The Fed’s Waller and Logan lay out some basic principles.

By Wolf Richter for WOLF STREET.

On Friday, Christopher Waller, member of the Federal Reserve Board of Governors, and Dallas Fed president Lorie Logan laid out some broad principles how far and how fast QT could or should go in order to “normalize” the balance sheet, how they would try to avoid an “accident” along the way so that QT could go on for longer, and how they might deal with a future emergency by doing QE without increasing the balance sheet.

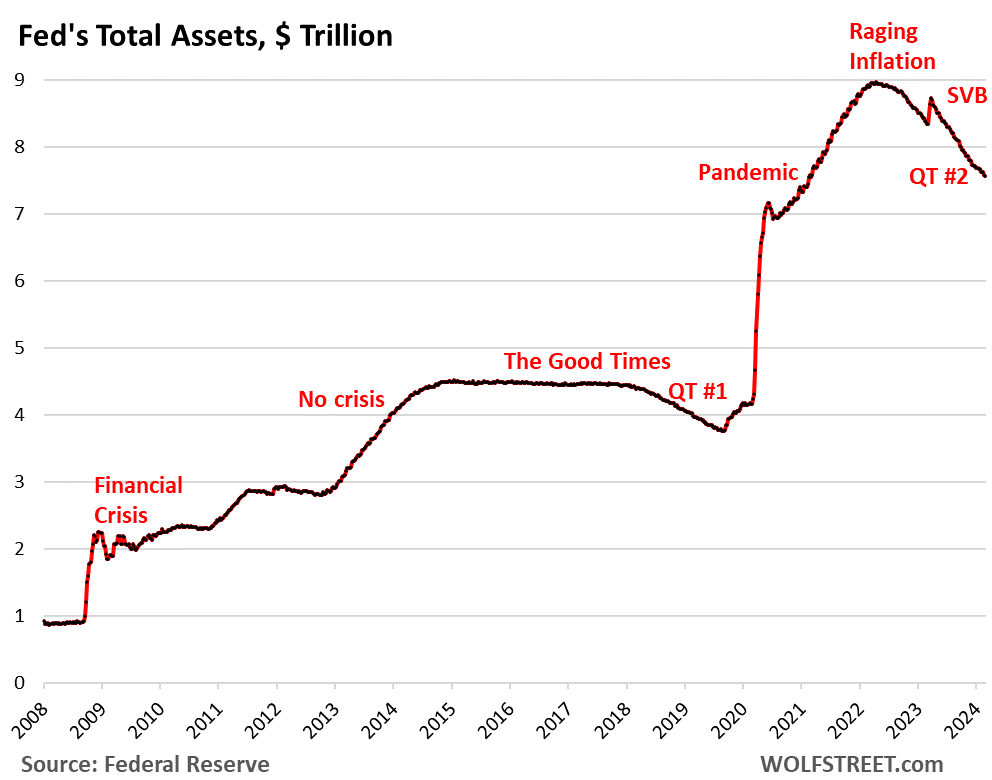

So far, QT has removed $1.40 trillion from the Fed’s balance sheet since the peak in April 2022. Total assets are now down to $7.57 trillion:

The principles they laid out.

In the FOMC minutes, released on February 22, the Fed had already outlined some basic ideas: The Fed Wants to Drive QT as Far as Possible Without Blowing Stuff Up, and it’s Working on a Plan. In their speeches, Waller and Logan provided a lot of additional material and principles. So here we go.

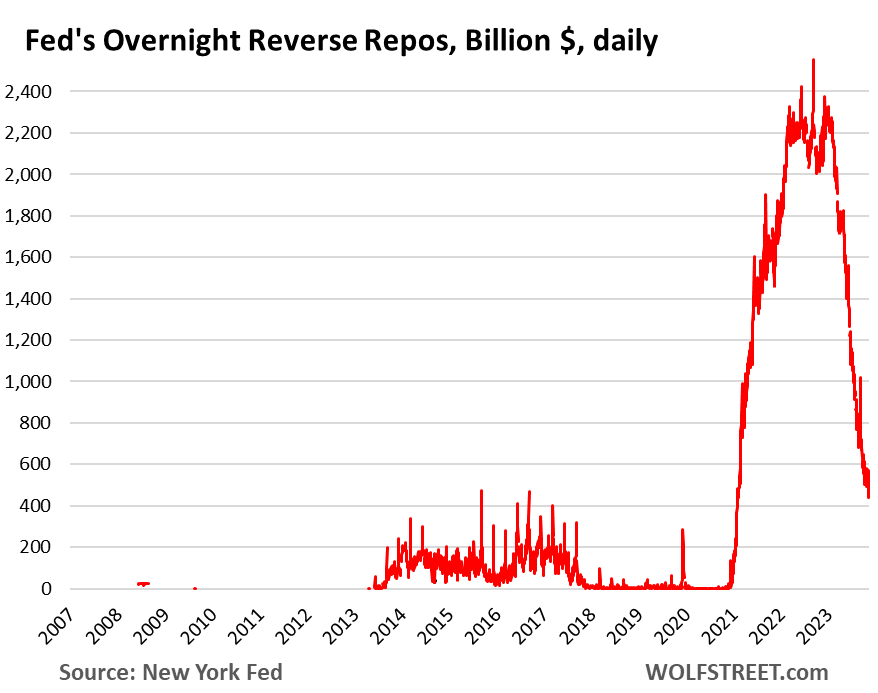

ON RRPs should go back to zero. These overnight reverse repurchase agreements signify “excess liquidity that financial market participants do not want,” Waller said in his speech. Logan confirmed in her speech; she expects them to be “drained.”

So the facility should go back to where it was, namely at or near zero. This means that close to $500 billion in QT would be required to wring out that “unwanted” excess liquidity.

MBS should “go to zero,” Waller said. This means that even after the Fed ends QT sometime in the future, MBS should continue to run off via the pass-through principal payments as underlying mortgages are paid off (sale of the home or refi), or are paid down (mortgage payments). “I believe it is important to see a continued reduction in these holdings,” Waller said. After QT ends, the MBS that run off would then be replaced with Treasury securities.

The Fed already did this before. After it ended QT-1 in the summer of 2019, MBS continued to run off the balance sheet and were replaced by Treasury securities until the pandemic QE began in March 2020 (our comment and chart of this period).

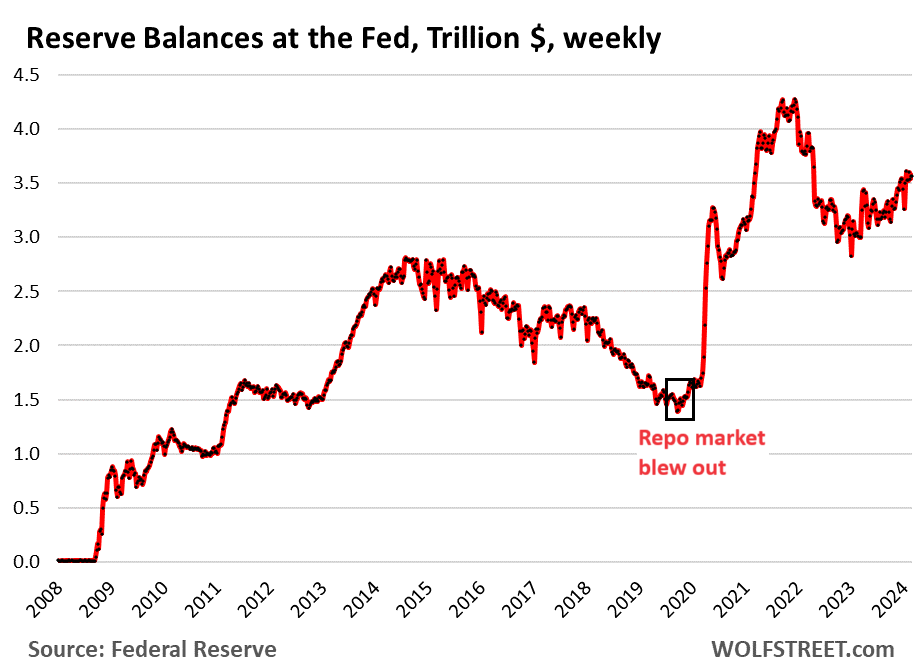

Reserves should drop after ON RRPs vanish. Reserves are cash that banks put on deposit at the Fed and represent bank liquidity. They could drop a lot because they’re essentially back to where they had been before QT started and have not absorbed any QT yet. QT was absorbed so far by ON RRPs.

During QT-1, reserves dropped a little below $1.5 trillion, which caused banks to stop lending to the repo market, which caused the repo market to blow out in September 2019 (black box in the chart below). So this was a sign that reserves were no longer “ample,” that they had been drawn down too far.

What does “ample” even mean: “The word ‘ample’ suggests comfortably but efficiently meeting banks’ demand,” Logan said. “The Fed’s operating regime is intended to supply ample reserves to banks—but only ample reserves and not more than that,” she said. But “the ample level of reserves is unknown,” she said.

The new Standing Repo Facility “may allow banks to lower the level of reserves below what reserves would be without the facility,” Waller said. The SRF prevents the repo market from blowing out even if reserves drop too far.

The Fed had an SRF through 2008. It was used to deal with market issues, including during 9/11 when markets were shut down. Repos mature within a relatively short term, such as within a day or within a week, and if they’re not rolled over, they vanish from the balance sheet and don’t get stuck on the balance sheet for years or decades like QE assets.

But in 2009, the Fed shut down its SRF because it wasn’t needed amid QE at the time. Then the Fed didn’t revive the SRF when QT-1 started in 2017, and in September 2019, the repo market blew out. So the Fed revived its SRF in July 2021 in preparation for QT-2.

The SRF “may provide a signal for when reserves are getting close to ample,” Waller said because the repo market will then make use of the facility, indicating that reserves had dropped so far that banks were no longer providing the liquidity. No one knows where this level is, but the SRF may “provide the signal.”

Slowing QT “can reduce the risk of an accident that would require us to stop too soon,” Logan said. The slowing QT “will occur when the Committee makes a decision to do so,” Waller said.

Slowing QT when the balance sheet drops to near $7.1 trillion? “After the ON RRP is drained, asset runoff will reduce reserves 1-for-1, all else equal. In this environment, moving more slowly can reduce the risk of an accident that would require us to stop too soon,” Logan said.

Logan suggests that as ON RRPs get drained to very low levels – “when ON RRP balances approach zero” as she’d said in her January 6 speech – it would be time to slow QT.

To get ON RRPs to zero, QT would need to progress by roughly another $500 billion, which would bring the balance sheet to about $7.1 trillion. In other words, as the balance sheet approaches the $6 trillion handle, it’s time to slow QT to avoid an accident that could end QT prematurely.

“Slower runoff, therefore, is a way to approach the ample point more gradually, allowing banks to redistribute funds and the FOMC to carefully judge when we have gone far enough,” Logan said. “This strategy will mitigate the risk of undesired liquidity stresses from QT.”

Slowing “doesn’t mean stopping”; it would allow the Fed to “get to a smaller balance sheet.” “I want to emphasize that slowing, to me, doesn’t mean stopping,” Logan said. “In fact, I believe that proceeding more gradually may allow the Fed to eventually get to a smaller balance sheet by providing banks with more time to adjust.”

The pace of QT is independent from interest rate decisions. The timing of slowing QT “will be independent of any changes to the policy rate target,” Waller said.

“Balance sheet plans are about getting liquidity levels right and approaching ‘ample’ at the correct speed. They do not imply anything about the stance of interest rate policy, which is focused on influencing the macroeconomy and achieving our dual mandate,” Waller said.

Short-term T-bills should replace a big chunk of Treasury notes and bonds. “I would like to see a shift in Treasury holdings toward a larger share of shorter-dated Treasury securities,” Waller said. “Prior to the Global Financial Crisis, we held approximately one-third of our portfolio in Treasury bills. Today, bills are less than 5% of our Treasury holdings and less than 3% of our total securities holdings,” he said.

Future QE could then just be an operation twist without increasing the balance sheet. Wow. “Moving toward more Treasury bills … could also assist a future asset purchase program because we could let the short-term securities roll off the portfolio and not increase the balance sheet,” Waller said. I mean, WOW! And he added: “This is an issue the FOMC will need to decide in the next couple of years.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Howdy Folks. Pretty much over my head, guess I am too stupid to understand, so, Operation Twist leaves who hanging out to dry????

“Operation Twist leaves who hanging out to dry????”

The QE mongers.

You need to read at least the whole paragraph, where it says:

“…a future asset purchase program because we could let the short-term securities [T-bills] roll off the portfolio and not increase the balance sheet,” Waller said.

Instead of buying long-term securities and increasing the balance sheet, the Fed would buy long-term securities and shed short-term securities in equal amounts and therefore not change the size of the balance sheet.

Howdy Lone Wolf. You are by far the best teacher I ever had. Will continue to try and understand what all the FED really does.

Do you have that backwards?

No. You need to read the entire article, including the part about why they would INCREASE the share of T-bills so that they would have enough T-bills to shed if they have an emergency where they need to buy long-term securities, while shedding T-bills to keep the balance sheet unchanged.

I did but I’m confused then about how the would shed THOSE long term securities once the time came.

I think the idea is that by shifting their balance sheet towards longer duration treasuries away from shorter duration tbills during times of stress, they could bring down long-term yields to support the financial system WITHOUT having to increase the overall size of the balance sheet?

I understood it like below.

Lets say FED balance sheet is 7 trillions. For simplicity purpose they have 3 Trillions in Bills and 2 in Notes and Bonds. Remaining 2 in other categories.

If FED wants to do another QE (lets say amount 1 Trillion). They will let go 1 Trillion in Bills by not renewing them and instead buy 1 Trillion in Notes and Bonds. FED buying Notes and Bonds will bring down long term rates and it will relax the financial conditions. But in this approach FED balance sheet remained same. If there is another need for QE means FED funds rate also will be down. So short term rates down too.

Well, this approach better than what they did in prior QE. But first and foremost they first need to bring down the Balance sheet now. It is like a Himalayan blunder now. That is now more important. If they had did good QT-1 execution, we didn’t have this mess.

Having smaller balance sheet and higher rates makes their tools more effective in recession times. Effective is relative. They have only couple of tools available.

SRK,

In this instance, you are the great teacher, I think. That makes perfect sense.

I probably could have figured it out if I read the GDF article three more times, but it’s early and I appreciate being spoon-fed.

I could be wrong, but I think Wolf already sniffed much of this in his Nov 1, 2023 post (Tsunami of Treasury…..). Complicated stuff.

Wow! (is correct). Aside from the focus on non-depository bank loans issuance/rates…it’s clear to me that this has to be driven in some respects by the Federal deficit and Yellen’s shift to shorter term securities.

Yeah, the normalization of monetary policy from a radical monetarist experiment can not be expected to be perfect.

When I stop and remember the specter of unemployment. I find myself in the camp, that the Fed is finally malfunctioning in a constructive manner.

I think to myself, what a wonderful world.

but given the massive size of the current bond holdings, are there not abundant longer dated bonds that are about to mature anyway such that new purchases of long bonds would not increase the balance sheet? seems like they should already have a good ladder of bonds since QE has been going on for 16 years.

Wolf, in the posting there is reference to accidents the Fed might have to respond to. Can you elaborate on what accidents are in this case? Would it be something the fed would cause or is it more likely they have to respond to irresponsible activity by the congress, the administration, wall street toddlers, or other actors in the world?

The repo market blowout in 2019 was an “accident” that the Fed was not prepared for and which came in reaction to QT. The idea is to prevent those accidents by slowing QT and by having the SRF on standby so that the Fed doesn’t need to respond to any accidents and can just keep QT on track.

Two childhood analogies come to mind:

1. The Cat In the Hat Comes Back – with the pink bathtub ring. Clean it up, and it’s flicked into another problem. Clean up that problem and the pink stain is elsewhere…ad if inifinitum. Only Dr. Seuss’ imagination and inventiveness could end the cycle….

2. Squeezing a water balloon between one’s fingers. First squeeze bulges here, second somewhere else, third still elsewhere. At some unknown squeeze, the balloon bursts.

Childish analogies with very adult consequences.

Well, they said that they need an obese balance sheet so that they can control the free markets.

Where did they say that?

I think you heard wrong. You just substituted what you wanted to hear for what they actually said.

“I would like to see a shift in Treasury holdings toward a larger share of shorter-dated Treasury securities”

To me, this sounds like a FEd guy who knows higher for WAY longer is the regime that markets just can’t seem to admit what lies ahead.

Locking in higher, long-term yields sounds like a very bad idea for interest expense as we move forward.

I think the Fed should have laid this out years ago. Likely exit plans should be known and communicated BEFORE stimulus is put in. The Fed doesn’t know what will happen in the future, but if they don’t a have a contemplated exit plan and time frame that is logical enough to be communicated, one must seriously question whether the interventions are doing more damage than good.

The Fed still hasn’t provided an adequate explanation of what they were trying to accomplish by buying MBS in the first place. What was the rational that led them down that path? The results of that move appear very bad.

In fairness, a dollar of printed money is a dollar of printed money. In the sense that agency MBS is guaranteed by the U.S., is it any worse than buying 10 or 30 year treasuries?

I see the problem as having printed way too much money, not what specific assets they held.

The MBS purchases specifically subsidized mortgage financing at a time when housing prices were already skyrocketing. It needs explanation. The Fed should not be buying any assets other than treasuries to minimize intrusion on market forces.

It was a venture into the long end of the yield curve. They shouldn’t be buying long term assets because it distorts long term planning. It’s deep and unnecessary intervention. Do we want the Fed dictate our future, 30 years in advance, or do we want supply and demand to dictate as it unfolds?

I agree with you, I’m just saying that I don’t think buying MBS is a priori worse than buying 10 or 30 year bonds. They’re both bad, and they did both. Had they bought no MBS but an equivalent dollar amount of 10 year treasuries, I think it would have led to the same distortions of the market.

Einhal your point of its an Asset they bought. Does it matter which type?

It matters. If those Home owners wanted to get the Mortgage they should have gone in Open Market and got it. Like any other Home buyer.

If you see the MBS bought by FED are Govt agencies underwritten and Tax-payers are on hook for those. Many people who could not get Mortgage from traditional routes, Govt got involved.

Whether Govt should get involved in housing is much bigger debate. But my point is FED should not get directly involved by buying MBS. Let Govt assisted borrow like anyone else.

Even FED knows they made a mistake in this. That’s why now they are saying they should NOT own MBS. That’s what Waller is saying.

They were trying to avoid Housing Bust 2 before it had a chance to happen, and boy did they ever. In the process they screwed up the housing market, bi time, for at least five years.

SRK, it doesn’t. Money is fungible. Had they purchased treasuries of equivalent duration, institutional money looking for government guaranteed yields would have instead bought the MBS, driving those yields down. There’s no free lunch.

MBS are slightly less liquid as the government guarantee is indirect, and there are other subtle differences as well, such as variable repayment stream. Some institutions place higher restrictions on MBS purchases.

Distinctions between MBS and LT treasuries aside, my key point is that MBS is LT paper and the total allocation of LT paper in the market is relatively small and getting smaller, so the Fed holding 30% of MBS is significant to the LT market. Who TF wants can lock in for 30 years on anything when a monetary “emergency” is deemed to exist every 5-10 years?

These days, people talk more about “monetary cycles” than business cycles because the Fed drives and distorts markets now. The natural laws of supply and demand have been suppressed. As long as this continues, moral hazards, inefficiencies, and speculations on things like stocks, Bitcoin and residential RE will run wild.

Agency MBS were not guaranteed by US prior to the 2008 crisis. One could see that by looking at the actual docs. But apparently MBS buyers did no due diligence.

The Federal Reserve bought up MBS contrary to the law at the time. FedGov made it legal afterwards and formalized the guarantee as part of the crisis response.

Now the guarantee is enshrined in the system but it’s just causing more problems, such as unaffordable houses traded as casino chips by speculators who think houses are an investment. Probably some are the same illiterates who thought MBS were guaranteed.

There should be no MBS guarantees by FedGov, and Fannie and Freddie should be re-privatized.

For the sake of housing affordability, U.S. Government needs to stop trying to be a lender or guarantee loans. The subsidies just make inflation worse.

Government intervention was previously guaranteed when Congress turned the thrifts into banks.

I agree completely. Everything the government and Fed did since 2009 with regard to housing and mortgages has just made things worse. They need to aggressively let MBS roll off (no monthly cap at all?) and make it very clear they will only deal in US debt from now on. Maybe Congress needs to tweak the NB charter a bit.

Housing will eventually find its true value in FRNs based on supply and demand. I think the prices may just stay flat from 2020 through 2030 to work off this distortion and as wages inflate 3-5% a year to catch up. The next generation is basically screwed in housing for a decade because of all these MBS shenanigans. Mortgages should never have dropped under about 5% which would have kept prices 20% or so lower over the last few years.

Instead they rent and wait for their income to catch up.

Can you call it a plan when you are making it up as you go?

In fairness, there has to be an element of flexibility involved. That looks like there’s no plan — but really it’s a managed plan. Meaning it incorporates twists and turns as it goes.

It’s not a plan. It’s a reaction to past events. The FED is a reactionary organization.

For AA:

Correcta Mundo old boy!!!

And EXACTLY the same of the CONgresses of the USA and individual states. We can WISH as much as we might for prescience for FRB, etc., but it will never happen until we have an education system that includes at least equal emphasis on ”Psycho-Spiritual Ability” development as well as the development of intellectual ability.

The obvious play is too stay in short term treasure securities and wait for the reckoning between the asset prices and affordability by the only ones that matter.

The poor people, the 89 pct that are responsible for the reputation that America is an egalitarian society.

I’m not sure I understand or agree with your proposal for how to stop the tilt towards the speculators, the big traders, and the rich, but I do agree on the crying need to stop plundering the poor and middle class to support them. The assault on ordinary Americans has been brazen and sustained – and they kept on doing it for little other reason than because they could get away with it.

Agree w ur comment gp, and will only suggest MAjor contrast with ”elites” attitudes after WW2, when they, ( in this case the rich and richer they ) DID all they could do to support the rise of the working folks who they understood WON the war. and saved all their assets, not to mention their asses, eh?

Since then, NOT so much, and here we are in the 2020s,,, with the elites once again at almost the same exact place as was the case in the 1920s.

FAITH AND BEGORRA,,, EH???

“… but I do agree on the crying need to stop plundering the poor and middle class to support them.”

This.

It is more difficult to coordinate insider theft, when you communicate to

outsiders what you are doing ——— so you (the FED) don’t. The MBS were purchased to support MBS prices and to support housing prices so the banks and other parties could get out of under-water assets.

It was a bailout.

“Short-term T-bills should replace a big chunk of Treasury notes and bonds“

So the gov new debt being issued as t bills is going to be monetized by the above action of fed? Also there by driving the t bill yield lower?

Concerned_guy,

Nonsense. Quit fantasizing about this stuff. T-bills used to be 1/3 of the Fed’s securities. Now they’re just 3%. They’re going back to how it was before 2008 QE.

Wolf, what could be a good reason for FED to ever want to purchase longer dated Treasury? How does the Fed’s ownership of long duration Ts help the economy or the financial system when SRF is in place?

Is this some sort of a backdoor yield curve control? Why not let the long term rates be decided by the markets?

Thanks in advance

Doesn’t there need to be some context as a 1/3 of 900 billion pre 2008 is a significantly different number that 1/3 of 7+ trillion.

Here is the context: Fed Treasury securities as percent of publicly traded Treasury securities (total amount of Treasuries in the Treasury market):

What impact would the implications of Wolf’s last paragraph, the one with the WOWs, have on Treasury bill rates? Right now they are about 5.4%.

You can’t assess the impact on Tbills in isolation, because Operation Twist doesn’t occur in a vacuum.

OT would occur during times of financial stress. So yes, OT increases the supply of Tbills to the market (all else being equal), but during times of financial stress liquidity is rushing towards safe, short-term assets like Tbills. In fact, that’s the problem. Liquidity is moving from long-term, less liquid assets towards short-term, more liquid assets.

This is why OT makes so much sense. It “adds” short-term, liquid assets to the market at a time of high demand for those assets, while providing demand to long-term, less liquid assets at a time when demand for those assets is shrinking.

Yes, perhaps. My view is the Fed’s balance sheet is obese. The asset markets are not setting records because the Fed has throttled liquidity.

OK, they have no choice but to fund the Treasury issuance which is so massive that the Fed is not in control.

T-bills yields are largely bracketed by the Fed’s five policy rates, esp. the 1-6 months. That won’t change. But long-term yield might rise because the Fed is stepping further away from the table.

“But long-term yield might rise because the Fed is stepping further away from the table”

Praise Jesus. It’s about time.

That might affect the housing market. Higher for longer indeed. It would tame the juicier returns that we see in short t bills.

Thanks.

Meanwhile Congress gets ready to pass new tax laws which will mostly benefit companies and shareholders will no real guaranteed benefits to society. These will likely just grow the deficit that much more by reducing revenues further.

It’s interesting to see all that is going on but clearly not seeing how the average person benefits. Sure, wage gains have been great recently especially after not much movement for a long time but those will be pulled back first chance they are able or of course as we see will just get pushed onto consumers.

I feel your angst about the future of what the 535 publicly, paid lobbyists in Congress will continue to strangle the golden goose.

The House passed it, the Senate is voting soon and Biden has pledged to sign it. Significant handouts for private equity, big business and others just around the corner. Of course it is being pushed as a bill to get children out of poverty but that shouldn’t be the case to start with in a country with our wealth and of course it is temporary. It is of course an election year….

You’re referring to the Tax Relief for American Families and Workers Act, the one that combines business tax cuts with expanding the Child Tax Credit?

If so, that bill has been stuck in the Senate for over a month because some senators have concerns about its cost.

Even if it passes, its cost pales in comparison to 2025, when the 2017 tax reform expires. Only divided government going into next year would produce any semblance of fiscal sanity.

The wage gains look to be permanent. The question is whether they will outpace inflation or not. If your salary increases by 3% and inflation is pegged at 7.5%, you’re still losing money at the end of the day.

I suspect wage gains will slightly edge out inflation, but no more.

Sure wages stay up but that doesnt mean hours can’t be cut, benefits reduced or your job can’t just be eliminated or the higher paid person replaced with lower paid or automated. Massive sums are spent to prevent unionizing. Few people remember once upon a time in the 1950s, despite racial and gender disparities, membership was 1/3 of the workforce. Unionizing of course helps but is only one part of the solution. That period of history as well as the 60s has been rewritten often by government agencies. Now the corporations mostly have taken on that role.

Not inflation the real inflation rate. Up in Canada wage gains are coming in at 5.4 percent and they tell the public the inflation rate is 2.9 percent. Wage gains are a good gauge of the real inflation rate.

Wage gains are no indication of consumer price inflation. Wage gains are wage inflation. Sometimes wage inflation is lower than consumer price inflation; other times, it’s higher. In 2023 and into 2024, wage inflation was higher than consumer price inflation; but in 2021 and 2022, wage inflation was lower than consumer price inflation.

In the FED/Banker’s system, the “average person” is meant to be a worker/service provider and a debt slave.

Comments like that are a mixture of ridiculousness and sad. No one is “meant” to be any such thing. As if there’s some grand committee conspiring with premeditated plans to screw an economic class and create debt slaves. GMAFB.

The fact that you can’t figure it our doesn’t make it ridiculous. It does make it sad though.

Just to be clear about “Operation Twist”, is the idea as follows:

During normal times, they carry a balance sheet of mostly Tbills.

Then, during times of financial stress, they start buying long-dated treasury notes while allowing an equal amount of Tbills to mature. This allows the Fed to support the financial system (through lower long-term borrowing costs) while keeping the balance sheet the same size.

And then as things calm down, they allow the long-duration notes to mature while replacing them with an equal amount of Tbills, shifting the balance sheet back to mostly Tbills over time without changing the size of the balance sheet.

This makes sense but seems like financial stress could be a reason to lower interest rates and thus yields might drop on long term, thus potentially inflating other things further. Lower yields better for US government but not for people who want safe income generating investments.

Limited knowledge about this, but the same thought initially crossed my mind, and I wondered if this Fed strategy announcement drove the sudden Treasury yield drops this past Friday.

Johnny5,

Yes, that’s what it looks like to me.

“And then as things calm down, they allow the long-duration notes to mature”

But how long will that take…30 years? They just traded out a huge chunk of T-bills for bonds and then expect a couple few decades of calm to let their balance sheet to sort itself out? What do they do if there’s more trouble in the meantime?

Like I said before, just QE with a new twist.

QE 2.0

ChS-

That’s my question, too.

– Fast liquidity injections

– Glacial liquidity drains

– Years of manipulated interest rates

– Invent new policy experiments as necessary

(I’m so old, I remember when liquidity policy didn’t even include the treasury markets: “Lend freely, at a penalty rate, against good collateral.”)

Just looking at the current situation your scenario certainly seems to be the case, eh? Spikes during crises, long slow QT.

It sounds optimistic to me that relying on the “situation to stabilize” quickly will suddenly be the way things operate.

The comment above about how we should have been informed of their exit plan before QT is a tad credulous too. These guys are experimenting as they go. How else could it be with as complicated a system as the economy? What’s that saying Everybody’s got a plan until they get punched in the mouth? ;-)

Indeed, I’m deeply skeptical of any Federal Reserve policy designed to buy time in reducing accommodation.

It’s more like kicking the can down the road and when that recession / black swan event (eg COVID) hits, suddenly accommodation is at a permanently high plateau because it wasn’t properly reduced when the economy could withstand it.

Wall Street knows this, which is why investors are so giddy. The important part is the “slowing QE” part which is immediate & guaranteed, not the “possible lower terminal balance sheet size” part which is further into the future & could be canceled at a moment’s notice if the economy sputters.

And, of course, there will always be a new emergency (read: event that causes wealthy people to miss yacht payments in significant numbers), “requiring” the Fed to ride to the rescue with massive accomodation, long before things have a chance to calm down on the kind of timeline that matters for long bonds.

The first emergency was the Global Financial Crisis in 2008, with 15 million unemployed in the US, and the second emergency was the pandemic in 2020 with 23 million unemployed in the US. Hardly related to “missing yacht payments.” This dumb stuff really gets old.

Wolf, sure, but every “rescue package” or “stimulus” somehow manages to save the stock market too (and in some cases, primarily)

Sure, and the Fed should have chosen a different approach than expanding its balance sheet like that. But those were serious effing events, not some rich people missing yacht payments.

What were the emergencies that made QE2 and QE3 “necessary”?

Wolf,

Do you think there is increasing recognition that the Fed will be blamed for any inflation resurgences and they are therefore trying to get the balance sheet and all of their internal policies in a pre-2008 posture?

With all of Powell’s talk about Volcker, if inflation starts raging again, I think there is a real risk the Federal Reserve Act might get amended and put the Treasury Dept in charge of things or something similar (which would be a disaster).

If the Fed actually steps back from the Financial Crisis playbook to something more traditional, this would have huge implications for asset prices.

How do you see this playing out?

It doesn’t sound like any officials are overly concerned about an inflation resurgence right now. Many of the FOMC policymakers on the speaking circuit right now are still talking about potential rate cuts later this year. This includes Bostic, Goolsbee, and Mester just last week. Mester specifically said inflation data is notoriously noisy/volatile and it was important not to overreact to one month of data.

How would the Treasury handle inflation? This is the same Treasury that’s increasing the national debt at a rate of $1 trillion every 3-4 months, and requires authority from an often-gridlocked Congress to take certain actions?

Bitcoin, gold, stock markets are all skyrocketing on excess liquidity. Crazy moves. They need to drain it now.

Liquidity has been draining for years and will continue. That is the point of the article

https://wolfstreet.com/2023/11/01/tsunami-of-treasury-issuance-shifts-from-longer-term-debt-to-short-term-t-bills-and-2-year-notes-amid-intense-navel-gazing-about-the-spike-in-10-year-yields/

So the yield curve is to never go back in line then?

If a greater share of the balance sheet is shifted into T-bills, which is what Waller says he wants to see, the Fed will therefore reduce its holdings of long-term securities, which would push up longer-term yields and steepen the yield curve.

And create the next financial crisis which will allow them to buy long duration and runoff T-bills, rinse, repeat.

Is there a way to front run this?? haha… ;)

It’s all good, man…

Thankyou Wolf. Only place to get any consistent sense. This balance sheet reduction via QT appears to be their priority for the Fed, rather than concerning themselves so much with interest rate levels. Perhaps this is why Fed officials sometimes give comments that appear to give fuel for the dovish angle. I know Wolf says that the media twist their words to suit their narrative, but I’m thinking more and more that the Fed are allowing this, even abetting this so as to buy time for the balance sheet to be reduced further….

Despite all the hikes and QT, markets are at ATH. Probably this is where the Fed gets its courage to even talk about going back to pre-2008 times. What happens if markets drop? Or can markets drop at all?

“about going back to pre-2008 times.”

I don’t know how much time I have wasted shooting down this BS over and over again.

READ THIS, it explains why:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

What I meant by ‘markets drop’ was a drop of 30% or more in a span of 1 year.

First 10 months of 2022 were about a 24% drop in the total stock market. So I don’t know what has you thinking such drops couldn’t happen anymore. That was just year before last.

I was asking would the Fed Speak change when you have market dropping like that.

I think that seems to be a reasonable bet just like a year ago when the collapse was more likely. A bet is a bet.

“”Future QE could then just be an operation twist without increasing the balance sheet.” Wow. ”

Under-effing-statement. Future QE? Say not so.

The other currency sponsors are continuing QE

The Fed would be irresponsible, at this point, to take a moral stance to defend the value of the dollar when so many are trying to redefine the relationship.

“The other currency sponsors are continuing QE”

BS. With the exception of Japan, they’re ALL doing QT, and massively so, including the ECB which unwound €2 trillion.

The telegraph

4 March 2024

“Japans’ government is reportedly considering declaring a formal end to its battle against deflation in a move that paves the way for its central bank to cease negative interest rates for the first time in eight years.

However, inflation has exceeded the Bank of Japan’s 2pc target for more than a year and its government is considering formally calling an end to deflation in the wake of rising prices, according to Kyodo news.”

Haha,

In the previous ECB article you called me a fool when I said that even the ECB is ahead of the Fed in QT

I don’t know if you read the articles or just write the nonsense that is born in your head.

Don’t think the Fed discussion on QT and future QE had any impact on the drop of the 10 year Friday . If any thing holding fewer long term bonds and not being a buyer of last resort would increase rates with less demand from other sources

Then what was the actual event/announcement that caused yields to plummet on Friday?

There was a report on Friday that someone had observed Powell leaving his home with a 3-piece suit on instead of his characteristic 2-piece suit. This of course was an unconscious signal from Powell that there would be at least three rate cuts in the 2nd half of the year instead of two.

Lol. Just wait for him to wear a bow tie!

JeffD,

“….caused yields to plummet on Friday?”

This is such BS. The 10-year yield edged down 6 basis points, from 4.25% to 4.19%, normal for a relatively calm day.

The ISM manufacturing PMI showed the manufacturing industry was in contraction. That’s what caused yields to drop.

The last several months have followed a relatively predictable cycle: strong jobs numbers cause yields to rise, then weak manufacturing data causes yields to fall. In practice, policymakers should weigh employment numbers far more heavily than manufacturing (the U.S. economy is predominantly a services economy), but because of the Federal Reserve’s easing bias, bond investors tend to focus a lot more on “bad” economic data than everything else indicating the economy is still holding strong.

Probably the article in Fortune, with the apparently well qualified professor at Wharton IIRC emphasizing the unusual DEBT load current at about $34TTs IMHO JD,,,

Just guessing we suppose, eh?

Clearly, as our WR has demonstrated, ”Markets” are a function of psychological factors AT least, and usually more than realistic factors of supply and demand as they should be.

SO, perhaps, WE, in this case the investing WE, should be asking if such psych factors are in play as much as or more than with whatever we are interested in, rather than any rational basis, eh???

Well, maybe. I tend to think that the UST 10 year is the cleanest dirty shirt. Being bought up by holders of other currencies, that may or may not, be worthless tomorrow.

So what kind of buying and selling will need to happen between the term structure they have now and the day they have the new term structure that they want? What is the path forward? You can’t get T bills from 3% to over 20% without actively selling long bonds and buying T-bills, steepening the yield curve significantly by pulling yields up on the long end *and* puliing yields down on the short end, unless this rebalancing happens over a 10+ year time frame, right? Or am I missing something? If I’m not missing something, do we really have 10 years to let this play out, given where inflation is at *today*?

JeffD-

I posted this quote a few months back, but it deals pretty directly with your musings, I think, and bears repeating:

“The greatest of all secular [bond] bear markets, which began in April of 1946, and probably ended in September 1981, carried prime long American corporate bond yield from their lowest recorded yields to their highest. The yield index rose from 2.46% to 15.49% for seasoned prime issues and up to 16.5% (industrials) and 18.0% (utilities) for high quality new issues. This was a yield increase of 1303 basis points on seasoned issues, and 1981 peak yields were more than six times greater than 1946 low yields. The great bear market lasted some thirty-five years, by far the longest duration for a bear bond market in U.S. history. If a constant maturity thirty-year 2 1/2% bond had been available throughout this second bear market of the century, its price would have declined from 101 in 1946 to 17 in 1981, or 83%. In contrast , in the first bear bond market of the century, 1899 to 1920, the same bond would have declined 35% in price. The recent bear bond market seemed to have much more social and economic significance than that of all earlier bear bond markets. In all the others, bond yields stayed within the traditional band that had prevailed for centuries. This time they broke decisively out of that band.”

— Sydney Homer and Richard Sylla, A History of Interest Rates

Of course history never repeats verbatim. The period Homer and Sylla discuss followed WWI and WWII and their horrible disfigurements; but it’s interesting that the federal debt to GDP was actually slightly LESS then, even following the wars, than it is today. Other systemic debt in the US was certainly lower.

At any rate, it seems entirely defensible to assume that THIS bond bear market, when it gets up its head of steam, could extend not just into years, but into several decades. (As Wolf aptly points out, perdition doesn’t arrive directly, or something to that effect).

IMHO

In 1952, the lowest federal income tax bracket was 22.2% and the highest tax bracket was 92%. I’m guessing that higer taxation right after WW2 had alot to do with reducing debt to GDP, even if people were able to shelter a good portion of their income from these high tax rates. Sadly, politicians no longer concern themselves with fiscal discipline, as recent CBO projections have shown. Keeping the US afloat as a going concern is just too bothersome. Lol!

Lots of pontificating from fed speakers — but I still think they’ll fold like cheap suits under public pressure, when folks start screaming about their paper wealth declining.

Let’s see what happens when we start getting price discovery on the big asset classes — commercial real estate…. and residential real estate as job losses creep up with 6%+ mortgages.

Let’s see how much QT and SRF use they’ll explore when small and medium regional banks are imploding.

These goons provoked asset speculation for over a decade, and have no idea how to get out of it…. they’re just hoping they can sing-and-dance about “balance sheet normalization” long enough for deficit spending and inflation to make asset prices less insane.

I hope all the QE advocates at central banks around the world lie awake at night and think “what have I done”

re: “These goons provoked asset speculation for over a decade,”

Waller: “when a central bank uses reserves to pay for government securities, it is decreasing the supply of these securities to private investors, which will bid up the price and lower the interest rate on government securities.”

Deliberately stoking asset prices was a monetary policy blunder. In the circular flow of income, you need higher and firmer real rates of interest for saver-holders. Then monetary savings need expeditiously activated into real investment outlets, aka, in the U.S. Golden Age in Capitalism.

I’ll add that all of this was known from the very start. The consequences were inevitable. Remedial actions were deferred and problems were allowed to grow in scope and magnitude.

Where does that leave us? With a huge monetary governance problem?

The rest of the world only had to look to Japan to see the damage zero interest rate policy would do. They enacted the same thing as Japan and got the exact same result. Now the entire world is much poorer.

“They enacted the same thing as Japan and got the exact same result.”

You mean they enacted the same thing and got the exact opposite result.

Japan — no inflation for decades

US — instant inflation

Japan — flat housing prices

US — rocketing housing prices

Japan — flat stock market

US — ATHs in a matter of months

“when folks start screaming about their paper wealth declining.”

————————————————————–

they have been screaming about their paper wealth, the lost purchasing power of the dollar and their savings, for some time now ……

the little folks don’t matter as much as the big people

….written on the chalkboard at a meeting in the Eccles bldg, engraved in every attendees heart – “how do WE stay solvent with credibility and avoid pitchforks outside before the(our) whole system collapses”.

Hahahaahha. No, it’s a white board, and some wise ass wrote it in permanent marker.

Sheesh. Everyone’s out to get us…

The problem is that the printed money after being disbursed comes back to the Fed as central bank as a deposit on which they must pay interest. The interest should come from the government but its considered a “deferred asset”. So the fed has to pay interest which is yet more money printing. The whole thing is just made up and will end with the dollar at zero. Its almost not worth reading charts of numbers that are entirely arbitrary when you can see rapid price inflation in every aspect of life.

You can see if you are on this site, or any economic blog that everybody knows the debasement is too rapid. The tragedy for the US with the pretense of following the “constitution” is that the most important part was “No State shall enter into any Treaty, Alliance, or Confederation; grant Letters of Marque and Reprisal; coin Money; emit Bills of Credit; make any Thing but gold and silver Coin a Tender in Payment of Debts;”

And as was appreciated at the time the whole country is now captive to the banking system. The one saving grace of the US monetary system is that so many Americans are in poverty they don’t have any opportunity to dump the dollar and thats what enables it to lumber mindlessly on. Yellen recently actively supports default on Russian treasuries.

The US is in no position to default.

I find it amazing that there is all the (entirely right) support for the gun lobby and associated rights but literally none for the founding principles of sound money.

@lord sunbeam, I think you are missing the entire point. How would the fed print gold when they need a fresh batch of qe, talf,tarp, cmbs, mbs, or strait treasury bond purchases?

Or if the markets need another batch of of liquidity injection, or two; daily, Then what? Free markets prevail again? Oh Lordy, can’t have any of that. Think of the dire consequences?

Yep.

Basing your whole economy on hiw much of a metal can be dug up out of the ground and put in a vault is the silliest thing ever.

Besides, an economy based on gold is just begging to be manipulated by its enemies. In recent history there have been attempts by private entities (mostly banks) to manipulate the price of gold. Now imagine what a nation state could do.

Why would anyone want to have an economy that could easily be driven into the ground by China?

There is a reason that almost every first and second world modern economy has a central bank with fiat currency.

Going back to a gold standard is dumber than going back to the horse drawn carriage as the primary means of transportation.

“And as was appreciated at the time the whole country is now captive to the banking system”

—————————————————–

one very large class is subservient to a small master class

cb-

“All animals are equal, but some animals are more equal than others.”

Seems to me if they raise rates markets drop and buy treasuries!?. Not raising rates and doing some fed yield curve conversion for price stability!?. Seems to me the Fed is going way too far. A monetary and fiscal war the cause here? Thanks Wolf now more complex than ever. One big experiment.

“Prior to the Global Financial Crisis, we held approximately one-third of our portfolio in Treasury bills. Today, bills are less than 5% of our Treasury holdings and less than 3% of our total securities holdings,” Waller said.

Sounds like the Fed has been practicing “mini” yield curve control without much pushback for years.

But… With treasury issuance hitting new records and govt interest expense expected to skyrocket over the next few years, it seems to me the Fed is going to be left with no choice but to eventually ramp up long-term treasury purchases again. Just a matter of time.

If the US budget deficits (as % of GDP) keeps running at almost twice its historical average though, I think there will be much more pushback if the Fed tries to run another mini-YCC program again, at least from certain segments of the market. Maybe the future “twist” program is meant to alleviate some of this anticipated pushback. However, given the absolute size of the deficits (and those are in “good” economic times”), I don’t see how a ‘twist’ operation on its own is gonna cut it next time the Fed is called upon to “rescue” the economy.

All fiscal sins lead to inflation. The Fed doesn’t have to buy any bonds. Inflation will take care of it. Inflation boosts tax receipts, which reduces the burden of the existing debt, wiping out its purchasing power over time. Inflation has been chosen by the government as the solution, it seems.

It’s a misunderstanding of inflation that causes people to say: “The Fed HAS to buy securities, it doesn’t have a choice.”

True, but maturing debt has to be rolled over. If current gargantuan deficits continue on top of the rollovers, the credit market will at some point demand to be fairly compensated for said future inflation risk. At that point, if the Fed doesn’t “help” the government, then the government might still have a big problem on its hand rolling over its debt and issuing new debt.

Currently the 10-year is at 4.2% on the assumption that a few years from now inflation is down to 2% and thereafter it’s sugar plums forever.

If $100 billion in maturing debt, whose purchasing power has plunged by 50%, is rolled over, it’s rolled over with $100 billion of new debt whose purchasing power has also plunged by 50%. That $100 billion won’t buy much anymore, and inflation-inflated tax receipts will be much bigger to pay for its interest. You see?

Yes, investors will eventually demand being compensated for this inflation via higher interest rates. But it won’t be much above the rate of inflation, and the purchasing power of the entire old and new principal gets devalued at the rate of inflation.

Inflation wipes out the burden of the debt at the expense of the debt holders. It’s NOT a good situation. but it does get rid of the burden of the debt. High inflation up to 17% was how the government got rid of the burden of the war debt in the late 1940s. Inflation is a well-known prescription to lighten the burden of the debt.

I understand what you’re saying, Wolf. The thing is that government might be able to play the game you describe over time if the budget deficit was say 3% of GDP, but instead, we’re dealing with something more than twice as much, and that’s during the supposedly good times!

Given how large the deficit is already as a share of the economy, if we have a recession we could easily see deficits well into the double digits. In my opinion, it’s going to be difficult for the government to raise those kinds of sums in an environment where there exists the threat of future inflation without ‘help’ from the central bank, including on the long end of the curve.

Wolf,

What’s your opinion on the possibilities/potential plans laid out by these two? I understand fine tuning QT as we move along, but why get into the giving signals on what future QE may look like? It makes it seem like they are laughing behind everyone’s back and doing a “wink wink” to certain groups.

Nunya-

Well-founded, widespread and healthy skepticism you express.

Here’s how a former Fed official sums it up:

“A fundamental characteristic of the United States is that its citizens have an enormous mistrust of concentration of power – political or financial.”

— Thomas Hoeneg, Back to the Business of Banking

That characteristic goes back to our founders, and rightly, to the founding circumstances.

You’re imagining things?

No, just wanted you to expand on your “wow” comments sprinkled in the article. I thought there was more there, guess not.

The Fed’s plan looks like keeping several types of weight-loss pills handy, instead of trying to eat nutritious food and exercise.

More like meth. They have done irreversible damage.

Easy to talk when most of the economic statistics are rosy. Wait until they get punched in the face by a market crash, volmageddon 2.0, or some such. Then we will see all these “plans” go out the window and new ones implemented to “save” the economy from the abyss.

Powell has been doing an exceptionally good job keeping the “means-of-payment” money supply in check. We will see the fruits of this effort in the last half of 2024.

The issue that concerns me most about the Fed’s ‘crisis planning’ is their seeming unconcern for the element of time. A financial crisis doesn’t creep up on you like a glacier; it’s more like a mugging on a New York City street corner – swift and deadly. Letting 30/60/90 day bills roll off could happen quickly, but wouldn’t the equivalent roll off of bonds and notes take years? Sounds great in theory, but in practice – with the Market breathing down their neck – wouldn’t the worthies of the Fed simply panic and do what they always do: print like the Devil is on their tail?

There were 12 years between financial crisis QE in 2008 and pandemic QE in 2020.

Over half ($2.4 trillion) of the Fed’s current holdings of Treasury notes and bonds ($4.0 trillion) will mature over the next five years. So if they don’t replace any of them, the Treasury notes and bonds on the balance sheet will be down to $1.6 trillion, which is way too low, given the liabilities of currency in circulation and the TGA, which are now combined over $3 trillion, which must be balanced by assets. So it really doesn’t take all that long to reduce the balance sheet to the minimum possible (the minimum is dictated by the externally-driven liabilities of currency in circulation and the TGA).

Wolf-

Have you presented a graph showing currency in circulation and TGA?

Going back 50 years would be interesting, though I expect there may have been structural changes along the way that would need some explaining and interpreting…

Yes, many times. All you have to do is my articles about the Fed’s balance sheet liabilities, for example here:

https://wolfstreet.com/2023/09/16/feds-balance-sheet-liabilities-rrps-plunge-reserves-rise-after-bank-panic-currency-in-circulation-dips-after-pandemic-spike-tga-gets-refilled/

I rarely go back 50 years in my charts because: 1. you cannot see ANY details of what happened over the past 12 months; 2. I generally no longer give a f**k about what happened 50 years ago because I’ve already seen it for 50 years. There are only rare occasions when I want to draw up a comparison to 50 years ago; and 3. the TGA was moved to the Fed in 2008, from the JPM (fear of banks collapsing and taking down the US government checking account?), and that’s how far the data goes back.

Thank you.

Wolf, is that why they’re going to buy bills? Because otherwise the bal sheet would get too low with notes/bonds/mbs continuing to roll off?

It seems like there’s plenty of demand for bills and oversupply isn’t an issue – Waller said that himself earlier in the speech.

Waller told you why they want to increase the share of T-bills. All you have to do is read that section in the article, and read the related comments here. Not repeating it.

Until rates fall near 0% on T-Bills? I was willing to hold some bills at that rate during the pandemic. I’m not sure I would do it again, and even if I did, I would only be willing to hold a lot less than before. I learned my lesson the hard way, and won’t be repeating my mistake. I’m guessing that would be even more so for foreign investors at this point.

Waller said he wants the SHARE (aka ratio, %) of bills to increase – which woud happen naturally given the runoff of stuff with duration from QT.

If they reduce the holding of notes & bonds, but keep the amount of bills the same, the ratio of bills to notes/bonds still goes up.

Your quote (not his) said REPLACING notes & bonds with bills – implyimg the purchase of bills.

So which is it? I re-read that section of the speach & your article multiple times and this isn’t clear.

JeffD: T-bill rates won’t go to 0% because the IORB and RRP rates create a floor.

MM,

The T-bills on the balance sheet are disappearing with QT and will be gone by July 2025. T-bills are used to fill in the gap of the roll-off cap. T-bills on the Fed’s balance sheet mature all the time and are replaced by the Fed buying new T-bills at auction, except those amounts that are used to fill the gap to the $60 billion cap. The section on T-bills here – heading: “The function of Treasury bills to steady the pace of QT” – explains this. So read the subsection on T-bills:

https://wolfstreet.com/2024/02/01/fed-balance-sheet-qt-1-34-trillion-from-peak-to-7-63-trillion-lowest-since-march-2021/

Then read the entire article on the Fed’s QT because it answers the core of your question about “replacing.”

In short, by “replace” we mean that the Fed buys at auction securities equal to the amount of those securities that matured that it wants to “replace,” rather than let roll off.

Currently, T-bills are already down to just $210 billion on the balance sheet, from $360 billion when QT started, and they will be down to $0 by July 2025, as part of QT. And then the Fed won’t have any T-bills unless it changes it system.

How can the Fed increase the % share and $ holdings of T-bills even as the balance sheet continues to decline?

During QT, when the Treasury runoff exceeds the $60 billion cap, instead of replacing the excess with notes and bonds, it could replace the excess with T-bills. For example, May is a huge month for Treasury maturities. $90 billion in notes and bonds will mature in May. Under the current system, with the current cap of $60 billion, the Fed would allow $60 billion to roll off without replacement, and it would buy $30 billion in new notes and bonds at auction, so that its Treasury holdings would drop by $60 billion in May, and not by $90 billion. But instead of replacing those $30 billion of notes and bonds with new notes and bonds, it could replace them with T-bills.

And for example, if in 2025, the Fed lowers the cap from $60 billion to $30 billion a month to slow the Treasury runoff, the excess of maturing securities would be larger that would have to be replaced, and instead of replacing them with new notes and bonds that it would buy at auction, it could replace them with T-bills that it would buy at auction.

In both of those examples, the Fed would increase the holdings and share of T-bills while the overall Treasury holdings would fall, and the holdings of notes and bonds would fall a lot faster.

How can the Fed increase the % share and $ holdings of T-bills in the future after QT ends and the balance sheet remains flat?

After QT ends and the balance sheet stays flat, the Fed would have to replace all maturing securities with new securities that it buys at auction to keep the balance sheet flat. The Fed could replace maturing notes and bonds with T-bills, which would lower its holdings of notes and bonds, and increase in equal amounts its holdings of T-bills, and the share of T-bills would rise, even as the balance sheet stays flat.

Waller’s actual quote which I still don’t quite understand…

“Moving toward more Treasury bills would shift the maturity structure more toward our policy rate—the overnight federal funds rate—and allow our income and expenses to rise and fall together as the FOMC increases and cuts the target range.”

Ok I get that a greater RATIO of bills on the bal sheet is good – but again, are they buying bills, or just comtinuing to let duration mature & roll off? If they are actually buying bills, why?

Thanks for the detailed explanation Wolf. Now I get it – I wasn’t thinking about rolloffs above the QT cap.

Really appreciate you taking the time to write that out.

Wolf — is the idea that the Fed will replace these maturing longer-dated securities with T-bills and in this way shift their portfolio to ST treasuries in the coming year(s)? Or do you have a different view on how & over what period of time Waller thinks the FED may/will shift its portfolio composition.

Thanks

This is the first time that anyone at the Fed laid this out. So I think when the Fed announces its official QT modification plan sometime this year, it may get spelled out in greater detail. Or this may be something that will be in the future plan to be released even later as to what happens after QT ends. The Fed made a similar change in 2019, when it announced that it would end QT, but would let MBS continue to run off and replace them with Treasuries, which is what it did until March 2020.

Unfortunately, fed officials and their plans are about as reliable as war plans printed in the pentagon after years of computer simulation.

Once the first bullet is fired everything changes.

Yes, the curve needs to normalize……because of demographic changes……but the point is……by the time this fed (if ever) gets control of inflation…..our currency will be depreciated by 50% over 10 years.

They are violating their mandate……and the cabal is rewarding them for it.

My guess is the war simulations are valid as they have been many times over which have proven over and over again. That said, it doesn’t factor in the other factors such as neocolonialism and imperialism in order to uphold US economic interests. We overthrow legally elected governments or support dictators in equal measure to anything else we do. Ironically tax payers foot the bill not those that reap the spoils, whether it be ensuring a society doesn’t industrialize and thus being able to exploit natural resources and low cost labor and compete where most profit is made, or simply destabilizing an area of the world based on deeply ingrained ideas around orientalism or exporting via cultural imperialism (McDonalds, Hollywood, and so on). Fascinating topics which seem unrelated but fundamental to understanding the economic picture.

The Fed is saying all the damage caused by QE will never be corrected and hopefully America won’t end up a basket case like Japan. That’s the way I read Powell’s speech.

They have permanently altered the landscape of the US, the results being very good for the billionaire/hundred millionaire class, and very bad for working classes and the poor. It was a giant reverse-Robinhood operation, stealing from the poor to give to the wealthy.

Logan said: “The Fed’s operating regime is intended to supply ample reserves to banks ”

———————————————-

Does the Fed’s operating regime supply reserves to banks?

Reserve requirements are zero, aren’t they?

I thought banks were the driver of what portion of their cash they chose to hold on deposit as reserves at the FED.

The FED can offer only incentives through the interest rates they choose to pay on bank reserves.

1. “Does the Fed’s operating regime supply reserves to banks?”

Banks must keep a portion of their cash in their reserve accounts at the Fed because that’s how banks pay each other every day. Every day, banks receive from and pay to other banks huge amounts as part of their normal transactions. When you make a mortgage payment, the money flows from your bank to the recipient’s bank via their reserve accounts. So that requires some reserve balances by all banks.

Banks must have enough in their reserve accounts to be able to meet liquidity demands. Required reserves forced banks to do that; now regulations put the decisions on the banks’ back. This is called the “lowest comfortable level of reserves.” Banks collapse when they don’t have enough liquidity (see SVB). So that’s a pretty stiff penalty for screwing this up.

2. “The FED can offer only incentives through the interest rates they choose to pay on bank reserves.”

The interest on reserves (IOR) is an incentive for banks to put additional cash on deposit at the Fed, instead of buying T-bills. Via this mechanism, the IOR keeps a floor under T-bill yields because banks are not as willing to buy T-bills when T-bill yields fall below the IOR. The IOR is one of the five Fed policy rates.

Policy rates:

https://wolfstreet.com/2024/01/31/wow-feds-statement-pushes-back-against-rate-cut-mania-and-end-of-qt-mania-holds-rates-at-5-50-top-of-range-qt-to-continue-as-planned/

Wolf gave a link to the transcript of Governor Waller’s speech – it’s worth reading. This is a great quote (watch out for misreading double negatives!) that shows insight into the Fed’s current state of mind:

As I said in a recent FEDS Note and in several speeches, the 2020 criteria for when to begin QT may have been too restrictive and did not allow the Committee to taper as soon and as gradually as desired.

Thanks for suggesting we read the actual speeches. Good advice. It was very helpful.

But now I’m even more sure the fed is full of goons. Waller compares QE to pouring water on a burning house:

“As an example, when a house is on fire, pouring water on the fire will put it out, which has great benefits for all. But when the fire is out, draining the water away does not reignite the fire—the initial benefits are not undone.”

He asserts QE had “great benefits to all” because the house was burning down (i.e., there was market trading dysfunction).

Oh the irony. The global economic house keeps burning down because central banks keep stuffing it full of tinder — debt with unnaturally low interest rates that doesn’t accurately reflect risk.

And since 2008, QE was actually the cause of that inappropriately prices debt.

I’m glad there are a few folks out there still talking sense (Dimon, Druckenmiller, Gundlach) otherwise I’d just have to give up the ghost.

In the part you’re talking about, Waller and Logan were DISCUSSING THEORETICAL RESEARCH PAPERS that some researchers had written. They cited their names too. That’s what you’re talking about. They were presenting that research. Read it more carefully, especially the beginning.

Actually reading something is hard.

>My thinking on this has long been guided by the conclusions of a paper I wrote with Alex Berentsen about optimal stabilization policy

Did you miss the part where he mentions that he himself is one of those researchers? Presumably he agrees with the conclusion of his own paper…

The paper he discusses is cited in paragraph 1: “I want to thank Kristin, Matt, and Wenxin for putting together a great paper that provides an overview of the effects of QT across seven central banks.”

He later mentions his own paper from 2011 and he uses it to support his discussion of the assumed asymmetry of QE and QT.

You will see that the “house on fire” is an analogy to “shocks and frictions to trading” (such as a market seizing), which is what he’s talking about. So when QE is used to unseize the market, then QT will not re-seize the market – that’s the concept of this “asymmetry” he is discussing.

Here is the relevant section in his speech:

“To me, for QE to be beneficial on net, there has to be asymmetry in the effects of QE relative to QT. My thinking on this has long been guided by the conclusions of a paper I wrote with Alex Berentsen about optimal stabilization policy, which is what QE and QT ultimately should be about.

“The gist of the argument is that when shocks and frictions to trading arise suddenly, the central bank can take actions such as injecting reserves to ease trading frictions or credit constraints and improve welfare.

“But by waiting until the frictions and shocks dissipate before undoing the injections, the positive effects are not reversed. As an example, when a house is on fire, pouring water on the fire will put it out, which has great benefits for all. But when the fire is out, draining the water away does not reignite the fire—the initial benefits are not undone.

“The punchline here is that QE is conducted under different market conditions than those that occur when QT is done, so it is not surprising that the effects will be different. The authors’ findings that QE has asymmetric effects compared to QT is not a puzzle but an indication that central banks timed QE and QT in the right manner such that society was better off.

Speaking of inflation, I see gas station gasoline prices just jumped ten percent this last month where I live, SF bay area north. Energy prices feed into some core CPI components. Next headline CPI and core CPI might see Powell pulling more hair, buying a rug.

I live in CA and I ignore prices here to abstract to anything larger. This is especially true as Winter winds down and special blend pricing will kick in. I noticed an increase in Sacramento but in some cases seems opportunistic as very inconsistent.

It’s not just a California thing. The average national (USA) retail gas price (regular) jumped about ten percent from Feb 1 to Mar 3. The Calif summer blend is supposed to start in March. Last month was February, last I looked.

Yeah, I just got gas today and it went up like 40 cents per gallon since the last time I got it.

Given the current plan, how many years will it take for the Federal Reserve to reduce it’s balance sheet to less than 1 trillion?

I don’t know how much time I have wasted shooting down this BS over and over again.

READ THIS, it explains why:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

Any kind of QE (even Operation Twist style without increasing the net size of the balance sheet) should be OFF THE TABLE in the near future.

The Federal Reserve has MORE THAN ENOUGH ammunition to fight a mild to moderate recession, in the form of 5.5 percentage points of possible interest rate cuts. In 2008, QE was used as a policy tool for additional stimulus when rates were already at 0%.

Slowly this monetary abracadabra gets out of fashion.

If a deflationary event becomes too unlikely and sustained inflation is the path things continue to evolve, the offloading of treasuries will quickly turn into an avalanche.

Why would one keep holding bonds yielding 5.4% when gold returned 9.5% annualized during the last 5 years?

Then the counterparty risks, and KYC regulations, taxes.

“,…when gold returned 9.5% annualized during the last 5 years?”

Cherry-picking your dates, eh? Gold had plunged over the prior 5 years, and now it’s up just 14% from where it had been 13 years ago. And it doesn’t pay dividends or interest. So lots of risk for little return. I mean, sure hold some gold, but don’t compare it to T-bills which are risk free, and you’ll get ALL of your money back PLUS interest at the end of the term, guaranteed.

Gold has not performed to that level recently…….because……it was out of air after a run from approximately $1050 per ounce in 2015 to its peak of approximately $2150 during August 2020. ……..it formed a base after its peak of August 2020……..the longer the base the bigger the potential advance……..the base was three and one half years…….broke out of the base during January 2024, retested nicely recently and now may be about to reward patient holders…..over time. So measuring the last five years will not provide an accurate picture.

Many have differing views of the US dollar. Personally, I hope gold goes to $200 an ounce because I hope AI and quantum computing drive inflation into the ground and allow the US to continue its dominance over world markets. After all as a US citizen….to hope other is madness.

However, as a rational economic person that is witnessing a generation which has been taught little self control, and it being easy to think the Chinese and others will match our technology, as a result of massive over consumption and other reasons I don’t have willingness or time to describe, the dollar may continue its slow drop. Sort of reexperiencing the pound in the 20th century. If the dollar drops, gold is a logical safe haven for a portion of your assets. Its recent breakout, at a time when BRICS is expanding, growing very quickly in terms of GDP etc. seems to be indicating a period of trouble may lay ahead. Inflation, while not the primary trigger, will certainly not help support the dollar in the long term.

Unfortunately our officials do not seem to care about seriously crushing inflation ……in fact I suspect they want the dollar to decline. This brings huge opportunities for our domestic companies and restrains the demand of the US middle class without a political fingerprint linking them to the crime……The potential dollar drop, may be why there is no top to the stock market. Between inflation and international cash being repatriated over the next decade this market could be just starting to flex its muscles.

As always….who knows…..as nobody…..can tell the future.

“Why would one keep holding bonds yielding 5.4% when gold returned 9.5% annualized during the last 5 years?”

Because gold doesn’t pay you a coupon – you have to exit your position in order to realize your gain.

By 5.4% I assume you’re referring to bills, which technically don’t pay a coupon, but their short duration allows them to function the same way. Everytime you roll over a maturing bill, you’ve realized this gain. So if the Fed does lower rates, you’ve only lost yield on future bills, not any current or past holdings.

Don’t get me wrong, there is no attempt to cherry-pick a time frame to fit any narrative.

As a foreign holder of T-bills if the confidence fades that 5-year annualized inflation is back within the 2% range I’ll swap them for an alternative repatriating US currency. So far we are way too far behind the curve.

Too many shenanigans: the Fed is now parading talking heads every day, more obscure programs, more questions about the way key stats are reported, and this speculative frenzy just backed in more inflation via the “wealth effect”. And let’s not start with troubled domestic and foreign politics.

Wolf is clearly wrong . rates are coming down , facts .

https://www.nzherald.co.nz/business/asb-drops-some-home-loan-rates/Z7VUR6SXGFHTPIGKVXRQ63SFZA/

🤣🤣🤣, this is what the article you linked says: “Major banks ASB and ANZ are cutting some home lending rates today.” Do you know what “ASB” and “ANZ” are??? I’ll tell you: ASB is a bank in New Zealand, owned by Commonwealth Bank of Australia. And ANZ is the Australia and New Zealand Banking Group. Those two banks in New Zealand are responding to the decision by the Reserve Bank of New Zealand last week to hold its rates steady. Neither the two banks in New Zealand nor the Reserve Bank of New Zealand have anything to do with interest rates in the US or anywhere else. And the article appeared in the New Zealand Herald. I know, reading is hard 🤣🤣🤣

They’ve totally lost control of everything and are just letting bubbles rage, completely reckless and in violation of their mandate. Look at the rampant speculation everywhere. We need an emergency rate hike.

If they follow Waller’s advice and really sell ALL their MBS (which they never should have bought in the first place), then The Fed will definitely not be able to get their balance sheet below 7 trillion before things start breaking. Has CONgress figured out how to balance the budget yet? They better.

You will be disappointed: as the balance sheet drops below $7 trillion in late 2024, nothing will “start breaking.” There is still way too much liquidity.

Waller is not proposing to sell MBS but to let them run off to zero via their normal passthrough principal payments and their call feature. It will take years just like the Treasury runoff takes years. QT is a matter of years, and we’re only a year and a half into it; it’s not a matter of weeks or months.

eks or months.

I know that criticism on the Fed especially at the Dallas branch is not welcomed, but what the speakers present here, will 1.) never implemented full and 2.) would be relatively soon outweight by the reality.

LOL. QE mongers don’t ever give up, do they?

I´m not a QE monger, but fact is central banks use QE since the GFC as permanent and standard monetary policy tool, despite the fact they name this as “non-standard or extrodinary.”

And the ongoing CRE crisis will require measures by the Federal Reserve like agency CMBS and CMBS purchases. How through a facility or direct, not matter, but it will happen.

You’re in fantasy land. Office CRE has a structural problem, like retail CRE, and it’s being dealt with just fine by investors losing their shirts, and by other investors coming in and creating something new out of the ashes, which is how that should be.

It’s nice to actually hear a longer term plan from the Fed, and in conjunction with Treasury issuances, actually makes sense. The Treasury has been heavy on the short end of the curve in issuance, that’s exactly what the Fed wants to absorb, and in terms of supply and demand has kept longer term rates in check. I do still agree with the liquidity question first and foremost–when the reverse repo is drained to zero, assuming reserves are the next category to decline, what is the breaking point there? Assumedly higher than $1.5T this time

Well I noticed Fed Bostic is talking a total different tune about inflation and rates. He was jawboning cuts forever.

What do you mean, “He was jawboning cuts forever.”

Another interesting one, Wolf, but it does not mention an important Fed funding liability, which is the Treasury General Account deposit with the NY Fed, which is now the notable sum of $767 billion or a very material more than 10% of Federal Reserve System total assets. It needs to be fit into the picture. On QT, recall that $3.9 Trillion of Fed assets have remaining maturities of more than ten years, so they will definitely be with us for quite a while! Best, Alex

1. The Fed does not control the TGA. It’s the government’s checking account at the New York Fed. JPM used to have it until the Financial Crisis in 2008. As banks were teetering on collapse, the US government moved its account from JPM to the NY Fed, which cannot collapse.

There is another balance sheet liability — this one MUCH bigger — that the Fed also does not control, and that is entirely demand-based: currency in circulation, currently $2.33 trillion. So combined, TGA and currency in circulation are $3 trillion roughly, and the Fed must counterbalance them with assets.

Those two combined, plus the minimum level of reserves mark the lowest possible point of the balance sheet, below which the Fed cannot go.

We discussed these relationships many times, including as a preview just after QT had started in Sep 2022:

https://wolfstreet.com/2022/09/05/by-how-much-can-the-fed-cut-its-assets-with-qt-feds-liabilities-set-a-floor/

So the absolute minimum balance sheet the Fed can maintain is over $5 trillion. The Fed cannot go below that unless demand for currency in circulation collapses (which I doubt since much of it is used overseas for hoarding and other purposes).

2. “On QT, recall that $3.9 Trillion of Fed assets have remaining maturities of more than ten years,… ”

So let me explain MBS to you.