They learned a lesson from the mess in 2019, which Powell referred to several times.

By Wolf Richter for WOLF STREET.

One of the two big topics at the press conference today, following the FOMC’s meeting and policy announcement, was when and how to slow the pace of QT. So far, QT has removed $1.43 trillion from the Fed’s balance sheet, and it continues on autopilot until the Fed changes its pace.

There have already been discussions about it at the prior meeting in January as we saw in the minutes of that meeting (The Fed Wants to Drive QT as Far as Possible Without Blowing Stuff Up, and it’s Working on a Plan.) And more detailed speeches by Dallas Fed president Lorie Logan and Fed governor Christopher Waller have expanded on those points (Fed Discusses Balance Sheet “Normalization”: ON RRPs & MBS Go to Zero, Reserves Drop a Lot, Slower QT Reduces Risk of “Accidents,” SRF Calms Repo Market). And today, the Big Kahuna himself got to talk to reporters about it.

When will slowing QT start? “Fairly soon.” Powell was asked what “fairly soon” means, and he said, “’Fairly soon’ is words we use to mean fairly soon.”

What about MBS? “Our longer-run goal is to return to a balance sheet that is mostly Treasuries,” Powell said. This parallels repeated commentary by others, including Waller – to the effect that they want to rid the balance sheet of MBS, for a variety of reasons.

After ON RRPs go to zero, QT shifts to reserves. “We broadly think once the overnight repos stabilize at zero or close to zero, after that, as the balance sheet shrinks, we should expect reserves to decline pretty close to dollar for dollar with that,” he said.

Why slow QT, part 1? To avoid blowing something up, an experience the Fed went through at the end of QT-1 in 2019 when the tightness of bank reserves caused the repo market to blow out, which forced the Fed to step back in with massive repo operations and unwind a big part of that QT-1. Powell made reference to that episode several times:

“Liquidity is not distributed evenly in the system. There can be times when, in the aggregate, reserves are ample or even abundant, but not in every part. Those parts where they’re not ample, there can be stress. That can cause you to prematurely start the [printing] press. Something like that happened in 2019 perhaps.”

And: “We don’t want to find ourselves in a situation where … we buy assets and put reserves back in the banking system the way we did in 2019.”

And: “We had some indicators the last time [QT-1 2019]. This is our second time in doing this. We’re going to be paying a lot of attention to things that started to happen, at the end of the [QT-1] cycle where we ended up in a short-reserve situation. We have a better sense of what the indicators are. It wasn’t so much in the banking system as it was, for example, where federal funds is trading relative to the administered rates.”

Why Slow QT, part 2? “It’s sort of ironic that by going slower, you can get farther,” Powell said. “The idea is that with a smoother transition, you’ll run much less risk of the kind of liquidity problems which can grow into shocks and cause you to drop the process prematurely.”

In other words, a slower QT will allow the balance sheet to decline to lower levels, the top theme that Logan and Waller hammered on as well.

“We may actually be able to get to a lower level because we would avoid the kind of frictions that can happen,” Powell said.

When will QT end? When reserves are barely ample — now they’re abundant. Powell: “Right now, we would characterize reserves as abundant. We’re aiming for ample which is a little lower than abundant. There’s not a dollar amount or percent of GDP where we think we have a pretty clear understanding. We’re going to be looking at what’s happening in money markets in particular – a bunch of different indicators, including the ones I mentioned, to tell us when we’re getting close.”

What comes after QT ends? Continued shrinking of reserves, but slowly. Once “you reach a point ultimately where you stop allowing the balance sheet to run off, then there’s another period in which non-reserve liabilities grow organically, such as currency in circulation, and that also shrinks the reserves at a slow pace,” Powell said.

So, in the future after QT ends, there is a phase when the balance sheet remains flat, but as currency in circulation, which is demand based, continues to grow as it always does, it shifts liabilities from reserves to currency in circulation, and reserves continue to shrink, which is a mild form of QT.

The Fed’s balance sheet has nearly always grown from day one, driven by currency in circulation (the paper dollars people stuff under mattresses), which now amounts to $2.34 trillion. Before QE, currency in circulation was the primary driver of the growth of Fed’s balance sheet.

So Powell said: “You have another time where you effectively hold the balance sheet constant and allow non-reserve liabilities to grow, and that brings it in to a nice, easy landing at a level which is above what we think the lowest possible ample number would be.”

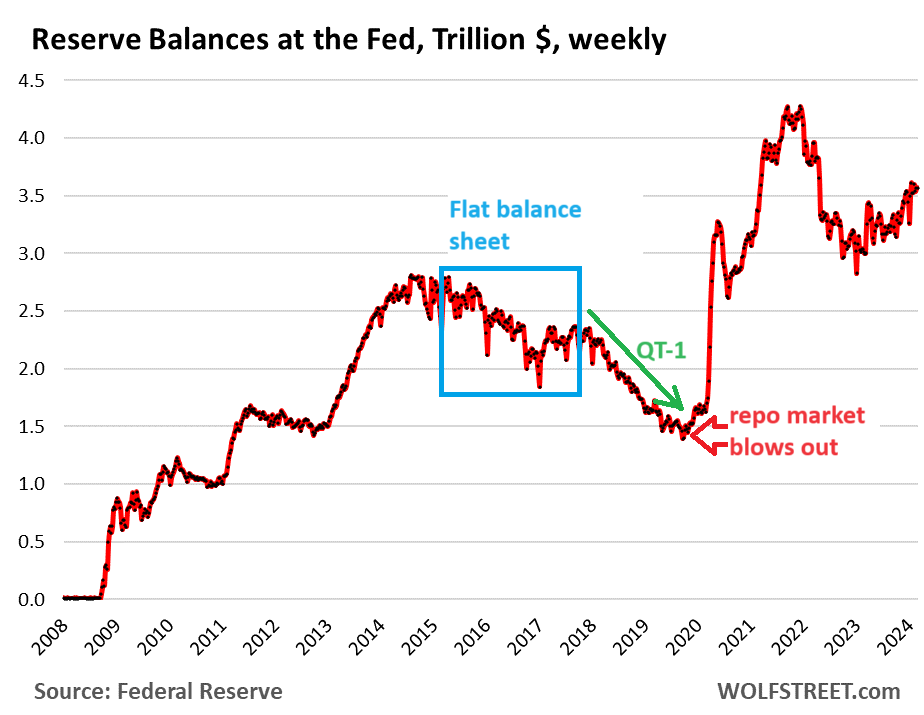

The Fed followed this flat-balance-sheet strategy in 2015 through 2017, after QE had ended, and during those three years, reserves dropped by over $400 billion (blue box), before QT-1 (green arrow) drove reserves down further. When the repo market blew out in the fall of 2019, the Fed plowed liquidity back into the financial system via massive repo operations, as a result of which reserves jumped by $260 billion (red arrow).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Russians have a saying “The quieter you go, the further you’ll get”.

FED shouldn’t explain what and why (especially when it comes to Powell – markets hear what they want to hear anyway). Volcker did exactly that and it worked out good in a long run.

Your russian quote is silly. Please stop.

Is there something “not true” about it?

Perhaps he’d prefer something more familiar regarding rabbits and turtles.

Outwest hates Russia and is afraid of the Russians.

He was educated in the US where they told him Russians were bad people and he believes them.

I’ll charge a buck for that:)

Guess I won’t be reading any more comments on this article.

Nissanfan :

Your Russian comment is excellent. Please continue

@Outwest your remark is hilarious!

To compound your discomfort, I’d like to emphasize that adjectives denoting people or things from a specific country or region should be capitalized. Henceforth, kindly refer to it as the ‘Russian quote’.

“The higher up you go (government) the crookeder it gets.” – Michael Corleone.

Yes… A fictional Mafia don is the best source of insight on the subject.

…as long as we’re quoting fictional characters:

“…wherever you go, there you are…”

-buckaroo banzai

may we all find a better day.

Volcker never tried monetarism. In his book “Keeping at it”

“Pg. 105: “We needed a new approach. To have more direct impact, we could strictly limit growth in the reserves that commercial bans held at the Federal Reserve against their deposits. That would effectively curb growth in deposits and the overall money supply. Put simply, we would control the quantity of money (the money supply) rather than the price of money (interest rates). “

First of all, the price of money is the reciprocal of the price level, not the level of interest rates.

Most of all, with the intro of the DIDMCA, total legal reserves increased at a 17% annual rate of change, & M1 exploded at a 20% annual rate (until 1980 year’s-end). Back then the money multiplier was operable.

Paul Volcker had courage, integrity, grit and the support of President Reagan.

Excellent summary from “Keeping at it”.

Thanks.

Al Capone said “You can get much farther with a smile and a gun, than with just a gun alone.”

Actually, you got it backwards – “further than with a *smile* alone.”

And I don’t know if Capone really said it…but it sounded good in the movie.

“And I don’t know if Capone really said it”

according to the internet, neither does anyone else. It’s probably original to a 1950’s comedian.

Wolf,

Many thanks.

FOMC still whistling past the graveyard. No mention or concern about inflation getting its second wind? Dot plot looks as ridiculous as ever.

Powell talked a lot about inflation rising again. I just didn’t discuss it because it’s old hat. I wanted to focus on QT. There was some discussion about that in the comments of the prior article. I included a quote of one of the things he said about it:

Here is one of the things he said about rising inflation:

“If you look at the incoming inflation data that we’ve had for January and February, I think very broadly that suggests that we were right to wait until we’re more confident. I did not hear anyone dismissing it as not information. So I think generally speaking it does go in the direction of saying yes, it is appropriate for us being careful as we approach this question.”

Seriously, Powell and company talk like “The hippy days” for those old enough to remember. I believe the reply to such circular babbling was: “You must be high.”

That applies to the reporters, not Powell. He should have tasered them.

Deflation in asset prices is a 5 alarm fire to be met with trillions in money-printing at the drop of a hat, but massive inflation is something to “be careful” of and take a wait and see approach about.

Depth Charge has it right.

Somehow using ZIRP to goose the stock mkt to idiot overvaluations for years and years (and years) ain’t a problem…but dropping a 90 PE to a 45 PE (when 15 was a pre-orgy norm) via unZIRP is (clutching pearls) “breaking things”.

The Fed wants it paint huffing delusion economy without OD’ing…but reality gets the final vote.

All the Fed has really done for 20 years is make the ultimate ruin more certain by introducing the disruption of delusion.

Far out, man!

So Mr Richter we have the longest consecutive days streak of all time with the 2 year yield and the 10 year yield being inverted. Is this just going to be the new normal? Even when the Fed increases its own inflation and GDP forecasts long term yields never seem to gain enough traction for the yield curve to uninvert. Is the old inverted yield curve means a recession is coming antiquated? This time its different in perpetuity?

What is different this time is that we’re not allowing banks to fail as part of the natural process. We keep running in with more bailouts – BTFP, slower QT, soon more rate cuts any day now even though inflation is still running hot.

There was a brief yield curve inversion in 2019 that precipitated the 2020 recession. All the carnage in March 2020 wasn’t just bc of the pandemic and shutdowns, there was a concurrent financial crisis that was literally papered over with massive stimulus.

Right now we’re in one of the deepest and longest running yield curve inversions that suggests something much worse could be up ahead for the banks, IMHO.

Since QE started in 2008, the yield curve has become meaningless as predictor of a business cycle recession. It also falsely signaled a business cycle recession in 2018 (we eventually got a pandemic and lockdowns in March 2020, but that’s not what the yield curve is supposed to predict a year in advance, LOL)

The reason is that the Fed’s huge bond holdings since QE began have mucked up the market for long-term yields (repressed them).

The yield curve could uninvert because short rates get cut enough and long rates stay higher; or it could uninvert because long rates rise above current short rates, and we got pretty close to that in Oct 2023, before rate cut mania set in.

He also said though that inflation tends to be higher in the first half of the year than the second half, which sounds like they think it’s just a “bump in the road”, but they just want to wait a little longer to make double sure that is what it is.

I’m skeptical though. This doesn’t feel like a bump in the road to me.

Having said that, I do see some things that could cause it to be just that:

Word on the street is the labor market has slowed quite dramatically and employers are hiring at lower wages, if they hire at all.

As a result of this as well as the recently increased prices seeming to be the straw that broke the camel’s back, people are starting to cut back.

Lastly, it seems housing prices are starting to come back down a little (or at least topping out), so those numbers might start showing up in the inflation stats.

Maybe you missed it.

Powell clearly said that the recent inflation readings may be seasonal.

I don’t know what to make of it. Another word for transitory?!! 😉

Srinivas Bingi,

He was asked about the seasonal issue at least twice and responded kind of in the same way. Here is what Powell actually said:

“As I mentioned, you can look at January and many people did see the possibility of seasonal adjustment problems there. You’ve got to be careful about dismissing the parts of the data that you don’t like.

“February wasn’t as high, but it was higher. The question is: What are we going to see? We tend to see a little bit stronger — this is in the data — a little bit stronger inflation earlier in the year, and less strong later in the year.

“We’re going to let the data show. I don’t think we really know if this is a bump on the road or something more. We will have to find out.

“In the meantime, the economy is strong. the Labor market is strong. Inflation has come way down and that gives us the ability to approach this question carefully and feel more confident that inflation is moving down sustainably to 2% before we take that step to begin dialing back our restrictive policy.

The only reason housing prices are coming down is because they are building smaller homes.

They’re also squeezing their profit margins. So you can tell that there is more going on than just building smaller homes.

For the first time, I was impressed with Powell. Yesterday he faced a full court press of cries for rate cuts, with the pressure coming from more than just the usual suspects.

Sure, CNBC and WSJ were pimping for cuts like they usually do. But so were all the talking heads on Bloomberg. I thought Mohamed El-Erian was gonna start crying and Diane Swonk was gonna start growing hair. Jonathan Ferro was the only one who maintained an even keel.

I can only imagine the pressure Powell is getting from the Biden camp. They don’t get that he’s helping them, because cuts now would fuel further inflation,

Wise to remember Powell is not the decision maker. He is a spokesperson for the decision makers.

One thing to contemplate at this latter stage in the demise of America 1.0 is that political pimp-ery (rate cut) so often fails (as a result of the cumulative historical pimp-ery) that politically it isn’t the *results* that matter (because they will fail/be bad) but the political deception profits that can be earned from the mere doomed “promise”.

So, for politicians, knowing their “promises” to be mere doomed lies…there is absolutely zero reason to make them early (creating more time for their failure to be apparent).

Much better for an “October Surprise” where the delusions induced by the political promises/lies are at a peak, and the actual results are at a minimum.

So why have Powell talk rate cuts now…when he can gibber about them in September/October?

I read an article this morning that I found disturbing. I found myself agreeing with it. Part-way through, I realized it was written by Larry Kudlow, which was the disturbing part.

But in this article, he said that Larry Summers “has reconstructed the old CPI from the ’70s and ’80s that included personal borrowing costs, such as mortgage, auto and credit card loans,” which were apparently deleted from the index in the 90s. After adding them back in, Summers “came up with an 18% inflation peak back in April 2002 and a 7% inflation rate as recently as November 2023.” I’m wondering how close to real this is.

The current monetary policy sweeps big problems under the rug. The Fed focuses too much on CPI and not enough on other issues including home price inflation, the rising cost of funding a decent retirement (i.e., via lower expected investment returns), and the rising cost of servicing excessive government debt. These are long-term employment, growth, and inflation issues well within the Fed’s mandate, if the blinders are taken off. The mandate doesn’t say the Fed should sacrifice long-term growth and employment to avoid recessions and grow bubbles. Yet, this is what the Fed did with monetary injections and excess liquidity.

It works for speculators and hamsters on a hamster wheel, who don’t understand the concept of “tomorrow”, but it does a disservice to people who plan for the future and expect reasonable rewards for hard work.

The Fed has a long way to go before it regains credibility. Talk of reducing interest rates, slowing QT, and gradually transitioning from excessive liquidity to ample liquidity isn’t what’s needed.

MJB,

This Summers stuff is BS. Economists say a lot of stupid stuff all the time, but now it fits in your narrative, and so suddenly he’d some kind of Jesus??

If you add mortgage rates into CPI, then you would have had mega DEFLATION from 2008-2018 and then again from 2020-2022.

Yes, mortgage rates were part of housing CPI before 1983. But thank god they removed them because we would have had DEFLATION, which would have caused the Fed to go to negative interest rates and even bigger QE, which would have inflated home prices even more.

These economists are idiots sometimes.

Also life has changed. Lots of products and services that we have today that are in the CPI basket didn’t even exist back then. So CPI has to be adjusted to modern times. People who claim that the old method was better don’t have a brain. They need to look at how people today spend their money and how that differs from what they bought 40 years ago.

Summers is responsible for a lot of stupid shit, including helping repeal Glass-Stegall.

Here is a fun-to-read piece on Summers from 2013 when he was trying out for the Fed chairman.

https://www.thenation.com/article/archive/return-lawrence-summers-mr-spectacular-failure/

This is how the article starts, to give you a flair:

“Tell me it’s a sick joke: Former US Treasury Secretary Lawrence Summers, the guy who tops the list of those responsible for sabotaging the world’s economy, is lobbying to be the next chairman of the Federal Reserve. But no, it makes perfect sense, since Summers has long succeeded spectacularly by failing.

“Why should his miserable record in the Clinton and Obama administrations hold him back from future disastrous adventures at our expense? With Ben Bernanke set to step down in January, and Obama still in deep denial over the pain and damage his former top economic adviser Summers brought to tens of millions of Americans, this darling of Wall Street has yet another shot to savage the economy.”

Just my 2 cents. If you look at energy, there has been very little inflation to the consumer when compared to almost everything else the past 10 years.

Why is that? Maybe

1) Fracking has allow more oil to be produced. But at the beginning of the Fracking bubble, lots of money was spent and companies went bankrupt wiping out lots and lots of debt. If that debt was still an overhang an on balance sheets of oil producers, Oil prices would need to be higher.

2) Green energy. We do not know the real cost yet. Governments globally are subsidizing anything related to green energy. Probably at least 30%. (just a guess) Tax breaks and incentives for the whole green energy product flow. R&D, Manufacturing, Infrastructure, Public and Private company Utility producers, Business and Consumer installations (roof tops, charging stations), Consumer houses and vehicles. This has led to governments taking on a lot of debt to fund green energy but eventually, they will need to reduce or stop subsidies.

3) Also, there are still subsidies for oil too.

If governments at any point decide they have to reduce energy subsidies, get ready for a big jump in overall inflation.

It maybe years before this happens. Maybe they never will reduce subsidies?

Its hard to trust any inflation/price/job numbers coming from the BLS any more. In the very short term, you never know whether the difference between this month and last month is going to get revised away next month or doubled. In the long term, you have all these problems with changing the measurement rules that make the numbers now not comparable to the numbers in 1980. Maybe in the medium term you can use them in a relative way – you can see whether the numbers are higher or lower than last year.

So when people assert that there’s probably more inflation going on now than the numbers admit to, I have to agree, but I don’t think anyone knows how much. Lots of estimates, all over the place.

If the inflation numbers are getting artificially lowered over time, then keeping the fed’s target constant at 2% doesn’t make sense, they should be increasing it slowly over time.

Wolf hates this take, under the claim that our economy is wildly different than it was then. He’s right that it’s different, but not on the ingredients to the calculus no longer being valid.

The old metrics from the 80s are arguably a better measure for regular Americans. Back then, CPI was a measure of prices necessary to maintain a constant standard of living. The basket of goods waa fixed, and allowed for far less manipulation. That manipulation now, applied to real goods (like a vehicle) produces a bogus result. Like a $10,000 car in the 90s would now be worth a few hundred dollars. This is really about a decoupling of interest rates from inflation, which used to be chained together. Consumers now, however do not have the ability to earn higher interest rates to compensate for inflation (which is the governments entire goal to moving the goalposts). that’s why interest rates never approached the 8%+ (more like 16%) inflation we were experiencing. their hands are tied because of the National debt. If lawfully executed, the Fed would have to destroy the Fed’s credit to do their job controlling inflation. It was easier to just change the rules than get honest about our situation. They’d also crush us under massively higher entitlement program costs, as theyre chained to inflation math as well.

This was all politically motivated, not economically, and there are dozens and dozens of quotes showing this was the politicians, not economists who wanted this change.

It’s just not convenient to the career ruling class as they go to great ends to keep the entitlement farce afloat, and therefore, their cushy jobs making 5X the average American, while “working” a measly 146 days per year.

Howdy HR01. The Dot Plot for me makes the most sense. The projection has been followed pretty much. Showing ZIRP dead for a few years is a very good thing.

Sounds like it will take some time to get there. Higher for longer. Fuel energy will be higher this summer. More of the same. Nothing changes if nothing changes. Thanks Wolf.

people have to change ride a bicycle to the store skip a meal a day .buy less nonsense.Always remember for the people . Politicians forgot where they came from ,but I think there about to be awakened. There seems to be something in the wind

You equate skipping a “meal a day” with buying “less nonsense”?!

I think they are obviously talking about different ways of saving money, not equating them. Why are you trying to start a fight?

Just trying to understand the comment. Most people don’t equate purchasing food with discretionary spending. If he meant stop eating out or skip the Starbucks, that makes total sense.

Howdy Fleas. Thought exactly what you typed for most of my working years. That something in the wind is just more of the same. Stay out of debt, live within your means. Financial Freedom brings more Freedom.

Fleas,

I get your generic point but also sounds a lot like personal responsibility will solve everything, similar to arguments that if I simply drive a little less or don’t use a plastic straw I can save our planet. It ignores all the important class distinctions that exist among other factors as the whole purpose is misdirection and lies. Exxon, for example, proved in 1977 that burning off excess fossil fuels created climate change. The executives consciously ignored it and decided to market their way out of it.

My point is of course broader than climate change but on how what our society broadly believe is a consciously and well crafted fiction. I have no doubt Powell is a product of that but also pertuates it but also truly believes it.

“Exxon, for example, proved in 1977 that burning off excess fossil fuels created climate change.”

What are you referring to specifically?

What did Exxon do in 1977?

What it is ain’t exactly clear. Gradually then suddenly. What would a bread riot look like in 2025?

Just a matter of time before the US 10 Year blows out ? …gold seems to be sniffing the higher inflation

Howdy The original Marco. 4 week T Bills ready . check Watch Bonds to double digits???? check. Leisure suit ready for party time??? check…..Boogie Down and Keep on Trucking????? check check check……

Maybe it would have been cool if, I dunno, they had learned not to f*ck with QE.

Howdy Gattopardo. They love bubbles and picking winners and losers. Watch the Lone Wolf articles about New Home Sales. Bubba predicts that is the new bubble.

Wolf, You got the seminal parts of the Fed speech reproduced here! Very helpful, Thanks!

Powell mentions he’s watching the right indicators for when QT will be nearly finished, specifically he mentions (1) “what’s happening in money markets in particular “, (2) Repo market stability (obvious, from 2019), and (3) “where federal funds is trading relative to the administered rates”.

I don’t know what (3) means (what are administered rates?) but i guess he means looking for rates blowing up due to tightness. And He’s watching repos, as we all are by now educated from 2019, and for (1) i think he’s watching flows into money markets to slow?

Administered rates are those that the Fed actually sets. The Fed has four of them, and they’re part of the rate setting decision (prior article):

Interest it pays the banks on reserves: 5.4%.

Interest it pays on overnight Reverse Repos (RRPs): 5.3%.

Interest it charges on overnight Repos: 5.5%.

Primary credit rate: 5.5% (banks’ costs to borrow at the “Discount Window”).

Is it fair to understand Powell’s comment, then, as watching for whether federal funds (lending of excess reserves from some Fed member banks to those without sufficient overnight reserves) starts to trade in volume and at rates near/breaking the top of the federal funds range, so that the Fed has very little excess reserves at the (say) 5.4%, indicating systemic reserves have become a bit scarce? Or at least, indicators that it’s starting to move in that direction?

Thank you. This is fascinating stuff: Powell’s admission of “indicator-led” signal of QT having run its course, as opposed to percent of GDP or nominal dollar amount, (which Bill Dudley seemed to be working off of in the 10/18/2023 Bloomberg article!).

Having read your points in the threads above, the biggest insight is what you said: the BIGGEST indicator of greater than required reserves (terms from “excess” to …”abundant” to “ample”..etc …lol..) is…… Treasury Yield curve inversion !

It has been more than 30bps for the last 4-5 years non stop! As you mentioned QE is a direct player in that. So add that to the list above of “indicators”. The best one yet!

I think if inversion hits 10bps….powell will throw in the towel into the ring. ding ding!

What Powell said has zero to do with the yield curve inversion. The rates they’re watching are essentially overnight rates and how they relate to each other. There is zero about longer-term rates in it. You’re making up stuff.

Wolf, what’s your honest opinion – do you think the Fed can pull this off without major problems?

The big kahuna has a plan? wait until the fat lady has her way with him.

There is and will be nothing normal going forward, buzzards and black swans will have their due, but please play along.

I’m sitting on the edge of my chair every day. Withdrawing liquidity at this rate poses some risks, stuff that no one is thinking about suddenly malfunctions. And suddenly it blows up. And that would be the end of QT. But they did learn a lesson from 2019, and I think they’re trying to be smart about it. So we’ll see.

I thought you’ve said previously that the 9/2019 event was caused bu the Fed having ended its Standing Reverse Repo facility after the 2008 crash?

If so and they’ve now re-implemented it, then why is there SO much concern for another blow out?

IMHO, I think this means, in part, the Fed doesn’t see a recession anytime soon. This means it’s okay to slow the pace of QT, because everyone knows the next recession will likely push the Fed’s balance sheet back WELL ABOVE 9$, reversing balance sheet reductions from QT2.

“I thought you’ve said previously that the 9/2019 event was caused bu the Fed having ended its Standing Reverse Repo facility after the 2008 crash?”

What I said was that the SRF would have been ready on day one to deal with the problem, and the problem probably wouldn’t have spiraled out of control and turn into a repo market panic. Instead, the Fed let it fester because it had no ready facility to deal with it, and when it got big and ugly, the Fed re-cobbled together its repo intervention system for the first time since 2008. But that late in the game, the intervention had to be much bigger. Just the existence of the SRF prevents a repo market panic because all participants know it’s there.

The need for the SRF when doing QT and afterwards is one of the lessons they learned in 2019, and in July 2021, before they even started talking about QT, the re-implemented the SRF in preparation.

For those of us not in this water park for very long, the term “blowing up” refers to a sudden severe loss of liquidity by many (and large) commercial banks? Thanks.

No, it refers to non-bank players such as those in the $5 trillion repo market. A mortgage REIT — they’re all highly leveraged — that invests in long-term mortgages and MBS and funds those assets in the repo market short-term can run into trouble if the repo market tightens up. And it cascades from there.

If a bank runs out of liquidity, it can borrow from the Fed, no problem, either at the Discount Window or at the Standing Repo Facility (SRF).

Thanks Wolf, for being frank. You know infinitely more about this stuff than I do, and considerably more about it than anyone else I follow. I have real concerns, as well.

One thing he learned, if the president wants lower interest rates (and its an election year) you better give it to him. (or the presumptive president) The subtext to all this is that JP is hamstrung by Treasury policy (bond pumping) and pumping stocks helps take some pressure off that gambit. Stock Vigilantes? One of the reporters posed the question, you call it ‘hippy’? Be careful markets had a brief fling in 2019, but they were rolling over before Covid. The long game here is controlled deflation, which they think they can pull off, as long as there is plenty of liquidity, no one notices there is actually less money in the system. Meanwhile if during the lifetime of that bond which you own, the spending power of that dollar increases you don’t really care much about the interest. Well maybe if stock values are indexed to the inflation value of the dollar you care. If the dollar falters, the Fed will have to do something.

*disinflation

The asset bubble is giddy. I do not see any way around the “blow up”.

AllTheRooms.com reported massive declines in airbnb revenues in much of the country, especially in “get out of the city” locations, where airbnb listings are multiples of the properties currently listed for sale. I was surprised how many of these airbnb tycoons used DSCR loans (a subprime loan) based upon the cash flow from the property alone.

He who takes the smallest loss, the fastest, will save the most skin. If your sales price is matching recent closings, you will never get out, you need to be below it.

Many Florida condos are due for a huge HOA assessment to prevent another building collapse. Insurance rates and taxes are skyrocketing. Builders and trades are still bidding “take it or leave it, I have plenty of work” pricing.

Just add this to the Commercial Real Estate debacle and I am wondering where is the good news? Well, you could always buy Chipotle Mexican Grill, a burrito maker selling at 7.8 times sales and a price to earnings of 64. Get in ahead of the 50 to 1 stock split (currently $2900).

You just had an Otis Redding song pop into my head! Not a bad future at all!

Watching my money wash away, sitting by the bay.

Otis at age 26 paid his final debt…

For the last 6 months, I’ve had a sneaking suspicion that something horrible is going to happen. Glad I’m not alone.

The FED thinks they’re a financial and economic God at this point, and that even the hint of a recession is too much to bear and cause for tinkering. F*** these people.

Adding liquidity at the rate they did is what broke shit. C’mon, Wolf.

I sure wish they would learn the lesson from 2009, 2010, 2011, 2012, 2013, 2014, 2015, 2016, 2017, 2018, 2019, and especially 2020, 2021, 2022, 2023, and 2024: Never, ever do QE again.

OK Wolf so that’s your job. To be the only one thinking about it. Why don’t you tell us? What is going to blow up?

I don’t expect anything to blow up. This stuff comes out of the blue. But there is a chance. A lot of people on Wall Street want something to blow up so that it would force the Fed to stop QT.

Howdy Djreef. Asking The Lone Wolf this question was a great choice. Ask some small business owners the same question. Not as many of US around anymore but the answers should reassure you about the future too…….

Having said this dot plot thing is weird. I still can’t find out how the final decision is made. A vote and majority rules ? Does Powell decide?

Divided Govt is one thing…a divided central bank?

They vote is on the rate today (they voted to not change the rates). The dot plot is a projection of the future, and there is no vote. Each member submits their estimates, and they get tabulated. And that’s it.

Understand that the dot plot is a free for all with no vote.

But they voted not to change rate.

Was it by majority rules as in Supreme Court or does Powell’s vote carry more weight, as in CEO of a biz board?

With their expectations of future via dot- plot all over the place it seems likely that a point will arrive where there is dissention about a change in the rate.

I just don’t think it’s the Fed’s job to prevent things from “blowing up.” an occasional “blow up” is part of a capitalistic society.

They failed at preventing things from blowing up.

Prices have blown up in an obscene manner.

Don’t you get it? The FED tampering with the monetary base is what causes things to blow up.

Not “capitalism.”

The Fed tampering too much with the monetary base causes greater volatility when things blow up; when things blow up with greater volatility it causes the Fed to tamper too much with the monetary base.

Scarcity of resource most commonly causes things to blow up. Today, even inherently worthless Bitcoin is scarce. It will blow up.

Yes, and the Fed no longer allows that to happen it’s become so corrupt. The entire country is a disaster.

You would be wrong. That is the ENTIRE POINT of their existence. If we wanted to have things occasionally blowing up then we could return to the boom-and-bust cycles of the 1800’s. Only this time without the opportunity to “head West” and start over.

LOL. The Fed has created more boom and bust in the past 30 years than the free market Wild West days ever did.

I think your giving the FED too much credit. The US government feels left out with that comment. Because they will say hey, Government debt was only 7 trillion thirty years ago. Give us some credit for spending and extra 27 trillion via deficit spending.

@ru82

“Give us some credit for spending…”

To quote Walter White: “We? Who’s ‘we’?”

I’ve been sitting here the whole time saying WTF

ru82, chicken and egg. Would Congress have spent as much if the Fed wasn’t repressing interest rates for the past 30 years?

Would be nice to see a more stability even within our system. Rent, healthcare, education, and even necessary price controls on essentials would help. Unlikely to see that here as the tendency is to create large programs that fundamentally redirect vast tax payer money back into profit based industries that I would argue should be fundamental rights in any society.

I agree with the latter part of your statement. The first part seemed like a plea for a soviet style form of government that undermines the whole project we in the US, have been tasked with.

By several generations of heroic parents that made the present possible.

I suspect that it is ravages of a hemorrhaging inflation caused by the monetarist policies that were put in place to insure the aristocratic wealth would not be affected by their bad bets in which they lost it all.

Just listened to Powell’s press conference. I got the sense that the Fed is still being data dependent. So the first two months of inflation data are not sufficient to prove that inflation is going back up. But if the incoming CPI continues to be hot, the Fed will have to adjust their outlook and rate cut plan. If we get a high CPI for March and April, there could be one or no cut in the next dot-plot and if CPI continues to be hot in the summer, then all bets are off. That could be a black swan event for Wall Street. I hate this market with a passion, but can’t seem to find any fault with Powell’s press conference today.

So the Fed’s “mandate” is to maximize employment and keep prices stable. And the balance sheet: “..that brings it in to a nice, easy landing” (Powell). Easy, aka, soft.

Regarding price stability, the S & P 500 is at the Shiller CAPE measure of 34.9. Historically the level in 1929 reached 31. In November of 1999, it reached its highest level of 44. In October, 2021, it was 38.6, the second highest level. And now, it’s nearly 35 which is the third highest level in more than 100 years. And the generally accepted level of a balanced market is around 15.

I’m reminded of the concluding crescendo in the Beatles’ song, “A day in the life”.

“…can’t seem to find any fault with Powell’s press conference today.”

I’m no powell hater, but I do wish he’d drop the language about “likely being at the peak of the tightening cycle” or however he words it. Maybe even add in some language like “future rate hikes may become necessary if inflation persists above our target” or something to that effect.

The whole point of the pressers (as powell himself said) is to transmit the Fed’s policies to the market – but the market is refusing to listen.

Completely agree. The second sentence you quoted is really the key to break the market delusion. That they won’t hesitate to raise rates if inflation stays at a high level. That should be included in the opening FOMC statement. The Fed still projects an impression that they are afraid of upsetting the market even though Powell’s conference yesterday felt neutral.

I’m don’t agree with the Fed’s assumption that liquidity can be in the wrong places.

Any market participant that has a need for cash can generate it quickly by redeploying cash flow, cutting expenses, selling assets, or selling equity. A company that can’t generate cash when needed is insolvent, mismanaged, or their business model depends on easy money, which isn’t sustainable. Mismanagement, over-leveraging, and overvalued assets are NOT liquidity issues that the Fed should be focusing on. It is not the Fed’s job to keep foolhardy speculators in business.

According to the Fed, the repo crisis was caused largely by a $120 billion reduction in bank reserves over a few days as people withdrew money to pay taxes. That seems like a very small amount. Wasn’t that “crisis” more about some big banks refusing to support the inter-bank lending system, in order to claim the system needs more liquidity?

In this time of super inflated asset prices and rampant speculation, claims of tight liquidity should be heavily scrutinized.

The 2019 repo crisis was due to disintermediation.

What caused the repo crisis was that banks stopped lending to the repo market, in part because they had other things to do with their cash. The other part that caused the repo crisis was that some hedge funds, mortgage REITs etc were heavily relying on borrowing short-term in the repo market to fund long-term positions, so they were forced borrowers, and they couldn’t back off when repo rates started rising.

Money market funds are also big lenders to the repo market. If you look at your money market fund’s assets, you will see that a big portion are repos, maybe even bigger than T-bills. I’m not sure why money market funds didn’t step in to lend more to the repo market – ease off on T-bills and make more by lending to the repo market.

This made me think at the time that there was also a crisis of confidence at play, a fear maybe that some big mortgage REITs were going to collapse, and that made lenders to the repo market skittish. There was a problem with mortgage REITs at the time.

About $4-5 trillion are on average borrowed and lent in the repo market, so this is a big thing.

“The other part that caused the repo crisis was that some hedge funds, mortgage REITs etc were heavily relying on borrowing short-term in the repo market to fund long-term positions, so they were forced borrowers, and they couldn’t back off when repo rates started rising.”

Exactly my point. Why is it the Fed’s concern when non-bank speculators get themselves in hot water trying to borrow short and lend long? Is that a liquidity issue, or a mismanagement issue?

In times of crisis, let the bad managers sell their assets or sell equity to generate needed liquidity. The Fed shouldn’t print it for them or slow QT. If it comes to it, let them declare Chapter 11 so there is no asset fire sale that disrupts markets. Long-term assets including treasury securities held by a bankrupt hedge fund (or bank) can be re-allocated in a bankruptcy reorganization or liquidation without creating a fire sale.

It’s time to cull the herd, for benefit of the herd.

A recession would be an indicator the Fed is doing its job correctly.

@Bobber

“Why is it the Fed’s concern when non-bank speculators get themselves in hot water trying to borrow short and lend long? Is that a liquidity issue, or a mismanagement issue?”

Compared to the USA economy of the past, sometimes it appears that not much is going on but hyper-financialization. They act like it’s all they’ve got.

The welfare of the DFIs is codependent upon the welfare of the NBFIs.

Funds flowing back to the DFIs reduces the supply of loan funds.

“The 1966 “credit crunch” is the paradigm. Sidney Homer and Henry Kaufman, economists at Salomon Brothers in the 1960’s, coined the term “crunch” to describe how the 1966 episode differed from those in the 1950’s. Although Homer and Kaufman did not formally define a crunch, Homer (1966) offered the following explanation:

The words squeeze or pinch have gentle connotations. The prehensile male sometimes “squeezes” or “pinches”, with the most affectionate intentions. No bruises need result, no pain need be inflicted. A “crunch” is different. It is painful by definition, and it can even break bones.”

See: “Identifying Credit Crunches” by Raymond E. Owens and Stacey L. Schreft. Federal Reserve Bank of Richmond, March 1993.

You’re misunderstanding equity and value with liquidity. When a company cannot access the cash and liquidity it has prudently manages because the banking system is broken, that is an issue. It generated the cash, it cannot access it. That is a liquidity crisis.

I don’t think he misunderstands. I think what he’s saying, if I’m reading it correctly, is that there are a lot of zombie companies that need ZIRP to survive. People see their liquidity issues and claim that they’re representative of liquidity issues as a whole.

Well said. The market, apparently with the Fed’s support, is trying to sell us extreme/ample “liquidity” as an elixir for rotten financial management. The real cure is recession.

When so many things have reached extremes, we can’t normalize with slight corrections. Asset prices, inflation, wealth concentration, fiscal profligacy, government debt levels, societal discontent, etc. are all at extremes.

With too much prancing and pussyfooting, the problems will become more severe and cause unpredictable extreme crisis down the road.

Sometimes I think the Fed knows this, and they are like the battlefield medic giving lethal doses of morphene to the mortally injured soldier.

That is complete BS. Especially considering the way companies have been allowed to generate cash by placing financial BETS (i.e. gambling). Look at the 2008/2009 FRAUD (call it what it really was).

Gambling is NOT investing. MBS were financial products that were technically ILLEGAL (the banks and financial firms have since lobbied CONgress and changed the law). Not only were MBS a slicing an illegal slicing and dicing of deeds, but then the very same players who knew the housing market was in a bubble still intentionally sold these “products” to everyone!!! At the same time placing more bets AGAINST the very same products they were selling!!!!

Remind us a$$hat, WHO WENT TO PRISON? WHO WENT BANKRUPT?

In a truly functioning market, which REQUIRES consistent RULE OF LAW, what you say might be true. THAT IS NOT WERE WE ARE.

Hedge accordingly.

Point being, companies that make BAD decisions and behave BADLY must be allowed to FAIL.

ZIRP prevents this, and it isn’t rocket science. Are any of us really surprised by all the bad behavior (at all levels of society)? We shouldn’t be, as the system has been rewarding bad behavior for 50+ years. Some might argue, even longer.

C,

I think it is the market that misunderstands. The market and the Fed seem to think liquidity should be something like oil that lubricates the gears in endless supply. That’s not the way it should work. Liquidity has become a euphemism for huge money supply, easy money, and repressed interest rates.

Liquidity needs to be somewhat scarce to enforce discipline in markets and create consequence for foolhardy speculation. Scarce liquidity promotes savings, low inflation, and sustainable asset prices based on interest rates set by conditions in the market, all of which facilitates sustainable investment and growth.

There is a balance to be struck with liquidity, but the Fed and markets seem to think ample liquidity is always the answer. It’s not. It’s the way to make the economy inefficient and uninvestable.

The best way to manage liquidity is to keep it consistent at a tight-enough level so interest rates and asset prices remain at reasonable levels. Consistent liquidity promotes a consistent economy, where people can manage their affairs, plan, and invest for future, without worrying about future decade long bouts of interest rate repression, or inflation that runs at 4x target.

When liquidity injections are used as a scapegoat to resolve structural issues, like bad investments, or over-investment, or financial bubbles, it prevents the market pricing mechanism from resolving issues. It promotes huge financial bubbles that inevitably pop.

The Fed understands this. They want to slowly migrate from extreme liquidity to ample liquidity so the asset price bubble does not pop. In my view, that should be the least of their worries. I think they should be more worried about long-term growth, an imbalanced work-reward relationship, extreme wealth concentration, and society’s perception (or understanding) that the economic system is rigged for benefit of asset holders.

So basically you are suggesting that after The Fed enabled the greatest financial fraud, greatest destruction of price discovery, greatest circumvention of rule-of-law in functioning markets, and greatest transfer of real wealth to the 1% and political class, they suddenly “found Jesus” and are trying to undo that?

LMFAO!!!!

Until bad management is allowed to fail (go bankrupt and become truly destitute to pay back creditors) and bad behavior is actually punished with prison time, we will continue to get more bad behavior.

The Fed has violated it’s charter, it needs to be ended and assets need to be seized. Including those of every board of governors since Greenspan.

The great thing about the time we live in is that all of these behaviors/decisions and wealth transfers are well documents so guillotines can be deployed with much greater, and more effective precision. So there’s that I guess.

This. Very well said. Wolf, I don’t know how anyone, at this point, can still think the Fed isn’t acting solely to protect the asset bubble, first and foremost.

Einhal,

“I don’t know how anyone, at this point, can still think the Fed isn’t acting solely to protect the asset bubble, first and foremost.”

This is just stupid bullshit. Rates are at 5.5% and they haven’t been cut, and QT continues at full pace. What the F**K are you talking about? I’m getting really tired of this stupid bullshit.

I’m also getting tired of having to delete you stupid and toxic comments about putting Powell on the “electric chair” and similar. You gotta taka a deep breath and calm down before you come here.

How to boil a frog. Yes, you are the frog.

Now come relax in a hot tub while we discuss this. :-)

Personally I think inflation is coming back but when the dot plot changes to fewer cuts it may help curb it even without raising rates. We’ll see…

There’s no ‚curbing it’. This crook said they will get to 2% with time…What does it even mean. Seems to me like abandoning 2% target. Pumping asset bubbles and promising rate cuts in an election year. This guy and his fed poodles are an absolute disgrace.

“Personally I think inflation is coming back but when the dot plot changes to fewer cuts it may help curb it even without raising rates. We’ll see…”

Agreed that inflation is returning… but long bond rates are telling me the market still believes in miraculous deflation and therefore future rate cuts.

Hopium is a hell of a drug.

Raise taxes on the super rich. That’s a government tool that has predictable results on inflation. Spend government money on productive improvements in the ‘real’ sector of the economy. That’s the other fiscal tool that has predictable results: raises labor income and lowers unemployment. Unfortunately we no longer have a democracy, nor do we have anywhere near a balanced economy. No can do anyway. 750 billionaires and 22 million millionaires say otherwise. And the Supreme Court has ruled campaign bribery is legal, AND anonymous. Gotcha America!

Why does inflation projections restart January and February? I believe Wolf highlighted that inflation has been increasing over the last 6 months since October 2023. That trend is more telling than Jan and Feb inflation data is slightly increasing.

Wow, Powell was so hawkish stonks loving it. Yes, I know it’s wall street B S, but I do know he should have shut the f up about rate cuts period. He knew what he was doing.

What I mean is he should have come out way more hawkish to counter the rate cut projections. So tired of this.

So you want the death penalty because you perceive that you are losing a few dollars ?

First, it’s not just a matter of losing a few dollars. Powell has STOLEN 25% of everyone’s cash in the past 3 years, all to hand it to his rich friends.

While I am doing okay because my assets went up by enough to cover the 25% loss, that isn’t the case for everyone,

Powell is destroying the value of the dollar as a reserve currency, which is one of the most precious gifts America has. It’s literally treason. If that isn’t worthy of the death penalty, I don’t know what is.

Just today, they announced on the news that home sale prices are up 5.7% since last February, and that sales increased by 10% due to increased inventory. So house prices continue to spiral out of control, leaving my generation out of luck.

It’s not a matter of “losing a few dollars.”

That despicable piece of shit got on TV yesterday knowing full well what he was doing.

I wish I had listened to myself in late 2019 when it was clear that the Fed was going to have to print again to keep not just the repo market from blowing up but to keep the entire debt based financial system from melting down again. Covid and the lockdowns and the amplified panic was just the excuse they needed and another $5T was magically conjured up and here we are. I remember commenting to a coworker that “the prove level just jumped 40%”. Houses, food, stocks, gold, everything. Stimmy came with a steep price that the middle class is just starting to understand.

I think houses immediately popped due to the fact that they can be rented at inflated prices year after year. They jumped to their +40% or more 2030 price right up front in 2020-21 Everything else is just steadily plowing along. A decade of 3.5% average inflation means prices up ~40% by the end of it. Investments will see that step change plus the normal growth.

I didn’t sell any real estate in 2020 but I should have bought more. I should have bought every rentable 3/2 I could find. By 2029 those will be renting at $4000 a month and the $1500 mortgages (from 2020 at 3-4%) will be laughable.

3.5% inflation from here on out. They are done. I don’t think they will actually lower rates very fast but right now is as tight as it gets for the decade. The Fed is throwing in the towel. What happens in 2030+ when the national debt is $50 trillion and gold is at $4000+ is anyone’s guess.

Agreed. They’ve raised the target to 3.5-4%, but without admitting it publicly, as that would make all assets, including bonds which are the most important, reset.

Howdy Ol’B. Exactly why we may be in another 70s 80s style inflation cycle, long duration, high inflation for a decade or more.

I don’t think rents going up with inflation is a guarantee. I read Japan had ~30% yen devaluation in a short time but most of their wages, which I think push up rents here, were stagnant, so I don’t know if their rents are rising as much, but maybe I’m wrong. Point is I think wage increases could stall here but inflation continue. Also I think it’s morally wrong to hoard a basic human need like housing and doing so could have bad effect.

Does US Law allow for the FED to be taken to Court for failing it’s Price stability mandate ? It seems that these unelected Officials are making it up as they go along.

Not until CONgress revokes their charter. At that point, they, and their member banks could be prosecuted, and assets could be seized. However, we all know that CONgress is fully bought-and-paid-for by the financial sector (i.e. The Fed and member banks), it’s why Hank Paulson got away with TARP and TALF and bailouts for GS and AIG etc. etc.

The “too big to fail” are now even bigger, when in a functioning capital market they would have all gone bankrupt.

I wonder if the Fed learned the RIGHT lessons from their QT history. The problem in 2019 wasn’t so much that QT was CONTINUING but that QT was INCREASING. They kept ratcheting up the monthly amounts… AT THE SAME TIME that they were increasing the Fed Funds rate without a speck of inflation on the horizon. The markets/banks got confused and then the markets/banks shut down.

This time they obviously cannot decrease interest rates (the way they could have chosen to in 2019) due to the current inflation situation… but is there really any sign that the QT cannot continue at this pace for a very long time? Due to their MBS portfolio problems they aren’t even meeting their QT targets this time around.

I suppose it is good that they are thinking about ways to extend QT… and maybe talking about those ideas is just a way of signaling to the markets/banks that “this time we really mean it”… but it is a hell of a way to run a railroad.

Or there’s the reasoning that the problem wasn’t the QT amount or pace but that gambling hedge funds, mortgage REITs, and whatever else, should be bailed out, or if they aren’t, it would be bad for the system. As another commenter said, that’s what bankruptcy is for, but maybe the fed was trying to support, at the expense of ordinary citizens who do the real work keeping the country going, the ones who give money to the politicians who nominate them (the fed) for their jobs.

What would happen if the Fed went on an extended vacation, say for 2 years and left everything exactly as it sits. Would everything and everyone simply adjust and keep rolling along? And if it did, what would that say about the Fed?

Asking for my friend, Alice from Wonderland.

You have seen the politicians that we have in Washington… and can still ask that question?

Point taken.

If bank reserve requirement has been reduced to zero, hence banks can create theoretically unlimited amount of loans, how does QT work to tighten credit?

Great question. Banks really need to go back to being “just banks” again and good money/currency stewards. There is a real problem with money-good collateral because of all the destruction of price discovery mechanisms done by central banks and large corporations through their bought-and-paid-for puppets in DC. The average tax-paying citizen has no representation, and without true price discovery the capital mis-allocation will continue.

By reducing liquidity. QT has already reduced liquidity in the money markets as you can see in the ON RRPs, they’re down by something like $1.8 trillion, but some of that reduction was because some of the liquidity moved from ON RRPs to the banking sector and is now in reserves, and so reserves went up in 2023. As QT goes on, and ON RRPs go to zero, then reserves will be drawn down. When reserves are drawn down to be only “ample” but no more, than QT will stop. Long way to go.

Do you see the Reverse Repo facility winding down this year? When that goes to 0, do you see any other consequences in the bond market?

It will go to zero, it should be at zero or near zero, and it used to be zero or near zero during normal times, and there aren’t going to be any problems. This represents excess liquidity that money markets don’t even know what to do with:

Just today, they announced on the news that home sale prices are up 5.7% since last February, and that sales increased by 10% due to increased inventory. So house prices continue to spiral out of control, leaving my generation out of luck.

Just the way Powell wanted it.

Howdy Einhal. You are not handcuffed or imprisoned with a 3 % Mortgage. Now find that starter home that most say does not exist.

Stupid headline bullshit designed to be spread by morons. READ THIS:

https://wolfstreet.com/2024/03/21/amid-weak-demand-for-existing-homes-active-listings-price-reductions-jump-listing-prices-weaken/

And here is the sales chart:

Powell says debatable things, like Yellen, who claims today that wage growth is awesome. Maybe it is, but those grocery prices still seem a bit higher than before pandemic…. So do houses, cars, rents, gas and virtually everything except huge smart TVs.

The Atlanta Fed wage growth tracker shows a different realtime picture, but, data is definitely open to interpretation — especially in regard to a smooth and gentle touchdown.

Here’s an illegal link:

https://www.atlantafed.org/chcs/wage-growth-tracker

The Atlanta Fed’s wage growth tracker (which you linked) shows that wages grew by 5% yoy, which is hefty wage growth, but it’s down from a growth rate of 6.5%. So don’t let the chart fool you, it shows the year-over-year growth rate, wages are NOT going down, they’re growing very fast at 5%, but a year ago that growth rate was 6.7%. That’s what the wage growth tracker shows you.

Everything will be fine as long as the practice of MMT works.

How can the economy not “feel” great when more and more of the economy is the government and the government is spending 1 or 2 trillion per year more than it brings in.

Perhaps damage accumulates in ways we can see and in ways we can’t see, but who cares…it will work for the forseeable future and after that we will be gone.

And really, should we even care about the size of the Fed’s balance sheet ? They can’t go broke. If they did go broke, they would just say they weren’t broke and that would be the end of it.

If something comes along and the fed needs to load up the BS again, there is nothing to stop them.

The only thing that will matter is if foreigners quit buying our debt or if foreign producers start demanding payment in something other than USD for the stuff they make or if the US suffers a major military embarrassment/defeat

Unrelated but saw the Four Seasons at Embarcadero defaulted. Certainly not the first and clearly not the last. Really bad luck timing on their purchase.

You need to clarify: it’s the LANDLORD that defaulted on the loan backed by the property. The hotel operator continues to operate the hotel just fine, and you can spend a wonderful night at the Four Seasons right now, though it’ll cost a bundle, I would think. Get a room with a view.

This is part of the CRE lodging issue we’ve been talking about for years.

Thanks. What generally happens in a big building scenario like this as they are only the top floors?

In this case, my gut feeling is that the landlord is using the default as a gun to the head of the lenders, while the lenders are holding the gun of foreclosure to the head of the landlord, with both trying to force a deal to happen. There has been a lot of this recently. They will try to renegotiate the mortgage and come up with some kind of deal that both can live with. It’s really tough, but by now, the illusions are all gone, and everyone is willing to work on a deal that has a chance to make it.

If they cannot come up with a deal, the lender becomes the landlord, and they can try to sell the property at a huge loss. So if they can make a deal that will entail a smaller loss, they’re ahead.

Lawrence K. Roos, Past President, Federal Reserve Bank of St. Louis & past member of the FOMC (the policy arm of the Fed) as cited in the WSJ April 10, 1986 “…I do not believe that the control of money growth ever became the primary priority of the Fed. I think that there was always & still is, a preoccupation with stabilization of interest rates”.

“Reserves don’t even factor into my model, that’s not what causes inflation and not how the Fed stimulates the economy. It’s a side effect.” – Former Fed Governor Laurence Meyer, co-founder of Macroeconomic Advisers

Donald Kohn “I know of no model that shows a transmission from bank reserves to inflation”

You can believe what you want, but the correct viewpoint is that Powell and the FED failed us. Monetarism has never been tried.

It’s ok with the FED that shitboxes cost a million dollars+ due to their money-printing extravaganza, but withdrawing liquidity too fast which would right-size asset prices is wholly unacceptable in their eyes. The FED is a cancer upon society.

The correct way to conduct QT is the 1966 Interest Rate Adjustment Act

Hi Wolf.

Unless I’m mistaken, you have said in the past that the Fed simply allows the terms of the bonds it bought to expire at their natural date. Furthermore, you have said, I believe, that from time to time the value of terminating bonds in a given month exceeds the set monthly value (60 billion?) and so the Fed’s open market operations dip into the secondary market to buy to compensate (e.g., 70 billion expiring, they go and buy 10 billion to make an even 60 billion in debt disappear forever).

If that is accurate, then why the heck would it matter how much they let ‘roll off’ (as the expression goes, I think) the balance sheet?

Isn’t there a critical difference in the effect on interest rates between (1) selling bonds into the secondary market vs. (2) allowing the bonds to roll off the balance sheet? As in, suppose they sold $60 billion into the secondary market (rather than $60 billion cancelling out), then all other things being equal the bond prices would fall in the secondary market (increased supply) and the interest on those bonds would increase. This letter scenario seems to me to be closer to the idea behind QT. If the Fed just lets the bonds they have expire, then how does that influence the interest rate at all? Don’t they want to keep the rates high?

Thanks in advance for considering my Q.

1. “…the Fed’s open market operations dip into the secondary market to buy to…”

That’s wrong. The Fed buys those bits and pieces at auction and you can see it in the auction results, under “SOMA.” Since T-bills on the balance sheet mature all the time, the Fed constantly replaces them to the extent needed.

2. In terms of the rest of it, if you haven’t figured this out yet, that’s fine with me. I’m not spending my time re-explaining all this stuff for the gazillionth time to people who refuse to get it because it would contradict their narrative.

I don’t care for narratives. Monetary plumbing is complicated. I’m just trying to learn your view of it and generate thought-experiment predictions to ask you about to determine whether I understand one aspect or another about your view.

Also, I don’t think the various ideas about monetary plumbing are necessarily narratives in the pejorative sense that you’re using it. I think there are folks like yourself who have spent a lit of time learning about it. Some have different ideas here, some have similar ones, and others a mix. No need to assume bad faith.

“The Fed buys those bits and pieces at auction and you can see it in the auction results, under “SOMA.” ”

Directly or through dealer banks? I thought federal statute restricts the Fed from buying directly at auction (as, say, the public can), and that the Fed must instead buy newly minted treasuries through dealer banks (who buy at auction on behalf of the Fed as well as on behalf of other bank and non bank entities). Is that right?

You say the Fed buys at auction. Can’t the Fed also buy the extra $10 billion (in the example) from non-dealer banks that have accounts at the Fed?

When the Fed replaces maturing Treasuries (including T-bills) it rolls them over directly with the US government at auction (which show up under SOMA), just like you would in your TreasuryDirect.gov account.

When the Fed buys Treasuries to increase its balance sheet, such as during QE, it buys those from its primary dealers.

I didn’t see or hear anything about the BTFP.

If a person believes that the BTFP increased the Fed’s balance sheet equal to a similar amount of QE when it was announced then over the next ~12 months the rolling off of the BTFP will in turn reduce the Fed’s balance sheet by an accelerated ~150 billion USD.

That has to have an impact if it had an impact when it was created?

There was a liquidity effect when it was created, and Powell even acknowledged that in a press conference. He said that the liquidity effects of QE and of this type bank liquidity support may be similar.

BTW, it dropped by $17 billion from a week ago as of today’s balance sheet. It might be going away more quickly than we expected.