The amazing labor market that just keeps plugging along despite the high interest rates.

By Wolf Richter for WOLF STREET.

It was the kind of jobs report that you’d expect from an economy that is plugging along just fine, growing at a solid pace while the gyrations of the pandemic have settled down.

There was a kink in it though: Average hourly earnings jumped, with growth accelerating for the third month in a row, rising at an annualized rate of 5.0% in November, at the high end of the range of the past 12 months, and we discussed that a minute ago

The question is why would the Fed “pivot” to multiple rate cuts starting in Q1, with the labor market this strong, with wage growth re-accelerating, and with inflation in services – where two-thirds of consumer spending goes – running at 4.6% according to the PCE price index and at 5.5% according to CPI? Sure, energy prices plunged, and durable goods prices dropped off their spike, but the action is in services, and Powell has lamented the stubborn core services inflation at every press conference.

So this was not a rate-cut jobs report – and there hasn’t been a rate-cut jobs report this year. This was another jobs report in a long series that changes the question of when the Fed would cut rates to why it would.

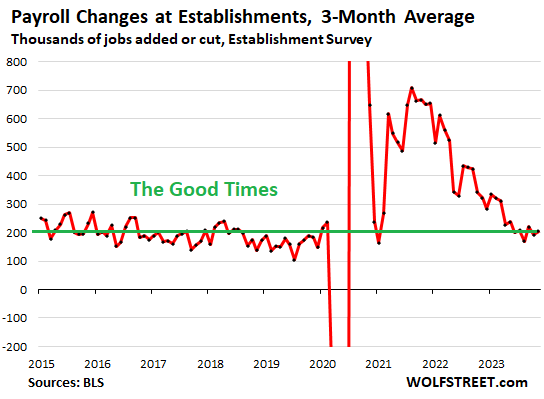

Employers added 199,000 workers to their payrolls in November, according to the survey of employers by the Bureau of Labor Statistics today.

The strikes in the manufacturing sector had caused manufacturing employment to fall by 35,000 in October, but by now, many of these workers went back to work – as we said a month ago they would, and here too. So in November, employment in manufacturing rose by 28,000 workers.

The three-month average of jobs created by employers rose to 204,000 and has been in the same range since June. In 2019, the three month-average of net job gains was running between 100,000 and 200,000.

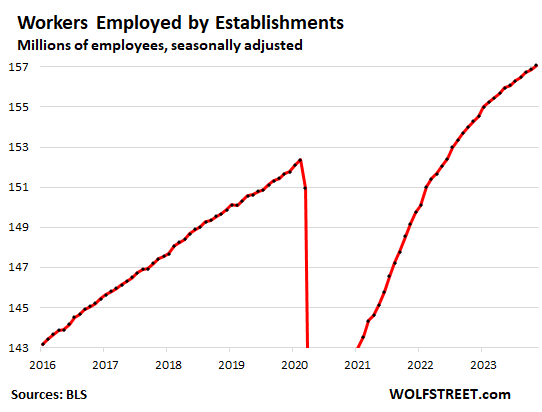

Total payrolls at employers rose to a record of 157.1 million.

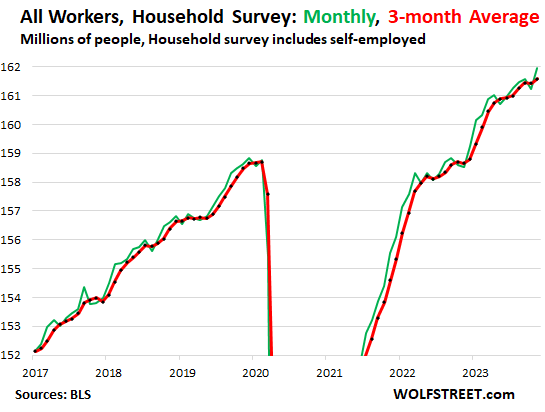

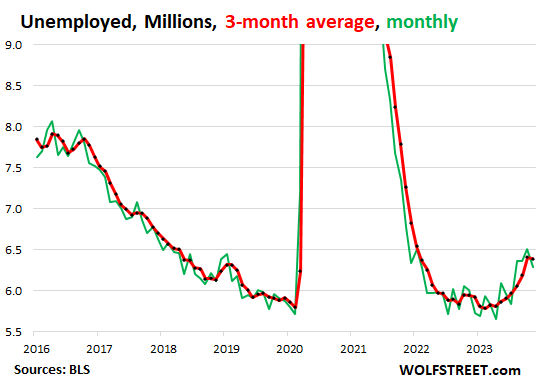

The total number of workers, including self-employed, jumped by 747,000 in November from October, to a record 162.0 million, based on the BLS survey of households, which accounts for all types of workers, even those that do not work for an employer per se (green line in the chart below).

To iron out these month-to-month ups and downs and see the trend, we look at the three-month moving average. It rose by 162,000 in November (red line).

The number of workers includes these categories that we’ll get into in greater detail:

- Workers with wages and salaries

- Self-employed workers

- Part-time workers

- Multiple jobholders – in this survey of households, each worker counts as one worker, no matter how many jobs they have, since this data counts people not jobs.

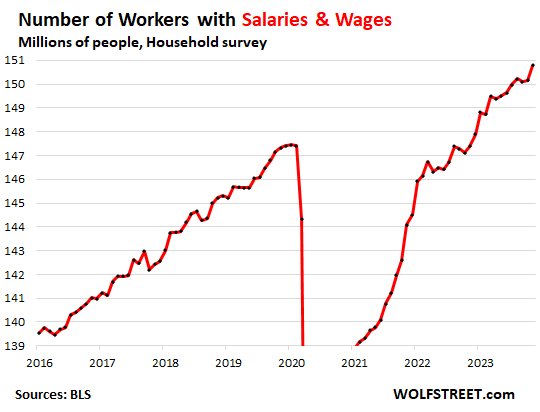

The number of workers with salaries and wages jumped by 644,000 in November, to 150.8 million, per the survey of households.

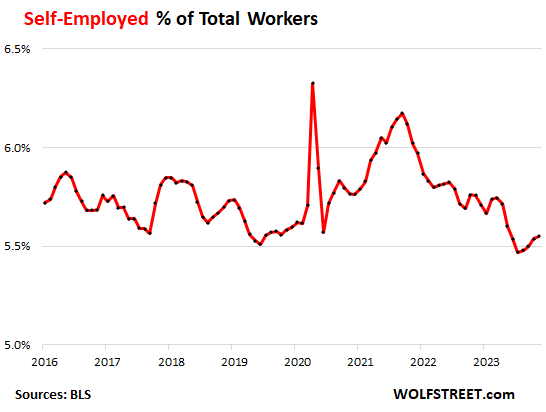

The number of self-employed workers rose by 55,000 in November after having dropped by 43,000 in October.

A larger population and a larger labor force and more working people means that self-employment should be looked at in relationship to the total number of workers – what portion of the workers are self-employed.

Self-employment as a percentage of total employment has dropped to the low end of the range before the pandemic, to just over 5.5%:

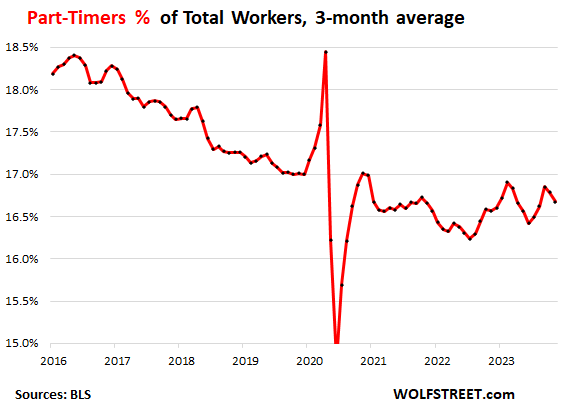

The number of part-time workers rose by 339,000 in November after plunging by 670,000 in October. At 27.0 million, the number of part-time workers was roughly in line or below the years before the pandemic (between 27-28 million). The BLS defines part-time work as 34 hours per week or less.

Part-timers as a percent of total employment dipped to 16.7%, roughly in the middle of the range of the past two years, and well below the declining range before the pandemic. In 2016, it was still above 18%:

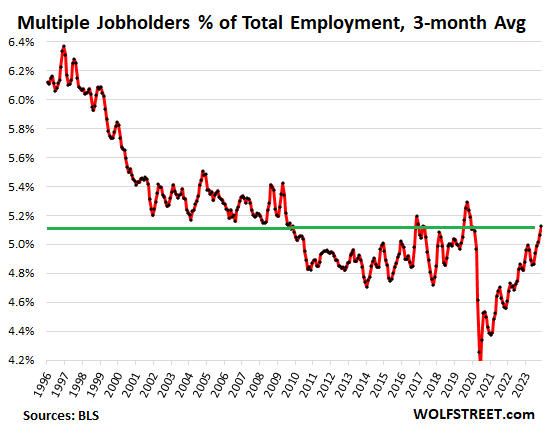

The number of multiple jobholders dipped in November to 8.34 million. As percent of all workers, multiple job holders dipped to 5.1%, same as where they’d been in November 2019. In the 1990s, multiple job holders accounted for over 6% of total employment.

Note that in this survey of households, each worker counts as one worker, no matter how many jobs they have, since this data counts people not jobs:

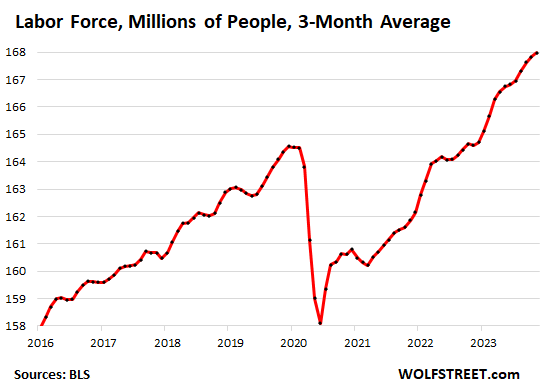

The labor force jumped by 532,000 people. These are people who are either working or actively looking for work. Over the past 12 months, the labor force grew by 3.73 million. The labor force is surging due to the increase in the number of workers and the influx of people looking for work, such as young people just starting out, immigrants, people returning to the labor force after some time off the hamster wheel, etc.

During the pandemic, the constrained labor force had been a huge problem and caused some of the labor shortages and the sharp increases in wages.

But the increase in the labor force in November has been more than absorbed by demand for labor, and the number of unemployed and the unemployment rate actually dipped.

The fact that supply of labor rose at a good clip and demand for labor rose even faster is another indication of a still strong labor market.

The number of unemployed people who are actively looking for a job fell by 215,000 to 6.29 million, the lowest since July, after having zigzagged higher from historic lows (green line). The three-month moving average dipped to 6.39 million (red line).

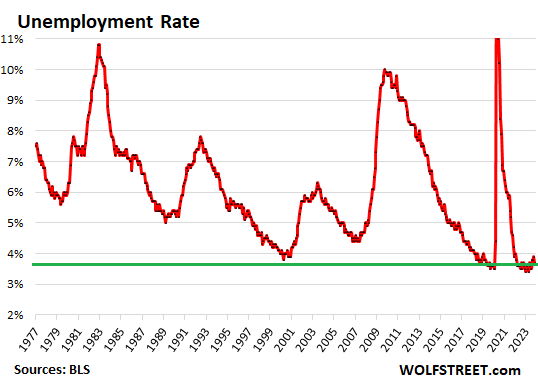

The unemployment rate, which accounts for the rising labor force, dipped to 3.7%, the lowest since July. These are historically low rates. The rate has hovered in the range between 3.4% and 3.9% since February 2022.

Just to see how historically low the unemployment rate is, here are the past four decades:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Why is there so much pessimism? I keep asking that but never get an answer. From now on I’ll just take that to mean the person commenting is having a rough time personally, and extrapolates that to everyone else. Even though everyone around them is buying cars and/or eating out nearly every meal.

People just like repeating the same garbage about the fed, and so forth.

“Why is there so much pessimism?” – Harold

The pessimism stems, I believe, from an informed recognition that an economy running on demand stimulant (in the form of both monetary and fiscal policy) will eventually face the reality of the mopping up of excess money, a return to fiscal discipline, a prolonged bout of institutionalized inflation, or all three. Though the disasters manifested differently, this was the case in 1921, 1930’s and the 1970’s, and the GFC.

Each generation is offered multiple opportunities to learn about cycles, but most individuals choose to assume that “this time is different,” and that “we are wiser now.” Confusingly, each time is AWAYS different…. but the cycles still occur.

(Kipling’ 1919 poem God’s of the Copybook Headings described it perfectly.)

IMHO.

The ‘Rob Peter to Pay Paul economy’ cannot go on forever.

@Harold: No, it’s not pessimism. As John H. and brad have mentioned above, it’s questioning the fiscal and monetary policies of our government and the Fed – and rightly so because they are short-sighted and inherently bad for most Americans except perhaps for the 1%.

Repression of interest rates and blowing up stock market and housing market bubbles causes enormous monetary and emotional pain to citizens as they ride this roller coaster economy month after months and year after year. If you are not able to see that, that’s ok.

So there’s indignation, anger, and frustration, not pessimism.

The Fed is less short-sighted than most and most that predicted differently (and correctly) were just lucky. There may be a few true visionaries the predicted accurately based on facts and good reasoning but most are just stopped clocks with no real track record.

So stop blaming people for being short-sighted while you look at them with the benefit of hind-sight.

Also realize that the Fed’s hand has been forced by dealing with major short-term problems like the GFC and the pandemic. Long-term planning just isn’t possible when your kitchen is on fire.

The punishment has already occurred. All prices were adjusted higher, and they are not coming back down.

Prices of used cars, electronics, and a bunch of other durable goods have already come down and will continue to come down. Deflation in durable goods is pretty common.

A single family home is durable, no?

I never heard of that poem before, but I love it.

Pessimism?

Maybe because the average worker can’t afford the average house or car, let alone anything extra: like a boat or RV.

I’m personally doing fine, but at 3x the median income for the area, my new dollars should go further than they do.

Inflation has come down, but prices have not. $100k a year is the new $50k.

Indeed.

How can “mopping up excess money and a return to fiscal discipline” co-exist with “institutionalized inflation” of the money supply?

Jim T.-

By “institutionalized inflation” I was referring to the historical favoring of:

– money printing and distribution and fiscal stimulus

over

– tightening and austerity (i.e. “discipline”)

The former involves government largesse, various asset bubbles, and is popular. Short term gain, but with long-term painful consequences to currency value.

The latter involves “belt tightening,” job losses, bankruptcies, and is unpopular. Short-term pain, but monetarily more protective of currency purchasing power.

Government agencies and legislature, being human, tend toward less-painful short-term solutions, especially as inevitable financial crises arise.

This bias is on display in the relatively new policy of a 2% inflation target, versus a more responsible and credible 0% target.

Sadly, this quote from Pat Paulson (1968 Presidential candidate and comedian) humorously summed up the question of the inflation problems of that era:

“I think I could solve it no matter how much money it took.”

Correct.

Deeper dive also shows primary employment gains have been in healthcare (which experienced profound changes downward during Covid) and federal/state government (a definite negative!).

“Why is there so much pessimism?”

Because there are a lot of miserable people in this country who watch cable news and live in fear. When you spend this much time consuming propaganda deliberately built to make you keep coming back, you’ll inevitably find reasons to be pessimistic about everything from immigrants to AI.

“Why Ded would cut rates?”

To give trillions of dollars to the 1% that can then throw cents to the bottom 50% to benefit their cronies in “both parties” in the upcoming elections.

Doesn’t matter which party wins elections, the cronies will rule.

I find those who have little to no skills are the pessimists

those with skills have bright future

I know 25 year old – bought 2nd home, no college, barely got out of high school – family with 2nd child on way

now so busy with projects he’s hiring out and basically being a general contractor on side projects

has great skills and can think out problems, gaining experience every day

To dream is free!*

*The hustle sold separately

The Fed will not cut rates until the labor market deteriorates over a sustained 2-4 month period. Like Wolf explains, it’s currently chugging along with no sign of heading south. The 1st-time unemployment claims will have to get up to about 250K weekly and stay there for at least 2 months before the Fed will even consider the first 25-basis point cut. They know the real issue is a ’74-’76 head fake where inflation shot higher after a brief respite. There’s a 50-50 chance headline inflation pushes up towards 4% by next summer.

I’m not miserable, but I certainly don’t have my head stuck in the sand. Anyone who doesn’t have any real complaints is easily in the top 40%. The other 50-60% are getting hammered pretty hard.

Massive income inequality, paralyzed government, weaponized FBI, DOJ & ATF, erosion of liberties, major geopolitical issues that could get much worse at a moment’s notice, ~$34T in national debt, $981B annualized interest expense, rising PCE inflation, rising existing homes prices (sidebar: new home prices are ONLY falling because they had become so egregiously high with commensurate gross margins for builders), rising insurance costs, including Heathcare, gas prices above $3, expensive cars, expensive food, airfare. The list goes on & on.

And, immigration & AI are really big issues, way bigger than your flippant reference to them implies. The former will be a MAJOR issue in the ’24 election, especially at the state level. AI is probably more of a ’28 & ’32 issue but it will be an extremely big deal once we start to move out of the “Oh, don’t worry, it’s going to make you better at your job phase.”

The pessimist complains about the wind; the optimist expects it to change; the realist adjusts the sails. … William Ward

Exactly right. They are hooked on it like junkies.

large majority of homeless are druggies

and they don’t care about damaging your property

I’ve seen them walk right into moving traffic and then yell at drivers to watch out for them

—–

there is so much work out there for those who have some skills, are teachable and have work ethic

you don’t get rich overnite like bitcoin boys/girls say

Many of the homeless are suffering from mental illness.

Well said! Fear is a great way to get votes and eyeballs to watch commercials.

I think Charles Dickens said it better in his Tale of Two Cities than I could. So I have copied it.

It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of light, it was the season of darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to heaven, we were all going direct the other way–in short, the period was so far like the present period, that some of its noisiest authorities insisted on its being received, for good or for evil, in the superlative degree of comparison only. ~ A Tale of Two Cities

Copied from Charles Dickens Info

Here’s another great Dickens quote that can explain some of the present misery:

“Annual income twenty pounds, annual expenditure nineteen nineteen and six, result happiness.

Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.”

― David Copperfield

Thank you Max Weber!

No one but you can think independently or has actual friggin experience in the military, intelligence, business, R&D communities!

I’ve said this before: there are a significant percentage of the population that rents, likes to own high-end pickups, and eats out a lot. Inflation has eaten them alive, but they can’t imagine any other way to live.

For the rest of us, its the best economy in our lifetimes.

Best economy?

I make more than I ever did in my lifetime and can’t afford a house that I could have easily bought three years ago. There’s an entire generation locked out of home ownership because of irresponsible fiscal policies.

Why should they be happy?

just wait to SHTF with fiat $dollar

think you have problem today

I’m making roughly same as I did 5 years ago

I ratchet up my prices for services

What I did since 2009 is payoff all mortgages

around $1million paid off since 2009 – made a lot of lemonaide

now all investments are Free and Clear – but costs are going up and so are the rents

That’s not true, doug. You can afford a house. Just maybe not the one you dream about, in the location you want. Not everyone can be rich. Adjust your expectations like a grown up.

@Harrold. So just grow up and overpay for a house you don’t really like at the peak of a massive real estate bubble and plan for no equity increase for 15 years or so and risk getting your face ripped off if the bubble implodes spectacularly? Is that your sage advice to young people looking for their first house? Give me a break. Try to consider how difficult all this economic volatility is on folks in different stages of their lives.

@Harrold,

In all but a handful of states median *household* income is not high enough to qualify for a median priced home *statewide*, and by a large margin. Doug has a point, backed up by real world statistics, not merely based on personal beliefs. Below are the mortgage payments (P&I only, 3% down payment, 7% rate) as a percent of *household* median income to buy a median priced house for a few states.

CA 72%

HI 65%

MT 64%

WA 57%

NY 55%

MA 55%

OR 55%

CO 54%

…

MS 41% (median ratio)

Since the debt to income ratio to qualy for a mortgage loan is 43%, you could barely quailfy to buy a home in Mississippi, assuming no other household debt, whatsoever.

There was an event, a pandemic. There was a response, a wave of money (yes, at an inopportune time). There was some overspend with that. This wave too will pass. It is showing it is passing.

Had you lived through a war, I mean a real one at scale, you would have much more to complain about. The world is at moments inequitable to a certain demographic. That is not strictly fixable, especially in a compressed time. But it is being addressed. Each life path too has some luck and randomness. Everybody doesn’t get the same free gum or opportunities.

Phleep,

You have to be kidding. I won’t get into what I feel about the shutdown since this isn’t the site for such discussion. But the level of monetary/fiscal stimulus that followed was completely unnecessary, and now we have a mess in services and asset prices that need to be unwound (deflation) from the past three years that never should have happened. The Fed was too quick to dismiss inflation that even the average Joe knew wasn’t transitory. I can’t believe you think this too shall pass. This wasn’t a little inflation, and with the way our government is still spending and wall street pushing for easy money, we will never get back to normal.

Jeff D:

The real crux of the problem is the “3% down payment”. If you can only come up with 3% down, you shouldn’t own a home or even consider buying one. Period. Full stop. It’s called champagne tastes and a beer budget.

I don’t give a rat’s patoot about “bubbles” and the like. There have been multiple bubbles over the decades. Multiple economic downturns. Multiple examples of skyrocketing interest rates. Guess what? If it’s important enough to you, you’ll figure it out and work tirelessly towards that goal. Generations before you did. So could you. But you prefer to sit on the couch and whine.

If you’re deluded enough to think that a 3% down payment for any major purchase is a wise financial choice, and that’s all you can muster, you will likely learn an unforgettable lesson in personal finance. And by waiting a year because “houses were too expensive”, you just learned an important lesson in personal finance. Make a plan, work your plan, adapt your plan. Keep your eye on the prize.

And…. nowhere in any period that I can recall prior to the 2008 implosion and the HGTV / Magnolia Network fantasies, did anyone run around and crow about what their house was worth… yesterday, today, tomorrow, or the next year. It was a frickin’ place to live – not an “investment”. Your monthly nut never changed much…. unlike the ramp ups in rent. You can then plan to build real wealth while wielding a paint brush rather than playing Grand Theft Auto or yelling at the TV set while watching sportsball. Walk in your garage (or street or parking lot) and add up those notes. How much other useless crap have you bought because “you make good money”?

Real world: 2010 my daughter bought a house. Interest rates were high and she had limited down money (10% – far more than you). She got kicked to the curb on everything she bid on. I lost count. Then we found a sugar shack that was completely redone, a little forlorn, and bank owned. They wanted off it. She looked like she was 12 at the time, so no other buyer at the open house (one weekend – best and final on Monday) considered her a competitor and talked openly about their “strategy” (most of which were stupid “get me dones”). We talked as she walked the property, put a full price offer with only an inspection contingency, 30 day close, the bank countered at +5K and we did the deal. We did increase her down payment with an inter-family loan. Her monthly nut was @ $1,500 per month all in. Her apartment at the time was $2,000 a month (2/3 the size) and went up to nearly $3,000 within a few years. Her monthly with the house remained nearly the same (small creep in property tax thanks to prop 13). From that point on, with predictable expenses, she could make bank as bonuses came in and career progression occurred. With the reduction in her rent, she had funds to repay the loan. (Note: Never spend a bonus – invest it. It’s found money.)

Lastly, house prices are adjusting. I just sold my sister’s house in FL for $1M “turnkey” as in all the stuff in it went with it. Gustav Stickley solid cherry furniture. Art (real art, not drymounted posters). Baccarat crystal. The works. House across the street sold in June of 2022 for $1.84M. Same house. Same pool. Same cul de sac. I discounted it $350K because the buyer was gold plated (cash), quick close (15 days), and I could GTFO of Florida forever. It will need a $30K+ roof in two years (otherwise uninsurable), needed landscaping renovation (I can’t be in two places at once and what the contractors do to geezers is borderline criminal), and – regardless – insurance will be a nose bleeder when the next renewal comes due in March. Plus, if a storm comes and it were to get damaged, I don’t know how I would deal with that from 2,500 miles away. It cost about $3,500 /mo to keep the house alive (utilities, etc.), so any “loss” on sale will be recovered over a period of a few years ($1M @ 5.2% = $52K simple math per year plus $42K of money not spent on a vacant house – bust out in about 3 years and zero risk of suffering any further dain bramage). And that doesn’t include the costs associated with me flying there every 6 weeks or so to keep the house insurable (aka “occupied”).

This.

@El Katz,

With 20% down instead of 3%, you can knock 5% off the ratios I gave. Still, deeply underwater in many states. And that is with no car loans, student loans, credit card debts, etc. in the household. Furthermore, costs of property tax, insurance, downpayment, etc. are not debts, but none the less cut into disposable income. Do you

expect people not to eat? My point is that there is an older cohort that believes economics for young people today is the same as economics from when they grew up, or even from a decade ago, simply because they are too lazy to run the numbers and see that today’s economy is, in fact, different from any historical period they were alive to see. Be a curmugeon if you want, but The Fed royally screwed the majority of people in this country (lower 50% of income) with their MBS purchases and ZIRP from 2020 to 2023. Meanwhile, landlords refi’d to a lower rate to reduce the cost of their investment while simultaleosly increasing rents by 50%. And no, repairs, insurance and taxes didn’t increase by anywhere near 50% over that period.

@El Katz,

Sorry. Knock 10 off the ratios I gave, not 5. All the comments still apply. Also, while the insurance and property tax may have increased by 50% somewhere, the point is that the extra costs come nowhere near the additional money from the 50% rent increase.

El Katz,

Interesting stuff, but I’d say your points apply to low-to-mid priced markets, where affordability has reduced but remains within reach. When people read your post from places like LA, Boston, Seattle, or San Fran, etc., the points don’t have reasonable application.

In markets where the median priced home is $1.5M and a two bedroom 1500 ft. dump goes for $1M, you’ll have a hard time convincing a hard-working nurse or firefighter high housing prices are not a problem, particularly when many of these areas are known for booms and busts. You can drop $1M on a fixer upper, spend 1,000 hours on it, then have to sell it for $700k five years later. At these price levels, it’s a real risk.

Pardon me Harrold but pack sand.

It’s clear as all day that the economy has been separated from true market forces and manipulated/orchestrated by huge ideologically founded gov’t spending priorities and regulations, endless executive orders, biased (on the take) media, etc., etc.

The “just smile and make due with what’s at hand” argument doesn’t cut it.

But hey! The Republican House just passed proposed legislation that expands FISA authorities to collect and act on data covering domestic communications! Better comply!

“…We did increase her down payment with an inter-family loan…”

You see! Its easy! Bootstraps is always the answer!

andhavinghighlysupportivefamilywithmoneytheyarewillingtopartwithbutnevermindthat

Bootstraps!

There are also a lot of people who rent, don’t drive cars at all, and eat our fairly rarely. I work with a lot of them.

They have seen their costs jump 25-50% over the past couple of years, and most have not gotten anything near that in raises.

Meanwhile, business owners were handed a gift by Congress in the form of “forgivable” PPP loans.

And asset holders, whether in the form of houses or stocks, have seen their assets skyrocket during that time of “pandemic hardship.” Many of them realize they were lucky, and others think they are brilliant investors, and “deserve” all of that new wealth.

They’re out spending it on luxuries, driving up the costs of living for the everyday Joe.

Meanwhile, the retired 80 year old has seen her meager $100,000 in savings be devalued by 25%, and the thugs in charge of the Federal Reserve gaslight us about “returning to 2%” while making no effort to undo the overshoot.

I think it’s pretty clear to see why people are pissed off, if you just use your head.

Einhal –

Good points about currency devaluation and sloppy and excessive fiscal stimulus.

But do you mean to villainize all “asset holders” as evil opportunists? If yes, I think you are taking on the vast majority of posters on this sight. They have tuned in to Wolf because they ARE asset holders now and want to enhance and protect their accumulated holdings, or because they ASPIRE TO BE asset holders so they can comfortably retire some distant day.

I don’t think the disparagement of asset ownership was necessarily your intent, but that’s how it reads…

Respectfully.

And perhaps this is a California only thing but plenty of people who have jobs still can’t afford rent and are homeless. Seems to be a general desire to have a reductionist view of various issues.

John H.,

It is just a matter of time before the asset holders (villains or otherwise) get nailed.

DC manipulation of interest rates (via manipulation of the money supply), horribly over-inflated asset prices (read up on discounted cash flow model) and every day with now-semi-normalized rates is a day when that bubble can pop horrifically (thus the pivot praying by Wall Street and realtors).

Equities have already fallen maybe 25% of the way to their final destination (a tiny handful of still-overvalued giants in the indices obscure this) and *actual home sales* have fallen by 35% (nobody can use merely theoretical paper gains…you have to be able to actually *sell* the house to use/enjoy alleged “wealth” on paper).

John H.,

I’m not villainizing all asset holders. However, there is a huge segment of asset holders who have no humility about the fact that the Fed handed them a gift, and fight like hell to keep it.

I heard talking heads on CNBC say that it’s not worth getting inflation under control if it causes a decline in the stock market.

As a great video I watched the other day said:

> if you give rich people money, it won’t trickle down

> they’ll buy your mum’s house and rent it back to you

Until rentier activity is outlawed through punitive taxation, this will remain true.

Then don’t SELL the house to them! It gets really old reading your silly comments about “rentier activity” to describe the business of investing (and risking a lot of money) in a building, and paying for improvements, remodeling, maintenance, insurance, taxes, and repairs, and then trying to make a return on that investment by renting out the apartment, office space, industrial space, self-storage, retail space, etc.

Einhal-

I hear you.

Those particular heads are selfish idiots intent on gaming the system to their own ends.

In the great circle of investors, on either side of the idiot, stands a more average Joe like you or me, I’d like to think. Hate to lump them all together too much.

(I hope my general estimate of 67% good:bad is not too naively aggressive…)

In an imaginary world, without monopoly and QE, the rich might deserve what they make. But in the real world, the amount of wealth they make with monopoly and with the help of government and Fed cannot be justified.

You said it as it is!

Don’t worry about asset holders feelings because they don’t care about yours!

“They denied that Wishes were Horses; they denied that a Pig had Wings;

So we worshipped the Gods of the Market who promised these beautiful things.” Kipling 1919

Counter-argument: one can be an asset (home)owner, and still be hurt by rising hme prices.

If you bought a home to live in and don’t have plans to sell, rising asset prices cost you more money and you don’t reap any of the gains.

“Asset holders” is a huge group ranging from folks with multiple vacation homes, to those living in <1000 sqft ranches with a food budget of $10/day (hi).

Renters aren't the only victim of Fed policy.

John H – look at what has happened to the distribution of wealth in this country over the last two decades.

It’s a losing hand for all but the top 1%-5%.

Phillip Jeffreys-

No argument that the “gates open” years of monetary and fiscal extravagance have temporarily benefited those with assets, but when the markets ultimately correct, the vast majority of those who benefited will fall from the top tier, and many will be permanently relegated to penury. Many will hold a LOSING hand, then. At least it seems that that’s how bubbles have played out in the past.

Allow me to ask: are the local fireman’s pension plan, or the the VALIC retirement plan (California Teachers), both of which benefited from the asset run-up over the past 10 years, also included in the “asset holders” net that might be implied in Einhal’s assertion?

Or the Catholic Church, or the AFL-CIO?

Who gets to judge where “the wealthy” begins, and where does “equalization” end?

Respectfully…

It’s just as likely that a number of those Raptor-driving, fine-dining renters are leasing strategically having sold their miserable little hovel to some numb nuts in ‘22 for triple what they paid. But by all means, preach a narrative that makes you feel smug.

If you think this is the best economy in your lifetime then you should feel very fortunate to be a have and not a have not.

While some people don’t manage money properly there are far more people homeless and starving because of the wealth inequality our government has bred.

Inflation is literally eating the poorest and most vulnerable parts of our society.

This economy nor country is not something to be proud of. We should all be ashamed and understand who the enemy really is

There are less people living in poverty on this planet than at any point in the past.

Are there way too many homeless people concentrated (mostly) in blue states who have policies that encourage their presence? Absolutely.

Is our immigration system broken? Absolutely.

All of these things can be true. Especially when we keep adding hundreds of millions in population every couple years. But with incredible medical advances and the fact that this many people are surviving or thriving (depending on your view) tells me that there has never been a better time to be alive.

The real enemy are those who destroyed the family unit. That’s when and where most of the damage was done to the U.S. society. A family (not a bunch of people who are merely related by birth) learns values, works together for each other’s benefit, and doesn’t turn their backs on a sibling, a child, or a parent, because they’re inconvenient. My parents were children of immigrants who came with bupkus from Europe. My wife’s grandmother was an indentured servant from Czeckoslovakia that escaped communism with nothing more than her Mayday dress on her back. Every one of them prospered despite the wars, Great Depression, recessions, job losses, financial setbacks, illnesses, and tragedies. They held each other together.

My kids have backstopped me when I needed it, backstopped their aunt, I’ve backstopped my sister – both from an emotionally draining perspective as well as financial ones. The kids are thriving. My son learned how to, and now loves, building things from me. My daughter picked up financial acumen and is clever about how, when, and where she spends her money (yet still lives a quality lifestyle on the beach in CA). I made sure they were educated without debt and *launched* as a young adult because being a father is much more than providing fertilization to an egg. My wife and I sacrificed *stuff* so Mom could be home – which paid off by producing a couple of productive members of society. We still did okay financially, despite not having a Porsche or Corvette (equivalent of today’s King Ranch pickup) in the driveway when we were in our 20’s or 30’s. We bought a crapbox house and made it our own over a period of years. Probably the best decision we made at that age as it set the stage for future prosperity. And, no, we didn’t worry about what it was “worth”. It was home. My parents and sister helped us with the down money (we paid them back within a year) so we could start building a life at the ripe old age of 24. My parents and my Sis/BIL weren’t rich… but they knew how to build a stable foundation for the future.

If you look at some other cultures and their multi-generational households (we experienced that firsthand in CA), how they care for and respect their elders, grandkids watching grandma while she toddles down the street in her walker then watch the hood rats, it’s not hard to figure out why you don’t see massive homelessness in their native countries. Their culture doesn’t allow it. Ours does.

So blame “da Fed”, “Raygun”, “J Pow”, and any other boogie man you choose… then look in the mirror and point your finger at that guy cuz that’s where the blame lies.

You are likely the enabler of much of what you profess to despise.

Jd

Blue states homeless people really?

Politics really??!? Clearly don’t get the problem

Currently in a red state plenty of homeless people came from a blue state plenty of homeless there to

Also I’d say it’s unlikely there is less raw number of poverty now then in the past… Based on the population growth you mentioned… Maybe you mean percentage wise and all I have to say to that is there shouldn’t be anybody who is hungry or homeless with the massive amount of wealth that has been accumulated in this world and in particular this country. Especially since that wealth had been accumulated by the blood sweat and tears of so many who still have so little.

Oh and the biggest medical advance we’ve had in this country is perfecting how to keep people alive long enough to vampire all there assets out of them before they die. Sound morbid? Take a look at long term care and hospice expenses. Ridiculous!

Economics is called the ‘dismal science’ for good reason. Economic uncertainty is always present. Cable news and blogs are full of negative spin resulting in constant pessimism. The financial media are spin doctors and ‘presstitutes’ who pump Wall Street narratives, creating fertile ground for writers and bloggers to attack and expose. The result is negativity, Fed bashing, skepticism and yes, general pessimism. It goes with the territory. It’s important use filters and limit daily intake. Moderation in all things.

Agreed. The best thing anyone can do is reduce their intake of innacurate, self serving “news”

Most folks would do just fine reading business news once a week or even less.

It’s a proven fact that holding profitable assets for the long term is the best investment strategy. If that’s the case, there’s no need to listen to “news” at all, but we’re addicted to it

Holding profitable assets for the long term is only possible if you can afford it. Also, just blindly holding profitable companies means I might still own IBM, GE, Kodak, GM, Ford, etc. Those of us who live off of our assets plus some SS, beating inflation is crucial, and only possible if we stay informed. The better thing to do is to pay enough attention so that we gather many dissenting views, realize that many are self-serving, as you said, analyze them to the best of our ability, and make good decisions. For example, if I just kept my investments in a 60/40 fund, as highly recommended by many pundits, and hadn’t done a deep dive, I’d have been killed in 2022.

…and entropy, never, ever, sleeps…

may we all find a better day.

CCCB-

You say: “It’s a proven fact that holding profitable assets for the long term is the best investment strategy.”

Your advice is perilously close to a plagiarism of the famous quote attributed to Will Rogers:

“Don’t gamble; take all your savings and buy some good stock and hold it till it goes up, then sell it. If it don’t go up, don’t buy it.”

…and your advice about as easy to put into practice!

That said, in some markets and for some people, buy and hold can be a good strategy.

Nonsense.

The best antidote is experience – actual hands on knowledge.

Sorry Pangloss…your message isn’t going top sell.

insecurity due to high prices (inflation 2), caused by money epansion (inflation 1)

courtesy of the FED

Isn’t unemployment always low at the top? The two recessions I have lived through had very low unemployment right before the downturn. People were out partying like the good times would never end. There are so many other indicators that show we are due for a recession, it just seems obvious.

YES EW, exactly correct!

As a GC with tons of work, it was very difficult to get subs to even call me back in the period of 06 to early 08,,, and it was usually the ”office boy” or some such if at all those years…

By early 09, it was the company owner calling back and ready, willing, and able to bid anything I might have to keep him busy.

Similar pattern in two earlier ”recessions,” but 06-07 was THE worst as many older skilled workers hung up their tools.

Very true.

We also lost the youngsters

Starting out in the trades.

We are paying for that now.

I mentor anyone who wants to be my competiton. A great time to be young and willing to risk starting up your business.

You can tell a market top by the breadth of speculators who are making gains.

At the top of the last bust, I visited a bar by my house and chatted with two mortgage brokers with high-school diplomas who were bragging about pulling in $500k per year. Their little mortgage shop dissolved by 2010 and both were working at Costco a year later.

The same night, I spoke with a group of police officers who were pooling funds to invest in RE investment opportunities. I don’t know how they came out, but I can make an educated guess.

Reminds me of the bragging mortgage brokers in “The Big Short” who end up looking for jobs at IKEA.

Re: The $500K brokers…. I’ll bet they lived a $500K+ lifestyle until it all collapsed. Smart people stay the course when their income goes up. You never know when it will do a hard turn for the worse. If you built a nest egg, it’s not quite as painful.

I have a friend who bought out his parent’s construction company. Things were going swimmingly. He bought everything in sight. Has a $6M sale proof house (at least he has it for the moment until he defaults on the loan), a building (with no business in it), scads of construction equipment (that he can’t sell), an ocean going racing boat, and a $3M++ judgement against him (remaining after the confiscation of all their bank accounts) because he let his ego get in the way of common sense and survival instincts. I watched them do this multiple times (restaurant investment that went sour, condo conversions just prior to the great recession, and a bunch of other get rich quick stuff. Every one of them had the same outcome. A shipwreck.

Storybook case of how not to enter your 50’s with three kids in college (none go to a state school because that wouldn’t be cool enough).

Which indicators are showing a recession?

Harold,

Probably different for everyone although I don’t consider myself a pessimist. I’m a Marxist/Leninist so I am against the nature of a system that by definition has class warfare and many contradictions. I follow here because I exist as part of the system and honestly most of Wall Street is, as people see it as some abstraction, is simply a set of institutions and the people working for them are just trying to support themselves and their families. So I root for the rise of the working class but material conditions really don’t exist for change here in any way and people consider token reforms as victories. But I must be pragmatic with my money as my children’s college and health care and so on isn’t something society prioritizes over imperialism and profit for the few.

Not trying to convince anybody of anything, just trying to answer your question.

‘I’m a Marxist/Leninist so I am against the nature of a system that by definition has class warfare’

Now that is odd, to be polite. The WHOLE basis of Marxism is the class struggle or in other words the clash of labor vs capital. See ‘Das Kapital’

They explicitly say that, so it would be interesting to see the reaction of the faithful to a comrade who is not interested in the class struggle. That’s why the first target of the various revolutions has been the

landlords, money lenders, etc. They then go on to sweep up all ‘rightists’, e.g., the liquidation of the kulaks, Russia’s peasants.

Could it be possible that you are a socialist, another target of the hard core Marxists? The original Russian Revolution was by a coalition of leftist groups, including the Peasants Party, led by Kerensky. It was then overthrown by a small violent group, led by Lenin.

PS: the group was the Bolsheviks

Not even clear what you definition of hard core Marxist is. Fascism in Germany was who went after communists and socialist as those were the first concentration camps. Interesting how all that same language is coming around again via US politics. Marx rarely used the word socialism except when criticizing utopian socialism, which is all but gone now. The concept of being a Leninist is the belief that revolution is required as those in power do not willingly give up that power. The material conditions would dictate what that might look like in any country. That said, I was simply answering a question about why people are pessimist, not looking for a reductionist view of the Russian revolution.

Any political definition is the same Marxist ,communist,,democracy. The money always goes to the ogliarchs .

‘A very basic principle of the Marxist theory is the theory of class division of society and class struggle. According to it, each society has the oppressors and the oppressed and the oppressed are eventually bound to revolt and build a new society and economy.’

From Study.com

To self describe as a Marxist but not subscribe to above is simply to have a private language.

Not clear how you interpreted my comments as anything other than that.

People worship Karl Marx as if he were some sort of god. Let’s assume that’s true, he is still the biggest failure in history for shamelessly leaching off of his own mother and instead of doing ANY manual labor his entire life, waited for “the old hag to die”.

Rasputin felt compelled to meet the man he first saw in a painting, this Karl!

There you have it, the eternal champion of the working man, who’s best friend was a millionaire and hated the company of working men.

I find actual humans who are Marxist/Leninist’s to be such amazingly smart yet dumb people. As a feel-good intellectual exercise, I understand the alure but as a practical matter and with all evidence of human history how does one accept that this is their worldview? It’s a failed ideology which has caused more misery than it purports to cure and ignores that the world is in a golden age as we read this, largely because of a market (EG Capitalist) system.

… and Marx’s megalomaniacal adolescent poetry was atrocious!

Harrold,

You ask – “Why is there so much pessimism?”

Pessimism or optimism has little to do with accurate economic or investment analysis, so I’m curious why you ask about it. If you believe the economy will enter recession or asset prices will fall, or you believe the opposite, these should be a cold hard conclusions based on analysis, not emotional bent.

Actions based on emotion are what cause bubbles and markets that can drop 50%.

Arguably, Fed leadership has done the most damage via emotional decision-making. Their actions suggest an irrational fear (of recessions) and irrational denial (believing problems will simply go away in the future). So, unfortunately, highly emotional decision-making has become institutionalized.

Of course, Wall Street understands this, and they’ve built a huge propaganda machine to manipulate the Fed and the public into acting irrationally. As Wolf points out, the overwhelming majority of main stream media “analysts” today, even at a high level, are simple propaganda conduits.

Why cut rates? Obviously, we want looser monetary policy to pump my crypto bags and real estate prices.

Accumulated risk assets for a while now. Let’s pump it baby! Bitcoin 100k!

Rent is too damn high

I’d like to say why I’m pessimistic.

I’d like to buy a home for my family at a reasonable price. I make 3X the median household income (which doesn’t include welfare) for my zip code and have no debt. I’d like to pay cash or maybe would tolerate a small 10 yr mortgage. Should be easy with my high income, right?

Prices of homes are insane and increasing faster than I can save up for them. Yes a lot of people i know in this town have bought homes, if I ask them about it they have all admitted to me they have huge mortgages.

Then we can talk about WHY the prices of homes are so insane, which rapidly leads to understanding that there are Unconstitutional govt (and FED) programs drivingc up the cost of homeownership, and the Fed/Fedgov keeping interest rates lower than the rate of increase of the fake currency supply. Finally, most people in their stupidity ardently support the Unamerican fed-worshipping status quo. It’s all very annoying idiotic etc.

… and similar thoughts and frustrations about education, healthcare, transportation, food – ya know, basically everything my family needs and wants is being messed with by abusive governments and >50% of the people are in favor of heaping ever more abuse on themselves and the rest of us along with them.

Now there are some things to be optimistic about, but that’s another discussion, and I have a different pseudonym for that.

“I’d like to pay cash or maybe would tolerate a small 10 yr mortgage. Should be easy with my high income, right?”

lol. So entitled. I don’t feel sorry for you. You live in a fantasy world.

Where does this expectation come from? Avg income doesn’t mean anything. Btw Those that are supposedly make avg income get paid under the table (contractors, waiters, etc) and make way more than avg.

They won’t cut rates.

They will probably have to raise them ,considering the amount of money this government has to borrow.

When you have such a deficit,you just create artificial growth,this is why we sould not expect a recession.

This is just temporary,before the elections.

Then you realise that debt creates less and less growth.and that raising the rates are destroying the economy.

That’s what I’m thinking. The real driver of interest rates has to be the debt. If not now, it will be soon. Wall Street should be betting on whether government has to raise or lower rates based on paying the interest on the debt.

I don’t see why they would cut rates. Doesn’t make sense. Food is still costly. My health insurance was raised almost 30% starting in March and I have to look for a new policy. Started working part time doing gig work to supplement my rentals income. My tenants are working extra to make ends meet. I still jobs advertised so I don’t see a decrease.

I have an Indian friend (India) and he tells me the Indians in tech are buying homes 600 grand and up-no problem. These guys work in tech. I checked the area where I have my rentals (lower income) and some prices dropped, but nowhere even near to 2008 crisis. That was an incredible. drop. The areas in MT, ID and WY that I’m looking to buy something have not dropped much. People still holding and price per acre is not cheap at all. Where I am finding value is purchasing a place out of America (not telling you where) where I can get citizenship.

I think Powell should just STFU and say we are staying the course or will go up in rates if economy starts overheating. The FED is America’s second biggest fiscal enemy behind Congress/President.

“They won’t cut rates.

They will probably have to raise them ,considering the amount of money this government has to borrow.”

Not necessarily. Treasury auctions will determine the price the government pays to borrow. The Fed overnight rates has influence, sure, but if .gov needs to borrow a lot (and they do), the primary driver of price will be what the market will bear.

Yes,this is what i said.The more they need to finance the deficits,the more they need takers for their bonds.

If it’s not the FED,then they need to find more and more takers for the bonds.

That should push the rates up.

Wall Street forced the Fed to cut rates in 2019. IMO They are going to do it again. Will it be terrorism somewhere different in the financial plumbing, or will another regional bank suddenly get torpedoed? Keep your binoculars on lookout for barely reported news about these going forward.

Back then (2019), inflation was BELOW the Fed’s target. Now inflation is at twice the Fed’s target. Everything has changed. You have to go back 40 years to make comparisons.

I agree there is not rational reason to lower but still to be seen if there is a rationalized reason. Hopefully they just go off the numbers. This is a decent time for most so keep it going, keep investing in manufacturing, and so on.

Exactly. Rationalized is what worries me. Time will tell. Until such time, I’ll remain cautiously optimistic.

Yes. Man is not a rational creature, he is a rationalizing creature.

It will be interesting to see the pay raise data come the first quarter of 2024 when most corporations give their employees a COLA. Putting that on top of already strong wage growth is going to have Fed Governors reaching for the Pepto Bismol.

Perhaps you can write them a new jingle. “When you’ve got low unemployment, rising wages, services inflation….”

You funny!

Dozens, nee hundreds of TV options. Everyone is watching something different but we all see the same flipping commercials.

Starting in April, 500,000 fast food workers in CA will get a raise to $20 from about $16.41. While of a course a relatively small percent of the workforce it will increase prices more than likely as well as wages obviously. Other laws in our state are boosting wages for healthcare workers and others, not to mention the settled “Hollywood” strikes which are getting a large industry back to work. Plus new jobs for pointless rail projects here which will kick in over time.

I hardly eat out, but went to El Pollo Loco which is a California fast food Mexican a step above Taco Bell. That burrito that used to cost under 10 bucks is now 12.50 or so. My eyeballs popped out of my head when I saw the menu price thru the drive thru.

Bought a bag of frozen Chimichangas for under 20 bucks that aren’t too bad. That’s my answer to that price increase. Prices are going up in segments if you’re paying attention, but add it all up over the last several years and it’s been brutal.

Should have gone down there road to Pollo Hermanos…

They should change the name to El Powello Loco.

Go to a Chipotle….. $20 for a fast food feast that looks absolutely nothing like the pictures.

Most fast food is very unhealthy, too, so people are paying a lot now for poor quality, to then have to pay a lot more in the future for the resulting health problems. Some burgers don’t even come with lettuce, tomato, onion, etc. If we don’t want to eat veggies now, our body won’t be able to work when we get old. And now we get Cos Mc’s. Overpriced sugar and caffeine bombs from a drive through only. McDonald’s seems to be doubling down on unhealthy products.

“…there are three basic components comprising product quality: fast, good, and cheap. You may select two, the non-selected component being your product’s lacking quality variable…”

-anonymous

may we all find a better day.

3.7% unemployment combined with a 7.3% budget deficit is pretty much guaranteed to have the Fed governors reaching for the Pepto Bismol

2024 is an election year is it not?

Pretty incredible. Most countries are the world would be pleased with those charts…

So, you have been Pavlovian trained by Wall Street and the Fed to believe that 5% on FFR is high and how can the economy bare these high rates. Actually, these rates will wash out the garbge and keep fantasy-land investing and risk taking somewhat grounded. Will be better for the economy if rates stabilize arounf the 5% FFR and gvts and corporations realize they need to be fiscally responsible!!

This is not a “pivot rally”; it’s a “soft landing rally.” The Fed pulled off a soft landing in the mid 90s (The Maestro’s magnum opus). This required a few insurance cuts in 1995-96. If history repeats itself (or rhymes), it’s stock-buying time.

Yes, someone always has to buy, or else the people that want to sell cannot sell. Every share sold must be bought by someone. The job that buyers have is to allow sellers to sell.

Buying and selling goes on all the time.

But the Question is at what price?

Rick Rider (Black Rock) and Mohamed El-Erain (Allianz) on Bloomberg on Friday morning GUESSED that the Fed might cut the Fed Funds Rate by 100 basis points in total in 2024 beginning in June or July.

So from that I guess that they do not see any large dark clouds anywhere near.

This right here.

First time in awhile I find myself disagreeing w El-Erain.

Fed can’t cut as long a inflation remains >2%.

El erian has been begging for rate cuts for quite some time.

He has been using fear mongering tactics asking for ratw cuts and has been very harsh in fed for such aggressive hikes per him.

Very difficult to get de addicted from cheap money.

You can guess where is he invested.

I came across El Erian interview pleading FED to increase their inflation target of 2% to 3% or so. The reasons he cited was: things have changed fundamentally and thus higher inflation is structural in our economy. Thus he wanted FED to increase their target.

He has been a vocal critic of FED for their fastest hikes done.

I tend to agree. My feeling is that Powell is a spineless coward, and would be happy to inflate asset prices as long as he can pretend he’s doing something else.

If he cuts rates with inflation significantly above 2%, he loses that plausible deniability.

It would be an implicit admission that the Fed has abandoned the 2% target.

I also think geopolitics is a factor – the Fed wants to ‘out-hawk’ other central banks by keeping UST rates higher than bond yields. In doing so the Fed is defending the dollar vs other currencies.

Case in point: look what happened with USDJPY when the BOJ teased the idea of higher rates.

…keeping UST rates higher than local** bond yields…

So many moving parts. Baby boomers retiring, birth rates historically down, people (labor) becoming more valuable as globalism dies, interest rate putting banks, indebted corporations (most), a govt that now spends on debt service than defense-all on the verge of collapse…. Interesting times

Rates are up because FED ,can’t borrow money on world markets ,so second best get it from Americans. This will end BAD

Congratulations to all of you Americans, truly world leaders, the envy of all others and constantly proving that capitalism is the only way to wealth and freedom for anyone who chooses to educate themselves and work hard. Long may it last, your businesses and currency are the only place I will invest in, all others are bleeding heart socialists or communists destined to sure failure.

🤣😂

Not sure what a bleeding heart socialist is unless you are implying social democrat and of course they aren’t on the left but hopefully one day we can meet and I can buy you some vodka and sunflower seeds. Great comment! Sarcasm without the need for /s is always the best.

Here in BC Canada we have a whole bunch of self described ‘social democrats’ who at the moment form the government: the NDP. They would all describe themselves as ‘on the left’ or possibly ‘center left’.

True, and same in the US but it doesn’t make it so. Outside of fringe groups the most left we get tends to be Bernie and he is not left relative to the definition. Admittedly I have nothing against reforms as improvements for the working class are never a bad thing but they also tend to be transitive and just the right amount to make the working class content. The recent strikes were a good example of this and of course best wage increases in 40 years. In any event this isn’t where I participate in these types of discussions as I find Wolfs data driven analysis interesting in the same way I find dialectical materialism fascinating, but I do that elsewhere.

Yep the big salary increases from the big 3… as they shutter plants for “retooling”. It wouldn’t be a wild bet that the “retooled” factory launches under another corporate umbrella and assembles EV’s without the need for either a dealer body or the UAW.

You’re always better off with a stable job that pays decent wages than shooting for the moon and finding yourself in the street with your belongings in a box when the company deems you highly paid but replaceable “associate”.

You are welcome!

TEF,

Wow! As an American thank you for the kind an encouraging words.

I have read that Zi once asked Biden (when they were Vice-Presidents) to explain America. Biden said I can do that in one word, “Possibilities”.

I agree. America is constant and great change. Living in it is often bewildering/worrying but I think it makes us strong/safe.

Lol you think he’s being serious??😂

Our country is pathetic and if you can’t see it for what it is all I gotta say is….

Bahhhhh

🐑🐑🐑🐑🐑

American Dream,

You said, “Lol you think he’s being serious??😂

Our country is pathetic and if you can’t see it for what it is all I gotta say is….

Bahhhhh”

You are possibly right. The thought occurred to me but I decided to believe he was sincere because cynicism is a mental disease. You should consider this.

I agree there is no logical reason for the Fed to cut rates, but when you look at the last 15 or so years, it’s no wonder people are skeptical. Ultra low interest rates and QE being used when not needed makes it difficult to trust the Fed. Also, Powell ruined his credibility with his inflation is transitory stance. I hope this is a changed Fed that will do right by the American people, but I’m still on the fence. We shall soon find out.

The last 15 years are the anomoly, not the norm. The bond bull market ended in 2020 and rates will keep going up. I’m literally betting on it.

The Fed shouldn’t have done years and years of QE and interest rate repression after the GFC, but it did. The Fed shouldn’t have cut QT short in 2019, but it did. The Fed shouldn’t have done QE and ZIRP in response to the pandemic, but it did. The Fed shouldn’t have continued to do QE and ZIRP long after its absurd market distortions became clear in 2021, but it did. The Fed shouldn’t have bailed out tech gazillionaires’ massive uninsured deposit accounts earlier this year, but it did.

Those who are betting on the Fed to cut rates next year may or may not be wrong (I suspect they are wrong), but their reasoning is not necessarily unsound. It’s simply not that unreasonable to expect an institution with a decade-plus history of doing the wrong thing over and over again to…do the wrong thing again.

Correction: The Fed itself didn’t bail out those tech gazillionaires who couldn’t read the plaque on the door of the bank, that was part of a plan jointly conceived by the Fed, the Treasury Dept, and the FDIC. I shouldn’t have included it in a list of the Fed’s own screwups. So instead I’ll add one that I had left out:

The Fed shouldn’t have assured investors, that it would keep rates near zero for years to come, thus encouraging investors to take on duration risk that blew up on them when the Fed panicked and reversed course, but it did.

I think the biggest issue is that people can’t seem to think beyond a 10-20 year timeframe. Look back long enough and you start realizing things tend to move in a 80-100 year cycle. This is especially true politically, with a major war every 4 generations.

I’d posit we’re just finishing up winter (financially), now comes spring and with that comes spring cleaning.

In Roman days, during the darkest time of the year, they would celebrate Saturnalia – a holiday where everything was upside down and everyone basically went crazy.

This is what this entire QE/ZIRP era was, our societal Saturnalia. The party has ended, but people are still somewhat slow to see daylight is coming back. And as light comes back, so too do people have to sober up again to reality.

Depth Charge Thanks for speaking the truth

Totally correct

Since the Wall Street establishment always wants cheap money, they forecast low inflation or ignore signs of sticky high inflation ( like the wage increases in the payroll number). To then push the Fed to ease.

I saw little to nothing from the Wall Street commentators on this sticky high wage increase.

Chris Waller even came out last week stating that if inflation comes down the Fed would then lower rates.

Music to Wall Street’s ears. He must be angling for a lucrative Wall Street job.

Wolf makes a good point, and no one is talking about it because they don’t want to.

But no way the Fed cuts rates 5 times next year

I can only think of two reasons, and they are weak ones:

1. To head off a crisis in the Commercial Real Estate sector.

2. Perhaps to prevent a repeat of Silicon Bank. Looking at the BFTP program, it offers “offers loans of up to one year in length to banks, savings associations, credit unions and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities and other qualifying assets as collateral.” Isn’t the one year anniversary coming up in April?

Honestly though, the Fed can always introduce a ton of other programs to bail everyone out. This time around, everyone will be a winner, guaranteed.

Bank Term Funding Program

121 Billion and continued outflows from banks to govt paper

The trend is disturbing, I suspect, to the Fed.

For some banks, the BTFP is just a less onerous way for banks to borrow than offering 5.5% on CDs to attract or keep funding. It’s a pretty good deal for banks, much better than the Discount Window and some other options, and so they use it.

BTW, $121 billion is nothing for the huge US banking sector with 4,000 banks that together have $22 trillion with a T in assets.

That is concerning. If banks are increasingly getting financing from the government (the Fed), banks become more dependent on government action and more insulated from market forces. Odds for bank bailouts increase.

If its small and doesn’t matter, why even do it? I say make them go out to market and attract CD money. Perhaps that is the plan and the reason why they put a one-year term on it.

That’s my thought as well. Also 121 billion discounts the possibility of contagion. Remember when subprime “was contained”? Pull the support and we’ll see if banks stop lending to one another, then we’ll see the true picture of the US banking industry. I mean, everything could be swell, but I think 121 is an underestimate.

SocalJimObjects,

“…and we’ll see if banks stop lending to one another,…”

Interbank lending in the US has withered since the Financial Crisis. In terms of contagion, that’s a very good thing. Interbank lending went from $450 billion in early 2008 to 70 billion (-85%) at the end of 2017 — $70 billion in a $22 trillion banking system — and at that point, the Federal Reserve Board of Governors stopped tracking interbank loans on its H8 as a separate line item but combined that with some other activities, maybe repos, can’t remember.

Interbank lending was still reported as separate line item for Nov 2017:

https://www.federalreserve.gov/releases/h8/20171222/

And it was no longer reported as a separate line item in Jan 2018 — this was of course announced and explained at the time:

https://www.federalreserve.gov/releases/h8/20180209/

The reason why the labor market is strong and wage growth is accelerating is because the printed money which was originally concentrated in the original receivers is now, still, in the process of spreading out into the economy at large i.e. historic QE is affecting a delayed stimulus.

At some point this meets tighter financial conditions for debtors in the private sector.

Thanks Wolf,

So now the rate cuts or interest rates shouldn’t even be mentioned anymore. Higher for longer said by Powell makes me think it’s all QT from here as the tool for now. Last hike was July. PCE at 4.6 and CPI at 5.5. I believe Wall Street knows what’s coming with the Fed shrinking its balance sheet. Higher for longer stays the same. 5.25-5.50 by the fed. What the interest rate on the curve says I don’t know.

The gubment spends three trillion dollars in new debt and that labor market just keeps going.

Amazing.

It’s a miracle.

Chicago spent millions on a tent city for their illegals…then tore it down

Look at all the govt funded jobs!

Broken window economics and Taylor Swift concerts

Earlier this week The Duran with Alex Christophou and Alexander Mercouris show entitled ‘Let’s talk about some news’ , Alexander said the U S. may as well elect Taylor Swift president.

Taylor Swift who made a song about how much better her life would be if she were a man ?

I mean, she could be a rock star ! And get filthy rich !

Stocks like NVDa are pricing in growth for the next five plus years. Not sustainable

The markets are similar to tech in 2000. The stocks fall on their own weight .But party on Garth

Party on Wayne!

And then after they price in the next five years, they’ll price in another five. And after they do that they’ll make up another narrative and price in five more. That’s what happens when the FED just prints money and hands it to cashed up oligarchs who turn the entire economy into a speculative orgy.

And just like the dot com bubble this bubble to will pop but I think we’re still in the 1999 part of this comparison. More bubbling to come before the drain gets pulled. Time will tell

The most dangerous wealth destroying economic statement…..

In the long run………this statement is implied in all sorts of internet based economic advice columns.

History tells us that in the long run there is no long run. Most of it is about tomorrow.

because things change in ways very few can anticipate.

Even the famous statement….in the long run we are all dead is starting to be challenged by modern science.

So……listen to the facts and make your own evaluation and don’t listen to the constant drum of advice from the internet.

This Wolfe site is a perfect example of a great source of unbiased facts being placed in context. Take what you need and apply. You will do better.

Don’t be afraid to invest. If you listen to the internet you’ll kill yourself to avoid the long run.

Just trying to help the younger crowd.

I agree that people shouldn’t in general be afraid to invest. But putting money into obscenely overpriced stocks when you can get 5.3% in treasury bills is the height of recklessness.

Everything in moderation…… The 5.3% can evaporate just like it has before and stocks may continue to climb. Or not. No one truly knows.

What? Once you buy a treasury, the coupon payments are fixed for life, and you cannot lose your principal if you hold until maturity.

Jackson Y –

Einhal specifically said treasury *bills* which are zero coupon. You buy them below par and get par back at maturity.

They’re also <1year in duration, which is what El Katz is referrimg to by "The 5.3% can evaporate just like it has before" (although I personally disagree with the assertion that rates will go down).

Nothing against your comments, however, I remember a gentleman telling a young me the same thing in 1973. If you buy at 1000 Dow you are a fool he said. It’s true, the dow dipped to 574 a year later……but…..I wished I had put every dime into the Dow at 1000.

The point is, growth will outrun even the worst timing.

Believe in the USA.

Yo, Fed,

Except you couldn’t just buy the Dow back then. Index funds were just getting started, not really available. But I get your point and agree.

This is me. I have cash accumulating risk-free interest. I’ll get into stocks when the party ends and people are afraid. Right now there is still too much music.

Consider the following:

The Fed has spent the last year saying “no rate cuts while inflation remains above our target.”

Inflation remains well above their target (despite the rate of price increases having slowed).

If the Fed cuts while inflation remains >2%, its an implicit admission that they’re abandoning their inflation target.

This could cause the Fed to lose control of the long end of the curve, as longer bonds reprice down & yields spike. The Fed does not want this.

Ergo, the Fed /cannot/ cut while inflation remains >2%.

Price of Gas has dropped significantly. Big input consideration.

We’re still above their target and they haven’t cut rates either.

Why won’t anyone believe the fed. They’ve been doing exctly what they said they would do for over 2 years now?

People don’t believe the fed because they don’t want the party to end. Nothing to do with logic or reason, just simple greed and addiction to easy money.

Keep in mind that many people today only really know a low-interest rate environment. The idea of hard-earned money is anathema to those who only thrive in an easy money environment.

‘…one doesn’t know what one doesn’t know…’ (paraphrasing one our past leaders), or, if having acquired some unease at the possibility of an advancing dark, might begin to whistle, loudly…

may we all find a better day.

That’s not what they said. Powell said they may well cut before the annualized (last 12 month) PCE number reaches 2.0%. Because by then they would have overshot their target to the downside.

He also said as inflation declines, leaving rates where they are is equivalent to tightening.

Do you listen to his press conferences?

I think you’re misinterpreting this quote:

“The next question will be for how long will we remain restrictive? We said we will keep policy restrictive until we are confident that inflation is on a sustainable path down to 2%. That will be the next question. But honestly right now, we are tightly focused on the first question.”

He’s talking about the general restrictiveness of monetary policy – NOT specifically rate cuts.

Howdy Folks. Less than 100 billion to go. What a mess THEY have created.

Looking at the chart, the current report is at good time levels but the trend line is different – flat during “good times” and trending down now.

The graph for multiple jobholders that’s a function of the real or true inflation rate minus the Fed funds rate which is positive. The news media spins this as being negative but the inflation rate is being understated. The longer it stays positive the poorer everyone will get and the more jobs they’ll have to work at the same time.

In my humble opinion, the FED under Jay Powell has been brilliant! Consider, normally the FED responds to data points as they appear in the business cycle. In 2020, the 25 trillion dollar U.S. economy as well as much of the world’s economy was basically SHUTOFF. Clearly that was a mess to navigate and they seem to have done a brilliant job of it. I would expect there would not be a rate cut any time soon UNLESS there was a black swan event. (think 9-11 or similar).

Howdy Louie. Don t forget Pow Pow raised and then lowered during the Trump Presidency. Our one party system does silly things …….

Yes, Covid-19 changed everything including perception. For the typical wage slave it was in a weird way kinda nice to not work, get government money to survive, and now they are questioning whether going back to being a wage slave is a good thing. No economic theory required.

If you’re not being sarcastic, you’re deluded.

There’s nothing brilliant about printing money. It’s a trick as old as the hills. All it does it is forcibly confiscates people’s savings, without any need for legislative action. In the long run, it kicks the can down the road, and postpones any hard decisions.

The only reason we can sort of get away with it is because we’re the reserve currency.

When nations like Argentina try it, they get hyperinflation.

I thought I mentioned the once in a lifetime (hopefully) shut down of the 25 trillion dollar economy. Drastic times call for drastic measures. I’m glad they were there to do what was necessary at the time.

Yeah, and next time it’ll be a shutdown because of war. Governments can always find an emergency to justify immoral actions.

They did way more than what was necessary. The costs of the response, if any, should have been borne by society as a whole. Not merely by cash holders. Taxes should have been raised to pay for it.

The shutdown was one of the dumbest, most unfair moves in history, with zero benefit whatsoever. It did nothing to control the spread of the virus.

What it did do, however, was destroy countless small businesses and their respective owners, and hand those customers to the mega-whales like Walmart, etc.

They told the local furniture store they couldn’t be open, but allowed people to cram into Walmart, shoulder to shoulder (that’s super fricking healthy to control a virus spread), and buy their furniture. “Necessary at the time” my asz.

Louie,

Are you serious? You are suggesting a 25% inflationary spike was unavoidable.

The Fed could have handled the crisis a lot better by withdrawing stimulus a lot sooner than it did. Approximately $5T of helicopter money was printed in 2020/2021. Common sense says that’s going to raise price levels by at least $5T (20% to 30% inflation) across the economy, particularly in an environment of constrained supply. Yet, as prices started rising, the Fed said it was transitory, which allowed the inflation to continue until the full $5T increase in money supply embedded into price levels and GDP. Even now, the Fed piddles as the inflationary spike rises from 20% to ??????.

Even more alarming, they kept buying MBS in the face of a quickly inflating RE market, AFTER prices had already skyrocketed by 100%-300% the past decade.

If that is brilliant performance, the scale needs to be recalibrated.

The shutdown took out 40% of the small business in the DC Metro areas. Small business were forced to close while the big box stores were allowed to stay open selling some of the same merchandise. The small business lost all their customers and many were forced into bankruptcy. Good job from the government.

Argentina is certainly in a world of hurt. Even Brazil is feeling sorry for what is happening there, although of course Brazil has its own struggles on the horizon but likely not on the hyperinflation front. For whatever reason I find South America fascinating as not sure why. America in 50 years might start to begin to go where the UK economically is currently at and that is very unlikely but not a lot of parallels I can see to South America outside of the generalization of a political pendulum.

Spend some time in Uruguay – you’ll never want to come back. Lots of upside to moving there if you can maintain your US income and/or move it offshore.

There are a few on here like that. They are either clueless or trolls.