Gasoline plunged, durable goods fell. Inflation still hot in services: housing, insurance, healthcare, transportation (incl. auto services). Food inflation simmers.

By Wolf Richter for WOLF STREET.

The PCE price index released today boils down to this, in October from September:

- Gasoline and other energy products plunged;

- Durable goods, dominated by motor vehicles, dropped for the fifth month in a row;

- Food prices keep rising from already very high levels;

- Housing (rent), insurance of all kinds, healthcare, transportation services (incl. auto repair!) were hot.

- Core services remained in the same hot range in which it has been bouncing up and down in for months.

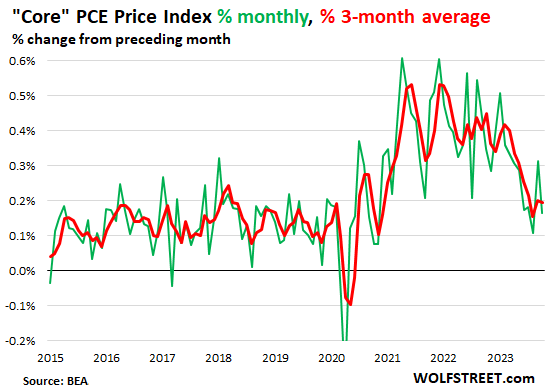

The core PCE price index, which excludes food and energy, decelerated to an increase of 0.16% in October from November, from 0.31% the month before, which had been the highest since March (green). The three-month moving average remained at 0.20% (red).

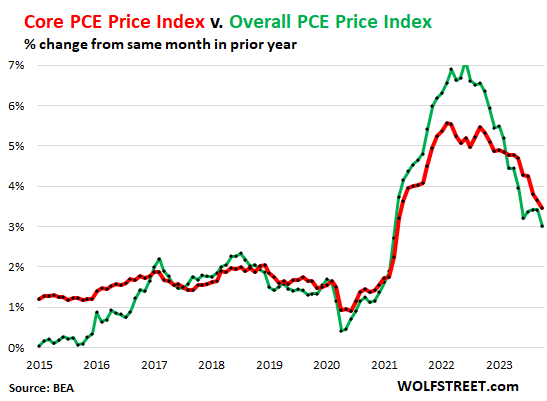

Year-over-year, the “core” PCE price index decelerated to 3.5% (red line). The overall PCE price index, driven down by energy, decelerated to 3.0%.

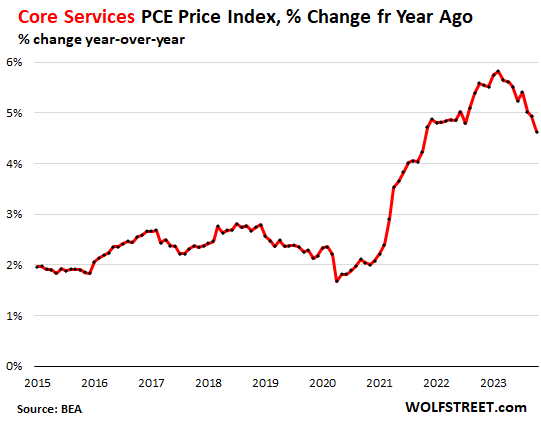

The core Services PCE price index (all services except energy services) has been bouncing up and down all year on a month-to-month basis. In August, it had decelerated to the slowest increase since 2020; in September it had spiked to the biggest increase since January; and in October, it decelerated again, increasing by 0.21%. There was a consistent deceleration earlier in the year, but the last four readings took turns spiking and dropping:

Year-over-year, the core services PCE price index decelerated to 4.6%. We’ll get into the major components of core services in a moment.

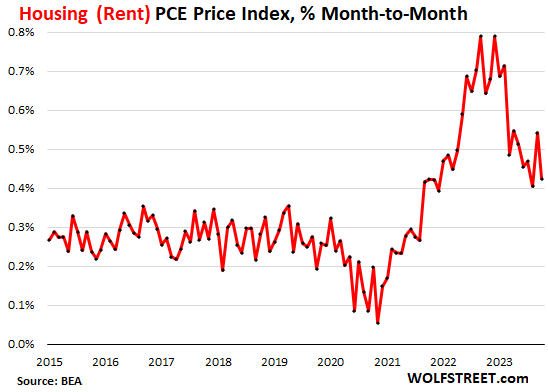

The PCE price index for housing, which is composed of various rent factors, rose by 0.42%, a deceleration from the spike in September, but an acceleration from August.

As you can see in the chart below, all the ups and downs from March on have been confined to the same range, and there hasn’t been much progress.

The big progress came early in the year, when the index dropped from its previous cluster around 0.7% to the current cluster of the past 10 months of around 0.45%.

The sudden lack of progress was confirmed by the six-month moving average which has been essentially unchanged for the past three months at around 0.48% after dropping substantially from March through August. This is close to 6% annualized rent inflation.

Year-over-year, the PCE price index for rent decelerated to 6.9%. The year-over-year deceleration is largely driven by the sharp month-to-month deceleration earlier this year.

The major “core services” categories.

Housing, insurance, healthcare, and transportation services (includes auto repair and air fares) remained hot on a month-to-month basis.

The financial services index plunged by 0.88% for the month, but it’s very volatile, including a 1.9% month-to-month spike in July. This -0.88% in October contributed to the deceleration of the core services index.

On a year-to-year basis most services remain in hot territory. These are the items that Powell has been talking about a lot during the FOMC press conference. This is where inflation has gotten entrenched.

| Core services categories | % MoM | % YoY | Includes |

| Housing | 0.42% | 6.9% | rents |

| Non-energy utilities | 0.25% | 5.4% | water, sewer, trash |

| Health care | 0.50% | 2.6% | Physicians, outpatient, hospital, nursing care, dental, etc. |

| Transportation services | 0.75% | 4.7% | auto repair & maintenance, auto leasing & rentals, public transportation, airfares, etc. |

| Recreation services | 0.20% | 5.4% | concerts, sports, movies, gambling, streaming, vet services, package tours, etc. |

| Food services, accommodation | 0.01% | 4.7% | meals & drinks at restaurants, bars, schools, cafeterias, etc.; accommodation at hotels, motels, schools, etc. |

| Financial services | -0.88% | 4.1% | fees & commissions at banks, brokers, funds, portfolio management, etc. |

| Insurance | 0.46% | 5.6% | insurance of all kinds, including health insurance |

| Other services | 0.11% | 3.5% | a vast collection of other services |

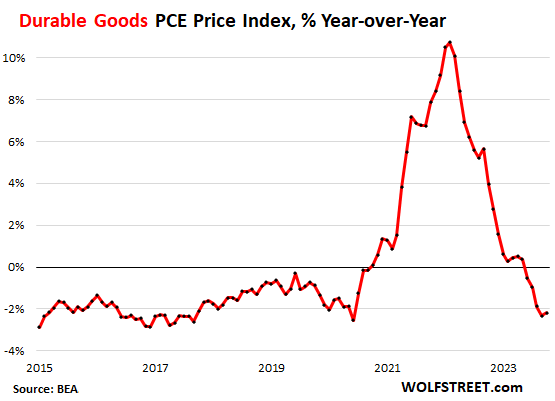

Durable-goods PCE price index fell by 0.27% month-to-month, the fifth month in a row of declines; and by 2.2% year-over-year, also the fifth month in a row of declines

| Durable Goods yoy | -2.2% |

| Motor vehicles & parts YOY | -1.5% |

| Furnishings and durable household equipment | -2.2% |

| Recreational goods and vehicles | -4.3% |

| Other durable goods YOY | 1.4% |

You can see how the huge spike in durable goods prices during the era of shortages is now slowly getting worked down some.

Prices of durable goods are still high but are coming down from the price spikes of 2021. The dynamics are driven by used vehicles, whose prices have been dropping since the peak at the end of 2021, though they’re also still way too high:

Food inflation keeps simmering. The PCE price index for food and beverages purchased at stores and markets rose by 0.25% for the month and by 2.4% year-over-year from already very high levels. There was a brief period earlier this year, when food prices dipped a little, but starting in the summer, the month-to-month increases off these high levels resumed.

This chart shows the index value, not percent change:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The ongoing problem here is that rents won’t come down any time soon. Prospective buyers who can’t afford homes are keeping vacancies low and rents high, even with overbuilding in the mutifamily area.

Crude oil will eventually respond to OPEC’s supply cuts as well.

Car sales (especially EV’s) are dead, from what my dealer friends tell me.

A quick Google shows that EVs had record market share (7.9%) in the US in Q3.

91,537 BEVs (battery EVs, as opposed to plug-in hybrids) were sold in October 2023, down from 104,015 in September but up from 70,443 BEVs in October 2022. The September 2022 number was 63,243 BEVs.

So: October EV sales were down 12% month over month but still up 30% year over year.

EV sales are increasing but not as fast as the dealer would like. 3900 dealers wrote a letter to the White House this past Tuesday.

————————————————————

Car dealers aren’t happy with President Joe Biden’s mandate to have two-thirds of all new cars be electric vehicles by 2032. Axios reported that a group of nearly 4,000 local dealerships sent a letter to Biden urging him to “tap the brakes” on his mandate.

The letter from the dealers group described slumping sales for EV, which means more cars languishing on the lot, which is bad for their small businesses.

Dealers have a 103-day supply of EVs compared to 56 days for all cars. It takes them on average 65 days to sell an EV, about twice as long as for gas-powered cars. EV sales are slowing though manufacturers have slashed prices and increased discounts. Consumers paid on average $50,683 for an EV in September, compared to $65,000 a year ago.

The reason, as the dealers explain, is that “early adopters formed an initial line and were ready to buy these vehicles as soon as we had them to sell.” But most consumers aren’t “ready to make the change,” in part because EVs are still too expensive. Many apartment renters also don’t have garages for home charging, and public charging networks are spotty with one in four not functional, according to one study.

A new study from the University of California, Berkeley’s Energy Institute at Haas finds a “strong and enduring correlation between political ideology and U.S. EV adoption.” About half of EVs registered as of last year were to “the 10% most Democratic counties, and about one-third to the top 5%,” the study notes. This suggests “it may be harder than previously believed to reach high levels of U.S. EV adoption.”

——————————————————-

I also read if people want an EV…they want a Telsa. I bet Tesla was not part of this letter.

ru82,

The US legacy automakers — GM, Ford, and Stellantis — got run over by a Tesla on autopilot.

Two years ago, GM, Ford, and Stellantis were 10 years behind Tesla, today they’re 14 years behind. Every executive from the CEO on down three levels should be fired on the spot. I’m furious. I have been waiting for years for the legacy automakers to put the heat on Tesla to knock Tesla off its high horse. Instead of designing and building competitive EVs, supply chains, and production methods, to where they can price EVs to out-sell Tesla, the US legacy automakers are trying to sell half-assed over-priced EVs, and since that’s hard to pull off, they’re blowing $15 billion on share buybacks instead, these idiots. They don’t even have anything to sell. GM killed its old Bolt, and the rest is just dabbling and announcements and high-priced BS. Ford has an overpriced mediocre compact SUV and an overpriced so-so truck that’s now getting outsold by a startup (Rivian). Stallantis has practically nothing in the US. Ford, these effing idiots, made a deal with China’s CATL for battery production after everyone knew that that was a total no-no, these effing idiots. In addition, they’re suffering from ICE dealers who’re refusing to sell EVs. Those morons are now begging Biden for help. They should just stick to ICE vehicles and go out of business, would be easier for them.

This likely doesn’t help:

From Green Car Reports November 30, 2021 (citing Consumer Reports study. Automotive News ran a similar article)

“The reliability of electric cars and plug-in hybrids is improving, but they still remain more trouble-prone than cars without plugs, according to a new Consumer Reports survey.

On average, EVs had 70% more problems than internal-combustion vehicles, the survey found. Electric cars, electric SUVs, and electric pickups are all among the least-reliable vehicle categories surveyed. Plug-in hybrids averaged 146% more problems than non-hybrid vehicles.

A previous survey pointed to the more complex interfaces and tech features automakers tend to pile onto EVs and plug-in hybrids as the main source of reliability issues. This time, it’s battery and charging systems as well, according to Consumer Reports.”

Wolf,

Don’t sugar-coat it. How do you really feel?

vecchio gatto veloce,

I’m going to write an article about how Ford and GM got run over by a Tesla on autopilot.

If I read correctly GM said that things have been so great that they were going to start up new stock buy backs and increase their dividend. This seem so contradictory to everything else that has been said in the past year. I am not sure what to make of any of this seems like GM things good time ahead?

GM is trying to boost its share price, after its super-hyped EV and robotaxi strategies collapsed.

An awful lot of media doing its best to bring Musk down. Not a Musk fan boi, he’s a weird rich dude doing his own thing and that’s the extent of my opinions of him. But I do appreciate his being a fly in the rancid ointment.

All you hear about is him ruining Tesla, X, crashing phallic rockets, etc. Yet while Tesla’s out-advancing US auto makers, the media is slagging him so we don’t see the automakers going hat-in-hand to the government.

Almost makes me want to trade in my “overpriced mediocre compact SUV” (great Lemmy that made me giggle) and get a Tesla, except they’re still too rich for my blood.

Lili Von Schtupp

“…a fly in the rancid ointment.”

🤣❤ gonna steal that from you someday. That “rancid” is worth its weight in gold.

@El Katz,

In theory, the EVs should need much less maintenance with lower cost of repair, not counting the battery pack. I suspect any current reliability issues are due to growing pains, that could be worked out within a decade. Battery pack technology should also continue to advance, and that could make a big difference in reliability.

Many of the problems are related to the non-Tesla charging stations. Lots of complaints about them, a big item in the Consumer Reports survey. But that’s NOT the vehicles, it’s the third-party charging stations

https://wolfstreet.com/2023/11/17/the-collapse-of-ev-charger-spacs-chargepoint-ceo-sacked-cfo-out-revenues-plunge-losses-mount-shares-96-from-peak-evgo-not-far-behind/

When you published the article linked above, I was curious to know how much power was transferred to a Tesla battery system via one of their Supercharger stations.

The V3 system uses liquid cooling in the cables and the maximum power flow is 250 thousand watts — of electricity. Converting 1 kW to horsepower is done by multiplying by 1.34. So, think of an internal combustion engine-powered car on a dyno kicking out 335 hp. That is how much power is being plugged into your Tesla at a Supercharger.

My limited perspective, as an owner of a Tesla Model 3 Long Range since Dec. 2019. I have had two tire changes and an frustratingly inconvenient stuck frunk. It was closed and had my favorite tools inside. A tech came to my home to fix it, but couldn’t get it. I had to drive it 75 miles to a service center in Chicago. Got $100 in uber credits and a few hours to wander around with my brother in-law.

We frequently make a 125 mile round trip trek to Madison and drove to Denver and back from Northern Illinois. My trip to Madison, WI and back today was through some of the nastiest winter weather. I appreciated the all wheel drive and infuriatingly accurate traction control (only frustrating when you really want to play in the snow).

I have never encountered a non-function Tesla super charger. I have never successfully charged at a non-Tesla supercharger (3 attempts). This is why other manufacturers are adopting Tesla’s connector and network. A desperate concession to catch up.

Experiences like mine are the reason Tesla is not included in these reports. It paints the wrong picture. The dealers are aware of the business Tesla is doing without dealer overhead. That’s why Tesla isn’t include isn’t included in their letter. They are desperate to slow down the competition because they thought they wouldn’t need to catch up.

We made an additional investment in solar panels for our home. My charge stats show 94% at home.

Regardless of solar panels or not. The biggest misconception I encounter is the the benefit of home charging and walking out to an always full tank. I don’t miss gas station stops and the occasional super charger stop is a simple plug in and wait. If your using navigation it will tell you its ok to continue to your next destination. Less than 15 minutes if you don’t skip charge points along the course. We arrived 1 hour later than the rest of our family on our 940 mile trip to Denver.

If you haven’t taken a test drive or rented a Tesla, you should.

*Disclaimer: I own no Tesla shares or hold any affiliations with that company other than my car. Sadly, I still hold Ford shares.

Interesting. I was reading an article about the Cybertruck.

“ The launch of Tesla’s new Cybertruck comes as automakers are experiencing slowing growth in EV sales and cutting prices. ”

Guess it had too many issues to keep it at the declared 2019 price tag.

Smoke and mirrors.

They are coming out with the Mad Max Cybertruck edition in a few months. Some cool upgrades and a nod to where it got its inspiration.

Bandon,

“… as automakers are experiencing slowing growth in EV sales and cutting prices. ”

Tesla’s year-over-year growth slowed to 35% down from 50%?

Rivian’s growth slowed to something like 130%, down from 200%?

I love those WSJ morons. These idiots should all be replaced by AI, would be cheaper and couldn’t do any worse.

EVs are eating market share from ICE vehicles at a pace that is scary.

Tesla is now the #2 automaker in California per registrations in Q3, just a smidgen behind Toyota, and far ahead of the other the other Japanese brands. US legacy automakers hardly register anymore.

Tesla’s Model 3 and Model Y are by FAR the biggest bestsellers in the state. Nothing comes even close. Ford GM and Stellantis are getting their heads handed to them.

In terms of what I think about the EV strategy of Ford, GM, and Stellantis, see my comment above. Their CEOs make me vomit.

The high take rate in CA is driven in part by:

“The CAV decal program is run by DMV in partnership with the California Air Resources Board (CARB). The program allows a vehicle that meets specified emissions standards to display CAV decals and to use HOV (carpool) lanes with only one occupant in the vehicle (see California Vehicle Code (CVC) §§5205.5 and 21655.9).”

Battery and Plug-In Hybrid vehicles qualify.

In my previous career (domiciled in California), any company vehicle with a HOV sticker was a hot commodity for freeway commuters. Allowed use of the carpool lanes without the requirement of a pesky additional occupant(s).

This is nationwide. CA is just ahead. People have been posting utter BS for 10 years about EVs, that they will never work, that they’re too expensive, too heavy, too whatever, and they still do, but EVs are eating market share at a scary pace because people love them and buy them.

If you don’t like EVs, fine. Don’t buy one. Great. Americans buy what they want. That’s what the car business is all about, which is why EV sales are soaring. But don’t post BS about EVs.

The adoption of EVs depends greatly on the specific use model.

The sweet spot appears to be a second car, suburban commuter, charges in the garage at night. No range anxiety or charging station problems. Also, toss in that HOV lane advantage and a tax credit…it looks great. Why wouldn’t you buy one?

Problem areas: long road trips, really cold climates, lack of charging infrastructure.

Zap…ask when all the subsidies end.

Rents are falling significantly all over the country.

LOL, that was funny.

They may not be falling all over the country but landlords attempting to gouge are having trouble!

In my condo complex in the best part of San Antonio, there are five units available for rent:

3 bed 2.5 bath $2100 down $400

2 bed 1 bath $1150 down $75

2 bed 1 bath $1195 down $25

1 bed 1 bath $1200 down $75

1 bed 1 bath $1200

All of them have been empty for months with almost zero traffic. I know because one of these units is directly across from me. I saw someone look at it a couple of weeks ago.

They’re falling around parts of Austin. I can post listings.

Liar

I am taking delivery of a new Model Y tomorrow. Took about 3 weeks from order to delivery which is consistent with recent backlog.

CCCB

I was shopping for a car to replace my totaled Toyota Corolla and noticed the unavailability of small cars for rent or to buy. I was in a dealer’s lot 20 miles out of the Swamp (DC) where I saw thousands of big cars and SUV’s, and trucks parked and collecting dust. I asked the sales dude about small cars for sale and said there ain’t any.

small cars are not being produced in large numbers for the US market. US automakers have abandoned them entirely. So there are not a lot of them out there.

However, I just checked online in your area for used Corollas, and there are quite a few listed by DEALERS, of all ages. You need to transition into the 21st century, the internet is here! Once you locate the one that fits your needs online, you can check the CarFax history online, etc. And if you still like it, you can go to that dealer and have a look. But yes, be prepared to pay out of your nose for it. Used car prices are coming down at the fastest rate ever, but they’re still very high.

Wolf,

“small cars are not being produced in large numbers for the US market. US automakers have abandoned them entirely. So there are not a lot of them out there.”

So true, So true

We need a small car to drive around here especially in DC and Bethesda Maryland where there are no parking spaces for big cars. Also, I like the good visibility and handling of this small Japanese car, a Mitsubushi Mirage. I got it for only $11,600 with 60K miles on it. Feels like a brand new car. I’m still in the 20th Century with cars at least. We use it for going to the grocery store, the Post Office, bank, golfing, visiting the kids, etc. For long trips I’ve got my Subaru SUV. I haven’t bought an American car since 1978 when I bought a lemon Ford Mustang. For then on it was all 100% Japanese cars and they have served me well.

Wolf,

” I just checked online in your area for used Corollas, and there are quite a few listed by DEALERS,”

We looked at Corollas in this area, but were very disappointed. After 2008 they changed the body style and made them into an ugly box which was too bulky for city driving. So, we gave up and switched to a small Japanese car which suited our needs just fine. DC has a European grid, and people there drive small cars. The American car makers have missed the boat. They don’t make small cars because they don’t have much markup on them. It’s all about making a fast buck, selling cars to maximize profits, not giving customers what they want and need. I don’t care about them or their unions. Let them all go bankrupt.

@CCCB

Basically agree. In Seattle, “rents won’t come down any time soon. Prospective buyers who can’t afford homes are keeping vacancies low and rents high. . .”

In the Seattle metro area, you can’t build anything except high-rise condos in Seattle proper and in Bellevue. There is a grinding housing shortage, with no end in sight.

In Tacoma, a starter house costs $400k, and anything remotely nice which comes on the market is sold in the first weekend. People who have been priced out of the market are stuck renting, and that will not change any time soon.

We are enjoying 2 months in Hawaii at Waikoloa beach. Now is the time to reserve another 2 X 2 month condo rentals. Scuba on ! Life is better at the beach.

We are all soooo happy for you! PA

I found the income side of the print to be more interesting. The drop in wage growth was really significant. One month does not a trend make, but that was the lowest monthly increase since April 2020 (covid crash).

1. It was an increase!!

2. This stuff is volatile month to month. Next month the increase will be bigger.

3. Inflation is down, so wages don’t need to rise as fast to beat inflation.

4. “Real” income grew month-to-month.

Look again, the full release with tables. Call it under the skin on personal income 😉.

Again, one month does not make a trend, but the true ‘core’ wage component decelerated across both good and services. Look back at the monthly data for the past 3 years, it’s been anything but volatile. Other components of income are more volatile. The average growth for 23 has been somewhere in the range of 60B, it fell by nearly 2/3.

Can’t read too much into a single data point, but wage growth is a critical driver and it is something we should keep our eye on going forward.

Employment is normalizing.

Inflation-adjusted income from all sources has been rising in 2023. In other words, in 2023, income growth outpaced inflation. That was not the case in 2021 and 2022.

https://wolfstreet.com/2023/12/01/oh-deary-no-our-drunken-sailors-did-not-suddenly-sober-up-on-the-contrary/

Personal income from all sources, adjusted for inflation, but without transfer payments from the government – so this is income from wages, interest, dividends, rental properties, farm income, small-business income, etc., but without Social Security benefits, unemployment insurance, VA benefits, etc. – jumped by 0.3% for the month by 2.3% year-over-year (adjusted for inflation).

This income growth is a function of rising employment, rising wages and salaries, rising interest incomes, rising rental incomes, etc.

Per-capita disposable income, adjusted for inflation (total income minus taxes), jumped by 0.3% for the month, the biggest increase since May; and by 3.9% year-over-year. This is what consumers had left to spend on goods and services and to save. And it has been outrunning inflation by a wide margin all year, after a steep setback due to inflation in 2022.

In other words, per-capita disposable income has been outrunning inflation by 3 to 5 percentage points all year. This is where the money came from to do all this spending:

I took the data back only to June 2022 to cut out the huge distortive effects of the stimulus payments, and the year-over-year comparisons to those stimulus payments a year later.

Everything is fine as long as you don’t need food or shelter… What happens next will be interesting as gas looks like it’s about to bottom.

Buckle up and an election year!

Around 40% of Americans own their houses free and clear of any mortgages whatsoever and do not have any higher costs.

Huh? Maintenance, insurance, and taxes through the roof. Those people still need to eat too lol. Everyone is suffering from what these m o r o ns at the helm did to this country.

Friend got a quote to paint his house at 6k. Was 2k not even 3 years ago.

Last year I spent $1284 in property taxes, $1181 in homeowner’s insurance, $225 for the HOA, and about $900 in maintenance. On a 2000 sq ft 3/2 in the burbs of East Central Florida. More than I’d like, but barely up from 10 years ago.

Yep my home paid for but demographics and baby boomer generation are aged out from jobs. Hundreds of jobs in my oilfield expertise but I am aged out at 66 years old engineer.

So inflation is killing me as my bond portfolio purchased in 2013 is down 40 percent . I need cash flow and a job who cares if my house is paid for when a new roof ac and car repairs are through the roof! Not to mention my utilities have doubled in 1 year. We don’t eat out much probably less than 1 time a month

Kent,

Yours is unusual then. No one I know has your situation.

Kent and fed up:

This year’s property taxes, 2023’s to be clear, are up 3% per state and local rules and regulations, to approx. $1,300.

Have done ”maintenance” this year approx. the same.

NO insurance on home, ever, because of obvious disconnect, and considering this house an obvious ”tearer downer.”

Clear enough to sell ”the dirt” and buy a much better place with cash left over, IF this old but ideally located house is destroyed by storm, fire, etc…

Folks, other than Amish and similar actual communities, need to coalesce against ”insurance” in spite of the insurance industry massive propaganda.

@Kent

Your situation is exceptionally unusual to say the least. Homeowners insurance, HOA dues, are up massively, especially in FL, and property taxes almost everywhere are up 30% ish

Kent is not alone. My condo annual expenses are:

Property taxes $371

Insurance $516

Maintenance $0 HOA does it all

HOA $4488 includes all my utilities

@Fed Up Things are not “through the roof” across the board. We are lucky in CA that property tax increases are capped at 2%. The insurance on my home on the Peninsula is up just ~3% this year but I got a 20%+ rate increase for the insurance on a San Mateo Apartment building and the rates went up more than 30% on a Sacramento Apartment building last year.

Happy 1, yes, that’s what I’m seeing with most people I know.

The rest of you are either lucky or you don’t see how you are being ripped off.

BS ini

I didn’t see your comment when I made my last comment. That sucks being aged out. And like you, most people are experiencing horrific services inflation.

The rest throwing out numbers tells me nothing, and I’m skeptical. I really find it hard to believe that Kent’s costs have hardly gone up in 10 years lol. He must be living in a vacuum.

Wolf:

Do you notice none of the FED officials come out and say succinctly what you said in the beginning:

“Inflation still hot in services: housing, insurance, healthcare, transportation (incl. auto services). Food inflation simmers.”

Do they want to have the cake and eat it too (keep the asset values as high as possible)? Are these are not going to go away (foreigners keep giving gift to this nation Vs our own lofty expectations, but how long that will continue — did I read that your wife is Japanese born!)?

I’ve heard Jpow mention most of these in the FOMC statements & subsequent pressers.

I agree he probably doesn’t want to spook markets too much with uber-hawkish words.

Because much of “inflation” is behavioral (based on expectations) the FED will not add fuel to the fire by being too candid. To expect them to be brutally honest is childish.

How – I look at us now, and realize the number of years passed in the zeitgeist since Nicholson growled that memorable line in Sorkin’s ‘A Few Good Men’.

Wolf still growls similar, with our thanks…

may we all find a better day.

You bet!

The Fed is directly responsible as a causal agent with a decade of QE and ZIRP; the Fed has played a major role in the insane redistribution of wealth to the top 1-5 percenters.

Yes…the Congressional idjits piled on eliminating historical processes for appropriations. Easier to corrupt the entire process with baseline budgeting hocus pocus.

It’s all one colossal mess.

What I find surreal is how quickly JPow changed his tune from no hiking to aggressive hiking. You can tell he realized he made a big mistake.

I actually think it had to do with the social atmosphere in 2021 versus ’22. The vibe in ’21 was very high strung and almost hysterical coming off COVID and no one was thinking clearly. But the delay made matters much worse than they ought to have been.

Nobody is thinking clearly, that is why we have models, validated over decades. Recent FR boards decided to ignore Taylor rule and play it by the year. ‘Data dependent’ is pure economic idiocy, we know there are long lags, effects of policy changes won’t be seen in months or years. An institution that should be completely rule based, on automatic pilot using long established models is being run by amateurs with disastrous consequences.

econ….concur!

But it aint an accident!

Doctor_…

The original quote was, ” you can’t eat your cake and have it too.” Makes more sense when you read it that way.

Russell – try saying that to someone these days only to find: “…don’t tell ME what I can or can’t have!!!…” as the rejoinder…

may we all find a better day.

Pending home sales drop to record low, even worse than during financial ‘crisis; of 2008-2009

In all the articles I read about the PCE print, none mentioned the 4.6% yoy core services…

Probably too scary of a number, which interferes with their imminent deflation/QE/rate cut fantasy.

I’m convinced now by what I’ve seen over the last month that the Fed is “done” with whatever they’re doing.

If they thought inflation was too high, and were at all concerned, they would have stopped the month long party that has taken place on Wall Street and across all assets (bonds, stocks, real estate, bitcoin, gold, everything) over the last 4-5 weeks.

But they haven’t. Any statements they have made have been “Oh well, we might be able to lower rates in a few months!”

There was no reason to make those statements, even if true.

I’m not in the camp of “The Fed is not serious.” Over the past 3 years, they’ve destroyed 25% of the value of the dollar. That’s not a “soft landing” however you say it.

It ends up being a soft landing in a different town than where we all took off from. It’s a strange, unfamiliar, sometimes stressful new place.

Agreed. The Fed seems to be happy to let the market telegraph their next move. There has never been a surprise rate hike or increasing the pace of QT. Only a hot CPI number could force their hand.

“There has never been a surprise rate hike…”

Wrong. They occur. March 2023 was the most recent one.

Surprises happen when the Fed miscommunicates or markets don’t listen. The last rate hike that surprised markets happened after the bank panic in March 2023. You can see the gyrations that the market went through dealing with the rate hike, when it expected a hold or cut. But then over the following month, it all got back on track:

The crypto bubble is proof of the extent of the speculative mania and excess liquidity still sloshing around right now.

My haircut at Great Clips in Denver was 12$ 7 years ago, 24$ now. I’m exploring the Wolf Richter method.

Thanks for the two decimal places. They make a lot more sense than one decimal place. The re-acceleration of food prices sort of surprised me. My Dots candy indicator is still $1.00 (but now showing “marked down from $1.49”) at the cheapest store. It is the only store that has it for $1.00 now. Other stores are as high as $2.19. Crazy.

Assuming the transportation and supply chain bottlenecks have more-or-less disappeared, the increase in food prices might be a consequence of wage inflation. Companies burdened by wage increases (sometimes mandated by the state), especially at the low end like at stores, will increase prices to compensate, which in turn will make employees clamor for more wage increases to keep up, and so on. The process then becomes the dreaded wage-price spiral. We will see.

WL – would caution that world population increase since WWII, and it’s demand on food production (the original ‘Green Revolution’s notwithstanding) and climate perturbations affecting same might have something to do with this supply/demand trend, as well (…any observations here, DanRo?).

may we all find a better day.

Plant breeders and soil scientists are always working at making food production better and more efficient. Technology in farm equipment also helps. Look at the new cameras on spray rigs & the computer-controlled herbicide spray systems as an example for this.

On the other hand, what I find as a very stupid thing to do, but has taken hold, is turning cropland production away from food and into biofuels. Government policy and tax subsidies leading the way.

And, look at what the farmers in the Netherlands have been told what to do by the bureaucrats in Brussels, and the consequences of these edicts. That is one large factor in the outcome of their recen elections. Since this article is about inflation, if you want more inflation in food prices, do what the EU is trying to do to Dutch farmers.

From my own little world, having gardens, raspberries and apple trees on my 51′ by 126′ property is very rewarding. But, since it’s December in Minneapolis . . .

DanRo – have been concerned/saddened by so much of California’s best cropland going under the ‘dozer/paver over the decades (…lookin’ @you, in particular Silly Valley…). Appreciate the insights & best…

may we all find a better day.

I’m wondering if the Dots candy indicator is a leading or lagging indicator. Certainly worthy of a doctoral thesis.

I think it is a leading indicator. I should make a Dots plot, as an alternative to the Fed’s.

I have always loved Dots! I remember when Tropical Dots came out in the 90’s. It was a very exciting day for me.

I think you are on to something…it’s kind of like a spoon full of sugar helps the medicine go down.

1) Core service : rent is 6.9% Y/Y, the highest. Healthcare is 2.6% Y/Y,

the lowest.

2) The healthcare business is squeezed, bc the elderly, doctors best

customers, don’t have enough money. In recession they will merge or

close operation.

3) Rent is the highest. The average rent is 2K/M, or 24K/Y. The median

sale price is 391K, about 60% below CS top 5.

4) If the average rent increases will be 5%/Y, in the next ten years,

rent accumulation will be : 24K, 24Kx1.05, 24Kx1.05^2, 24Kx1.05^3…or

about 300K.

5) The value of a house is : 391K + 300K = 700K. Since the RE is in bubble

territory the expected sale price will be much lower. Therefore, rent

cannot rise at 5%/Y.

6) The nonstop deflation. Rates clusters : 3M, 6M, 1Y, 2Y, 5Y, 10Y, 20Y

and 30Y. Cluster #1 : between 1989 and 1995. Cluster #2 : between

2000 and 2006. Cluster #3 : between 2007 and 2019. Two flatbed zero

rate : between 2008 and 2015 and between 2020 and 2021, Since 2021

all rates were tangled with each other, rising together, but lately the

spread between the 3M and the long duration is rising.

For the first time the 3M is above the long duration. Cluster #4 might be formed, until the long duration rises above the 3M. Between them a recession that will cleanse excessive debt.

“Cleanse debt…” Debt is not dirt. They have different letters. The letters, e and b, are clustered closer to the beginning of the alphabet whereas the i and the r are near the latter. This is something that Professor Irwin Corey had spent considerable effort explaining. You may find some of his exploratory work on alphabetic clustering on youtube. He still stands out as being one of the most distinguished academics in the modern era.

How – the good prof! Certainly a a ruin standing tall and proud over the surrounding rubble!

may we all find a better day.

New privately owned housing units under construction, 5+ units :

987K, down from 1,001K in July 2023.

Lots of Wolf Street readers take interest in the money supply and its effect on inflation.

I’m not particularly knowledgeable about this in spite of reading the comments here.

That said, Morningstar’s John Rekenthaler has a short article, November 27:

“What’s Really Driving Inflation and Bond Yields?

Long-standing questions about macroeconomic behavior are relevant again.”

At one point he provides a graph comparing M2 money supply with CPI, 2 year lag.

In the 70s and very recently there was a fairly strong correlation. But from 1980 through 2020 there was minimal, if any, correlation.

The 70s and early 2020s had spikes in money supply, the 40 year period in between had more modest changes to money supply.

His conclusion: The money supply indicator is ambiguous except when it rises or falls quickly.

This is a reply to my post regarding money supply correlation (and lack thereof) and inflation: Rekenthaler’s article.

Outside the 1970s and 2020s there certainly isn’t evidence of much correlation between the two. However visual inspection suggests there may have been some causation between the two in short intervals. Given that other factors presumably affect inflation besides money supply, these intervals may not be that noteworthy (?).

Can we talk about the price of men’s haircuts? A visit to the barber—in LA—is $40 easy (not including tip). It’s twenty minutes work for a simple clipper cleanup. However, in London, supposedly one of the world’s priciest cities, there are rows of shops offering cuts for £15 (~$19), including a hot towel finish. What’s the economics with this disparity? Does the UK subsidize clip shops?

Ca pricing and cost of living . Supercuts in East Texas 15 usd . Houston had haircuts from 5 to 10 usd at the Asian places

Been cutting my own for 29 years. I dont do a great job (sometimes I do) always, but 95% of the time it is as good as and usually better than what I got long ago from Supercuts or (was it ?) Procuts.

And they would ask : Is that ok ?

Seriously ?

Admittedly I’m not Brad Pitt or Tom Cruise good looking, but the haircut usually took me down a couple points unfortunately.

I did get an extremely good cut once but the gal up and left for Idaho (I was living in TX at the time, early 90s).

During the covid forced small-business shutdowns, I learned to cut my own hair with a $40 clipper set. Considering the price increases (after reopening) I decided not to go back to my old barbershop. One of many products/services I’ve walked away from.

HollywoodDog,

Two haircuts of $40 pay for electric clippers. YouTube videos on how to cut your own hair are free. Takes a little time to get the hang of it (work from home during that time, LOL), then it’s kind of fun in the sense of using power tools in a skillful manner. Not going back to the barber.

Did same. I suspect if you’re handy, it’s easy. If you’re not, and you just don’t have “skills” it ain’t going to go well. Some people can do stuff, others can’t.

I’ve saved at least $1k since the kick off of Covid. And sometimes the cut is better than I got at the barber (only sometimes!).

You got clipped. Cut your own hair. It’s not hard, unless you want it styled so you look like a poofta.

HD – hey, if you’d been going to John Edwards’ barber, forty bucks would look a bargain, nay?

may we all find a better day.

This seems to be a very DIY crowd. I guess I don’t need to ask about the best place for an oil change! :)

You could also find a like-minded friend and cut each other’s hair. I have a buddy who I do that with bc haircuts in my town are also $40+.

HollywoodDog

Just do what you like. I’ll cut my hair but pay to have the lawn mowed. I’m a ginger and don’t enjoy working in the sun. I save the few rays my body can handle for play. Others cut cable, drive cars till they die, and stop drinking lattes. To each their own.

When the Fed says soft landing, they mean not crashing asset prices. The

dollar of course will get crushed and

those who don’t have the ability to command higher wages or haven’t

any assets to shelter wealth in, get

left behind. Same as always.

Almost choked on my coffee this morning although I shouldn’t be surprised at the propaganda coming out of Business Insider (yellow journalism at its finest).

Their headline, “The Fed will cut interest rates 6 times in 2024 as the US economy slows, ING says.”

I realize it is ING saying it, but BI used it as their headline.

Can’t honestly trust the media for much. Kissinger died and most of the press celebrated his legacy instead of calling him an unconvicted war criminal, with some media exceptions. I was surprised Wells Fargo made reasonable equity predictions, from my perspective, for the 2024 market.

Replace ALL reporters by AI, would be a lot cheaper, and no worse.

Exasperated article coming on consumer spending and the BS headlines it got.

I read a story yesterday that Sports Illustrated just got caught using AI writers. P.S, I bet at least one person that comments here had a Sports Illustrated “Football Phone” (the worst phone ever) in the 80’s…

Went to get a duplicate key for my recently purchased Mitsubushi Mirage sub compact. The price was $300 plus tax for one key. The dude said this was a great deal as the manufacturer was charging $500. That’s some serious inflation in my book.

BS. Inflation isn’t a fixed price, but a change of price of the same thing over time. So where is the price of the key fob you bought a year ago? Or a month ago, for month-to-month inflation data? Duh.

All the info you gave us is a $200 DISCOUNT. That’s the opposite of inflation.

Wolf,

I was just joking with you. You took the bait.

I know you don’t like my inflation tirades.

Meanwhile the yellow metal makes another move. Looking to make a new all time high very soon. Maybe today.

OMG. You picked a great user name because only a caveman still believes these rocks have value. Correction, one of them does have value. Silver does have a lot of uses and is definitely underpriced. Not so much for the yellow rock.

Well, the rocks I picked up at 200 an ounce 2 decades ago I can sell for 2100 an ounce now……yaba daba doo!…..with no analysis or worry. That’s some inflation protection plan.

yep me too = at least over time it seems to keep up with inflation

Well, stocks with 100 PEs are hardly less questionable in value…

Sounds like somebody burned their fingers on yellow rocks and won’t be fooled again. Industrial demand for materials doesn’t have anything to do with their suitability as money.

Quote from Wall Street Journal today:

Federal Reserve officials are increasingly confident that they don’t need to keep raising interest rates to defeat inflation. But they aren’t satisfied enough to declare an end to hikes—let alone to start a discussion about lowering rates.

On Friday, Fed Chair Jerome Powell offered the strongest signal yet that officials are likely done raising rates, but his comments were laced with caution.

“It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease,” Powell said in remarks prepared for delivery in Atlanta.

…he signaled a higher bar for any further hikes when he said officials would “tighten policy further if it becomes appropriate to do so.”

Powell’s comments leave the central bank on track to hold rates steady at their December meeting while maintaining public guidance that their next rate change is more likely to be an increase than a cut.

And the market is rallying on that again. Hasn’t the end of rate hikes been “priced in” now for months? How many times can the market rally on the same thing?

It looked like today was a small cap day. Basically they have been flat all year while the big growth stocks (mag 7) took all the gains until now. I think Russel 2000 was negative for the year up until a few weeks ago.

For as long as the excess liquidity is still sloshing around, juicing all asset prices.

The FED completely failed to rein in the speculators. Some of these soundbites almost make it sound like they’re jawboning them to run everything up even higher.

Exactly. They want to get CPI inflation under control, but they clearly don’t see asset bubbles as problematic.

You are absolutely right. Bitcoin up 150% for the whole year makes me sick. Too much liquidity and Fed’s slow QT is done on purpose to prolong the asset bubble.

Kevin, yup. The problem is that asset inflation ultimately leads to CPI inflation. As long as the asset class feels “rich” from their stock and housing gains, inflation will be at 4-6% every year indefinitely.

I saw that too. It’s like Powell says X, and the media (all the media) says he said negative X. It’s a little creepy.

I didn’t watch much of the talk he did this morning. I tuned in for one question he was asked about the wealth inequality and how the Fed can address it. He talked about that’s the fiscal side issue with tools to help with tax policy and education. He didn’t mention how QE was to blame and QT could conceivably reduce the gap unless I missed it. Algos went crazy though and I’m sure they are reloading for the 2PM discussion to get all the retirement plan 2PM order executions to be bagholders at least for the day.

“he was asked about the wealth inequality and how the Fed can address it”

When the hell did that become the Fed’s job?!

When they created the problem, it became their job to fix it.

Consider the WSJ is merely the print version of Fox News. Your mileage may vary.

Not sure what happened today but the home builders stocks are all up big. Did I miss something? I saw the economic construction report was at .6% growth and was triple over the prior report of .2% growth. The expected number was .3%. Is this why?

I am thinking Homebuilders would not be hitting ATHs if there was trouble on the horizon? Homebuilders stocks tend to trend down before trouble starts hitting the rest of the housing market (foreclosures).

Powell said, we’re debating whether to hike or to hold, and he said, “It’s too early to speculate about rate cuts.”

The only two words Wall Street heard were “rate cuts.”

🤣

LOL Selective hearing.

JP is smart. Just keep all the sheep focused on the shiny “rate cuts”. The first rule of QT is don’t talk about QT. Thankfully, most can’t even spell it.

Don’t assume the market is rational, or that there’s a reason for price moves. Trust your gut.

So, for the average wage slave and salaried Joe, as long as you don’t have to eat (let along feed a family) or pay rent, everything’s swell.

Is it me, or is Mr. Market calling Jerome’s bluff?

Inflation-adjusted income from all sources has been rising in 2023. In other words, in 2023, income growth outpaced inflation. That was not the case in 2021 and 2022.

https://wolfstreet.com/2023/12/01/oh-deary-no-our-drunken-sailors-did-not-suddenly-sober-up-on-the-contrary/

Personal income from all sources, adjusted for inflation, but without transfer payments from the government – so this is income from wages, interest, dividends, rental properties, farm income, small-business income, etc., but without Social Security benefits, unemployment insurance, VA benefits, etc. – jumped by 0.3% for the month by 2.3% year-over-year (adjusted for inflation).

This income growth is a function of rising employment, rising wages and salaries, rising interest incomes, rising rental incomes, etc.

Per-capita disposable income, adjusted for inflation (total income minus taxes), jumped by 0.3% for the month, the biggest increase since May; and by 3.9% year-over-year. This is what consumers had left to spend on goods and services and to save. And it has been outrunning inflation by a wide margin all year, after a steep setback due to inflation in 2022.

In other words, per-capita disposable income has been outrunning inflation by 3 to 5 percentage points all year. This is where the money came from to do all this spending:

I took the data back only to June 2022 to cut out the huge distortive effects of the stimulus payments, and the year-over-year comparisons to those stimulus payments a year later.

Per capita means average. The median, and mode, could be quite different. You’ve seen the comments on this site that think all (ALL) the income gains go to the top and the middle class gets squeezed. I have no data, just reporting the mood by many.

I see the middle-class spending like drunken sailors all around me. They come from all over the country (tourist town), and from the neighborhoods around here, and they’re spending like drunken sailors. I also see homeless people. But the homeless people will never move the needle of consumer spending because they don’t have any money to spend.

BTW, this is about the economy overall, growth v. recession, and it doesn’t make one iota of difference to the economy who does the spending as long as the money gets spent and circulates. And when wealthy people spend — they tend to spend a lot more than poor people — it also creates jobs and incomes for others. Spending is important. The problem arises when the wealthy people don’t spend; when they just hog their wealth.

Powell should just give up and resign in shame. He’s a clown at this point.

The market is the clown.

My opinion……Over the decades one thing I have learned……when the markets speak…….listen…… They usually know a lot more than we do.

The markets, including gold, are expressing a strong feeling that rate hikes are over. As for cuts……but Powell has never been someone that leads markets, he always follows, so cuts are probably not on the table for a while. . As for the level of rates, in a boom generated by the largest and second largest generations in history, the level we’re at is barely back to normalcy and will not be enough to throw us into a tailspin…..hence the markets like what they hear.

But rate hikes being over isn’t enough. They have to drop substantially for current market euphoria to be justified.

Do the markets know something we don’t?

Is the spineless Powell planning on returning to ZIRP in the next few months?

@fred flintstone any idea why platinum after decades of being about the same price as gold is now worth about half as much as gold (I just noticed this recently and really have no idea why there is such a big difference in the price of the metals, or why platinum watches are still usually more expensive than the same model in gold).

I will not pretend to know much about platinum other than to state there is only one gold. When the US decides to sell its 700 billion dollar official store (does not count what private citizens or other us government agencies and states own)of yellow rocks I’ll consider an alternate.

catalytic converters evs do not need

Platinum is an industrial metal. Gold has been money for about 5000 years.

Apartment…who knows?

Perhaps platinum prices are manipulated like gold prices are (see JPM folks recently sentenced for such).

“My opinion……Over the decades one thing I have learned……when the markets speak…….listen…… ”

You mean like when the market pushed bond rates to near zero? And equities to PEs never seen before?

GOT IT.

Well…..LOL……that was not really a market. It was a fed gone berserk.

Who cares? ‚Markets’ are rallying seeing nothing but rate cuts. 10 yr yields lost 85bps from it’s high of 5.05% very quick.. Gold’s at ATH. Stonks not much behind. Happy days.

Wolf, I can’t reply further to the thread, you’re answering the wrong question / missing the point. PCE data tracks nominal changes in income and expenditures. I’m simply looking at wages. The downshift in nominal wage growth is a really important data point worth watching and tracking. I’m not making a forecast based on a single month. I spend far too much personal time watching this data myself and when something significant changes, it’s worth noticing and watching to see if the trend continues. The change in October is either an anomaly, or something broke. The streak ended in October until November and beyond prove otherwise.

No, I didn’t answer the wrong question. As long as wage growth is higher than inflation, it’s stimulative. Nominal wage growth by itself doesn’t matter. If you get 5% wage growth, and inflation is 9%, consumers are in terrible shape. If you get 3% wage growth and inflation is 2%, consumers are in pretty good shape. To check on the health of consumers, wage growth has to be seen in light of inflation.

Sure, wage growth has come down from the surge of the prior two years. Inflation has come down too. That’s what rate hikes were supposed to accomplish, and they’re doing it. Lower inflation, lower wage growth, more balanced labor market (instead of labor shortages). That’s what the tightening cycle has been all about. Did you miss it?

What you NEED to pay for: up.

What you WANT to pay for: level

Other than gas which is now back to its annual autumn drop aided by US and global slowdown.