Treasury QT will naturally slow in June 2025 when the Fed runs out of T-bills. Fed governors have teased us with interesting options.

By Wolf Richter for WOLF STREET.

The Fed has started laying out some basic principles about how QT might evolve in the future. So far, the Fed’s QT has shed $1.43 trillion in assets, including 1.14 trillion in Treasury securities. So it’s time to look at how the Fed’s Treasury holdings will mature over the next few years, because that determines the maximum possible pace of the QT roll-off since the Fed does not sell them outright.

As the pile of Treasury securities on its balance sheet shrinks – currently down to $4.63 trillion – fewer securities will mature each month. We can see where this is going because the New York Fed posts the Fed’s portfolio of securities online, including purchase price, CUSIP numbers, and maturity dates.

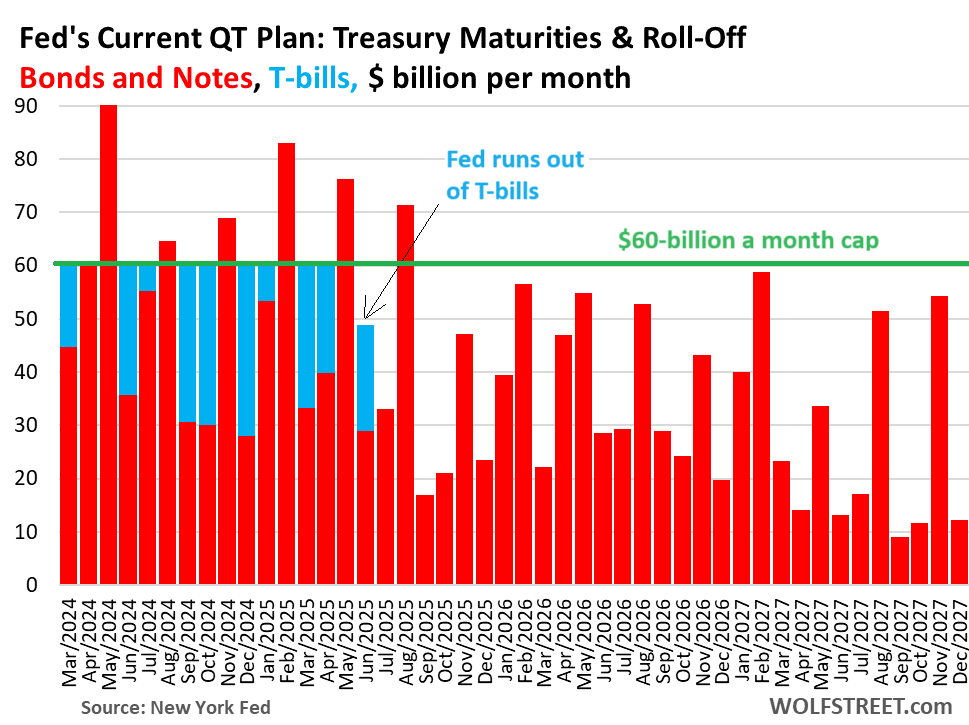

The current QT Plan. When it designed its QT plan in 2022, the Fed capped the maximum Treasury roll-off at $60 billion per month. Here is the visual depiction of the amounts in Treasury notes and bonds that will mature every month going forward (red columns), the $60-billion cap (green horizontal line), and the use of T-bills to get to the $60 billion cap until the Fed runs out of T-bills (blue bars), based on the current QT plan.

Making up the shortage to the $60-billion cap. When fewer than $60 billion in Treasury notes (2 to 10 years) and bonds (20 and 30 years) mature in one month, the Fed makes up the difference by letting some of its Treasury bills (1-12 months) roll off to get to the $60 billion cap.

For example, this month, $45 billion in notes and bonds will mature (first red column in the chart above), which is below the $60-billion cap (green line), and the Fed will let about $15 billion in T-bills roll off (first blue column) to bring the total roll-off to $60 billion.

In April, about $60 billion in notes and bonds mature and roll off. The Fed will not use any T-bills because the roll-off is already at the cap.

In May, $90 billion in notes and bonds mature. The Fed will let $60 billion roll off, and it will replace the other $30 billion that matured with new securities that it buys at auction. It will not use any T-bills.

QT will naturally slow in June 2025 because the Fed will run out of T-bills, as indicated in the chart above, and it will have no more T-bills to fill the gap to the cap, and the amounts of maturing notes and bonds left in the declining pile also decline.

The Fed has $209 billion in T-bills left, down from $326 billion at the beginning of QT in June 2022. It used $117 billion of T-bills so far to make up the shortages in months when fewer than $60 billion in notes and bonds matured. We discussed the details here last week, under the subheading, “How Treasury bills fit into QT.”

The first months when the Treasury roll-off will be substantially below the cap will be June 2025 ($48 billion maturing), which is the month the Fed runs out of T-bills, and July 2025 ($33 billion maturing).

August 2025 ($71 billion maturing) is the last month when the Treasury maturities exceed $60 billion, as we saw in the chart above.

After August 2025, maturities will be below $60 billion every month, and over time, they’re shrinking further as the pile of Treasuries shrinks.

- H2 2025: maturities average $36 billion per month.

- H1 2026: maturities average $41 billion per month.

- H2 2026: maturities average $33 billion per month.

- H1 2027: maturities average $30 billion per month.

- H2 2027: maturities average $26 billion per month.

Only 6 months left with maturities over the cap. When more than $60 billion in notes and bonds mature in a month, the Fed lets $60 billion “roll off,” and replaces the overage by buying notes and bonds at auction in the amount of the overage.

As the chart above shows, there are only six months left going forward when this occurs (amount of overage):

- May 2024 ($30 billion)

- Aug 2024 ($5 billion)

- Nov 2024 ($9 billion)

- Feb 2025 ($23 billion)

- May 2025 ($16 billion)

- Aug 2025 ($11 billion).

The future plan for QT and the balance sheet.

Fed governors Christopher Waller and Lorie Logan have come out to tease us with some ideas when and how the pace of QT might slow to avoid an “accident” that would stop QT prematurely. A QT accident occurred in late 2019 when the repo market blew out. The Fed has two tools to avoid a QT “accident”:

- In July 2021, before QT was even announced, the Fed already implemented the first tool by reviving the Standing Repo Facility, which it had always had until it killed it in 2009 amid QE.

- The second tool will be to slow down the pace of QT. Details will be forthcoming sometime in the future.

So as we see, the pace of Treasury QT will naturally slow down, starting in June 2025. If the Fed lowers the cap before then, the slowdown would begin earlier.

Waller laid out the idea of replacing maturing longer-term Treasury securities with T-bills because the Fed used to hold a much larger share of T-bills compared to the rest of its balance sheet. Starting in 2009, the balance sheet has veered into the opposite direction. Currently, the Fed holds only $209 billion in T-bills but $4.63 trillion in Treasury notes and bonds. Waller said he would like to see the share of T-bills start reverting toward a normal level, which would lead to a much a much faster roll-off of notes and bonds.

Under a new QT plan, the Fed could start this process during QT, replacing the overage in notes and bonds over the cap with T-bills. The cap is now $60 billion, but under a new plan, the Fed might reduce it, maybe to $30 billion. And then there would be more months with overages, and those overages of notes and bonds could be replaced with T-bills. So we’re eagerly awaiting more details on this idea.

Waller also said that he would like to see MBS go to zero on the balance sheet, so let them run off even after QT ends and replace them with Treasuries – which is what the Fed did from the end of QT-1 in the summer of 2019 until March 2020. The likely replacement would be T-bills given the urge to get the share of T-bills back up toward where it used to be before 2008. We can’t wait to see the details.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The Fed is always over confident about what it can achieve.

In terms of QT, the Fed has already achieved a lot more than most people thought it ever could. Lots of people out there thought that the Fed would HAVE to veer to QE within months of starting QT. And $1.4 trillion later, QT is still clicking along.

The Fed could literally cure cancer and invent sustainable fusion power, and the naysayers would complain that it wrecked the healthcare and energy industries.

The ghost of zirp back from the grave to defend its creators.

Reminds me of the frankenstein creation, and then having to destroy it after it runs wild.

Remove free money from circulation doesn’t sound very hard to do. It is not rocket science. All it takes is some backbone to say no to politicians.

Thats a case of Stockholm syndrome if i have ever seen it

The people who rightfully hated the Fed for doing QE and 0% are now hating the Fed for doing QT and 5.5%?

LOL!!!!

Right, a bunch of eCONomists are going to cure cancer or develop and build a fusion reactor.

The fed “creates” DEBT out of NOTHING. This is literally done with the click of a keyboard other invest real work, real energy to develop and build the very real life changing things you mention. Give me a break. The Fed and the entire financial/political class has been behaving BADLY without consequence. It’s high time that ENDED.

The Fed had ONE job, not to F-up TRUE PRICE DISCOVER.

There’s reason eCONomics is a social “science”.

LMFAO!!!

The Fed has other jobs, too, which is to keep the economy relatively stable. Inflation is a problem but letting the GFC become Great Depression 2.0 would have been worse, as would have letting the pandemic free-fall continue to the same.

The Fed avoided those! They deserve kudos for those successes. Don’t discount what didn’t happen. The inflation problem is big but small in comparison.

Now they’re dealing with inflation, fairly successfully so far. The job’s not done but on the right track.

Their biggest mistake, IMO, was not seeing that inflation was inevitable and ending their aid programs sooner to avoid or reduce the inflation to come. QE was a new tool they didn’t fully understand and invalidated much of the history they were using to guide them. Understandable but still unfortunate. Still, only hindsight is perfect.

So open your eyes and look at the reasons behind their choices. They were made to save us from worse problems, not because of incompetence or nefarious purposes.

I

know it does not matter but from.my perspective fed had been an utter failure when it comes to price stability and especially of housing locking millions of young people out of homes hecause of affordability.

Praising fed is like praising a habitual big arsonist who is trying to douse a fire in a small building after burning down lot of buildings over the years.

I know you vociferously hate the Fed because it’s doing QT and 5.5%. You’ve been spewing Fed-hater stuff for a year, but when it was doing QE and 0%, you were quiet about the Fed. Don’t be ashamed of it, admit it LOL

You got Me wrong WR.

I hate fed for their policies which helped the rich and increased the wealth inequality.

I hate the fed for locking millions of young people out of basic necessities of life ie hosting

I hate fed for their love to brown nose to rich and elites.

I know and am surprised to see your new found love for fed based on qt and 5.5 percent which is commendable but I am looking at the bigger picture.

As always you lose the forest for trees.

The Fed has been doing the opposite of what you claim for the past 18 months by imposing record QT and the highest rates in decades. If you hated the Fed for QE and 0%, you should acknowledge that the Fed is now doing QT and 5.5% against an army of people who said that the Fed could never do that. You’re a manipulative QE monger, but you’re going at it from behind. You loved QE and want it back, and you now hate the Fed for doing QT and 5.5%. A year’s worth of comments document that.

@WR… please dig out comments where I said I love qe. I think you have mistaken me for some one else.

Although I have been big beneficiary of feds qe but I hate fed doing qe for their friends and families.

Wolf, I don’t hate QT and certainly don’t want QE back. But the fact that Bitcoin is at $70k and Nvidia is back up 6% today shows that what the Fed is doing is NOT WORKING.

What they should do is immediately sell $3 trillion off their balance sheet, in the same month period that it took them to “purchase” those assets in 2020. That will cause the S&P and housing prices to drop by 50% in a matter of weeks, and Bitcoin to drop probably by 80%. That’s what they need to do. Anything less is insufficient.

I for one believe, the Fed is doing a masterful job. i have stated this many times. The Fed has a dual mandate. Price stability across the board and full employment. that is the mandate. they do not have a mandate to control specific asset prices such as housing as one example. You can blame the congress for not having a third mandate, you can blame the congress for the employment mandate which made the Fed’s job even harder, but I would be cautious about blaming the Fed for the masterful way they have been navigating the messes created by others. Time to review the financial crisis pre Fed 1913 to get a flavor for it all.

What about their “price stability” mandate has been masterful?

Housing price stability is a form of price stability, no?

Einhal,

I stopped caring about the price of crypto ages ago and am much happier for it. Crypto price quotes are akin to guys in a bar on the moon bidding up the price of coasters and broadcasting it in times square. Safest to just ignore it.

Tom S., except to the extent that these asset prices cause “wealth effect” inflation that the Fed then decides must become the new floor, because oh noes DEFLATION! Worse than nuclear holocaust and cancer, all in one.

Why is the Fed so reluctant to sell some of its notes and bonds and retire the cash received on sale, as compared with just letting the bonds and notes run off? Is there a qualitative difference to the effects on liquidity between the “let them run off” approach and just selling the notes and bonds. We are lead to believe that when bonds are allowed to “run off” the equivalent cash that was used to acquire them in the first place (the printed money) is retired (to maintain balance). How does this actually happen? That cash is in the economy. How do we know that it does happen? I apologise if my questions display a level of misunderstanding.

I basically don’t understand how letting bonds “run off “ reduces liquidity which is the stated aim of QT

“I basically don’t understand how letting bonds “run off “ reduces liquidity which is the stated aim of QT”

That’s fine. You don’t need to understand everything. The first step to understanding is that you want to understand, and then read my Fed articles.

Well, if one were to have predicted the commupance for the bankrupt banking system before the invention of QE,

Since QE, they seemed to have ended up at the top of the pile as a direct result of Federal Reserve Policy.

I would suggest that you, James, really don’t know the Fed at all.

They have far exceeded their own expectations, and not necessarily in a good way.

“Waller also said that he would like to see MBS go to zero on the balance sheet, so let them run off even after QT ends and replace them with Treasuries”

Getting MBS to zero is going to be a monumental feat. That old avg timeframe of 7 years for mortgages to be paid off via sales is easily going to double. MBS QT has since its inception been rolling off below projections, and this will only worsen. I’d love to see the Fed come out with a REAL projection of how long it expects it to take for MBS to “go to zero” along with a prediction of how likely it is that they start buying MBS again during that timeframe. My swag is at least 15 years for MBS to go to zero and a 100% probability that the Fed buys more MBS during that timeframe.

Why would the Fed replace MBS with treasuries as the MBS mature?

When passthrough principal payments reduce the mortgages in a mortgage pool below a certain level, the issuer calls the MBS at face value and repackages the remaining mortgages into a new pool and MBS. That’s another way in which MBS come off the balance sheet, and it kicks in some years after issuance. So I doubt it will take nearly as long as you suspect to get rid of the MBS.

The Federal Reserve owns $2.4 trillion of MBS per Federal Reserve St. Louis data. The Federal Reserve is rolling off a maximum of $35 billion in MBS. Our banker friends don’t use much math considering that negative numbers aren’t even used in accounting (that is why the Federal Reserve thinks it magically creates money with no repercussions). However, they should have learned division. $2.4 trillion is $2,400 billion divided by $35 billion rounds up to 69 months or almost 6 years. If that slows it could be 10+ years easy.

Except there is no need for them to slow the MBS drawdown. With rare exception they haven’t been able to hit the $35 billion target in any month since QT 2022 started. In fact, the whole point of setting the level of rolloff so high was to get them out of the MBS market for good. It has now been two years since they increased their MBS holdings at all… and eighteen months since they bought any.

Moreover, the MBS level is not likely to precipitate any problems for the Fed going forward. Certainly not enough to justify stopping the QT program the way that they had to in 2019. Curiously… even when they stopped the QT program then (due to the Repo market seizing up)… the Fed did NOT stop the rolloff of Mortgage Backed Securities. Those continued right up to the COVID panic QE of February 2020.

What is most likely to happen is that the MBS rolloff continues slowly ($35 billion per month or less) until something happens where it picks up speed (home sales/refinancings). At that point an assessment will be made by the Fed as to whether to continue with the $35 billion level (by entering the market to buy small amounts of MBS) or to let it run off naturally. Rather than a six year process getting stretched to ten years it is likely to be done in five years or less. The Fed has even spoken of selling off its MBS portfolio outright at some point (although that would be hard to do at current levels and interest rates).

Read more here: https://wolfstreet.com/2022/09/16/the-fed-stopped-buying-mbs-today/

Just curious, what is the “certain level” usually? 20% of the original value?

So there’s a pre-set date after which the MBS can be called, and when the mortgage pool has fallen enough, the MBS will be called. I don’t know what “enough” is in terms of %. Here is from Fannie Mae:

“When a Fannie Mae callable debt issue has reached its call or redemption date, Fannie Mae can call the issue in whole or in part. Fannie Mae generally calls its securities issues in whole.

“In the case of an issue that is callable at Fannie Mae’s option, when Fannie Mae determines that the issue should be called, Fannie Mae gives notice in the manner set forth in the terms of the securities…”

>>When passthrough principal payments reduce the mortgages in a mortgage pool below a certain level, the issuer calls the MBS at face value and repackages the remaining mortgages into a new pool and MBS.

This is incredibly important to know. Thanks, Wolf. Good stuff.

Hi Wolf,

Do you have a view on the overall liquidity situation in the US or globally i.e. still Positive/Negative etc. ? Are Markets still being moved mostly by the incoming or remaining liquidity ? Thank you

The world is still awash in liquidity.

No one ever knows what moves markets, but markets move a lot in every direction, and everyone has their own theory why.

What you said, ” The world is still awash in liquidity.”

reminds me that Saint Patrick’s Day is a week away, time to start thinking of how too spout off my mouth. One thing came too mind:

A happy man, often, has good relations with his family.

You can call it liquidity, I prefer to call it WEALTH INEQUALITY.

But it’s secondary (unless you live in a place like Gaza, where the world’s largest open air prison has become the world’s largest open air torture chamber) to how hot 2024 appears to be getting, and the Planetary consequences of our collective stupidity.

(Although, I still wonder what the rich will try to do with the rest of us.)

I need to hang a brown cardboard sign on me and hang out on a street corner. Grow what hair I can.

Complete tripe. Every market move is predictable.

🤣❤️

I know this question is for Wolf but for more info on liquidity in the US Lyn Alden publishes some decent work on that with charts showing the recent reduction from monetary policy and increase from fiscal policy for a net increase in liquidity. I know Wolf has talked about this as well but I can’t think of a specific article I’ve read to link off the top of my head, maybe someone else can.

Seba,

Fiscal policy doesn’t increase liquidity because the government has to collect in taxes or borrow what it spends, so it only shifts liquidity around. But fiscal policy stimulates spending in the economy, and therefor stimulates inflation — and thereby it’s on collision course with monetary policy.

Good news, the Fed will cut short-term rates at their May meeting.

Bad news, the S&P will be at 1,100.

The Black Swan in this cycle is political, on the matter of legitimacy.

Good luck, frens.

A black swan is something that it sudden and unexpected. This election cycle well defined and easily understood.

A black swan would be life insurers getting into trouble because they carry way too many unsecuritized real estate loans. There is an unackowledged domino situation waiting to happen there.

it’s not unexpected, it’s unpredictable – in NNT’s own words.

Predicting black swans is a contradiction in terms.

People don’t know what a black swan is. I denigrated Nassim Nicholas Taleb’s “Black Swan” theory (unforeseeable event) on May 6th, 2010 and October 15th, 2014, 6 months in advance and within one day.

Well, I will step up and buy the S and P at 1100 seeing as it currently selling for somewhere around 5110. The financial apocalypse that you fear actually has a probability projection that would put that kind of 6 sigma move in perspective. On the order of another asteroid striking the earth.

Lol 1,100. So many stock predictions on here the last year have been proven wrong so many times. Have fun shorting and losing money like lots have.

The obvious question: Why not sell securities when maturing securities aren’t sufficient to reach the cap?

When the Fed leaves monetary stimulus in place for too long, it becomes embedded and it cannot be removed without a blow-up. The Fed is forced to end QT early and the balance sheet normalizes at a much higher level after each stimulus event. The Fed’s balance sheet already evidences this step pattern.

The real hazard is taking out monetary stimulus too gradually, particularly when there is little evidence of “blow-ups” on the horizon.

Am I alone in this thinking?

If the Fed waged a stronger fight against inflation, would markets be bidding up inflation-protected assets (stocks, RE, gold, Bitcoin, etc.), pouring more gas on the fire and elevating financial risks?

After a decade or two of money printing and interest rate repression, the burden of proof is on the Fed to show it has enough conviction to fight inflation. The pandemic was over two years ago, and inflation is still way above target and threatening to move higher. The Fed never should have promised 2% average inflation if it didn’t have the conviction to achieve it.

Show me.

I always wonder why older tools weren’t used, admittedly all have their pros and cons. When WW II started it was recognized that because much of America’s resources would go into the war machines that shortages would exist and so of course inflation would exist and likely divide the country. A divided country is especially bad during war so wage freeze and price control policies were implemented. Some of our inflation was real in terms of supply chain issues which were written off as falsely temporary but often was simply exploitation by corporations. Some of these could have been controlled, especially in an era of computers today. Of course neither party wants to interfere with neoliberalism and perhaps it would have been the wrong choice but seemed like not even discussed.

Bobber,

Withdrawing liquidity too fast is very risky because liquidity doesn’t flow where it needs to go in a predictable smooth manner. Yields accomplish that: when liquidity gets tight in a corner, yields rise in that corner and then eventually liquidity starts flowing to that corner from the corners of excess liquidity. But it takes time. And when the liquidity doesn’t flow quickly enough into that corner, something blows up, and QT ends.

So people who want to speed up QT actually want an “accident” to happen so that the Fed will instantly stop QT and revert to QE.

The way the Fed can reduce its balance sheet by the most is to do it slowly without blowing anything up.

We’ll have to disagree on that. I want QT to speed up because I think the bloated money supply is artificially propping up asset prices, which is a problem in itself. It creates unnecessary arbitrary wealth transfers and sows societal division. On top of that problem, the asset inflation feeds back into consumer price inflation via the wealth effect, which rubs salt into the societal wound and creates an inflation cycle.

I know I’m not alone in that thinking.

I don’t want the economy to blow-up, but I would like to see asset prices revert to a sustainable level. That won’t happen if the Fed comes to the rescue with stimulus every time the stock market stubs its toe. It also won’t happen if the Fed prolongs its inflation fight in hopes of finding a “soft-landing”. What good is a soft landing if most of the people in the aircraft have lost their oxygen due to inflation.

“The way the Fed can reduce its balance sheet by the most is to do it slowly without blowing anything up.”

I hate to say it but things are ALREADY blowing up for the average American consumer, including myself. Went to the grocery store the other day to buy my 15 items that I get every week. 2 were out of stock. The other three were produce items of such poor quality that I had to make another trip to a high end grocery chain that has prices 30 to 50% higher. Giant Food which has been in business here in the DC metro area for over 75 years has lowered their food quality to the point where they have turned into another junk food distribution center like Safeway. Going to a high end grocery chain with decent quality healthy food is the only solution. Rich people shop there. Put that 30% to 50% surcharge for eatable food into the bogus inflation numbers put out every month and you get the real picture of what’s happening out there. Worse yet, what kind of country is this where rich people get to eat good quality food and poor and lower middle class eat junk food and have higher health issues as a result.

@Swamp Creature,

I have noticed this, also. Perishables at the grocery store like milk and produce are going bad within days, if not already bad once you start cutting into them. Quality is dead. No one cares.

For people talking about food prices, there are still lots of healthy foods, available at Walmart, that you can live off of, and are so cheap you effectively get paid to eat them, such as oatmeal, rice, beans, cabbage, carrots, bananas, roma tomatoes, potatoes, peanuts. Apples and oranges aren’t too pricey either.

“Of course neither party wants to interfere with neoliberalism”

Hey Glen, neo-liberalism died in 2008. It has been replaced by neo-communism, which I believe you have an affinity for, and which has been in conflict with neo-fascism since 2016. The 40%+ of us in the middle wish for the days of neo-liberalism. Heck, I’d eat my hat for a few years of some classic liberalism.

I’d consider my hat food if you read the basics of Marx and avoid assigning labels at random.

Well it’s a bit of a soft science, so labels are somewhat in the eye of the beholder. But I disagree that either party adhere to neo-liberalism anymore.

…you gotta wonder. Recall reading that back in the GD of the 1930’s, polling of the time (as much as one can ever rely on them) pronounced prox. 25% of the ‘Murican populace favored the Soviet methods of running things and prox. 25% those of the Third Reich (…the more things change?)…

may we all find a better day.

I think the Fed appears, for the time being, to be employing a sophisticated monetary strategy that is attempting to thread the needle of the transition from the distortions created by QE to a more egalitarian posture.

‘I think the Fed appears, for the time being’

Exactly, it’s all a play on ‘time’. But one tool the fed doesn’t have, is a crystal ball.

They are entrenching inflation at the expense of the working class and poor. They are stealing from them to give to the rich – a reverse-Robinhood scheme. The longer they take to get inflation back to 2% – it should be 0% – the worse the outcome for the less fortunate.

They have duped young people into voting progressive as if somehow their lies are truths. In reality, it’s all a scheme to make life so unaffordable that you exist on almost nothing. “You will own nothing and like it” is not a conspiracy theory, they actually said that out loud.

They have quickly stolen the ability of the young to afford shelter, new cars and a host of other things. And it’s never coming back. They will have you in a state of indentured servitude before long – their dream where the oligarchs live a life of opulence while you wander around trying to find some crumbs.

There was a class war. The wealthy won.

The FED doesn’t know that banks are credit creators, and not credit transmitters. So, Bernanke eliminated reserve requirements.

Dr. Daniel L. Thornton, May 12, 2022:

“However, on March 26, 2020, the Board of Governors reduced the reserve requirement on checkable deposits to zero. This action ended the Fed’s ability to control M1.”

Powell, not Bernanke.

Where does the issue of funding new deficit spending fit in? My understanding is that it is accumulating at about 1 trillion every 100 days. Does all of that just get issued in new treasuries? It seems that all of that deficit spending is on a collision course with the Feds objectives.

I feel like I am missing some basic economic concept here.

And a follow-up question, who is the buyer of this 1 trillion every 100 days? Who is the creditor? I cannot believe there is somewhere stashed such massive unallocated spare liquidity.

Vadim,

Investors are the buyers. I mean, who the heck would buy a 10-year Treasury with a 4.1% yield in this environment, but there is mindboggling demand for this stuff. A lot of people think that inflation will be below 2% for the next 10 years and that therefore this 4.1% Treasury will be a good deal. Maybe they’re right. But i just don’t see that.

I and many others have been asking that for well over a decade. The best response I got was from a wealth manager for some very rich folks, who looked surprised. He said it was simple. There are now a lot of folk with over $30MM in assets and at that point they don’t need to make money, losing a percent each year is fine. They don’t want to LOSE money, and don’t want to invest in anything which the government might attack for revenue. This stuff is stashed in trusts that somehow don’t pay taxes. Look to your rich 0.01% – they are buyers. They also got paid via QE and got richer.

Sorry for second reply, but I missed the other half of the comment on review. Lots of people are in 60/40 bond allocations or target date funds in their 401K / IRA so also don’t pay immediate taxes. Many don’t even know they are in some of these packages from Wall Street. 4.1% “tax deferred” which many don’t understand until RMDs bite sounds good in a volatile market.

I see Kirk Cousins is going to be playing for the Atlanta Falcons this season. He’s 35 years old, and is coming with a healing Achilles tendon tear.

He’s being paid a $180 million-dollar 4-year contract of which $100 million is guaranteed. I don’t see the mind-boggling demand for a 35-year-old injured QB at this price either.

Whatever…………

@observer – NFL raised their salary cap this year by 30 million ot 255 million.

13% increase. I guess that is the NFL inflation metric?

…you gotta wonder at this, viewed in conjunction with the movement to officially pay college athletes in their previously unpaid roles as members of ‘farm clubs’ for professional sports. Link this to greatly-expanded sports-betting and view a great deal of circulating coin doubtlessly attracting interest, legit and nefarious…

may we all find a better day.

I heard an interesting theory/explanation for why there’s so much demand for the 10-year @ just above 4%:

Unlike corporate bonds, there’s no credit risk with US Treasury debt. If you buy the 10-year note & hold to maturity, you are guaranteed to not lose money (in nominal terms). Yes the duration presents inflation risk, but this would also be true with a 10-year corporate bond.

Buying the 10-year at current rates is a bet on future interest rates – i.e. these buyers think that rates will be lower at some point over the next 10 years.

Currently the ‘valley’ in the yield curve is right around the 5-year mark; ergo, after 5-years, bond buyers want /increased/ compensation for duration. But for maturities sooner than that, the compensation /decreases/ as duration increases, presumably because more duration = more likelihood rates will fall.

NB: bond funds like TLT are 100% a bet on rates, but at least owning the actual note/bond itself gives you the benefit of pull to par.

Glen,

“I feel like I am missing some basic economic concept here.”

Yes. The Treasury sells this massive amount of debt every week at auctions, and investors are grabbing this stuff hand-over-fist — including all the stuff that the Fed used to grab under QE but is now walking away from. The relatively low yields on longer-term Treasuries document just how much demand there is for this stuff.

Thanks. That makes sense now as the Fed is walking away from its purchasing but still significant auctions in general.

I am one of those who had to take all the econ classes and was confused when common sense explanations would have made it clear. Not unlike lawyers I suppose whom are needed to solve what should be common sense disputes! It’s almost as if econ jargon was created for job security.

Definitely waiting for those longer term yields to rise but for now sticking with 17 week and shorter with auto reinvest.

Glen,

Amen, brother. I’m: 1) confused as to how long-term Treasury rates can be so low and how long it can last, and 2) sticking with Treasury bills of 4 to 13 week maturity. For the time being (while asset markets are so overvalued) I’ll take a risk-free return of 5.5% (with no state income tax). My interest income after federal tax may even be keeping up with inflation at this point. Hallelujah!

Only in economics can everything be overcomplicated. It could actually be very simple really, as free markets kind of are. But if they don’t complicate it, they can’t get away with it.

Blake,

True. The question as well is do free markets exist and if so is it the best system? Look at Mexico City as an example for which is running out of water. Guess which people have flowing water and which do not.

Well don’t lose any sleep over the perspective victim the Fed with a responsibility that is infected by the political influence they always claim to adhere to, wink, wink.

Yep.

Your right. The FED is going to remove capital requirements for T-Bills.

ISDA is recommending a permanent exemption of Treasuries from Basel III leverage calculations.

Oh my, what could possibly go wrong…

“Full FAITH and credit” as it were.

This is really the minsky moment here if that isda rec gets imp.

> some ppl at fed telgraphing desire to drain market of bill liq

> no public access to real time infomation on risk at ccps

> permanent exemp for us gov sh*t coin denom ious from leverage ratios

“In May, $90 billion in notes and bonds mature. The Fed will let $60 billion roll off, and it will replace the other $30 billion that matured with new securities that it buys at auction. It will not use any T-bills.”

Does the $30mm they buy at auction reflect the same maturity structure as the total roll off from that month? I.e. with the $90mm rolloff, they buy 1/3rd the amount of each maturity that rolled off to get to the $30mm replacement?

Or is the replacement skewed some other way?

The May maturities are:

CUSIP 91282CCC3: 3-yr $39.5B (44% of $90B))

CUSIP 912828WJ5: 10-yr $7.5B (8.3% of $90B)

CUSIP 912828XT2: 7-yr $36.1B (40% of $90B)

CUSIP 91282CER8: 2-yr $7.1B (7.8% of $90B)

The the replacement purchases of $30 billion should roughly be $13B in 3-yr notes (44% of $30B), $2.5B in 10-yr notes (8.3% of $30B), etc. etc.

Are you sure? This seems inconsistent with:

“Waller laid out the idea of replacing maturing longer-term Treasury securities with T-bills because the Fed used to hold a much larger share of T-bills compared to the rest of its balance sheet. “

I think Waller was talking about his preferred future policy whereas Wolf is assuming a continuation of current policy.

We’re on the current plan. QT runs on the current plan. The roll-off in May is under the current plan.

There is still no future plan. But Waller and Logan laid out some principles for a future plan.

We have seen some minor deviations from these guidelines in the past implementations. Given the longer time to roll off the 7-yr and 10-yrs, wouldn’t it make more sense to you (if you were on the Fed) to bias these replacements to shorter terms? Even a trifle billion or two might help.

I certainly would like to see no replacement at all, and if they have to be replaced, replace them with T-bills. The additional T-bills would then allow the fill-up to the cap to continue for a little longer.

But there are only 8 months left with excess maturities, and May is the biggest one, so it’s not a big deal one way or the other.

Thank you wolf.

Ya know the more I think about Waller’s idea of using bills to replace rolloffs above the cap, the more I think this makes a lot of sense. Hopefully this comes to fruition.

NB; $30mm should be $30B in my original comment.

Wolf, Do you see a problem with the variability of future run-offs if the cap is maintained at 60 after June 25.

This is the way the Bank of Canada and some other central banks are doing QT. They have no caps, and what matures rolls off. In Canada, the situation is now that no bond issues mature for a few months, and then a big one matures and rolls off. So we’ve got a big one coming April 1, after a small one in March, and after nothing over the prior months. And it seems to be working fine. I will cover the BoC’s balance sheet and that issue in early April, when the big roll-off is booked. There are economists that say that this is disruptive, that it draws too much liquidity out in a very concentrated time period. But it seems to work OK, knock on wood. The BoC also does repos to smoothen out sudden liquidity issues and control its policy rate.

Canada’s experience is a data point that shows that the peanut gallery screaming for faster QT (including me), may have been right all along. No caps means faster QT.

Wolf, could you please clarify these:

“In May, $90 billion in notes and bonds mature. The Fed will let $60 billion roll off, and it will replace the other $30 billion that matured with new securities that it buys at auction. It will not use any T-bills.”

“Only 6 months left with maturities over the cap. When more than $60 billion in notes and bonds mature in a month, the Fed lets $60 billion “roll off,” and replaces the overage by buying notes and bonds at auction in the amount of the overage.”

Is it reasonable to assume that the replacement securities here will be T-Bills, not notes or bonds? Or, does the FED policy explicitly say that the duration of replacement must match that of what is being replaced?

Yes, I guess, it is reasonable to assume that the Fed is likely too go off the rails, which is not the solution most beneficial to the median American citizen.

In addition to being highly unlikely. With similar odds too impossible.

I agree the impossible seems to occur too many times, all explained by the parameters of the normal distribution

I predict the Fed maintains the current interest rate profile until after the election.

“In May, $90 billion in notes and bonds mature. The Fed will let $60 billion roll off, and it will replace the other $30 billion that matured with new securities that it buys at auction.” Will the $30 billion of new securities that the Fed buys at auction be Treasury notes, bonds or bills?

See my comment about this above in reply to MM.

I never understood why there are two separate buckets for MBS and Treasuries, especially since MBS never seems to hit its cap. It would be simpler if the next phase sets a cap of, say, $50 billion per month of overall QT (MBS + Treasuries) with any excess from whatever source plowed back into T-bills…

I propose that the Fed has no business buying MBS and should rid their balance sheet of them, post haste. Although, I suspect they bought the worthless dregs with the plan being to allow them to expire.

“…bought the worthless dregs”

The Fed only has government-backed MBS on the balance sheet. If the underlying mortgages go bad, the taxpayer is on the hook, not the Fed.

When are taxpayers not on the hook? Apparently we do get the government we deserve…

It looks like QT naturally slowing around a $6T balance in June 2025, which would be close to the bare minimum possible of $5T Wolf has written about, anyway. Given that constraint, it doesn’t seem as though there will be a huge need for T-bills to continue current pace of QT at that time. (My estimates not exact, just expressing a general point.)

The treasury has an upcoming record issuance of fiscal debt that needs to be financed which the Treasury Secretary insinuated would be financed with expensive, short term debt. Eschewing the lower, long term rates that they expect to decline.

Yes. I think this is a ploy to keep the ten year yield low. You thought the yield curve was inverted now, just wait.

I see lots of posters insisting that the Fed start dumping as many assets as they can, immediately, at firesale prices.

Either they’re not reading the multitude of articles where Wolf says “fast QT crashes the economic system and forces the Fed to step in with QE, defeating the whole point of the QT”

Or they’ve read the articles, and they think Wolf is a clown who’s got it all wrong.

Either way, I wonder why they’re on this site? just to argue with the wind?

Not exactly, unless you favor communism and kleptocracy. I might suggest that the Fed has been the greatest enabler of bad behavior. in a real market, bad debt, bad management, and bad behavior should be allowed to FAIL. Case in point, the Fed NEVER should have bought MBS. I think Wolf agrees.

Yes, the Fed never should have bought MBS, and it should have never done QE (buying bonds). It should have stuck to repos to fix market issues and let the markets sort it out, which is how it used to do it before 2008.

That said, the question is: what to do NOW. So the Fed is answering the question correctly: unwind QE. But if it does that too quickly, something WILL blow up, and then the market issues start all over again.

That said, I think it could sell enough MBS to get to the $35 billion a month cap without running into a big problem. And it should do that, and it was talking about it over a year ago, but then the banks blew up a year ago, and that stopped that discussion.

shoulda, coulda, woulda, Wolf!

If “ifs” and “buts” were candy and nuts we would all have a merry Christmas!

The good new is, this time around, the behavior of all these narcissists in banking, finance, and politics has been well-documented. If only the French had such resources in 1780. Regardless, your optimism is appreciated, despite the fact that math and physics will have the last say because people are beginning to believe their “lying eyes”, and not just the peasants.

Howdy Lone Wolf. Really glad to read this post from you. Since 2008, some of those FED theft tools should never have been used…….Looking forward to CPI day and the DOT PLOT today because of Wolf Street.

THANKS

Financial Times – As Sheila Bair said: “It should replace the shock and awe of major interest rate hikes with new targets based on money supply, and aggressively shrink its portfolio, selling securities at a loss to do so, if necessary.”

The problem is that the FED doesn’t know how to measure AD.

Crashing the economic system doesn’t “force” the Fed to step in with QE. My desire is that the economic system crashes and it stays crashed until it can organically be fixed through growth, not “stimulus.”

The best thing to do is raise all the taxes on the poor and cut them for the rich. The poor have had it too good for too long. QE just tries to trick the penniless into thinking you can become very rich starting with nothing or less than nothing. Endless QT will teach the poverty stricken degenerates you will always stay poor.

like paint drying but i find it fascinating

Anxiously awaiting The Wolf Street CPI breakdown.

Howdy Steelers Fan. Ditto

Regarding CPI numbers, CNBC seems to be downplaying the numbers whereas Bloomberg says it reinforces Fed caution.

CNBC: The consumer price index, a broad measure of goods and services costs, increased 0.4% for the month and 3.2% from a year ago. The monthly measure was in line with expectations while the 12-month reading was slightly higher.

Bloomberg: US Core Inflation Tops Forecasts Again, Reinforcing Fed Caution

Howdy Sean Read your post, reminded me of that Circus Promoter who coined some great quotes.

CNBC always downplays inflation and then Wolf gives us, his less educated minions, the real story on CPI and PCE days. Its become a fun twice monthly tradition for me.

Yes, what would we do without Wolf to set things straight. The fact that there is only one person who tells it as it is without spin or propaganda is mind-boggling and very, very scary..!!

Howdy Folks The Lone Wolf puts out so many truths for me, that his love of EVs is AOK with me. HEE HEE

I don’t “love” EVs any more than I “love” ICE vehicles, and we don’t own an EV. But the propulsion method is the biggest thing that happened to the US auto industry in my lifetime, and it’s shaking up the legacy automakers whose management twiddled their thumbs for 10 years and cannot manage themselves out of a paper bag. What I cannot stand is when people abuse my site to spread lies and BS about EVs to “prevent mass adoption,” as an EV-hater commenter exhorted everyone to do. EVs have become politicized – though they just have a different and vastly more efficient propulsion technology. I have no idea what goes on in people’s brains when they post these anti-EV lies, but I no longer tolerate it. Zero tolerance for anti-EV lies and BS.

Yes, but I also find the market response interesting as well. Still just seems like tons of liquidity to go into everything so yields are low on treasuries and markets shrug it off. Nothing really on the horizon that will shake that it seems. Market has already priced in Congressional gridlock and likely inaction relative to the deficit. Will have to be something out of nowhere thats moves anything in my completely subjective opinion. One thing is clear is that a transition point of an unknown duration has arrived but impossible to put a timeline on it although likely a predictable US response.

All the talking heads say we are not in a big bubble yet. We are more like stocks in 1996 – 1997. We are mid innings of a bubble.

Even a very cautious Financial Advisor I follow who got out of stocks in 1998 and called the housing bubble in 2007 said he thinks we are like the 1997 time frame for dot.com stock prices. Enjoy the ride but don’t sell yet. Sell some calls on your longs if your worried but bubbles go higher than one would think especially now that retail investors are back.

The big increases in fiscal spending by the government is not being countered enough by the slightly restrictive FED interest rates and QT. Plus add in all the stock buybacks and future rate hikes (hikes may not happen but at least the FED is not talking about rate hikes)

I of course….have no idea where the market will be in 6 months.

I meant rate cuts

Ehh, valuations seem stretched, even relative to the other bubbles.

The deficit spending also has to be financed unless it’s printed (and right now, there is no printing).

I’m not at all confident that we’re going to see it “riding up” for the next 2 years.

A couple of questions:

If the Fed issues less T-bills does that increase or decrease the interest rates they are offering? How does the T-bill auction work?

With investors getting 5% return on their short term T-bill investments giving them extra dollars to spend on products and services (drunken sailors), doesn’t this actually work against QT?

Sorry for my naïveté. Just trying to understand.

1. The government (US Treasury Dept) issues T-bills, not the Fed. But the Fed might buy some of them.

2. T-bill yields are largely bracketed by the Fed’s five policy rates and where markets think they’re going to be in a few months. If the Fed cuts rates, T-bill yields will fall in parallel, usually in response to the Fed’s jawboning ahead of time before it actually cuts rates.

3. QT is designed to remove liquidity from the market. Higher interest rates are designed to slow the economy. Two different things. A small part of higher interest rates (interest income) adds fuel to the economy, and a much larger part of higher interest rates (higher debt service costs) removes fuel from the economy.

MW: CPI shrug-off intensifies: S&P up 1%, while Nasdaq jumps 1.4%

I’m basically a monkey tossing darts at a stack of old wall Street journal pages, but I’m just curious about the pace of rolling off balance sheet stuff and how that influences future Treasury issuance.

Although that’s an idiotic thing to ponder, the roots of this simple thought is based on the overall framework of what some banks were thinking (like SVB) when they bet the farm on long treasures, when prices went unexpectedly way down.

Sitting here with darts in hand, I’m just curious if this QT magic might contribute to maturity mismatching in a future sorority dance.

I almost always get everything about this wrong, but these models that the Fed plays with, are often open to interpretation by market forces.

I have to ask, because the next dart tournament is approaching fast.

Maybe a WolfStreet headline something along the lines of “Powell is going to need a wig”

I’m gonna keep my Powell in the box today. I don’t want people to get tired him. He can use his off-time in the dark to let his hair grow back.

Ok, let’s go back to basics and ask an appropriate question — possibly even re-read this article.

Is the Fed balance sheet in balance? Maybe another question is, does QT balance the Fed balance sheet?

These are just darts being tossed, but is there any mismatchings going on that might shine a light on accounting irregularities?

Random web capture:

“SVB’s collapse was largely due to duration mismatch. This means that the bank failed to match the duration of loans with the duration of assets”

Monkey Troop 409

“Is the Fed balance sheet in balance?”

Yes, it always is, as is every balance sheet. Accounting 101. Assets = liabilities + capital. And that’s the case with the Fed’s balance sheet too.

The rest of your comment is a word salad. You really should take a basic accounting course at your junior college.

Wolf,

Many thanks.

Crunching the numbers, if the Fed does nothing from here but continue to let QT run on autopilot then by the end of 2026 total assets should be sitting somewhere around $5.4 T. Probably the point where they have to stop anyway.

So why all the fuss from the Fed about slowing down, tweaking, etc? Much ado about nothing?

The saying “Once Bitten… Twice Shy” comes to mind. They got bit in the 2017-2019 QT and had to prematurely halt it. They are looking for ways to prevent a Black Swan interfering with their plans this time… even though it probably won’t happen at all.

What’s the “bag limit” on Black Swans?

Trump made Powell pivot or his job was toast. Real estate, the Trump empire, interest rates. In retrospect it was all about dollars and cents for Donald and most of his family.

If they go too fast, they might not make it to the end of 2025 or 2024 before something blows up. That’s their fear. If they go slower, they might make it through 2026 and end up with a smaller balance sheet.

I’ve got 21% Total inflation since 2021 began. Not exactly a flesh wound is it.

That only affects the poverty stricken middle class workers. Today is one of the few times in the last decades where interest rates and wages have outpaced the so called inflation rate. In a perfect world this needs to continue forever.

The simplest solution at the time they run out of treasury bills, would be to get the federal government to start spending cuts to pull out additional liquidity. One side of the federal government is in QT (Reserve), and the other in QE (Legislative and Executive Branches). Since we’re likely heading into rapid (double digit) and potentially hyper (triple digit) inflation, the roles will have to swap, and the reserve will monetize debt while the federal government tightens.

MW: U.S. budget deficit swells to $296 billion in February U.S. budget deficit swells to $296 billion in February

MW: Treasury’s $39 billion auction of 10-year notes goes badly

It’s kind of funny to time a 10-year auction with an awful CPI release

https://wolfstreet.com/2024/03/12/beneath-the-skin-of-cpi-inflation-february-inflation-saga-far-from-over-core-cpi-core-services-cpi-in-ominous-6-month-trend/

Is there any way of knowing the MBS mix 15 vs 30-year notes compared to the last round of QT, where the Fed continued to allow MBS rolloff while stabilizing the balance sheet through treasury purchases? 15-year notes would contribute to a larger % of passthrough rolloff, compared to 30’s and the MBS rolloff could be a bit quicker, proportionately this time around?

Or has refinancing and home selling typically been the largest contributor to MBS rolloff?

I go to ZH for “the sky is falling”. I come to Wolf for “this is the best of all possible worlds”. Perhaps reality is somewhere in between and perhaps both are simply mirror images of the other.

For me personally, I love 5% interest rates. I don’t care if the Fed is in QT or QE because I don’t fundamentally understand the ramifications of either…and probably neither does the fed.

People are scolded for hating the fed. But it’s not just the FED, its every single institution that is suffering a dysentery of credibility. Deserved or not.

This all feels like Europe just before Luther nailed his complaints to the church door crystalizing 200 years of of sneaking suspicion that the institutional Church was a fraud and the secular “Church” of our day reacts in the same way.

QT equals freedom 55, QE equals working until you drop dead its that simple. QE has caused more damage than the atomic bomb and all wars combined.

MW: S&P 500 closes at new all-time high as market shrugs off February inflation data

QT, shrinking the balance sheet, is ill-defined. When you increase reserves, you’re increasing liquidity.

Some liquidity moved from ON RRPs to reserves, and both are liabilities for the Fed — and you know that. ON RRPs plunged by $1.8 trillion since April 2023. Over the same period, reserves rose by $600 billion. The net is a decline of $1.2 trillion (-1.8 trillion + 0.6 trillion), roughly matching QT over the same period.

No, MMMFs aren’t money.

1. I said “liquidity.” I specifically avoided saying “money,” just to dodged our beloved commenters here that would otherwise heckle me with: “‘Gold is money. Everything else is credit’: J.P. Morgan”

2. You also said “liquidity” in the comment I replied to. Neither you nor I used the term “money.”

In fact, I’m really not interested in what your definition of “money” is.

MMMFs are nonbanks. “No asset has the “monetary store of purchasing power” quality unless there can be a net conversion of that asset into money. It must be possible to affect this conversion without necessitating that any present money holder reduce/liquidate his holdings”

People here will heckle you here with: “‘Gold is money. Everything else is credit’: J.P. Morgan”

DM: Average US credit score FALLS for the first time in a decade thanks to steep prices and record-high interest rates

American credit scores are falling for the first time in over a decade.

They got way inflated during the era of free money and forbearance when delinquent mortgages and student loans didn’t count as delinquent because they were in forbearance. It got to the point that credit scores became meaningless because people with a defaulted mortgage had pristine credit scores. Those were the times, and they’re gone.

Isn’t it both ignorant and reckless for the US Federal Reserve to reduce its balance sheet down close to the annual budget for the US?

🤣

The Wall Street Journal’s reporting is usually dripping with anticipation of Fed rate cuts. And so, I was amazed to read these words in the WSJ editorial comments this morning: “In this kind of market run in the 1990s, former Fed Chair Alan Greenspan counseled against “irrational exuberance.” There’s no such caution at the central bank now, as the Fed is eager to declare that inflation victory is at hand. Maybe wait until prices aren’t re-accelerating.” The people over at the Wall Street Journal must be reading Wolf’s analysis! We can only hope.

QT is relative. QT suggests a braking effect on the economy – not a lessening of QE. In my eyes it isn’t QT until the Fed balance sheet drops below $4.75 trillion – which is the level it was pre-pandemic adjusted for inflation. Otherwise it is still QE… just lesser levels of QE as the amount of monetary expansion is lessened. Those dollars are still out there – still driving economic activity – and one can argue – inflation.

That’s the problem with these huge expansions in the money supply – they become self-sustaining. You’ve got people screaming that they need to start increasing the Fed balance sheet again… when we haven’t even gotten back close to the starting point.

Sure, everyone can just make up their own definition of what QT is.

Knowing what the fed is doing is just half of the answer. We get no correspondence from the PPT, and since this market is fat with liquidity, my best guess is they have their hands full too. Pulling levers day and night. I wonder why the presidents working group aka ‘ppt’ only reports to the president because everyone knows they can and do buy stocks and bonds in the open market under the ruse of stabilization.

Lots of good stuff in this article:

1. I did not know that Fed was using T-bills to fill up the current 60B runoff quota. I had somehow thought they only let the longer-term bonds and notes (minimum 1-year) run off.

2. I did not know that Fed so far has been replacing runoff over the cap with like-maturity bonds (same percentage)

Comment: It could be that Fed’s “QT taper talk” is simply a reflection of the

fact that “QT will naturally slow in June 2025” combined with an unwillingness of the Fed to be been as an outright seller of USG bonds/notes. Whether such a “natural tapering” also means to have an official declaration that the the cap is being lowered remains to be seen,. Lowering the cap, officially, may be seen as inflationary and may indeed BE inflationary because wall st will read it is a signal.