It wasn’t big hedge funds that blew up, but £1.5 trillion in leveraged pension funds. BoE stepped in to bail them out and prevent further contagion.

By Wolf Richter for WOLF STREET.

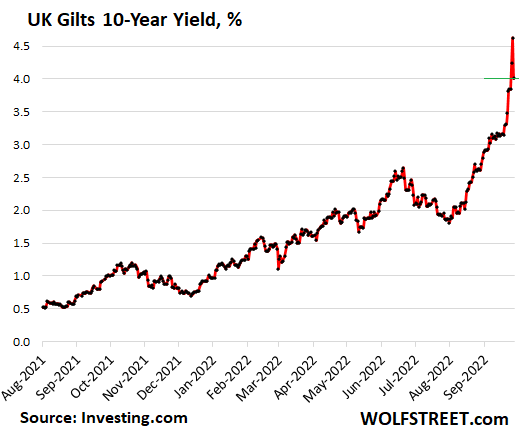

Over the past few days, the pound plunged, including with a flash-crash on Monday that briefly took it to record lows against the US dollar. Prices of long-dated bonds went into a death spiral, with the 10-year yield spiking by 130 basis points in four trading days to 4.63% early today, and by 275 basis points in seven weeks ago (up from 1.88% in early August).

The bond market reaction represents a colossal and sudden degree of “tightening” of the financial conditions, before the Bank of England’s QT had even started. QT is designed to bring up long-term yields, but they already exploded due to chaos.

It was the market’s backlash against the new government’s reckless plan to cut taxes for the rich and for corporations, funded by new debt, while piling on spending to subsidize energy costs, also funded by new debt, thereby requiring the issuance of large amounts of new debt, even as inflation has already reached to 10%.

The Bank of England, which is in charge of maintaining financial stability, now has a slew of problems to deal with: inflation spiraling out of control, currency plunging, bond market in chaos, financial stability at risk, and spreading contagion. And some of them require the response that the others require. So this is a mess, and there are no good solutions.

The BoE chose to maintain financial stability first because the bond market chaos was starting to blow up the financial system, as leveraged pension funds were getting collateral calls triggered by the spike in yields, and as UK lenders had suspended making mortgage offers because no one knew how to price them amid this chaotic volatility in bond yields.

Worried about “contagion” and “financial stability”

So the BoE came out today and said that it would purchase long-dated gilts with remaining maturities of over 20 years. The purchases would go through October 14.

“The purchases will be unwound in a smooth and orderly fashion once risks to market functioning are judged to have subsided,” it said.

And the 10-year yield plunged by around 60 basis points, to 4.01% at the moment, undoing the spike early today and yesterday:

Specifically, the BoE said it’s “monitoring developments in financial markets very closely in light of the significant repricing of UK and global financial assets.”

“This repricing has become more significant in the past day – and it is particularly affecting long-dated UK government debt,” it said.

“Were dysfunction in this market to continue or worsen, there would be a material risk to UK financial stability,” it said.

“This would lead to an unwarranted tightening of financing conditions and a reduction of the flow of credit to the real economy,” it said.

“In line with its financial stability objective, the Bank of England stands ready to restore market functioning and reduce any risks from contagion to credit conditions for UK households and businesses,” it said.

“To achieve this, the Bank will carry out temporary purchases of long-dated UK government bonds from 28 September,” it said.

“The purpose of these purchases will be to restore orderly market conditions. The purchases will be carried out on whatever scale is necessary to effect this outcome,” it said.

“These purchases will be strictly time limited. They are intended to tackle a specific problem in the long-dated government bond market,” it said.

“Auctions will take place from today until 14 October. The purchases will be unwound in a smooth and orderly fashion once risks to market functioning are judged to have subsided,” it said.

Bailing out leveraged pension funds.

Defined-benefit pension plans in the UK that were using an investment strategy, called liability-driven investment (LDI), got hit by collateral calls as long-dated gilts went into the death spiral.

“The amount of liabilities held by UK pension funds that have been hedged with LDI strategies has tripled in size to £1.5 trillion in the 10 years through 2020,” according to Bloomberg.

BlackRock, Legal & General Group Plc, and Schroders Plc manage LDI funds on behalf of pension clients. “The pension firms use them to match their liabilities with their assets, often using derivatives,” according to Bloomberg.

“LDI collateral buffers are partly set using historical data to build models based on the likely probability of gilt price movements,” Shalin Bhagwan, head of pension advisory at DWS Group, told Bloomberg.

I mean, surely this strategy is very conservative and is not risky at all and is very suitable for £1.5 trillion in pension funds. Until it suddenly blows up.

The massive spike in yields of long-dated gilts “blew through the models and the collateral buffers,” Bhagwan told Bloomberg. LDI funds got margin calls from their investment banks and had to post more collateral.

To meet the collateral calls and maintain their LDI positions, pension systems asked their managers to sell holdings in equities, bonds, and UK open-ended real estate funds, Bhagwan told Bloomberg.

And that’s precisely how contagions spreads: by having to sell unrelated assets in order to meet margin calls.

“The BOE had been warned by investment banks and fund managers in recent days that the collateral requirements could trigger a gilt crash, according to a person familiar with the BOE’s deliberations before they stepped in,” according to Bloomberg.

“The BOE intervention was required to prevent a vicious cycle becoming even more dangerous for pension funds forced to sell their gilt exposures,” Calum Mackenzie, an investment partner at Aon, told Bloomberg.

“The market’s swift and significant reaction underlined the big risk faced by pension funds who have had or who could have had their liability hedges reduced,” Mackenzie said.

“Any pension funds which has used even moderate levels of leverage are struggling to keep pace with the moves,” Mackenzie told Bloomberg before the BoE stepped in. “You have a bit of a death spiral potentially where pension funds in particular are being forced to sell because they’re breaching their leverage agreements with their LDI counterparties.”

The Pensions Regulator told Bloomberg today:

“We are monitoring the situation in the financial markets closely to assess the impact on defined benefit pension scheme funding.”

“We again call on trustees of DB schemes and their advisers to continue to review the resilience and liquidity of their investments, risk management and funding arrangements, and plan accordingly to protect the interest of scheme members.”

Note that the UK use of the word “scheme” to mean “fund” is endlessly amusing to USians, particularly in this context where the UK meaning of “scheme” is much closer to the USian meaning of “scheme.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just to make anyone aware who isn’t, the governing Conservative Party are the ones with the hard-won reputation for sound money management and fiscal responsibility. Or at least they did, up until last week.

In democracy it’s upto people to hold their politicians accountable.

These periods of upheavals and inflationary pain present opportunities to create new political parties that work in interest of people.

The old ones are too corrupt to change.

What’s working in the interest of the people to you?

When I read this sentiment, I always have in mind two wolves and a sheep choosing the dinner menu.

The problem isn’t any specific political party. It’s a rotting and decaying society. No new party can fix that.

The biggest problem are people expecting politicians to fix financial issues. Same politicians that cannot balance their own budgets.

Sadly, you are probably right, at least partially in the US. Cutting taxes on those who have used tax shelters to pay little in taxes, as things have stood for many decades, is insane. That policy worked for JFK only because the working, upper class did pay high taxes then and few then used the foreign income tax exclusion from US taxation.

Our election financing system, and the Supremes’ Citizens’ United decision, ensure the “Quiet Coup” of which Simon Johnson wrote, will not be reversed in our congress or legislatures.

@DanW,

It’s been amusing to read about Stephen Moore (who has been perched atop his soap box yelling about tax & spend Bidenflation) *applauding* “Trussonomics”. Arthur Laffer adherents die hard…

Ya trickle down approach is much better. Not.

They cant stop the money printing…..I wonder how this will end?

Are their any adults left in the room at these central banks?

You can’t stop the printing, nobody can stop the printing.

Take the cold from snow, tell the trees, don’t grow,

Tell the wind, don’t blow, ’cause it’s easier.

No, you can’t stop the printing, nobody can stop the printing.

Take the spark from love, make the rain fall up

’cause that’s easier to do.

A good, unappreciated, US president (George H.W. Bush, not junior) called this kind of thing “Voodoo economics.” LOL. He was so very right.

Yeah. He was a good egg as New England Blue-Bloods go. Was in real combat up close and personal, and knew the ME was a quagmire….threw Iraqis out of Kuwait, put out the oil fires, and got the hell out. Didn’t kill many kids, he’d been there as one.

Even raised taxes and took the shit for doing it after he said he wouldn’t.

The UK – the new Zimbabwe.

Exciting new frontier following in the footsteps of the United States.

At the moment the UK isn’t following the US in these regards but leading. True even if that lead is only by a little bit.

They did up until 1995 ish when they let the over indebted go whistle causing a massive house price crash. Since then it’s been bail out after bailout

The mere fact pensions can be leveraged should be a crime.

Sad reality is they are leveraged in order to meet their outlandish promises that never should have been made. I was in a pension in the early part of my career and after 5 years was vested around 27 years old. Even back then I could see the promised returns were absurd compared to average historical returns in the market. After many years was able to take a lump sum last year and roll it over to a self directed IRA. Sleep a lot better at night now.

Nope – it was the Tories (Norman Lamont et al.) who increased interest rates twice in one day from 7% up to 15% (before BOE independence) back in the early 90s in a vain attempt to peg the pond to the euro and ended up losing billions of dollars to speculators.

OTOH Labor have a lousy record too – Gordon Brown most of Britain’s gold reserves back in 2000 when gold was at multi-decade lows.

So neither party has any sort of claim to sound money management IMHO

I didn’t say that reputation was accurate ;)

You didn’t say “accurate” but did say “hard won.” Right away I wanted to know when and how was the reputation won.

And, more interesting, how do political party “reputations” manage to last as long as they do? Several unsavory analogies come to mind, here’s a politer one: Is a political party reputation that is decades old worth any more than this from Winston cigarettes?

https://en.wikipedia.org/wiki/Black_Wednesday

Euro was not introduced until 1999, the mechanism at play was the fixed exchange rate mechanism, which set bandings on exchange rates between European currency such as the Deutsche Mark

So the UK has opted for more inflationary fiscal and monetary policy, which makes the now lower yeilding bonds even less attractive, and compounds the issues when they try to tighten again? What a mess.

I call hyperinflation in UK by end of 2023 i.e. Official inflation rate will reach 25% by end of 2023 and will keep increasing. The gap between Official and unofficial inflation will increase even faster.

UK imports almost everything, it has no way out!

It’s a re-exporter technically. Doesn’t mean you are wrong though. Snap election in 3…2…

Brexit coming back to haunt them?

No, they weren’t part of the Eurozone so the ECB could bail them out.

Besides, the EU is its own disaster in the making and isn’t far behind.

There are many stupid and counterproductive policies I’m aware of in the UK, but leaving the EU definitely was not one.

No better time to check out and leave Hotel California than right now.

Another aspect is regarding people who own guilts. They were probably thinking about getting into Us treasuries (or some other dollar asset) for safety. But as long as gilt yields were increasing less than treasury yields they had to think twice. Now, with gilt yields crashing they’re going to rush into dollar assets. And to make it an even easier decision crashing gilt yield has made their gilts more valuable.

‘People who own guilts’ haha

Back to QE. Yay! Did not even take that long. Watch the Fed fold like a cheap suite.

Edit: Also, watch inflation ‘target rate’ corrected to 4%.

It’s so disappointing to see Bank of England Pivot so soon. Wallstreet is already celebrating this with a big rally. Pound is doomed and UK, the big importer will soon start seeing hyperinflation. WINTER is coming!

Will the bigger scumbag follow BoE soon?

It’s ok because they are “monitoring developments”. Just temporary QE to flatten the contagion curve. Two weeks. Tops.

All QEs started as “Temporary “.

Maybe the wallstreet is pumping another bear market rally by selling the BoE and Fed Pivot story. They may be successful as Fed is no longer trusted and this can cause inflation to run hotter despite the “slow QT for softish landing” plan.

I guess the English are so blinded by coverage of “Monarchy”, that they can no longer see or feel the hyperinflation that may have already started. I hope Americans remain more alert and hold out politicians accountable.

Americans holding their politicians accountable, that’s a good one.

When 10-year gilts yields spike by 130 basis points in four days, and prices plunges, and markets lock up, who needs QT?

In terms of the Fed: I’m just going to keep reporting every month by how much the Fed reduced its balance sheet. There is a certain amount of pleasure in watching QT deniers stew in their own juices on a monthly basis. They set themselves up for it.

It seems to me that most people here would like to see this QT continue. Unfortunately, the past 15+ years shows that the Central Bankers will most likely pivot. Wolf seems to have so much faith in the central banks that have let us down time and time again. I Like the articles but his snide comments to users in the comment section I could do without. I think he is suffering from Stockholm Syndrome.

He was just as certain back in 2018.

Tyler,

Are you sufferings from the ZH syndrome?

As sort of rule, do not drag the ZH stuff into here. If you like to wallow in it, wallow in it over there.

Banana-republic Jerome is a fake inflation fighter. Rates should be much higher and hiking much sooner if was serious about inflation.

If he were truly fighting inflation the s&p would be back to 2008 lows! The destruction of America! Can’t have that can we so he is he is dancing around the ring afraid to engage his heavyweight opponent! Jerome already talked about living with 3% inflation–well, try 5 or 6% or higher! britain and europe are collapsing and America will follow! Time to pay the piper!

This isn’t feeling like it will be a soft landing with a mild recession.

But why not just pause QT, instead of explicitly beginning QE again? Maybe there’s not much practical difference there.

In terms of the QT deniers, I think what they were wrong about was thinking that the Fed wouldn’t tolerate an orderly selloff of stocks and bonds. That’s what we’ve had so far, and the QT deniers have been dead wrong. But they are saying NOW that Powell will fold too if the same disorder that hit the UK bond market hits the US debt and equity markets.

Are they right? I don’t know. And did they move the goalposts? Absolutely. But while I can definitively say that they were wrong in the past, that doesn’t necessarily mean their future predictions are wrong.

Einhal,

“But why not just pause QT,…”

The BoE hasn’t even started QT yet. So they cannot “pause.” The beginning was scheduled for the week starting on Oct 3, when it would “sell” (actually sell) the first batch of its gilt holdings.

This frustrates the Fed’s mission, costs them credibility (as could be seen today in the market), and seems like it could have been avoided by back room meetings with the pension funds’ counter-parties.

The Fed did this in 2016 when oil prices fell off a cliff and many banks decided not to mark to market oil fields held as collateral so as to avoid liquidations. Although maybe the new PM and Chancellor needed this wakeup call.

I found your backgrounder info enlightening.

My understanding is that IN Canada regulatory bodies are only now really getting an understanding of shadow markets and derivatives post 2008 mess

SP 500 E Mini spiked up 51pts in 20 minutes after BOE bond bailout news hit as the simple equation for markets at the moment seems to be:

USD down = treasury yields down = Stocks and Bonds up

I’m neutral on QT/QE, and I play both sides as I attempt to ride the liquidity waves to the best of my skillsets.

That said, there are limits to both as 99% of society and businesses have leverage such as SBLs, mortgages, CC debt, etc. For example the 30 year was 33.5% down last week from the highs, so there are risks to all the leverage at this point due to margin calls that create a run-away cascade of liquidations of all assets to cover gigantic paper losses. And that is when the Global Feds (OverLords) step in to bail out the highly leveraged who thought it wise to borrow heavily from their bonds and stocks to buy more bonds and stock as the Fed ensured for decades that risk assets would never go down due to QE infinity and ZIRP/NIRP without limits.

Turns out QE/ZIRP/NIRP was transitory and has mathematical limits, and so will the opposite side of that coin…

Good luck in all your investments!

@Wolf, re “In terms of the Fed: I’m just going to keep reporting every month by how much the Fed reduced its balance sheet.”

sure, but it is such a trickle that you’ll be doing it for the next 3+ years just for Fed to unwind the mega COVID QE stimulus that is still jacking up markets, margin debt, and cash on-hand that is driving asset/goods inflation. Why do you figure that stock traders are sitting on record cash while the markets have suffered 30-50% losses? B/c of historic COVID QE . So, Fed’s QT trickle makes for nice headlines and talking points for financial pundits, but is in fact a joke. JMTC.

Isaac S.,

It’s not a joke. Look at the markets. It’s working very well, and it just started.

B of E didn’t “pivot”. They’re just setting guardrails along their previously announced path along the cliff’s edge. Financial conditions in the UK tightened faster than they anticipated, is all.

Whatever, wallstreet took the opportunity to spin up another bear market rally, and Fed Pivot crowd is all riled up.

So, inflation will just keep increasing :(.

They’re really big into recycling over there.

Unbelievable how they can be using a derivative product that doesn’t provide protection when you need it most.

I understand that some pension funds in the US (my one does) use LDI strategies by matching their bond allocation duration to match the plans payout profile based on the participants age and forecast retirement age.

I saw an economist in London comment that this was less punishment for the incremental debt than it was punishment the bond market metes out when they suspect “morons” are in charge.

No, it’s just bankrupt economies trapped in too much debt with no way to get out. Print, Print, Print, bailout rich by indenting the poor. Transfer money to cronies through bond buying and stealing it from poor through inflation.

This is what happens when the fuse gets too short to put out.

“Were dysfunction in this market to continue or worsen, there would be a material risk” … ” the Bank will carry out temporary purchases”

Haha, see? Our modern high-debt economies cannot stomach even a little bit a monetary policy tightening. When something breaks, central banks get us right back on the morphine drip. We know this is going to eventually kill the patient, but pain is not politically expedient. When the economy starts writhing in agony, central banks apply pain killers. Enabling our debt addiction is the only treatment for unstable credit markets that they know.

And make no mistake… When the, uh, “tyres” really start coming off of our credit markets, our central bank will do the same with lightening speed. It’s a horrible solution, but it’s what they’ll do. Oh, and nothing that central banks call “temporary” or “transitory” is ever as they describe.

The UK is not that far off where they will have to choose between defending the currency or the credit markets. Problem is, whichever one they choose, it will be bad for the economy.

If the BOE doesn’t defend the currency, it will be dumped by other central banks from its FX reserves and the GBP will possibly lose remaining reserve currency status altogether. That will make inflation worse and sink the bond market anyway.

At that point, the BOE will lose much of its remaining influence as that’s the source of it, the national currency.

They would be better off throwing the economy, markets, and public under the bus and saving the GBP. They can’t preserve living standards at current levels matter what they do.

@Augustus Frost,

I’m suprised nobody has yet pointed out the irony that the GBP makes up 7.44% of the IMF’s current SDR currency basket!

Seems there’s a “basket case” in that “basket”!

Bitcoin fixes that. Stanely Drunkenmiller said as much just the other day.

@Augustus Frost,

Also worth pointing out the irony that much of “Trussonomics” seemed to rely on a widespread belief that they could transform the UK into the largest global banking center. That idea seems as airworthy as a concrete airplane…

My view is that going “all in” on financial services is one the country’s biggest problems. I know it’s not the entire economy but it’s an outsized proportion of GDP and presumably employment.

The financial sector is supposed to exist for the rest of the economy, particularly manufacturing and agriculture which will always be the foundation supporting living standards as it’s real production. The financial sector is not supposed to be THE economy.

I see great things for the UK as an enlarged British Virgin Islands: money haven for scoundrels. Cute little gardens, nice polite nannies, well-behaved schoolteachers and accountants. High end prostitutes.

Yeah, will the City of London will still remain a Vatican for worshippers of money? Has the big feeder network, but also may have to add walls like the real Vatican did.

AF-your last sentence again illustrating the case of possession of powerful tools becoming more important than their use in accomplishing their mission…

(something currently encountered by Russian arms…).

may we all find a better day.

“They would be better off throwing the economy, markets, and public under the bus and saving the GBP.”

IMHO the problem with this approach is that once GBP has been stabilized, government will immediately start abusing it again, to a point where the dilemma of what to throw under the proverbial bus will re-appear within years or perhaps month.

IMHO the root problem is all these ills is the fact that fiat money are very easily abusable. It was thought that inflation would stop the abuse of fiat money, but it looks like this may not be the case (at least in UK at the moment).

Yes, fiat currency is the foundation of a financial system which is designed to fail. The one we have now with fake “wealth” and artificial prosperity.

Debt must expand forever or the system collapses. See GFC for a trial run when debt barely decreased.

Modern economics criticizes the gold standard because of the recurring boom-bust cycle.

Well, since the 1930’s, the global financial system has been building up toward a future “fat tail” catastrophic systemic failure from a combination of leverage on steroids + mostly government created moral hazard. Virtually no one sees it because it’s contrary to their personal preference, they believe in magical thinking where there is something for nothing, and/or they believe in the omnipotence of government “wizards behind the curtain”.

Silent generation and baby boomers lived to get maximum benefit from it, mostly “carrots”. Subsequent generations received some “carrots” while the younger and youngest will receive mostly or all “stick.

Current system is build on debt, with debt being a foundation of everything. Bond market is the last line of defense, CB’s will do whatever to keep it from falling apart. Will trash markets, standard of living, currency, whatever comes first to protect the bond market.

As falling bond market will take everything with it anyway.

With UK now, bond market saved for now, but it’s just a matter of time before markets will switch from “yahoooo, we got printer brrrrr again”, to – ohh, “we got some freshly printed rotten potatos” , and will start dumping GBP.

BOE will try to protect the currency with it’s limited FX reserves, and will run to the FED asking for swap lines very soon. The rest will depend on FED, provide swap lines, and allow some kind of orderly pound and UK meltdown, or just have fireworks started right away.

Have no idea what it is US preferred outcome in UK case.

They are out right liars and people do nothing. People are being screwed and by doing nothing they deserve it and good job.

99% of people have no idea their being screwed. They don’t understand any of this.

I disagree. They are enthusiastically running towards it. And why not? All the incentives are there.

“We know this is going to eventually kill the patient”

Eventually? What we are seeing now is a comatose patient having convulsions. Won’t be long now. Unplugging the machine would be the most humane thing to do but only a few people see that.

Your so right. What does the BOE think will be different in a few weeks when they quit buying long term guilts? Nothing will be fixed and the sell off will continue.

“So this is a mess, and there are no good solutions.”

This is the end result when the “can” has been kicked to the end of the road. Practically everyone believes there is always some way out of the consequences to postpone the day of reckoning into the future. At some point, the day of reckoning arrives.

If it hasn’t arrived for the UK, it’s not that far off. With high inflation, rising rates, and a sharply declining currency almost certainly to be followed by a bursting housing bubble, the majority of UK residents are already noticeably poorer now and will be even poorer later.

It isn’t and won’t be limited to the UK either.

Agreed. You can see the wallstreet celebrating BoE Pivot with a big rally! Wait till analysts suddenly forecasting Fed Pivot.

No one cares about impending hyperinflation any more in UK. The country is literally blinded by their loyalty for their “Kings and Queens”.

@WA,

If the market were certain about a “pivot” – there would have been a *much bigger* rally then we saw today. 1.8% Dow, 2.0% NASDAQ is big – but *real confidence* in a pivot would have seen a much larger rally….particularly in Cryptocurrencies.

Rapid appreciation in the USD was crushing UK, EuroZone, Japan, South Korea, etc. – so Powell is being forced to let up on the brake to avoid messing up the USA’s foreign policy goals which require those countries to be “on board”.

The timing, of course, is not great because some of the “disinflationary forces” (like COVID-Zero lockdowns in China) might be dissipating.

I’m with BigAl on this. This was a stabilization-of-current-policy move, not a pivot. It’s being played for a short squeeze.

In crazy unstable markets like we have now, if you go short, take a close look at the late 2008 charts to see if you can stomach the counter-trend 5-10% short-squeeze days that happen during panics. And always remember that the entire financial establishment collectively has to own all those assets you’re shorting, and they can and will Change The Rules mid-game to put you at every possible disadvantage. This includes buying up what you’re short (either overtly or via proxies), or banning short selling, so you’re forced to cover at worst possible time.

WS,

I am not worried about a 2% rally because “nothing goes to heck in a straight line”.

Nothing changed on ground in US as of now.

However, there was a major change in UK. BoE had 2 options to control the pound drop:

1. Raise interest rates by 600 basis point that would keep inflation in check. If Russia can raises rates by 1000 basis points in a week, the so called 5th strongest economy can do it as well.

2. Start QE again thereby releasing hyperinflation.

BoE also knows there is no way out as its crap blew up even before QT could be started.

BoE chose the second option because it feels that it can keep giving pain to its 99% but not to its 1% and it will need to keep doing more QE for significant time.

I thought these pension funds hired the best and brightest fund managers your money could buy. Turns out they are just gamblers hiding behind models that provide the answer they want.

They *have* the best and the brightest!

At least they are according to our current value system: The barrel of “the right sorts of people” has been scraped and that’s what we have.

The BoE is admittedly sticking bonds into a “bad bank” that they control “until market conditions improve”. Which sounds an awful lot like what the Fed did with QE and now seeks to unwind by selling bonds and MBS. But according to the pundits, it is never a good time to sell, so debt will keep piling up and bankers will keep making billions buying and selling derivatives to each other.

I think we should adopt North Korea as our economic model. Kamila H just said they have a vibrant economy.

These action by BoE could end up being a temporary fix, and then collapse onto itself.

In a comment yesterday, Bloomberg columnist John Authers noted: “This isn’t at core a currency crisis, but a crisis of confidence in the bond market, which is much more dangerous. The shock to gilt yields [those on UK 10-year bonds] in the last five trading days has been epic. No shock this great and this sudden has happened before.”

“The UK appears to be the first case of a truly disorderly bond selloff, where the moves are so swift that they affect the functioning of the financial system,” Authers wrote. The whole world had to watch what was happening in Britain because it was a “test case for the confidence game that’s likely to be repeated everywhere.”

It’s too bad that the quants can’t design financial models that accurately represent actual economies.

The models are designed to influence decision making so as to eventually produce the most lucrative outcome for those who commissioned the models in the first place.

In other words -the models are not broken because they themselves are designed to break things in just the right way (c.f. “Too Big To Fail”)

Quants gonna be doing their usual ruckus about “10-sigma events” and “unprecedented” “unexpected” changes over the next year.

People are wired to expect the future to be like the past, but in reality “things that never happened before, happen all the time”.

Markets don’t really do the “standard deviation” thing we’re taught in stats. Markets are human constructs, and human psychology results in chaotic nonlinear behavior.

Markets have various “regimes”, islands of partial stability, where standard deviations appear to make sense. But then the market leaves a particular regime and veers unstably toward some other one off in the distance. When those transitions occur all prior statistical data becomes deeply questionable – if not utterly invalid. That’s when the Black Swans fly and it’s time to Expect the Unexpected.

From the article: “Any pension funds which has [sic] used even moderate levels of leverage are struggling ….”

When risk gets repriced in the kinds of discontinuous jumps suggested here, with failure to hit bids as usual, and big gaps down, “moderate levels of leverage” can become dire heavy anchors dragging one to the bottom of a turbulent sea. Exhibit A: USA subprime 2008.

The models are built for fair weather. It is a sort of carry trade, picking up nickels steadily, in front of a seemingly slow-moving steamroller. Until it isn’t. It seems like fair weather will return, until that year it doesn’t.

Since a carry trade dynamic yields nickels, the temptation is to leverage up. Especially in that suppressed interest rate environment. Then — oopsy!

Fun fact: The age of the universe, in trading days, is only eight sigmas.

The most I’ve seen in a serious work was something from Goldman back in 2007 that referred to a certain market move as 28 sigmas.

I’m pretty sure you gotta be questioning your assumptions at that point.

You’re refreshingly mathematically literate and insightful for a MD

Wis-an elegant pickup of the eternal 7-10 split…

may we all find a better day.

I wonder if it has really been pension funds and not some heavy leveraged parity hedge funds, we’ll find out soon

“leveraged pension funds”: read the article; it explains what they were doing that blew up.

I did read it, but as usual the official explanation may not reveal the real reason, I’m just speculating. It is easier to get public approval for a bailout if ppl money was at stake

That wasn’t an “official explanation.” That was insiders talking to Bloomberg.

Or you have to shut down entire economies for “reasons” ;)

So it was Bloomberg’s “official” explanation. There’s still an agenda being pushed that might not reflect the full market reality.

Even if the Bloomberg version is 100% accurate, the “leveraged pension funds” have counterparties who probably don’t want to see their best customers blow up and go away. Margin calls only work in your favor when your counterparty isn’t BK and/or the collateral still has some value…

The counterparties are the investment banks of the pension funds, as I said in the article. It’s the investment banks that issued the margin calls.

Why can’t the investment banks eat the loss? And have the leverage margin call cancelled?

Without wiping out all the pension funds?

@Info, better question — why doesn’t the UK government simply suspend/ignore the rule of law, like the US did during Covid? They just have to tsll the banks that the pension funds don’t have to sell their assets or mark to market. Kind of like saying no one has to pay rent, or mortgages, or student loans, or face an eviction, or have potections from being treated like a puppet and arbitraily fired, or …

Wolf, appreciate your hard work and great article. Few days later it looks like it was BlackRock that blackmailed Boe to bail out pension funds

Mily,

I replied to another “blackmail” comment on a thread of one of today’s articles. Same answer here.

https://wolfstreet.com/2022/09/30/eurozone-inflation-spikes-to-10-in-germany-10-9-without-energy-6-4-from-temporary-inflation-mid-2021-to-runaway-inflation/#comment-469556

You gotta read beyond the headlines. The credit market was blowing up in the UK. BlackRock said it would execute on its collateral, which it had a right to do, which would have protected BlackRock but sunk the pensions. The pensions were idiotic getting into these LDIs at this scale, and so now there was a price to pay when they blew up. When you get into ZIRP, everyone starts taking huge risks. So now rates blew out in the UK, and the BoE gave everyone a little time to untangle those issues without panic selling of Gilts. It actually makes sense to me that they stepped in to calm down the credit market panic.

BTW, the 10-year Gilt yield is still at 4.14%! Not much effect of this “QE,” eh?

Wolf, next you’ll be doing an article on the housing bust 2.0 where homeowners can’t afford their mortgage when it resets from ZIRP to FFR at 4% or higher. This time it won’t just be America, but Britain and the rest of the West if they don’t soon throw the towel into the ring!

Lagarrde is particularly hilarious with her statements on how she’ll keep bond yield low for the defacto banko PIIGS but hike bond yields much higher for the rest of the EU! What????

This strikes me as the kind of thing we’re not going to know the full story behind for some time, weeks or months.

We are near the end of the quarter and some funds/plan sponsors may be about to put out some real ugly numbers.

I agree risk parity is suspect in this environment. Bridgewater in particular likes to push it, or used to.

Does it bother anyone else that the people who came up with “Leveraged Pension Funds” and almost blew up the entire UK economy will either stay employed or go work at another extremely high paying job while we’re combatting inflation by trying to put regular people who need their paychecks to eat and live out of a job as a stated goal?

Well, it is really central banks that introduced zirp and nirp causing all funds to search for yield by picking up penny’s in front of a steamroller, I think extend and pretend phase has just ended and it’s time to face consequences

Yes, extend and pretend ended when inflation went way higher than interest rates, which is a failure of price stability. They protected the labor market at the cost of price stability, it was a planned decision to limit protests during the pandemic. They will look back and say at least it wasn’t worse. Money printing is not a replacement for productivity.

Yep, you can wish and pray that you aren’t bankrupt and tell all the lies you can think of for 14 years to keep the plates spinning, but eventually reality will come calling.

2008 was a big lesson and it seems even many here didn’t learn it.

How much easier to just slam that free-money dope and drool in one’s shoe until the roof caves in. Path of least political resistance, road to heck paved with marketable good intentions.

First… As always, THANK YOU for the way you described what happened this morning. I had a basic understanding, but now have more clarity as it was the pension funds blowing up first.

This morning was very interesting. First, the news from Apple’s suppliers that production is not being ramped up as expected due to weaker demand. This news sent the Futures (particularly NASDAQ) down big. On BOE’s announcement everything changed fast. Treasuries caught a bid and DXY, which was up to 114.78 (+ .60 pre-market), only to start falling fast, which in turn sent Gold soaring and became the final impetus to light a fire under stocks. The markets have been trying to rally this week, only to run head on into rising bond yields and then the news from Apple. Markets still went back and forth before getting the all clear sign from continued dollar weakness and falling yields.

I think it goes up the rest of the week, due to

1. Oversold nature

2. Funds trying to make their Qrtly report not look as bad

3. Here’s the biggie… Everyone was short with TONS of puts being bought

All this sets us up for the reversal….an OCTOBER to REMEMBER

BTW, I was licking my chops on my SQQQ options after the Apple news, only to decide to sell them shortly after the market opened, as the yields and DXY were falling. Right now, DXY is 112.68 down 2.10 from the high this morning at about 5:00 am

P.P.S. As i was trying to type quickly, I forgot about Reason 4 why the markets will rally for a bit..

All of the Pivot People, who’ve been screaming that the FED absolutely will have to pivot, were given yet another chance to scream about the inevitability of a pivot. Now, like then, they will be wrong…

Now it looks like the financial media fake news should spin the apple story like this, “apple reportedly restart the plan to boost the iphone production despite earlier ditching the plan due to weaker demand as supply of newly printed money from Bank of England outweighed demand worries”

@Rosarito Dave,

I think *certainty* about a Pivot would have been reflected in a much larger rally in stocks, bonds, crypto and commodities.

But it *does strongly suggest* that the US Federal Reserve is being forced to co-ordinate its policies with other central banks. That much is apparent and I think it’s pretty clear that Powell’s left foot will likely not be on the brake pedal with much force…at least as far as rate increases are concerned.

A desire to *preserve* the wealth effect might not be the motivation here…but those who profit from it will see some rewards. For now.

Why do people keep calling the stock markets “oversold” when the P/E multiples ant noe even in line with current bond yields, much less the CPI inflation rate. The markets are *screaming* overbought, with the housjng market being the clearest znd first visible example.

Well… I’m not one to say I got it right when I do, but when I’m dead wrong, I own it… I was dead wrong! ;-)

@Wolf, as I commented only yesterday…

https://wolfstreet.com/2022/09/26/my-wealth-disparity-monitor-september-update-qt-rate-hikes-dropping-stocks-bonds-reduce-outrageous-us-wealth-disparity/#comment-468476

The stronger USD could pose a risk to holding together the anti-Russian coalition which is made up of countries whose currencies are geting whalloped by the strong USD.

And thus, there is the case for a pivot.

It turns out the Federal Reserve answers to “The Blob”, too.

Of course the timing is lousy, because several of the disinflationary forces of the past couple months are already dissipating…

Can’t do both at the SAME time – something will bust, the only question is WHEN???

When you have an everything bubble, surely the risks are everywhere as well. My completely conjectural prediction is that we’ll see more and more of what I’ll call “under-anticipated” crises popping up. Instability across systems in rapidly increasing, and I just don’t think it’s feasible to contain all the leaks.

Yeah, things start colliding that people hadn’t thought of as connected. I wasn’t thinking “leveraged pensions” when this gilt news first flashed ….

Yes, this is how a crisis starts: it’s always something that hardly anyone paid attention to because it was just something that has never been an issue. It has gotten big over time, and it worked smoothly, and money piled in, and leverage grew, and it made money, and the models worked just fine and gave everyone a false sense of confidence, and suddenly, the thing cracks, and threatens to blow up the financial system.

We’ll probably see more of those things cracking.

Leveraged pensions is one of the last things I would have thought…..lessons learned from.these crazy times right now.

Thanks for the info Wolf.

This seems like a perfect example of a Black Swan like Nassim Taleb describes. The models all show some structure is plenty conservative but don’t account for the “fat tails” of the distribution. As opposed to nature, which is inherently antifragile (to a point), meaning it is pretty robust and adaptive to shocks, human behaviors and financial systems tend to have positive feedback loops (e.g., forced selling), that can turn unlikely probabilities into realities right quick. And these systems tend to get more fragile and prone to such events the longer we’ve had minimal smaller shocks, as Wolf has been talking about for a long time, especially regarding Silicon Valley long-term money-losing companies.

Or maybe it’s just that I’ve been reading too much Taleb recently.

Folded like a cheap suit. Don’t tell me they had to do it. Anyone with half a brain new tightening credit markets would break something after binging on free money for over a decade. The whole point was to reverse those excesses due to runaway inflation. I guess inflation is the winner.

The pivot crowd never believed the central banks would have the guts to see it through. You and others disagreed. Well here we are. Your move Mr. Powell. Game on!

Hahahaha, look at the yield chart. The 10-year yield spiking from 1.88% to 4.63% in seven weeks: that’s a HUGE AMOUNT OF TIGHTENING of financial conditions, a lot more tightening than any QT could ever accomplish. There is a HUGE amount of tightening in the UK right now, to the point where mortgages stopped being offered. That’s the reality of drastic tightening of financial conditions.

Fair point. But that tightening came because of bond vigilantes which you pointed out in your article from a couple of days ago. Great, that’s exactly what should be happening to kill inflation and reverse the mad run up in asset prices and reign in crazy fiscal policy. But when it broke something, the BOE decided to do bail outs via QE!!! This stinks of 2008/9 when were told that we had to give rich people billions of tax payer money or tanks would roll. BULLSHIT. I’m done with the excuses. These people made their bets and should have to live with consequences. Otherwise this mess will NEVER be undone. Yeah, it’s gonna suck. But you know what sucks more, hyper inflation which destroys societies which you astutely pointed out.

My nightmare scenario is the Fed buying equities. They came closer in March 2020, buying some pretty dodgy debt.

@ Arya Stark –

good post, and not to nit-pick, but

It didn’t break anything. It just identified something that was already broken. Now the Powers are compounding further breakage by continuing the corrupt policies that they have been practicing for decades.

Thats because they never fixed the issues from 2008. 2008 was a “we’re bankrupt moment” and we decided to ignore it and print money because those at the top of the current pyramid scheme wouldn’t be at the top anymore. It’s as simple as that.

exactly as it should be.

Ironic to call it tightening. It is a marginal response by lenders to the proposed tax cuts and continued QE. I havn’t seen the continued QE plan retracted.

As you said in another post: “The BoE hasn’t even started QT yet.”

Not one dollar has been sucked out of the system. and 4% interest rates in an an 8% inflation environment; doesn’t add up to tightening from my perspective.

Getting tired of hearing the market is about to “break”. That happened long ago, this is an attempt to normalize or fix. Maybe it just breaks for those that came to rely on its artificial existence.

BP-much of human tool-making/HR-organizing civilization could be termed ‘artificial existence’, confirming your observation of reliance, and our repetitive history of empire-building-and-collapse. We may be again approaching a point where running as hard as we can to stay in the same place won’t avoid the deck being reshuffled…

(…old saying: ‘life is usually not a case of being dealt good cards, but learning how to play a poor hand well…’).

may we all find a better day.

When something in the US economy breaks as it has in the UK, how long will it take for the Fed to pivot? You can see by the Stock Market action today that “Mr Market” expects the Fed to follow the lead of the BoE. My bet is that my popcorn will not get stale before we know.

Yep. Need to watch the LBOs. Many Zombie companies have sold their debt that normally nobody would buy and put them in LBOs.

Nobody is going to want to roll over this debt now with ZIRP gone. Basically, when you hear the word Zombie Company. Those are the ones using LBOs to sell their debt. Typically, their income does not cover the interest for their debt payments so they just refinance and roll the debt over.

I keep waiting for something to crack in this space too. But the debt maybe longer dated and not do until a year or two.

I meant to say the LBO used CLOs to sell or roll debt.

What Is a Leveraged Buyout?

A leveraged buyout (LBO) is the acquisition of another company using a significant amount of borrowed money (bonds or loans) to meet the cost of acquisition. The assets of the company being acquired are often used as collateral for the loans, along with the assets of the acquiring company.

What are Collateralized Loan Obligations (CLO)?

Collateralized loan obligations (CLO) are securities that are backed by a pool of loans. In other words, CLOs are repackaged loans that are sold to investors. They are similar to a collateralized mortgage obligation (CMO), except that the underlying instruments are loans instead of mortgages.

I keep head-scratching over this trashy covenant-lite debt out there still seemingly afloat. This points toward a possible explanation which aint pretty. Then if the Fed buys and warehouses a bunch of that crap, I will start thinking the tin hat “hang”em high” crowd have a point.

@ phleep –

if the tin hat “hang”em high” crowd have a point, them they are not tin hat. and they are not.

Thank you for defining those acronyms!

Just because the market goes up or down doesn’t mean they’re blowing off the Fed or “taking the Fed seriously.” That’s nonsense. The Fed is not all powerful and often is at the mercy of the markets.

The question is: what happens when the Fed tries to fight the market? Which is really in charge?

When confidence is lost in the “can kicking”, it’s over. It doesn’t matter which government or central bank.

It may “be over” for a given central bank or govt., but the “wealth” goes somewhere. It doesn’t go into a mattress.

HowNow,

You don’t understand what you wrote. Most “paper” wealth comes from nowhere and it can and will disappear into nowhere.

What you wrote is one of the most common fallacies out there, thinking that this “value” is real and has to be transferred to someone else.

That’s what rising asset markets represents, nothing. It’s not connected in any way to the physical world and doesn’t exist except on a ledger. It’s possible for a small proportion to use it as if it’s real but eventually reality asserts itself and it disappears either through inflation or default.

AF, you’re smoking something. Currency serves as a unit of exchange. In and of itself it’s more a cultural artifact than “nothing”. If it works, that is, people exchange real things or services with it, it’s functionally a real thing. If you are arguing that currencies (fiat, gold, sea shells) are not real but only products are real, then you may want to get in touch with your brethren in prehistoric dwellings. But let’s not digress. See how many hamburgers you can buy at Wendy’s with a few bales of hay.

@ HereItComes

Wolf had a column a few months ago… if you haven’t read it, you should…

‘One of the most important dictums in finance is this: “Don’t fight the Fed.” And this could get ugly.’

https://wolfstreet.com/2022/08/03/markets-are-fighting-the-fed/

Thanks, RD and Wolf! I reread the column and it’s quite explicit and prophetic. I wonder what will happen with the apparent flight from UK assets and currency and how it will affect the FED’s resolve.

The recent UK energy and tax packages — in totality — after all additions minus (quietly announced) subtractions — are only going to add a tiny 1-4% extra to UK total state debt.

The market reaction looks ridiculously overblown.

@R2D2

That’s a very US-centric view, though. The UK’s GBP does not enjoy the exhorbitant privilege of the USD.

The UK state has significantly less debt than the US. A heck of a lot less. Adding a small 1-4% extra debt should not spark a big market reaction.

What’s more, go look at CDS swaps for UK gilts. Insurance for UK state debt. Those swaps have barely moved. No panic. The insurance industry sees this energy and tax package as a nothing burger.

You’re talking about gross debt, and that is hugely misleading. The relevant indicator is net debt and debt service cost.

US net debt is smaller then UK’s (88% vs 95%); and even before the Truss’s big plan, net interest expenses increased in UK from 10% of revenues to 16%.

Last but not least, you can pout about the irrelavancy of 1-4% PROJECTED debt increase and the mean Eurocentric media, but freezing energy bills for 2 years is a open-endend promise with a big embedded derivative on it, so no one really knows how much it would cost, and the markets just love that much uncertainity.

If you are so sure it is just hype and hopla, by all means buy a lot of gilts. And in the meantime, I also have a bridge to sell to you.

That’s because the reaction is psychological. It’s not due to the news or fundamentals.

If any reaction was overblown, it’s the bubble blown on the way up which remains intact. Not just in the UK, but worldwide. “Printing” and deficit spending (the source of this fake economy and mania) aren’t real wealth.

It should have collapsed a long time ago but virtually no one wants to hear that.

One can get a very real yacht and crowd of groupies with that fake ill-gotten wealth. So goes the tawdry fantasy. I fear for the youths tempted to give up on a legit life path.

What this 1-4% addition to state debt is expected to accomplish ? Save UK economy from recession ?

Betting on it, Wolf. Have a boatload of Tesla and Apple puts (among others). Added couple of trial Eli Lilly puts today (new 52-week hight).

Apple is trying to sell iPone 5 as new model again (iPhone 14 Pro Max).

Apple is currently priced at $149.84. When you say you have a put, does that mean you have the right to sell it at a price below that? If you don’t mind:

What price?

What duration (time which you can force the buy)?

What did it cost you?

Do you currently own any Apple stock?

Thanks.

cb, mine is not simple system to explain. I worked it out before pundemic crash. Was planning to make 10 times my investment. It actually went to 25 times, but sold too early.

Anyway, I look for sweet spots where I can buy 6 months (or longer) out of money puts for about 1% of strike price in hi-flyers. You can hardly find this now ( you’ll need VIX at around 10). When risk premiums expand (fear/panic) and prices slide, that 1% goes to 10% or more. I always get out of that trade before I have 2-3 months left on any put. Or I roll into next trench with longer timeline.

This is not easy to do.

Hope this helps.

Thank you. I seem to be a bit thick in some of the financial investment areas. I should get a handle eventually.

I do not own any Apple stock. It barely pays any dividend. And if they open western market to Chinese made phones (same quality as Apple obviously as they are the ones making them) like Huawei, then Apple is toast.

Wolf,

“2. With a 50% decline, many homeowners in aggregate would just be giving back the ridiculous casino money-printing gains of the past 3 years … Those gains were the result of central bank money printing and interest rate repression. .. So what? Easy come, easy go.”.

Well, if you look back at your chart, 2 things stand out:

1) Remember 2007 Great Recession? The ultimate factor that Monkey started printing, was because housing price went down, and brought down the consumption via collapse of Home Equity Extraction, etc. Fed Monkeys did not imagine there was such big consumptions tie to Housing. Home price did NOT even drop 50% then, and substantial deflation ensued.

So Reckless Monkey Powell would no doubt start printing or pivot when Home Price plunge. I bet at most 40% drop he would start panic pivot.

2) Look at your chart again of MBS balance. Every time there was a slow down in growth, the MBS balance went straight back up. It could never has a chance to go back to $0 since 2007, and that’s with Uninterrupted GDP growth of 10+ years and unemployment at historical low.

You can be sure, Reckless Monkeys at Fed now would embrace inflation. Heck, your Fed governor at San Francisco recently said something along the line that She has a Great Life, and many of her friends are doing Great too in life. What Inflation?! What UnAffordable Food and Home Price?! Scxxx you middle class minions. That’s what she mean and say. Look it up.

Seems you meant to post this under the housing article.

She is on record saying that cash should not be considered a store of value and thinks the Fed should not worry that money printing may increase inequality. Rather than worry about inflation she supports expanding programs to assist lower and middle-class people to buy assets to help them build wealth.

1) The deer hunting season have started. The Fed aim at 6dots on bucks

heads, but 4dots are good enough. Wall street know it,

The hunting season will be over in Jan.

2) Few Programmers making 800/day, doing nothing all day, might join tent cities, but the rest will have to work, to bootstrap themselves, There will be no more royal jubilees and checks for u and me.

3) There will be a change of character. There are about 20 million males

between 15-64, mostly minorities, watching their cell phones screen, surviving on gov disability or other “resources. It started in the sixties. Nerd #1 and #2 blasts will flush them out. Sink or Swim. Life is brutal.

A new trend.

@Michael Engel,

The UK could well be worse off than Venezuela. The latter, at least, has commodities it can trade with the world in the absence of sanctions.

What exactly *does* the UK have that the rest of the world needs when this plays out?

> What exactly *does* the UK have that the rest of the world needs when this plays out?

Fire sale. Nannies, tax-dodging accountants. High end art dealers and prostitutes. Great audio book readers with posh tones. Nice furniture that hasn’t already been hawked.

It was either Napoleon and / or H- who referred to them as a nation of shopkeepers.

> Sink or Swim.

Sort those labor markets. My college students are behaving like listless third world slackers. They will get a country up to their standards: poor and dysfunctional. They need adequate incentives. The prospect of sleeping on a sidewalk is a good start.

That’s because they are slackers. In another time many of them wouldn’t even be in “college.”

What is there so much of that needs doing?

I’ll be convinced of this shortage of hardworking young people when the right wing stops demonizing immigrants.

Phil-…mebbe a more-common-than-i like-to-acknowledge attitude that a lot of ‘what needs doing’ should be done for almost nothing by someone whose labor/humanity need not be honored…

may we all find a better day.

This chaos was triggered by fiscal easing and the chosen solution relies on monetary easing.

The BoE has not detailed the amount of its money printing operation, denying the market the opportunity to reprice Sterling with these data. That’s untenable and dangerous.

Staggeringly, the UK Government has openly denied any link between its fiscal budget and these market ructions. Genuinely, it is simply hoping the problem will go away and is preparing to blame the Bank of England if it doesn’t.

Only capable of being guided by ideology, please do not underestimate the level of inexperience at the helm of the UK government.

In the short term, there is only one conceivable way through this mess; abolish the tax cutting elements of the disastrous fiscal plan.

BOE saves the day. Makes me wonder if my pension is safe, staring at the big 50 next year, I hope my US pension fund is Too Big to Fail. Self induced affliction takes a while too heal. Liquidity is everything, trillions of dollars running in the same direction to safety, as FED tightens the vise grip I’m sure we will see a rat race to safety in US.

Where’s them pivot deniers now?

I was contemplating posting the very same question. ahem & cough. Going to fight the Fed here boys.

Show me the Fed pivot! Where is that dang thing??

Yellen says all clear, no liquidity and/or deleveraging issues as far as she can see, which is about what, 3-4 inches from her face from past blunders…HA

Per Bloomberg:

Yellen on Tuesday downplayed the turbulence, saying that financial markets are functioning well.

“We haven’t seen liquidity problems develop in markets — we’re not seeing, to the best of my knowledge, the kind of deleveraging that could signify some financial stability risks,” she said.

Wait for the Feds moment of truth! The BOE just has theirs. And what did they do – pivot!

The scary part about any future “Pivot” is that it only takes a single phone call and 24 hours for one of the Fed(s) to panic and poof…”Too Big To Fail”

Per FT.com

“It appears that some players in the market ran out of collateral and dumped gilts,” said Peter Harrison, chief executive of Schroders, which has $55bn in global LDI business. “We were more conservatively positioned and we had enough collateral to meet all of our margin calls.”

But a senior executive at a large asset manager said they had contacted the BoE on Tuesday warning that it needed “to intervene in the market otherwise it will seize up” – but the bank failed to act until Wednesday. It declined to comment.

Got that Hickory mallet handy?

Throwing good money after bad?

Oops. Got that wrong. The pivot deniers are licking their chops, thankful for the opportunity to get short.

May 2007:

Bernanke: Subprime Mortgage Woes Won’t Seriously Hurt Economy

September 2022:

US Treasury Secretary Janet Yellen has moved to reassure markets about the health of the global economy after the IMF stoked fears of spillover from the market crisis in the UK.

Ms Yellen insisted that financial markets are “functioning well” as the relentless rise of government borrowing costs paused and stocks in Europe and on Wall Street bounced back.

Wait a minute. So things almost blowing the eff up in GB is cause for a giant rally here? Are the pivot dreamers still pushing the action? This might be my chance to short the market soon.

1) Big Al, UK deflated like Turkey. Turkey became a major industrial power

serving Europe and the ME. Inflation crushed Turkey’s working people.

2) London RE deflated, but within few years England will compete with Germany.

3) Those who collect “rent” will suffer. The rest will have to work to survive.

4) In the last 70 years gov interventions dominated politics, ex Maggie.

5) Inflation will force men to work, do less bs. New immigrants, refugees and the illegals will compete in the job market.

6) Inflation is changing the labor market characters.

7) Italy Seria “A” might imitate EPL.

8) The BOE might imitate Turkey yield curve : The front end is higher than the long duration.

9) Backwardation in US

But what about of the female’s in HR and DIE?

What about the hurricane?

The elephant in the room is that those pension funds were robbed of their income for more than a decade by the artificial suppression of long term rates brought about by central bank quantitative easing. They were encouraged, perhaps even forced, to engage in risky derivatives to replace that lost income. Now more quantitative easing. The real villains are central banks.

Totally agree: this has pushed pension funds into very risky investments that are now coming to haunt them. This includes mundane things like a much larger portion of holdings in stocks. The ZIRP-era will turn out to have been a very costly experiment.

It’s been a very rewarding experiment for insiders and those on the right side of the trade. rewarded corruption …………

Wolf, do you cover a broad-based view of US pension funds in any of your articles on a regular basis, even if very infrequent? The good old 60/40 portfolio is looking pretty sketchy nowadays, ripe for blowups soon?

I’m not sure that TIAA-CREF needed that much encouraging to get into risky investments. As of 2021, TIAA had more than 5 million active and retired employee accounts at more than 15,000 institutions, with $1.3 trillion under management. Back in the 1990s “TIAA shifted its model to become a for-profit financial services corporation.”

QCGRRX, a CREF growth fund account, is down 34% from its Nov. 1991 high. Thanks partly to Wolf’s articles, I got out of QCGRRX sometime in mid-1991. I only got into it to ride the bull for a while anyway.

Since I consider TIAA-CREF to be corrupt bloodsuckers, my small next egg there is the first thing I am liquidating in retirement. It take about three years, in order to keep my SS and other income from being taxed.

Oops, replace 1991 with 2021

“Collateral buffers” sound a lot like algorithmic stablecoins.

“So this is a mess, and there are no good solutions”

I seems to me that this has become the permanent state of Western societies, and that there is no exit from this state unless via the path of sound money that ruling class can’t counterfeit.

Sound money is what bitcoin is. It was designed to be controlled by no one[1].

[1] And I mean bitcoin not other cryptos like Ethereum, which has sold out to PoS.

It is amazing that investors front ran and the mkts zoomed, on what assumptions?

1. Similar (like UK) events can happen here. Most of the pension plans in UK are ‘defined’ benefit, risk to the employers, unlike here more like defined contribution. which puts the risk to the employees.

2. B/c of the global financial chaos, Fed may pause or pivot soon!?

3. Is the money coming into the US mkts, from outside?

Is bad news is good news is back!?

US FED would not hesitate to pivot as early as possible. A precedence has been set

jon

As usual a bear trap rally!

Small traders are bullish. They know they are going to win in the market.

Successful traders are bearish. They enter a buy preparing for a loss.

When they lose they don’t blame the Fed or madam ECB. They cut their losses.

In 2016 UK gambled on Brexit. The BOE deflated GBP/USD. It breached the Plaza Accord in Feb 1985 low. It’s a trigger. It might carry England

to better days.

Leveraged pensions to juice returns is a direct result of central bank yield repression. BoE bailing what they caused.

or, a direct result of over promising benefits

Yup. 100% this.

“liability-driven investment (LDI)”

——————————————–

In common American English we would just call that gambling ………..

Why would a pension fund EVER lever itself (either derivatively or otherwise) in any way? This is the height of “too smart by half” idiocy. Now they’ve basically held the entire financial world hostage. QT cannot continue, and inflation will continue to rampage.

They have only held the world hostage if the world allows it. The answer is not to cave, but let them eat their just deserts, providing what ever binding payable guarantees that were offered and providing welfare if needed to keep affected pensioners from starving.

The pension system needs to be reformed, particularly government pensions.

and prosecuting the fund managers, where possible …………

“The amount of liabilities held by UK pension funds that have been hedged with LDI strategies has tripled in size to £1.5 trillion in the 10 years through 2020,” according to Bloomberg.”

You get these strategies because the pension funds end up owning tons of long term government debt with microscopic yields. The other alternatives, while maybe more honest, is to cut benefits to present recipients, or greatly raise the contributions of the workers hoping to draw on the pensions in the future.

The other alternative is for central banks to never-ever push interest rates to 0%. That is just totally nuts, and going forward, those ZIRPs are going to turn out to have been very costly.

the whole concept of central banks and the FED has turned out to be costly for many Americans. Look at the coast of housing.

It’s part of a grift. A confidence game designed to concentrate ownership and power.

cb-whether spell-check, wide fingertip, or intentional, ‘coast of housing’ made me spray my java, yet again, on the keyboard…

(Wolf’s most-excellent establishment’s host and commentariat give me smiles far beyond those expected in a den of the ‘dismal science’…).

may we all find a better day.

Yep…2008-09 took us down the rabbit hole and we’ve been going ever deeper since.

Or the government could have not cut interest rates so low in the first place and paid a decent return on bonds.

So in order to prevent the collapse of a distorted financial system, we keep piling more liquidity and debt on top of the liquidity and debt that has already caused the system to be unstable?

Where does it end?

1. US people calling out Uk is lie pot calling kettle black. US FED will exactly do a pivot just like them.

2. Inflation will be brought under control, either by raising rates or changing the real definition of inflation.

3. UAW once ran a gambling casino from the Pension fund. Seems like, they are more honest than our pension funds.

4. Uk is the source of the word bubbles. (Not as in every english word must come from Uk). They caused so many financial panics such as south sea bubble, canal, railroad and so on. The world bubble officially entered the book.

5. uk is just another PIIGS of europe.

6. Germans might be wondering where the brits got the idea about printing too much money?

7. We must conduct another referendum for wolfstreet. QE or QT 2023?

Love to come here to mock some loser who had been losing money since Jun 2020, and hoping this year will finally be the year for him to recoup, but ended up losing more due to his greed to not close his position before the fed pivots. Feels so bloody good. Please ban my comment. It’s good enough to know that you have read it and got hurt by it. Feels so good!

Been a good year so far for my short position, thank you for asking. It’s up something like 22% YTD.

These kinds of silly comments come out of the woodwork only on the few up-days in the market, and you’re silent during the long series of down-days. It’s such predictable trolling, that it’s funny.

Like.

Thanks for letting that comment through, it was good for a laugh as the market has already coughed up yesterday’s gains.

Time to raise Fed Funds Rate to 3.5%.

Looks like the GFC was not fixed. It’s taken a lot longer that I expected, but it appears that we are now out of the eye of the hurricane, and this side of the storm is exponentially worse.

ZIRP sure was fun while it lasted! But what cannot continue, will stop (Herb Stein)

Some more context might help frame the market’s reaction more clearly:

Liz Truss promised tax cuts of £30bn in order to win the election. Then Kwasi Kwarteng unveiled his “plan for growth.” That included an additional £15bn of handouts, which are going to the richest people in the UK, who clearly don’t need handouts – especially when families are literally making decisions as to whether they will run the heat or buy food.

Remember all of this is on top of emergency support for energy bills, which will cost around £60bn for just this winter alone.

Did the Smart Money Act Like Fools Today?

In an earlier comment in this article, Wolf wrote:

“…and suddenly, the thing cracks, and threatens to blow up the financial system.

We’ll probably see more of those things cracking.”

On September 18, in response to Wolf’s podcast, I wrote:

“But what happens next time once the reserve drawdown from QT crosses that critical inflection point and some multi-trillion-dollar market sector experiences sudden and unexpected strains due to a cash shortage?

With inflation still raging, will the Fed intervene again?

If it refuses, the economic gyrations will be profound.”

So what happened today?

Prior to today, you have the BoE saying it is prepared to “hike rates to whatever is needed” to fight inflation (see Wolf’s article on September 26).

Then, with inflation at generational highs at 10%, on September 23 (five days ago) the UK politicians announce a spending-and-borrowing spree.

The markets reacted appropriately because they detected that the politicians don’t seem to care or understand that government deficits don’t overcome recessions but will fuel inflation.

Either way, despite how small the spending program is in terms of GDP, the policy signals an attitude: long-term tolerance for inflation. So in response, the bond vigilantes “rose from their graves,” as Wolf so eloquently put it, and dumped their bonds. Rates soared. It was not “tightening” that broke the markets. It was the skyrocketing investor demand for an inflation premium.

Private investors announced they would not be buying anymore long-term UK debt at the cheap rates at which the government wanted to sell them. The result is that the pension funds (and who knows who else) who are leveraged to their eyeballs got caught short.

The pension funds represent the British boomers. They represent the financial interests of a dominant voting block. And that voting block has the nose of the politicians. That voting block is clear: the government will not visibly default on its pension obligations to granny. It prefers another way.

So what does Britain’s central bank do just as it is talking tough about “raising rates” to whatever is needed to fight inflation?

It acts exactly contrary to its words and monetizes the government debt. What will be the result?

Higher inflation.

Make no mistake, what we witnessed today was default: default by the UK pension funds. But a visible default, calling it a default, and forcing the world to see that the pension funds are unable to meet their legal obligations, would trigger derivative contracts and default insurance. That would cascade into a “credit event.”

So instead, the Bank of England, the world’s most ancient central banking organization, in partnership with the politicians, publicly announced that there will be no stomach for open defaults. Instead, they are committed to a policy of concealed default through mass inflation.

And what happened to the value of the British pound compared to the US dollar in response to this long-term inflationary announcement?

It rose.

How in the world did the British pound, after the British politicians and bankers announced a joint commitment to diluting their currency by inflation, RISE against the tightening, deflating US dollar?

Either the smartest investors in the world in the currency markets are idiots…

….or else they are projecting confidence that the Fed will shortly follow suit and resume inflating the US dollar also.

The Fed and all central bankers have only two tools: inflation and blarney. Today, the Bank of England used both.

Will the Fed also fund a series of concealed defaults in the US through mass inflation?

Or will it stick to its guns and let the markets do their work?

I would ask granny if she is okay with open defaults on pension obligations. Her answer will tell you all you need to know.

Pancho – well done.

So, the gauntlet’s down. In this corner, we have:

Wolf, who’s adamant that QT continues, rates rise until inflation falls, come what may…Wolf is accompanied by a host of schadenfreude-ers and some wistful-for-normalcy types…

And in this corner, we have:

Pancho (stand-in for Granny), BigAl (who recognizes the power of the Blob) and a host of other people who are wondering why the Powers had to distort the markets _that_ much to keep the plates spinning, and why the Powers react _so_ much when (apparently) rather slight disruptions occur.

Well, my vote is with Pancho, BigAl and those folks.

If it can be said “don’t fight the Fed”, it can also be said “don’t fight the Blob”. Granny’s tough, but she’s a pushover compared to the Blob.

The Blob showed their power @ GFC: a little tightening, a sell-off in RE, who-coulda-known-the-models-said-its-cool caused some cascading…

Fed dramatically changed course, bailed ’em all out.

Followed by 15 years of can-kicking with no structural changes to speak of except ZIRP, which was how they delayed the reckoning.

Granny got ripped off; even she was no match for the Blob. Neither is the Fed.

Gonna be the same this time till it just comes apart altogether.

I do respect your effort, Wolf, to get the market to transmit the message.

However, I think you’re not giving enough credence to the politics (e.g. the who-gets-what part of “political economy”). Inflation hurts the little people way more than the big people.

“to cut taxes for the rich and for corporations, funded by new debt, while piling on spending to subsidize energy costs, also funded by new debt, thereby requiring the issuance of large amounts of new debt, even as inflation has already reached to 10%.”

Some of that sounded very familiar. Uncle Sam too loves cutting taxes for the rich and big corporations, and the national debt has been growing like crazy.

Basically coming to the USA in a couple of years.

The main difference with the US is that we are the world’s currency, so during times of financial stress, the dollar just moves higher. In a world of one-eye men, it is the man with two eyes that is king.

*wink*

The world’s reserve currency can always change.

I’m not familiar with the specifics of British tax law but a 45% marginal tax rate at about $165,000 taxable income is obscene. (That’s what I read elsewhere.) Unless someone in that bracket has massive deductions to exclude most of their income, this isn’t close to being wealthy.