The Case-Shiller index, which lags by several months, is starting to flip market by market, including in Phoenix, Dallas, Washington DC, and Boston.

By Wolf Richter for WOLF STREET.

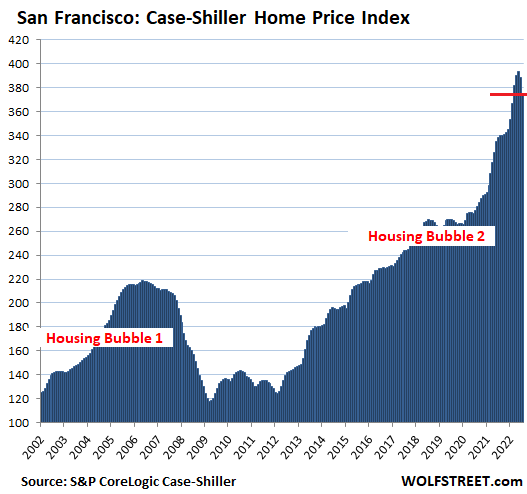

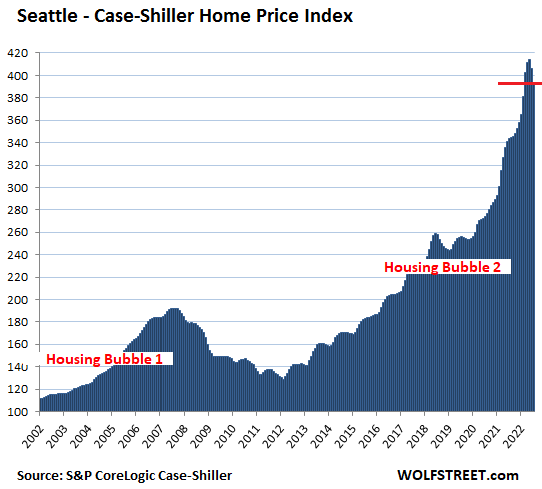

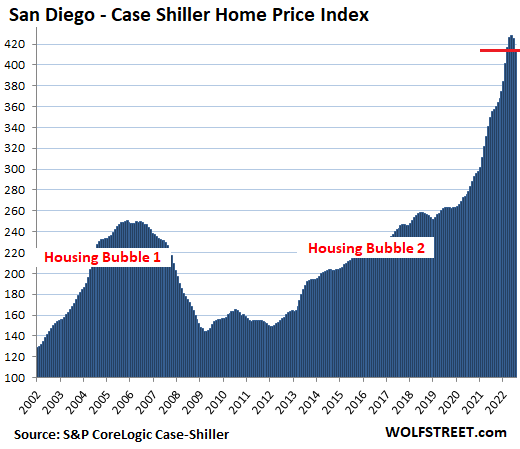

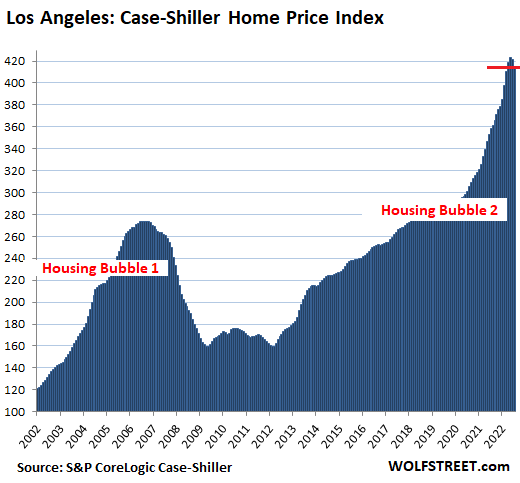

A month ago, the S&P CoreLogic Case-Shiller Home Price Index, which lags housing market reality on the ground by 4-6 months, started picking up the first month-to-month price declines, all of them in the West: the metros of Seattle, San Francisco, San Diego, Los Angeles, Denver, and Portland.

Those price declines have now sharply steepened, according to today’s Case-Shiller Home Price Index, and price declines are now spreading across the US, including Boston, Phoenix, Dallas, and Washington DC. And what a huge shocker, even in San Diego, the #1 Most Splendid Housing Bubble in America, prices dropped by 2.5%, the metro’s largest month-to-month drop since Housing Bust 1.

That the housing market is seriously weakening in sales and prices across the US has been apparent in other data that is more immediate but easily skewed by changes in the mix of what was sold. The housing market in California is among the trail blazers, with dismal sales volume and sharply dropping prices. In the big Bay Area counties, including San Francisco, the median prices are down below where they’d been a year ago, and even in Southern California they’re seriously sagging.

Today’s release of the Case-Shiller Index was for “July,” which consists of the three-month average of closed home sales that were entered into public records in May, June, and July. Due to the delay between when a deal is made to sell a house and when the “closed sale” is entered into public records, the time span today for “July” roughly covers deals made in April through June. During that time, the average 30-year fixed mortgage rate was in the 5% to 6% range.

The Most Splendid Housing Bubbles where prices fell.

In the San Francisco Bay Area, house prices plunged by 3.5% in “July” (three month moving average of May, June, and July) from June, the steepest month-to-month drop since February 2012, at the bottom of Housing Bust 1, after having dropped 1.3% in June.

These two drops came after the ridiculous spike over the past two years, and brought the year-over-year gain down to 10.8%, from 16% in the prior month and from over 24% earlier this year. A couple more drops like this, and the index will catch up with the median price and be negative year-over-year.

For the Case Shiller Index, the metro consists of the five-counties covering San Francisco, part of Silicon Valley, part of the East Bay, and part of the North Bay.

In the Seattle metro, house prices plunged by 3.1% in “July” from June, the biggest month-to-month plunge since January 2009, during the depth of Housing Bust 1. This followed the 1.9% drop in the prior month. Both drops combined wiped out the prior four months of gains, thereby going down on the other side of a totally ridiculous spike. This slashed the year-over-year gain down to 8.4%, from 27% earlier this year.

In the San Diego metro, house prices fell by 2.5% in “July,” the biggest month-to-month drop since January 2012, and the second month-to-month decline in a row, after a most splendidly ridiculous spike. The index is now below the March level. This slashed the year-over-year gain to 16.6%.

The index value of 414 for San Diego means that home prices shot up by 314% since January 2000, when the index was set at 100 (over the same period, the Consumer Price Index rose by 75%). The index for San Diego has now dropped to the same level as Los Angeles (414), and both share the honor of being the #1 Most Splendid Housing Bubble in America.

In the Los Angeles metro, house prices fell by 1.6% in July from June, the sharpest decline since March 2012, and the second month in a row of declines. This whittled the year-over-year price gain down to +15.7%.

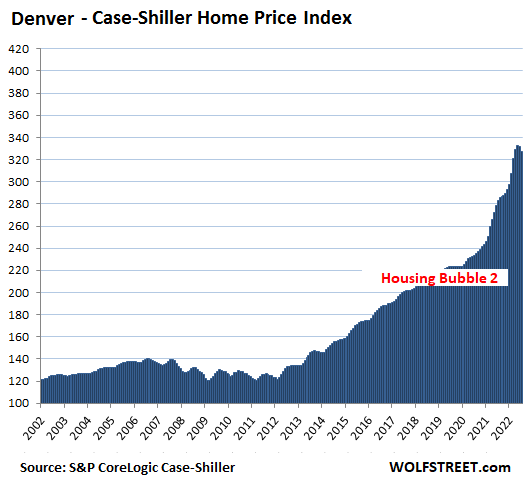

In the Denver metro, house prices dropped 1.4% in July from June, the second month in a row of declines, whittling down the year-over-year gain to 15.6%:

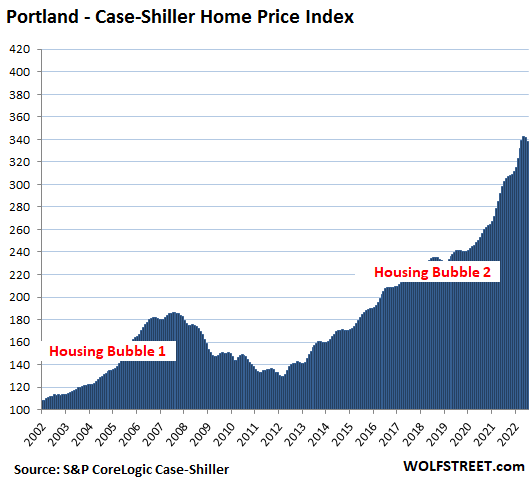

In the Portland metro, house prices dropped 1.1% in July from June, the second month in a row of declines, after a ridiculous spike. This whittled down the year-over-year gain to 11.7%:

The Case-Shiller Index uses the “sales pairs” method, comparing sales in the current month to when the same houses sold previously. The price changes within each sales pair are integrated into the index for the metro, and adjustments are made for home improvements (methodology). By tracking the change in dollars it took to buy the same house over time, the index is a measure of house price inflation.

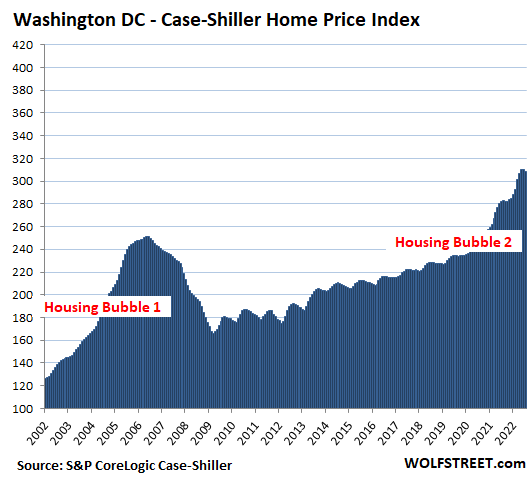

In the Washington D.C. metro, house prices dipped 0.7% for the month, after having been flat in the prior month. This whittled down the year-over-year gain to +9.4%:

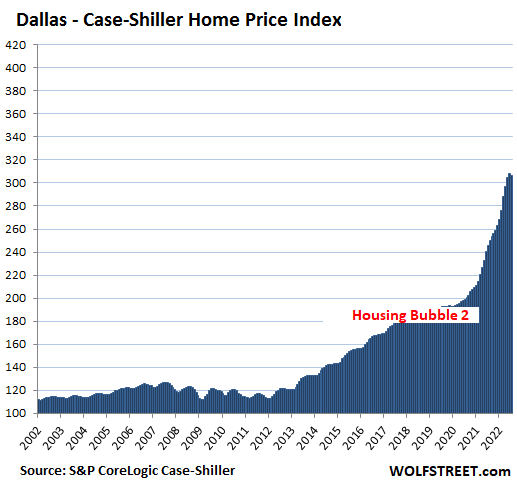

In the Dallas metro, prices dipped 0.4% for the month, the first decline since 2019. And while this seems like a small dip, it was the largest decline since October 2012. This whittled from the year-over-year gain to 24.7% from the 30%+ range earlier this year.

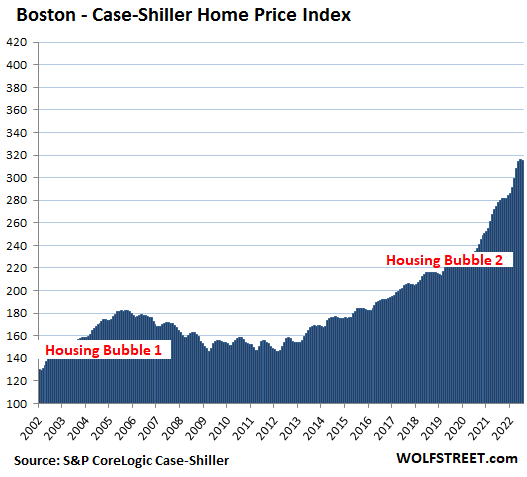

In the Boston metro, house prices dipped 0.3% for the month, which whittled down the year-over-year gain to 13.3%:

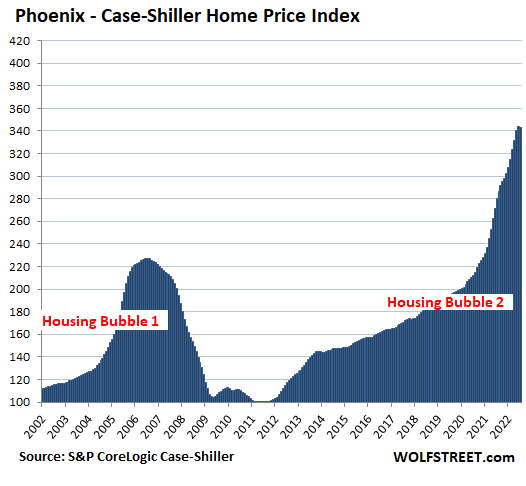

In the Phoenix metro, house prices edged down 0.1% for the month, so roughly flat, after the huge spikes earlier this year and last year. This whittled down the year-over-year gain to +22.4% from +32% earlier this year:

The Most Splendid Housing Bubbles where price gains “decelerated” or stalled.

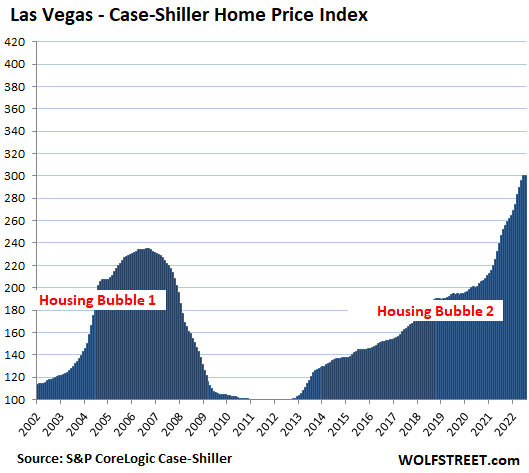

Las Vegas metro: prices stalled and were unchanged for the month, compared to jumps in the 3% range earlier this year. This whittled down the year-over-year gain to +21.8%, from the 28% range earlier this year:

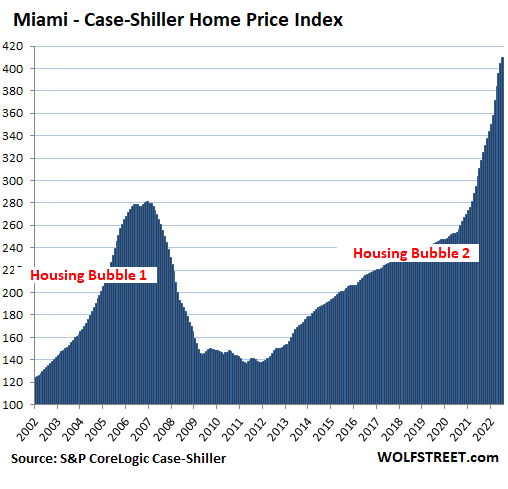

Miami metro: +1.3% for the month, “decelerating” from month-to-month gains in the 3.5% range in prior months. This whittled down the year-over-year gains to a still ridiculous 31.7%, from +33% in June and +34% in May.

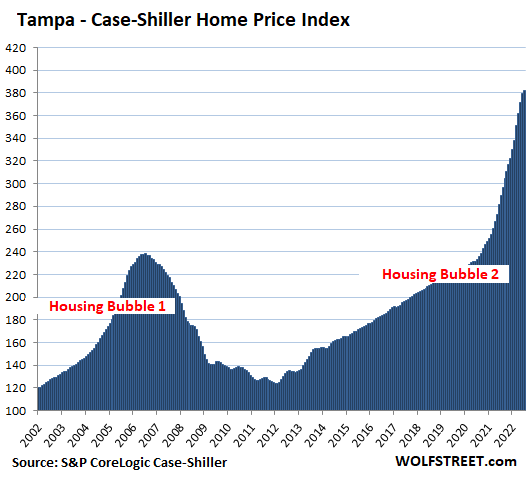

Tampa metro: +0.6% for the month, decelerating from 3%+ gains earlier this year. This whittled down the year-over-year spike to 31.8% from 36% in the prior month, still solidly in ridiculous territory.

In the New York metro: +0.2% for the month, decelerating from the +1.5% range in the prior months, which whittled down the year-over-year gain to +13.7%:

Based on the Case-Shiller Index value of 276, the New York metro has experienced 176% house price inflation since January 2000. The remaining cities in the 20-City Case-Shiller Index (Chicago, Charlotte, Minneapolis, Atlanta, Detroit, and Cleveland) have had less house price inflation and don’t qualify for this illustrious list. Among them, there were monthly declines in Detroit (-0.1%) and Minneapolis (-0.2%).

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is the most epic roller coaster of the last 40 years.

wonder how may Gs the next drop will exert? Gonna be a fun one!

These homes are so unaffordable now. Prices near all time high and mortgage rates more than doubled cutting affordability on 30 year mortgage to half.

These houses won’t be easily sellable despite a 50% correction!

Spot on. And mortgage rates will probably still increase further.

My amateur guess, anyhow.

Throw in a $100k pickup truck on top of the $800,000 starter home. What the FED and politicians did to this country was criminal. There should be prison sentences for these people.

I think we will see drops of ~25% in some of the hot markets. This will play out over the next 12-18 months. I think the currency crisis, the economy and bond market will crack and the Fed will step in (possible pivot) by Q2 next year. I think unemployment will hit almost 5% by Q2.

Our economy (and the rest of the world) is SO far in debt that we will see such low growth and we will see low interest rates again.

Real Estate will continue to provide riches and tears to those who invest. Those who have the fortunate sitution to buy and live in their home for 20+ years will be able to accumulate wealth but have to ignore the gyrations and hope they don’t lose their job…..

The Fed will pivot long before that. Look at the BoE capitulation and restart of QE. Things are already breaking. Fed is not even getting to 4% inflation.

Carl,

Seattle dropped 3% a month and data is 4 months old. Most of Seattle has already dropped 15% by now. It will reach 25% within a quarter and 40% in a year. The fall will be faster than rise thanks to 7% mortgage rates.

First rule of investment buy low. So real e is not an investment today. Also a house needs maintenance (1.5%/year) and property taxes and utilities and HOA.

Carl, also you do sound just like the real estate agents that I come across in open houses that are on market fo more than 2 months without a single visitor.

Can’t blame you, it’s a tough business now. Will advice moonlighting for next 2 years.

“….the Fed will step in (possible pivot) by Q2 next year….”

Oh, it’s the pivot CROWd again.

Smartest person I’ve ever heard! If they are not listening shame on them! I’m going to loose my ass and your telling everyone it’s happening!

People please pay attention watch the debit to income ratio this is what he’s trying to say!

the problem I have with this kind of analysis is that it assumes that the mix of homes that are selling is constant.

yet in areas like those on the west coast, much of the price change can be explained by a change in the type of homes on the market

unlike 2008, most homes are either free and clear or financed with traditional hyper low long term mortgage rates.

When and if the real estate market becomes a real problem is when unemployment rises and defaults rise. The last time that number bottomed out was around q2 2005 at 1.6%. Over the next 5 years that shot up over 10%. We are now just below 2% and has been trending down.

Lower home ownership rates- particularly at the entry level means that those most at risk of losing their jobs and having less financial reserves will likely delay impact to the mortgage industry. But when it does rise, it could be even faster than 2005-2010.

So start watching the eviction data. That will be the canary.

The analysis presented here is based on the Case-Shiller index which uses sales pairs of the same home. The analysis therefore does not assume the mix of homes that are selling is constant or that price changes can be explained by a change in the type of homes on the market. Case-Shiller avoids both those problems by looking at resales of the same home.

Tottaly epic. Stock market is down all the way back to January 2021 level. I even see housing prices decline when I use my good reading glasses.

Even worst, it looks like UK central bank has already started pivoting with bond purchases as pound starts going to heck and bond yield rises. I predict hyperinflation in UK by end of 2023!

There a banana replic followed by Japan,eu,USA China. Hell the whole world is leveraged like never before ,maybe fiat currency is the problem.Also common sense went out the window long ago .The RESEY is here prepare accordingly

Thank you Wolf, Good News!

Price reductions stalled a bit in my area when stocks went up, now looking to see them fall a bit more. Everything still a bit out of my (and most peoples’) price range..

A lot got taken off the market when stocks went up, it’ll be a while before they come back, at yes, a reduced price.

No Austin or Houston?

Thanks Wolf for your report.

IN San Diego, home prices went up almost 50% or so in last 2 years and people with skin in the game are feeling invincible.

Yes, that’s why these price spikes can be so dangerous to your wealth — they cloud your vision. Been there, done that.

I bought in San Diego county in 1985 at $55k. Still living in the same house And now the house next door just sold for over$1M!

Never thought I’d see thin in my community.

TRUE that Wolf, also been and done, etc., and paid dearly for that cloudy phase…

Meanwhile, the spike is SO much that our 70+ year old ”cottage” has got to the point that the alleged value is really and truly mind blowing — driving some of us to at least drink more, if not seek a retreat somewhere…

WE, in this case the family WE, are very thankful to be homesteaded in a state with small cap on property tax rises,,, as well as state mandated ”real” evaluation so that IF residential value falls, so do taxes…

GUV MINT immediately starts looking for ”fees” that compensate, but those also seem to be capped here.

Very true. All my friends that own in San Diego think the value of their house will stay inflated. It will take a bit longer for them to realize their property is worth 30% less than it is today when one of them trys to sell and they have to keep dropping the price and still nobody buys.

I feel so fortunate to have sold my place end of May this year. I’m sitting on the sidelines renting with my pile of cash waiting patiently. I say another 6-9 months and we should have huge drops!

Could it really be different this time in that institutional investors will snap up everything before prices can crater?

No, because institutional investors hate to overpay. Last time (2011-2012) the snapped up houses after prices had collapsed, and they snapped them up out of foreclosure. They didn’t overpay at all. They went for the deals. Today’s prices are ridiculous. And it’s hands-off time for institutional investors.

Wolf, do you see institutional investors selling sooner than later? I know Zillow and Black Rock bought up a bunch of real estate. I guess my question is will they liquidate their holdings now while prices are still relatively high to avoid losing too much money as the air comes out of the ballon? Or ride out the market?

Institutional investors know that there is a lot of crap in balance sheets. So they are still hoping that something will brake causing Fed to Pivot.

Fed is going too slow promising a softish landing. However there has been no landing. The real proof will come when something really breaks (a 5% drop on 50% jump is not enough).

If the Fed frets and pivots, the 99% will get screwed, if not, the institutions will fret and stop dumping. So far its all jawboning and we still don’t know who will blink first.

Correction: Institutions will fret and “start” dumping.

Rick,

Let’s not lump Zillow and BlackRock together.

Zillow was trying to flip homes, lost a ton of money, and then got out of it by selling them mostly to some financial firms. I don’t know what the buyers intend to do with those houses.

BlackRock is a fund manager. It bought some existing rental properties with tenants in them from other institutional landlords and grouped them into funds that investors can buy shares in, similar to apartment properties (high-rises, etc.). It’s NOT buying any homes on the for-sale market. Never has. If it sells its properties, it would be to another big landlord. Most of the houses are purpose-built for rentals, and they’re usually in subdivisions of nothing but rentals, with its own leasing office. These are just income-producing assets (hopefully) that are getting shuffled around between big companies. They were never designed to be sold to individuals, and will likely never be sold to individuals.

It’s not as lucrative to buy houses at these rates. They are hands off until the general public is in tears and are forced to give up their homes.

Wash, rinse, and repeat. The uneducated home buyers (FOMO, YOLO) will probably take it on the chin.

Some distressed debt and assets private equity will come in and swoop up more properties. I think I read Blackstone is building up a war chest for such an event.

During HB1, you would be surprised few great deals there were. Banks many times sold blocks of properties to insiders or big companies and never let the public have a fair chance to pick up steals. You could get a decent deal but not those 50$ price cuts shown on Zillow.

Is HB1 an abbreviation for the global financial crisis?

If so, there were bargains galore. Tons of houses in Phoenix and Las Vegas and Florida that could be had at any price. Lots of short sales and bank owned properties in Denver where I was at the time as well. If you couldn’t find a bargain in 2010 to 2013 you just weren’t looking. I passed up on one short sale not far from where I live in 2012 that would have netted a 400% return…

HB1 = Housing Bubble One, which was part of the global financial crisis.

Wake me when those graphs look symmetrical. They still look obscene to me.

There is the bear cub,

There is the bear,

There is the Grizzly bear,

Then there is Depth Charge.

Please don’t feed the animals.

I have a blanket ditto for Depth Charge when he hits the Fed and speculators. Saves me from having to comment.

“I have a blanket ditto for Depth Charge”

Me too Way to go

Still gotta say, for us lowly monthly payment non cash buyers, the bubble is just getting worse.

Let’s take Seattle and say it’s been a 10% reduction in housing sales prices since the peak.

600k dollar “starter home” – 10% = 540k

600k @ 3.5% w/ 20% down = 2155/mo

540k @ 7.09% w/ 20% down = 2900/mo

That’s just principle and interest. With Google’s handy dandy taxes and insurance, it’s 2955/mo and 3621/mo respectively. That’s what, a 20% increase in housing costs to us mortgaging serfs in a matter of a few months?

Wake me up when interest rates are at 10% and housing has cratered 60%. I’ll be watching then. I’d also like to say that in the zips I watch, there is no price cuts to stuff at the low end that amount to anything noticeable. Nothing is selling anywhere here anymore but the price cuts are to everything over 500k. And even those are a snooze fest when rates have doubled. 20k off of a 700k asking price is utterly laughable.

Spot on.

Yes indeed the NAR’s HAI will likely hit new 35 year lows this month.

It may yet hit an all time low in the next few months.

If prices do drop significantly and take house payments back to what they were last year it’s probably a much better deal for the buyer – much more deductible interest, lower property taxes and much more likely to be able to refi to a lower rate at some point in the future.

I still see the low end threshold increasing month over month in several metros. That may continue for a few months, even as the median price comes down.

It’s true but list prices aren’t reflecting current reality, it’s very likely a lot of those homes don’t sell and get taken off the market. The only people who sell at a discount are those who feel they “need” to, there’s not many of those at this time. If there is to be a significant housing correction then it will take time, people have to be in a position where they have no choice but sell at lower prices, but if that happens it may not make it any better for us working stiffs because many of us could be out of a job in that scenario and not able to buy anything anyway.

Some sellers may even make money. They bought that long ago that selling now for a “profit” is better than waut and sell for a smaller “profit”. Those that bougt on top of housing bubble one is still on the black.

Yes, was going to mention them as I know someone who has been “deleveraging” like my last RE agent who at one point was holding around 20 homes. Anyone who is dealing with primary residence though may see a profit but then still have to pay high prices for a new property, the very few I know about who have done that went for a location they prefer or to a cheaper market to reduce or eliminate their mortgage. So those people don’t make up a huge number right now and everyone else is holding tight to see what happens next, that’s why sales are so low.

Not really sure what happens next, I think we need something to give in order to see prices move down significantly or sustained interest increases that will eventually catch up with more people who are in over their heads. Then again, wolf alluded elsewhere to the possibility of FED reversing course at that point, which would probably reduce the number of people in trouble and therefore the “discounts” some are hoping for.

I don’t know enough to predict anything, that’s why I come here and read, best analysis I’ve ever come across.

That is why if mortgage rates stay at ~7%, housing prices will come down more than 10%….

Is 3.5% really a plunge?

More a medium doopledalsh.

“In the San Francisco Bay Area, house prices plunged by 3.5%”

Minus 3.5% in a month = 42% annualized. Given the context yes that is steep.

It’s actually 35% annualized BUT agree that it’s very steep and given the worsening conditions since then (significantly higher mortgage rates) the pace of declines is likely to accelerate if anything.

A 35% drop would erase all the pandemic gains and more.

How did you get to 35%? He’s right 3.5×12 months = 42.

Austin,

It works this way:

$100 – 3.5% = 95.6 – 3.5% = 93.12 – 3.5 = 89.86 – 3.5% = 86.72 – 3.5% = 86.68 -3.5% = $80.75

So after six month of dropping 3.5% each month, the value has dropped by 19.25%; And YET: 6*3.5% = 21%

You see, each month that the value drops 3.5%, there is a smaller base left over (in $) to drop from, and the base shrinks each month, and so the same 3.5% represents a smaller dollar drop each month.

not to split hairs, but if you live somewhere with twelve months per year, i think the 42% figure is correct. ;-)

Austin:

There’s a formula for compounding to make it easier:

For each $1000, decline of 3.5%/month for 12 months:

1000 x (.965^ 12 = $652.12.

~(35%)

Alternatively, if it were an increase of 3.5%/month:

1000 x (1.035^12) = 1511.06.

~+51%

Maff is hard.

Google “future value” formula and/or

“future value calculator”.

The total is (1 – 0.965^12), not 3.5 x 12.

As others have tried to explain the concept of compound interest working in reverse, it can be a bit hard to grasp. Especially if one already has an answer firmly entrenched in their mind.

Let’s try to address that sticking point first. If one accepts the answer can be arrived at by simply multiplying -3.5% x 12 = -42%, then after 3 years, the drop would be -42% x 3 = -126% which means the seller would be paying the buyer 26% to take the property off their hands.

One has to think of this like a bucket of water having a hole low on one side. When the bucket is full, water spews out quickly, but as the level drops, the flow slows. As the water nears the bottom, the flow slows to just a drip, but it never stops completely. One gets a completely different answer if one measures the initial flow and assumes it flows at that rate constantly. Especially if one extends the time frame and calculates more flowing out than the bucket initially contained.

2banana,

3.5% month-to-month adds up in a hurry. That’s very fast for RE, which moves slowly. So you don’t want many 3.5% month-to-month plunges in a row. And they don’t occur outside of a Housing Bust. Last that occurred in San Francisco was in Feb. 2012.

“Is 3.5% really a plunge?”

Not when I need reading glasses to even see the “decline” on the chart.

Housing market ? Please. See you in 3 years

The rise and drop in percentages aren’t linear. A 100% rise in prices only requires a 50% drop to eliminate all gains. A 3.5% drop annualized over a year is a 35% correction reduces a 100% gain to only 30%. This can add up quickly.

Many homeowners are locked in 3% mortgages and can’t sell.

Who will sell at lower prices?

Builders

Retirees without mortgages

Boomers passing

Investors

Foreclosures

Job hoppers and layoff casualties

AirBNB owners

2nd home owners

Hopefully there will be a story about AirBnB sales, if it ever happens. AirBnB rental profit is so obscene, they may hold the properties for a few years until the economy comes back after collapse. I’ve got to think any AirBnBers that intended to sell have already done so, or have their homes on the market now. These are people who REALLY like money, so I wouldn’t expect they could be caught on the back foot.

Powell said home prices have to come down. Plus a recession is coming. That cannot be good for AirBnB properties. I wouldn’t second guess obvious conclusions.

The problem is that once the job market starts taking a hit, the AirBnB market will soften and profits will start to dry up as the economy heads south. IF a chunk of those AirBnB homes start being sold because the carrying costs begin to make them less profitable -and- the owner sees the asset price drop, maintnenance costs start to rise…..this could add another weight to the housing market…

Makes sense.

Now that house prices have stalled and started trending downward, it’s time to take profits in all those vacant second homes and investment properties since gains no longer cover carrying costs. So these properties will be added to for sale or rental inventory. That’s how Fed will gets its housing correction and lower shelter inflation.

Estimates I’ve read in the past year on how many housing units sold in the past 5 or 10 years went to investors varies between 1.3% to 25%. I’m thinking close to 20% if anyone could ever find accurate data on that. Including empty second and tenth “second homes” owned by foreign investors and their US citizen or student children, cousins and nephews. Add in house hoarder gamblers. Add naive techies who bought without stepping foot in a house that needed foundation and structural work.

If rates keep going up and leverage is shortened I think a lot of these ghost houses will be on the market sooner or later. Probably sooner.

In my area, I am seeing a house for rent. It sold in May for $875,000, and was listed for rent for $9,000/month in July. It was then lowered to $8,500, then $8,000, now $7,000.

I hope “investors” like these lose their shirts.

at $7k/month, that’s over 12 years to recoup your investment. before maintenance, servicing the mortgage, bad tenants over the course of those 12 years, and most importantly insurance, property tax, &c.

assuming nothing goes wrong… and a can opener, sign me up !

Exactly…!!!

San Diegan here. We’re making our California exit next year, but for funsies—last week I looked on Redfin for our neighborhood that we currently rent in. Other than a few new listings, all have been sitting on the market for 30-100 days (and all are still asking for at least a million, some of which are hideous and in need of major repairs such as ceiling leaks). In February I brought my son to a birthday party in a house that had a brand new kitchen but the mother said they are beginning to gut it because of their re-fi. Get ready my priced out compatriots who just want a nice home for their family.

That’s exclusively a female thing, to rip out a perfectly good, new kitchen and replace it just because the existing one is not EXACTLY what she wanted.

A smart man will run from that, married or not.

Right…?!?

The husband was on board too! He told me the neighbors just trimmed their trees and it was a “really big deal” for them as their view was a little less obstructed. The least interesting conversationalists are people who just want to talk about their damn over-priced house and wealth.

“The least interesting conversationalists are people who just want to talk about their damn over-priced house and wealth.”

Lol!! So true. I had a co-worker who used always talk about how much money he had in stocks and how much his house was increasing in value. In 2020 he moved to Boise and has been working remotely. I’m kind of interested to see what he talks about the next time he is in the office.

Irony.

NAH LD, but only to the ”least interesting conversationalists” part; in general, that would be folks claiming to be ”vegan” etc.

Though your point is very well taken, far damn shore re: wealth idiots of the ”new money” kind !!!

> The least interesting conversationalists

I love it when such folks, prattling on about what they paid for their new barbecue setup or whatever, take it in the dookie on the downside. It makes all my abstinence worthwhile.

You waited too long and are going to be “stuck” trying to sell when everyone does. Good luck.

Living in Carlsbad renting for a year then we are also out. When I look on Redfin and Zillow the prices are still outrageous. Seems its going to take a few more months for these folks to realize they missed their opportunity. I think its a mental thing at the moment, but when jobs start being short the real drops will happen. I think it could drop more than 30-40% by the summer of 2023.

I performed a Google search for metro Atlanta where I live; technically Atlanta-Roswell-Sandy Springs which isn’t all of the metro.

It shows the index at 219 in March and 232 in June. It doesn’t seem right but if it is, no relief here.

Atlanta ticked up 0.6% in July (Case Shiller), slowest increase since mid-2020, after month-to-month increases of 3%+ earlier this year. So it’s in the “deceleration” phase. It doesn’t qualify for inclusion here, but it had a massive price spike over the past two years.

I wonder what Raleigh NC stats look like – I’ve just seen a small-ish (by recent local standards) house in one of the towns 20 min from Raleigh hitting the market with almost 400k asking price. It was purchased in 2018 for 185k based on public records.

I still beat myself up for not committing to move to NC right away after my divorce in 2019 – I would’ve saved a lot of money and beat the giant crowd of folks who decided to move here all at once in 2020-2021.

I live about an hour away. Seems like a bubble.

My rural area just got multi billion dollar EV plant, a mult billion dollar Toyota battery plant and a multi billion dollar chip plant all located here with state and Federal funds.

Housing developments started everywhere. Seems like a top. When housing is the most unaffordable ever, how is general population going to afford $50-$80 EV?

Just curious, are you talking about Apex, NC?

Sanford NC. The new billion dollar plants are in rural areas of Chatham and Randolph counties.

@Harvey Mushman, I meant Fuquay. The amount of new construction here is absolutely unbelievable – I like the area in general, but I already start getting worried about local infrastructure failing quickly if something is not done. Local middle school already has a 50 minute wait for a school bus after dismissal for many kids because they simply can’t hire enough drivers for exploding number of kids, so most drivers do at least 2 routes from the same school, one after another.

And so far I don’t see much of “real” drops in prices here. Yes, techically a house initially listed for $700k now went pending after a recent price cut to $650k, so one may say it was a huge drop, like 7% instantly, but this house previously got sold for $350k or less and it doesn’t look like any renovations were done. It’s still in a crazy price territory by local standards.

Good news and not bad news, real estate prices are dropping!

Zillow says my house decreased by 2% in the last 30 days. Ventura County, Southern California.

It must be compared to interest rate, and unknown future inflation, as well.

With the average 30 year fixed mortgage rate exceeding 7% on MND today, it appears the trend of dropping prices will continue. At least if the home isn’t in a special place immune to dropping prices.

Yes indeed – that seemed to happen awfully fast.

8% by Xmas?

Good read.

The US average house-price-to-income ratio currently sits around 5-6 in 2022. This is still quite a way below a number of other major countries across the world. For example, the UK is about 7-8, while Australia sits around 7-9. Suspect the US housing market won’t fall too far in this downcycle. And, if it does, it will boomerang back in a year or two.

You cannot use national house price average and national income average because there’s no national housing market. You have to use local income to local house prices.

Last week’s drama around UK’s fiscal and monetary policy, the pound’s collapse and gilt selloff seems to be causing severe dislocations in the UK mortgage market – variable and short-term fixed rates seem likely to reset much higher in the next few months which along with the COL crisis will likely lead to a severe crash in the UK housing market as many homeowners find it impossible to pay their mortgages and utility bills and are forced to sell.

I thought house prices are already falling sharply in NZ, Canada and Australia. Big banks in Australia are predicting 20-25% price declines.

Given the size of Australia’s housing bubble, 25% isn’t much. That’s the banks hope.

This reminds me of when I was on my HOA board. We had monthly dues down to $285/month in a community that was winning awards for landscaping and architecture. A new guy was elected to the board and said, “the housing development across the street is paying $625 a month. Why aren’t we spending more?” And he was dead serious. True story. That place across the street wasn’t winning awards for *anything*, BTW.

EXACTLY the problem with ANY HOA IMHO JD:

Signing up to give someone else absolute control of your monthly housing expenses is just crazy and sloppy thinking IMHO.

Why SO many do that continues to be a major mystery to me???

Thanks for this report. While ”anecdotal” far shore,,, anyone who knows how statistics actually provide ”cover” for these kinds of things will realize the dangers involved and avoid those dangers, maybe,,,

Suppose it depends on how attractive and persuasive the selling agent, eh?

That’s where I would say “If you want to donate and pay more, go right ahead.”

The key is to keep people like that off the board, or at least deny them a majority. In my experience though, most people don’t get involved in the HOAs until the boards do something they don’t like.

Reminds me of a friend’s HOA, they were thinking to pay a consultant $5k to tell them what their reserve should be. 4 condo HOA. She asked me what I thought I said put the $5k in the reserve.

Right…?!?

The ratios you cited equally applied in 2006.

How did that work out?

I am No Expert However it seems that the ” Continued Inflation ” is Driving Gold Lower rather then Higher very unusual creating an interesting situation.Until prices drop overall this looks to be continuing.

On Top of that we have the strong Dollar very Strong

With all the Cash around price drops don’t seem to have a agenda of speed attached yet but this now starting Home Price drop should prove to be the exception in spite of the vastly over priced market .

Sellers hate losses in general so it shall be the driven Sellers cracking

first those who must sell and then their is the Seller who wants to preserve what left of the Home Value before loosing to much saving whats left > So in fact are several Groups now aren’t their I am thinking

slow and need to wake up here lol hummm

I am thinking once the sellers Bus becomes full the Home market may be hit hard .

What concerns I have is that the way the Fed was left free driving the market up up and away making personal investments with huge gains

and on top of that President Biden has reappointed Jerome Powell in spite of what Happened ??? overall to the US economy affecting markets world wide is simply whats to stop them from doing the “same thing all over again ” and again and again ?

are we to short Gold Now ? awaiting a slowing of Inflation ?

How exactly do you find a good end to all this ?

Demand is down ,and we’re in a deflating environment. GOLD

Gold is for handling tail risk of loss of faith in monetary system, like insurance. Last I looked it was up ltm against pound, Euro and yen.

Thank you Wolf for the excellent graphs!

In almost every chart, the insane appreciation bubble had the steepest rise during the pandemic. (Mid 2020-Mid 2022). In SF, the rise was 40+%. The current 3.5% drop is likely just a start.

If rates stay high or go higher, I predict prices will fall to mid-2020 levels by late 2023 or early 2024.

The stock market has already started re-tracing back to this time. House prices move slower.

I also predict by Jan 2023, house price will be back to Jan 2022 levels and house prices will be flat for the year.

The good news is that this only happened over 2 years with lower than normal inventory being sold. Less people will walk away since they didn’t have the opportunity to overpay by 40% during these 2 years.

It will be referred to as “The lost 2 years” or “The miracle soft-landing”

I may be an optimist on the lower bound since during the GFC, houses in 2012 bottomed at 2001 prices and that was considered “The lost decade” It could happen again with a job-loss recession. In that case, houses will drop back to 2012/2001 levels and it will be called “The lost decades”

There will be no “soft landing” for either the economy or the housing market. This is a belief in magical thinking.

As for the housing market, by logic and common sense, the decline should be worse this time than the GFC. However, anticipating the obvious government response of foreclosure moratoriums and mortgage forbearance (again), I equally anticipate it won’t be as fast or as deep, for now.

Ultimately though, since the overvaluation is a lot worse and the fundamentals are worse too, the housing bust should still be bigger, unless the government decides to trash the currency a lot more than has already happened. With the current lack of affordability, steeply rising rates, and a much weaker economy still to come, the recent inflation isn’t enough to support housing prices in many markets anywhere near current levels.

Correct. Our business is tied to residential construction.

This report is old news as Wolf stated.

Like 08-11, the youngsters will go out & chase construction in

the oil/gas patch. With LNG going global, and the war on carbon, prices will stay profitable.

No chasing here. No debt personal or business. Will hold or up our rates, and work “normal” hours for a change.

Augustus,

Yes, houses have inflated more rapidly and higher than in 2008. I think this was driven by insane stock market and crypto gains. People were cashing in their 6000% BTC gains and overpaying for houses. This didn’t seem to be a problem for the Fed at the time.

Now wage inflation is growing. If more people see 10-20% increase in wages, the housing price floor will also rise. ie instead of house prices falling 30-40%, higher inflated wages will possibly raise the floor to only a 20% decrease in house prices.

Somehow, wage inflation is a much bigger problem for the Fed and they are trying to stomp it out.

We did not have massive wage inflation in 2008.

This time it is different. :-)

“This time it is different. :-)”

It’s evident that you are writing your posts primarily if not entirely from your personal preference. I see that all that time, both here and elsewhere.

I’ll repeat what I said before. If the 39 YR bond bull market ended in 2020, rates are later destined to “blow out” and it doesn’t matter what any government or central bank does or doesn’t do.

As for employment and wages, no different than any other prior economic contraction, except that this time unemployment will increase a lot more from a lower base.

There will be no full employment recession. Whichever door you want to choose, the majority of Americans are destined to become poorer or a lot poorer.

Augustus,

I deal with reality every day. I am an engineer. I deal with facts and not ZH negative speculation.

I don’t deal with theoretically possible 39 year bond pulls.

I am not ZH. These possibilities are not even likely.

You seem to forget that we live in a Centrally planned economy. Fascism, if you must call it something. The Fed can wave its hand and lower interest rates to save us all from certain doom (ie the Fed will wave its hands and the riots in the streets won’t even start).

Unfortunately, IMHO, the Fed has been waving its hands way too much the last 3 years which got us into this mess.

Before the HPIs – Case-Shiller and FHFA – came out today, there was some press coverage of a report from some Fed researchers claiming that 50%+ of the pandemic era increases in house and rent prices was due to WFH not a speculative bubble.

I read the research paper as well as the media article – was wondering if anyone else had done so too and if so what y’all thought of it?

It’s the first attempt I’ve seen to rigorously quantify the impact of WFH.

Since it came from the Fed I was wondering if I might factor into their calculations for their desired “Housing correction” – they might want to eliminate the speculative froth but not the change in fundamental valuation due to WFH.

That’s a great point! I work with several families who purchased and moved to a larger home during the pandemic to work remotely.

It was too difficult to work from home in a 2 bedroom condo with 2-3 kids also at home.

They kept the condos and rented them. One family is moving back to be back in the office.

The question is: Which one if any will eventually be sold?

It’s amazing to me that so many people acted so impulsively with such a large purchase. It’s one thing to buy a $2,000 Peloton on a whim because you’re working and exercising from home. It’s another thing to buy a house in a rural area you aren’t into (if you’re a city person) and then being surprised you don’t like it.

Einhal,

It is difficult in normal circumstances to live with a family of 4 in a 2 bedroom condo. They had long term plans to purchase a bigger home in suburbia.

They just accelerated the plans when 4 people were trying to work, homeschool, and live in a 2 bedroom condo.

Bob, I’m not referring to those people. I’m referring to the city slickers who moved to exurbs, and then were shocked, SHOCKED, that there aren’t 24 hour delis or coffee shops at every corner. I’ve read many articles in newspapers about people like that who are selling their suburban/exurban/rural home and moving back to the city.

City 2 bedroom condos seem to be for the DINKs (Dual Income, No Kids). This is an old cliche. Sorry.

People who had been hanging on to their city lifestyle with kids were high motivated to move when the pandemic hit.

When I had kids, I had no time for the nightlife. Though 24 hour delis and coffee shops would have kept me going for those 3 AM baby wake-up calls. I realized eventually that I had to sleep sometime without caffeine and popping leftover pizza in the toaster oven was quicker than a trip to the deli. Circumstances changed and life changed.

The transition to suburbia was easy with kids. It did help that I had a job in suburbia at that time. BC (Before Children), it was easier to crash on the cot supplied by the company in my cube in order to finish my projects. That was an effective form of birth control since my wife couldn’t enter the building without a badge.

What is WFH?

WFH = Work from Home

Thank you Wolf. That’s what I thought, I just wanted to clarify.

WFH = Work from home

Can also stand for this stupid housing bubble..WFH = What F$$$ing Horsesxxt

Phoenix,

I remember you were utterly pessimistic it would never end and I was telling to wait until CS tops.

Now when we are there – what are your thoughts?

Still pessimistic as ever and it’s nice from my POV to see price is trending the other way now finally. Although still being cautious to not put the cart before the horse and claim victory on the burst just yet since most price decrease is still pathetic. If it can continue with 2-3+% drop every month in SoCal, then 5-6 months from now I would have much more confidence in the strength of the burst.

The market IMHO has been nuts since the bottom around 2011-2012 but really went insane last 2 years, both the velocity and breadth of the increase, what we need now is a reverse if not just as fast and perhaps twice as fast, that would be my wish but reality might be different and can play out much slower. Looking at those graphs from Wolf, I am still trying to wrap my head on how we can ever go back down to sane level? Case in point for San Diego, even if Case Shiller goes back down to 240 from where we are at now, it’s still bubble 1 level. I just have a hard time seeing 420 goes back to 160ish level. Don’t get me wrong, would love to see it but feels like unicorn fantasy.

Just really sick of seeing listings pretty much popping up daily now on Redfin, sellers still asking for dumps in Placentia, Chino Hills..etc for $1.1M to $1.5M, crash 40% and we might be at fair market value. One encouraging sign though, see way more back on market in those emails, thing RE agents are playing games out there to try to spark some last min FOMO.

Yeah all the markets need to retrace to at least 2012, before QE2. The wheels were coming off even back then.

Utter nonsense, like most Fed research.

This potentially makes sense for local markets. Nationally, it’s a rationalization.

WFH is one factor, but it doesn’t change the lack of affordability to the locals in those markets already living there. It also ignores the reduced demand when those WFH vacate their prior market. The only way this works is if those moving don’t sell their existing home, something included in numerous articles on this site as a source of the housing bubble.

So basically, whatever is added to the receiving market is subtracted from the one being left.

When the economy starts to tank, I can promise you that there will be a surge in squatters breaking into empty homes, if only to have somewhere to sleep and not to steal anything. I say this, because unlike during the GFC, I am noticing many more single family homes with two or three families living in them. If/when “squatter events” become more frequent, sales should increase.

JeffD,

I am already seeing more people living out of their cars than I did in 2009. That’s without a large number of layoffs.

Just received new lease terms, only 11% increase after a 9% increase last year. Promptly filed notice to vacate. There are more affordable options. Perhaps not as pleasant, but amenities are useless when you are hungry.

I received a long explanation about how they set rates. My response: Let’s see how much the current owner paid for this set of buildings when the evictions start rolling. No tears shall be shed.

That which went up vertically appears to be coming down vertically!

This a difference from last time. Rate of increase and decrease, based on this limited data.

Driven by obscenely low interest rates changing to relatively high interest rates in a short period of time.

Alright alright already, you’ve convinced me that San Diego has definitely arrived to the housing crash party, there’s no doubting that. But, the women at this party are still hotter than any party in those other cities. This ought to cause a kerfuffle.

Yeah, but it’s the high maintenance on those women that will get ya!

I wonder if the increases in those maintenance costs are reflected in the cpi?

My latest Corporate HR training prevents me from commenting on this thread.

Yeah. just remember that *Marriage* is a patriarchal thing, so it is so misogynist … don’t ever get married. just live together and apply the apple plan… (upgrade every 2 years). No need for contracts now, it’s all about the month-to-month services now a days…

Major metros are the worst places to live, especially in California. Taxation, cost of services and cost of goods is ridiculous.

The best thing is move and WFH… for those that can. Even better leave the USA for cheaper lands while working remotely.

Wolf,

Can you humor me for a second? I believe we are sitting on a ‘cash out refinance bubble’. If house values drop to a point that these owners have two choices – lose all gains or keep the cash and walk out of the house – could that trigger a mass foreclosure? These are people who perfectly afford the house they are in – but have large Chunk of cash from the refi and don’t want to lose it. Could walking out of house provide double gains – they keep the cash and avoid paying taxes and interest?

There is obviously a 7 year credit hit. But for high value homes like seattle, itmay be worth taking for large chunk of $$.

Am I thinking right? Or missing something obvious?

While witing for Wolf, I believe the standard loan to value for refis is usually 80%. If I remember correctly, during the 2006 crisis, some people were getting loans for over home value, and a lot of people were buying homes with 3% down (or less?)

I know at least one bank, key bank, that would 10% down with no PMI. Meaning loan tovalue ratio of 90%.

Yep. I saw many cases that a 2nd mortgage lenders had no problem going to 110% of the home value.

I remember getting a 125% loan around 1998 from GMAC, the long since defunct Mortgage division of General Motors. I can still see that Fedex envelope with the $50K check and documents on that June day.

So far, so good. People still have lots of equity in their homes. Maybe that’ll be an issue a year or two from now. But then we would still needed an employment crisis. So who knows. But not yet.

I think the total is over 26 trillion. It was $11 trillion peak in HB1.

I just have to say wow. That is a lot housing wealth.

Take the money and run!!

Not ethical – perhaps even criminal – but our rulers have taught us well.

On most if not all refi’s, the loans are full recourse. New purchase money in many states is not. If they have money to run with, the bank can come after them and prevail.

In the last bust, people would refi the existing house they couldn’t sell, buy a replacement on the cheap, and send jingle mail for the first house. That was a *thing* in CA.

Even if USA tries very hard, US law is not the law elsewhere. To curb money fleeing they may inadvently shut some tax loopholes for the affluent. A well planned run with the money may work out.😉

Yes, if you run to another country. If you run to the next suburb, maybe not so much.

I’ve heard of the same thing locally, the refi/jingle/launder sequence also works for shrimp boats. And since all the shrimpers are related… must be very profitable business for banks to want to finance boats for this bunch. I’ve great respect for their industriousness and thrift, but I don’t do their work, they’re too tight.

ST, I agree that cash-out refi activity played a big role in all of this. Unfortunately, no, people aren’t generally going to walk away from their houses like they did after the last housing bubble popped. As long as jobs are maintained, people that bought before the pandemic are generally OK with lots of equity and people that bough at a high price but at 3% interest are going to be OK too. Those folks, especially the high-price/low-interest crowd may be stuck in their house for a long time, but if they can keep making the monthly payment, they’ll stay.

Add to that the fact that only handful of states (12 states I think?) are non-recourse for the original mortgage. So in most states. lenders can come after a homeowner’s other resources to cover their losses (including that cash-out refi money). And if I remember this correctly as it’s been described in other Wolfstreet article comments, most refis are recourse loans regardless of the state’s position. Recourse loans are going to get paid unless we see a major change in unemployment that leaves many homeowners with no options other than foreclosure.

Basically the jobs market is key. If it stays even remotely strong, don’t expect a housing collapse. That’s going to require millions of job openings to turn into millions of layoffs.

@ SeattleTechie – well is fun to dream… but some one correct me if i am wrong. The Original loan is non-Recourse. BUT if you refinance – cash-out or Not, or take a HELOC, these loans become full recourse. The devil is in the details.

So, no you can’t cash out and let it foreclosure, they will come back to get the money from you if you cash out refinance.

I think we may be starting to grow a HELOC bubble. ALL of my latest SPAM calls that I am receiving are for HELOCs. ie I don’t have to give up my 3.0% loan but can draw out more cash for home improvements. Wow! That means I can use my extra personal cash for a new boat or private jet!!!!

The Refi people calls have thankfully given up and hopefully found a new job in this low unemployment environment.

Personally, I will stick with my 3.0% mortgage to the bitter end. I actually mean an extremely happy end.

Well, unless the Fed pivots during a major recession and I can get a 2% loan.

Where are those sub-prime mortgages when you need them? /s

How far behind can the stock market be?

The stock market and housing market are completely different. Financial markets don’t work like a standard seller/buyer transactional market. Plus stock markets can move much more quickly than housing.

There is likely a bug bounce in the stock market nearing soon, possibly taking us to new all time highs. The housing market on the other hand has most likely topped and may get a lot worse before any bounces appear due to the sensitivity of buyers to interest rates.

There is no way the stock market goes to new highs anytime soon (SPY4800). With interest rates up and the economy down and dollar high – corporate profits will come down and interest rates reprice future income streams.

Now – if the FED pivots because all of a sudden inflation craters AND employment cools – then stock market will stableize and head north – but – housing and food are a huge part of core inflation – so we have a classic tug of war here….

My guess is we are in a choppy, volitile market that bottoms out at 3100-3200 but never gets off to the races for quite some time. Once the market takes one last fall – get into a covered call strategy and actually buy LONG dated bonds. That will outperfrom the market….

It can happen. It only takes changing sentiment, not any “fundamental”.

However, there is no need for it to happen.

The stock market already hit a temporary low in June which was just breached on the Dow and S&P, only three months ago. There is nothing even close to panic selling now. The decline since January has been very “orderly”.

Which lenders are like country wide this time? Somebody must be sitting on billions of leveraged low FICO score loans. Which bank tips over the financial system without a huge bailout???

I’ve heard on several financial sites and podcasts that Deutsche bank is in serious trouble. Maybe not necessarily low fico loans, but all sorts of other troubles.

I’ve heard on several financial sites and podcasts that Deutschland is in serious trouble. Maybe not necessarily high gas prices, but all sorts of other troubles.

Douchebags are being repriced even as we speak. Possibly to the point of liquidation.

National mortgage rates just went over 7%. In one month they jumped from 6% to over 7.

First time since 2000 mortgage rates carried a 7-handle. Let’s see what happens when Powell’s harpoons are puncturing the bubble from all directions.

Dearest Wolf, the recession of 2007 was not the “Housing Bust #1”. It was just another in a long line of housing bubble bursting since probably the beginning of time.

I started counting at Y2K, not Adam and Eve. I started the series in 2017. Ancient history is not topic of this site.

1) C/S SF peak might be tested or breached. Suppose few wealthy investor, very few, who accumulated rental properties since the 70’s decide to sell few pcs, by supporting buyers, because it’s time to cash in.

2) Few pairs, houses bought 20Y-50Y ago, sold in Aug, when mortgage rates were under 5.5% and ==> C/S will rock.

3) LA is down, but the flyover Davis is up.

4) Tampa under the hurricane.

1. Rent bubble is even more splendid. This will break the back of the serfs. They are barely hanging in there.

2. Renters are too poor to afford a house but the rental payments are way higher than monthly house payments.

3. Rent is a viscous cycle that prevents saving, investing and even spending on other comfort items.

4. Dear Lord Rent is too high…

Everyone needs a place to sleep, but wages have not kept pace with inflation or (especially in California!) rent. Just how much can rent increase? I mean there are already over a hundred thousand homeless Californians. And this has been a problem for over forty years.

People are always either making excuses or saying that they Are Going To Do Something! But it only gets worse. I swear it feels like I have been on a financial rent rack for decades with most years Torquemada is yelling at the wheel man to pull it another notch.

Maybe the landlords will get into the organ trade. Can’t make the rent, but have a kidney, a bit of liver, or maybe some marrow to spare?

So, will the ending of this bubble have any positive effect for renters like me?

Cobalt, you have become Michael Engel. Michael makes me think.

Wages will rise with inflation is the solution. I’m not entirely convinced that the Fed is against this.

Wages rising will prevent:

1) Riots in the street due to starvation and high rents.

2) The housing and stock market from crashing more than 40%. Wage inflation will float the entire boat higher to counteract any drastic crash in housing and equities. This will partially cover rent.

The US government is so fortunate to have rising inflation during this crisis compared to 2008. /sarc Nobody wants to hear their house crashed 50% like last time. With magical 30% wage inflation, their house will only temporarily drop 20%. At least until the next bubble: HB3

Fed policy is going to work primarily through residential real estate new construction. If your job depends on that industry, you are in the bulls eye of Feds somebody has to lose their job policy.

Listened to Lacy Hunt. He says it’s going to take roughly 6 – 9 months for fed to get excess money out of system. Effective money supply has went from 27% growth to a negative number. That has to hurt.

1) This morning the monthly Dow futures have a close < June low.

2) In order to keep the downtrend Sept close must stay below. // Sept might end up with a buying tail above. We don't know what will happen next in the next 3TD until Fri close.

3) RE and the Dow were up since the 70's & the, 80's, but silver, soybeans and sugar… are down. The 50 years commodities bust might be over. It's hard to dislodge inflation. C/S might rise, but not in real terms.

4) C/S should come in tranches.

I wonder how long until we see YOY drops in multiple metros on single family. That’s when things would start getting interesting.

Wolf,

What are your thoughts on the Bank of England “pivoting” and trying to crush the bond vigilantes?

There is real CHAOS going on in the UK bond and currency markets triggered by the stunningly reckless policy announcement of the new government.

The 10-year yield exploded from 1.9% to 4.5% in two months — without even QT. That kind of “tightening” blows up everything. How much “tightening” of this type do you want???

But to what end? Won’t their pivot undo all the tightening progress they made?

Bonds will not clear, except at extremely tight (high) rates. How much self-buying can BoE do? At some point it goes parabolic, then fractal. (Is this sort of a repeat of the 1991 drama? Of Weimar dynamics?) What does that strain do to the financial system? Something breaks, maybe something big. Somebody important abandons ship.

This is what it looks like when a central bank is trapped by high levels of debt.

The first to pivot (I suppose the BoJ was first since they haven’t even started trying to tighten yet) is the Bank of England.

What is any central bank going to do when rates “blow out” anyway?

“Pivoting” is just one form of “can kicking”. It doesn’t resolve anything.

Builders are going to start dropping prices quickly now. Material costs like lumber are back to pre-pandemic levels. As unemployment hits the construction industry, labor costs and profit margins will be falling as well.

Transaction volume has dropped off the charts in September based on the real time data I’m reviewing. Part of that is seasonal, and part is a severe slowdown.

We have this weird disparity in prices coming, I suspect. Labor markets are tight but materials and goods will be falling?

Some construction materials haven’t dropped noticeably:

Southwire 12-2w/g Romex electrical cable, 250′, at Lowe’s, before tax:

Under $70 through 2020

2/12/21 $88.00

3/15/21 $98.00

5/1/21 $127.30

5/7/21 $140.00

6/30/21 $152.00

Today it’s $149.00. now they lock it up somewhere.

For years after Katrina it was $33.00 a roll.

#1 bare bright copper scrap brought 3.84/lb locally last summer, a bit more than the spot copper market price today, but the manufacturers aren’t coming off their money in like measure. The last time this happened people started using aluminum wire and cheap devices for branch circuits and burned houses. Hope that doesn’t happen again.

I haven’t checked 3″ and 4″ PVC pipe and fittings in a couple of months, but it was way up there, and oil is down now, but nobody has threatened Charlotte Pipe with excommunication and banishment to the void like the cowering gas companies, so pipe is going to stay expensive.

Lumber prices have eased. But there’s impending demand in the wake of Ian that will support prices for lumber and roofing materials generally in the Southeast.this may be the low point for the next ten or twelve months.

People are still paying top money to live near SocalJim!!!

I am blissed out in SoCal, and I often reflect, a bunch of it is the proximity to SocalJim.

2.5% off nosebeed-high prices isn’t much sweat, yet. I’ll take that trade.

But what the world needs now, is regression, and that is spelled r-e-c-e-s-s-i-o-n.

When I was growing up in the early 90s, I had a T shirt with a picture of milk carton depicting Mikhail Gorbachev as a missing person.

I think we can do the same for SoCalJim, haven’t seen him post recently or at least from my observation.

they parted ways with Wolf :)

I am missing his insights as well.

P.S. thanks for the detailed response above!

Np, as for SoCaljim, don’t miss him too much…we can always count on Kunal to fill those empty shoes..

I am looking forward to an article from you on the Bank of England reversing course and buying bonds to prop up the market.

I wish we could just STOP these central banks from intervention. There is a good reason the interest rates were rising, it was a reaction to government policies that are out of whack. These central banks are repressing the market signals that would force politicians to knock off the crazy deficit spending.

UK Chaos Economics: Fretting over “Financial Stability” & “Contagion” after Gilts Plunged, Bank of England Buys Bonds

It wasn’t big hedge funds that blew up, but £1.5 trillion in leveraged pension funds. BoE stepped in to bail them out as bond chaos blew up their strategy.

https://wolfstreet.com/2022/09/28/uk-chaos-economics-fretting-over-financial-stability-contagion-after-gilt-plunge-bank-of-england-buys-long-dated-bonds/

Looks like the real estate party is over for this cycle. It’s been a great run. Buyers will eventually get accustomed to 7%+ mortgage rates. By then prices will have to drop further to compensate.

To all the potential sellers out there, there’s still time to sell and lock in profits. The residential real estate market reacts very slowly. In 2008 I sold properties for close to pre-crash prices up to a year after the initial drop.

The runway might not be as long this time and the clock started ticking this spring.

Hello CCCB,

I helped someone refinance their property into a 30 year fixed mortgage approximately a year ago at a 2.5% interest rate! With the same excellent credit and same low-cost bank, this person would get a 6.25% 30 year fixed mortgage today. That is 2.5x higher interest than just 1 year ago, which I estimate would have raised their payments by $1200/month in interest costs. This is the main reason housing is dropping and will continue to drop until interest rates stabilize when the FED gets inflation under control.

In the 2008 crisis you had the perfect storm; a dramatic increase in housing supply along with decreased housing demand. Housing supply increased due to negative amortization mortgage resets that significantly increased mortgage payments and pressured owners to sell, short sell, or go into foreclosure. Housing demand decreased because the only way the masses could afford houses at that time was through negative amortization loans and those ceased to exist, standard 30 year mortgage lending got stringent, and the few buyers that could afford a home were spooked and decided to look for signs of a bottom to the crisis before jumping into buying a home.

I would say today’s crisis will be less severe because it is a story of decreasing housing demand due to a significant decrease in affordability caused by a dramatic rise in mortgage rates. Unlike 2008, I do not see housing supply increasing dramatically due to forced selling, short selling, or foreclosures because homeowners are not seeing their affordability decrease significantly as they did when their mortgages reset in 2008. If anything, this drop in housing demand may push housing supply down once builders react and slow down construction and homeowners only sell in emergency situations at lower prices.

Since this is mostly a story of decreased demand due to a lack of affordability, along with keeping an eye on mortgage rates, I believe rent increases due to inflation will be important to watch. This will help put a floor on housing demand since it will keep pressure on potential buyers to get out of renting and into buying. That is why I believe that if the FED can get inflation under control and mortgage rates to stabilize, buyers will be ready to jump back into buying homes again, especially if their rents continue to go up and pressure them to take a second look into buying a home. Now that millennials are older and starting families, it is a lot harder for them to move back to mom and dad’s basement to ride out the storm.

Am starting to see reports that rent prices have peaked and started falling in many cities.

This is quite surprising.

Apparently new supply is coming online (e.g. new apartment buildings completed or renovated) and demand has dropped.

I am following SFHs for rent where I live. What I am observing during last several month:

1) supply has definitely increased.

2) homes stay much longer on the market, with price reductions common

3) there come offers like 10% below market, usually posted by a mgmt company. These still generate 10s of application on the day 1, but even in the mid summer such offers were unheard of

And as discussed in comments above (you should read those), many houses have been bought by investors and there are lots of second/third homes sitting vacant for which the last couple of years of spectacular gains were covering carrying costs while the Fed’s massive QE and inflation had made other investments unattractive.

Now that the housing market has peaked, prices are falling and the Fed has started tightening, holding those vacant properties doesn’t look so good – carrying costs plus losses plus alternatives like TIPs and CDs giving positive yields.

So selling by investors and other owners of multiple vacant homes to cash out on pandemic boom profits could lead to a big surge in supply in short order.

Hello Dazed and Confused,

The big question is are they forced to sell like homeowners in 2008, or is it a choice to sell due to the opportunity costs of holding these properties? My take is that it will be a choice, and that will not be enough to mimic the housing supply increase that occurred in 2008.

Something else to consider is that in 2008-2012, the Feds (government and CB) was desperately trying to prop up the crashing housing market by buying up MBS, bailouts, moratoriums etc. Housing bears were fighting the Fed.

Now it’s the opposite. The Fed has made it very clear that they want a housing crash (their euphemisms are becoming less euphemistic at each meeting – first “reset”, now “correction”). So housing investors are now fighting the Fed. Investors know not to fight the Fed so they will be dumping houses onto the market en masse in short order.

Building some of the most expensive rral estate in the world in the path of a CAT5 hurricane might not have been such a brilliant idea after all.

But Nobody coild have seen that one coming.

Just kiddin’.

That’s life in America. Nature is not forgiving here. In addition to hurricanes, there are earthquakes, tornadoes, firestorms, long droughts, water shortages, massive floods, blizzards, hard cold snaps, deadly heatwaves, etc. that occur routinely. That’s life in America. Americans have to live somewhere, and they deal with whatever they get. That’s how life here is. You’re in central Europe where you don’t have many of those events, so you might not fully understand.

I think there might be other reasons of a non-natural kimd why a lot of people moved to florida lately.

But ket’s not get into politics here.

People have moved to Florida in large numbers ever since the commercialization of air conditioning. Look at a population chart of Florida. The state is very appealing for lots of reasons, including ironically the weather because it doesn’t get cold in the winder, and the beauty of the huge long coast line. The coast-facing portions of the cities are gorgeous.

I’ve been to Germany and can attest the houses there look to me much more capable of surviving annual Florida’s natural disasters than the houses in Florida itself :)

Probably not. German houses are often made out of brick, which is one of the worst construction materials in terms of strength. Wood and steel are the two strongest construction materials in terms of strength. The good thing is that there are no hurricanes and big earthquakes in Germany.

Houses built to modern building codes in Florida are holding up pretty well. But with hurricanes, the biggest issue isn’t the wind but flooding. Nothing protects your house from a 10-foot storm surge. It’s going to get flooded.

By the way: there’s a new three-letter hellhole just entering the stage now.

It’s not an MBS.

It’s not s CDO.

It’s not an ABS.

It’s not a BTO (“Bespoke Tranche Opportunity”).

It’s an (drum roll)

ILS !

Which stands for: “insurance linked security”

Gonna be the star of the show real soon. The closing act, if you will.

Jay is already on the Phone. Maybe they can detonate a neutron bomb to stop the hurricane or something.

“Securitize this !”

Seriouslyy you guys had it coming to you.

Wolf, do you think Los Angeles will go back to 2020 prices? There’s so much competition and limited housing here. It’s such a weird overpriced market

Any love for Atlanta? I thought your article was really interesting and well founded but, as is often the case for housing articles, there’s no local coverage for the biggest city in the South (Miami isn’t part of the South, imo).

Real estate is local, right?Are you open to running a similar analysis on a new, but less nationally prominent city?

Atlanta’s housing market, though it shot up over the past two years, doesn’t qualify for this list of the “most splendid housing bubbles in America.” The definition to qualify is that the Case-Shiller index must be up at least 175% since Jan. 2000. Atlanta is up only 101%, far below the qualifications:

What is this about prices dropping like a lead brick in the future? I would say an actual 8% drop NOW qualifies:

From SLC Fox news 13 (Sept. 22)

“Bidding wars are over; Utah home sales plummet as rates rise”

“…numbers are falling as the price of single-family homes in Salt Lake County are down 8 percent from their peak of $650,000 in May to $601,000 in August.”

8% in 3 months is what, 35% annualized? CRASH!!!@%#!