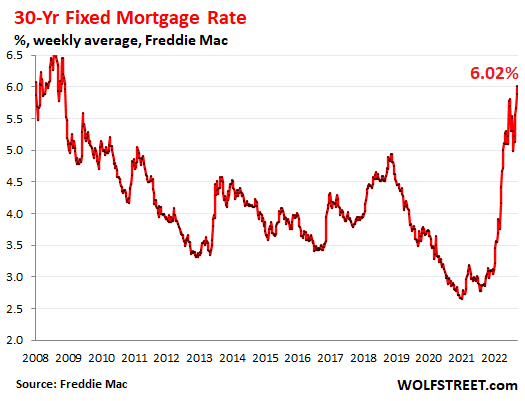

But these sales happened during the “Fed pivot” fantasy that pushed mortgage rates down to 5%. Now mortgage rates are near 6.5%.

By Wolf Richter for WOLF STREET.

In July and through mid-August, mortgage rates fell sharply from the 6%-range in mid-June, on the widely propagated fantasy of a Fed “pivot” on rate hikes. By mid-August, the average 30-year fixed mortgage rate was down to 5%. Yesterday, they were at 6.47%. But the brief interlude of dropping mortgage rates slowed down the decline in home sales – sales declined again in August from July but at a slower rate – with Realtors in mid-August talking about the market waking back up.

But prices backed off for the second month in a row, and in a big way, amid widespread price reductions, and that also helped getting some deals done.

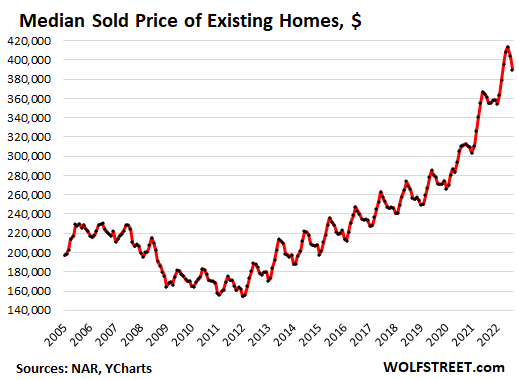

The median price of existing single-family houses, condos, and co-ops whose sales closed in August dropped a hefty 3.5% in August from July, the largest month-to-month percentage drop since January 2016, after the 2.4% drop in the prior month, to $389,500, according to the National Association of Realtors. While there is some seasonality involved, the percentage drop was much bigger than normal in August, whittling down the year-over-year price increase to 7.7%, down from the 25% year-over-year increases last summer (data via YCharts):

In the West, price drops are further advanced, amid dismal sales. For example, in San Francisco and in Silicon Valley, median prices have plunged in recent months – now down on a year-over-year basis in San Francisco and Santa Clara County (San Jose) and up just a hair in San Mateo County, according to data from the California Association of Realtors.

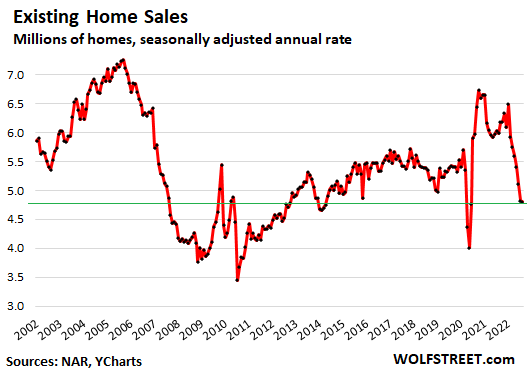

Sales of existing houses, condos, and co-ops across the US dipped a smidgen from July, after the 5.9% plunge in the prior month, to a seasonally adjusted annual rate of sales of 4.80 million homes, roughly level with lockdown-June 2020, according to the National Association of Realtors. This was the seventh month in a row of month-to-month declines.

Beyond the lockdown months, it was the lowest sales rate since 2014, and down by 29% from October 2020 (historic data via YCharts):

Sales of single-family houses dropped by 0.9% in August from July, and by 19% year-over-year, to a seasonally adjusted annual rate of 4.28 million houses.

Sales of condos and co-ops rose 4% from July, to 520,000 seasonally adjusted annual rate, down 25% year-over-year.

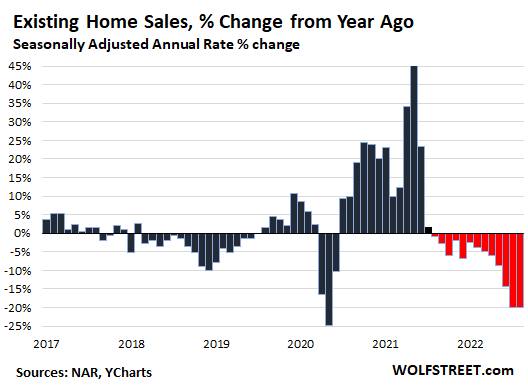

Compared to August last year, sales fell by 20%, the 13th month in a row of year-over-year declines, based on the seasonally adjusted annual rate of sales (historic data via YCharts):

Sales by region: On a year-over-year basis, sales dropped sharply in all regions. On a month-over-month (mom) basis, you can see a little uptick in two of the four regions:

- Northeast: +1.6% mom; -13.7% yoy.

- Midwest: -3.3% mom; -15.9% yoy.

- South: 0% mom; -19.3% yoy.

- West: +1.1% mom; -29.0% yoy.

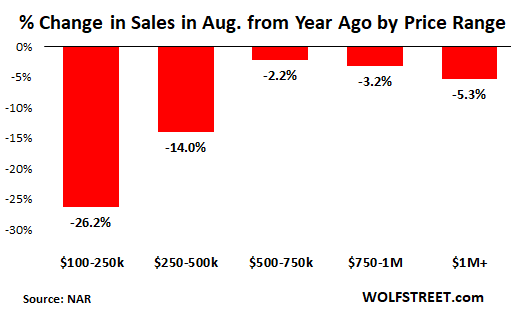

Sales dropped in all price ranges but dropped the most at the low end.

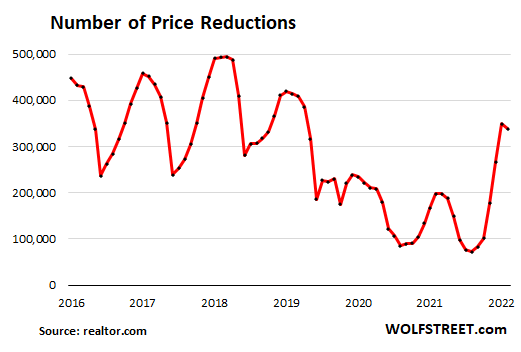

Sales volume has been low because potential sellers are clinging to their aspirational prices of yesteryear, when mortgage rates were 3%, and many would rather keep the home off the market or pull it off the market than sell for less, for as long as they can. But price reductions have now taken off by sellers who want to sell.

Price reductions started spiking in May from record low levels last winter and spring as sales stalled, and as mortgage rates surged. In July, they reached the highest level since 2019, according to data from realtor.com. In August, price reductions dipped just a little as sellers might have felt that price reductions were less needed, amid the declining-mortgage-rate-Fed-pivot fantasy in July and August:

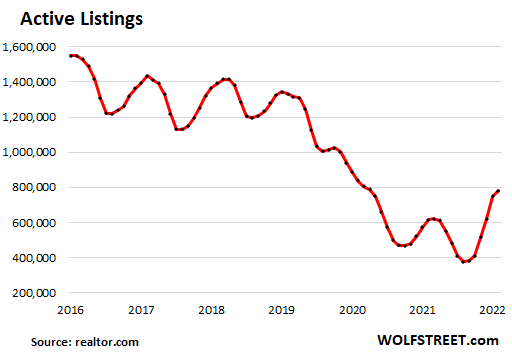

Active listings – total inventory for sale minus the properties with pending sales – rose to 779,400 homes in August, the highest since October 2020, up by 27% from a year ago, according to data from realtor.com:

The National Association of Realtors is clamoring for more single-family houses to be built. But homebuilders, they are having trouble selling the houses that they have already built or are building, sales have plunged, inventories have spiked to the highest since 2008, and homebuilders have started cutting prices, buying down mortgage rates, and piling on other incentives to get their inventory moving.

Investors or second home buyers purchased 16% of the homes in August, up from 14% in July, but down from the 17%-22% range in the spring and winter, according to NAR data.

“All-cash” buyers, which include many investors and second home buyers, remained at 24% of total sales, down from a share of 25% to 26% April through June.

Going forward: holy-moly mortgage rates. After the fantasy-drop from 6% in mid-June to 5% by mid-August, mortgage rates are now solidly over 6%.

The daily measure of the average 30-year-fixed mortgage rate is at 6.47%, according to Mortgage News Daily.

According to Freddie Mac’s weekly measure, released last week, based on mortgage rates early last week, rose to 6.02%, more than double a year ago. These 6%-plus mortgage rates are still very low, considering that CPI inflation is over 8%. But they’re catching up.

And potential sellers that hung on to their homes in July and August because they didn’t want to meet the price where the buyers were – hoping the “pivot” fantasy would push down mortgage rates further – now face the effects of these 6%-plus mortgage rates:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Bracing for Powell’s 5th.

I hope Powell guns it. Low interest rates got us into this mess and they can use high interest rates to get us out.

.75 it was. I’m no expert on these matters (thats why I come for Mr. Richter’s expert knowledge/data/insights). However, I don’t think higher interest rates alone can fix this situation. As with all complex systems, nobody truly knows what’s going on.

It was disappointing to see that Fed again announced a ceiling of 4.6% on Fed rate when it has not even gotten close to controlling inflation.

At -4% real interest rate, inflation is going to run hyper!

“to see that Fed again announced a ceiling of 4.6% on Fed rate”

That’s total BS. READ THIS:

https://wolfstreet.com/2022/09/21/powells-whatever-it-takes-moment-our-policy-will-be-enough-to-restore-price-stability-fed-hikes-by-75-basis-points-in-shocker-sees-4-4-by-end-of-2022/

I’m definitely no expert either. I’m definitely not as astute as many of the commenters on here, but it seems to me raising interest rates are a step in the right direction for taming inflation.

Wolf I was just quoting what’s written here: ..

Your article does provide more clarity.

Thanks for clarifying.

Housing prices are directly related to mortgage rates.

If the rates go up then prices have to go down provided the wages don’t go up.

Inventory needs to move substantially higher for prices to drop a lot more. 3.2 month supply is still only about half of what is considered a balanced market (6 months).

The upcoming interest rate induced recession should change this, though. Yield curve inverting too so it’s coming.

Now a days closing is happened much faster.

So 6 months inventory historically is quite high.

I thing 3 4 month inventory is high enough.

It’s take year or two for things to play out bit we are seeing the trend.

Not just inventory. Jobs have to be lost, and the stock market has to go much lower, whether anyone wants to hear this or not. Many people that are financially secure enough to own second and third homes are not going to feel the pressure to sell until their other assets are chopped down, their job is on the line and their tenants cannot pay their rent (after their jobs are lost and there are no more bailouts). We still need a traditional recession to devalue assets and curb inflation. No soft landing coming.

Interest rates only address demand. But our issue is supply not demand. There’s no guarantee that suppliers wont just cut production when demand falls in order to keep margins high. Then you get into the viscuous cycle.

“But our issue is supply not demand.”

Nope. The problem is the most grotesquely overstimulate economy ever (with pandemic money, monetary and fiscal) that created a historic explosion in demand, which created the spike in prices. You can see this in all my charts over the past two years. That demand has to be brought down.

Prices of services started spiking months ago, and there is no shortage of services:

My advice for the last year:

you can always refinance but you can never renegotiate the sales price of a home…

Good advice and so true. Unfortunately, a builder in Maine where my spouse and I are looking to move sent an email this morning advertising rate locks. I responded that we would rather wait for the prices to come down than lock in an interest rate. If they don’t reduce their prices much in the next year, we plan to buy an existing home.

There are appraisers and realtors that act as intermediaries between buyers and sellers, and those people have the power to push prices down.

Your advice saved our family from making a gigantic mistake. We walked away from the deal with little $ lost. This reminds me of the last bubble. We will wait when prices come back down. Thank you for sharing your wise words!

Disagree. When rates are trending up, you CAN’T always refinance.

The 40-year era of generally falling rates appears to be over. We are now seeing higher-highs on interest rates.

But should your financial fortunes improve through career advancement, an unexpected bonus, etc., it’s easier to pay off $100 at 10% than it is $1,000 at 0%.

We always paid one additional mortgage payment per year that went against the principal. That’s a simple way to amortize a mortgage faster than the 30 years (or 15 or whatever) and pay it off years in advance. Paid off my first house before I was 35.

So, maybe he wouldn’t need to refinance. It’s always what you pay for something, never the payments. Payment buyers are a seller’s wet dream. Leverage is not always your friend.

USA probably just turned into 80s JAPAN ,except we don’t export enough

This. One of the reasons why we are holding out for our first home and just socking away cash. Hard to compete against the institutional buyers erm I meant Blackstone uh I mean ‘cash buyers’

Luckily I own property in a magical neighborhood near the beach where prices never go down. Property is scarce, residents are rich and everyone buys in cash. Wolf’s statistics don’t apply here because we are special.

Riveting comment. The dinner party conversations must be off the freaking chaiiiiiin…

Thanks Tim r, I think my laugh from your comment was heard all the way to that magical neighborhood.

The handle is Seneca’s Cliff. Assume all is irony. Maybe a little copper, some trace elements.

There are a few places that are like this. The key is high demand, low availability. A backlog of buyers who not price sensitive. For wealthy baby boomers hitting retirement, who want that dream beach/mountain property, they can’t wait it out. Time is precious. Location, location, location…

I thought Seneca’s Cliff was being sarcastic, based on what he said in his many prior comments.

+1

And having a good laught. At a well phrased comment.

Your focus on demand reduction is over kill, the better focus is on y-t-y price change. If home prices, mortgage rates and rents flatten at 6% mortgage interest rates (roughly 2.5-3.5 Fed fund rates) +-, then in one year inflation from CPI costs for that category goes close to zero. Why go lower? Why reduce the asset value of the middle class?

Zero inflation is the target for each CPI component. Why add the human cost of reducing asset value. I could add that to the human cost of labor reduction, etc. ITS NOT NECESSARY. Getting y-t-y change down closer to zero should be the goal. I read your comment yesterday, and your focus on demand reduction (yes, old time economic strategy) clearly shows you didnt get the point on shooting for zero PRICE change, not reducing assets or other economic variables such as labor, rents, services, etc. What value is high unemployment, labor price reduction to the Middle class to a healthy economy? It only handicaps future growth. If you want to reduces more esoteric valuations, mandate tax increases with every QE and inflationary fiscal policy. Focus on the asset classes. While this sounds either impossible or asinine, future energy inflation shocks would make it more manageable.

And we always pay above asking.

… and every house sells for above the median price.

Are you in southern California?

We in so California think like this 😀

Seneca, please take a hike off a cliff.

Or just wait for the cliff to erode and fall into the sea.

My mom says I’m special

No surprise here. Number crunchers are lagging v.s. real time.

Its no longer just housing. No shortage of manufacture’s in my area

that are seeing orders collapse. Inventory rebuild is about finished.

Gonna be one heck of a ride.

Northern Virginia area, online listings of even “trophy” properties, $2.0 mil plus listing prices show, “price drops “of as high as $100,000K.

Also, FNMA’s website, Homepath, indicates massive rise in inventory of foreclosed homes in all US states.

Things are not looking so great in the cottage ownership industry!

Thanks for the HomePath cite…potentially a useful tool.

Kinda surprised the FCS are already rising…it normally takes substantially longer.

If the government passed laws to phase out RE subsidies, I think you’d see see future RE transactions perk up to a normal level. Prices would recede as well.

Now that RE subsidies have distorted the RE market beyond expectations, it’s a great to remove subsidies. The RE industry obviously can handle it after 100% to 300% price gains over the past decade.

Like-Kind exchanges, lifetime gain exemptions, mortgage interest deductions, MBS purchases by the Fed, etc. It all needs to be scaled back.

Eliminated! Already…..

The Fed stopped buying MBS securities last week.

Mortgage interest deduction is not practical for most families. A married couple has to have over $27k of deductions before it makes sense to itemize.

Wrong. If the deductions weren’t there, the price paid would have been *much* lower.

The corporate landlord deductions are alive and well – Schedule C Business deductions.

Ma & Pa Kettle landlord – Schedule E.

Huge difference.

Spoken like a true non-homeowner or from a family where there isn’t a snowball’s chance in hell that you’ll inherit a dime.

You do realize that many, if not all, of those deductions for individuals (I’m in favor of not allowing any of those for corporations) are intended to support the family unit.

Remember those?

Home prices will always be out of reach for some, especially those that want to live a luxury lifestyle on a beer income.

The family unit does not subsist on real estate alone.

Subsidizing one thing always comes at the expense of *everything else*.

This is melodramatic. A married couple making $60000 only pays about $3800/yr in taxes, so that’s the maximum the mortgage deduction is worth, and it is likely worth much less than that due to the other deductions that family can take.

If Congress just did one thing — remove mortgage interest deductions — the price of houses wkuld fall substantially.

The mortgage interest deduction HAS been getting reduced steadily. It’s been chopped a couple times in tax bills, and of course INFLATION has been eroding it substantially. I think it’s maybe $750k of principal, max. Remember back when that was real money?

The cap gains deduction has also been slashed via inflation. It’s worth what, half of what it was in real dollars since Clinton changed the law?

That’s $46,500 you can deduct for the first year of a mortgage at 6%. Without that deduction, the house would have been substantially cheaper.

And capital gains is still a $500K exemption. Also a massive distortion on price, especially since the money from that can be applied to the next purchase.

All laws that make homes attractive *investments* should be removed so more people can afford a place to live.

If you would roll back time to 2010, a 6% to 7% mortgage rate would look good if not great. LOL

After, 2019 and when the FED artificially reduced interest rates, all banks stopped keeping home loans and just sold them. Who wants to loan $400k for 30 years at 2.75%. Too much risk at that interest rate.

I am guessing the 6% or higher will get us back to normal rates. It may take people awhile to get used to.

People will always need a roof over their head. It may mean a smaller roof. Inflation can be sticky and unless the input prices for new homes drop (land, lumber, labor, etc), some of the single family housing price appreciation is going to stick.

How far will housing fall? Anyone want to make educational guesses. I know it is regional, but considering inflation is sticky. From the median house price peak of around $400k, I say an early 2021 median prices of low $330k – $340k if we have a soft landing and 2019 prices of $300k if we have a hard landing.

ru82

I would say your estimates are spot on. The 1st of Wolf’s charts shows a normal trajectory would have a median home price just over $300K in 2023. There will be swing pockets – there always are, but the sand state homes that went up 50% in 3 years (like they did in 2004-2006) will lose 40% and people will be screaming “crash crash.” Not a crash, just a correction to normal. The Midwest will correct its standard 10-15% and it will probably take another 2 years.

The volume of buying opportunities that came in 2008-2013 will not be there this time.

“The volume of buying opportunities that came in 2008-2013 will not be there this time.”

Pure, unfettered bovine excrement based upon wishful thinking.

Forced selling – massive foreclosures and teaser rate ARM expiration – was a major factor in the price declines 2007-2010. Those factors are not present here. A correction to a normal long-term trajectory is a reasonable prediction. A repeat of the subprime borrowing situation is not a reasonable prediction.

Unemployment rate in 2009 was 10%.

Fetter them bovines.

DC

I would be interested in hearing a theory to back up your standard vitriol.

David points out even further reasoning to support my hypothesis.

Beardawg & David,

While those factors (ARM, unemployment) aren’t an issue right now, there will be others that will take their place, no?

Also no fast v shaped recovery ,congress is broke only more fake currency

“David points out even further reasoning to support my hypothesis.”

No he doesn’t, he just shovels more bullshit into the mix. Prime loans were, BY FAR, the bulk of the foreclosures last time. But shills like you just parrot nauseating crap that is meaningless.

Never say never.

I am surprised at people making predictions that home prices won’t fall a lot.

I have been wrong before and I thought the same in 2009 hb1..

If we have a serious depression 40,000 happened before history repeats

We’re guaranteed a hard landing, its not possible given all the insane speculation in every asset class over the past decade or so. Housing index per Case Shiller will lose 30% easy, but if you have cash you’ll be able to pick up something for 50% off no problem, just like what occurred in the aftermath of the last bubble.

We havent even seen the waves of layoffs coming, the bankruptcies and defaults to follow but its inevitable as the free money gravy train gets a stake through its heart.

Layoffs are not inevitable. Corporate profits are they highest they have been since 1950.

All financed with basically free money Harrold. That gravy train is nearing the end of the line. Rate hikes take time to filter into the bottom line of businesses. Around 9 months on average. You ain’t seen nothing yet. We have more “zombie” companies now than ever before in history. What happens when they can no longer finance their debt at 0%??

Layoffs and insolvency, that’s what.

The tight labor market was created mostly by government overstimulus causing overspending on tangible goods. Businesses had orders to fulfill and not enough people to do the work, so it drove unemployment down and wages up.

We are clearly past the peak in that demand, but it takes a while for businesses to work through elevated backlogs.

In our truck equipment business, we are about four more bad order weeks away from the first round of layoffs. That is down from a buffer of about 16 weeks at “peak crazy”.

Two of our aluminum suppliers had lead times nearing a full year in 2021. One is now at 2 weeks and the other is at 8. In an average year, both would be 12-16 weeks out at any given time. Their product demand has disappeared. Poof.

Small/medium businesses like our will tolerate a drop in profit to preserve core jobs if we feel it necessary but we are still required to stay cash flow positive.

Big public companies are expected to make ever more money than the last year, so I think it is in error to think they will allow profits to fall take save jobs. And even if they do tolerate lower profits, those can evaporate overnight with even a modest shift in demand.

Layoffs will follow a slowdown in buying activity. To think otherwise is downright crazy IMO.

I think the mortgages were being sold long before 2019. Why do you think that big MERS mess happened back in the 2000’s when no one knew who owned the mortgage on what?

For a bank to hold a mortgage or a car loan is nearly unheard of. If you’re the son of a banker or his nephew…. maybe. Car loans are bundled up into bonds and sold. So are mortgages. Car loans have been that way next to forever. Do you think Ally has billions laying around just waiting to finance your dream ride? Nope.

Typo…I meant 2009

“From the median house price peak of around $400k, I say an early 2021 median prices of low $330k – $340k if we have a soft landing and 2019 prices of $300k if we have a hard landing.”

I think your estimate is very accurate. I think a 20% loss in housing prices with 10% wage inflation would be a lower limit for a soft landing. ie 320K with a 10% wage increase for everyone. These would be late 2020 prices.

It should be fairly painless since most of the increases have happened within the last 3 years. Not as many people will be underwater with the latest bubble deflating 20%. The volume of home sales during this time was less than the previous bubble.

Most of these buyers within the last 2 years have an extremely low mortgage rate and are less likely to panic and walk away.

I believe the vast majority of homeowners purchased their houses before 2020 and have an extremely low mortgage rate and over 20% equity. They won’t panic (Unless they HELOC’d all of the cash out their home)

The Fed doesn’t want a hard landing and to repeat 2008 and have massive foreclosures, so they will not let home prices drop over 30% (280K). All they have to do is start buying MBS’s again to lower mortgage rates to start the homebuying again.

Massive unemployment would wreck my theory and cause buyers to flee and house prices would spiral down unchecked. Like 2008. I don’t see that yet.

The Fed is extremely unlikely to purchase MBS as you suggest. They have openly admitted that they don’t like MBS. And don’t forget, any form of QE is inflationary. Just today Powell warned of what is happening in housing. Since the banking system is not vulnerable to price declines, the Fed will not only let them occur, but will point to them as a much needed correction, which is precisely what Powell did today.

I think if a deeper recession occurs like in 2008 with massive job losses, the Fed will use any tools possible to prevent 10+million homeowners from jingle mailing back the keys.

This includes driving down mortgage rates with MBS purchases.

I am not a conspiracy theorist so I don’t think the government wants to take back everyone’s home with foreclosures and make us all a rental society.

It’s bad for gaining voters.

Rents have also gone up. It may not be cheaper to walk away from a mortgage and rent a place.

Often in a recession, people don’t have the luxury of choice. Most Americans live pay check to paycheck with little in savings. When you loose your job and you have a few weeks to a month in savings then you’re sh$t out of luck.

Home prices are set at the margins.

People won’t want to sell but they won’t be forced to sell.

For example.. my friend bought in 2021 fixed rate at 2.75% but is now selling his home because of divorce.

Many reasons people would be selling

Jon,

I agree, people will always have to sell due to death, divorces, and voluntary moves. This is normal. It happens in a normal market. It typically doesn’t drastically affect home prices.

If a massive increase in death, divorces, or job losses force people to sell, then the housing market would plummet.

Also. Hotels are now very expensive. I was looking at maybe taking a 3 day weekend vacation in October to New York but good luck finding a hotel under $400 / night including tax. I thought October might be off season.

Then I took a look at Charlotte, SC. Same thing. Everything is $300 and up.

So a 3 day weekend with air would run $1500 to $1800 and that does not include food.

I am nixing the idea of traveling and just staying home

You are correct. We are traveling for a few days. Meals will cost what I used to pay for a room, and a room will cost what I used to pay for a months rent. I don’t care. Or I am going to do my best not to care.

Until “pay anything” people like you stop traveling, look for more of the same. The question is “how are you in a financial position to not care what you pay for something?” Powell created too many of you, now he needs to financially destroy those like you.

Being frugal, reading this blog and acting from what I learn, driving on one 4 day trip a year in the shoulder season, staying healthy and saving money with a garden and vegetarian diet. Sorry to disappoint, JP is helping all my treasury notes.

I think you and I would get along in real life!

You dont care!?

You may save some money from planting veggies but you spend carelessly on expensive trips 1000x more, lol 😂

I get the idea that everywhere is expensive now and you cant wait to get out somewhere. Hope next year will be less desperate demand from people that were lucked down for 2-3 years, so the prices will be logical, checked and same thing is happening in AirB&B (AirB$B)

I’d guess a lot of vacations are just expensive fantasies of freedom which the unhappy afford themselves. This can be anything from chips ‘n’ dips in a hammock in Club Med to a drug binge in your own (barely) living room.

Travel is different; going places. Spending money on exploring your planet — not even anywhere glamorous or passport fodder — just checking stuff out. That’s always a pretty great investment.

“I think you and I would get along in real life!”

Probably. I was just pointing out that it’s the “pay anything” mentality that needs to be extinguished in order to get inflation under control.

Perhaps in the future people will save on

“escaping” for vacations by participating in a virtual reality session and/or taking a custom hallucinogenic enablers; or if you really don’t mind spending the money, do both, like the 2023 version of “Total Recall”. Sometimes people will pay up to escape their present reality.

I was hopeful September would be off season pricing as well, at least cheaper than June to August but not the case. The only thing that saved me is discounts from my buddies GF who works for one of the big chains.

That was my last Vaca for the year and I’m hopeful that as people start running out of their excess cash hotel prices will start to come down by the time I need to go again. So far, as per Wolf’s articles, employment numbers and consumer debt levels still look good in the US (where I mostly travel), but participation rate seems to be ticking up so maybe we are on the way to some normalcy and tighter personal budgets in this inflationary period. Who knows though, I seem to be wrong on everything all the time these days 😆

Just looked at choicehotels website and charlotte NC for three day weekend mid oct there are plenty of hotels listed at 50-70$ a night.

I suppose a lot of people cant drop their egos enough to take a decent clean room for that price and need top of the line instead.

So be it but maybe dont complain about lack of lower priced rooms. They still are out there. But you have to look.

I just completed an 18 day road trip midwest and west and paid average per night 0f $64.71.

The gas price though for that trip I will complain about.

There was a typo above but I’d guess it was the city name and they meant Charleston, SC. Who wants to vacation in Charlotte?!

Plenty of hotels in Charleston SC under $100.00 also. Hard to find one that price if you need to be in the harbor / old town but within 15 miles plenty.

I spent a night recently on business travel and just stayed a the closest place to the worksite for $80/night. My boss wanted to know if I had stayed in a hostel when I turned in my expense report.

What I also was surprised about was how Hilton Honors points seem to have devalued lately – I still remember times when we stayed in a very nice Hampton Inn in Atlantic Beach NC just minutes from the ocean (not oceanfront, but really close) for around 32000 points per night.

Not only the cheapest one in that area (almost 20 minutes drive from the ocean) is 35000 now, many properties have “This property cannot be booked using points at this time” message on them.

My favorite one though is a motel-style Hilton property in Bethany Beach DE that wanted ~430 000 points per night for a regular room in July-August. This is just insane.

I’m in a 80 sq ft “pod” hotel room in NY. 520 dollars a night.

I wonder how long it’ll be before the chart with the active listings will take to reach 2016 levels. Is this something that speeds up or slows down over time?

The active listings are so manipulated by realtors, I doubt we will see those numbers again.

I suspect most people know they are priced out of the current market and will not list their home unless forced too by lost income.

When I walk through the nearby neighborhood, I see empty homes but no for sale signs. This has been true for five years in a couple different towns. I don’t know why this would be true, not for for sale and not rented, given the housing shortage, of affordable house. Who is sitting on empty homes? Who can afford to?

Locally even folks making $100,000 a year can’t find affordable housing.

The Fed has everything F’d up, and I don’t believe it is by accident. Someone is benefiting, just not the majority of Americans. It could be an ugly election season.

Property taxes!,

Bingo. In my area, they are insane. I have one neighbor paying $48,000/yr in property taxes.

I think that we are basically seeing a market that is starved of buyers, but sellers are not yet piling in to sell. The sellers need to feel some pain, seeing declines for multple months before they start to really hit the sell button.

This is a little like the trajectory of someone on a trampoline, as gravity overcomes the upward momentum, they just hang there for a short while, before the plunge.

Some sellers will sell after the reading of their wills.

Not unusual to find 80+ year olds in the same houses 50+ years in my neighborhood. No senior or assisted living. No going to FL or AZ. Going down with the ship. It’s their home.

Fed pivot fantasy? The Fed just told us when they’ll pivot. The Fed dot plot as reported by several major financial news outlets shows more hikes tapering into the the end of 2022 with a mid-4% terminal rate (a pause for 2023). As QT effects sink-in while debt actually starts to cost something, they think they’ll have inflation on the run in 2024 and back to 2% by 2025. They’ll pivot either as inflation fades closer to 2% (soft landing) or they’ll get hit with a scenario they haven’t acknowledged in which a major dive into a deep recession occurs killing inflation sooner than their 2025 target (hard landing). I vote for the latter option and I don’t think they’ll even make it past 4.5% without something breaking catastrophically. The economy nearly broke under a lower FFR and slower QT prompting the last pivot. It’ll break faster and harder this time, and the only things the Fed knows how to do to address a crashing economy is drop rates and monetize debt. There’s a 0% chance this debt-ridden economy can survive even another year of historically normal-ish interest rates and fast balance sheet run-off. It’s already breaking, with this Wolfstreet article as proof.

The fed pivot fantasy label wolf uses refers to a specific period between mid-July to mid-August, every fund manager and analyst with a microphone was spreading that message and markets rallied, mortgage rates dipped.. he’s just referencing those past articles for those of us here who read them.

Fair enough Seba, but I think there is still room to theorize that a pivot could happen much sooner than I suspect Wolf would be willing to acknowledge. It all hinges on where employment is headed in the next couple quarters. If tightening causes a significant slowdown going into 2023 and credit availability starts to lock up, heavily indebted institutions collapse, equity evaporates, lending freezes, inflation stops in its tracks, and the fed pivots faster than you can spell “QE.” Anyway around it, I posit that the Fed will not be able to maintain a 4%+ FFR and $95B/mo QT for very long. Something in the financial system is going to break catastrophically long before the Fed is able to reach any really meaningful balance sheet reduction.

Well, it sure seems like the system is holding up just fine so far. I’ve wondered if the massive money supply might make it possible for the Fed to sustain rates of roughly 4% or maybe even more. I think this is a really new situation. One in which there is massive money sloshing around, which causes the inflation, of course, but it might make it possible to sustain meaningful rates for a significant period of time. Your point about QT may be the key. Too much QT could make things too normal, and we can’t have that.

Not Sure,

READ THIS:

https://wolfstreet.com/2022/09/21/powells-whatever-it-takes-moment-our-policy-will-be-enough-to-restore-price-stability-fed-hikes-by-75-basis-points-in-shocker-sees-4-4-by-end-of-2022/

Unemployment always rises after thanksgiving,construction industry really slows down in flyover country,plus no more data centers ,cost to high . Semiconductors will get slaughtered,also effects of less driving in winter.Of course will take credit for slowing conditions,there so full of shit .

Re “The Fed just told us when they’ll pivot. ”

No, they didn’t. None of their previous statements has been accurate. Today’s wasn’t any more accurate.

In any case, the whole interest-rate / dot-plot thing is theatrical distraction. Low interest rates didn’t create inflation anywhere, so high rates won’t stop it. What goosed inflation was the pandemic money-printing. What will stop inflation is the QT (money supply contraction) that they barely talk about. Today’s QT is a slow process, at best -1% of peak money per month. Since the money supply is probably 2x where it should be, it could take about 4 years to get the money supply back to normal. But they can’t go faster without destroying the financial system.

https://wolfstreet.com/2022/09/21/powells-whatever-it-takes-moment-our-policy-will-be-enough-to-restore-price-stability-fed-hikes-by-75-basis-points-in-shocker-sees-4-4-by-end-of-2022/

So, it is OK for home prices to increase 50% or more in just 24 months or so enriching the elites but it goes down by 5% or less, then the economy is breaking ?

Just asking.

Are rents going up in response to the interest rate hikes like in Canada?

A one bedroom apartment in a small town Ontario is almost as high as renting in Toronto.

Rents are rising crazy in Ontario.

I assume you refer to asking rents. My hypothesis is the new rentals coming on to the market are the investors who think they will ride out the dip in prices by just renting at some astronomical price. The rent can only go as high as employees can afford. It is just temporary because real estate prices will come down (with a lag), due to rate increases which means housing may be back to normal range of mortgage payments being CHEAPER than rent, imagine? I am renting for about 3000 per month a detached home. If I were to purchase this home, my mortgage would be 7000 per month, and I require a 20% down payment ($280,000) due to rules in Canada.

“….the widely propagated fantasy of a Fed “pivot” on rate hikes.”

Paging talking head Luke Groman. This guy was spouting off all over the place that the FED would be pivoting in Q3, and early Q3 at that.

A different market a different place. Housing prices may flaten out, or at least for the time beeing stick.

More telling, startup of new single family home builds are down 25% from august last year to august this year.

We in southern california think the same:

Home prices cant crash. Either it can go up or remains flat but never go down. Even if it goes down in an unlikely scenario, it’d only go down 10-15%, so what it increased 50% in last 2 years.

We are special and this type is different

Two million billion ‘undocumented’ (using a euphemism) don’t drive up rents. Right Joe?

Wait, I thought we blamed Powell for everything on this blog?

Credit where credit is due.

It’s all about ‘fairness’ isn’t it?

Crook County IL is starting UBI. Seriously.

Yes, but 2 million “undocumented” workers working under the table will drive down wage inflation.

Maybe we don’t have to get off our comfy couches to work for less money and help save the country from wage inflation.

City stuff, same as always. It IS a bigger volume these days. There are HUGE increases in rural RE – even off grid stuff. If one can get away and exist. Without metro services. Gee, how does someone pump a septic and know when to do it?!? Water – duh.

It is curious to me, living in the sticks for many years. Absolutely clueless people that are going to discover freedom. Or is it Liberty, democracy, etc. We’ll just get some land!

Then they sell out or just never come to occupy their place. It’s too hard.

With great freedom comes great responsibility?

With Putin’s nuclear saber rattling the sticks might be calling my name. I’m living in a big SouthWest city without even a basement to serve as a bomb shelter. I once poked around at woodsy property (raw dirt) in Idaho. How do we get water? How deep a well would it take at what cost? What about trash disposal? And like you mentioned, septic tank issues. For someone accustomed to suburban living the sticks could be a challenge.

Don’t waste your time nuclear fallout ,will get u anyway .Or nuclear winter, Russia has been speaking this bullshit for 60 years,called diplomacy

My strategy is to always have a very cold 6 pack of my favorite beer to drink between the hour or so when they first drop on DC / surrounding counties until they catch up with me in flyover.

On the bright side, a nuclear war would certainly drive down house prices in major cities.

I don’t think it would happen unless Putin believes that he could start a nuclear war without causing massive nuclear retaliation against Russia. No sane leader would want to the the head of a former major country reduced to nuclear rubble. It sounds MAD.

There is a chance that he isn’t sane and is currently asking his advisors why he can’t use the nukes. Just like when it was asked in the US. Hopefully he has sane advisors stating the obvious.

It is interesting that longer term bonds actually rose today, after the Fed meeting. The market is more scared of a recession than believing in long term inflation.

I still dont see this inflation being similar to the 70’s. I dont see the drivers of a wage-price cycle of inflation. We have had more supply chain disruptions, which get fixed. We have had more specific industry related issues and we had massive monetary stimulus. As the Fed keeps selling bonds and MBS and raising rates and the stock markets and real estate markets sell off, that will rid us of the fuel that has caused these big price increases.

Energy prices fell today even after Putin upped the ante in Ukraine. I just think that the world economy will be in full contraction very soon and that is not an infationary environment.

Yes, inflation numbers will continue to look bad for a few months, but they are peaking, rents in Los Angeles have even started to fall in the past month.

The wage price spiral has already lifted off. The local casino hotel had a TV ad running for housekeepers at $22/hr and a multi-thousand dollar signing bonus. Powell has got his work cut out for him and wage / rent inflation will be the toughest to curtail. This could take years.

An actual stock crash (not like the price declines since January) would solve the problem you describe really quick. Same for junk bond market since both are tightly correlated.

That’s all it will take for C-Suites to initiate large scale layoffs to attempt to support the stock price and exceed EPS estimates.

Wolf, Do you think this Fed rate increase along with the prospects of further increases in mortgage rates will spur a short mini sales spike? Sort of buying in before it gets really crazy?

That mini-sales spike already happened late last year when rates started rising. Now it’s too late.

Low-interest rates and QE seemed to push the stock

market as high as possible. Re still had room to grow

though but the big money was made.

Though it took a while it is time for the savers to cash in.

For us its CDs and tips but the people in the know are

playing a bigger game

.We will find out what in due time.

In the meantime stay in your lane.

want to get burned stay in your lane.

Sorry the want to get burned was an error.Please ignore.

Still a sellers market if u are looking to cash in on over inflated values. The devaluation of homes and stocks beginning the long journey back to reality. Hard to believe just 5 months ago the market was on fire. Buy low Sell high. The last 2 years of economic expansion maybe the fastest and greatest some will ever see in this lifetime.

New to this site but devouring the past and current content. As a first time buyer, it’s a brutal time.

My question is, what will actually motivate people to sell? Sellers have locked in low rates having refinanced in the past two years, they are attached to the high prices they’ve seen their house valued at on Zillow, they may not WANT to sell. But will there be a reason they HAVE to sell?

I know that depends on the job market, economy, and other factors. It’s just crazy to think a decade ago, thousands, if not millions, were in over their heads, and now everyone is able to make their payments. Especially given how many people quit their jobs in recent years. Maybe it will just take time for all of the normal cycles and factors that typically impact housing to come back into Play after having hit pause during the pandemic. I see that taking a while.

Have to sell?

When property tax keeps going up while value goes down, or income at fixed / lower level while that is happening.

For those with government jobs the above is not applicable.

Don’t focus too much on housing. Focus on wealth-building. Things are about to blow in this artificial economy, and you want to have options when that happens. Don’t commit yourself to a single asset category when asset prices are super high.

The worst move now would be to tie-up all your capital in an overpriced home and furnishings.

This was meant to be a reply to First Time Buyer.

They opened pandoras box, wealthy people sucking up income property like it was crypto and looking to live off of low income servants. These people need to be burned. Let the bank stocks/debt go to zero. FDIC deposits should be only thing bailed out. These market traders searching for yield for their high net wealth need to find closest high story building.

Moving to the country, gonna eat a lot of peaches. In the last financial contretemps, lots of burglary in semi-ruralities while the owner’s gone at work or play. Locks are for honest people and technology is defeatable if you’ve got stuff worth stealing and nobody’s around. On my street we look after each other. And there’s always people at home. The prospect of encountering an armed citizen is much more daunting to would-be burglars than arrest by police here, which is not fun. Our DA’s don’t play either, convictions are typically swift. In the country you wait on the sheriff while defending yourself or picking up the mess the crooks made. Not everyone who moves there can face these uncomfortable possibilities.

There’s a farm in the family, but I wouldn’t stay there alone these days.nothing bad has happened there since cattle rustlers in 1966, doesn’t mean nothing will. These times will see much desperation and loss, those who thought they had something and then lose it won’t be overly concerned with following rules.

Doom alert- Sometimes more than one problem (inflation) happen during the same period of time. People now think things are bad and getting worse, but imagine if we had wide scale grid failure for one reason or the other in addition to a recession. There are plenty of possibilities: nuclear attack, meteor strike, terrorists, war with a major power like Russia, weather related etc…

Being down and out and ill-prepared probably increases the chances of getting kicked. Prepare for the worst and hope for the best!

I think what we are seeing is the dark side of living on debt. Granted it is near impossible to purchase a home without taking on a large debt but too much emphasis is placed on mini mansions mortgaged as much as the market will bear.

In my mid 50s, my company underwent massive acquisitions and I saw the results on acquired professional staff. Took note of that, and determined to get out of all debt within 15 years. Yes, a lot can change in that time but that was the goal. Remortgaged the balance on a 30 year down to a 15 year, and started weaning off the credit cards.

When the company finally started to implode as many bloated global firms do, I was 66 years old and ready to retire if and when the “exit offer” was made. It came and I grabbed it, 2nd from last man standing in the finance group I was in. I was within 10 payments of the end of that 15 year mortgage when I left and just continued until paid in full.

Now moved to the country and happy as a clam at the beach. Because I have no debt, I really don’t care if the ranch home I have is worth $600k or $100k. It is a great place on a lake, and very, very comfortable.

For those in their 50s or earlier, suggest you get real and focus on a debt free future as soon as you can. The sense of liberation is overwhelming.

I agree. 52 and on an all out mission to pay off remaining investment debt by years end. Diverted $300k over last 3 years to build my sons homes so they will not be mortgage slaves. That messed up my timeline quite a bit.

No more leveraging to build wealth. I have plenty. From now on, cash only. I feel…relieved. like a self imposed stress weight has been removed. It was great while it lasted, but I am out of energy.

“Diverted $300k over last 3 years to build my sons homes so they will not be mortgage slaves.”

Coddling your adult son? Unreal. Make him pay for his own shack.

I could see this bubble forming, which is why I sold my condo in Bozeman MT, which I bought in 2020 for $305,000. I sold it a few months ago for $450,000. It sold in a week for asking price. Now if you look in the market there nothing is selling and you have $50,000-$100,000 price drops all over the place. Bozeman MT is building so much right now that inventory will be so high that price drops every where will be inevitable. I wouldn’t be shocked to be able to rebuy my condo I just sold for $250,000 in a year. Anyway I’m renting a place in Southern CA sitting on the sidelines with my pile of cash waiting patiently.