“Balance sheet normalization” will continue even if the BoC cuts its rates. It’s all about “settlement balances.”

By Wolf Richter for WOLF STREET.

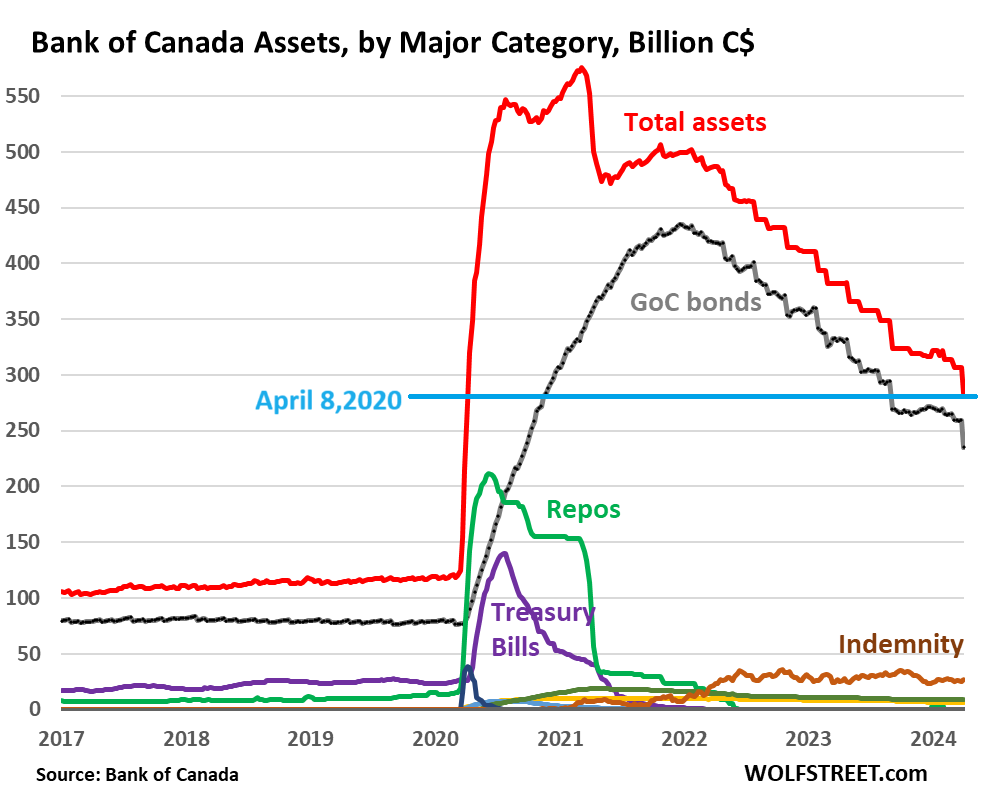

The Bank of Canada, in its quantitative tightening program, does not cap the roll-off. Whenever Government of Canada bonds in its portfolio mature, the BoC gets paid for them at face value and doesn’t replace them. That’s the roll-off. There are months when nothing in the BoC’s portfolio matures, and there are months when a big bond issue matures. GoC bonds mature on the first day of the month. There were no maturities in December and January; $3.6 billion matured on February 1; $6.6 billion matured on March 1, and on April 1, $23.3 billion matured.

So, in latest weekly balance sheet, released Friday afternoon, total assets dropped by $23.3 billion, to $283.5 billion, the lowest since April 8, 2020.

In terms of pandemic QE: -64%. The BoC has now shed 64% of the assets it had loaded up during pandemic QE (gray line). In terms of GoC bonds alone, the BoC has shed 56% of the GoC bonds it had added during pandemic QE. The BoC already shed its entire holdings of Canadian Treasury bills (purple) and repos (green).

“Indemnity” of $26.9 billion (brown in the chart above) is the value of the indemnity agreements between the federal government and the BoC that represents the unrealized losses on the bond holdings, if the BoC ever sold the bonds outright today at today’s market prices.

The BoC and the government have a deal that requires the government to reimburse (indemnify) the BoC for those losses on the GoC bonds, if the BoC actually sells those bonds and thereby realizes the losses. But if the BoC holds them to maturity, it will get paid face value, and those losses vanish.

The BoC doesn’t sell bonds, but sheds them when they mature, which is when the BoC gets paid face value for them. So as the remaining bonds mature over the years, this “indemnity” account will slowly go to zero.

What QT looks like going forward:

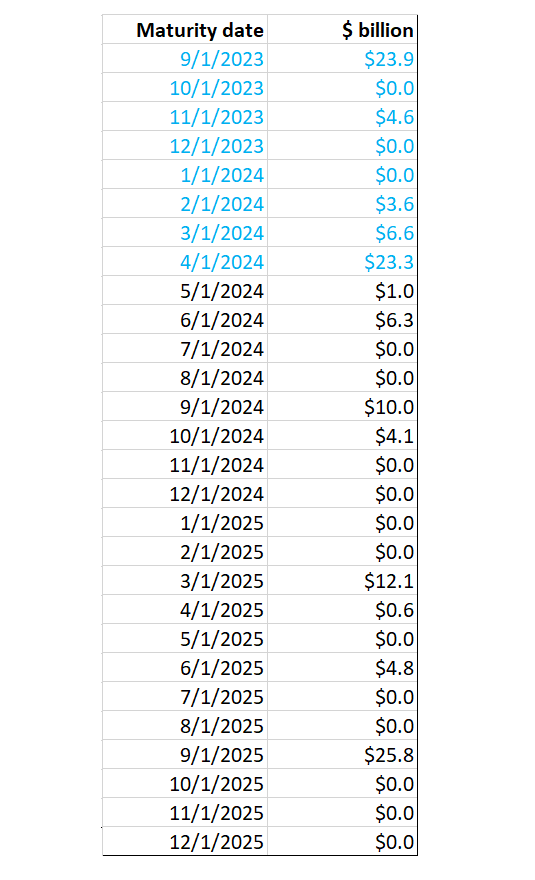

Below is the maturity schedule of the BoC’s holdings of GoC bonds. For illustration purposes, we have included the last 8 months (blue figures); those bonds are already gone.

The future maturities in GoC bonds through 2025 (black figures) amount to $65 billion at face value. The last maturity in 2025 is on September 1. There are no maturities in October, November, and December 2025. In other words, if QT continues through September 1, 2025, another $65 billion in GoC bonds will roll off. We’ll get to that in a moment because the Bank of Canada has started discussing it.

When will the Bank of Canada’s QT end and what will come afterwards?

The Fed has also started talking about this issue of how low the balance sheet might go – withdrawing liquidity can get very tricky because liquidity doesn’t always smoothly and quickly flow to where it’s needed, and that could turn into a mess – and we dove into it most recently here: The Fed’s Liabilities: How Far Can QT Go? What’s the Lowest Possible Level of the Balance Sheet without Blowing Stuff Up?

During QE, a balance sheet level is driven by assets that the central bank purchases in large quantities, and liabilities come up in equal measure (always: assets = liabilities + capital). If assets go up, liabilities must go up in equal measure.

During QT, when a central bank sheds assets, liabilities must decline in equal measure.

The BoC’s big three liabilities.

Bank notes: The largest liability during normal times is currency in circulation (“bank notes in circulation,” as the BoC calls them), and they’re demand driven. When you withdraw $500 from an ATM, you expect the ATM to have the $500, and it’s the banking system’s job to get enough bank notes from the central bank and have them ready for customers.

The BoC has a liability of $115 billion for bank notes in circulation, which have continued to grow over the years. And they’re market driven.

Government deposits. The BoC is also the checking account provider for the government of Canada, and the deposits of the government are determined by the government, not the BoC. The deposits currently amount to $32 billion.

So already, there are $147 billion in liabilities that the BoC does not control. And they must be balanced with $147 billion in assets.

Bank settlement balances. The other large liability represents cash that banks put on deposit at the Bank of Canada, $127 billion on the current balance sheet. But two weeks earlier, they’d been at $105 billion. They have fluctuated in that range for months.

Settlement balances are similar to the “reserves” at the Fed. They represent liquidity in the banking system. Banks use these settlement balances to pay each other via the BoC. And they use them to keep extra liquidity at the BoC.

Settlement balances ballooned during QE and are now shrinking during QT. If they shrink too far under the current setup, the banking system and the broader financial system may run into liquidity issues.

Other liabilities. The BoC has some other liabilities, including reverse repos, but the amounts are small.

Settlement balances determine when QT ends: September 2025?

Deputy governor Toni Gravelle outlined this process on March 21. In his speech, he said: “The right amount of settlement balances to supply the system is uncertain. The bottom line is we will lean toward holding them at the minimum level needed to effectively implement monetary policy in a floor system.”

So what’s that minimum level? He said the BoC expects settlement balances “to land in a range of $20 billion to $60 billion.”

And he added: “But we are aware there is a risk that we could be wrong about the $20 billion to $60 billion range. There is uncertainty because it is fundamentally difficult to assess the demand for settlement balances.”

Settlement balances were $127 billion on the current balance sheet, but were $105 billion weeks earlier. And they fluctuate a lot. So we’ll go with the $105 billion. To get into the $20-billion to $60-billion range, they would have to drop by $45 billion to $85 billion.

Looking that the maturity schedule above, we see that the maturities through June 2025 amount to $39 billion, which wouldn’t get settlement balances into the range Gravelle indicated; it might only get them to $66 billion ($105 minus $39), a little above the range.

Then there are no maturities until September 1, when $25.8 billion mature, and that’s the last maturity of the year. So with the September maturities, the total maturities amount to $65 billion, which might get the settlement balances to $40 billion ($105 minus $65), smack-dab in the middle of the $20-$60 billion range that Gravelle proposed.

QT and rate cuts are separate. Gravelle re-pointed out that any rate cuts and QT (“balance sheet normalization”) are separate. The BoC can cut rates and continue “normalizing” its balance sheet until the desired settlement balances are reached. The Fed is on the same program, as is the ECB, which may cut in June and continue with its massive QT.

After QT ends, short-term T-bills and term repos will replace GoC bonds that will continue to run off over a “multi-year transition period.” The balance sheet will then grow as before QE, driven by the liabilities, but for the multi-year transition period, the composition will change with short-term T-bills and short-term repos (both are now zero) growing and replacing longer-term GoC bonds. There have been similar discussions to that effect at the Fed.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Meanwhile, in the neighboring country to the south:

Bloomberg, Apr 5 (Christopher Anstey, Senior Editor): “Former Treasury Secretary Lawrence Summers said that the surge in US payrolls in March illustrates that the Federal Reserve is well off in its estimate of where the neutral interest rate is, and cautioned against any move to lower rates in June. ‘This was a hot report that suggested that, if anything, the economy is re-accelerating,’ Summers said… Alongside other factors including an ‘epic’ loosening in financial conditions, ‘it seems to me the evidence is overwhelming that the neutral rate is far higher than the Fed supposes,’ he said.”

Exactly. These clowns paused way too soon, paraded themselves around talking about rate cuts this year, then have egg all over their “transitory” faces again. Jerome Powell should be removed from office immediately. He is a miserable failure of a human being.

That is BS. Powell’s actual results have been pretty good in that inflation has come down significantly *without breaking anything*.

The Fed could certainly have moved faster or gone higher but it’s impossible to know how much faster/higher before something _did_ break, which you of course would whine about.

The Fed’s predictions are based on the recent trends continuing with clear language that actual policy of the future will depend on actual measurements in that future. Exactly as it should be.

This is like thanking the firefighter for lighting your house on fire and then putting out the fire quickly even though 70% of your house got burned down in the process. Or thanking the kid for throwing a rock at 4 windows and then repairing 3 of them for you. The point is, they didnt have to do this stupid crap to begin with….and there would be nothing to fix. To which you will say ‘but if they didnt give out a bunch of free money in 2020, the whole world would have imminently imploded’ even though you actually have no idea what would have happened, this is just a theory that gets perpetuated to justify the bad choices made by our leaders in a time of crises (and after) that we have to work through still today, years and years later. You probably just benefitted from the crap policy, as many did, which is why many ppl feel what was done is OKAY, even if its to the detriment of our country’s future.

You do know that firefighters WILL light and burn things to stop a greater threat, right? It’s called a “fire break”.

The Fed’s actions prevented the Financial Crisis from becoming Great Depression 2.0. The Feds actions stopped the free-fall of the economy at the start of the pandemic. So yeah… I benefitted, as did everybody else. The cost seems worth paying, at least to me.

We can argue about how far things would have gone had they not acted – nobody can say for sure – but it’s clear that their actions reversed the directions at the time.

I think you missed the point.

You are just speculating. You have no idea if it would have been a great depression 2.0. Maybe our economy would have been BETTER OFF, who knows??? I won’t claim to.

Right now, for the poor, due to the newfound cost of living, it might as well be Great Depression 2.0. But you are sitting pretty because of poor policy, so that’s fine, right? Meanwhile they are figuring out how to let low class workers sleep in their car because they cant afford a place to live. Is that prosperity to you?

Classic out of touch mentality. Justified by a propagated, speculated theory.

Around this past January, senior lead economists at Canada’s major banks were asked to forecast the interest rate by the end of 2025 (really calling for the neutral rate – as it was under the guise that inflation was tamed). From what I can recall it ranged from 2.25% to 3.5%. Scotiabank’s Derek Holt was at the top end with 3.5%. Like most others, I think higher for longer is the outlook.

I’m not saying the Fed couldn’t have made better choices but to me the crux of the problem was with Congress and some state governments. The role of government is to help in times of great need like the pandemic, but it should have focused on need, not some arbitrary, extremely high household income number. I used the money to send to family overseas as I certainly didn’t need it but they did. Some of this is political, some of it is incompetence, and some simply relates to IT systems that can neither adapt quickly enough or have fraud prevention in place.

Why can our military game plan for every situation but we can’t do this for expected economic situations, especially 2008-2009? COVID of course can’t be predicted but sudden massive loss of employment, how to address it, and so forth can. Admittedly the problem there is that regardless of the planning it then depends on a highly political Congress to them pass it, but that should bring awareness too.

Again, I can excuse SOME of the mistakes made in March – May of 2020. It was absolutely INEXCUSABLE to continue making them by December of 2020 (and that includes Congress, who doled out another $3 trillion in unnecessary stimulus in December 2020 and March 2021). But the Fed screwed around and didn’t raise rates or stop printing until March 2022, a whole YEAR after the last unnecessary stimulus, and then didn’t start QT until June or July 2022 if I recall correctly.

There are three possibilities.

1) The Fed was stupid and incompetent

2) The Fed was maliciously printing in order to pump up asset prices

3) The Fed was trying to assist the spendthrifts in Congress by monetizing the stimulus from December and March.

I don’t see a fourth possibility.

Also I think it was the corps and other big political/campaign donors telling the gov’t to pass all the excessive unnecessary stimulus. They want people to keep spending to keep the revenue flowing for their operations, debt servicing, stock buybacks, bonuses, whatever else, and the dollar losing purchasing power, which is wrong to savers and doesn’t reflect well on our values worldwide, and asset bubbles aren’t deemed as important. But change starts from within. All of the us in aggregate need to decide to cut spending and learn to get by with less to rebuild our safety net for when times inevitably get tough, or they will be a lot tougher than they would’ve been if we had prepared.

Glen:

Agree on military game planning, but the lack of it in our monetary house is embarrassing. For instance, absolutely none of the stress testing of banks assumed higher interest rates… ZIRP forever????? Really??? So as a result Silicon Valley and other banks got caught naked and are no longer around due to a bad assumption.

Sad, as all of us here know there will be more, just not where.

The military can game plan for every situation but they often do not get it right either. A lot of times best to just leave things be.

Good morning Wolf,

Presently, it seems as though some people are already pushing for rate cuts and getting ready to blame the BOC for a wounded economy if they pause too long or don’t cut fast enough – I am definitely not one of these people. I think Mr. Macklem will be engaging in a slow methodical rate decrease anyways (provided there’s no major recession). Historically, if Canada has had an interest rate 0.75 to 1% lower than the American rate, that gives the BOC 1 or 2 quarter point decreases without doing much damage to the loonie – and it symbolizes that more decreases are likely when conditions permit. Right now, the BOC is the least of my worries; the current federal government has this country a bit of a financial basket case.

Happy eclipse day folks

Actually a footnote to the claim of no worries with the BOC. The verbal gaffes by the BOC are a bit frustrating but overall tolerable. The last one being Tiff claiming in the house of commons just a couple months ago that the level of interest rates won’t have an effect on the price of housing… this of course is complete BS. Then a mere 2 to 3 weeks later Tiff openly states in one of the BOC’s policy meetings that there’s growing concern over reduced interest rates inflating the housing market – one statement contradicts the other. I merely want the BOC to actually stay their arms length from the federal government.

ScrappyDoo,

Nobody notices BOC gaffes when you have Trudeau! That said, the US has you beat there!

Fair point. Outside of the claim of legalizing cannabis (a trained monkey could’ve done just as good a job of rolling it out), I don’t really hear anyone praise Trudeau.

Canada’s economic growth HAS slowed down, but hasn’t dipped into a recession yet (as of Q4). Inflation in many categories has come down a lot too. One of the glaring exceptions is rents, which continue to spike at a red-hot pace, but the BOC blames the reckless immigration policies by the government, so what can the BOC do about that, is the implication here.

https://wolfstreet.com/2024/03/27/amid-canadas-huge-immigration-surge-population-growth-hits-3-2-triggers-10-rent-inflation-even-as-home-prices-drop/

So it makes sense for the BOC to eventually cut rates once, maybe twice this year, and wait and see. If inflation continues to decline, OK then. But if inflation re-accelerates, the BOC can wave the inflation data to justify not cutting further or even re-hiking. It’s hard to defend high rates when the economy is near a recession and inflation figures (except rent) have slowed down a bunch. And then you can always hike again — that’s the classic playbook.

In terms of your federal government being a “financial basket case,” I’m just going to be mouse-quiet here, in face of the colossal financial basket case that is our own federal government.

“…the BOC blames the reckless immigration policies by the government, so what can the BOC do about that, is the implication here…”

It seems that the majority of the Canadian people like the spiking rents and mass immigration, because they continue to vote for it. You get what you vote for.

Given the amount of Chinese government interference in the last Canadian election, it is moot whether or not Canadians actually voted the Trudeau regime in.

I didn’t vote for the Liberals. I always vote for the Bloc Québécois – je me souviens, baby!

Thanks for the response Wolf. Everything you stated makes perfect sense. And there’s no doubting America’s level of public debt. However, your newest entry and Mr. Dimon’s point of “ongoing fiscal spending in non recessionary times”; what cures the affliction of low interest rate addiction? Can’t be more low rates.

Historically interest rates in Canada have always been about ten percent higher than in America to support the Canadian dollar. So if interest rates were 10 percent in America they’d be 11 percent in Canada. Everything changed in Canada when Stephen Poloz got in. Look at the charts dating back hundreds of years Canadian versus American interest rates.

All these numbers as though Canada adds up.

It doesn’t.

Here’s the off balance sheet requirements:

– Everyone’s house, shack, trailer or tent is worth at least one million dollars

– Thou shalt add one million people every year

– Thou shalt be massively underpaid

– Thou shalt pay for healthcare but receveth none

– Thou shalt pay for roads and receive potholes

– Thou shalt pay for police and receveth criminals

-and all that one works for will be taxed away…excepting lottery winnings and welfare (renamed “support” payments)

Extrapolating this information one may be inclined to conclude that there is good reason why gold, the ancient metal of kings soars in price each and every day without a care in the world? Then again, people that think this way are simply ‘bugs’ as in gold bugs…. Ha ha what does ole markymark know anyways.

How much in dividends or interest have your gold holdings paid in recent decades?

Did it matter in 1970-1980 that gold did not pay dividends? Gold skyrocketed over 20 times. Stock market went nowhere. We are in a similar cycle. I do not expect 20 times gain, but it will significantly outperform stock market plus dividends.

Interest, dividends, and capital gains of the alternatives always matter.

To use your date: If you bought a 30-year Treasury bond at auction in mid 1981, for $1,000 with zero risk of losing principal value, you would have earned 14% a year for the next 30 years. And in 2011, after collecting 30 years of $140 a year (=$4,200 plus add the interest you would have earned on that $4,200), you then get your $1,000 back. So in 2011, after 30 years you have $5,200, you made 420% on your investment, plus the interest on the interest.

So lets use another example why interest matters:

If you bought a $1,000 10-year Treasury note in mid-1981, you would have earned $150 a year for 10 years (=$1,500 plus the interest you would have earned on the interest). In mid-1991, you got $1,000 back, so you ended up with $2,500 on a $1,000 investment for a return of 150%.

Over the same period: If you bought $1,000 in gold in mid-1981, you would have paid about $500/oz, and would have gotten about 2 oz. Then in mid-1991, those 2 oz of gold were worth $740 (470/oz), for a loss of 26%.

While a 10-year T-note over that time produced a gain of 150% due to interest alone, gold lost 26%.

That’s why interest and dividends matter. And why capital gains matter. Today, people earn 5%-plus on their cash in T-bills and CDs. If you ignore the interest and dividends and capital gains of the alternatives, you’re just a gold bug. No reason to discuss anything further.

If you figure interest, dividends, and capital gains of the alternatives, then there’s reason to compare.

If you’re betting that gold will spike 1,000% or whatever, then you’re just a speculator, and that’s fine too. But you need to understand that speculating is what you’re doing.

Since 2011, gold is up only 21%. There is lots of stuff that did a whole lot better.

7.6% for the last 25 years, compounded, in capital appreciation, less you initial acquisition cost. Or 9.75% compounded for 23 years, etc.

But like a house, you can’t spend it unless you cash out. You just get to look at it. In the case of a house it’s probably a 5-bagger and you get to have a place to live.

Oh, and the money buys half over the last 25 years.

Complicated.

The problem with all these discussions is everyone picks the timeframe that suits their position. Twenty-five years ago gold was at a generational low. I can equally point out that gold hasn’t even tripled since hitting $850 in January 1980. The period between 1980 and 1999 was not good for gold and that period also saw lots of inflation, though not as bad as the 1970s. Maybe gold is a store of value over long periods, but it can also be out of favor for decades at a time.

That’s not why people should hold gold. It’s an insurance policy, chugs along quietly, maintains its purchasing power and you have it fall back on for a rainy day. Imo it should be an important part of one’s portfolio. Equities for dividends while the going is good.

Agreed.

Agreed. (see name above).

I actually find the current government’s selectivity of city housing infrastructure funding and pushing provinces to rubberstamp 4plex approvals over riding municipal councils to be embarrassing. It’s obvious that this is a desperate last ditch effort to try and lure private credit into pumping up the housing market. The infrastructure funding is their ideological preference of greater population density. Currently this government is not the least bit interested in letting the market correct its self – I believe on April 16th this will be made oh so sadly evident yet again (in addition to the billions this long in the tooth government has thrown at the housing market).

I am not sure what you are trying to say here. The Feds are trying to override the municipal and provincial nimby’s that are driving up housing prices by creating artificial bureaucratic hurdles that are preventing the market from solving the housing shortage with increased production of housing. This is a good thing, and will lead to lower prices (by shifting the supply curve), not higher prices, if it is successful

We don’t have enough trades and developers to produce a large scale housing boom. The government knows this. The government also knows developers build to market conditions and not policy decisions. Rubber stamping 4 plexes doesn’t improve market conditions. Labor and materials are still as expensive as ever. The government also pushes for this while simultaneously announcing a renters bill of rights – sure to attract investors (landlords). Doug Ford likely made the right decision in referring the decision to approve 4plexes to municipal councils. Let the people who live locally have the say of approval/disapproval. Nimby’s aren’t driving up housing prices – access to increasing mortgage credit (low interest rates), windfall equity gains from housing price inflation, and recently, considerable population growth juicing demand – are driving up housing prices; nothing to do with nimby’s.

Wow, the laws of supply and demand have been repealed, restrictions on supply don’t impact prices. Time to re-write the economics textbooks from the ground up, lol.

But don’t take my word for it, or even the basic common sense of econ101 supply and demand curves, people have done study after study in place after place. If you loosen zoning requirements, more gets built and prices are lower (vs. the counterfactual of not loosening zoning requirements).

Putting immigration to the side, development based on higher population density is better for the the long-run economy, society, and the environment, so more power to them.

Baffling to see literate people believe that government’s attempts to increase housing supply is “a last ditch effort to pump up the housing market.”

If the government’s goal was “pumping the housing market” then easily done: outlaw all housing construction.

I meant “pumping up the market” as in increase the volume of builds. Trying to support population growth with the public subsidizing some of it has gotten expensive in a hurry. The CMHC already stated that over 3 million more units are needed on top of what is forecasted to be constructed. The federal government has started a program to purchase up to $30 billion in Canadian mortgage bonds annually (where there previously was no program). The narrative of a housing crisis due to a mass housing shortage is quite misleading – there’s thousands of listings on CREA. There is however a major affordability issue due to a housing price bubble. Existing homes depreciate in price more and quicker than new builds; developers are only willing to build so small and have limits to cheaper materials. We’ll much more likely to drink ourselves sober then we are to over build the market to such an extent that we deflate prices. We’ll know better on the 16th – I’m expecting the government to roll out the red carpet for 1st time home buyers, for them to gain access to more mortgage credit in order to afford today’s overly inflated prices.

Just read a blurb about Jamie D at JPM saying he’s worried about potential risk or shock from QT, on a scale that’s never been done before.

I’m not sure what he said about the scale of QE.

Nonetheless, that comment makes me think about the pandemic shock and the resilient adjustments to inflation and the likelihood that there isn’t a good understanding of how higher prices for longer, will impact growth.

Here’s an interesting thought from some ridiculous ancient paper about GDP growth and oil, but I’m thinking in terms of how people will cut back spending with higher prices. Will QT play a role here?

“9

The channel through which oil shocks retard economic growth should make it clear that it

is the change in oil prices, rather than the level of oil prices, that affects economic output.

Once an economy has adjusted to an increase in oil prices, high oil prices have no effect on

its ability to grow from that point forward. The permanent effect for oil consuming nations

such as the U.S. is that the nation’s income purchases fewer goods and services henceforth.”

Very good stats and also great comments by Scrappy.

Canada’s latest jobs report was also pretty low compared to US. Plus, housing asking prices are starting to finally be noticed dropping. The Fed Govt funding for 4 plexes is a good news story for housing, but then that also depends on NIMBY and where one lives? It will certainly build out more rental accommodations. Add in the new restrictions on foreign students for Cdn universities, maybe this ship is starting to slow down and turn. This week a Vancouver Island uni put out a notice of phasing out some programs, interestingly enough GIS sytem degrees and advanced GIS degrees…as they had very very low enrollment and most likely were propped up with foreign student enrollment and other more popular offerings.

As for our interest rates, it always depends on what the US does. If ours stay higher per then our dollar will climb and exports of goods and services will suffer. When you live next to an elephant your health is impacted if they turn over and flail about.

A good news add on to the article is our BC Provincial govt restricting Air B&B type short terms in cities above 5,000 population. They now can only be offered in the owners own homes, so that source of housing is being redirected into the rental market. Maybe motels and hotels will stick around yet, and not have to be repurposed to house the homeless which has been done all over the place the last 5-7 years. Furthermore, also in BC, a RE flipping tax of 20% has been instigated for anything sold in less than one year after purchase, sliding lower thereafter, of course exceptions/exemptions for job loss, deaths, divorce, etc. Speculators only will be hit with the 20% new tax.

Wading through our news the greatest source of irritation seems to be inflation of grocery prices, in particular at Loblaws (our major monopoly chain). Gas is $2.00 per litre here, but mostly it is shrug and bear it. People will drive less and slow down for awhile, but I suspect the tourist hordes will still arrive in every location.

The hate of Trudeau and his Govt is palpable. Hell, we hate him in our house, but then you look at the alternatives and just wish he would step down already. Anyway, anti Trudeau sentiment is clouding some of the positive changes that are being instigated, or as I like to call him, PM Namby Pamby. Hopefully he’ll pack it in.

Regards

Loblaw’s is the punching bag for the high-cost of-food complainers. But they have always been 30 to 50% higher on prices. A simple solution is to just go across the street and pay about a third less. You’ll find a 4.50 item is maybe 3 bucks or so, and that pricing pattern holds for most goods.

Just seeing people leave Loblaw’s with full shopping carts having probably spent an extra 50 bucks and complain about high prices reveals that a lot of people don’t bother to check prices, typical for the last two generations.

In fairness to Loblaw’s, the reason for the high prices is that they carry all sorts of specialty items like fresh pastries, sweets, and custom hot menu items that add significantly to the overhead.

Overall of course, the money-printing mania of the past few years hasn’t helped – generally food prices are up 40 to 50% and shrinkflation is rampant.

Definitely good to be selective and avoid impulse buys if money is tight but that was always the case. Obviously eating out has gone up by quite a bit but honestly don’t feel overwhelmed by grocery start prices, at least out in California. Milk is $5 a gallon and often on sale as well as eggs, potatoes and other similar staples reasonable. Even meat isn’t super expensive if you shop the sales. At least in the States of you aren’t using rewards programs and app then you are simply throwing money away.

Going across the street does not guarantee competition. Grocery stores flying different banners are owned by a few, e.g. in B.C., Quality Foods, Save On and Buy Low are all owened by Patterson.

If prices are 1/3rd less across the street or maybe a little further away, that is the definition of competition. Even Loblaw’s owns No Frills, perfectly fine, same brand name stuff (even many Loblaw’s house brands), no fancy premium priced delicacies, the environment differs (plainer), and the prices are significantly less.

I said ‘across the street’ because we are fortunate to have several competing stores within walking distance. Some may not be so fortunate, especially in smaller communities.

Do the stores you mention charge the same or similar prices? Their names suggest not.

Also, 90% of what I buy is sale price – I buy ahead, and in the case of meat, I freeze it. Of course, ‘sale’ price today is what normal retail price was a couple of years ago before the Great Inflation.

Loblaws is much cheaper than the main grocery chain alternatives of Sobey’s, Safeway, and Save On Foods, where prices are upwards of 40% more.

That only leaves Walmart and Costco – whose prices are often very comparable to Loblaw’s.

Thank you Wolf for reporting on Canada always enjoy your work. Do you have any thoughts on Canadian vs. US in terms of inflation? US seems to be in a far better position economically with most mortgages 30Y while in Canada we have a ton of variable & 5-10Y fixed. More pain economically. BoC really shouldn’t cut before the US FED otherwise we could see significant devaluation of the currency wrt to USD?

I made a comment in the past to you Wolf concerning Canada’s economy front running America’s economy on a downward trend of shrinking employment and a slow down of gdp. I was also wondering if the central bank’s “newer” dual mandate could play a role in the not so far off future – as in, using increasing unemployment to try and justify letting inflation run at elevated levels or at least risk inflation coming back at higher levels. I know the BOC won’t butcher the loonie but I can’t help but question if there’s more of a set in excuse to try and justify higher inflation and risk in the name of this dual mandate (full employment)?

James Nicoll,

See my comment above.

Wolf, Have you been watching the USD/JPY pair? Appear to be breaking above the 152 line in the sand set by BOJ. Could have significant repercussions for markets. Could be quite a story.

The BOJ is going to have to do QT and hike rates to defend the yen — this intervention stuff doesn’t cut it. A few months ago, they too thought the US would cut a lot, but now that’s in doubt, and the onus is on the BOJ to defend the yen. There’s already talk they might hike sooner, and they’re probably going to start QT pretty soon. The yen is forcing them to rethink their policy stance.

Liabilities can go down as well, CB just need to increase purchasing power of a currency. After that banks’ liabilities and government ‘s account will go down, and there is less need of physical currency and can be destroyed.

Thus assets can go much more lower!

But, as you correctly “assume”, the destruction of purchasing power of currencies will go on and on [QE, GOV debt increase].. Therefore, there is a limit on how deep the assets can go down.