To “address unexpected and extraordinary inflation increases,” the ECB starts QT by “recalibrating” TLTRO III, which will further reduce its balance sheet.

By Wolf Richter for WOLF STREET.

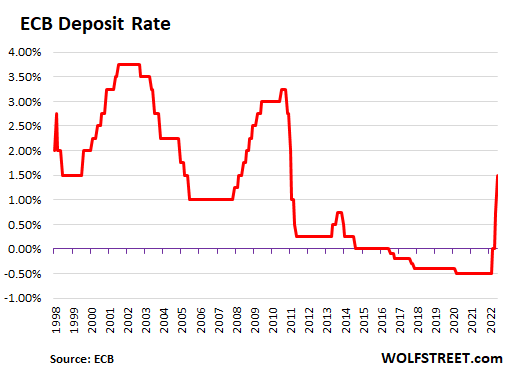

The ECB is now scrambling to not fall further behind the Fed, as the euro got hammered below parity with the dollar and as 10% inflation is tearing up consumers and the economy. It will hike all three policy rates by 75 basis points – its deposit rate to 1.5%; its main refinancing rate to 2.0%; and its marginal lending rate to 2.25% — as “inflation remains far too high and will stay above the target for an extended period,” it said today.

The 75 basis points today come after 75 basis points in September and 50 basis points in July, for a combined 200 basis points in three meetings. The two 75-basis-point hikes were the biggest since 1998. The 200 basis points combined were the steepest three-meeting hikes ever.

It “expects to raise interest rates further, to ensure the timely return of inflation to its 2% medium-term inflation target,” it said. From around 10% now, long way to go, dear.

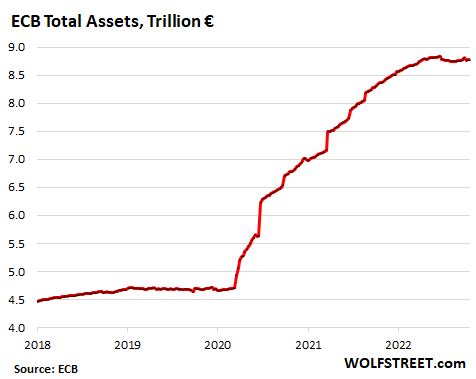

Starts QT with TLTRO III rather than bonds.

To “help address unexpected and extraordinary inflation increases,” the ECB said today that it will “recalibrate” the terms and conditions of its targeted longer-term refinancing operations (TLTRO III) to make these loans more expensive and less attractive for the banks, which will speed up the banks’ exit from those loans.

TLTRO III was a form of QE by lending directly to the banks. At the peak in June 2021, TLTRO III balances amounted to €2.22 trillion on the ECB’s balance sheet.

Effective November 23, the interest rate on those loans will “be indexed to average applicable key ECB interest rates,” the ECB said today. This raises the rates of those loans, making them more expensive and less attractive. The ECB will add three additional “voluntary early repayment dates” to let banks “partly, or fully, repay their respective TLTRO III borrowings before their maturity.”

The ECB reiterated today that its bond holdings under the Asset Purchase Program (APP) and its Pandemic Emergency Purchase Program (PEPP) will remain flat by replacing maturing securities with new securities.

So the loan holdings (TLTRO III) is where QT has started on the ECB’s balance sheet, rather than with its bond holdings (APP and PEPP). The TLTRO III balances have already dropped some. The changes of the terms and conditions announced today will cause those balances to drop further. The Bank of Japan has started QT similarly by reducing its loan holdings rather than its bond holdings.

The drop in the loan balances so far is responsible for the €61 billion decline in total assets from the peak in June 2021. And this form of QT will accelerate after the changes take effect in late November:

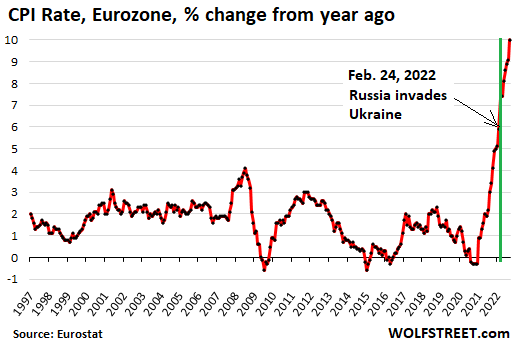

Inflation started surging in March 2021.

As in the US, inflation in the Eurozone began surging in early 2021, nearly a year before the war in Ukraine. In July 2021, it blew past the ECB’s target. In February 2022, it hit 5.9%. For nearly all of this time, the ECB brushed off this raging inflation. And then it went from there to 9.9% in seven months. And now, way too late, the ECB is taking inflation seriously:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf –

Why not hike 200 basis points a couple times initially, then scale back to 75 basis points? I’m not really understanding what that would “break” since inflation is just raging out of control. You need some “shock and awe” to get this thing under control.

Cause it’s smoke and mirrors?

If governments were deadly serious about controlling inflation, this would not be the course of action.

ECB is the dark hole that makes the Fed look bright!

Japan, too!

A true shock-and-awe “surprise” 200 bp hike would destroy a lot of the financial system. It would be like jamming a crowbar into the wheels of a Tour de France rider, or trying to put out a Tesla fire by spraying water on the battery pack.

There are too many derivatives over-calibrated to the current market regime, as we saw with the British “pensions” setting themselves up as over-leveraged hedge funds because “liability driven investing” (as if you could choose your own rate of return!!) … and getting themselves destroyed by even an obviously-foreseeable hike in Gilt rates.

Honestly, destroying that part of the financial system will be good in the long term, but you have to do these sorts of demolitions gradually with a bulldozer rather than a single giant explosion.

> you have to do these sorts of demolitions gradually with a bulldozer rather than a single giant explosion.

Agreed. Regardless of how we got here, outright demolition would destroy all sorts of value and relationships. These are serious things that underpin, for example, your neighbors’ ability to pay their bills next month. If your neighbor is acting foolishly, hitting him in the head with a hammer would not generally lead to better behavior, or shock him into doing things right.

The arrow of time cannot be shoved into reverse. It only goes forward from where we are. This is something “cultural conservatives” think we can do: just abolish a bunch of stuff and somehow a storied past will reconstruct itself.

Yes, principled monetary policy is very much due (and very low-cost to brazenly champion, on paper). That’s not the same as engineering the path for the parts to fit and work, going forward. Admittedly, my faith in Powell’s track record is not great for him as the engineer.

Spraying water on the battery pack is pretty much the only solution for lithium ion battery fire, since water conducts heat away and the only way to extinguish the reaction is by cooling the battery enough, from my limited understanding. Just sayin’

If you’re in charge, what’s scarier? Millions of angry people tweeting about high inflation, or a mob of 15 million unemployed workers showing up at your mansion/palace?

Monetary policy is not science. They tinker, wait, and then months down the line, see what happened. They’re moving cautiously because moving too recklessly at this point could have terrible consequences for their portfolios lol.

Not only would it have terrible consequences for their portfolios, but also the same for their political careers.

my point exactly. :)

Their portfolios and political careers are one in the same…

More of reality (think arab spring):

If you’re in charge, what’s scarier? Millions of angry people rioting and looting because high inflation has them on the brink of starvation, or a mob of unemployed workers tweeting about their unemployment benefits?

The central banks know they have to get inflation under control because inflation at 15, 20, or 30% could mean mass rioting. But they can’t push too hard because the other two outcomes are recession and civil unrest, or (apparently even worse for the ruling class) asset price collapse and a period of sustained currency revaluation. AKA the dreaded “D” word.

Depth Charge,

Why not just shock the markets and the economy into full shutdown and see what happens? I know you’d love that.

Just imagine, turn on the lights one morning in Italy, and they don’t come on because the financial system froze up, payments ended, everything shut down…

Going from 14% to 18% in two meetings is not a big deal — that’s a 28% increase in the rate.

Going from -0.5% to +3.5% in two meetings is something like a 800% increase. That’s just a shock to the system. Once rates are this low, everything is very fragile.

“Why not just shock the markets and the economy into full shutdown and see what happens? I know you’d love that.”

Actually, no, I don’t want to shut down the economy. That’s what these idiots in charge did a few years ago and created damage so bad that many small business owners lost everything.

However, I’m trying to understand what precisely would break if there were a few jumbo-sized rate hikes initially, of that 200 basis point variety. It seems to me that what would break are leveraged speculators, who need to get their clocks cleaned anyway.

If you go back to the financial crisis of 2008, we were sold a bill of goods by bankers and their toady politicians who told us if we didn’t bail out these pigmen bankers, the whole world would collapse. I frankly don’t believe it. We were overbanked to begin with, and all that would have happened is the big banks would have gone bust and their assets would have been transferred to the smaller, more responsible banks who were dealing in rat poison – the derivatives market.

Everything is about fear. They push fear of an economic collapse to justify their theft of everything the middle class and the poor own. Ultimately you get millions of people just like me, who consider everything out of their mouths to be bold-faced lies designed to generate support for “economies of bail” and “too big to fail.” I don’t buy anything they’re selling. It’s all BS. “Subprime is contained.” “Transitory.” They’re frontin.’

*who WEREN’T dealing in rat poison

If you go back to the financial crisis of 2008, we were sold a bill of goods by bankers and their toady politicians who told us if we didn’t bail out these pigmen bankers…

Agree 1000%

It’s amazing that the “end of the world” scenarios always seem to recover/stabilize within six months after huge losses, if not within weeks. Wall streets fear mongering is always empty, and should be summarily ignored.

Depth Charge,

I agree with you.

Motorcycle guy

I agree with your general sentiment. I always felt that the government should intervene to stabilize *markets* but not individual market players. So for example, bail out money market funding, but don’t bail out Goldman Sachs. Goldman Sachs going bankrupt is not the same as ensuring that a certain market doesn’t fail. Of course, that’s not what was done.

And I do agree that doom-and-gloom fears from Wall Street are overblown. Every person in the finance industry is convinced that we can’t have another “Lehman moment” and I always ask: what was so bad from the first one? Using Wolf’s analogy, the lights still worked, even after Lehman’s bust. I’m sure lots of people on Wall St. were sweating it out, but Lehman deserved to die. It (along with Bear Stearns) were the only firms to face consequences for their actions (not enough; their CEOs and a bunch of their traders should be penniless and in jail).

So I agree in spirit, BUT… this is different. A shock-and-awe 2% hike would break *markets*, not just individual players. First the yield curve has to stay normal-ish. Trillion dollar markets of derivatives, interest rate swaps, bond agreements, etc. are built with the expectation of a positive yield curve to maybe a slightly inverted yield curve. Raising overnight rates by 2% would massively spike short rates, while the rest of the yield curve would take months or years to fully digest it. Not only would the yield curve invert, it’s shape wouldn’t be a smooth curve at all. Most likely a lumpy mess with random spikes here and there reflecting more market inefficiencies as trillions of dollars struggle to shift around to the new realities, rather than a relatively smooth curve that “makes sense”. Do that and watch most bond markets freeze.

Similarly, currencies would make massive moves. Already, companies (not to mention world governments) are struggling to deal with the rapid rise of the dollar. Not all companies (even big ones) are fully hedged against currency moves (not to mention those hedges would break against large moves). Now imagine the havoc to currency markets (and ultimately your economy) if central banks started tossing 2% hikes around rather than the already aggressive 0.5-0.75%.

Those are just 2, but the scariest outcome of all is: the one we don’t know about. For example, I doubt many people could have predicted UK pension funds getting slaughtered by leveraged derivatives. A 2% raise in this environment is like putting your whole economy in a box, shaking it vigorously, and seeing what breaks. Maybe some parts stay together. But some parts will undoubtedly break, and you don’t know ahead of time which will be which.

I’ve said it before, but turning around an economy as large as US/EU/Japan is like steering a massive freight ship. You can’t make sudden moves or your cargo will be tossed into the sea and/or your hull will crack. IMHO, I think the Fed is going about as fast as it can go on interest rates, but can go faster on QT (at least initially), because there’s literally trillions of dollars sitting on the sidelines not being used that need to be mopped up before QT starts affecting the real economy. But overall, they haven’t been too bad.

Lune said: “I always felt that the government should intervene to stabilize *markets*”

—————————————-

Why not let the markets and market action stabilize markets?

This is 2022 – nothing is about the Economy anymore, it is all about looking good for the next 2 weeks.

A 2% rise (or the 8+% that is needed) would be a public admission that the ECB has cocked it up for the past 10 months, indeed more accurately for the past 14 years since 2008.

No one nowadays is going to admit to that.

It seems like the CB should have been smart enough to know what the long-term effects of negative rates would be: lots of bonds sold that will deliver GIANT haircuts to the bond holders somehow, someday.

Was this sabotage? Simple can-kicking jack-assery?

I don’t have a lot of direct exposure to duration risk on crappy bonds, and watching inerest rate shenannigans feels like a spectator sport right now (except for the inflation), but something tells me that we are all about to get splattered by that proverbial fan very soon.

dpy

“It seems like the CB should have been smart enough to know what the long-term effects of negative rates would be:”

If they were that smart, they wouldn’t be selected to run the CB, in the first place. It is that simple. They all are political hacks to please their masters who appointed. Same here with FOMC members.

It seems the ECB learned all the wrong lessons from Bank of Japan and from the Fed. The ECB used to be hawkish until the Eurozone threatened to fall apart.

Reply to hot tub ,unlike 2008 now all citizens are on the hook if banks play derivatives and end up losing capital,law passed to let them confiscate your bank accounts. And maybe your brokerage account I don’t know if it’s true ,but at this point it wouldn’t matter .Probably be chaos

Well, how the pieces are picked up after a crash may matter the most. If the payment transaction system is keept going, farming, extraction of natural resources and industry production is keept going, a total colapse of the financial part may not be the end of the world.

If that is possible to do is questionable and the methods needed to do it would be brutal to those with financial power today.

@ Wolf –

Why assume a couple of 2% raises would shut down the economy?

In the US, if something breaks, it will just be asset prices and a hedge fund or two. In the eurozone, the thing that breaks will be a country or six. Italy is first up, followed by a long list of candidates (Portugal, Spain, Greece are the leading ones). Contagion spreads to banks with billions in govt debt on their books. Inflation, on the other hand, helps Italian debt in real terms.

They need to financially fail. They are comatose and terminal due to debt. We’ve been reading about Greece and their insolvency for over a decade. It’s all just kicking the can. Have they done anything meaningful to improve the situation? Of course not. A collapse NEEDS to happen. The longer we wait to allow it, the more damage done to the younger generation. You can’t heal until you treat the sickness.

Let’s be honest. Every single move is designed to try to protect the wealth of the moneyed special interests at the expense of the poor. They keep trying to throw a bone or two to the unwashed masses to tamp down social unrest, but everything’s getting worse. They know it, but they don’t want to stop. The greed is too powerful.

Funny the poor pay no attention to anything we chat about here. They complain about the rich and if they can figure out how to survive they repeat the cycle. Charts, Fed, Interest rates, QE QT ECB REPO 10 yr FFR

Greece bail out in 2012 was all about shifting privately owned Greek bonds worth 10c on the dollar (if that) to the ECB for 100c on the dollar.

Stuff the Greeks with loans you know they cant pay, then shift to public purse when it blows.

Socialising losses.

The Greeks were also to blame, but got done over, courtesy the ECB troika.

BigBird

“In the US, if something breaks, it will just be asset prices and a hedge fund or two”

If something breaks in Treasury’ mkt, it will affect the whole credit mkt, which affects the Equity mkt, unlike any time before. The whole global credit and Equity mkts are affected.

Don’t think for a minute that the US is immune to systemic financial collapse because it isn’t.

That’s a complete myth.

Countries like Greece and Italy have their problems but are more cohesive (for now) than the US, which is a modern Tower of Babel.

You do realize we live in a global economy,if countries start falling no one is safe .Bonds are a worldwide business,every ship sinks

“Why not hike 200 basis points a couple times initially, then scale back to 75 basis points? ”

Because they’re inept. This is the only logical conclusion as it explains both how we got to where we are (Everything Bubble), and where we’ll be going shortly (Everything Bust).

There is no middle ground with imbeciles, only boom and bust.

That last sentence belongs in Ecclesiastes if it’s not already there somewhere. Well said.

I probably would have agreed with you 10 months ago. But I am really seeing the effects of the rate increases first hand now and I don’t think they need to go any faster. Today my company laid off another 39 factory workers and some salaried workers too, but I don’t know how many. And this is just at two facilities, there are several more around the country. And I’m sure this is happening at a bunch of other companies. Be careful what you wish for… that “shock and awe” might bite you the A**.

What does your company make?

Had all rate cuts been undertaken with the same methodical cadence, it might be justifiable. The asymmetry of reductions and increases reveals the bias toward loose irresponsible reckless monetary policy.

Depth Charge,

I agree with you having lived through the Paul Volker years.

10% inflation in the EU? It’s much higher than that – yes, that may be the rate out of Brussels, but not the actual rate at all.

1. this is NOT the EU but the Eurozone (countries that use the euro), which is what the ECB is in charge of

2. You have no idea because the rates vary from country to country and go as high as 24% in Estonia.

Europe has decided on de-industrialization. No one voted for it in the Garden. The sounds of the Jungle are calling like Tarzan. BASF has heard the primal call as is responding.

Wolf’s charts underline the fact that monetary policy changes take a *miminum* of 12 months to show up in the economy.

We won’t know the effects of today’s increases until next year at this time.

why the hel did all major CB (FED, ECB, JAPAN etc) allow all these derivates at all? warren Buffet warned a long time ago,

Best Fred

To Fred: Yes Warren Buffet (and others) warned long ago that derivatives were ‘weapons of mass financial destruction’. Why was nothing done? Because the individuals who ‘play’ in this zone and live off it are the individuals that rule us.

In the Eurozone the ridicule exploded where debts paid interest to debtors while creditors were laminated by the zero interest policy.

Now this economic policy is back under the hammer of reality with runaway inflation.

News just in. Inflation was 11.9% in October in Italy. Not good.

Hi Wolf

I posted a fairly long comment on this thread which loaded OK and it went off to moderation and that was the last I saw of it.

Could you please explain why it was trashed so I don’t make similar future blunders?

Cheers and thanks

Col

Yes, waaaaaaaaaay tooooooooooooooooooooooooo looooooooooooooooooooooog

It was 2,400 words long. That’s about 3-4 times the length my normal articles. And about 10 times as long as the max length of a comment should be. That’s not what comments are for. If you want to publish something that long, you need to do it on your own blog.

My apologies Wolf, and thanks for letting me know what the rules are.

“address unexpected and extraordinary inflation increases”

Claiming this inflation is unexpected is really insulting isn’t it? They can’t be that dumb, so the only conclusion left is they are nothing but shills for the bankers. That makes me root for total chaos and destruction. Regardless of my pain, these clowns will lose a lot more.

For money printers, inflation is by definition “unexpected.”