Wages of production and non-supervisory employees accelerate for third month to 5% annualized. Turns out, the big drop in August was a head fake.

By Wolf Richter for WOLF STREET.

The labor market in November showed once again that it refuses to kowtow to Wall Street, which has wanted a decline in the labor market along with a recession that would force the Fed to cut rates, and this has been going on since about mid last year, but now it has reached a crescendo with rate-cut bets for 2024 that would assume a plunge in the labor market. But hilariously, the labor market just keeps on plugging, and the crazy gyrations during the pandemic caused by labor shortages and other issues have settled down.

The number of working people jumped, the number of jobs created rose more than feared, the labor force jumped, the number of unemployed people fell and was low, the unemployment rate fell and was low, the employment-population ratio rose…

So this is a labor market that is in pretty good shape, in amazingly good shape actually, given the interest rate environment. It’s roughly growing at similar and higher rates than before the pandemic, despite the interest rate environment.

With the labor shortages and gyrations during the pandemic having settled down, one would expect wages to slow their growth in alignment with this normalizing scenario, but they did not.

Fed trigger point: Wages

Wage growth accelerated. And as recent labor actions have shown – they won massive increases in wages for 2024 and future years – wage growth might just be the thing that doesn’t cooperate with this normalizing scenario.

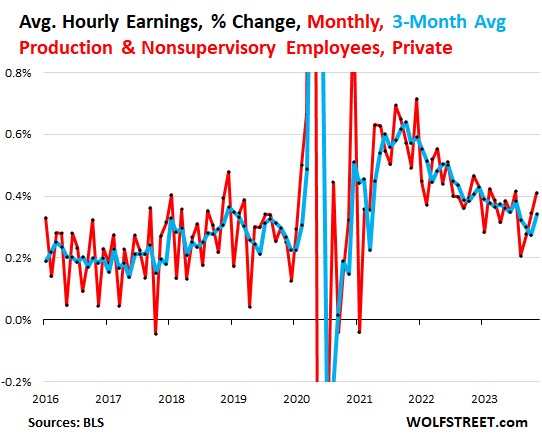

Average hourly wages of Production and Nonsupervisory Employees in the private sector jumped by 0.41% in November (5.0% annualized), the third month in a row of acceleration, after the low point in August. This puts November wage growth at the upper end of the range since late last year (red line in the chart below).

These “production and non-supervisory employees” include working supervisors and all employees in nonsupervisory roles, such as engineers, designers, doctors and nurses, teachers, office workers, sales people, bartenders, technicians, drivers, retail workers, wait staff, construction workers, plumbers, etc. This is the bulk of private sector employment.

The three month-to-month accelerations in a row cause the three-month moving average to jump to 0.34% (blue line).

Note the big deceleration in August to 0.21% growth, which has now turned out to have been a head fake.

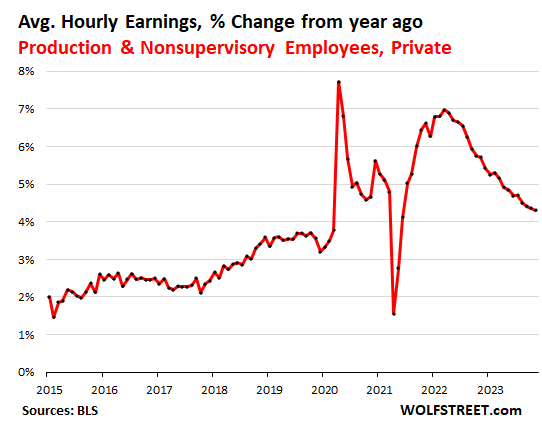

Compared to a year ago, average hourly wages of Production and Nonsupervisory Employees decelerated to a growth rate of 4.31%, down from 4.36% in the prior month. The deceleration largely stemmed from the month-to-month head-fake in August.

On the verge of a year-over-year U-Turn.

- Another month of 0.41% growth, so in December, and the year-over-year growth rate would be stuck at 4.3%.

- And a second month of 0.41% wage growth, so in January, and the year-over-year growth rate would rise to 4.42%.

In other words, year-over-year wage growth, with another two months of this type of increase, would be U-turning and heading higher.

Month-to-month wage growth is very zigzaggy, so it’s unlikely it will produce three months in a row of the same month-to-month growth figure. Instead, it will zigzag. But the last three months showed that the August zag to +0.28% was a head fake, followed by three zigs.

Month-to-month wage growth is now back at the upper range where it had been earlier this year and late last year. It got back to that upper end of the range by re-accelerating three months in a row, which it hadn’t done since early 2021 during the big gyrations. And this upper end of the range is an annualized wage growth of 5%. And for the Fed, this kind of wage growth is not compatible with inflation decelerating toward 2%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

After today’s report, markets are STILL pricing in a 45% chance of a rate cut in March.

Stocks have gone up on every jobs report after the Federal Reserve’s most recent (final?) rate increase in July. If the jobs report is hot, the headlines say “stocks rise on strong economy & soft landing hopes.” If the jobs report is cool, the headlines say “stocks rise on rate cut hopes.” Either way, it’s win-win for the markets.

I’m thinking maybe stocks only go up? I mean, if a worldwide shutdown of the economy didn’t meaningfully crash markets, nor the Ukraine war, nor the fastest rate hike cycle in whenever, then maybe it’s true that stocks go up.

When the FED prints money at the drop of a hat, of course stocks only go up. But it’s not stocks actually going up, it’s the value of the dollar and your labor going down.

The Federal Reserve does not own a single stock.

Usually the type of comment that identifies tops but it’s been a relentless several weeks.

Next year will be quite different imo. Bit higher in the first part I’d guess but should be getting fun around election time. Time will tell

Perhaps a dumb question. How do we know markets have priced in a rate cut? Admittedly the market have been up, albeit below the highs from years ago, but the idea some rational decisions have occurred in the market seems ambiguous at best for a specific rate cut date.

Finally after a month of horrible news some good news today.

Look at a long term chart of the DOW up to the year 1993 and throw out all the rigged malarkey the last 30 years and draw a trend line through it to the year 2023. That’s supposed to be where the DOW is today.

Look at the last 30 years of Federal debt and M2SL and overlay it with your Dow 30 chart and you’ll see why the Dow is where it is. It follows debt/money supply pretty well.

The T-bill markets show it much more obviously

There are federal funds futures, a type of financial derivative that enables investors to bet on the direction of interest rates at upcoming FOMC meetings.

Who knew that more people working and people getting paid more would be so upsetting to so many investors.

I believe you’ve long been mentioning the fed holding rates at the current level for 13 months wouldn’t be unheard of, might be a good call.

I think it really upset the economists. High interest rates are supposed to drive unemployment up and have done quite the opposite.

Imo the interest rate raises aren’t having any effect other then paying more interest into the economy via fixed savings vehicles. They really only cut off demand on the lending side with higher rates but with fiscal policy so far the other way the actions by the Fed are negated plus some clearly

The Fed has no control of the situation and is flying blind. Fingers crossed inflation comes down. Jobs report confirms again that won’t be happening anytime soon. Higher for longer.

Wolf,

Is it correct to say that inflation is firmly entrenched in services and still the economy is chugging along? How could a pivot be even be possible? I assume the $2T in extra spending has been factored by the markets. Higher for longer? Patience? I feel lost in this situation.

The people who talk about a pivot (rate cuts) starting in Q1 are those that desperately want rate cuts, and lots of them, and asap, and they bet lots of money on those rate cuts, and they’re now out there hyping their book. The Fed isn’t talking about rate cuts.

I too feel nauseous when hearing the pivot-crowd.

Given everything we’re seeing right now as a direct result of interest-rate manipulation, moneyprinting, insane deficitspending, massive levels of debt and reckless stimulus….they are rooting for MORE of this, regardless of the damage to society and the rising inequality.

It would be awesome if every time a billionaire started yammering on about rate cuts, etc., they got the physical sensation of a baseball bat to the kneecaps. I mean, you’ve got enough money, pig man, go spend some of it instead of crying and annoying me.

“go spend some of it…”

NO! That’s inflationary!

Give them the same taser zap we want for dumb questions at the FOMC pressers LOL

Wolf, off topic but thanks for the first chart. It was beautiful to see the difference in the color of the two lines.

Red/green deficient makes all kinds of gyrations in order to distinguish between the lines. Either do them or ask the wife the colors.

With the unemployment rate at 3.7%, there is zero incentive to even entertain the idea of a rate cut; and wall street is currently delusional. There is zero recession anywhere close to the horizon right now with the labor market where it currently is. This is a new environment post covid and people (analysts and economists) continue to pound their desk screaming recession and depression and look at old meaningless charts that have zero bearing and zero meaning in todays environment which is a completely different environment than pre covid.

I heard someone say this earlier today. The wrong question is, its not when the Fed is going to cut, that question is meaningless. The important question is, WHY the fed should actually cut?

The job market is beyond fine right now. So the Fed can focus on inflation and more importantly, core inflation and services inflation which is still double the Fed target. The Fed is not going to cut now or anywhere in the near future with the way things are currently. When the job market changes and when it actually looks like a recession besides a meaningless inverted yield curve and a bond market that has been dead wrong for years, there is something more to talk about.

There is zero WHY the fed should cut rates in March, June, or next year at all right now. The fed can just sit back and let things play out for a long period of time to fight inflation. The last thing the fed needs to do is cut early and cut too fast to early and let inflation come roaring back. Team transitory and team zirp policy has already made things beyond bad. With a 34 trillion dollar US debt and rising fast, the last thing the fed needs to do is screw up inflation a 2nd time around by cutting to early.

The odds should be in favor of zero cuts next year or maybe 1 at the back end of the year.

Thanks Wolf,

Do you think this is where The Fed expected things to be given where rates are at? It seems today’s report was a surprise (to the financial press anyways), but I’m wondering if Powell and company were surprised too and if that will cause them to raise rates another 25bps. Guess I’m just not sure this is what the Fed was aiming for at this point.

I don’t think the Fed was surprised. Powell has long talked about the strength of the labor market the “head fakes” inflation dishes up. It’s just that Wall Street isn’t listening to anyone at the Fed. They just fabricate “Powell was dovish” and run with it.

Simultaneously relieved and disappointed, I’d guess.

Relieved that their command economics has fulfilled the employment mandate.

And at the same time, a recognition that full(er) employment can lead to wage pressures, and potentially the dreaded “wage/price” spiral, where inflation expectations enter the fray.

Perpetual watch-a-mole.

Perhaps that’s what Arthur Burns meant by the “Anguish of Central Banking.” He described many of the issues we face today in his 1979 speech by that name. (Find it by googling Fraser + the anguish of central banking… 12 pages, and very well written).

The price spiral seems to be unravelling a bit. Tesla keeps cutting the price of their cars and the excessive dealership markups seem to be disappearing.

Even housing prices are decreasing in several markets.

Apple-

Despite autos (and food and fuel, too), the overall YOY 4% inflation print is still 100% higher than the 2% target. And that 2% target rate is arguably higher than it should be. As Wolf points out convincingly, nothing goes to heck in a straight line (including short-term inflation readings)

That said, I’m not predicting hyper-inflation, but the magnitude of the last 25 years of stimulus has yet to be fully recognized via:

– purchasing power give-up

– asset price roll-backs

– or both

Remember the 6 to 8 month lag period of time for interest rate cuts to take effect before the November election. This is the reason we hear all these stores about rate cuts in the November minus 6 to 8 months time frame next year. Any economic conditions are secondary. Talking about the last 30 years on the DOW I fully understand things happen now more like in fairy tales than in the real world.

The Real Tony,

Powell is a Republican. He isn’t going to try hard to help Democrats, LOL. People need to get this meme out of their mind.

And it’s of no use for now anyway: the economy is doing fine, the labor market is strong, wages are rising. But inflation is hanging over the election, and is hanging over Biden, and an acceleration of inflation is going to put voters into a shitty mood — people hate hate hate inflation — and that’s not good for incumbents. The absolutely last thing Biden wants is an acceleration of inflation in 2024.

The capitalist bankers don’t care who the US President frontman is, they already have Jerome Powell as their front man for their control of the nation’s money and world reserve currency. Besides for the capitalist the US President is more like the court jester.

Right now the “capitalists” hate Powell because he jacked up the rates to 5.5% and yanked $1.2 trillion off his balance sheet, when they were counting on 0% and QE infinity, and now they’re trying to do everything they can to force the Fed to pivot.

I think the part that bothers me is, there are so many people on TV and social media treating inflation like its no big deal. So many people want to believe inflation is slayed and its done forever and we aren’t even close to bringing core and service inflation to its knees yet.

Inflation always has a habit of bringing up nasty surprises and reaccelerating. These people are literally gambling on the sake of the well being of the country without a care about it.

The Roman Empire got slaughtered because of inflation which entered hyper inflation and having poor trade deficits with a ton of debt. That sounds like the US without the hyperinflation. Inflation can bury a superpower back then or today.

The Roman Empire was a superpower the lasted nearly 1000 years. If they went back in time Im sure they would think differently about inflation and hyperinflation and took it way more seriously like the US SHOULD be doing.

Without turning this political, Trump already has mentioned about jawboning the FED if he retakes office to lower rates like he did in his first term. Sometimes I wonder if Powell would cave with Trump and his party crucifying Powell on social media like Trump did the last time when Powell caved.

I think the last thing Powell wants is to be is Arthur Burns. With Biden in office, I think Powell remains firm. With Trump in office, I have some concerns with Powell holding firm to fight inflation assuming we haven’t beaten it yet by next election, which I dont think we will.

“powell is a republican”i think he’ll choose democracy over authoritarianism. and if cuts are needed to help prop up markets i think he’ll cave regardless of data so as to help biden get through this next election,

“So this is a labor market that is in pretty good shape, in amazingly good shape actually, given the interest rate environment. “-Wolf

Fed Funds Rate at about 5% is historically normal. Inflation rate of around 4% is historically normal (trying to get to 2% is crazy, but Powell can do what he likes). The strength of our economy is not surprising to me. It is pretty much normal. People have lost site of normalcy because of prolonged ZIRP. It is interesting to watch them freak out.

I harken back to my days as a ten year old when I opened a bank passbook account for ten dollars (all I had) and got 5% interest. I remember a common ad by banks “deposit before the 15th and earn from the first.”

“Inflation rate of around 4% is historically normal”

That depends on where in history you look. The Fed managed 2% for 30+ years. The benefits of a lower inflation rate are clear: It’s better form the people. It’s better form the country. And the variations are less in absolute terms meaning it’s more stable and less likely to get away from you.

It is interesting how Wall Street doesn’t like “full” employment of 5% as reserve labor is great to have to put downward pressure on wages. They aren’t getting what they want. Imagine if we invested in our infrastructure and other areas we might truly hit FULL employment and what would be so bad about that!

1) We’re at, or very near, full employment. Check the stats. Way more open jobs than job seekers, at all levels. Anyone who wants a job can find one (whether they like that job is a whole ‘nother issue).

2) What would be so bad about that? More inflation, that’s what. Maybe you like inflation? ;-)

My point was different in that we shouldn’t have a society built around the necessity of the boom, bust cycles to maintain stable employment. Boom, bust cycles certainly have their role in our economic model and on one level could be seen as valuable but on another they simply concentrate wealth. We take the cycles we go through as natural and really not harmful as long as wage gains outpace inflation. Admittedly the US economy won’t change but when those cycles happen those who lose their jobs should not be mostly left to their own devices to survive.

At this point it isn’t clear employment is impacting inflation as we have low unemployment, significant wage gains, and lowering inflation (although a bit stuck right now). But even if we argued 8% or higher unemployment would be good for inflation is it really a good thing for society and of course additional spending that might occur at the government level? There are many ways to impact inflation as sometimes it is commodity imbalances but often times it is simply greed.

Howdy Youngins. HEE HEE aint this stuff great??? So, PLEASE remember, its OK to just save some of your hard earned $$$ and just earn some interest. Do you really want everything in Wallstreets hands ????

Better learn how to Boogie down to disco fever too. Its coming back…..

I’m too young to have experienced bell bottoms the first time around. I’d welcome a second chance. I hear they’re very slimming.

Howdy Captive. I think you may get your chance. Not the bell bottoms thingy but the 70s 80s deficit inflation is back…. Almost 34 trillion.

I’ll take the disco but pass on the inflation…

Sooner or later you have to think that Wall St. will figure out that they will never get the recession they want with a 7% of GDP government deficit and shift their obsessive focus from the Fed to Congress. Of course I would have expected that to have happened already. so who really knows.

Well that is good news for America. In my experience there is no other activity as much fun as one’s job.

2019 saw unexpected rate cuts and QT halted because of financial plumbing problems. Will 2024 also?

The Fed revived its Standing Repo Facility in July 2021, which it had had before QE until 2008. Bernanke killed it when he started QE. The repo market issues in late 2019 you referred to wouldn’t have happened with this SRF.

Also, reserves were down to $1.4 trillion when the repo market started acting up. We’re $2 trillion in reserves away from that. So it’ll be a couple of years-plus before reserves get this low again

The times are so crazy, almost like when I graduated from high school and became eligible to be drafted into the army to fight for the success of the US police action in Southeast Asia.

This morning I heard about companies commercializing star wars technologies like CRISPIR gene replacement to cure sickle cell anemia, the race to develop the quantum computer, and Googles vision of the profit potential of AI is too develop an avatar of every human being that predicts what it’s human host is most likely to do.

It is a world that is always changing, held together by the glue of tradition.

Tell me why jobs even matter? How do you predict economic activity using jobs? The Philips curve was denigrated in the 60’s.

“Tell me why jobs even matter?”

LOL. Lose your job, and you’ll find out why a job matters to people, and why jobs matter to the economy overall.

In terms of inflation, what matters is how much people get paid in aggregate. So high and strongly growing employment along with big wage increases due to labor shortages create a lot of consumer income that’s going to get spent very quickly, as we have seen, which helps fuel price increases.

Look at what happened in 2021 and 2022, when people didn’t want to, or couldn’t work for whatever reason, and labor shortages cropped up, watch the effect on the economy, wages, prices… inflation.

In 2021 and 2022, the Phillips curve was un-denigrated in real time.

Generally, low unemployment has been seen as meaning plenty of spending money, leading to higher prices (inflation). It is one of the key measurements used by the Fed, and therefore, Fed watchers. If Fed wants to reduce inflation, they seek to increase borrowing costs, which eventually bleed into employment readings. Many use job data as one of the indicators of what the Fed might do, and gamble accordingly. I agree that the Phillips curve has been overstated as a reliable predictor. To me it is more one of those correlating, even trailing, measurements, rather than a predictor, but it doesn’t matter what I think, it matters what the Fed thinks, and they rely on that data, so investors rightly pay attention to it to. We ignore it at our own risk. As Wolf mentions, it has had pretty high correlation the past couple of years. Plenty of jobs available (in fact, labor shortages in many sectors, and at many levels), leading to higher wages, leading to higher prices. When jobs and wage reports continue to indicate stronger than expected health, higher inflation could easily be following, and lower inflation less likely in the near term. If the Fed feels the same way, the “pivot” is a fairy tale investors tell themselves.

Sorry, meant to hook this reply to spencer.

Is there a historical basis on a country being a net trade exporter, having global reserve currency, and being energy independent?

I can’t think of one. If anything, rates are probably still too low. Factory investment is insane right now.

Mexico will definitely benefit. Canada needs to get its act together. They show a little backbone for increased investment in responsible resources extraction they could make a killing.

I have heard a “rule” that to slay inflation (as has only occurred a few times in the central banking era in the US) interest rates must rise above the peak of inflation.

Others say that holding above current inflation numbers will continue the downward pressure.

We know: nobody knows.

I consider the psychology here. People dealt with a 5-15% increase in various costs.

Increasing the cost of money (mostly “doing business”) is just another cost increase. When applied to personal finance (and ‘Merica) we must factor in resiliency and determination.

The American Consumer is programmed to consume! We are taught to overcome obstacles at whatever cost or effort.

With a 5% safe asset income, and a 10% cost of money (mortgage or auto finance rates), it feels pretty neutral compared to rapidly spiking goods prices.

Service costs are directly related to wages, all lifted by the same tide. My pay goes up, I am good with your pay going up: I have solidly baked in my expectations.

The individual doesn’t care about government debt servicing, capex or startup funding, assuming their income is ongoing (as jobs are ample).

Almost by definition, you can’t be a global reserve currency (in the modern sense) and also be a net trade exporter. To be a reserve currency you need to be (a) massive, (b) have very few capital controls, and (c) have functioning/lawful markets.

But if you’re a massive lawful market, everyone will want to move their capital into your economy, and if you have no capital controls, they’ll be able to do so. And in doing so, they create a trade deficit.

Being a global reserve currency has a number of geopolitical benefits but economically it’s extremely distortionary, and it’s an easy argument to make that Americans, at least those who don’t own multinational companies, would be better off without it.

And weirdly, being a reserve currency is America’s own choice — China is not going to loosen their capital controls or fairly enforce property law within their own economy, so changing the status quo would require the US to *introduce* some sort of capital control. Perhaps you think this is also a “never gonna happen”, but the original justification for it was to create a global trading bloc to counter the USSR, and that justification is well past its expiry date.

I do see a USA that have started to introduce capital control. In the name of sanctions and tarrifs. So the status quo may not be that static.

Andrew, those are some worthwhile things to consider so it’s a good comment.

Glad “Average Joe’s” incomes are holding up… am hoping “Median Joe” is doing OK too but considering the massive gap between them on most numbers, I’d be surprised.

JPMorgan makes it sound like the extra manna from heaven is gone now so gonna have to count on surplus wages to take up the slack.

“Most Americans have already drained the excess savings they made during the Covid-19 pandemic, Marko Kolanovic, a senior stock strategist at JPMorgan bank, said in a note this week.

According to Kolanovic, inflation-adjusted liquid assets such as deposits and money market funds of nearly all US consumers will be below 2019 levels by mid-2024.”

“Most Americans have already drained the excess savings…”

The “excess savings” theory is the biggest braindead bullshit ever. By morons for morons. It has been completely debunked.

Just look at the ACTUAL savings: CDs, savings accounts, money market funds, T-bills, etc. They’re huge and they’re growing and they’re earning over 5% now.

Plus, consumers continue to save more than they spend, and they continue to add to their savings.

Here are the numbers and charts of the trillions of dollars that consumers have purchased in CDs and money market funds. Charts too. Look at. That the actual savings consumers have, and it’s gigantic:

https://wolfstreet.com/2023/11/24/money-market-funds-large-cds-small-cds-all-surged-americans-figured-it-out/

That’s good to hear thanks. Maybe we will get some sane political leadership out of a continued good times for all.

I suppose it’s the “Average Man” who spends the money in the US economy anyway. Statitica has a different take on how flush most are tho.

https://www.statista.com/statistics/1356265/mean-and-median-amount-of-savings-in-the-us-by-type/

RTGDFA I linked for you, instead of browsing around the internet until you find some internet survey BS that suits your narrative.

The article I linked for you gives you the actual data of the trillions in liquid assets that consumers have. Look at the chart of the small CDs. This is NOT survey based.

The Statista article is just “savings” — it’s based on an internet survey of 2,000 people, LOL that respond to internet surveys. It doesn’t include T-bills (bonds), money market funds (securities), stocks, bonds, rentals, home equity….

People who keep spreading this bullshit about most Americans being poor and living from paycheck to paycheck will NEVER understand the strength of the consumer and will always be surprised by it, DUH!!! And they wonder where all this money comes from because consumers are so poor, LOL, then they come up with stupid-ass conspiracy theories as to why consumer spending keeps growing at a good clip, though consumers are so poor.

I’m sick of this shit. It’s clickbait, and people click on it and share it, this shit goes viral, and people keep dragging this shit into here to spread it further, and that’s why media outlets keep publishing this shit. That’s why clickbait exists. This stuff pollutes your brain!!!

This website is full of articles with data that debunks this shit. Don’t comment anymore on this topic until you’ve read at least the last 10 of my articles about this topic all the way down and looked at all the charts.

This comment section is not a repository for clickbait bullshit. That’s what X is for.

The FRED chart for real median income was just in the news, for whatever reason. It is only updated every year and the last observation was for 2022, but it shows a continual downward slide.

https://fred.stlouisfed.org/series/MEHOINUSA672N

I don’t have a clear idea how to compare this to Wolf’s data from BLS which seems to show the opposite.

Andrew,

1. you’re confusing INCOME with ASSETS (such as savings, homes, stocks, ets.) That’s why I should delete your “income” response on an “asset” question. That’s just another layer of BS.

2. But I’m not deleting it because you need to know something. Are you not reading the articles here?

“real income” means adjusted for inflation. In 2021 and 2022 inflation took off massively and finally went over 9% in early 2022, and slowly rising incomes didn’t keep up with the exploding inflation, and “real incomes” fell. I’ve been saying this since early 2021.

But in 2023, it flipped. And your link is annual and doesn’t show 2023. It only shows 2022, where real incomes fell, as I have been saying…

Starting in 2022 into early 2023, workers have gotten HUGE pay increases, and those “pay increases” have turned into “income” in 2023 through Oct 2023 (last data we have), income increases have outrun inflation, and the “real incomes” have grown substantially, the most in years, which is why consumer spending has been so strong.

Quoted from this article published on Dec 1 (RTGDFA):

https://wolfstreet.com/2023/12/01/oh-deary-no-our-drunken-sailors-did-not-suddenly-sober-up-on-the-contrary/