“Many potential buyers are postponing their purchasing plans in hopes of securing lower rates. Consequently, lower buyer competitions exerted downward pressure on prices”: Realtor.com

By Wolf Richter for WOLF STREET.

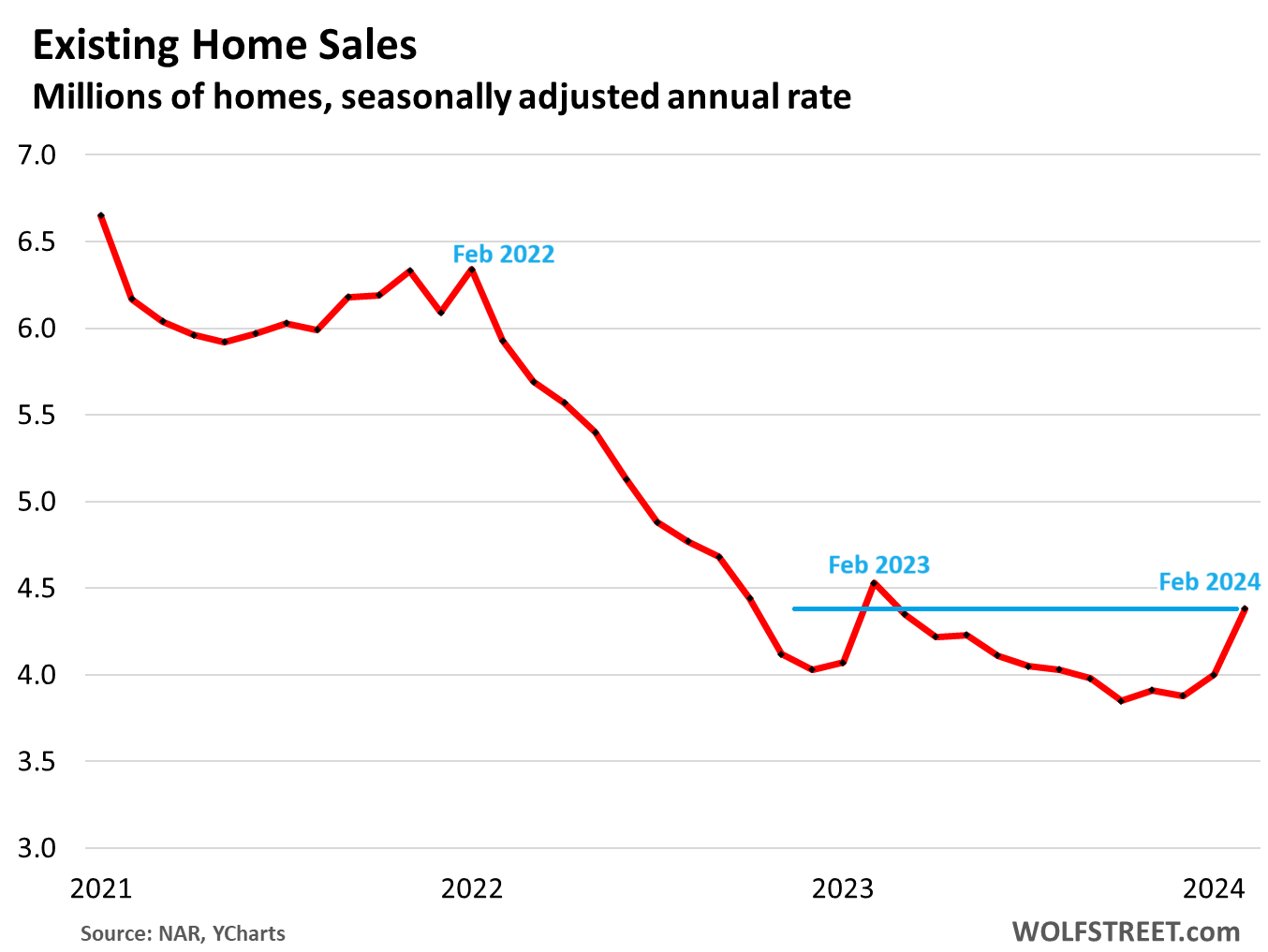

The seasonally adjusted annual rate of sales of existing single-family houses, condos, and co-ops rose 9.5% in February from January, but that increase was smaller than the increase in February 2023 (+11.5%), and so the annual rate of sales at 4.38 million homes, was still down 3.3% from the already collapsed levels of February 2023, according to data from the National Association of Realtors (NAR) today

And the rate of sales was down 26% from February 2022, and down 29% from February 2021, and down 19% from February 2019.

In other words, home sales remain at very low levels as the entire housing market has shrunk by 20% to 25% because homeowners with 3% mortgages are neither buying nor selling, so they have vanished as demand, and they have vanished in equal number as supply, and so churn is down, along with sales and supply, and Realtors hate it because they make their commissions off churn (historic data via YCharts):

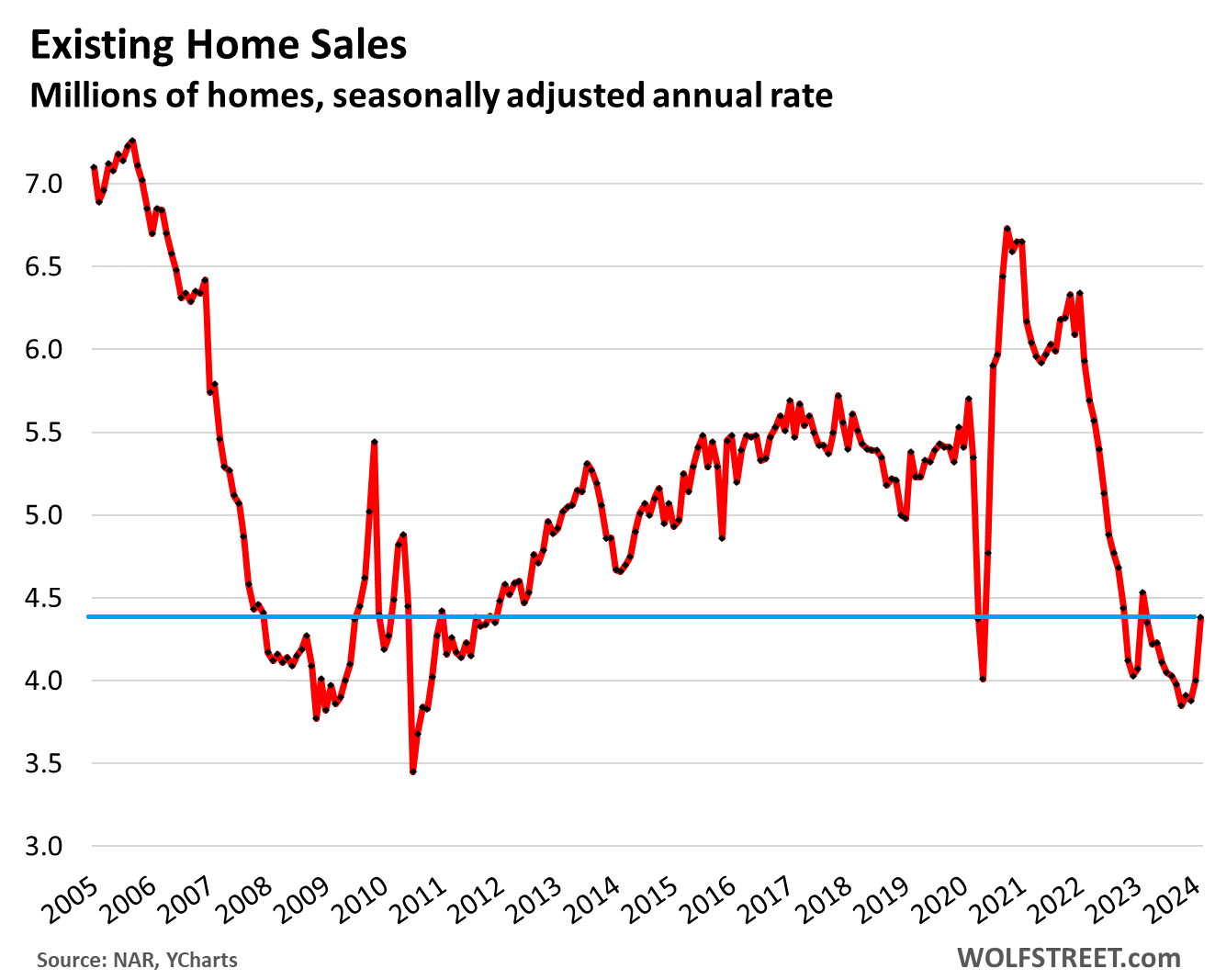

The long-term view shows that the rate of sales in January and in the last few months of 2023 had been the lowest since the worst months of the Housing Bust in 2010. February was an increase off low and was still low and below a year ago (historic data via YCharts):

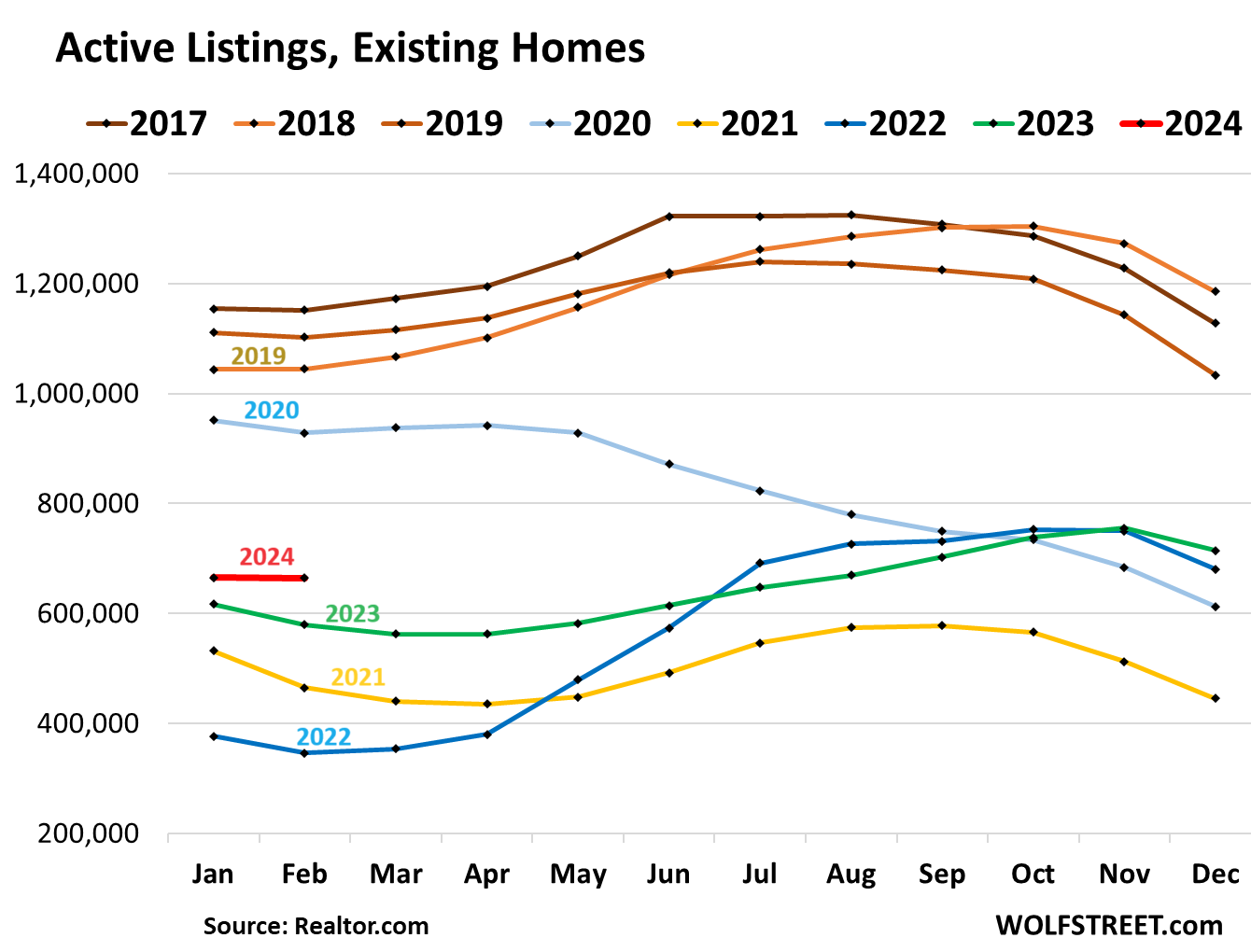

Active listings highest since before the pandemic. In February, active listings, at 665,000, were up by 14.7% from February 2023, up by 92% from February 2022, and up by 43% from February 2021, according to data from Realtor.com.

This came as new listings jumped by 11% year-over-year.

As homeowners with 3% mortgages have vanished both as demand and as supply, we have this situation where sales in February 2024 were down by 19% from February 2019, and active listings were down by 28% over the same span (data via Realtor.com):

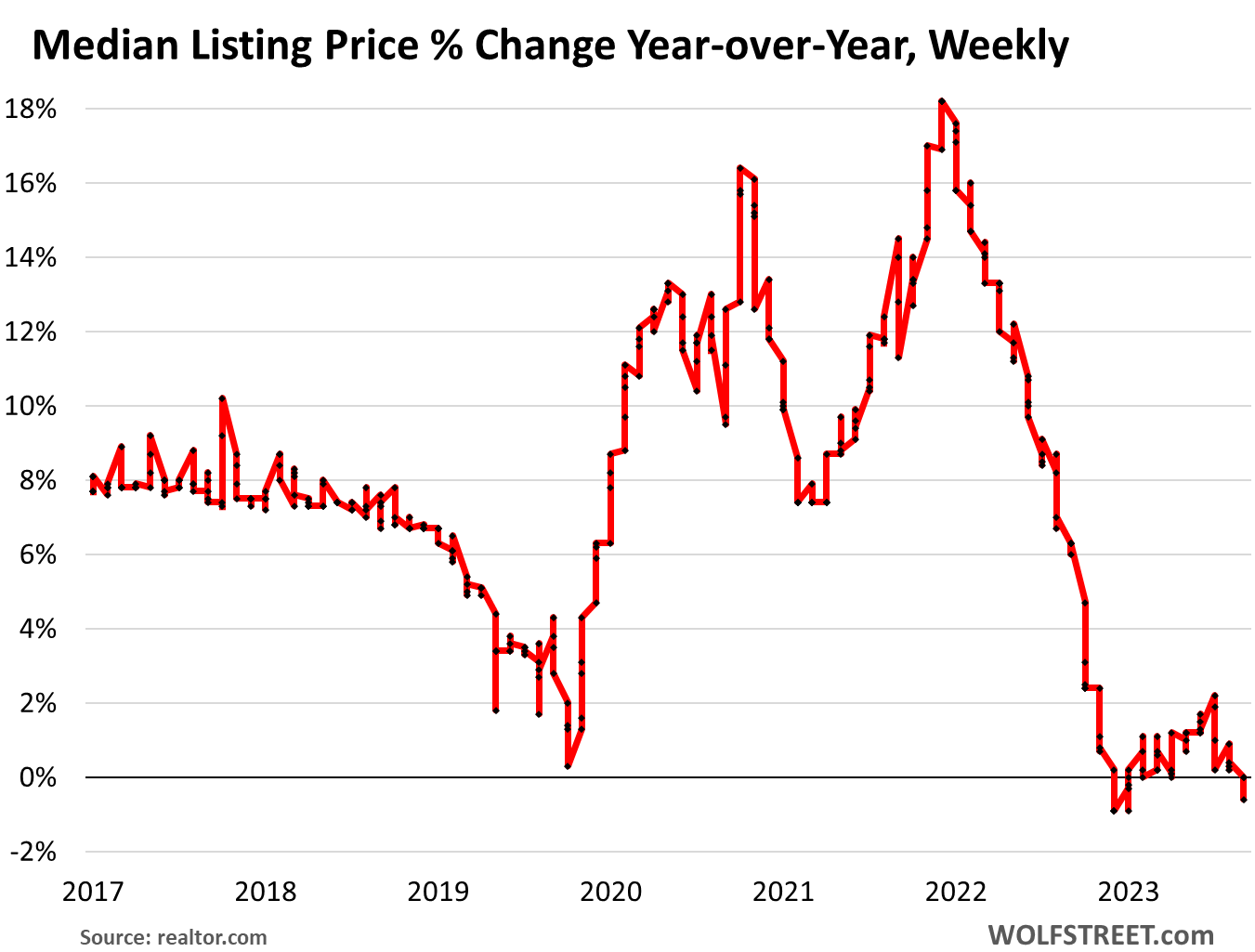

Listing prices are weakening. The year-over-year change of the weekly median listing price, released by Realtor.com, is an indication where the median sold price might end up. The year-over-year change went through a brief mini-surge in the second half of 2023 through January 13, which was then reflected in the year-over-year increases in the median sold price that we have seen in recent months.

But starting in mid-January, the year-over-year increases of the listing price shrank and then started hobbling along the 0% line, and in the most recent week, the listing price was below a year ago (-0.6%), as sellers face more competition from other sellers and fewer buyers. This year-over-year weakness in the listing price is an indicator that the median sold price through the spring selling season will also see year-over-year weakness.

In its note sent out two days ago, Realtor.com explained:

“It marks the first week of year-over-year price declines since July 2023, attributed to mortgage rates hovering around 7% and an ongoing increase in available for-sale homes, notably an upsurge in affordable listings spotlighted in the February Realtor.com Housing Trends Report. With mortgage rates nearly returning to 7% in February, many potential buyers are postponing their purchasing plans in hopes of securing lower rates. Consequently, lower buyer competitions exerted downward pressure on prices.”

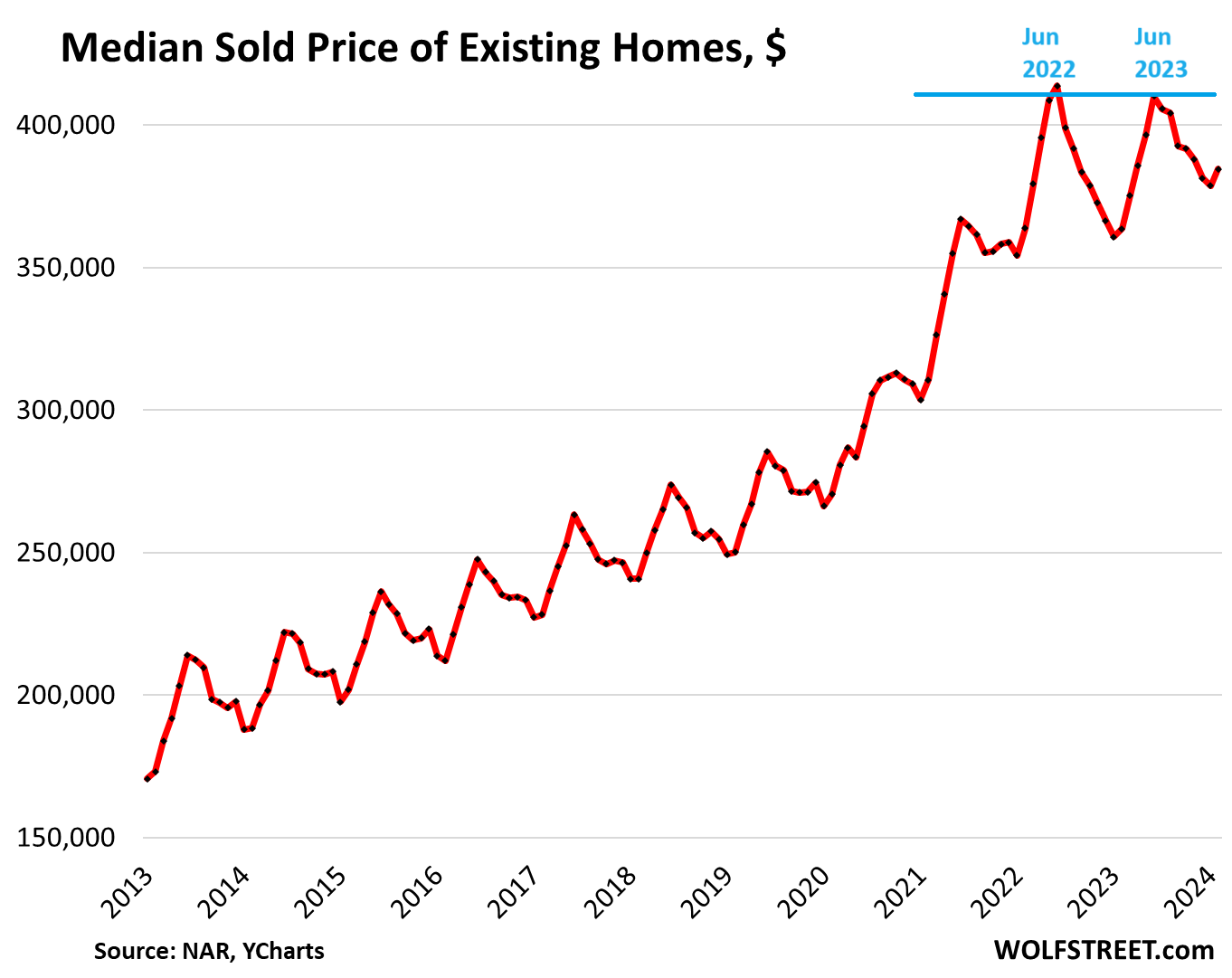

The national median sold price in February at $384,500 was up 5.7% year-over-year, but was down by 7.1% from the all-time high in June 2022.

The year-over-year increase in the median sold price of homes whose sales closed in February reflects the brief mini-surge in the median listing price in late 2023 and through mid-January.

The listing price’s weakness year-over-year since late January and the negative reading in early March should begin showing up in the median sold price over the spring.

The year 2023 was the first year since the Housing Bust when the seasonal high in June was lower than the seasonal high and all-time high a year earlier (historic data via YCharts):

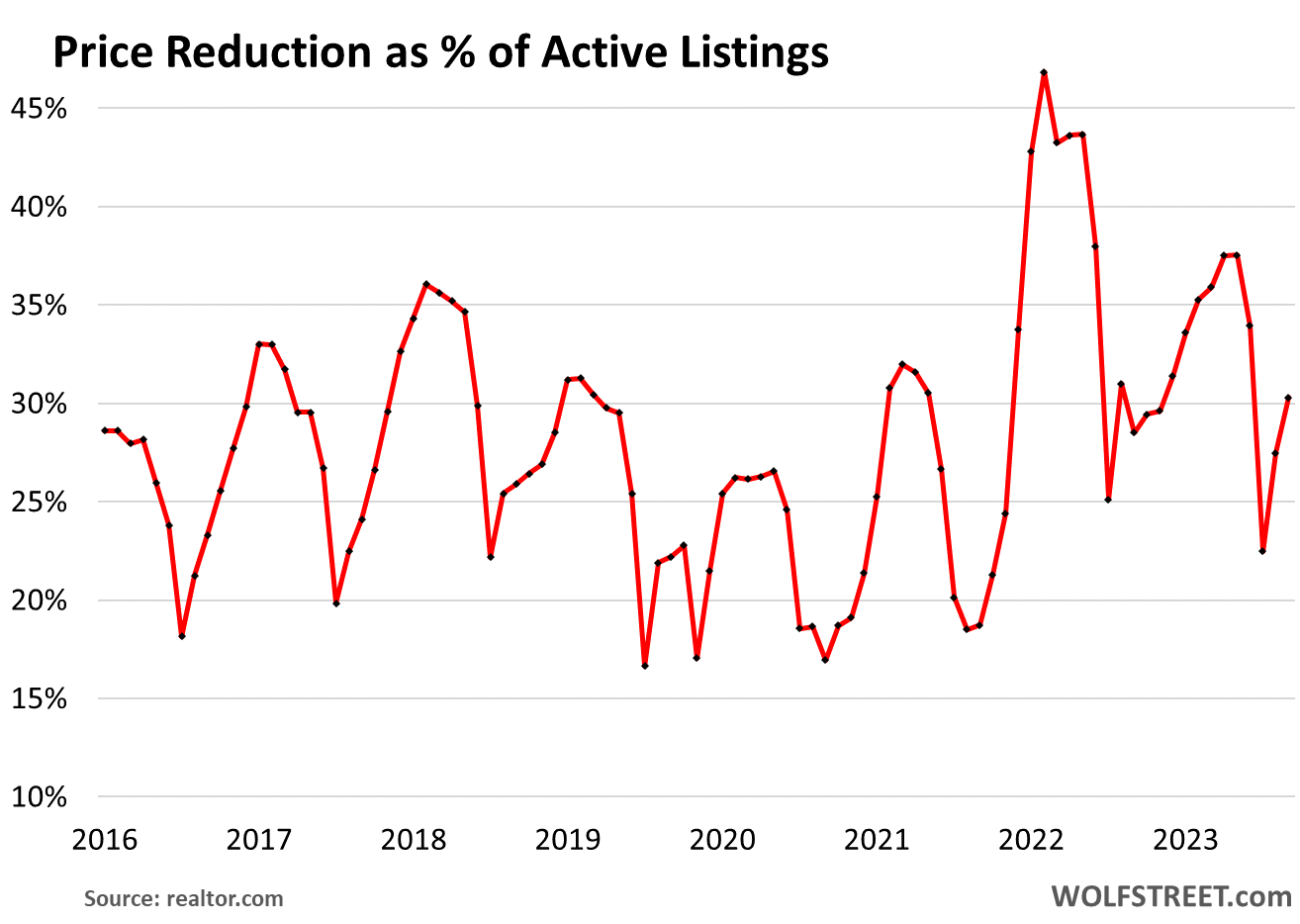

Price reductions as % of active listings jumped to 30% in February, up substantially from prepandemic Februarys of 2017 through 2020, when that rate ranged from 22% to 25% (data via Realtor.com):

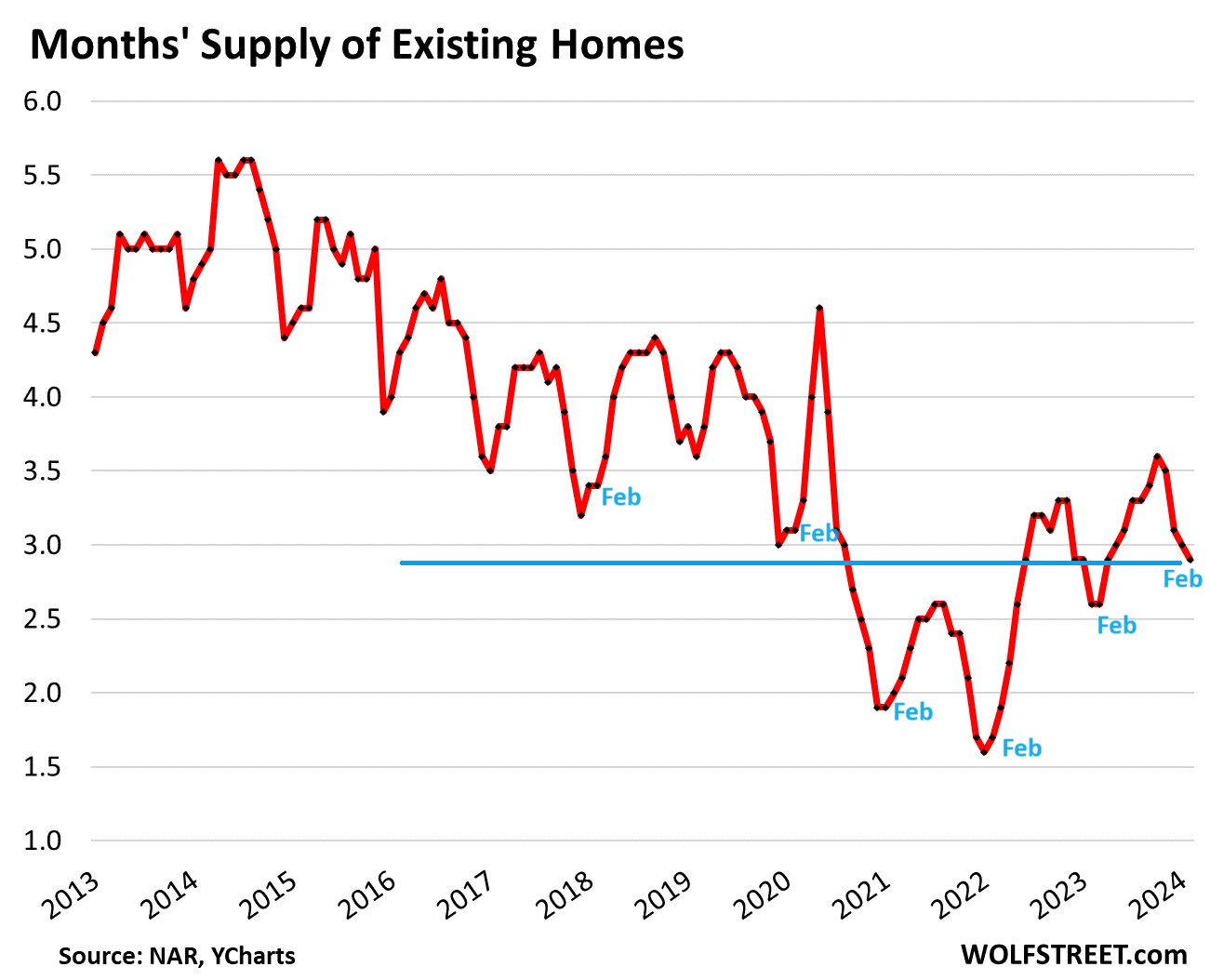

Supply of 2.9 months was the highest for any February since February 2020 (3.1 months). December through February tend to be near the seasonal low points in supply (historic data via YCharts).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Howdy Prisoners. Like your 3% Mortgage, you will have to keep it or pay more. Good News for buyers wanting new construction. The inspection period is so important to buyers of old homes. Now that all licensed agents represent the seller, a buyers agent is not as important with new construction. The NAR has a new buyers app for you. HEE HEE. The new RE Bubba Bubble will be in new residential construction, so BUY BUY BUY……

With a low interest loan and big wage inflation it should be easier and easier for people to pay off home loans, but it seems like less and less people every year even think about paying off debt early. For a guy with a $1 million 30 year loan he can save about a quarter million in interest paying it off in 15 years (most people today stick with the 30 year am + get a HELOC to buy more stuff they don’t need).

Howdy ApratmentInvestor ZIRPed to stupidly. No reason to save a buck. Years of programs making homeownership too easy. No $ down, no income verification loans. Smart folks know what a HELOC can do for you…. There is just so much stupid out there making the people in control seem smart…..

“With a low interest loan and big wage inflation it should be easier and easier for people to pay off home loans, but it seems like less and less people every year even think about paying off debt early.”

Why pay off a 3% mortgage when one can earn 5%+ in T-bills?

Because you pay income tax on the 5% interest… which lowers the delta and you run the risk of tossing your butt into a different bracket. If you’re on Medicare, you risk having your Part B tithe increase as well as your part D.

Nothing is linear.

El Katz,

If you earned enough from tbills for some of the interest to be in the 32% bracket youd still pocket ~60% of the 5% after medicare taxes and break even compared to a 3% mortgage. And that would only be on income above that threshold.

I think anyone paying off a 3% loan would be “doing it wrong” personally.

El Katz,

If you itemize your taxes, then you also get a deduction on mortgage interest, which could theoretically offset plenty of additional income through T Bills. Not to mention the low rate mortgage itself being a great hedge against inflation.

Howdy MM. If you have more in T Bills than mortgage debt, is there really any debt?

Fortunately I live in a state with no income tax, and my mortgage is actually a lot lower than 3% – so it works for me, but good point El Katz.

DFB, you make an interesting point I’ve been thinking about… I owe money on my mortgage to Fannie Mae (so really the US gov), but the gov owes me money on my various gov’t bonds (mix of T-bills, I-bonds, and agency bonds). So doesn’t it kind of cancel out?

Eventually, its my goal to have a bond ladder with coupon payments that are matched to my monthly mortgage P&I cost. I already have a small CD ladder with amounts & maturities that match my upcoming property tax bills.

The other benefit to a bill ladder instead of mortgage prepayment is liquidity – if I need emergency funds, I can quickly convert the bills to cash.

Essentially I’d be borrowing from myself at 5%, instead of doing a HELOC that would surely cost more in interest.

Well, I’m earning 5% on around a 15k principal, and paying 3% on 168k, so…

My wife and I didn’t time the market; we just got lucky. We were already in the home market when covid started and bought in the beginning before home prices sky rocketed. I have no intention of trying to pay off my home early at this point in time. Not everyone wants to pay off their home early. With such a low rate I don’t really see the point in paying it off early. I can take that extra money that I’d spend paying it down and earn more elsewhere. Also, I was listening to what the Fed was conveying and refinanced my student loans at low rates when I had the chance and would rather pay those off early instead. Different strokes for different folks.

Same – 2020 just happened to be the year I had finally saved enough and was ready to buy.

I don’t think we’ll ever see 30YFM rates that low again in our lifetimes. Our mortgages are a historical relic.

You can make principal payments from the spread on your CD’s/T-bills. Cut your mortgage interest substantially over the life of the loan.

Too many people think short term.

Man — you kinda way overpaid if you bought in any of the decent American metros in 2020. The house I purchases in Austin for $450k in 7/13 has sold three times since then, the last sale being in 2017 for 1.2 million. No improvements (save some dubious attempts to make it look like blah as hell). So things were already ten exits past ridiculous by 2020 — low mortgage rate or not.

Maybe your hovel is especially special, though; maybe Lincoln slept there or it’s built atop a lithium mine.

I’m involved in many aspects of the real estate business and I honestly thought prices would drop dramatically when the fed raised interest rates. Boy was I wrong.

I also thought we’d would have had a recession by now. Neither is happening. New paradigm maybe? Too much cash and liquidity? Maybe someone here has an answer.

Howdy CCCB. I thought the RE POP would be bigger like I anticipated bigger recessions. I truly believe they are papering over everything. Trillions on everyones books. Moving up there and now lets move it this way over there and call something new. Plain old stealing is all it is……

DFB – I totally agree with your comments and insight.

Prices didn’t drop a lot, but volume collapsed. That tells you something.

Howdy Lone Wolf. I can t wait for your articles about new residential construction. My crystal ball shows lots of construction going on. We shall see….

Crashed volume is good but does not really help buyers as the prices are obscenely high

This comment may get censored but I’d still try.

WR has been writing about housing bubble ie HB2 for last 8 or more years.

Think about the repercussion if people took this hint from WR and didn’t buy home for last 8 years or so.

They’d have been in big financial soup and may never be able to afford home to call a shelter.

“Housing bubble” is on the way up, “Housing Bust” in on the way down. We had Housing Hubble 1, and we had Housing Bust 1. This website was born after “Housing Bust 1.”

By about 2017, I started documenting “Housing Bubble 2” because that’s what it was shaping up to be. And now we’re watching out for “Housing Bust 2.”

Is this too hard to understand for you? Or do you simply refuse to understand it because it doesn’t fit your trolling?

Howdy Jon. Many of US knew Housing Bubble 2 was being created. We all have our opinions what we should do before, during, and after each bubble. And don t worry, if we all live long enough, there will be more bubbles created.

“Prices didn’t drop a lot, but volume collapsed. That tells you something.”

Indeed, just like with HB1, sales fell off a cliff. It took 6 years for prices in 2006 to get to the bottom from in 2012, and as Wolf has pointed out, housing is not stawks, so patience is key.

What really surprised me though, was the double-top a year after the initial price drop in 2022. Just goes to show there’s no knowing when we’ll run out of Greater Fools, but it’ll happen eventually.

Well, Wolf’s articles on housing and labor are worth reading through to see why there isn’t a housing based recession in US, including this article. Labor market is still good and it was very tight before, people are making money and paying their bills, so it’s tough to get a housing based recession, people aren’t forced to sell so they don’t and new houses are selling with various incentives effectively lowering prices for new buyers. The drop in prices isn’t very big at this point and more buyers bought in at lower prices so many are still sitting on gains. In the labor articles you’ll see something else of note, a boom in commercial/industrial construction in the US, so even if residential construction slows down enough to get any significant layoffs many of those workers are likely to land on their feet in commercial anyway, I’m sure some residential trades people have already made the jump if they can get better pay and/or conditions. But, rents keep climbing, as long as the rental business is good then even residential construction will keep kicking on IMO.

As a Canadian I’m pretty envious of these 30yr fixed rate mortgage schemes you guys have in the US, we can only lock in for 5yrs so every year there’s a bunch of people that need to refinance at higher rates. IMO if that was the case in the US then price decline would be a bit quicker, but that’s not the case.

Not a new paradigm. It’s demographics. Boomers with large retirement accounts are leaving the workforce. Millennials entering their prime earning years are replacing them. Both are sources of increased demand. For millennials, it’s seen in massive consumer discretionary spending. For Boomers, it’s seen in massive services spending. Boomers leaving the workforce are a source of decreased supply. Combine the two and you have a hot economy.

There are more boomers than millenials, who have less money and smaller families anyway, so prices will drop. Realtor.com should just say: “FMV prices have dropped but sellers refuse to recognize decrease; buyers are not fooled.”

A correction is inevitable. We are not like the RE disaster in commie China but are grossly overvalued nevertheless. We have good, long term future prospects but for now, our bubbles will pop, nonetheless. I want to see which RE and CCP-Ponzi company investors (often same fellows) will survive! Read about Blackstone.

Lower priced real estate will not drop much: retiring boomers and others will compete for smaller, cheaper homes.

One possible answer CCCB:

In spite of the common ”meme” that most folks are too dumb to understand the fine points of the financial situation, it just may be possible that many, if not most above the lowest percentiles know exactly what is happening as the FRB and the CONgrssers continue to degrade the US Dollar.

NOT saying that this alone is the total basis, but it certainly seems part of it.

Also gotta keep in mind that the stop of the RE markets in various recessions/AKA depressions were caused by MUCH higher interest rates, such as 18% when we bought our first house in SF Bay Area for $40K, sold it with significant upgrades for $105K couple years later,,,,

same exact house was over $800K last time I looked couple years ago, likely well over M now.

Govt borrowing and spending an EXTRA trillion every 100 days?

The FED has to shrink AD, it hasn’t done so. That’s the basis for N-gDp targeting.

“CCCB” I’ve had the same thoughts and been just as wrong, should have been in recession by now. I am also involved in the residential development industry.

“Wolf” I greatly enjoy your insight.h

Well.. or pay it off and stay forever. Thank you low mortgage rate. Ya shaved off years. 👍

Howdy Sufferin. Congrats. Save $ or pay off debt. Way to go…

Stock Brokers will tell you the opposite though…..

There you go again….do U realize that you posted 5 out of 9 comments? TOO MUCH!

Howdy James. What if I told you I just bought an EV???

There is one additional aspect of paying off debt that is beyond finance. It is personal freedom. In my early twenties my father in law told me that owing money was economic servitude. He was right, as anyone who has paid off a mortgage will tell you. I started out working for some pretty crappy bosses and they liked it when their employees were under their thumb. But when you owe nothing, and you can walk at anytime there is unspoken respect. It is akin to working for yourself, and I have done both.

No debt, pay cash or don’t buy….. And anti home ownership people will tell you that you are still a slave to the taxman. My solution was a rental that covers all taxes and insurance on neverything, plus. None of us are truly free, and nothing wrong with obligations, but there are ways to maximise independence and choice, and debt does not do it.

Actually for Paul S.:

ABSOLUTELY RIGHT ON!!!

The personal and FAMILY benefits from being free of a mortgage is one of the best feelings ever!!!

And then, the benefits for family continue at least until the grandchildren or multiple cousins cannot agree.

GOOD comment, please continue to add to “Wolf’s Wonder.”

Thank you,

Floridiots and half-backs are still moving here to rural Red America. A friend listed her house last week for $559K and it was under contract yesterday for $549K. She paid $440K two years ago. It’s a very well taken care of home and those move fast in this price range. This county builds about 250 new homes each year and 99% are homeowner-funded custom homes. Real estate is local.

Nemo300blk,

Can I ask what county you are in?

Nemo300blk,

She cut her price by $10k to make a deal! I love it. That’s what it takes.

My friend put his house for sale in NC for $1.45M about 280 days ago. Now the price is $1.2M and still has not been sold.

Because so many homes and home owners are out of the market, I wonder if a decent indicator for the direction of prices will be the ratio of active listings to the number of sales?… as an indicator of supply and demand.

Howdy ChS. They have to keep the hissing going and NO POP. The 3% percenters will have to move sometime, divorce, job, dead. New residential construction will boom. NAR agents say so. Sorry, NAR selling agents…..

I’m convinced that the only way to fix the housing market is for Congress to seize it. Meaning to retroactively increase everyone’s mortgage to 5-6%, and if that means you can’t pay your mortgage and have to move out, that’s just too damn bad.

People get harmed by government decisions all the time. No reason that homeowners should be protected when no one else is.

Well, as someone with a 2.875% mortgage, I don’t care for your idea at all. lol

Howdy Einhal. Not a good idea. Don t ever trust a thief to be honest or return something they stole. Govern ment picks winners and losers all the time…

How does making people move help the housing market in any way? Anyone who has a home and is forced to sell would then be forced to buy. We need to change the ratio of sellers to buyers in a meaningful way and the only way to that is buildouts. Or genocide I guess but that seems messier.

Speeding up the game of chairs only makes things more competitive. We need more chairs.

Howdy ChS and Congrats on less than 3%. A HELOC can be a great way to unlock those handcuffs. Very easy to build wealth that way if you are smart enough…. Good Job……

Einhal, do you really believe that government forcing homeowners to pay a higher rate TO BANKS is the right move? Retroactive law is disastrous and breaks one of the fundamental rules of law: new law cannot litigate past actions which were legal. The only instance of retroactive law on the US government’s books that I’m aware of are the Resource Conservation and Recovery Act (RCRA, 1976) and Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA, 1980). These are environmental laws relating to liability for spills, clean ups, dumping, etc.

Even these laws have been protested by folks for decades because they erode the rule of law.

The government doing something like that would be swiftly met with pitchforks and drones.

The government just needs to STOP messing with markets. We the People must demand to reduce the number of regulations, eliminate tariffs, abolish minimum wage laws, abolish direct government support of unions, stop providing money to companies (*cough *cough INTEL), streamline immigration, and the eliminate Departments of Education, Housing and Urban Development, Veterans Affairs, Interior, Labor, Agriculture, Energy, Transportation, etc.

Let’s demand a lean government with fewer functions and less meddling. Then we can all get on with our lives with more personal freedoms and economic opportunities.

“Meaning to retroactively increase everyone’s mortgage to 5-6%”

No. No more interest rate manipulation please.

The way to fix the housing market (if lowering prices is your definition of fixing the market) is more supply. Especially in popular living areas. We under built for decades. Resistance to increased density by current homeowners only makes things worse (for new buyers). It is that simple….

This tide would also turn

People are forced to sell their homes for variety of reasons and over time some of them would be impacted.

Another way to do that is no tax write-offs for interest. None. Especially for Blackrock. Then they’ll puke out their SFR back onto the market.

E

Congratulations !

Loopiest idea ever !

By the way….. love how you seem be suffering.

May it always be so.

‘and eliminate Departments of Education, Housing and Urban Development, Veterans Affairs, Interior, Labor, Agriculture, Energy, Transportation, etc.

Let’s demand a lean government with fewer functions.’

Well it would certainly have fewer functions. Doesn’t Dept Energy have something to do with electricity and Transportation have something to do with highways?

It’s not the banks that would be the beneficiaries, but taxpayers, under my plan. The sub 3% rate is a taxpayer subsidy. What the government giveth, the government can taketh away.

Einhal:

My counter is that if you raise my mortgage rate by 300bps, you have to raise the rates on all my bonds & CDs by the same amount.

If the 3% mortgage is a gov’t subsidy (I don’t necessarily disagree) than so is literally every other rate. If I have to pay a higher rate on the debt I owe, then my debtors should also pay a higher rate on their debt to me.

Then*

MM, wait a second. You think you have a right to have a 3% delta because the rate you pay to borrow and the rate you lend? Why?

Wonder how many citizens will be thrown into the bath tub and drowned along with the Gov’t when the time comes?

Will “they” (and I mean most of you here that don’t have at least $20M) go easily once you figure the REAL game out?

I think a lot about that…..but I’m not worried about myself at ALL……unlike the rest of you.

Thoughts and prayers…..that’s where empathy ends now, right?

Two wrongs don’t make a right and no one is being protected the wasteful destabilizing actions of the Republican and Democrat uni-party. The result of this debt, deficit spending, dollar devaluation, and unfree markets is at best stagnation and declining living standards, at worst, war and destruction. Plus, they probably are paying those extra percents in inflated costs of ownership.

MC Bear – doubtless you’ll do all of your own, individual, undrafted, uncompensated, effin’ soldiering, no matter your age, when the time arrives (…and sadly, history demonstrates it always does…).

may we all find a better day.

CoreLogic recently did a study comparing in-market home buyer incomes vs. out-of-market home buyer incomes.

https://www.corelogic.com/intelligence/examining-income-gap-between-migrating-homebuyers-locals/

Perhaps not surprisingly, many years of Fed f*ckery-pokery regarding interest rate manipulation turned the housing market into a speculator’s casino (see also, 2008…)

Howdy Cas127. Before 2008, you could sign your name and walk out of closing with a house and a check.

Plus, do not forget when the GSEs said that they would back MBS from the Wall Street Rental home companies. That allowed them to overbid because they could now pass the risk onto MBS investors. The MBS investors are not worried because the GSE back these mortgages 100%. What could go wrong.

In 2017, when I read the following in an article, I knew that Wall Street was going to enter the rental housing market big time.

——————————————————————

Fannie Mae, the government-backed agency said it is going into business with private equity giant and major housing player Blackstone by backing $1 billion in debt. Blackstone’s Invitation Homes filed for an initial public offering this week, and the Fannie Mae relationship was disclosed afterward. Blackstone is looking to raise $1.6 billion by selling shares to the public.

Fannie Mae, currently under government conservatorship, will back $1 billion in debt collateralized by rental homes owned by Blackstone.

Some have already voiced concern that the deal puts taxpayers on the hook yet again, should the rental market end up in a “bubble.” Rental demand is high and rents are high currently, but homebuying demand is also strong and home sales have been rising steadily.

“Blackstone is a market-leader when it comes to securitization innovation. Other corporate landlords will soon jump on this bandwagon, and demand for rental properties will rise,” wrote Andrew Roalstad, senior analyst at TIS Group.

“We predict the increase in these type of government-guaranteed securities will grow exponentially in the coming four years, and the impact on the rental property market will be extraordinary,” added Roalstad. Shifting corporate risk to taxpayers has been a profitable business over the past few decades, and throughout history. We expect we will see more of this shift in the coming years.”

The implication here is insanity. The common man is essentially bidding against the government for a single family home to raise his family in.

My reaction is that fatigue is going to play an increasingly important role in all economic matters, from grocery shopping to home transactions, stocks and consumption. Fatigue, burnout, hesitancy and disillusionment pairing with ambiguity, chaos, confusion and distortion.

As mortgages and yields stay higher for longer and as affordability stands out as insane, and as GAAP earnings decline and earnings yield falls, the Gold Rush will abate — the tsunami has made landfall and is receding.

The fear of missing out mentality will slosh into the fear of losing.

The grinding down of euphoric excess will help housing inventory grow and expand into a period that will phase in as malaise and grow like cancer.

Thankfully, there’s an infinite amount of apartments available to help smooth out the coming transition…

Best macro observation I’ve seen on here in ages. People are bored with this shit, and I bet a lot of first time buyers who actually saved and deferred gratification to get their nut together are having second thoughts in this market; certainly they’re not going to be in a hurry to over-allocate the precious drippings of their labor to some overpriced millstone.

Are you allowed to live in an uninsured house? (I honestly don’t know..never bought one…..I built one class K off grid and it was too far out in the woods (10 SLOW shale road mi from 101) to insure. A private broker quoted me around $2500/mo (if I threw in my truck). If legal, is it a wise economic move? I know it’s illegal to drive an uninsured car, but our “useless” government doesn’t pick up that tab, like FEMA does for houses that were “disaster crashed”. Also, people get injured and property gets damaged by something that wasn’t code. And I see an awful lot of ambulance chaser ads on TV.

So, combined with ever more natural disasters every year (solidly proven) I was just wondering if that fits somehow into that “best macro here” comment.

Oh, class K in Mendocino County is no inspections at all, and sold “as is”, buyer beware and all that. 16 years (5 full-time) and it still wasn’t “finished” in the normal sense…..but I found it livable….after the first 8-10 years, anyway………it gets easier as you go along.

NBay – …so true…

may we all find a better day.

Five new foundations were poured in my new development of SFH’s this week and four have sold signs in front of them (one spec home, I guess).

This is in south Texas in a SMALL development of homes ranging in size from 1,200 to 2,500 sq. ft. and include all appliances and landscaping (minimal). Our development will be built out by Christmas and maybe have 150 homes in it. Then the builder starts on another parcel a few miles away.

There are 1/2 dozen builders popping homes on new land around here and it’s going gangbusters. Pricing is from mid $200’s to maybe $350+ K depending on upgrades. Developers are buying down the mortgage rate (recent – 5.99%).

Buyers are young families, singles and retirees, like me. On my street of maybe 20 new homes there are 8 retirees (three widows, one widower (me) and the rest couples). Better than renting since a nice rental around here is near $2,000/month.

Real estate is local, for sure.

Bring on the supply. Building houses is good for the economy and good for supply.

On a very marginally related note, I find it odd/disquietiing that entities that have the reputation for facilitating homebuilding (Habitat for Humanity, government housing agencies, etc.) do not particularly facilitate the dissemination of detailed information (via the essentially costless internet) on the actual, detailed costs/processes of home construction.

Simple, low cost home plans/take off lists with periodically updated prices could be put out on the internet once/twice a year.

If nothing else, such efforts would put inflationary home costs in context (somehow homes that could be built for X in 2000 can “only” be built in 2023 for 3 or 4X).

Putting the Excel/Pencil work online would take a tiny fraction of the resources that H4H and Housing Agencies expend for their higher profile public activities…and yet Google searches don’t seem to turn up much at all.

The Census Bureau has construction cost indices for single-family houses, and there had been some huge spikes, and I reported on it.

The PPI also includes special indices for costs of construction of various types, industrial, office, etc., plus broader nonresidential and residential indices. When I report on factory construction, I include the PPI nonresidential construction costs. They’re pretty good. They all picked up the huge spike in construction costs since 2020.

The biggest deterrent to affordable housing is government regulation on the local, state and federal level. Single family neighborhoods that used to take 3 months for design approvals now take 18 months and with the addition of so many more requirements keep driving the cost to build higher.

I’m all for more housing. Affordable housing that is. New construction here is sitting at 1.2-1.5m….no one buying. No one wants to spend $10,000/month on a cookie cutter mcmansion in Nassau County.

Still fighting on getting a home. Lost out to 8 offers so far, had an accepted one that got reneged on when the sellers sister got involved, and countless others that get listed, I call to ask only to find out accepted all cash offer. I’m beyond stumped as to where people have 700k liquid…..did I not work hard enough or am I in the wrong line of work? Lol

“I call to ask only to find out accepted all cash offer. I’m beyond stumped as to where people have 700k liquid”

Well the guy who sold that house now has $700k of cash.

You’re looking in Nassau county, probably one of the most expensive mkts on the east coast. Not sure if it was you or another commenter I said this to, but why not look in southern CT and take the ferry over?

Real estate sure is local, I just got an email that a new construction (5br 4,627sf) home just hit the market in Olympic Valley, CA for $5.3mm (343 Creeks End Ct.). I don’t know how developers can sell homes in TX for a profit in the “mid 200’s” when it will cost that much in soft costs before you get a building permit for a new home in CA (planning fees, permit fees, architectural plans, engineering reports, site survey, soil reports, landscape plans, etc. etc.). I recently paid over $100K for just the sprinkler system in a new 1,400sf leasing office (the city made me connect it directly to the water main in the street and pay all the cost to dig up and repair the street and sidewalk).

They can do it here because the builders are not in California. I lived in Thousand Oaks, california for 12 years and know the deal. You are overrun with regulations, high paid local government employees, nonsense taxes, high cost labor, and people who make big salaries.

I have 1,479 sq. ft. home with a small yard and just paid $2,200.00 for a sprinkler system with a digital controller and the local water company gave me a $50 rebate for using a digital one. My landscape guy put in my system in 1/2 day (two sides, front and back – 5 zones).

My home is a starter one, but is very energy efficient with a high SEER A/C unit, lots of insulation and double pane windows throughout.

California is nice, but expensive. I just paid $2.89 per gallon for 89 octane gasoline today.

When we lived in CA (Orange County), a developer bought a small plot of land that was once a water tank farm. His plan was to build 13 homes – big bombers on postage stamp lots. In order to get the permits, he had to re-do the streets outside the development. Turning lanes, median strips, new sidewalks with the “bubbles” for the vision impaired, bury the power lines, move the street and traffic lights, build a block wall, and lord knows what else. Then, of course, there was the status symbol of “gates”.

He did build them…. sold (back then circa 2014) in the $1.5-2M range… but it gives an idea of what lunacy exists in CA vs. the rest of the world.

BTW, the comment that “we need more housing in popular areas”: The thing that makes them popular is the lack of housing. At least in my mind. I like the quiet, few street lamps so you can still see the night sky, and unobstructed views of natural beauty – not my neighbor’s bathroom window. Fortunately, they can only develop on one side of us… the rest is national forest, county nature preserve or Native American reservation land (agricultural). We bought in this development for that reason – it’s tranquil and we are a mile from any road with meaningful traffic. Hopefully, any new development will lay fallow as the RE “investors” run for the exits. The HOA “ruled” out the VRBO’s (now a 30 day minimum) which triggered some of the sales.

Anthony A., I’m sorry for your loss. Great opportunity to buy in TX for new builds. I’m looking as well. Yeehaw. Hope you’re able to negotiate for the builder covering $$$ for upgrades. If you have the cash, skip the rate buydowns and put towards structural upgrades. Make it as comfortable as possible. Hope you’re out of the flood zone; away from creeks and preferably near the top of the local watershed.

To everyone buying, stay safe out there. The US has been hit with heavy showers ($$$ printing) and water runs downhill. Picks up feces along the way…

Thanks, Bear, she’s been gone 15 months now but I still miss her a lot.

Yes, the builder threw in a new double door fridge, window blinds throughout, garage door opener, ceiling fans in a couple of rooms, some extra landscaping, and a full walk in shower since I paid cash. Too hard for an 80 year old to get a mortgage..LOL.

No flood zone here (way north of Houston proper). Lots of surface drainage nearby and a big retention pond the builder had to engineer in.

It’s really a nice little house, but I think I should have gotten one a bit smaller (1,250 Sq. ft.) as there are two rooms I don’t have any need for.

The red hot real estate market here for second home/vacation lakefront property has slowed considerably. (Northern Michigan here, prime multi-million dollar vacation home area). It’s a bit of a mystery since the wealthy should be flush with cash due to the stock market windfall.

Four possible theories/factors:

1) The stock market is on fire, so they’d rather keep their money there for now

2) Even they are shell-shocked by inflation and now higher interest rates and property taxes, etc.

3) They expect a real estate correction. Nobody—even the ultra-wealthy— wants to overpay

4) The pandemic/low interest rates front-loaded the demand. There just aren’t as many people left now still looking for that vacation home…

Thought of another:

5) Their businesses aren’t actually doing that well (with higher labor costs and narrowed margins) despite what the stock market is doing. They see recession.

Stock market is just a marker of liquidity in brokerage accounts and not really tied to the real economy until those funds are withdrawn (imo). So if everyone puts their money in their brokerage accounts and not real economy I guess you could have super high equity prices and a dead economy lol.

Housing market in central FL is wacky. I see places that are super high priced go pending in a day still, but then other places I think would go fast sit for a longtime and get price cuts. Baffling…

Agreed. The wealth concentration in the U.S. that the Fed has helped to propagate means that the stock market is basically just the top 5-10% selling bubble shares back and forth to each other.

It’s not a marker of the economic health of the country anymore.

“It’s not a marker of the economic health of the country anymore.”

I’d actually say it is the best marker, but obviously an indicator of poor health rather than good health. We need the stock market to crash 90% or so, and the same goes for house prices.

And we need 90% tax rates on billionaires and hundred millionaires. Seizing their assets is a good start.

DC

What we really need is for kitchen cabinets and their installers fees to fall by 90%.

You can’t even afford the cabinets to begin with, OTB. And skilled labor rates are only going up so you can forget about ever affording them. You can’t pay the salary of somebody who makes 5 times as much as you.

Kitchen cabinet makers in US really have a monopoly on cabinets…they basically blocked Chinese cabinet makers from shipping RTA cabinets by imposing 262% tariffs lol. So now we get MDF cabinets that cost like $50k.

Howdy, 10 out of 28 so far!

Just wondering, Wolf are all of the comment rules void or just #6?

Howdy DougP. Liten up Francis. HEE HEE The Lone Wolf knows what he is doing.

Too Bad U don’t!

Are you a Realtor?

What makes yo an “expert” (Big Mouth) on RE?

I wonder.

Howdy James. I was a Licensed Broker with my own brokerage in the mid west. Made a great living rehabbing Residential RE Foreclosures, Short Sales, and good old POS and resold for profit. Have a bad back to prove it too.. Maybe my mouth is just old school and not so big after all?? Not many Self Employed old school Bubba s out there any more. Maybe they have a Bubba App. for youngins to understand???

Howdy Youngins We have been sitting at 42 for awhile so. First Sentence by the Lone Wolf.

“Many potential buyers are postponing their purchasing plans in hopes of securing lower rates.

A buyers agent should know all about teaser rates, balloon loans, bridge loans, HELOCs OH sorry. We no longer have NAR Buyers Agents.

Residential mortgage interest rates are moving nicely upwards to around 7.27% based on the 10-year US Treasury yield now around 4.27% plus the around 3% additional amount for mortgages.

Those were about 1995 interest rates.

At what point will new home sales take a bite out of rental demand? Seems the ever increasing rents are pushing renters of choice into becoming new home buyers. I’m assuming you are correct in saying that renters of choice have financial means to buy and are not renting due to poor credit scores.

I know increased immigration is great for the economy, but what is the relationship between new citizens and demand for new housing or rental units and changes in rental rates.

The competition is like this: home builders, sellers of existing homes, and landlords are all competing against each other. So there is a lot of this arbitrage going on, but it may be in the other direction than what your question asks.

Build-to-rent is huge. The biggest single-family landlords are building through their own home-builder divisions or are buying entire build-to-rent subdivisions (some of them already leased out). These subdivisions have leasing/maintenance offices, staffing, and various amenities. And these landlords are seeing big demand because, as one of them said, it costs people $1,200 a month less to rent a nice house than to buy an equivalent house in the same area, even with the rate-buydowns from homebuilders. Families have some pretty good alternatives to overpaying for an existing house.

I started out in construction building houses with my brother, then on to bigger projects for bigger companies, then bailed in my twenties to fly bush planes. Now, at 68 and retired for 12 years and still building my own stuff, I talked two relatives into purchasing modular homes as opposed to contractor builds. (They own their property outright.) Modulars are NOT trailers, they are to code, energy efficient out the ying yang, can be somewhat customised on the build, and can certainly be dolled up and personalised after location to site. Brother in law, also a carpenter, doing the foundations. It takes about 1 week for set up and completion. 1 Week, and that’s everything. I have seen them set up in a day. But there are always those little details to complete.

This will be the future and will save mucho dollars for buyers. As for that elusive individuality that contractors support, just how personal are tract home developments with 3-4 designs and some mirror images of same? A modular can have select kitchens, appliances, decks, etc.

I have built scads of single family homes, from concrete to finish. Start at 8:00am and finish up at 4:30. Breaks and lunch. Pack the lumber, cut the rafters or set trusses. Build stairs, install windows, wait for the sub trades to show up and wire, or plumb, drywall. There is nothing more inefficient. And toss in some new owners wanting to make changes along the way?

I live in my own custom home I built for myself, by myself. If we have to relocate one day, I would go for a 2 bedroom modular or a fixer upper. As modular homes take hold in the market all prices will drop as a result. The market will have to compete with efficiency.

Was your car built in your garage, or in a factory?

regards

Howdy Paul S. Short Version of your post. or Title

Individuals Freedoms PRICELESS

Modulars can be great. From foundation to a locked door in a day. As far as the future, I see a lot of rules against them from municipalities and HOA’s.

Live & work in flyover.

Modulars have been a large part of our work

for years. From lake homes to replacing the existing

single wide.

I think modulars themselves are great – a buddy of mine has one with a jacuzzi tub.

But in my area, all the modulars for sale come with insane HOA fees – sometimes as much as a few hundred$$ per month.

When you rig the system to put the majority of houses and all assets in the hands of the wealthy, this is what you get.

Yes, that’s what these people have in store for us. We’re all debt slaves working for them.

Don’t worry guys, median house prices sold were “only” up 5.7% – time to pat JPow and the Bailout Boys on the back for a job well done. Time for rate cuts! /s

I wish that was a joke, but sadly is the market consensus.

Median home price in the USA:

“The entry of an estimated 3.3 million migrants in 2023 is likely creating demand for housing”

S

Oh look !

The most completely speculative sentence ever !

Good luck with a recession call.

When are buyers going to get off the interest rate drug. Stop buying and prices will fall. It’s price not rates that is the problem

People have been trained to be payment buyers. Starts with the car biz and pours over into their next logical major purchase as they build a life and family. If you’ve ever seen a “four square”, you’d know how it works – and how people are buffaloed into buying more than they can truly afford. It’s kind of like three card monte….

It’s not what your payments are, but what you pay for an item. It’s always been true. Most people have poor impulse control.

ElK – true dat.

may we all find a better day.