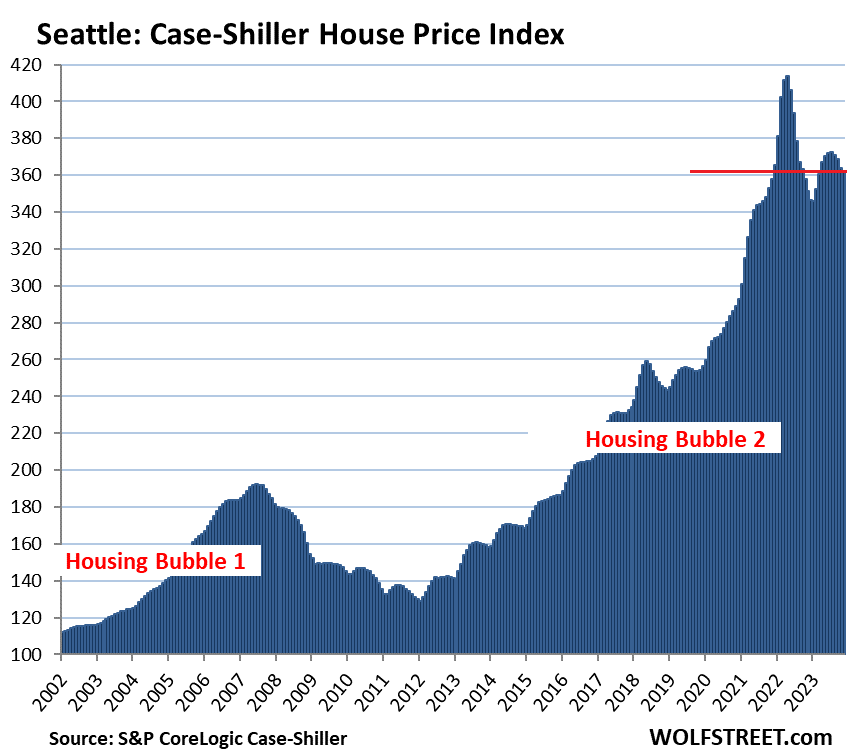

- Seattle: -12.5% (May 2022)

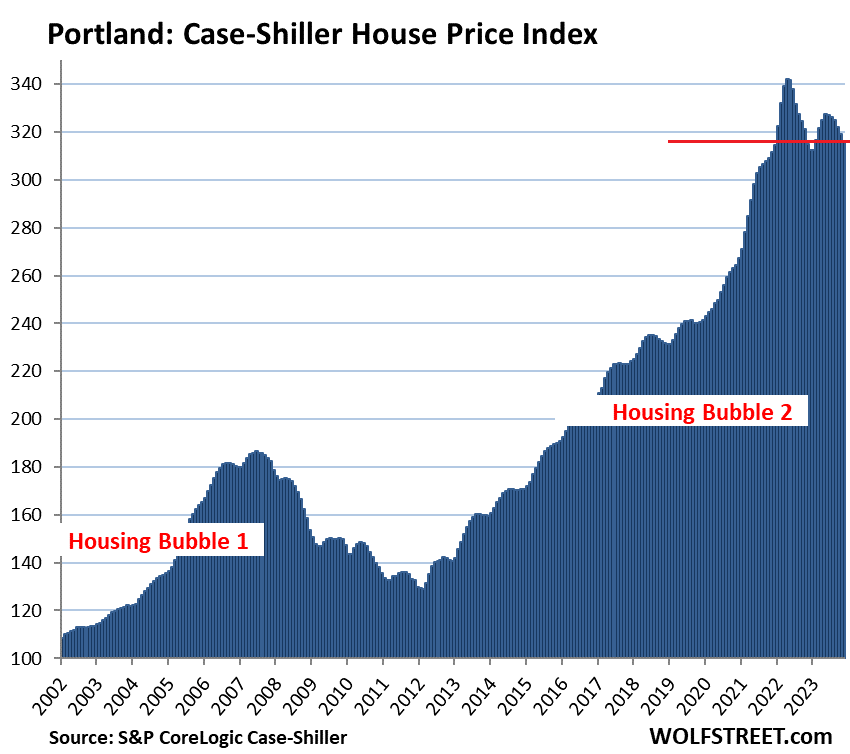

- Portland: -7.7% (May 2022)

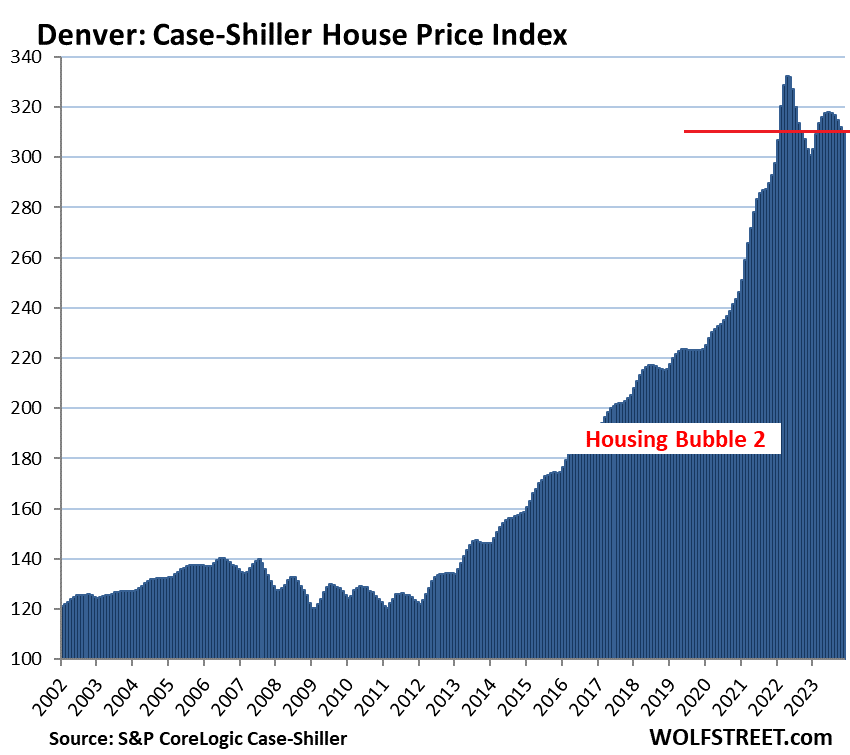

- Denver: -6.6% (May 2022)

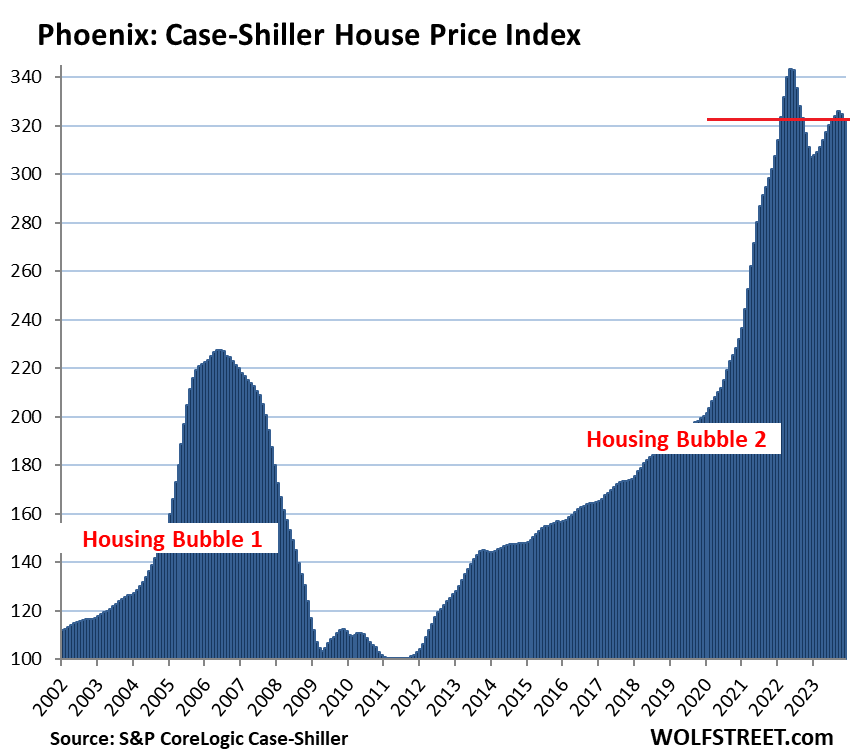

- Phoenix: -6.0% (June 2022)

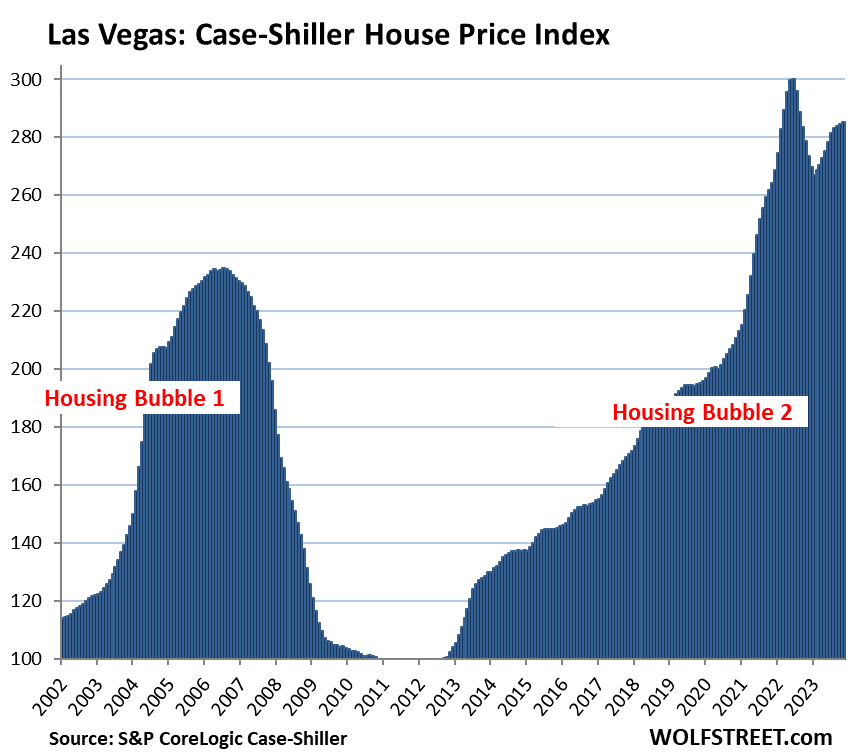

- Las Vegas: -5.0% (July 2022)

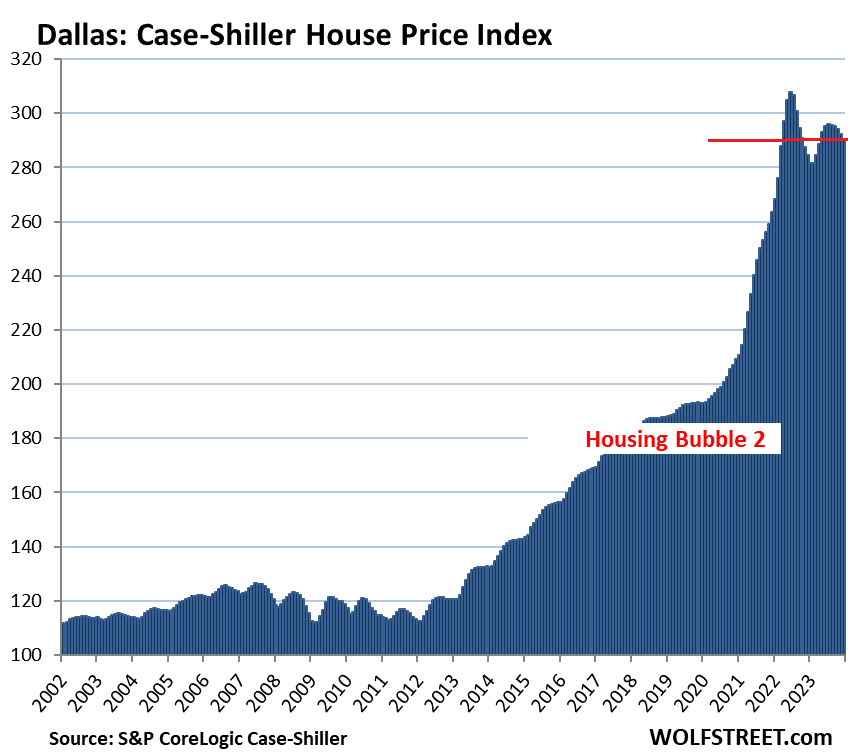

- Dallas: -5.6% (June 2022)

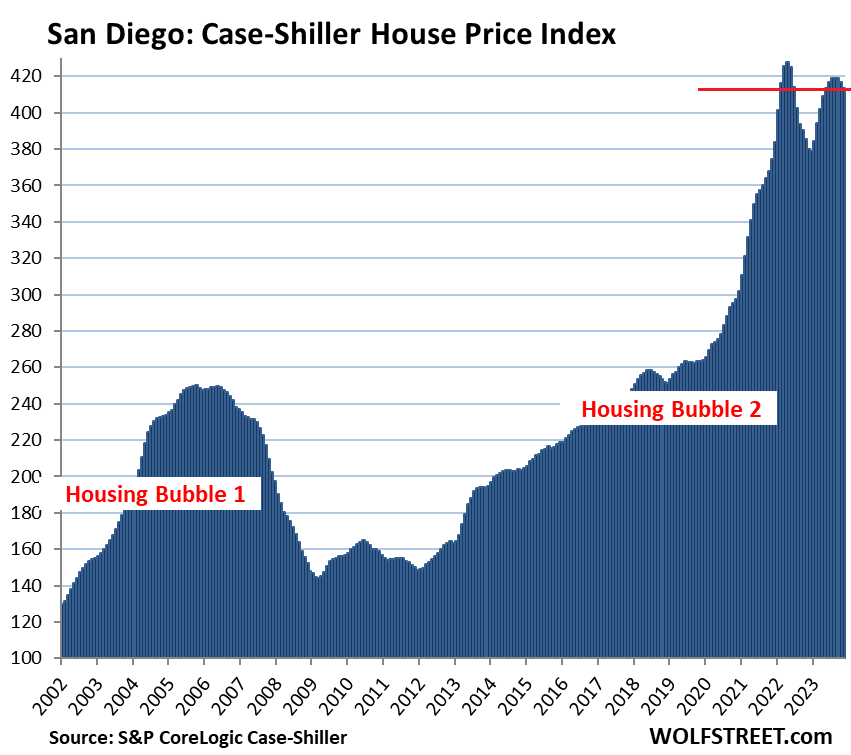

- San Diego: -3.4% (May 2022)

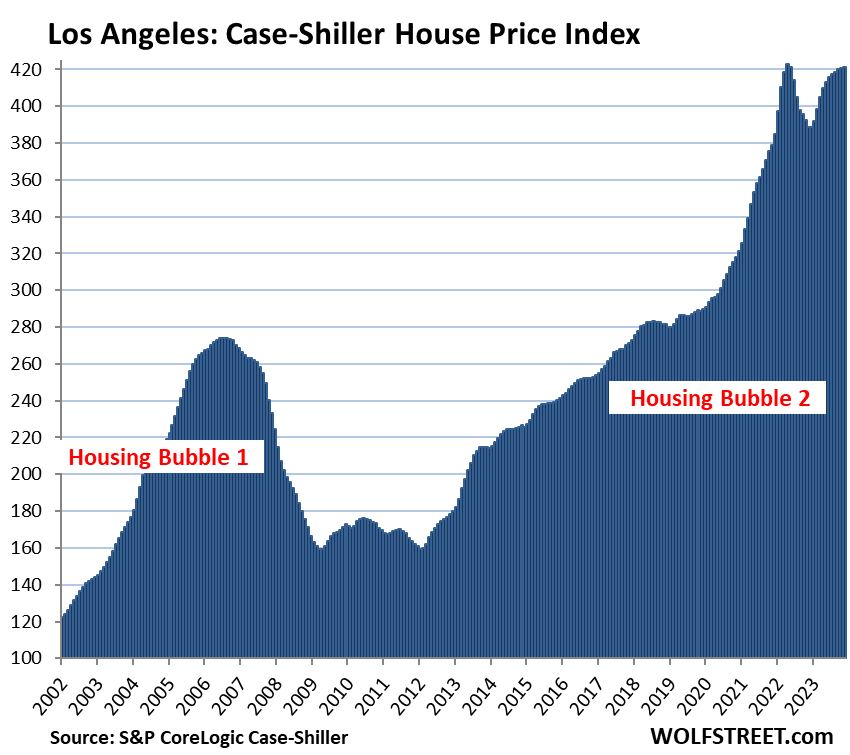

- Los Angeles: -0.4% (May 2022)

Month-to-month declines occurred in 17 of the 20 metros. Only Miami, Los Angeles, and Las Vegas had month-to-month increases. The index for Las Vegas and Los Angeles remained below the 2022 peaks.

Miami was the only metro of the 20 metros to set a new high in December.

The most splendid housing bubbles by metro.

San Francisco Bay Area single family houses:

- Month to month: -0.9%

- Year over year: +3.2%

- From the peak in May 2022: -13.4%.

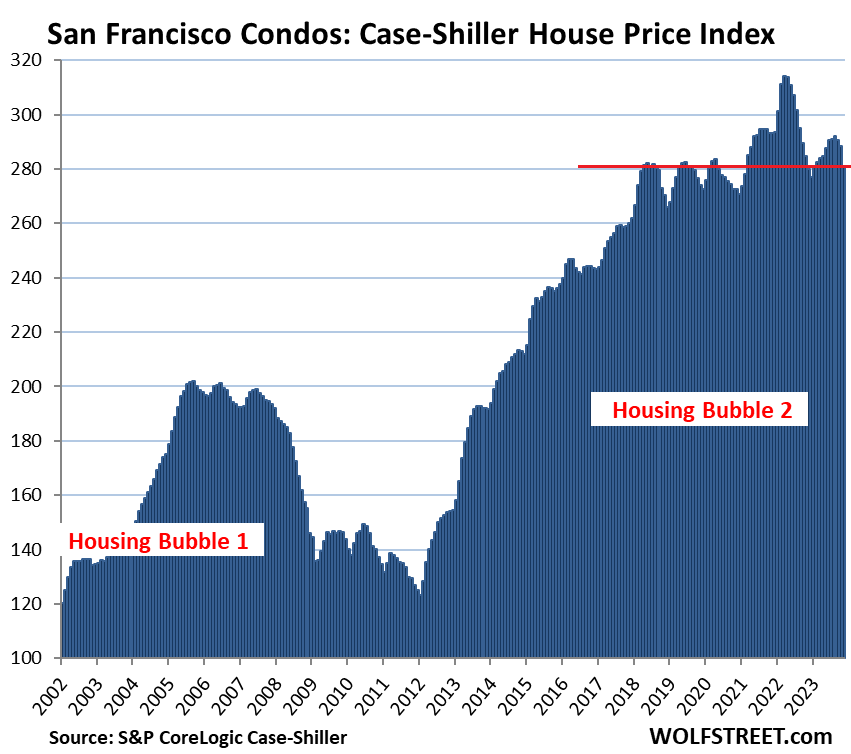

San Francisco Bay Area condos:

- Dropped to level first seen in April 2018

- Month to month: -2.6%

- Year over year: +0.04%

- From the peak in May 2022: -10.6%.

Seattle metro:

- Month to month: -0.5%.

- Year over year: +3.0%.

- From the peak in May 2022: -12.5%.

Portland metro:

- Month to month: -1.0%.

- Year over year: +0.3%.

- From the peak in May 2022: -6.8%.

Las Vegas metro:

- Month to month: +0.2%.

- Year over year: +4.2%.

- From the peak in July 2022: -5.0%.

Denver metro:

- Month to month: -0.5%.

- Year over year: +2.3%.

- From the peak in May 2022: -6.6%.

Phoenix metro:

- Month to month: -0.6%.

- Year over year: +3.8%.

- From the peak in June 2022: -6.0%.

Dallas metro:

- Month to month: -0.7%.

- Year over year: +2.1%.

- From the peak in June 2022: -5.6%.

San Diego metro:

- Month to month: -0.8%.

- Year over year: +8.8%.

- From the peak in May 2022: -3.4%.

Los Angeles metro

- Month to month: +0.1%.

- Year over year: +8.3%.

- From the peak in May 2022: -0.4%.

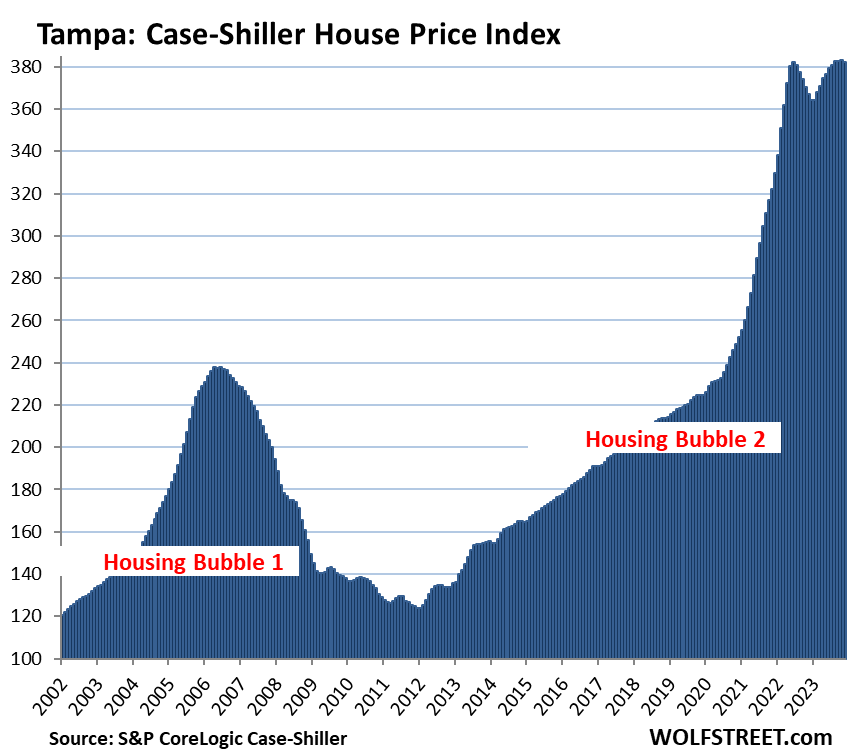

Tampa metro:

- Month to month: -0.3%, essentially unchanged for four months

- Year over year: +4.1%.

- From high in November 2023: -0.3%.

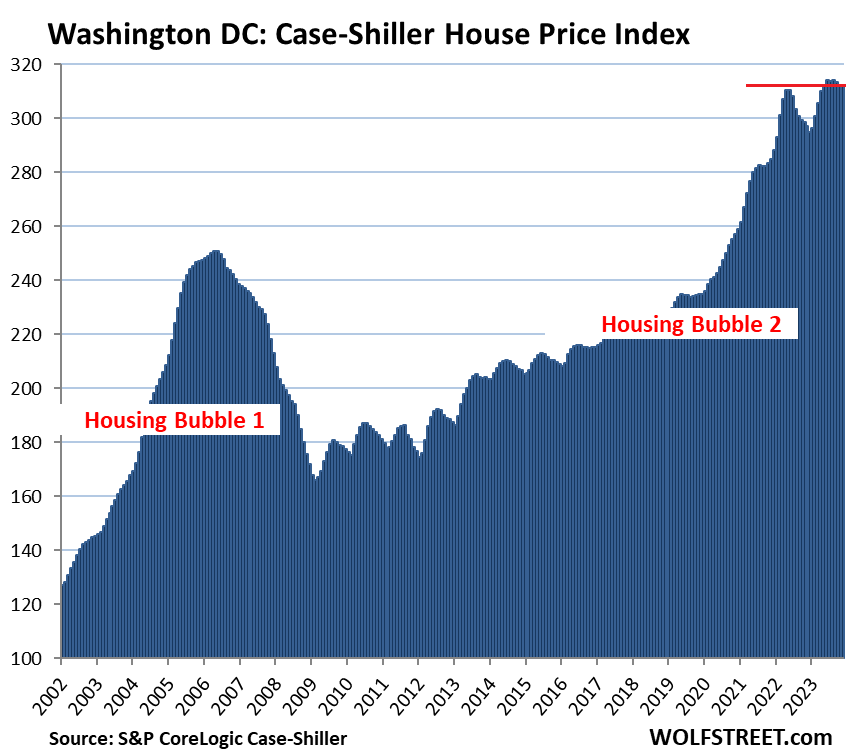

Washington D.C. metro:

- Month to month: -0.04%.

- Year over year: +5.1%.

- From high in September: -0.6%.

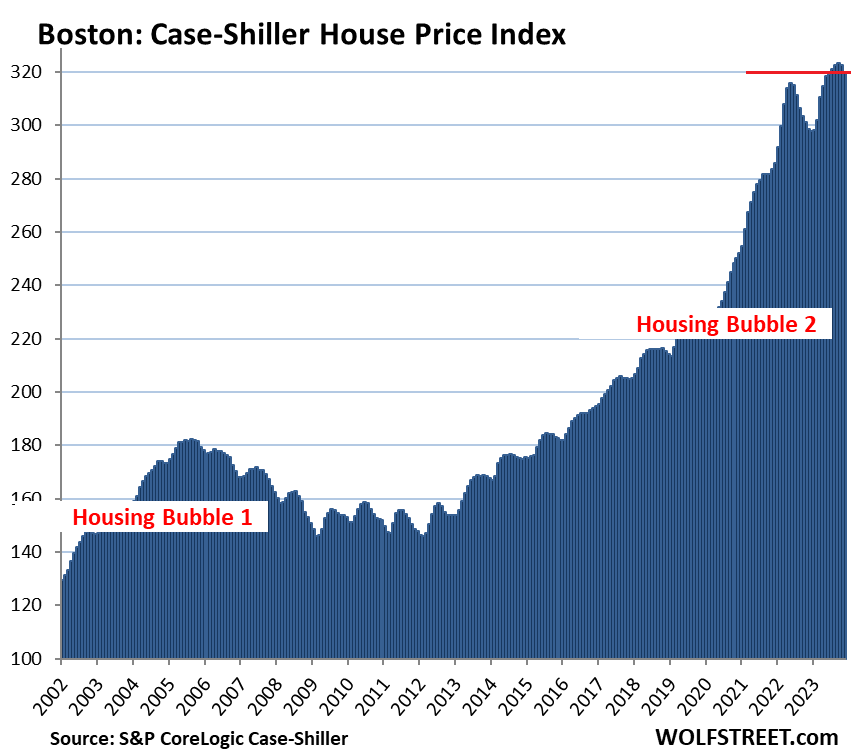

Boston metro:

- Month to month: -0.8%.

- Year over year: +7.2%.

- From high in October: -1.0%.

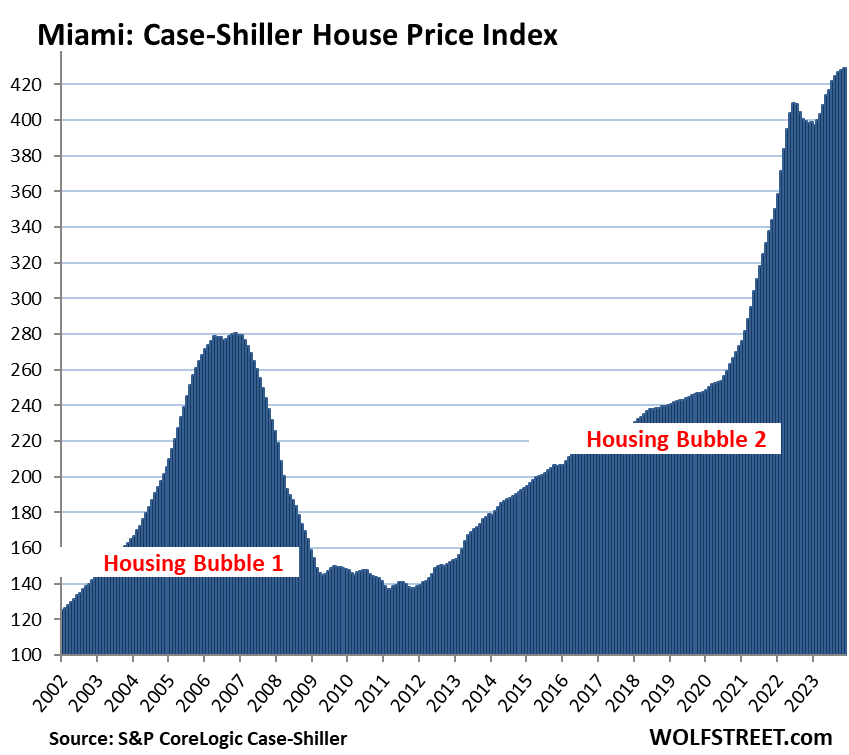

Miami metro:

- Month to month: +0.2%

- Year over year: +7.8%.

- Set new high.

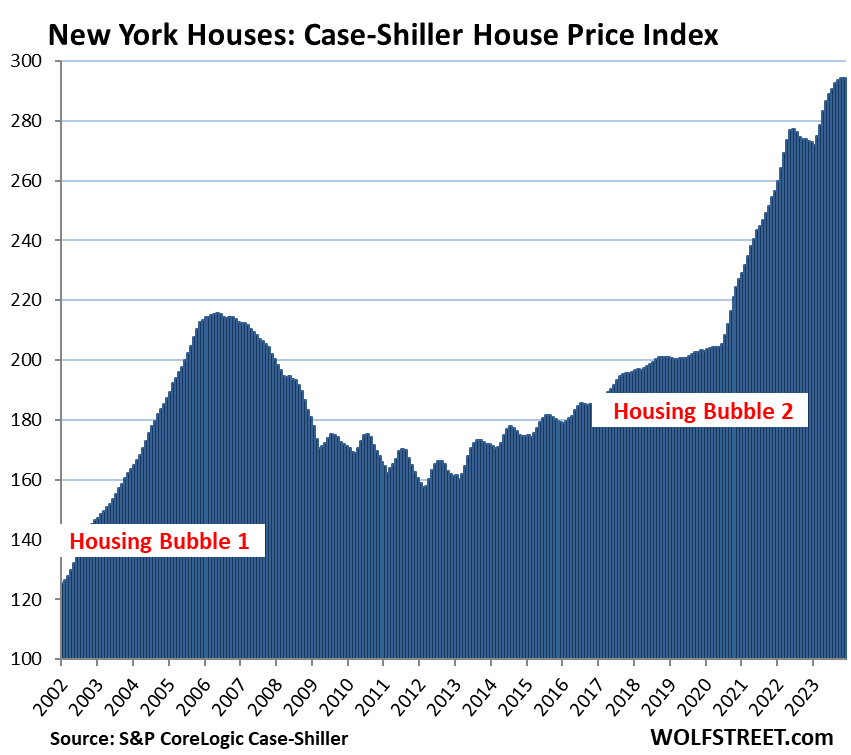

New York metro:

- Month to month: -0.04%.

- Year over year: +7.6%.

- The high was the prior month.

To qualify for the Most Splendid Housing Bubbles, the metro must have experienced home price inflation since 2000 of at least 180%. The indices were set at 100 for the year 2000. Today’s index value for Miami of 429 is up 329% since 2000, making Miami the most splendid housing bubble on this list.

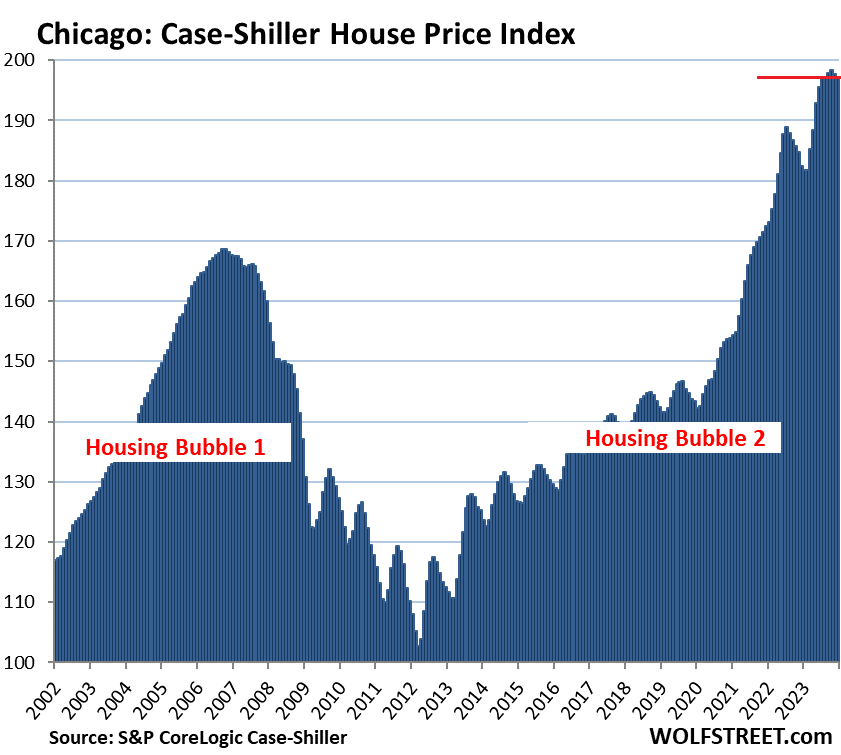

The remaining 6 of the 20 metros in the Case-Shiller index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) had less home price inflation than 180% since 2000, despite the price spikes in recent years.

Chicago, with an index value of 197 is up by 97% from 2000, and therefore does not qualify for this list of the Most Splendid Housing Bubbles, but prices experienced a red-hot spike since May 2020, and so here is Chicago anyway:

- Month to month: -0.2%

- The high was in October 2023

- Year over year: +8.1%.

Methodology. The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses were sold previously. The price changes are weighted based on how long ago the prior sale occurred, and adjustments are made for home improvements and other factors. This “sales pairs” method makes the Case-Shiller index a more reliable indicator than median price indices (37-page methodology).

Home-Price Inflation. By measuring how many dollars it takes to buy the same house over time via the “sales pairs” method, the Case-Shiller index is a measure of home price inflation. So Miami had 329% home price inflation since 2000. By comparison, consumer price inflation, as measured by CPI, was 82% over the same period.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks a lot for this WR.

In my hood SD.. this is just a noise..

Urban working class got really effed up and their dreams of buying a house got crushed with unaffordability.

Can they hold their leaders accountable for this mess?

I have the power to fix house value by locking people up in their houses using higher mortgage rates.

These jailed souls will still appreciate me and thank me for their higher house prices even it gets them the same house, but with higher cost of maintenance, higher taxes and insurance etc.

I gave a new meaning to freedom and independence in this country. Its time to thank me again.

The plebes are happily employed and probably losing weight by eating less and driving less. So Krugman is correct: Bidenomics and Fed policy are appropriate.

Why is there always so much negativity here? Some of us who’ve invested in homes and built equity don’t feel the need to constantly flaunt it. Perhaps Wolf is filtering out those comments. I’ll find out if this gets posted. Anyway, let’s maintain some dignity, folks. If you look far back enough at US asset trends, the graph always points upward and to the right. Simply invest when you’re able and strive to enjoy life rather than harboring bitterness.

I no longer allow RE hype trolls to abuse this site to hype RE. If they want to hype RE on this site, they can contact me to buy a banner ad, and they can hype whatever they want on that banner, but they have to pay me to post that banner. RE hype trolls are all the same, the whole RE industry is that way: they want publishers to provide them with free advertising to hype RE, just like the crypto hype trolls, etc. It never ends. I looked back at your comments (each with a different screen name) going back to June, and that’s kind of what you’re doing. Those are the only kinds of comments you’re posting, and only on this “Splendid” series.

You can hype RE on X. You can hype anything on X. Highly recommended. But not here.

Howdy Jpow Would love to know how many are incarcerated. The Lone Wolf might know. Will be interesting to see how many are foreclosed, short sales in the coming years. If that were to happen, you could find a new tool to fix things right up. Good Job, keep up the good work.

Since 2020 how much has inflation gone up. I am curious how much the dollar amount vs dollar value (I am sure there are more correct terms) of these homes have changed given the inflation. I’ve seen data on this before from Wolf but I don’t remember where I can find it.

In my little corner of “Fly-Over” country this kind of wild real estate speculation is also mostly just “noise”. But it is difficult for me to gauge exactly, as I don’t /can’t follow real estate closely.

But I am seeing some weird goings on. People converting duplexes into two story four-plexes, tear-downs of nice sfh ranches, and because there is a big tourist trade here, some houses are being converted into airbnb.

I am really surprized that so many posters here can not see the difference between “money printing” and “credit”. Only the government can print money, but any bank can hand out credit. Purchases (and related prices) made with credit can can turn on a dime. The Psychology around credit can move the so called “market” quicker than many here realize.

Mix easy credit with Covid, add a taste of MMT given to the poors for the first time ever, shake well, and we are in uncharted territory.

The market is in absolute gridlock right now. With a lack of movement volume, it’s basically down to who will blink first. The buyers or the sellers? Although I have to wonder, I wonder when the house carrying costs for institutional investors will come home to roost?

Not even close to “absolute gridlock”. Sales sure ain’t robust, but they also aren’t anywhere near zero. C’mon, man. Stuff is selling all over the place.

Gridlock? 291,000 buyers blinked just last month (new and existing homes sold). That’s a lot lower than it was during the most recent buying frenzy, but certainly not gridlock. And carrying costs are not a problem for institutional investors who pay cash and rent the house out. Invitation Homes, a big institutional landlord, posted a net income of $261M in 2021, $383M in 2022, and they crossed half a billion in 2023. They’re doing just fine.

The American consumer’s credit is nominally excellent, so there’s no debt crisis coming. That is what money printing does. It vaporizes debt and jacks up nominal pricing. You need to come to terms with the overwhelming likelihood that no housing crash is coming. Home values didn’t go up, the value of the dollar went down. 2008 is what a debt crisis looks like. The last few years is what money printing looks like. Simple.

I wish more people understood this, it’s not that the housing prices are going up, it’s the purchasing power of your money is going down, your money is being diluted, devalued, people just don’t get it.

Howdy John. When they sent America checks? Few knew they would be paying it back ten fold with inflation. How about it America??? Lets go ZIRPing again?

So much in here is just false.

First, institutional investors don’t pay cash, at least not in the sense that you think. They might settle a particular closing with cash, but they have large credit facilities that are secured by all of their houses or all of their assets in general. That means that they are very much affected by the cost of capital. The current numbers for buying to rent out don’t work. They are making a profit, but from purchases made in the past.

Second, the American consumer’s credit might be excellent now, but as soon as there are job losses, that’ll change. It’s always the case. There are enough people that don’t have any safety cushion and will run into trouble once they don’t have a paycheck.

Third, while I agree that money printing has led to a lot of the price increases in the past 2-3 years, it certainly doesn’t explain all of it, especially in areas that saw housing prices increase by 80-100%.

You are right that the housing market won’t crash as long as unemployment remains low. But if unemployment remains low, the Fed won’t be able to control inflation, and rates will have to stay high.

Eventually, sellers who are holding multiple houses will blink. I’m already seeing the cracks appear down here in South Florida, where a cluster of homes are for sale in a neighborhood (listed for 2022 bubble pricing) and nearly all are owned by LLCs. In other words, they were purchased not to live in, but as an investment.

It doesn’t take a lot of those (or AirBNB people dumping houses) to change the psychology of the market.

No argument here with the exception of your liberal use of the word “investment”. although the land under the house may be appreciating in value, the structure itself is a depreciating asset. That combined with the expense burden, (taxes, insurance, wear and tear) makes it the opposite of investment. Necessary shelter yes, a speculation yes, an investment, no.

@Einhal thanks for reminding people that “institutional investors don’t pay cash” (at least “most ” of the time). I have always “closed with cash” when buying both homes to live in and investment property to get the deal done then put a permanent fixed rate loan on the property. @Louie in some depressed rural and urban areas an empty home may “depreciate” but in most urban areas over the last 50 years an empty home will “appreciate” more than the cost of taxes, insurance and basic maintenance.

First, go to INVH investor relations and look at their 4Q2023 statements. They made a boatload of cash, spent a fraction if that cash buying houses in the southeast, and made some cash selling houses in the west. Residential RE institutions like INVH are flush with their own cash and/or investor cash and they use that cash to do business buying, selling, and shifting their assets all the time. They are most certainly profiting from aquisitions in the past as well as the present. Their scale allows them to make deals and insure their assets in ways you and I can’t. Their decisions often make plenty of sense given the current conditions.

Second, job losses don’t always have a big effect on asset prices. Not all recessions are the same. Deleveraging events (debt recessions) cause asset deflation. Inflationary recessions do not tend to kill asset prices from a macro perspective. Printed money doesn’t spread evenly, so you have to zoom out to see the big picture. On a nationwide scale, there were two inflationary recessions in the 70s and big double recessions in the early 80s. None of them saw a drop in national median house prices, quite the opposite. Nominal house prices exploded upwards despite big job losses and double digit interest rates.

Third, again money doesn’t spread evenly. Some areas have seen huge price growth and others haven’t. The money supply exploded and the national median house price followed suit. QT destroyed some money, and house prices dropped accordingly. Money supply flattened out and so did prices. On a national scale, it’s a surprisingly linear correlation.

Einhal, I know you’re one of the more pessimistic commenters here. And that’s fine, I actually agree with a lot of your posts. You’ve been bitterly clamoring for a huge crash, and you were right, but the crash already happened. The dollar crashed by a third of its value very quickly. It was a huge bust. If you’re still waiting for something big to break, you should listen to what Wolf has said over and over… Something big did break. Price stability broke.

Not Sure, you are right in that I am pessimistic about the future of America, largely because of uncontrolled immigration. But that is separate from the housing market.

INVH and other institutions may be flush with cash, but they still have opportunity cost. No one wants their cash used to purchase properties with 2% cap rates when treasuries return 5%. That’s all I meant.

Not Sure,

What broke was inflation, but the effects of that are not priced into LT bond prices yet. How can the Fed return to a long term 2% inflation rate when they needed 6% inflation the past three years to avoid recession?

Yes, part of housing inflation is the dollar getting worthless, but we are also in a bubble. Double the fun!! The U.S. House Price to Income, both numerator and demonator are nominal numbers, both are rising due to inflaiton. And we are at 6x, in the last bubble we were peak at 4.7x, just to get to the normal range of the last 20 years, price need to fall 33%. And home ownership is at or above long-term averages, so don’t push the whole “housing shortage” mantra to support silly used housing price. 8,000 baby boomers die everyday, and they have ownership in the 80% range. That plus high home building rate and slow population growth will eventually current the income/price ratio, if high interest rate or poor macro don’t do it first.

I’ve never seen or heard of this site before but it showed up in my Google aggregate news feed. I live in the Midwest and have been looking at houses for at least 6 months. All of them are ~25-50%+ price increases over the last ~4 years. It’s absolutely absurd and that is everything from shit bag venture capital flippers to small families who look like they’re ready to cash out.

If their loan is under 3%, sellers may never blink.

My friend has 3 percent mortgage and is forced to sell because of divorce 🙄

I suspect the low rates have locked many others into their marriages as well as their mortgages!

Nobody “needs” to buy a house. However, many “need” to sell. Guess who blinks first….

I think it’s hilarious how everyone acts like every homeowner who sells is going to go live under a bridge after they sell.

72% of all sellers buy another home right after they sell. Another 10% will rent temporarily until they find a replacement home. Thats 82% of all sellers who are also home BUYERS.

This market is undergoing a normal price correction of 15-20%. The crash happened in 2008. If you didn’t buy during the past 15 years of cheaper home prices, you might just be s out of luck.

By that logic, what sustains the price increase? The population hasn’t increased THAT much.

Couple things. 1) Increased purchasing power. 2) Increased willingness to pay. I’ve called the top in housing many times only to be wrong repeatedly. It’s that latter factor that I assumed was maxed out already that turned out not to be.

Lots of trillions of dollars printed by the last three administrations is what increases prices.

The same number of people with twice the amount of cash chasing the same number of homes or cars or stocks or anything. Economics 101 back when I got my degree.

@Einhal, there are more and more non-conventional families sharing houses. Not all senior are downsizing, some are actually upsizing (you can find articles online) to accommodate boomerang children living with them

Gotta say…disappointing to say the least….yeah yeah I know Titanic takes forever…let’s hope that’s still the case and it doesn’t turn into any re-accelaration..

Los Angeles metro

Month to month: +0.1%.

Year over year: +8.3%.

From the peak in May 2022: -0.4%.

San Diego metro:

Month to month: -0.8%.

Year over year: +8.8%.

From the peak in May 2022: -3.4%.

The big story today in the San Diego Union Tribune is the YOY of 8.8. The actual headline reads: “San Diego home prices rising fastest in nation” but there’s no point in linking to it as it’s paywalled. These numbers are all around two months old at best; anyone in this city will tell you that it has re-accelerated. I know many a millennial and gen Z who are very worried that they’re getting priced out of the market. My guess is that next month’s Case Shiller will show double digit increases here as will numbers posted in April.

That’s why I gave you the charts so I don’t have to listen to this BS.

Here is a free lesson:

YoY is made up of 3 components: #1. what happened at the “base” 12 months earlier (the “base effect”); #2 what it did after the base; and #3, what it did recently. That #1 was low, after a steep plunge 18 months ago — so it starts off a low base (= base effect); that #2 was a huge surge in the first four months of last year off the low base; and the #3 was the recent decline.

YoY is used by RE hype trolls as a propaganda tool when it suits them.

YoY is also going to rip your hype to shreds over the first half this year as the base effect reverses, LOL. You’ll be silent then, right?

Meanwhile, I’ll keep showing the chart so people can see what is actually going on, without having to worry about base effect, etc.

So here it again, in case you missed it:

I love love love it when Wolf shred these narratives to pieces..I stay for this..

But but but this time is different I am sure…

p.s. the data for a weird looking double-top chart like this is going to give you weird yoy comparisons. Just look at it on a spreadsheet what that does.

I’m a big Wolf fan, yet I don’t understand why the YoY is brushed over when we talk about housing. It’s a critical metric to account for seasonality. The hard fact is that most markets are up YoY and that is not unimportant.

JF,

The problem is that the price movements were not seasonal and the peaks were in different periods of the year.

Peak #1 was in May/June 2022 and peak #2 was around October 2023; the trough between them was in December 2022/January 2023. So December 2023 (the current month), coming off that peak #2, is lining up with the trough in December 2022/January 2023.

This is why the YoY data is distorted this time around. The distortion will flip the other way in the first half of 2024, we already know that from the data of the past 12 months. So we’ll some big negative yoy numbers.

The first four months of 2023 were a special thing, a sudden jump in prices, after a sudden plunge in prices, but it was ultimately unrelated to seasonality, but was some kind of psychological effect. People will write books about that. And it’s not happening this year through February, based on early data. So the YoY comparisons in the first half of 2024 are going to be a hoot.

Only in a few years will we be able to look back and actually see if this was a real double top and the market dropped substantially further, or if it was a normal correction on the way to higher levels.

Until then, we’re all just speculating and/or hoping – some for lower prices to buy and some for higher prices to hold or sell.

*** On a statistical note, the inflation adjusted value of $1.00 from the year 2000 to now is $1.83, so I wouldn’t exactly call a 180% home price increase in that timeframe bubble territory. 300% + yes. 180% doesn’t even keep up with inflation.

$1.00 to $1.80 is not a 180% increase – only 80%.

$1.00 to $2.80 would be a 180% increase.

CCCB,

I think you need to redo your calculations when you say: “On a statistical note, the inflation adjusted value of $1.00 from the year 2000 to now is $1.83, so I wouldn’t exactly call a 180% home price increase in that timeframe bubble territory. 300% + yes. 180% doesn’t even keep up with inflation.”

Assuming your inflation numbers of a dollar in 2000 being the same as a $1.83 today are correct, your conclusion that a 180% increase in house prices doesn’t keep up with inflation is incorrect. For example, If you owned a home worth $100,000 in 2000 and it went up in price based on inflation alone, it would be worth $183,000 today. An increase of 83%. If house prices have gone up 180%, prices have far exceeded inflation generally and that $100,000 home would now cost $280,000. Percentages can be confusing if you don’t remember to account for the base value.

Ha, you beat me MM

Lets take the opposite side of this.

As you pounce on RE hype trolls using Y/Y showing RE appreciation, is it any better to be using 2022 outlier peaks and yelling ‘fire’ for clickbait headlines?

Personally, I prefer to look at the macro enviornment as a whole, market trends (employment, sales, local industry, etc. etc.) and make my determination.

@Louie who doesn’t like to refer to RE as an ‘investment’, I ask is buying NVDA, MSFT, LLY, TSLA, etc. ‘investing’ ?

Our (10) rentals in WA and AZ that grossed us over $250K in 2023, call it what you want.

I look forward to getting tarred and feathered.

Jim,

“RE hype trolls” hate charts like these because these charts allow readers to see what is going on, and they don’t have to listing to this BS.

Jim, yes, real estate can be a good investment for income-properties if you buy in at the right entry point.

Right now is not that time, in my opinion.

“So the YoY comparisons in the first half of 2024 are going to be a hoot.”

And that’s then, conveniently, the media, realtors and various cheerleaders will ignore that and switch to a new metric.

Oops! Apologies Rojo, etc. on my math in my other comment. I failed to add the 180% price increase to the 100% base. Duh!!!

I still don’t think were in for a 2008 style crash though.

As Wolf once said in an interview a few years back, the comments section can get lively. I’m like a moth and this site is the flame I keep flying into. Let’s see what happens in the next couple of months. My main focus in on the City of San Diego and single family housing. I think the multi family market here is quickly becoming over saturated.

San Diego needs to explore improving the border crossing or a light rail into Tijuana, Mexico. Mexico is where San Diego’s affordable housing is located.

There is light rail almost to the border. You can get off in Imperial Beach and walk to Tijuana through a one way revolving gate…

I’m guessing you’re joking, but a growing number of both young and older Americans are actually moving to Mexico, Costa Rica, the Philippines, Turkey etc. and claim to be living amazing lives there at a fraction of the cost of living in the US

Light rail, or as we call in in San Diego, the Trolley, runs to San Ysidro and is about 400 feet from the border. A lot of folks live there and work here but most of them need their cars or trucks as they’re in construction. Tijuana is quickly growing, specifically the downtown area on or near Ave Revolucion, which has historically been the party spot in TJ. Tall buildings are being built there and lots of TJ style burbs are being built, not only near TJ but also at the Otay port of entry. The big problem living there and working here is the tremendous border waits, not only coming her, but going back, even with Sentri. If they ever get that border crossing situation fixed it will do a lot to help with the housing need in San Diego, but the bigger problem there is the water, or lack of it. We barely leave a trickle for Mexico from the Colorado River. The other huge problem with more folks there is that the sewage comes right up into the US into border filed state park and all of the rural communities by the border. There’s actually a state park there that never gets visitors because of this problem.

Do you want to know what the housing markets going to do just watch what the fed does. If the fed keeps interest rates high or even goes higher and continues quantitative tightening then you will see asset prices go down, if you see the fed come out and say they’re reversing course then you know asset classes are going to go right back up and take into consideration there’s a long lag between monetary policy changes.

I live in San Diego and stepped out of the market to rent. I can afford to buy but it just doesn’t make sense. A house in my neighborhood would cost $12K per month. I rent for $4.5k.

Every person I know who is buying tells me the same thing. The fed is going to cut rates soon and home prices will accelerate as soon as low interest rates return. There is no analysis or reasoning with these people. They are convinced that ZIRP/QE and rapidly rising asset prices are normal and that they need to get in now or be priced out forever.

Buy Now – You renting for $4.5k/month vs owning for $12k/month is a good move, that is over a 60% discount! The second part of your comment is where we disagree, what makes you think that home prices will not accelerate as soon as low interest rates return? Here you are, taking advantage of a 60% discount available partly thanks to the high interest rates, and yet the San Diego housing market price index is still managing to be near the high of May 2022. So what do you think will happen when this discount your enjoying shrinks as interest rates go down? If a whopping 60%+ discount is not driving the market down like I expected, what do you think a 30% discount is going to do? I do agree that the “get in now or be priced out forever” sentiment is usually short-lived and misguided, but I have no idea when the housing crash that brings affordability will come, maybe at the end of the next presidential cycle?

@beatleme

Why do you think interest rates are going to come down anytime soon?

Buy Now – I don’t know if they will come down soon, but I do know that they will eventually come down, and when they do housing prices will rebound. It is very difficult to time the market, so enjoy the discount while you can but don’t be surprised if we get another leg up in housing at some point.

“Eventually” could take 30 years or so, if the 1970s-2000s are a reasonable precedent.

According to the Fed’s data on average 30 year mortgage rates:

The last time mortgage rates crossed 7.5% after being below 6.5% was 1968.

It took 34 years before one could again get an 30 year mortgage for less than 6.5%, in 2002.

Historically in the US, rates also stayed high for over 95 years from 1790 to around 1875.

Assuming “low rates are normal” can be hazardous to one’s wealth.

A recession with job losses would make it happen ie home price crash

Also fed cutting rates don’t impact mortgage rates

Mortgage rates are tied to 10 yr.. which is tied to qe or qt .

“A tendency to go to extremes is often observed at the highs and lows of a protracted market trend. At such times, precedent and overwhelming psychological expectations reinforce prevailing economic factors.”

—Sydney Homer & Richard Sylla, A History of Interest Rates

Very sticky…

Especially with mortgage rates near 8%.

In absence of big job loss I don’t see home prices going down in a big way.

Govt would rather sacrifice dollar than face the recession..

What we are seeing in real life is dollar losing purchasing power over time .

Never has Houston on these charts.

Houston is not included. Back in the 1990s, when the CS was designed, they ran into big problems getting public records data in Texas, which doesn’t allow public access to deeds. But that’s where the CS data comes from.

To get the data for the Dallas metro, the CS people at the time worked out a deal with a Realtor association to get data from their multiple listing service.

And in terms of Houston, one of the founders of the CS said this:

“And when it was all put together, the decision was that was a bit of a hassle, so we’d stick with one city,” he said. Also, “we had Boston, New York and Washington so we decided that was enough for the Northeast, with apologies to Philadelphia.”

Crazy times- I have a friend looking to buy a duplex in the Boston area- all the bids are $50k over asking (list was $480k). It’s madness. They want best and final be tomorrow at 5:00. Also seeing other 2-3 families places near Manchester NH selling for 60% more then they sold for in 2019. Is this just the increase in demand from millennials or just FOMO?

My take is that it’s people doing what they want to do, living how they want live, and paying what they need to pay.

I guess as long as they stay solvent no problem!

These buyers are all Wendy’s franchise owners, and the ai dynamic pricing gains will cover it.

I think it’s FOMO, Isn’t that what happened at the end of a bubble.

Rick – all the new builds I see around here are either condos, townhomes, or modular homes, none of which include land & all come with substantial monthly HOA fees.

If you want your own place, on your own plot, you have to buy existing. Ergo, there’s no comprpetition from new builds (with their rate buydowns, warranties etc.).

Boston has a projected and overly optimistic budget deficit of $1 billion over the next three years. The state is already projecting a deficit $1 billion or more for this year. All this in a very small state. Most commercial permitting has dried up and the last desirable commercial and residential core area (Seaport) has now been designated for a large “”migrant” (illegals) shelter. Massachusetts is #1 for outmigration in the U.S. and most of those folks (80%) have incomes at or above 200k. Hard to believe bids so high. Come November young adults looking for reasonably priced housing will punish big time the party in power.

Just a shot in the dark but I feel the core PCE will come in pretty hot on 2/29 perhaps sending equity markets in a tailspin…… which might become the trigger to a recession. Let’s face it ….. until people in masses begin to lose their jobs, the housing market is going to remain stagnant.

One month Core PCE wont do much. Only Series of hot inflation data will wake up FED members completely. Stock Market has been laughing at any bad news coming. In DEC 2023 Powell dovish Press Conference and SEP projections started the rally. Later Powell said only 3 rate hikes and that too they can wait and be patient. Many FED Governors have come out and given speeches about 2-3 rate hikes and can wait with Whats Rush mind. S&P went ATH this month even after all of this and hot CPI. 10 year is still around 4.25%. Yes its higher than 3.75% which it reached during Dec 2023 time-frame. But still very low compared to what it should be.

In my mind reason is clear. FED is underestimating the amount of liquidity they created during last 15 years and mega-QE during COVID. Funds rate 5.25-5.5 rates didn’t make lot of difference. One can argue this is Strong economy. Yes it is. But that also tells us rates are not restrictive enough then. Federal Govt is spending money like drunken sailor and negating much of the FED’s inflation control work.

No one can deny Wolf’s analysis and numbers here. But I also see lot of buyers still out there who have made lot of money in last 2 years with Stock market gains. Homes are moving in good neighborhoods. 10% correction from ATH is not a lot of correction. Wolf’s graph paint very clear picture.

If Bubble 1 was a bubble, Bubble 2 feels like Hot Air Balloon.

Only good old old recession with higher unemployment rate can fix the Home prices.

It will take more time than most people expect.

The pig (money supply) has not worked its way through the python (consumer) yet.

The state of Illinois has yet to find a way to spend all its federal money (ARPA). this corrupt, liberal state has choked on the flood of money. It now has a historically “balanced budget” due to the increased inflow, not a reduction in outflow.

They are still looking for innovative ways to distribute those funds, like repaying businesses in the state for their unemployment insurance expenses.

We will be in the nonsense until those funds work their way through and become the new water level.

The markets will continue to rise with the water level and multiple new laws increasing the number of contributors through 401Ks. Equities will be moderately successful for the next decade due to bling index investments, with anything newsworthy getting a bigger bump.

The craziness will continue until people believe high rates are here to stay and that ZIPR/QE is over.

The general public doesn’t believe the fed will stay the course. And why would they? The fed stepped in as soon as banks had problems in early 2023. So why would the public believe the fed wouldn’t turn the money printer back on when things start to crack?

Buy now or be priced out forever is the current sentiment.

“The general public doesn’t believe the fed will stay the course. ”

The general public doesn’t even know what the Fed is.

🤣👍

The first baby boomers are now 78. Therefore, boomers have 8-10 years of remaining life (male and female respectively) according to the actuarial tables. Assuming by 85 they need to sell their homes to move to assisted living, that means by around 2030 Housing Bubble 3.0 will have popped…?

Most boomers will age in place rather than hand all their remaining assets and their soul to the PE-firm-driven medical-industrial-financial complex. But they might downsize when they get into their 80s.

Everyone in my family and in my in laws’ family have either stayed in their homes until they died or are still there in the process of doing so.

Afterwards, the homes of those who have passed were either taken over by their spouse, another family member or are rented out for income.

I wouldn’t count on a huge amount of new inventory coming from aging homeowners. Only those who absolutely can’t afford to age in place will give up their lifelong homes. Besides, in both Texas and Florida, the cost of a memory care or assisted living facilities starts at $10,000-$12,000 per month and goes up from there. And to be properly cared for you still have to hire a private caretaker on top of that.

It’s cheaper and healthier to hire full time help and stay in your own comfortable home.

It’s only cheaper to hire full time help because America has imported many third world immigrants. Socialize the costs, privatize the gains.

@CCCB My parents still own the SF home my Mom grew up in, but after working in Real Estate for over 40 years and talking to people about Real Estate every day I can tell you that just a small minority of families keep family homes after their parents die. The majority of Boomer kids will sell once the parents die since most want the cash and many that want to keep the home are “forced” to sell because they can’t afford to buy out their siblings. A friend with living parents in their 90’s recently told me that I should try and make it out to his family beach house on the Seadrift sandspit this summer since when his parents die he won’t have the money to give each of his sisters (who live out of state) $2 million each for the place that Zillow says is “worth” about $6 million…

I think Apartment investor has that right. Often times the homes being sold are in retirement communities, far away from jobs and good school districts. The beneficiaries with Jobs and kids of their own can’t live in the inherited home, and they don’t want the hassle of being a long distance landlord…generally.

Three retirement places were sold in my family the past three years when people died. No houses were kept. We cashed out the appreciation and paid zero tax because of the gain exclusion.

My neighbours are 88 and 96. They are aging in place. In our rural area enough people pitch in help with maintenance, shopping, etc as they have no family. Their biggest concern is having a fall. If they moved to assisted living it would kill them….it isn’t even a consideration. If he (96) takes a tumble she will buy a condo in town. If she takes a tumble, he’ll kill himself….at home. Seriously. This topic comes up quite often. Going over for an espresso in a few. She makes the best Italian (only) espresso on the planet.

Example, I just plowed their driveway and a path to the mailbox. They’ll pay me back with a nice coffee.

Assisted living has already priced out most boomers.

Not if they sell their house(s) for an still-impressive -6% below 2022 peak. Plenty of home equity among boomers. They don’t want to leave.

I hear this one a couple times a day: “They’ll have to take me out of this house in a pine box.”

My good friend works in a assisted living facility.

No one wants to leave their own home and live in assisted living facility. All of them living there are forced to be there.

I’m nowhere close to retirement but I’m ok with living out the rest of my life in my current home.

I’ll also drive my (2011) car till the day they take my license away.

I know it’s anecdotal, but I know of at least three 80+ year old men/women who’ve aged very well. They are not only physically spry (swimming, biking and climbing) but also very much “with it” cognitively, holding their own in discussions/debates and readily grasping modern technology/UIs.

Try to observe wholistic healthy living throughout your years and your autumn will not serve as your second infancy.

Many boomers are no where near needing assisted living, What is the fixation with boomers? Many people in older generations are aging in place. I know. I work with people in their 80s and early 90s in their own homes they have owned for 50 years. And one generation is not responsible for the housing shortage. I’m so sick of the propaganda. I plan on dying in my own home.

Current demographic projections show the U.S. population declining by 2050, even with high net migration, due to far more deaths than births. So yes, housing prices should go down (relative to inflation) in future decades

For me, those stats are irrelevant. I was born in the early 1960s (so a “younger boomer?”), and want to sell my paid-up house (bought 22 years ago) and move to a property with the potential to improve into everything I want. I am not downsizing, and fully expect the new property plus improvements to end up costing 50-75% more than what I sell my current house for. (So I’m fine with a market crash.)

Unfortunately, due to the current lack of inventory and relatively high prices, my real estate searches over four states yield very few potential properties. When I add the cost of improvements to the list price, most properties would end up much higher than the current comps. So I wait. Eventually, I might give up and have a house built to-suit. But I think that would be just as expensive, if not more so.

MaddieB

Your situation sounds exactly like mine.

Boomers that are relative young, healthy and are financially comfortable.

We will be around for

A tad bit longer!! Lmao.

Patience and enjoying the downtime is mandatory.

And the youngest are only 59 to 60, so what’s your stupid point? You idiotically stated the FIRST boomers are 78 and then went on to stupidly say boomers have 8 to 10 years remaining, suggesting all boomers had 8 to 10 years to live even when you admitted the first were 78 (which suggests there are younger ones which there are). So if the youngest are 59 to 60, why would you make such a stupid statement? Is that the critical thinking they taught your generation in school? If so, I want my property taxes money back. Plus, who gave you the expiration chart? You stated, as if fact, that boomers will live to 86 or 88 only. Please don’t comment as you have nothing meaningful to add to the conversation.

The payment of interest on interbank demand deposits, which if exceeded short-term money market rates was specifically illegal per the FSRRA of 2006, caused investors to recalibrate.

Bernanke, pg. 287 in his book “The Courage to Act”, “Lower long-term rates also tend to raise asset prices, including house and stock prices, which, by making people feel wealthier, tends to stimulate consumer spending” (aka the “wealth effect”).

“Housing is considered unaffordable if it costs more than 30% of an individual’s income”.

If you use outside money to suppress interest rates, you stoke asset prices. That’s backwards. It’s subterfuge.

It is much more desirable to promote prosperity by inducing a smooth and continuous flow of monetary savings, income not spent, into real investment, than to rely, as we have done c. 1965, on a vast expansion of bank credit with accompanying inflation to stimulate production.

The economic engine is being run in reverse. Lending/investing by the banks is inflationary (expands both the volume and turnover of new money). (where S “≠” I ). Lending/investing by the nonbanks is noninflationary (other things equal). (where S = I ).

The FED is nowhere near 2% inflation if you consider asset prices in the definition of inflation.

Wof: on the Boston metro chart, which months did the last peak and subsequent trough occur in?

I feel like that large yoy gain is misleading, as it looks like the trough between the double tops occured right around this time last year. So that ‘gain’ is just the delta between the local low last year, and now.

Wolf* sorry. Also I now see you addressed this in a prev comment.

Yes, that’s the problem with the recent price movements. They were not seasonal, and so YoY comparisons deliver distortions: In many of the double-peak charts, peak #1 was May-June 2022, with the trough in December-January. And peak #2 around October 2023, closer to the low point 12 months earlier and not lined up with peak #1, which distorts the YoY comparison.

YoY comparisons only make sense when the fluctuations are highly seasonal and lined up 12 months apart. I pointed this year-over-year distortion out in my reply to “The Bob who cried Wolf” near the top.

In Boston, peak #1 was in June 2022, the trough in January 2023, and peak #2 in October 2023. So we’re now (December) getting comparisons to the trough, but we’re just a couple of months of peak #2. Which is why we’re getting these yoy distortions.

As I pointed out above in my reply to “The Bob who cried Wolf”, we already know by looking at the past 12-month data that this yoy distortion will flip in the first half of 2024.

The first four months of 2023 were a special thing, a sudden jump in prices, after a sudden plunge in prices, but it was ultimately unrelated to seasonality, but was some kind of psychological effect. People will write books about that. And it’s not happening this year through February, based on early data. So the YoY comparisons in the first half of 2024 are going to be a hoot.

I used to believe in a housing crash, but I firmly believe that we’ve already seen the bottom of our current market.

Why?

1) Americans have become extremely educated about the housing market, and it’s easier for people to have multiple jobs.

2) There are long-term impacts of the COVID housing policies that will take years to wring out of the market.

3) There are too many creative financial schemes to de-risk high interest rates.

4) For the foreseeable future, the economy is soaring based on COVID-era money that was properly invested in infrastructure and manufacturing.

5) We’re entering an era where most real estate will be passed between families.

6) The labor market is almost permanently smaller than it was before COVID.

7) Remote work has forever changed geographical constraints, and despite the current fad of return-to-office, remote work will eventually grow back to the high pandemic numbers.

This isn’t to say that there could be regional crashes (i.e. Florida) due to local issues. However, I’m finding it difficult to discover what exactly is going to lead to a housing crash at this point.

Unemployment up, it will be enough

How high do you think unemployment will go?

I had similar feelings during 2007 2008 .

It all hinges on recession and thus un employment.

The market would surprise us when no one expects and in a big way.

A lot of people think like you about stock market as well that it has reached a permanent high plateau.

How high do you think unemployment will go in the next year or so?

It certainly looks that way.

It’s Different This Time!™

I’ve come to despise that cheeky saying. It doesn’t even know what it’s mocking. Different compared to what? Different from the GFC, different from WWII, different from the 1970s?

If you’re comparing 2024 to 2008, then yes, it is very different this time. Today’s consumer debt is nominally fantastic because it was papered over by the fed. Big banks are in excellent shape with the gov and investors carrying the real liabilities. The consumer will not be facing a debt crisis anytime soon. But if you’re talking about aggressive money printing leading to inflation (like in the 70s), then no, it’s not different this time.

New York metro:

Month to month: +0.04%.

Year over year: +7.6%.

The high was the prior month

Does this make sense? High +0.04% is lower than prior month?

No, it doesn’t make sense, the + was a typo; it should be – as in -0.04%.

Thanks

Wolf,

With the price difference you have been seeing between new builds and resales, have you seen a correlation between cities with overall price declines and the inventory ratio of new builds to resale?

Would you consider this the main reason why prices have held up in the Northeast compared to other regions? (Fewer new builds)

I am also curious about this.

As I mentioned above, all the new builds in my area are condos, townhomes, or mobile homes – and all come with HOA fees, some of which are very expensive.

If you want a house on your own plot of land, with no HOA, the only choice is to buy existing.

Seeing new listings and price drops (mostly 3-5%) hitting market daily in this corner of SW Florida. Feels like the psychological inertia is toward listing now rather than waiting it out.

A return to 7-8% mortgages, along with the end of sunbird season, seem likely to accelerate that inertia…

Or is it just my wishful thinking on my part, as a prospective buyer!?

Outrageous increases in Florida homeowner insurance premiums (in some cases 300%) and ridiculous tax appraisal increases on non-homestead property is very likely the cause of a lot of new listings there. Income producing properties no longer produce reasonable income compared to other investments.

I have long said that those two items, insurance and taxes, more than high interest rates, will make owning a home impossible for many.

The taxes in FL are pretty bad for homebuyers that can’t carry over a save out homes cap/savings from a prior property. The new assessment and taxes after a sale even if you homestead it can be multiples of the prior owner if they are older with years of caps/savings in FL applied to their property and you don’t. That’s not even getting into the insurance headaches lol.

Seeing lots of chatter about many SFH, purchased by investors with cash, are starting to list for sale due to no one wanting to rent at crazy prices. The houses, purchased with cash, are asking for current market price (nearly +30% what it was purchased for). They are still sitting with a few bites, but no serious offers. The larger firms sit longer, but the smaller landlords are selling for a 5-10% profit. I think from reading Wolf – this is due to other investment tools making sense again?

Wolf – since you’re pulling down the data anyway, can you make charts for all 20 cities in the index?

the others are not “housing bubbles,” and so they don’t fit into the series. If one one them makes it into the housing bubble definition here (180% house price inflation since 2000), I’ll add it, like I added Dallas a few years ago.

Great work as always! I apologize if this has already been addressed and I’ve somehow missed it. I am just curious how lending standards are today versus the lead up to the GFC. I would assume they have improved, but the reason I ask is because this summer we moved and were approved for a large mortgage. Much higher than we had expected and realistically impossible to maintain over time. We were encouraged to wrap a bunch of expenses into the loan as well. We didn’t end up buying, but I definitely had a flashback to 2007 when we were delusional enough to buy.

1. lending standards are pretty good in general, and default rates and foreclosures are minuscule. But it doesn’t matter for the banks because…

2. Banks are no longer on the hook. For most of the mortgages, the taxpayers are on the hook, and for mortgages that don’t qualify for government backing, investors of private-label MBS are on the hook, so banks don’t really care what happens to those mortgages. That is one of the biggest changes coming out of the Financial Crisis.

The FED and .gov have engineered the most massive, reckless everything bubble imaginable. They have turned all of life’s necessities into speculative assets and commodities where the wealthy pump them into levels unconscionable.

There is hell to pay coming, make no mistake about it. The FED should have never stopped raising rates, and they should have never bought those MBS. And they should be selling those MBS at a much faster clip. Instead, they and all of their crooked political toadies are doing everything in their power to support said bubble.

The big mistake is thinking asset price inflation is not damaging and not within the Fed’s mandate. It’s a profound error logically and morally.

Bobber: A BIG yes to you!

And, we have a very meaningful global example right under our noses, which is Japan.

In around 1989-1991, Japan monetary policies created huge bubbles in real estate, low-interest loans, bonds, and stocks. It has taken Japan the last 35 years to grind up the rubble that was created when those multiple big bubbles popped!

Listening now to all of the rationalizing propaganda, brainwashing, and excusing of ignorant easy money policies is repulsive and disgusting!

I agree with you that it is damaging, but Powell has explicitly said home price inflation is not part of the Fed’s mandate.

The mandate is like any other law. The Fed has to use common sense when interpreting it.

There are clear links between money supply, asset prices, consumer prices, and economic activity. It’s pure tunnel vision to think asset prices have no impact on consumer prices or employment.

Depth charge was right all along. Bitcoin up 60000 and stock market near all time high. And it all began when Powell started talking about rate cut November 2023. And they still not doing anything to increase the pace of QT to stop this speculative madness. This bubble has been going on for way too long. What a messed-up world.

That is what is nice about the FED. They tell you in advance of what they are going to do and you can front run it. At the end of 2021, the FED said they would raise interest rates. I went all cash and avoided the stock market downturn. When they said they were going to cut rates, I pivoted and went from cash to stocks.

Yeah the problem with that is that it means that inflation will stay out of control for many years.

True Einhal. The CBO predicts the Gov needs to add 20 trillion more debt over the next 10 years. But we know that estimate will be wrong and I bet the number will likely be 25 trillion. That is and increase of $75k per person in the US. Where the government spend that $75k per person.

Even right now, the Government is being asked by the Chip companies to increase the grants from 39 billion to 80 billion.

The green transformation was supposed to cost $300 billion but now we are looking at over $600 billion and most expect to go over 1 trillion.

You have millions of new people arriving in the US and many cities are asking the government for aid to pay for food, shelter, and health care.

Currently the Government is giving so much money away, it is going to cause inflation in things people need.

i.e. Twenty-five percent of farms received government payments in calendar year 2022, the latest year for which estimates are available. Government payments to the farm sector averaged $16,308 for those operations receiving payments,

I am not saying if the any of the above it good or bad. It is what it is.

I have a friend who works for the government that gives out grants and loans to rural communities for water districts, rest homes, new business. In the past he said they averaged $6 to $7 million a year. Last year was over $125 million. He says the are so freaking busy giving out all this money.

There is perhaps no better example of the distortions in the economy from the FED’s recklessness than crypto. Gambling tokens with zero intrinsic value have become tools for the billionaires and their political toadies to make obscene profits while luring in unsuspecting fools and get-rich-quick types. And it has been working.

And now that so many politicians and bureaucrats have started gambling and winning, maybe we’ll hear from .gov that with every new birth certificate comes a crypto wallet and a free puppycoin or something, to get the little kiddies hooked early. Everything is rigged.

At least “meme stocks” have a company behind them. Crypto is literally nothing. And so the pigmen have created a product of “nothing” with a total market cap over $2 TRILLION where they can just squeeze blood out of a turnip for years. This is the result of decades of ZIRP and the desperate chase for yield and just pure, rapacious greed.

I love Wolf and his site, and this is not meant to criticize him whatsoever, but I mentioned after the FED’s first pause that they wilted and that stocks would be setting new, all-time highs. He disagreed and said something like “how?” We now see how.

There is simply way too much money sloshing around. The FED never took away the punch bowl, they just went from Everclear to 80 proof. There has been no landing, only smooth flying at altitude.

Regarding paper money and it’s correspondent problems, two and a half centuries ago:

“A nursery of tyranny, corruption, and delusion; a veritable debauch of authority in delirium.”

— Honoré Gabriel Riqueti, Count Mirabeau, A Letter To Cerutti, 1789

Didn’t work then, and the problems are even more intractable now.

Intentionally pursuing a wealth effect is particularly illogical and immoral, as it favors asset holders over non asset holders (a reverse RobinHood effect) and exacerbates wealth inequality.

The wealth effect and asset prices, once artificially elevated, have to be protected because the popping of a financial bubble threatens to create deflation in the real economy. Options become limited. You can continue the asset bubble or trigger a deep recession. Thus, the pursuit of wealth effect has no escape plan. It’s illogical to head down that road to begin with.

Yes, this is the problem. Assuming the Fed governors are acting in good faith, their mistake is thinking that asset inflation benefits everyone. They, and everyone they know, probably has a handsome stock portfolio, and don’t know anyone who doesn’t benefit from a run up of asset prices that come with CPI inflation.

Overly narrow perspective.

Its liberal ideals that have inflated the value of home ownership and set so many up for the most devastating loss of their lives by government-supported home loans. Are these loans to support home ownership or the market? Are student loans for students or Universities? Is medical insurance for patients or the medical establishment? The same is true of the new laws to force workers into 401k contributions. Is this for the worker’s future or the market’s?

We are all getting fleeced by our government’s programs.

Bobber, you know that “full employment” thing the Fed also has to manage? That’s a logical reason.

Is your point saying the Fed has a mandate? That always been clear.

You seem to be implying that the Fed’s approach was the only way or best way to achieve the mandate, which also implies you think the results of that strategy have been acceptable. I think victims of asset inflation and CPI inflation would disagree with you. The level of financial uncertainty today is off the charts.

The only viable strategy for the long-term is to keep the money supply stable in relation to GDP and keep interest rates at a reasonable level so companies must compete on the merits and purge inefficiencies on a regular basis.

We are in our 40s and I’m starting to think that home buying will never again be in our future. The last time we bought a reasonably priced house was in 2003. Its depressing to think about.

Now imagine how depressing it is to be priced out without ever having bought one.

Sorry, that is depressing. If you don’t mind me asking, how old are you? Do you have time to wait the market out? I personally think high(er) prices are here to stay, but they will at least back off from these ridiculous highs. Just my thoughts though, wish I had a crystal ball.

I cannot speak for Pea Sea, but I am 37. Never owned a home because we didn’t want to lever up on excessive debt when we weren’t financially stable/well off.

I have two degrees in Stem, Biochemistry and a Masters in Analytical Chemistry. My wife is a School teacher who helped support me through my Masters and weak employment years after GFC and the following awful job market, which we both graduated into with our respective Bachelors.

I love this site and love the comments, but there is one thing that I see a lot of older commenter’s say that is rather frustrating. They imply that the younger generation is either lazy or not financially literate enough to make good choices and end up in a house.

My Family’s story does not support this narrative at all. We tried to be financially responsible and are both educated in very applicable fields with Job options. Neither has been enough in our time line to net us a home. Bootstraps isn’t the issue, nor is a degree in basket weaving. It’s mostly timing and a prolific spike in home costs relative to income in recent years.

Now that I’m well employed house prices are just very very high with concurrently high interest rates.

I also see people say “just get a starter home” your generation wants/expects too much etc.

I’m not 25 anymore and we have a second daughter on the way. A starter home isn’t even appropriate for our family anymore. What’s more, my father at this time in his career, with far less technical skills/education was on his 3rd house… I think it has much more to do with stagnant real wages and massively inflated assets in that time frame. Not one generation being harder working than any other.

Biorganic – I hear your story, but every generation has faced something difficult and has pushed through. For example, I just saw a chart that looks at California existing single-family median prices and the runup from 1970 ($24,640) to 1990 ($193,770) is nearly 8x appreciation! Now how do you think people felt in 1990, wouldn’t you think it would be a similar story than today’s generation? Now of course home price appreciation is not the whole story when it comes to affordability, so lets look at the % of California households that can afford a median priced home along with some historic lows: 4th QTR 2023 = 15%; 2006 = 12%; 1989 = 17%; 1980 = 17%. The hardest times to buy a home in California look ballpark, so are we simply at another one of those times? Were people during all these terrible times never able to buy a home? Of course not, they just had to buy at a better time. In the meantime they saved for a good down payment, took care of their credit, and kept an eye on the prices in the neighborhood they wanted to buy in. It took me about 8 years of frustration, saving, monitoring, and feeling left behind to finally make it happen.

Bio,

“but there is one thing that I see a lot of older commenter’s say that is rather frustrating. They imply that the younger generation is either lazy or not financially literate enough to make good choices and end up in a house.”

My opinion, it’s less about lazy and a lot more about lack of patience. I get the impression the younger crowd thinks they should have a sweet pad and a Porsche early in their career. PLENTY in the Gen X and after had to wait to 37 and beyond. Anecdotally, around my circles, those who bought younger bought tiny places.

BTW, lots and lots of those in their 40s and up lost their homes in the GFC, too.

Don’t go thinking I’m one of those who bought early and rode the asset appreciation train to wealth. No. I bought later, underbought, and watched the nice houses rally without me. Sucks. But there are no rules….

I agree 100% with you but I also believe that FED works for the asset holders.

Few months back, Powell was saying tighter financial conditions are doing the job of rate hikes.

Now financial conditions are historically loose, would he come out and say opposite ? He won’t say it ever.

We can’t change the system, as it is rigged, but we can make money out of it.

I think the goal is to slowly let the air out of the housing balloon instead of popping it (or letting air out very fast) and causing massive panic.

The desire outcome is for housing prices to drop no more than 15% from the peak price in early 2022, and then hold steady while income grows +3% a year.

AD

I think because of the lag in RE sales stats the double peak makes sense – 3 months after the start of rate hikes was the first peak, and 3 months after the stock echo peak is the second peak. We could expect a third peak due to the recent stock run up except rates are not favorable, but I think think this peak will be a bit lower then the previous.

Amazing to see people still in denial about the coming pain. Facts don’t care about your feels and CRE (among other indicators) is showing us what’s in store.

If it’s true that home prices will not decrease, and that a good third of America will never be able to afford houses or afford rents, then civil unrest is coming.

America is not special, and we’re not immune to the forces of human nature.

I know a senior citizen who now has to rent rooms from strangers to be able to survive. He used to be able to afford his own apartment but at 81 years old no longer can. I’m sure Jerome Powell and all his buddies have a kind message like “f**k him if he can’t take a joke,” or some such.

I’m sure that’s because the Fed confiscated 25% of his savings over the past few years, to pay for $2,000 “checks,” wasteful PPP, and god knows what else.

Sorry if I missed it, but are the magnitudes of these changes of price indices inflation-adjusted? If not, then the inflation-independent fold-changes of valuations must be smaller. Right?

Yes, correct: you totally missed it. So here for the gazillionth time:

THIS IS AN INFLATION GAUGE, of “HOUSE PRICE INFLATION”

As explained in the subtitle:

Because the Case-Shiller Index compares the sales price of a house in the current month to the price of the same house when it sold previously, it tracks how many dollars it takes over time to buy the same house. The house didn’t get twice as big, but it just takes twice as many dollars to buy the same house. In other words, it measures the purchasing power of the dollar with regards to houses. This makes the Case-Shiller Index a good measure of “house-price inflation.”

It’s NUTS to adjust one inflation gauge for another inflation gauge, such as adjusting CPI for PPI, or adjusting “House Price Inflation” for “Consumer Price Inflation.” All that tells you is which is worse./ If the outcome is zero, it doesn’t mean there is no house price inflation. It means that both house price inflation and consumer price inflation have moved in the same direction by the same amount. And so what?

I even compare the rent CPI to the Case-Shiller house price inflation index in one of my classic charts:

SoCal had essentially a double-bottom in the ’09-’12 time frame so I am trying not to read too much into the recent double-top. Meaning that I don’t think a double-top is necessarily a major predictor of anything forthcoming, especially since the SoCal market has been so thinly traded lately.

The number of homes for sale in the coastal SoCal markets I watch are much higher than the past few years (but still well below historical #’s) But the rise in homes on the market is an encouraging sign. Also, more rentals available and listed than the prior few years.

I expect ’24 will end up looking somewhat similar to ’23. I still think we see an ultimate devaluated bottom (nominally) in the ’25-’29 time frame. Yeah I know, way to be precise buddy…

You can look at a place like San Diego for instance and the numbers seem to indicate that population growth/households added from the ’10 census to now did not outpace housing units added over the same time period, so the mantra of a ‘housing shortage’ does not add up so to speak.

If there is a shortage of affordable housing both for sale or for rent, for whatever reason, leading to no available housing for a large working population, is there not a housing shortage?

I agree, in that respect there is a shortage of housing.

But in 2023, the number of homes per capita has been historically highest although homes available for sale/rent are not that high.

Because of cheap money and greed, people/corps have been hording homes for various purposes:: empty, str etc etc.

A lot of people may be happy that their home prices are going and up but I guess they are missing the bigger picture.

A society where most of the people have been locked out of affordable housing is not a healthy society.

Only time would tell I guess.

I think this measure using the same property sales price shift is going to always show more price increase than “real” as most homes get remodeling updates. How is the 75 thousand kitchen redo filtered out? Do they search building permits? Doubt that. I certainly would not bet this approach is as valid as it seems on the surface

No. The index is adjusted for improvements/remodeling, among other things. Please read the methodology:

https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf

What shrinks their future samples and skews current prices is that a large percentage of the SFR’s for sale in San Diego are being bought by developers. This is driving up the index as developers are overbidding on houses, and then those same houses will no longer be used for the index as they become multi unit properties (no longer SFR). Digging deeper into their samples sizes shows that the samples they’re using is already shrinking.

No, you got that wrong. You’re fabricating BS. You’re trying by hook or crook to discredit yourself. And you’re succeeding.

1. there is no “sample” in the Case-Shiller. This is NOT a survey of 1,000 people by phone. Only surveys have “samples.” This is based on a “census” of ALL sales transactions; some sales transactions will be eliminated from the count for various reasons (weren’t arm’s length, were outliers in some other aspects, etc.), and the rest of the sales pairs are in the index.

2. The transactions (closed sales) have plunged in San Diego by something like 50% from 2019, because buyers have gone on strike, and so the sales-pairs count of the CS has shrunk by an equal rate.

You have to make up your mind. You can’t have it both ways. Either you have Socialism with the gubment owning all the mortgages, or you have a market. It’s as simple as that.

Obviously, we don’t have to make up our minds. We have socialism in that the government owns or guarantees the mortgages, and we have markets where we trade MBS backed by these government-owned or guaranteed mortgages 🤣

Exactly. And if the gubment has to do everything it can to keep house prices from falling so their buddies can keep on trading these MBS, it certainly will !

With other people’s money.

Illogical fallacy of false choice.

The usual drek of the ideologue.

Yup, that’s what happens when $9 trillion is printed out of thin air to support the markets. That’s a lot of money sloshing around. Since the advent of QE, we are in uncharted territory. All the historical market indicators are now useless.

The housing market is obviously overpriced, especially given rates, so I thought for a long time that there was going to be a big crash.

I came to realize that there are other paths forward. Housing prices can bounce along relatively even (maybe slightly down) for a long time. Meanwhile inflation chips away at the value of a dollar and after a while, housing prices seem much more reasonable compared to wages.

I don’t think housing is going to drop drastically (i.e. more than 15-20%) unless there is a recession. There is always a recession on the horizon, problem is it might be just around the corner or it might be years into the future. Predicting them are folly.

My advice to young people looking to buy a home would be to save as much as your ever growing wages that you can. Aim for a larger down payment than the minimum. Once you get a decent down payment, find a house that meets your minimum requirements that is the least evil in terms of price. You are not going to get a good deal, get the least worst deal and buy it.

It won’t make you tons of money, you might even lose some over the next few years, but you will have a place to call your own.

JimL-

That’s good advice.

I’d add something about keeping yourself more employable — more “sought after” — than your peers.

Some day, remaining on the payroll will be even more important than today.

If you plot “median” wage between 2000 and now, starting 100 for 2000, you can tell how much “wage” is “catching” up to housing-inflation.

You will realize how bad a hand the younger generation had to deal with.

I don’t understand the difference in the YoY stats between Redfin and Case-Schiller? Redfin has been saying that Portland, OR has been seeing increases of around 3% YoY. I do understand that Case-Schiller uses the sales pair method…but how can we account for such a large increase by Redfin vs the 0.3% of Case-Schiller? I’m assuming that Redfin has the same issue with the YoY stat not having the peak/trough lining up so perhaps this 3% increase means less anyways?

Read the methodology of the CS. The methodology is linked in the article. All you have to do is click on it and read it. I explained some parts, including: the CS is a three-month moving average, and I gave you the three months that were averaged out; and the CS looks at the Portland metro, not the city of Portland, so go to the CS methodology which tells you what’s included in the Portland metro. That’s the place to start.

Thanks for your reply. I guess I should have clarified – I don’t understand how *Redfin* gets their metrics. I do understand more about CS since you explain it well here (and I do read it!). I just don’t understand why they seem so far off from each other despite CS being a 3 month moving average and I suppose Redfin being a specific month?