The Spiking 10-Year Treasury Yields Apparently Rattled the Government’s Nerves.

By Wolf Richter for WOLF STREET.

There was a lot of navel-gazing in the “Quarterly Refunding” documents released today and on Monday by the US Treasury Department about the explosive surge of the 10-year Treasury yield.

These documents project how much in marketable debt the government will have to issue to refinance maturing debt and add new debt to fund the ballooning deficits in Q4 2023 and Q1 2024.

The total amounts were released on Monday — $776 billion in Q4 and $816 billion in Q1 to be added to the marketable debt. Today, the details were released, including to what extent that new debt will be composed of longer-term notes and bonds.

There was a lot of navel-gazing because the last Quarterly Refunding documents released on August 2, and the expectations of that info in the month before had triggered a 120-basis point surge in the 10-year yield from about 3.8% in early July to 5% briefly on October 23, which was quite a spectacle. And that had apparently rattled the government’s nerves.

So the recommendations today by the Treasury Borrowing Advisory Committee (TBAC) de-emphasized the issuance of longer-term securities, particularly those ranging from 7-year notes to 30-year bonds.

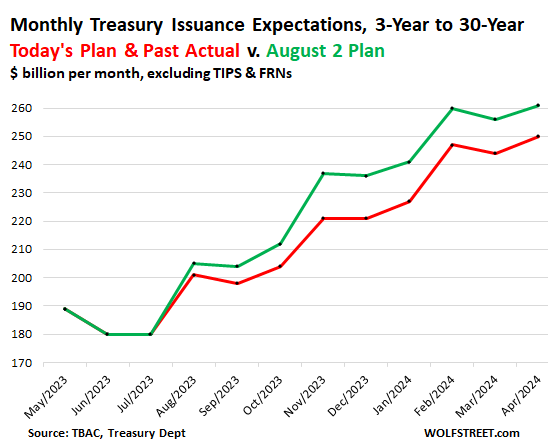

And instead, the recommendations shifted more weight to short-term Treasury bills (1 month to 1 year) and to 2-year notes and 5-year notes which respectively increased by $11 billion and $10 billion over the next six months in today’s plan compared to the August 2 plan for the same period.

The chart shows the TBAC’s issuance recommendations for 3-year notes through 30-year bonds, not including TIPS and FRNs, in today’s documents (red line), and the documents released on August 2 (green line). Issuance of those 3-year notes through 30-year bonds will still balloon, but less than projected on August 2.

OK, so T-bills out the wazoo. TBAC figured that the shift to T-bill issuance will cause the amount of T-bills outstanding to balloon by $460 billion in Q4, and by an additional $586 billion in Q1, or by a combined $1.05 trillion in just two quarters!

At the end of Q3, there were $5.26 trillion in T-bills outstanding. The additional issuance in Q4 and Q1 would increase the total by 20% to $6.31 trillion.

At the end of Q3, T-bills accounted for 20% of marketable Treasury securities outstanding. By the end of Q1 2024, the share of T-bills would rise to 23%.

The navel-gazing about the surge in longer-term yields.

The TBAC’s report went into details about why longer-term yields surged, and it came up with a laundry list — I counted a dozen — of reasons:

1. “Stronger-than-expected” economic activity. It cited the 4.9% surge in GDP in Q3, “strong consumption” of goods and services, growth in residential investment, growth in durable goods orders, job growth, etc.

2. “The possibility that the ‘neutral’ real rate of interest is now higher.”

3. “Changing expectations around the near-term monetary policy path”—the higher for longer may finally be sinking in.

4. “Higher real yields as measured by TIPS securities.”

5. The ballooning debt. Oops, someone figured it out. “The growing imbalance between supply of and demand for US Treasury debt may also have contributed to the sell-off.” The ballooning debt will have to be sold, and new buyers need to be lured in with higher yields. We’ve been saying that here on WOLF STREET for a long while.

6. The Fed’s QT that includes a $60 billion a month runoff in Treasury securities, totaling close to $900 billion on the balance sheet to be released tomorrow. This is “funding that will need to be replaced by issuance to the private market,” TBAC said.

7. Oh, and “on August 1st Fitch downgraded the US long-term rating from AAA to AA+,” which was a hoot.

8. Foreign investors and central banks, oh my. They are still adding to their positions but a lot more slowly than the debt increases, and their share has been tumbling. And worse: “The appreciation of the US dollar means some foreign central banks may consider liquidating Treasury securities in the process of defending their currencies,” TBAC said.

9. Investors got caught on the wrong foot: “Anecdotally, some investors had expected that ten-year Treasury yields would not rise beyond the approximately 4.25% high of last year and had already extended the duration of their fixed-income portfolios – meaning they now have limited capacity to add more interest rate exposure,” TBAC said.

10. Banks, after imploding, lost interest?: Their “security portfolio assets have been declining since last year with bank holdings of Treasuries down $154 billion compared to one year ago,” I would think largely because a handful of banks have imploded because of those bets?

11. Treasury auctions show “some early evidence of waning demand,” while still “consistently oversubscribed.” TBAC said that “On October 12th a reopening of the thirty-year bond auctioned 3.7bp cheaper than the prevailing rate before the auction, the largest “tail” in a thirty-year bond auction since 2021.”

12. The term premium demanded by investors: “Investors may now require an additional yield or ‘term premium’ to hold longer-term debt.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I see we got another “very hawkish hold”

today from the fed.

Another “Hawkish Hold” with Tightening Bias: Fed Keeps Rates at 5.50% Top of Range, Rate Hike Still on the Table. QT Continues

Higher for how much longer? “The extent of additional policy firming that may be appropriate….”

Hot off the press:

https://wolfstreet.com/2023/11/01/another-hawkish-hold-with-tightening-bias-fed-keeps-rates-at-5-50-top-of-range-rate-hike-still-on-the-table-qt-continues/

Wolf,

Ah, just regular hawkish this time.

Maybe we’ll get a very hawkish

hold next meeting, as their way of

showing how serious they are

about controlling inflation.

Personally, I’m still camped out in

the very short term T-bills, and

would require far higher yields to

consider chasing longer duration

bonds.

J.

“Ah, just regular hawkish this time. Maybe we’ll get a very hawkish”

LOL, I just ran out of space in the headline, and something had to go.

Just maybe one of the major reasons the Fed started to lose control of the back end was because it decided to hold front end rates with inflation starting to tick up again mixed with a consumer that spends like they’re on shore leave. Bond investors are funny folk and they tend to take long run inflation implications seriously. They also know the value of a dollar unlike equity market types who were seemingly put on this earth to just buy things. There has been a lot of talk about moving the inflation target to three percent and that has to make longer dated treasury buyers skittish. There is a mountain of debt out there that has to be rolled every month. The governments fiscal exuberance isn’t helpful either. Bottom line if the kids aren’t careful they could trigger a run on the currency or the bond market. Better to have a deep recession than a Wiemar experience in my view but maybe the powers that be think they can fix that in short order. When it starts I don’t think so.

Dovish or neutral imo.

Weaksauce

It’s by now really funny when the same stuff gets trotted out for 18 months after each Fed meeting where algos and folks try very very hard to imagine what Powell might have imagined he wanted to say between the lines but failed to imagine to say it between the lines. When you step back a little, this stuff is just hilarious. After EVERY meeting.

The worst part is some of the usual suspects in the pivot-mongering sections of the financial media today literally calling this hawkish Fed hold a “pivot”. That’s right they actually took a very clear signal from JPow and the full Fed of “higher for longer”, warnings on ongoing inflation (to likely soon get worse with expiration of the health insurance inflation “damper”), and ongoing QT and a good chance of a hike next meeting as been talked about for months, as… a pivot. Just can’t make these things up.

This is even worse than the “inflation is transitory” (or even “inflation is actually good for you”) happy talk of 2021 or the general collective hallucination of the squawkers and speculators that’s led to the Everything Bubble, housing bubble and worsening housing affordability in the US to begin with. The pivot-mongers now aren’t even trying anymore, they’re totally drunk and high on their own fumes.

Exactly, another case of “WHAT Powell said… and WHAT the markets chose to hear..”

I’m not a trader or an algo.

Remember the “Taper Tantrum” in 2013 tho?

Hike when you can!

Get rates back up. It’s only a matter of time before some “disaster” a la SVB derails the hiking again.

If the economy is crazy strong it can take it.

Also the “wealth effect” of stonks & housing is inflationary. Rallies in risk assets = bad.

The whole “hiking bias” exchange w/ Steve Lieseman was cringy too

Miller,

Bloomberg headline: “Powell Hints Fed Is Done With Hikes in Pivot Cheered by Markets”

They used the word pivot as a dog whistle to the casino.

It’s so disgusting I really can’t take it anymore.

I get that they buy treasuries when the amount that rolls off exceeds the QT in the month. Now that QT has been going on for a while, do they look ahead to see what months might have less than the target amount and top those up? Or do you think they will be buying longer terms to decrease the chance that those rates “get away” from them? I’ve no idea if the fed even announces the durations bought, or cares to micromanage to this extent

If the lower yield on the ten year today is because of this news, one can assume the same news should have increased the yield on the 2 years.

And yet both the one and two years yield are a little lower today even though there will be more of them soon!

Wolf, paragraph two above reads “Q4 2023 and Q4 2024”, should it be “Q4 2023 and Q1 2024”? More importantly, I very much appreciate the factual coverage you provide peons like me. It helps me plan for the mess at hand and the bigger one coming. Cheers!

Does the Treasury specify the distribution of T-Bills by length of maturity? Are they expected to be a mix or are these all 1 month or all 1 year, etc?

Yellen doesn’t want to spook the bond market, it seems.

J. Pow should “kill the chicken to scare the monkey.”

He punked out when he needs to kill inflation.

25 bps won’t crash us.

Inflation re-accelerated and economy still too strong.

Risk on! Great message. Stonks loved it

I do think he could speed up QT just a teeny tiny bit without crashing markets.

Like, just a smidge of MBS selling every month. MBS are rolling off as slow as they can, since refis have collapsed and there’s no incentive to make extra payments to the principal.

It’s possible that not bringing attention to the rolloff is allowing it to happen. It is steady, to put another way. Changing the monthly amount, or forced selling, could bring an unwanted spotlight back onto it. Fed balance is down a trillion, which is a surprise to most. I think in part because of consistency. Or, maybe I’m just overthinking the social aspect of it.

Ltlftc – interesting point that I hadn’t considered.

I’m so sick of our damn government and the Fed. We don’t need the 10 year coming down. I hope what Treasury is doing backfires. Burn it down. It’s not worth saving.

I like #7 the best. Only one more rating agency left to go that downgrades government debt (moodys I think?). Congress might just build up the military and tell foreign governments they won’t get paid upon maturity if they hold the debt. $35 trillion dollars? Can’t we just be friends and not owe anyone anything?

The Fed also holds treasuries and might not let congress nullify the debt. From the shadows none of this public of course.

Deep state congress critters who want to print national currency and bypass the fed, vesus deep state banking critters who want their six percent.

Who would win?

Is it possible that long bonds would eventually disappear along with the 30 year mortgage in order to hide the ugly financial state of the country? My understanding is that most other countries don’t have fixed rate mortgages for 30 years, although that hasnt reduced speculation given examples such as Canada and Australia where their bubbles are even more insane that ours.

I doubt the long bond will disappear. It has been a staple in the Treasury market forever, and it’s a lot shorter than the 100-year bonds that Austria, Argentina, and other countries have sold. The UK sold perpetual bonds a long time ago. So these kinds of bonds serve their purpose.

Mortgages are a different story. Without government backing, the 30-year mortgage might vanish because it would be horribly expensive for the homeowner.

I did a study of German municipal bonds sold in the 1890s. Some were set to mature in1955. This would be a good case of buy at auction but sell well before maturity.

“the 30-year mortgage might vanish because it would be horribly expensive for the homeowner.”

Wolf – how would it be horribly expensive for the homeowner? Wouldn’t the lender be the one getting the short end of the stick here?

I can’t imagine anyone would have wanted to lend to me for 30 years @ 2.7%, without being able to pawn it off on Fannie Mae.

MM,

Lenders would want to be compensated for the risks. So they will charge a premium. All kinds of stuff happens in 30 years — the risks are big. That’s why without government backing, mortgage rates tend to be either variable or fixed for shorter periods of time because homeowners couldn’t afford a 30-year fixed. 30-fixed-rate mortgages are the biggest housing subsidy by the government (to buy votes?).

Wolf, it may have been intended to buy votes, but it’s really just a subsidy for existing homeowners, as prices rose to account for the extra credit available.

Oh I see – without gov’t backing, 30 YRFM rates would have to be a lot higher. That makes complete sense.

Will an increase in t-bill issuance pose the same problem where buyers will only show with higher yield or are they pegged so tightly to the fed rate to overcome this pressure?

I would imagine that demand into January for short-term treasuries will be guided by the Dec FFR rate hike expectations that start to develop over November. I would imagine demand will be lower, if the rate FFR increase becomes more likely. Investors will sit out longer for higher yields coming down the pike. Likewise, I’d imagine today’s announcement will cause long-term yields to fall in the coming weeks.

That could happen. There are other issues with this, and for long it’s not sustainable. So this is a short-term effort at best.

Short term thinking is what they do best.

Thanks, Wolf!

Exactly. This game is not going to work for too long. As inflation continues to surge back, t-Bill will have to push to 5-6% — you can roll for a few quarters but can’t doing that for 4-5 years.

It’s called crowding out. The size of the Federal deficits guarantee that the FED will monetize a substantial proportion of the upcoming issuance.

Really? So you are predicting the end of QT? You care to put a date on that prediction?

I don’t think Wolf agrees with you. Higher for longer!

“The size of the Federal deficits guarantee that the FED will monetize a substantial proportion of the upcoming issuance” is a ridiculous BS statement not worth my time.

To be fair Wolf, when The Fed was expanding it’s balance sheet, isn’t that exactly what they were doing (buying/monetizing the debt)?

Can’t have it both ways. Regardless, ZIRP and direct buying of treasury issuance with newly printed money are two things that NEVER should have happened.

That was NOT what the statement said. Read it. The statement was a prediction for QE coming NOW to absorb the new issuance in Q4 and Q1 2024.

So over 6 months they currently need 1.6T for renovations but just like my my experience with home renovations, I expect they are going to need to go back to the Cookie Jar multiple times more.

The way the Congress spends tax dollars, it does not take a genius to see $40Trillion on the countries credit card in 6 quarters.

This is madness !

I have been thinking about the Reverse Repo drawdown.

Five months ago it was at 2.3 trillion and now it is 1.1 trillion. So more than 50% drawdown, very rapidly. It seems logical that alot of that money, which was where money markets were stashing depositor cash moved the funds into short dated Treasuries, which provided liquidity (demand) for those Treasuries.

So my question is if this was a primary source of liquidity for the sale of 1 trillion in short-dated Treasuries, then what happens when the RRP balances get closer to zero?

The Treasury has said that they will use more short term bills for the coming 2 quarters and that might be appropriate as they drain more of the RRP, but how much demand is there for short dated bills once the RRP is gone? Does the lack of demand that is showing up in long duration bonds start to show up in short dated bonds also?

Is there some other big source of liquidity I am missing here? Apart from the Fed restarting QE, is there some big governmental source of liquidity that is still out there? Is the Treasury simply assuming that by the time they drain out this next trillion, inflation will be vanquished and the Fed can start to absorb extra debt with a new QE program that doesnt cause inflation? (due to a weak economy or recession)

It seems to me that this is a FUBAR situation in the making.

I do realize that the ultimate source of liquidity will be investors selling other assets as the Treasury is forced to offer even higher rates to attract capital. I was more curious about whether I am missing some big source of funds that wouldnt demand a higher interest rate?

Bank deposits at the Fed. ~3.2Trillion as of Oct 25th. Still some liquidity out there after RRP.

But once you drain the RRPs down to 0, that’s when you might start to see a lot more pressure placed on the financial markets (and the banking system). That’s why they are going slow with this.

I had to Google “Navel Gazing”

I’m usually just trying to reverse my “phone posture”. Haha

Omphaloskepsis

Me too. Totally different meaning in East versus West!

The bottom line is that the Federal Reserve did nothing, yet again.

If you drive a car and you just keep your foot steadily on the brake, you’re not doing anything either?

Now imagine that you’re in a driver’s ed car with two sets of pedals, and your co-driver has the foot on the gas (government), and you have the foot on the brake (Fed), both steadily, so neither is doing anything?

The Treasury should have been selling all the paper it could at 30-year maturities when they could have borrowed almost to infinity with a low-2 handle. Has anyone been held responsible for that error, which will cost taxpayers untold trillions of dollars in excess interest payments?

Of course not.

Everyone was talking about negative rates during that time period.

If only the Fed knew rates would rise.

The Fed did things in the wrong order. Too many martini lunches might do that.

…tee many martoonis?

may we all find a better day.

So a dozen reasons… not including the OBVIOUS… they are choking the LT Bond market with their Inflation Reduction Act spending. There aren’t enough bond buyers out there dumb enough to get sucked into a Long Term position when inflation is being goosed by the government… so they are switching to selling more short-term notes in the hopes that buyers will buy them instead.

The Inflation Reduction Act spending is included in #5: ““The growing imbalance between supply of and demand for US Treasury debt may also have contributed to the sell-off.” It’s in the “supply” part of the debt.

I see nothing good coming out of all this mess Maybe putting all your money in 3-month and 6-month T-Bills If you believe the govt won’t default

If the government (i.e. currency) experiences a hard/true default, your paper investments will be the least of your concerns. Full Faith and Credit and all that.

“Tsunami of Treasury Issuance Will Shift from Longer-Term Debt to Short-Term T-Bills & 2-Year Notes”

I think this change in policy to the short term could be interpreted as, “We’re going to be cutting rates soon, so why should we bother to pay 5% for twenty years.”

No wonder stocks are in rally mode. It’s clear the Fed will give us low rates with high stealth inflation.

My health insurance for 2024 just went up another 10%.(Up 23% in two years). Didn’t I read govt stats that said health care costs were going down?