Inflation spiking, yen getting beaten half to death, yield peg under attack, and Kuroda’s term won’t expire till April. Here’s what the BOJ did.

By Wolf Richter for WOLF STREET:

The Bank of Japan, queen of QE that started the whole circus over 20 years ago and took it to extremes and got away with it, was also the central bank that actually did QT in 2006-2007 and reduced its assets by 36% over an 18-month period – while the Fed’s timid QT in 2017-2019 whittled down its assets by only 16% in 20 months.

And now the BOJ is at it again, and this time, inflation is spiking, including core inflation, and the yen is getting beaten half to death, both of which would require much higher rates and lots of QT to get under control. But the BOJ’s verbiage is copy-and-paste ultra-dovish, and its short-term policy rate is still negative, and it caps the 10-year yield at 0.25%, while the 10-year US Treasury yield is approaching 4%, and the BOJ needs to defend this yield peg with rhetoric, threatening to buy “unlimited” amounts of bonds, and with actual purchases. And yet, the BOJ has undertaken a shock-and-awe balance sheet reduction.

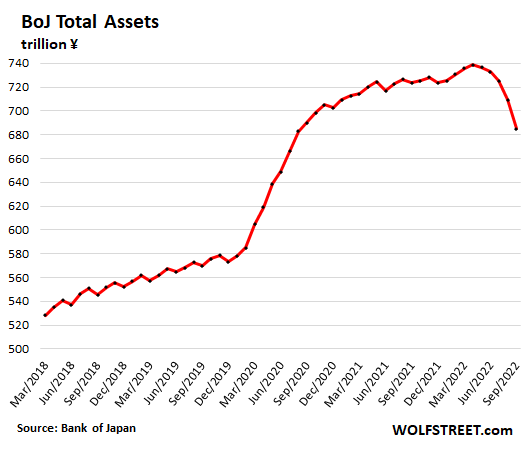

Total assets on the BOJ balance sheet as of September 30, released on October 7, plunged by ¥24 trillion from the prior month, after having plunged by ¥16 trillion in August, by ¥7.4 trillion in July, by ¥3.8 trillion in June, and by ¥2.2 trillion in May. Since peak-balance sheet in April, total assets have plunged by ¥54 trillion, or by 7.3%, or by $371 billion at the current exchange rate. It unwound roughly one-third of the pandemic-era QE:

Total assets on the BOJ’s balance sheet fell to ¥684.9 trillion at the end of September. Over roughly the same period, the Fed’s total assets dropped by just 2.2%, and markets are already having a cow.

I promised myself a while back that I wouldn’t be surprised anymore by what central banks do, that I would be unsurprised by whatever they do, but September was a doozie. If the Fed did this, the whole world would collapse, according to Wall Street, I think.

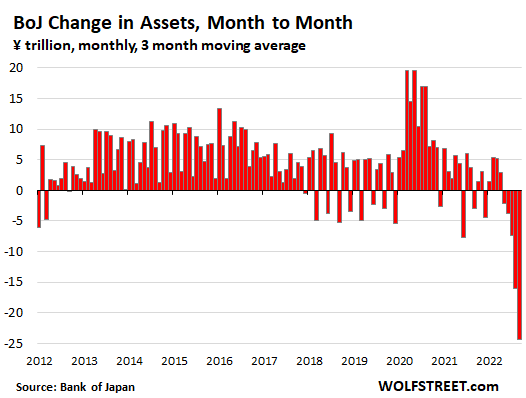

The month-to-month changes of the BOJ’s balance sheet are captured in the chart below, in trillion yen, per month compared to the prior month. The drops every third month in the not-so-heavy QE periods, such as 2018-2019, result from big issues of long-term government bonds maturing and coming off the balance sheet that month and being replaced in another month. This happens every third month but gets overpowered in periods of heavy QE.

The chart starts in 2012, the year before Abenomics, which relied mostly on ridiculous amounts of QE and ridiculous amounts of government deficit spending to stimulate the economy. But now inflation is spiking and the yen is crashing, and the party is over.

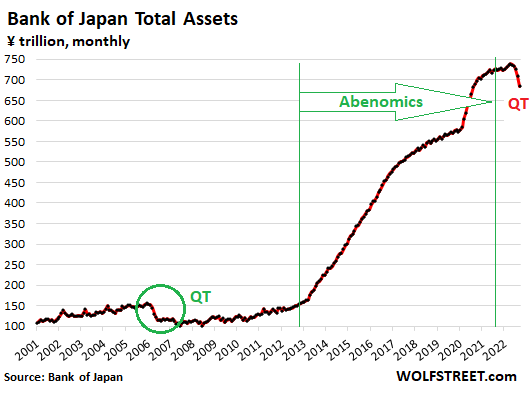

Total assets, long term.

Even on this 22-year chart, spanning the history of modern-day QE, you can see the drop in total assets since peak-balance sheet in April, and you can also see the period of QT from January 2006 through June 2007 (circled in green), during which the BOJ reduced its assets by 36%, unwinding five years of QE. Total assets didn’t get back to the 2005-peak until 8 years later when Abenomics started:

The BOJ has a variety of assets on its balance sheet, including Japanese government securities, loans, gold, corporate paper, corporate bonds, “pecuniary trusts” (stock ETFs and Japan REITs), and other stuff.

The two biggest asset categories are government securities and loans. And the BOJ is using them in different ways.

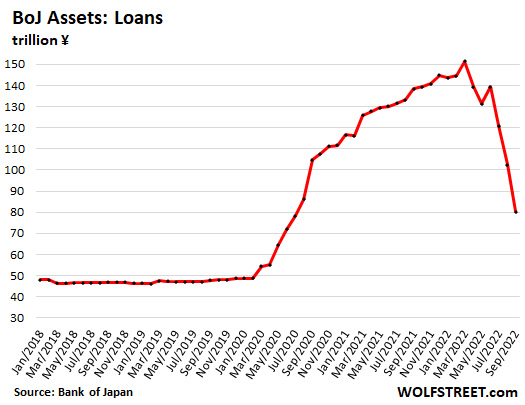

Loans, the primary pandemic stimulus.

During the pandemic, the total amount of loans outstanding under various stimulus programs, more than tripled from ¥48.8 trillion in February 2020 to ¥151.5 trillion in March 2022, having increased by ¥103 trillion in two years.

Rather than creating money and buying government bonds from the banks, the BOJ created money and lent this free money directly to the banks. This is designed as a direct stimulus. The ECB has had even bigger loan programs since the euro debt crisis. Like bonds, loans mature, and if they don’t get rolled over, they are to be paid back.

Since the peak in March, the loan balances have been slashed by ¥71 trillion, or by nearly half, unwinding a majority of the pandemic stimulus:

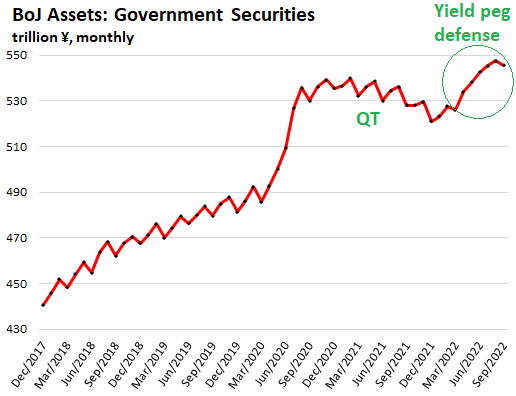

Japanese government securities.

As part of its pandemic stimulus, the BOJ increased its government securities holdings by ¥48 trillion – less than half the increase in loans. And it stopped increasing its holdings in early 2021 and then let its holdings decline by ¥11 trillion over the next 12 months through February 2022. So even while its loan-portion of its QE was still rocking and rolling, the bond portions of its QE had already turned into QT.

But then in early 2022, the Fed started hiking its rates and bandied about the idea of QT, and the ECB started talking about rate hikes, and other central banks had been hiking rates for months, while the BOJ was still clinging to its negative policy rate and to the cap on the 10-year Japanese Government Bond (JGB) yield of 0.25%, even as inflation started to rise.

And investors started dumping JGBs, and the yield was bumping into the yield peg, and the BOJ decided to defend the yield peg, mostly with rhetoric of “unlimited” bond buys that was widely printed in the financial media, but also with actual purchases. Its holdings increased by ¥18 trillion, undoing the ¥11 trillion in QT and adding ¥7 trillion on top. It wasn’t a large amount, but large enough to defend the yield peg:

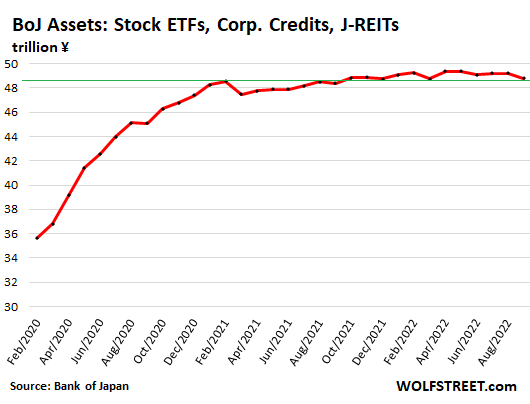

Stock ETFs, corporate bonds, commercial paper, and J-REITs.

Though they got ballyhooed extravagantly in the Western financial media and financial blogosphere, those purchases were relatively small. Total holdings at the end of September of Stock ETFs, corporate bonds, commercial paper, and J-REITs all combined accounted for just 7% of the BOJ’s total assets. The equity funds are valued at market, and fluctuate with market movements. The equity ETF portion, at ¥36.9 trillion on September 30, accounts for the majority. During the pandemic stimulus phase, the BOJ added to these holdings, but stopped in early 2021, and they have remained roughly flat:

So now, inflation is spiking in Japan and the yen is getting killed. Unwinding a portion of the balance sheet in this manner likely removed some fuel from inflation and maybe kept the yen from plunging further. But what the BOJ really needs to do, in addition to QT, is raise its policy interest rates by a bunch to not be left further behind by the Fed and even by the ECB, and it needs to remove the peg on the 10-year JGB yield and let the yield float higher.

And that will likely happen, but not before BOJ governor Haruhiko Kuroda – who was one of the architects of Abenomics – rides off into the sunset when his term expires next April. And that’s a long time to try to keep things together.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I am not sure I would describe 7.3% from a peak exactly shock and Awe. Wake me when we get. to 50%+.

Stephen,

You’re clueless about what QT does. Look at the markets in the US, and the Fed just did 2% QT.

Stephen,

And no, I won’t wake you up. You’re better off sleeping through what is happening in the markets due to this little-bitty QT.

Agree, Wolf. Just can’t help some people I guess.

I on the other hand sold out a third of my puts today (got my initial investment out). Rolled the rest into June. And even picked up couple of Jan ’24 calls in Verizon and Intel. Tesla of course is going to 50 (dollars then yen). Need to wake up my friend Kunal soon.

Andy- I’ve been eyeing Verizon, as well as AT&T as possible buys, but their 150+ billion in debt they both hold on their balance sheets (especially in this rising interest rate environment) makes me nervous.

Staunton, some due diligence on these 2 companies for you.

AT&T current leadership has shown they are slightly more prudent than the idiots that overpaid for DirectTV, but they will be paying for that mistake for a long time. They have finally embraced expansion of their fiber network and retirement of the old copper U-Verse crap, and they have talked about how users who switch to their fiber internet do not churn away. They have made smart investments in their mobile network as well. If they can successfully deleverage with their current goals, they should be safe.

Verizon is led by an idiot who does not understand the business. Their wireless network is falling apart and is vastly behind T-Mobile and AT&T in the US now (they are living off their past reputation of being the best, now their towers are not dense enough because they won’t spend the money improving like T-Mobile did), so they rely on gimmicks like giving away Disney+ and trying to lock people in for 36 months with device payments/loans.

I’m expecting both Verizon and AT&T to later cut their dividends substantially.

Debt coverage ratio isn’t a problem now but that’s because earnings and cash flow haven’t been hit yet. It’s coming though.

AT&T has a better balance sheet and the dividend payout ratio is a lot lower, but with a P/E ratio of about 6, market participants seem to be anticipating that earnings are about to fall through the floor. That’s my read anyway, though I have not tracked this stock consistently.

Otherwise, the dividend yield wouldn’t be 7.23%.

My wife has a couple of hundred shares of VZ and T in her small IRA that have been in there for over a decade. Might this be a good time to unload them?

Thanks for staying on topic, Andy, et’al🙄

It seems like the “steady state” of developed country economies is that they must have central bank intervention (or fiscal deficits) to grow. I would love to see a chart of central bank balances, plus global fiscal deficits in aggregate.

Is this maybe saying that without central bank intervention over this many years, developed country economies would have been catatonic?

My theory is that developed countries have outsourced most of their production to third world countries and as a result have so hollowed out the economies that they require massive deficit spending and monetary stimulus for “growth”.

So the question becomes, how long can the central banks tighten before it all collapses? It feels like this is fungible across countries, so bond repurchases in Japan, ECB, US effect not only their economy, but other countries as well. After all, money can go where it is treated best.

Another aspect is rentier activity. The level of rentier taxation of the economy would have made it grind to a halt long time ago without central bank intervention. Still it have only been kicking the can down the road.

At some time the amount of rentier taxation must go down or the economy will grind to a halt.

When the working population is shrinking, the economy isn’t SUPPOSED to grow. The economy should be shrinking. Fake growth can’t possibly work very long, as most countries are finally admitting.

Unfortunately, that “growth” in the US is happening in consumption, not production. This won’t end well.

Well, Wolf, there is how fast/deeply QT may affect

1) financial markets (as quickly as picking up a phone or typing on a keyboard or saying, “Alexa, sell my absurdly overvalued stocks”

Versus

2) real asset allocations/investments, which take a lot longer to gin up or unwind.

Funny, the 2pct draw didn’t really correspond in market downdraft vs all the accumulation did on the way up. So overdone is the market reaction.

Not “overdone.” It’s not symmetrical. The Everything Bubble was the biggest bubble ever. The only thing that kept it going was a MASSIVE AMOUNT OF QE and 0%. It already deflated in late 2021 (Nasdaq peaked in Nov 2021) when the Fed started TAPERING QE. Even just LESS QE brought the market down. S&P 500 peaked on Jan 3, not even halfway into the taper. By the time QE had ended in early April, the S&P 500 was down a bunch. And continued to tank with just NO QE!! That’s what you need to realize: Just NO QE is tanking these hyper-inflated bubbles.

So now we have the beginning of QT.

Go up by escalator, go down by elevator.

Wolf,

re “Look at the markets in the US, and the Fed just did 2% QT.”

you are wrong about that. It was the interest rate hikes/ expectations that smashed the market, not trivial amounts of QT.

Recent Fed internal research concluded that $2T of QT only has the effect of the Fed raising rates only ~.25%, and at the $60B/mo QT rate it will take the Fed well over 2 years to even do that, and inflation is monetary, so until they drain the $2-4T they dumped into the mid/low end of the consumer economy, inflation will not go down to the prior population growth rate. all that support the thesis of many years of pain to come; however, if the Fed lets stagflation continue for years it may get entrenched in psychology, esp. wage gains, and Fed will lose credibility if that goes on for over 1 year, which cuts against your thesis. Making me think the Fed will get a Volker moment in early/mid 2023 if CPI is not at least trending fast towards back below EFFR.

That “Fed research” was a whitewash. QE was enormously powerful in inflating markets. Tapering QE already sank the markets — it started in November. The end of QE in a hyper-inflated market is the end of the Bull Market. You don’t even need QT to deflate these markets, just ending QE. Rates didn’t seriously start until the market had already tanked.

The collapse is baked in. All that remains is to decide who will pay the bigger price.

Wolf is right: the wallstreet yells “Bloody Murder” for nothing.

The Fed can clearly do faster balance sheet reductions, including MBS that it has been holding like “MY PRECIOUS”, and BoJ can clearly start raising rates faster.

In essence, both of these banks have not been able to control inflation. So both of them suck! The housing remain unprofitable, the working class is screwed and productive businesses remain non profitable due to artificial pricing of the market.

Correction: housing remain unprofitable => housing remain unaffordable

it’s difficult to make a profit on something that is unaffordable.

and i mean by unaffordable: something you, personally, can’t afford.

As far as Shock-&-Awe – Wolf, you are the bomb! Wow!

Does Haruhiko Kuroda understand what is going on? How can he be this intransigent?

Not only is he intransigent, he is also totally tone-deaf. He told the Japanese people, when they were getting restless about the rising prices, that their tolerance for higher prices was rising. That didn’t go over well with them at all.

Wow! I understand the idea behind central bank independence, but it’s difficult to justify if central bankers are more clueless than your average politician.

Along those lines, this is one of my favorite, related quotes:

BOJ officials used to be cautious about purchasing ETFs, worried that it could distort market activities and put the central bank’s own financial health at risk. But under pressure from politicians following the global financial crisis, the bank changed its stance in late 2010.

“We led the cows to water, but they didn’t drink it, even though we told them it tasted good,” Miyako Suda, who was a board member then, wrote in a 2014 book discussing monetary easing at that time. “So we thought we should drink it ourselves, showing them it was tasty.”

Somebody should have told this central planning elitist about Narcissus.

I thing our friend did a TTMYGH where he profiled Kuroda; pronounced Corroder, as in one who corrodes…

D’ow! Need an edit function. Our friend Grant Williams…

Abenomics is like a dead man walking, yet they keep trying.

Probably too soon to phrase it that way.

The BOJ is still buying government bonds to support yield curve control (0% yield on 10 year JGBs). This is likely to continue exerting downward pressure on the Yen, regardless of any sell down of other assets on the BOJ’s balance sheet.

With their massive debt load, the BoJ cannot let their average yields move above 0% by any meaningful amount. Maybe up to 1% for less than 12 months at most. Otherwise, the interest on debt will explode, pushing the BoJ towards insolvency in terms of public confidence.

a central bank “cannot” is a patently incorrect statement.

You don’t seem to know that the BOJ holds over half of Japan’s public debt, and it remits its interest income back to the government (just like the Fed does). In other words, that debt that the BOJ holds will never cost the government anything because it’s getting its interest back. So on that portion of the debt, it doesn’t matter what the interest rate is.

In addition, if interest rates go up, they only impact the small portion of NEW debt that the government issues. The existing debt is not impacted by rising interest rate until it matures and is replaced with NEW debt at higher rates.

But, the BoJ can lose copious amounts of money just like the Fed can. Granted, it’s all moot, since neither can actually go bankrupt.

Wolf,

Kinda get what you are saying *but* what is the weighted Ave maturity of the Japanese G’s debt?

In the US, it is much shorter than a lot of people think (approx 10 years if recollection serves) – that means 10% of a ginormous debt load has to be rolled over *every year* at a much higher interest rate (if rates are allowed to rise much).

Japan has a G debt load of like 250% of GDP.

If their weighted Ave maturity is about 10 yrs too, that means that debt equiv to *25% of GDP* would get repriced higher every yr that QT goes on.

Saying the Apocalypse is two months from now isn’t really better than saying it is next week (substitute 5-10 years and 1 yr to use actual numbers).

Am I missing something from your analysis?

I get your point about ruin coming slower…but considering that US deficit financing has essentially gone on for 52 years straight and that ZIRP pretty much failed for 20…I don’t think giving the US (or Japanese) G an extra 5 yrs is going to save anybody.

These are institutions that have been failing economically for *decades* (that is exactly how the astronomical debts got piled up in the first place).

Cas127,

A government that controls its own currency can never default on debt in its own currency. It just prints more to get out of trouble.

Where they get in trouble is with inflation. And you cannot print yourself out of inflation. If inflation takes off when government debt is large, there are two options:

1. the central bank can hike rates including via QT

2. the government can raise taxes by a bunch.

Both will eventually drain demand and tamp down on inflation. The latter, as a side benefit it might lower the deficit.

But one thing is clear, when inflation sets in, the Free Lunch is over. Now it’s time to pay for it, either with loss of purchasing power or with taxation. The other option? Hiking interest rates. So take your pick (none of them are any good).

Maybe I understand a bit what’s happening in the US, but Japan? I don’t even try.

1) SPX monthly : September 2022 and Sept 2020 almost had a fight, but were separated, at least for now.

2) The first sign of troubles was in May 2022. May long “buying tail” breached Jan 2021 high.

3) June 2022 closed below Jan 2021 high, after breaching the low.

4) Oct is still hanging in the open space between Sept 2020 high and Jan 2021 low, above last month close. Oct might stay green, closing below June 2022 close.

5) Sept 2020 high was not touched. SPX might move higher, before

it happen…

685,000,000,000,000 yen.

I know Japan is not Zimbabwe. (Yet) But still ….

Japan is an industrial powerhouse, unified culture, and educated workforce.

If it is lucky, Zimbabwe would revert to a hunter-gatherer society if it weren’t for outside influence.

Kevin W,

It’s like counting the Fed’s balance sheet in a fraction of pennies, such as 2/3 of a penny. It then becomes a very large and hard-to-deal-with number as well.

1 yen = 0.7 pennies

Multiply by 0.007 and it’s about $4.8T. We’re at around $31T.

1. If you have something to say, just say it. Don’t twaddle.

2. As the Japanese population is shrinking, all the properties will be inherited by smaller number of people

3. A sort of pyramid scheme but in reverse, less people will own more. Less work buys more of Japanese properties.

4. Japan do not have a strong military, which reduces their spending. If they build a stronger military, that will take even more money from economy.

‘“2. As the Japanese population is shrinking, all the properties will be inherited by smaller number of people

3. A sort of pyramid scheme but in reverse, less people will own more. Less work buys more of Japanese properties.”

Using this logic, people living in Detroit are the richest people in the world.

Obviously, my comment was not in reference to you (that other guy).

Somehow you got in front of the legend.

Japan is a country closed to immigration or wild child birth.

Detroit or similar towns are in a bigger country of USA.

Then, Detroit has a culture different from Japan.

Another false analogy.

Japan probably needs to experience a deflationary depression to “reset” their financial system and economy.

They don’t need mass immigration to continue on the perpetual treadmill of fake debt fueled “growth”. I can’t speak to the causes of their declining birthrate but if living costs were cheaper, then maybe this would at least partly reverse.

Detroit is a dysfunctional third world basket case.

There is no comparison whatsoever.

They also have a culture that prioritizes order. Even if they experience a depression, it’ll be like the 1930s depression when our culture was still more or less unified. People will be suffering, but you won’t have tons of violent crime.

Look at the summer of 2020 if you want to see what we’ll experience when the asset mania falls apart and our standard of living is no longer affordable.

Look to Jan 6th to see what happens when privileged runes don’t get what they are promised.

When I was in Detroit on business I would drive on those roads that were like spokes in a wheel: Woodward, Michigan Avenue, Grand River, Groesbeck, etc.

Highly recommend the book Detroit City Is The Place To Be: The Afterlife Of An American Metropolis by Mark Binelli. What it was and how it came to be what it is.

They have razed a good chunk of the properties in Detroit, so the government’s response is to take more away rather than give more to everyone. Isn’t government grand?

Does Japan have a strong navy?

Image result for Japanese navy

Japan’s Maritime Self-Defense Force (MSDF), as it is officially known, is one of the world’s most powerful navies. Its fleet is larger than those of traditional European powers like France and the United Kingdom combined.Dec 4, 2020

Most people in Japan that inherit property immediately sell it. Why? Well, because of “inheritance tax”, which tops out at 55%, the world’s highest.

Here’s what happens in Tokyo (from my observations high in the sky). A big post-war house, obviously owned by very old people, gets inherited by the already old kids (yes, Japan may be shrinking in terms of population, but that’s a relatively recent phenomenon, they also had a huge postwar baby boom, and most people born from the 50s to the 1980s here usually have one or more siblings to split things up.)

They immediately sell the house (which is worthless, and immediately torn down: it’s the land, not the house, that’s so valuable.) The kids get a 30 Million plus 6 Million yen per successor tax-free allowance (so about $250K if you’re an only child). After that, you pay a progressive tax on the rest. Say the house is worth 1 million USD: That only child will still reach the 30% tax bracket for about half of what they’ve inherited even after the tax-free allowance, so if they have to divide this up amongst other siblings like most people here do, they will probably NOT be able to afford outright a new house in Tokyo with what’s left.

Usually, the land/house is sold to a company, usually a developer. That developer either: A) divides the plot into tiny multiple plots for tiny multiple new houses, all at about half a million dollars each or more, 2) make tiny, one-room, one-person 1DK apartments to rent to young single workers to hide in alone, or 3) convert it into a parking lot (really popular strategy right now in residential areas). All of these routes help to keep property prices sky high, while making it even harder to start a family and have kids here!

PS, Starting from October 1st, more than 15,000 food products were price-hiked, the cost increase was on average 15%, while inflation is also working its magic in many other areas. And wage hikes are almost unheard of here, so if fact, people are working more for far, far less. Just like the rest of the world!

I’ve always been fascinated not only by Japan’s growth exponentially in many areas of engineering expertise but their economic mess in the last century as well.

How had they done this QE so massively? Was it indirect influence of the outer investment?

People have a lot to learn about how Japan “works” and how it is different from the USA and many other countries.

One of the biggest changes in Japan in recent times is the huge increase in inheritance taxes.

This has impacted real estate in a big way as there is one loophole that allows people inheriting real estate to avoid all the taxes and expenses on it.

This is especially so when the house and land is basically worthless or worth so little that it would never find a buyer.

This is common with rural properties or small plots of land with a derelict house on a piece of land that is not suitable for redevelopment in big cities.

Estimates are that around 19% of all Japanese housing is currently vacant with lots of those type properties even in the big cities such as Tokyo.

Japanese law still allows a person to reject the inheritance of anything in the will. If the people/person doesn’t want the item, they can reject it and the “ownership” remains with the dead person’s estate…..in effect it is owned by a dead person. As it is “owned” by a dead person it can not be “bought” by another entity either.

Some of these properties are seized by the Japanese tax authorities and sold at auction which has the effect of wiping out the tax due to the government.

*The law is supposed to be changed to eliminate this loophole, but I don’t know the status.

As the owner is dead no taxes are paid and maintenance is not done and the property falls into greater disrepair.

And this is not limited to just houses. You can find a lot of condos for sale in ski resort areas for sale for under $US1000 or even less. “Owners” of these properties have not paid the monthly fees on these properties for years and the owners association has taken possession of the property.

If you buy it you are stuck with paying the accumulated unpaid fees which is often more than the value of the property!!!!

Japanese real estate outside of the big cities it cheap compared to the rest of the world. And even cheaper now in US$ terms as a result of the fall in the value of the yen.

You can buy an ocean view 700 square foot condo near the ocean in a decent resort town for around US$50,000…………..

@Cobalt Programmer

“4. Japan do not have a strong military, which reduces their spending. If they build a stronger military, that will take even more money from economy.”

Compared to the US, the Japanese military is not so strong. Compared to the rest of the world, they are very strong. Specifically their Navy is strong.

As a JSDF Army Renger qualified Captain once told me, the Japanese Army is more like a “boy scout” outfit playing with dangerous toys.

They may have great weapons and lots of training, but they lack the actual experience of fighting a war.

Training and “war games” are just that.

Actual experience is required.

I’ve written Cobol but never cobalt. You’ll have to explain to me what that language is.

Scott and Cobalt Programmer,

Hahaha, Scott, you missed all that fun here in the comments some time ago.

Cobalt Programmer, tell Scott why you picked your name.

I think there would be considerable domestic distress if BoJ put interest rates up. Probably Tokyo is different, but from what I see, although the land is becoming cheaper when Japanese couples settle down, they usually tear down the existing property and build a new one. This seems a bit weird but honestly you see them being taken down and a new one put up all over the place.

The construction costs of a new house are very high and the couples take on a lot of debt, so although the land is truly getting cheaper they kind of miss the benefit of it unless they want to head out farming (absurdly cheap).

Personally I think in the near term, the reaction to inflation will simply be to consume less and there won’t be any wage reaction as desired.

The house of my in-laws will be torn down too after they pass away. It was built in the early 1970s with a 30-year design lifespan. It’s now 50 years old, and it’s beyond hope. These houses weren’t built to last and be remodeled and updated. My understanding is that new houses are built better to last longer.

“unless they want to head out farming (absurdly cheap).”

It is cheap because many of the local nokyo and governments restrict who can buy farmland.

If you don’t have a farming license you can not buy farmland in many places. That restricts who can buy the land and makes it cheap.

And don’t even think about buying farmland and trying to change the designation to housing if you are an individual. In 99.9999999999% of the cases you can’t.

You want to make a good long term investment in Japanese land look at land that could be used for harvesting timber…………A plot of land that already has a bunch of middle aged timber on it. Lots of cheap land like that all over Japan and very few restrictions on it.

So should I be selling my yen and convert it back to Euro now or wait until this crisis is over?

At some point in the not too distant future, you might want to buy some yen, but not with euros, but with USD.

Agreed. Around April 2023 maybe.

I’m trying to think of a poor man’s carry trade, doable through a discount US brokerage. Hmm, some play between Japanese and US bond ETFs?

I guess the nickels yielded are too small, for a poor man’s carry trade. Something more geared is needed.

1) Japan yield curve : the front end is underwater up to 4Y, the 40Y

is 1.5%. Japan is behind the curve, slow to adjust. Kuroda don’t dare doing it, but he does.

2) The strong dx deflated BOJ assets. Gravity with US and BOJ asset sales

will lift the long duration, before raising the front end above water.

3) NIKK backbone #1 sent the market higher to BB #2, before rising

to 30,715 in Feb 2021. The NIKK made around trip to BB #1 in Oct 2022.

BB #1 : Nov 17/20 2020, 26K/25.4K. // BB#2 : Jan 14/18 2022

4) Raising rate is good for small businesses that innovate, bad for the Japan’s Giants. Small businesses might move to the abandoned flyover, applying WFH

5) Japan houses are paper thin with a short life expectancy, to protect from earthquakes.

6) If SPX will rise to a new all time high, the NIKK will test 1989 high.

7) Japan was behind the curve for centuries, a until a British trader established a post nearby. During the Gilded Age recessions GB built the Japanese navy. After defeating Russia Stalin was afraid that Japan will

occupy Siberia for the second time. Japan became so powerful it dominated China Korea and the pacific.

Maybe this century, the stress test moves in an opposite direction, from China (capturing trade and technology, not land and materials as Japan did with Manchukuo) and the Koreas (trade in the case of South Korea, nuclear blackmail with North Korea) as turning winds toward Japan. Japan has tech (and culture) for an aging world.

Tony Blair imposed sanctions on Zimbabwe after confiscating white

farmers, Dec 2003.

Tony did not confiscating white farmers. LOL

The pushback on Powell has started. We shall see how big his cojones are. Will he allow Wall Street to fall 50%? I doubt it.

Japan- time to pay the check for the Abenomics dinner.

Yen falls 50 % from 90-140 vs USD with > 10% reduction in balance sheet.

As sales of Govt securities begin in size, yields will rise and BOJ losses and Japan economy spiral out of control.

Game over Japan.

Time to book a cheap holiday there, for the spring cherry blossoms.

If the BOJ owns 50% of all 10 year JGB’s and people are short these bonds, what happens when they are unable to deliver the bonds as a result of some unforeseen event promulgated by government or central bank action?

Japan is doing some really great things in pockets, but their overall montary policy strikes me as confused. Kudos for the 7.3% QT though. I’d like to see that level resolve in the US, despite whining from Wallstreet.

Wolf, I think I’m missing something obvious. How is it possible for the BoJ to be both ultra dovish (rates, YCC) and hawkish (QT) simultaneously? How are they defending the yield cap but running down the balance sheet? Surely these two are in opposition to one another?

Read the article. It explains it.

Does this mean that the “widowmaker” trade will be sparing its proponents, or are they still going to be getting killed?

Indeed….the BOJ started all this central banking “magic” of ZIRP and NIRP, and as I recall, Krugman was one of the advisors to the BOJ .

The daisy chain arrangement of governments and central banks is coming to a screeching halt. The BOJ “canary in the coal mine” is wobbling on its perch….and this might be a case of “first in first out” …

the hubris of the BOJ to say they will defend the ten year at .25% is the last stand. It would be expected that a “fabian retreat” is in order and they will announce they will allow it to slide to .50%. A domino tumbles in the central banking “forest”, will anyone hear it?

Let’s talk Turkey! How are they even still solvent?

Wolf-incredible read…What happens to Japanese equities going forward?

Buy as they are the cheapest, best quality companies in the world with good balances sheets except for the banks.