You guessed it: For over half of it, taxpayers are on the hook. Time to take a look.

By Wolf Richter for WOLF STREET.

The mortgage for “2 Cooper Square,” a 15-story luxury apartment tower with 143 units in the NoHo neighborhood of Manhattan, is now over 30 days delinquent, according to the Commercial Observer. In 2010, when the building opened, three-bedroom apartments sported asking rents “as high as $20,000 per month,” gushed the Wall Street Journal at the time. In 2012, the developer, Atlantic Development Group, sold the long-term leasehold in the building to Wafra Capital Partners in Kuwait for $134 million. In 2019, Wafra unloaded the leasehold to David Werner Real Estate and Emerald Equity for about $85 million – a loss of nearly $50 million, or about 37%.

At the time of the deal, David Werner and Emerald obtained a mortgage from Goldman Sachs of $65 million. The mortgage was securitized by Goldman Sachs in September 2019, along with mortgages on other commercial properties, into the commercial mortgage backed security GSMS 2019-GC42, where it represents 6.1% of the collateral.

And 15 months later, the mortgage is 30 days delinquent.

Occupancy plunged from 96% last year when it was securitized to 82% in the third quarter of 2020, according to a note by Trepp, which tracks and analyzes CMBS. Trepp notes that the loan has not yet been moved to the servicer’s watch list or the special servicer.

The other day, we discussed two luxury apartment towers whose occupancy rates had plunged into the 70% range during the Pandemic – the “New York by Gehry” in Manhattan whose mortgage had been moved to the servicer watch list, and the NEMA in San Francisco. But the mortgages on those properties were still marked as “current.”

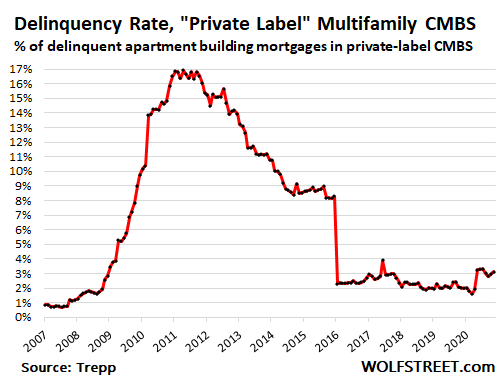

Overall, the delinquency rate for these multifamily “private label” CMBS loans – “private label” because they’re not backed by the government – has ticked up to 3.1% in November but is still relatively low compared to the blow-up during the 2009-2012 mortgage crisis when the delinquency rate reached 17% and stayed there for a year, and compared to current delinquency rates of hotel CMBS (19.7%) and mall CMBS (14.2%). More on that straight line south in a moment (delinquency data through November provided by Trepp):

That straight line south occurred in January 2016 when a delinquent $3-billion CMBS loan tied to Blackstone’s $5.3-billion purchase of Stuyvesant Town-Peter Cooper Village in Manhattan – a property with 110 apartment buildings on 80 acres with 11,250 apartments – was paid off.

So for now, landlords of apartment towers in the centers of large cities, afflicted by the renters’ exodus and plunging rents, and landlords anywhere afflicted by renters not making rent payments, protected by eviction bans, are still trying to make mortgage payments on their rental properties, hoping that the surge in vacancies and non-payment of rents are short-term phenomena and that people will come back and fill those apartments and that tenants will catch up with the rent.

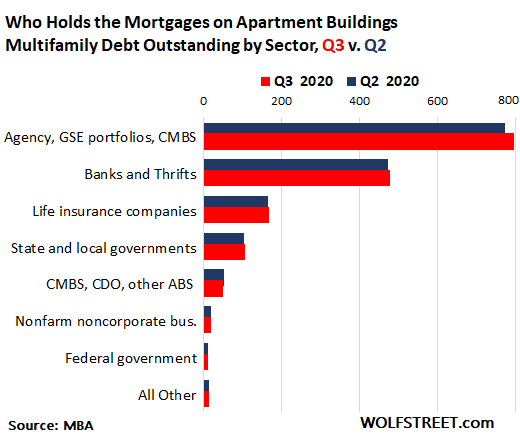

But how much apartment building debt is there, and who holds it?

These “private label” CMBS and other private label securitizations only hold a small portion of the total commercial mortgages backed by apartment buildings.

The total amount of multifamily mortgages outstanding in Q3 was $1.65 trillion, up by $31 billion from Q2, according to the Q3 report this week by the Mortgage Bankers Association, based on data from the Fed’s Financial Accounts of the United States, the FDIC’s Quarterly Banking Profile, and Wells Fargo Securities.

The US government: $798 billion, or 48.4% of the $1.65 trillion in apartment building debt, is backed by the federal government through Government Sponsored Enterprises (GSEs), such as Fannie Mae and Freddie Mac, and government agencies such as Ginnie Mae, which securitized many of these loans into CMBS, and sold them to investors. The government is on the hook for losses. And the Fed has acquired $9.3 billion of these “Agency” CMBS.

Banks and thrifts: $478 billion or 29% of the multifamily debt is held by banks and thrifts. The Fed has pointed out in the past that some regional and smaller banks are heavily concentrated on commercial mortgages, and that for these specific banks, a downturn in commercial real estate would pose a significant risk.

Life insurance companies hold $168 billion or 10.2% of this multifamily mortgage debt.

State and local governments hold $108 billion or 6.5% of this debt in pension funds and the like. This ultimately also sits on the backs of taxpayers.

Private label CMBS, collateralized debt obligations (CDOs), and other asset-backed securities only hold $52 billion, or 3.1% of this $1.65 trillion in apartment building debt.

The chart shows holdings by sector, red for Q3 and blue for Q2 (data from the MBA):

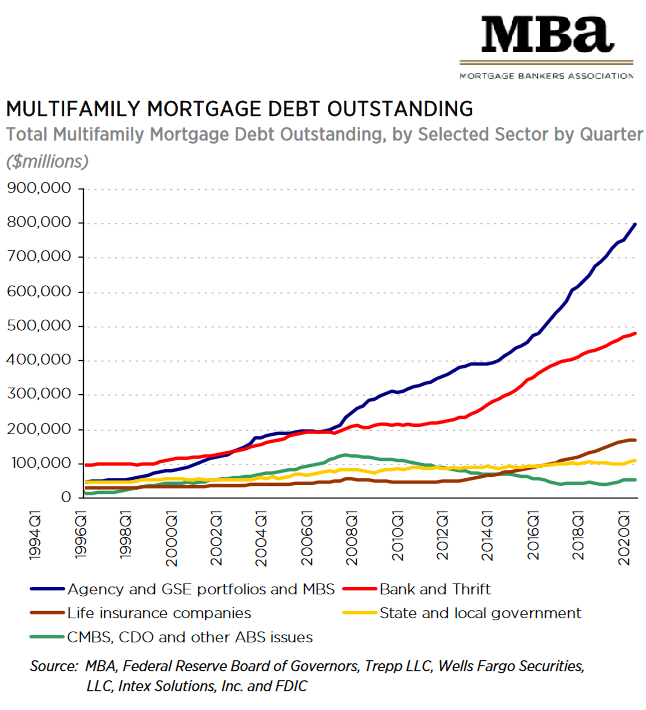

The US government started barreling into multifamily debt during the Financial Crisis. Until then, government-backed multifamily debt was about on par with the holdings of banks and thrifts. Since then, the government’s share (blue line in the chart below) has shot up to nearly 50%.

Banks and thrifts have remained active, and their total holdings grew over the years (red line), but their share declined, as the government’s share surged.

Private label multifamily CMBS (green line), which blew up royally during the Financial Crisis and since then had to compete with government-backed entities, are down by about half from their heyday before the Financial Crisis and dropped again in Q3 from Q2 (chart via the MBA, click to enlarge):

The federal government is guaranteeing nearly half of the multifamily debt outstanding. With state and local government holdings included, taxpayers are ultimately on the hook for $906 billion, or 55%, of it. So if this debt begins to topple in a serious way, it’s the GSEs and agencies that take a big part of the licking, even on CMBS that they sold to investors.

The good thing is that, in terms of commercial real estate, the GSEs and agencies are limited to multifamily commercial debt and they don’t work with mall loans and hotel loans, whose losses are now accruing to investors and institutions around the world.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Create a bubble and sell it to passive investors’ retirement plans

If that doesn’t work sell it to the FED

If that doesn’t work hold a politician hostage until the taxpayer buys it.

But under no circumstances can a billionaire ever be required to lose even one penny!

Billionaires not losing isn’t good enough, sorry. The wealth must double.

No Billionaire Left Behind.

– The Fed

bingo

as the cabals continue to run merica

a ONCE GREAT COUNTRY

…continue to RUIN merica… fixed

No Billionair Left Behind .. the Guillotine.

Trickle down only works if there’s BILLIONS upstream!!!

Ok I’ll stop posting. You are doing good work. But you are underestimating the fundamental lack of accounting at the Fed and banks. Banks haven’t had to follow accounting rules for any of their trades, per Deloitte, since January 2020 because they defanged the Volcker rule in September 2019 the same month I left the accounting profession. Auditors don’t throw words like “defanged accounting for bank trades”, especially not Deloitte, especially after Arthur Anderson. When learning to write accounting opinions there are only 2 opinions that we can issue and we have to memorize them. All the opinions are standard issue so in the case of accounting being “defanged” we need to be able to clearly specify the fact AND give an opinion. The lack of opinion regarding the Volcker rule means that it’s not a positive opinion.

I’ll try to stop posting and filling up the modbox but there is so much good information here and the bigger picture isn’t even in focus. What’s the saying about building a house on sand? Well that sand is now our accounting standards.

I left accounting but now I’m completely focused on distributed ledgers. Can you think of a reason why? Enron? 2008? September 2019? January 2020?

– huge fan regardless.

“distributed ledgers” = “cryptocurrency”, correct?

Focus grouping on the internet is a terrible idea so this might not go so well.

Crypto definitions:

Bitcoin – reference to the entire ecosystem crypto graphically secured. Including CBDC. If you can access the Bitcoin liquidity then you are part of the ecosystem.

Blockchain – reference to the technology.

Distributed ledger – reference to accounting that is verified and not centralized.

Cryptocurrency – jargon to confuse you. If it’s decentralized it’s a currency if it’s centralized it’s a security. These definitions come directly from the SEC, IRS, Treasury,and FTC all saying BTC is a currency. Cryptocurrency just means it’s encrypted. But it doesn’t tell you if it’s a currency. Investing in cryptocurrency is a bad bad bad idea.

I think most people understand “cryptocurrency” to refer to a distributed ledger relying on cryptography and blockchain.

It’s not really possible to do a practical distributed ledger without some for of cryptography.

I mean I know there are many things you can do with a cryptographically verified distributed ledger but … most applications are very niche, except for currency.

Cryptocurrency doesn’t have to use a distributed ledger. Central bank digital currencies aren’t going to be using a distributed ledger because they are ‘centralized’. You can use the Bitcoin code and just keep it in house like an intranet controlled by the central bank decision makers. Cryptographically secure but not trustless or verifiable. It’s like having a really powerful safe to keep the contents safe but it’s empty. Otherwise they would verify.

Oh Millie! You made a few rather astute comments, but I can see where you don’t know what the truthful definition of money is. I’ll give it to you now. Money is an idea backed by confidence. The amount of confidence people have in ANY medium of exchange is how sound of a money it is. The confidence that someone down the street or around the corner will accept it in exchange for what YOU want, is what makes it stable. As the confidence level goes down, the perceived purchasing power of that medium of exchange goes down as well, and that is why we have what we call inflation. It’s the costs of goods and services going up and up to keep the equation balanced.

In 1925, an ounce of gold would buy a man a pretty nice suit, and in 2020, an ounce of gold will still buy a man a pretty nice suit! Even in ancient Rome, an ounce of gold would buy a man a pretty nice outfit of a toga with a sash and broach, sandals and a sword too! How about that?? This is all the proof we need to see about how it’s the human labor we are trading back and forth via our mediums of exchange.

You are 100% correct about digital currencies and cryptos too, they can evaporate back into the aether in the blink of an eye when the power goes off!! Nobody but a total FOOL would ever buy into THAT scam!!

Randy you are sooooooo wrong!

Money comes from the government! It’s a check in the mail or an electronic deposit in your bank account. The reason we vote is to decide who gets the money! That’s all you need to know! Stop making things complicated!

Millie Brown,

When I was an accountant, I recall that one of the main accounting concepts was prudence and of course there was the “going concern” concept.

I am not sure if some of these accountancy firms senior partners know about these.

Excellent thinking.

@Randy

“Money is an idea backed by confidence. ”

Money is a medium for economic transactions backed by the history of successful transactions.

The confidence in money is built on volume, success of past transactions and perceived security of the money.

In today’s world there are many different moneys in competition.

It begs the question .. who is the billionaire & is it a case of ‘who is the billionaire’ .. are we choosy ?

You are so right. I feel a slight schadenfreude at the idea that the utterly corrupt, greedy, grasping banksters are going to ultimately suffer some of these loses, even though most will be suffered by legitimate persons like states, local governments, insurers (many legitimate if not very nice people), etc.

Unfortunately, our economy is amazingly interlinked, like a spider’s web but in multiple dimensions. Thus, we will all ultimately suffer. The most catastrophe-proof businesses, ordinarily, will suffer more and more: e.g., few people now seek legal help with traditional cases, so even large groups of lawyers are suffering. Lawyers are now even reluctant to take wage and hour cases, for unpaid overtime and doubletime which allow recovery of statutory legal attorney fees, because some companies are not expected to be around to pay later.

I fear that one side wants to spend a lot of funds, which is only practical if they agree to tax the vast fortunes of the ultra rich, which have escaped taxation for decades through the exclusion from taxation of their foreign income. (That foreign income exclusion from US income taxation has meant that it is much more profitable for the ultra rich to invest in countries like China: they pay no taxes there, get subsidized loans (albeit they are required to get a CCP-parasite as business partner), get the services of quasi-slave labor, probably even access to the bodily organs from murdered Falong Gong, Uighurs, etc., avoid the risk of their workforce unionizing, are not subject to environmental laws, etc., etc.)

They even managed to pass the “investors” visas laws, which I like to call the organized criminals immigration preference act. Higher-level, organized criminals, who do not have criminal records, have profited enormously from being able to immigrate to the USA just by showing that they accumulated enough capital (regardless of how they actually got their money.)

The other side does not want to spend enough money except to bail out the banksters and their largest, crony companies. It is only willing to provide a just enough, a tiny amount of aid to the rest of Americans, to make the huge gifting of US government funds to the ultra rich barely palatable. Hence, while congresspersons struggle as the boat goes nearer and nearer the gigantic falls, it is safe to predict that we are all going over those falls in 2021.

Which ordinary Americans will suffer? It is safe to predict that the largest, essential companies’ employees will surely be safe: e.g., Walmart, Amazon, supermarkets, etc. The rest will just have to take their chances.

No wonder people are getting skeptical of free market capitalism.

We haven’t seen it for so long we’ve forgotten what it looks like.

True original 1776 free market capitalism, could no longer exist after the industrial revolution. The best current option is a properly tuned mixed market economy (that over time could more and more resemble that 1776 free market economy). But, America is now effectively a plutocracy, with a wellfare system.

1776 free market capitalism would be a far fetched standard. Even 1976 free market capitalism would be an improvement over what we’re looking at now.

It would, but you cannot revert back to a previous economic state, you have to figure how to create a new one with inspirations from a particular time period or country.

Very good and interesting discussion above, here’s my 2 cents.

ANY “market” will always be dominated by the largest players, i.e., those with the most money and/or control/influence over “law”, our supposed mechanism for deciding what is right and wrong, best and worst, instead of just letting a Monarch and relatives do most all of it.

So how about for starters we completely drop this mystical mythical self-adjusting “FREE” notion crapp so we can solve our distribution of “stuff” problems with clearer and more rational thinking? I’d say we first need some boundaries to this game of marginal propensity to consume.

The ancient Greeks (at least those who had the time to, as they used lots of slaves as their fossil fuel) endlessly debated, “What is the good life”, but then growth forever was obviously no problem back then, it is now.

A,

Almost entirely accurate, but, you can’t forget about the millionaires with only tens and hundreds of millions. These are the true job creators and the economy can’t prosper without them.

Relax, once deflation sets in, everything will balance out and stocks will go to the dark side of the moon and income from rents will be offset by exploding property values. It’s easy money everywhere for everyone because debt and risk are just old fashioned crap that doesn’t matter.

” Japan’s core consumer prices dropped in November at their fastest pace in a decade as the coronavirus pandemic hit demand, stoking fears of a return to deflation and wiping out the benefits former premier Shinzo Abe’s stimulus policies.”

MC, when and where did property values explode during deflationary episodes? I think implode is the right term.

explode is correct this time

because the DEFLATION will be 100% in currency(our great fiat $dollar)

so $100 will by piece of gum but no BREAD FOR POOR

try that on when I charge $100,000 a month for rent and govt pays it for you

protect your wheel-barrels (they’ll be worth more)

of course the GREAT RESET will wipe out 99.9%

then we can have govt GREEN SOY for dinner

sure glad us boomers won’t be around

but mils and ZERO’S will get their just rewards for being woke

Unless you plan on checking out in the next 2 weeks boomers are 10x more leveraged than the woke generations. Your house of cards will go up like Moses burning bush.

Why are us Gen Xers always forgotten?

rip,

Not forgotten, just skipped over. The Xers want to follow the ways of the Hipppie generation, but, don’t have nearly as much money or positions of power as their parents have. Whereas, the younger generations see and are forced to live in the aftermath of it all, and want change. The X’s lack of a commanding amount of money or power, combined with their lack of ambition to change anything, means they are usually not worth mentioning.

Wow, Thomas, did some Gen Xers hurt your feelings somewhere along the way? My comment was directed at Joe Saba, not you. But your screed shows your nasty contempt, so let me clear a few things up for you:

Us Gen Xers have no interest in being like the burned out Boomer druggies who came before us and who steer this country into hell. We are not the children of Boomers, we are the children of The Silent Generation, and their values are what we carry. We have a lot of ambition, and have worked hard for everything we have, yet were the first to get the shaft.

Nope didn’t get my feelings hurt, I was more describing the general younger generations attitude. My more accurate dipiction of Gen X’s isn’t gonna pass the censsors.

Lol to the rest of what you said.

Japanese people have long memories. Americans have none. That’s not an insult, rather it’s an advantage when it comes to bubbles.

How can deflation ever set in? What’s the mechanics?

continual debasement of $dollar as usual

you all just have WOKE up to it yet

been happening since 1972 when NIXON took us off gold standard

REAGAN used it to buy votes and every politician since figured it out

SPEND TODAY and give bill to next guy

but next guy’s time – today IT’S DUE

why PENSION DEBACLE has been pushed down road for decades now

now it’s due and we’re reaping its just rewards

worthless $DOLLARS abound and going exponential

debasement is HOW govt is going to bailout SOCIAL SECURITY

you’re still only going to get $1,500 month or whatever

but you ain’t gonna be able to live on it for long

I’m already pricing out retired who get $1,000 a month

I still rent to them but that surely isn’t 2 1/2 times rent(ie minimal qualifications for working folk)

Protect against dollar deflation with leveraged real money-gold and silver miners :>{) Disclosing my bet

The median income doesn’t even remotely support the median rent if 2 1/2 x income is the metric.

One mechanism is debt deflation. If you loan me $100, that loan is your asset and worth $100. If I fail to pay, your asset is now worth zero, thus reducing money supply.

When people have no money, demand drops to zero, and so do prices. This deflation mechanism helped wreck agriculture in the Great Depression. No one had money for ag commodities, so crops rotted while people starved. That is a complete system failure on the part of Dear Leaders that control the system.

That is the brick wall we are headed for.

This is why the FED is shoveling money into the banks and buying up their garbage, while the banks continue to loan massive money for houses, cars and everything else to people who have no prayer of ever paying it back. Because the moment they stop lending, the entire house of cards is toast.

According to financial economist Michael Hudson deflation sets in when the financial sector suck all the profits up for themselves, leaving ordinary people bereft of disposable income (i.e., not enough money to buy all the stuff we so much like). Lack of demand reduces prices. It’s why Hudson recommends large scale debt forgiveness. To avoid debt deflation.

Chris Herbert,

Nonsense. There is already a well-established and functional process for debt forgiveness in the US, and it’s called “bankruptcy” whereby a federal court supervises the process. There are different chapters in the federal bankruptcy code for different types of debtors and different types of debt forgiveness, from restructuring to liquidation. It works.

You think we have huge wealth inequality right now? Wait till debt forgiveness is done in full. A lot of wealthy people are wealthy because of debt.

Lack of income growth equals lack of demand.

Lack of economic growth equals lack of income growth.

Lack of workforce growth and productivity growth equals lack of economic growth.

It’s been happening for over 20 years.

‘debt & risk are just old fashioned crap’ gone are the days of thrills & chills.

I guess I Can now tell Women that I am a Real Estate Investor, with vast holdings.

?

The government bans evictions thus forcing defaults on the loans they own.

The circle of life?

“The federal government is guaranteeing nearly half of the multifamily debt outstanding. With state and local government holdings included, taxpayers are ultimately on the hook for $906 billion, or 55%, of it. So if this debt begins to topple in a serious way, it’s the GSEs and agencies that take a big part of the licking, even on CMBS that they sold to investors.”

Does GSE really take a licking…OR…do they take the keys to those castles and then sell for a fraction to the same entities (different LLC from same Master Co) from whom they foreclosed? Taxpayers eat the diff, but keeps the asset(s) working ??

That sounds like the usual asset stripping of the taxpayer exercise I’ve come to expect from the corporate types running our government.

But they could also monetize it in a big ongoing bailout with a lot of freshly printed (or digitalized) moolah. That’d be a great way to ‘introduce’ a digitial coin straight from Yellen at the Treasury, no Fed needed. Plus a handy jump on the inflation front.

Don’t worry, blackrock will buy them all up for pennys on the dollar and then you can rent from them at an inflated price! Yinz people aren’t thinking in terms of the great reset.

ah working for STORE

Taxes fight inflation, as well as income inequality. Reverse the Trump windfall tax cuts. Resources are the ‘hard cap’ on Congressional spending. You cannot buy that which is not for sale. Fairly simple. But of course incompetent political leadership could screw it all up.

Exactly and this should be held as a criminal act against both parties.

True, but our financial criminal laws and judicial methods/rules are being printed/shaped right along with the money….all “as needed”. Nothing happened to anyone in ’09, except Madoff who just confessed and sorta forced them to prosecute.

Couldn’t even guess at any end game plans, I don’t run in the right circles. But I doubt very few do, other than the hide in NZ type stuff, which won’t work for long, anyway.

Corporate socialism is beautiful! Broke peasants and government balance sheet are the best places for the society to allocate losses.

Wolf , terrific analysis . Debt is debt ,but leverage is an altogether other dimension . Once it goes in the negative direction it slides so fast that the owners of the debt have no time to respond to the event and then it is , whoosh .

Very wise statement. Everyone likes leverage on the upswing, none more than real estate ‘owners’ with little equity in the game. Downside they are looking to make sure someone else takes the loss.

In Portland a lot of new apartment buildings , just opened for occupancy at the beginning of the pandemic. I have heard that often the debt for these is held by local banks during the construction and pre-lease out phases and then when they have reached a certain occupancy these loans can be cleared by turning it in to a CMBS giving the original bank and developer a chance to get their profit from the project. Most of these places are almost vacant ,as you would assume given the challenges of leasing during covid and the exodus from the urban core. So will most of the pain for these fall on local banks or the holders of CMBs’s as described in the article.

Sounds like CMBS holders are the bag-holders – by your own analysis. Then CMBS holders get bailed out by Fed SPV (presumably).

The developer is the likely bag holder if the building cannot be securitized into CMBS. The developer’s equity is disappearing if the income is nonexistent and the loan cannot be securitized if there is no income stream. The bank will foreclose if the developer’s equity disappears.

> So will most of the pain for these fall on local banks or the holders of CMBs’s as described in the article.

No, it will fall on all market participants who rely on the secured repo market because agency debt and agency derivatives are used as collateral, HQLA collateral at that… once that HQLA becomes trash… it will start a whole chain reaction of insolvency in repo where people are post fractions of the collateral backing transactions and dealers use said collateral in other transactions (rehypothication).

Will make sept 2019 look like a cake walk… cross asset correlations go to one in wholesale liquidations of leveraged positions unwinding on thin markets.

I’d be willing to rent one of these places for pennies on the dollar, but they “aren’t gonna give it away,” so they sit vacant. Not in Portland, mind you, but somewhere else.

“Not in Portland, mind you, but somewhere else.”

Pre-Obama QE and gentrification Portland was a very reasonably priced place to live. (Seattle too!) Oregon’s economy was largely built on forestry and agriculture/fishing and the population was not wealthy. Most demand for real estate has been coming from outside the state. Almost moved there once because the housing prices were so low compared to the east coast. The question is how long the speculators can keep housing prices inflated.

How soon everyone forgets.

What’s happened is sinful. These central bankers, in my opinion, are economic terrorists.

I’m so excited! I always wanted to own big real estate like this! (Said no sane taxpayers ever)

Right but most of this isn’t with a view of Central Park, that is only a small portion. No comfort, seems the housing bubble of 2007 is the apartment bubble of 2020.

Covid and a decade of construction focused on tier 1 downtowns is creating some interesting outcomes. There is a glut of faux luxury condos and apts, middle class folks with good jobs gonna be priced into up scale market lol

They won’t be able to even afford the property taxes and condo fees.

After the financial destruction of the rentier class, we might see local governments giving property tax deals to plumbers, elevator repairmen and such to take over the HOA payments on luxury condos to keep the downtowns from emptying out.

Does anyone know what happens to contracts that default on the blockchain? The contract foreclosures on you. Austerity just leads to more austerity. Solidarity or this nightmare doesn’t end.

yah we turned power off – hahahaha

blockchain is pure stealing of the Stup kind

James Corbett just did a video on that very subject brought to us by the reset king himself Klaus Schwab Supposedly they plan to take down the power grid and this “ Boomer” has zero debt and lots and lots of real hard money

If you have to turn off the grid to kill Bitcoin you agree it’s really really really big. Going to such extreme lengths, to global blackouts, nuclear fallout, and solar storms I think you secretly comprehend the scale of Bitcoin. You aren’t convincing yourself and you aren’t convincing me.

Final Austerity: Some big men with guns come and torture the defaulter to give up his code keys; then they rob him of any digital assets available, unless they never knew the defaulters true identity.

It really depends on what kind of contract it is, you could have a solidity contract on ethereum that requires over collateralization held with a third party that can only be released back to the owner when the last payment to address, you could have a solidity contract that requires x amount of cpu power verified every min via root access to the machines while mining XMR… or you can just plain old unsecured lend in a stable coin…

So when does the federal government enforce the law and arrest people for laundering fake money into real dollars. You know the money that Congress creates. The money that is a real IOU, not a snake-oil salesman IOU. Capitalism is based on greed versus fear of loss. If the Feds guarantee something, the fear of loss disappears.

Governments never had a monopoly on “what is money”… sure they can enforce whatever they can, when they can, where they can, and sometimes even issued their own… but it doesn’t and has never constrained the boundary of what is possible… one only needs to look at this history of trade to understand this and jettison any beliefs of “what money should be”…

So, Wafra crystallised a $49mm loss, from 2012 to 2019.

I wonder if anyone knows, who did they sell their rotten apples to ?

Or did Fed outsource them a license to do some in-house printing?

Thank you for the great insights Wolf.

Interesting info, but right now nothing is liquidating at least in SoCal and prices are as high as ever.

It seems that everyone has hit the pause button.

I don’t see opportunities as in 2010 , none.

Anecdotally, a friend who owns a big construction company is building three hotels right now, and it seems investors are optimistic looking beyond the pandemic as a temporary aberration.

It will be interesting to see how it plays out.

Memento mori,

I’ve talked to several landlords with larger buildings. They’re convinced this apartment issue will blow over by the summer/fall: vaccines, people will go back to normal, tech will bring people back to the office and will make them live in the big city again, etc. etc. That’s what they’re hoping and counting on.

So there are hardly any transaction in those cities since no one knows how to price a building that now has 30% vacancy rate, and is surrounded by buildings with similar vacancy rates, and where current owners are convinced that these buildings will be fully rented out a year from now. Buyers don’t see it that way. There is just no meeting of the minds.

Schedule E tax form landlords are screwed more than Schedule C tax form landlords.

I think these landlords are living in a fantasy world. I’ve talked to many people, who work at tech companies, banks, marketing companies, some even the Fed, and many others. Almost NOBODY is eager to go back to an office five days a week. That means that companies will either have to collude to make everyone come back, or those that don’t allow any work from home will lose their good employees to competitors.

Now that people have seen the light, I just don’t see the world going back to exactly the way it was 10 months ago.

Maybe I’m wrong, but I don’t think so.

RightNYer,

From what I have seen, I think you’re right. But try to tell landlords that.

Right on rightr,,,

While the political and hopium effects of the vaccines will be very helpful for a lot of folks, the majority IMO,,, the actual results are likely to be a ton less, if for no other reason the ability of this particular virus to change/mutate/adapt.

Some deep thinkers of the past century or so have speculated that the ability to change,,, and especially the ability to change fast in response to environmental challenges, will be the deciding factor as to which species, or possibly types of species, will be the eventual ”winner” of the process suggested by Darwin and developed by several biologists, both biochemists and microbiologists.

We are, in fact, once again, ”living in interesting times.”

For which many of us living through the very boring decades, decades ago might give thanks for at least trying to keep us paying attention, eh?? LOL

To paraphrase what has been said many times, many ways – It is difficult for a person to accept change when their income depends upon not accepting the change.

Hope springs eternal in the minds of Real Estate people of all genre. Have never heard a realtor say it is a price soft market in residential homes. This is really a sea change in commercial real estate, and secondarily, in residential rental properties.

If the population of potential renters is job and income poor, they may be doubling and tripling up in private homes across the country before they attempt that kind of people packing in a traditional rental apartment complex. Harkens back to the living conditions in Soviet Russia after WWII.

Landlords will be doing spot checks going forward, and taking down license plate numbers to try to trace occupants. Would not want to own residential rental property at this point.

Frankly, rented out a condo on a lake in Florida for 11 years, and would rather take a bullet than ever do it again. Most tenants must have grown up in a barn, they will sublet space if you are an absentee landlord, were perpetually late on the rent, and always used the Security Deposit for their last month’s rent. Then when I sold it for a loss (bought at top in 1980), the IRS hit me with tax on Depreciation Recapture. WHAT’S NOT TO LIKE.

Have always thought a good business would be turning our 2500+ sq ft homes into duplexes.

Could probably do it for much less than these “tiny house” contractors are charging.

There was quite a bit of “doubling up” and multi-generational families in the US in the 30’s.

Here in the North SF Bay area, I’m now seeing “offices” for rent on Craigslist within suburban homes. 4 offices in a 4 bedroom house, for example. Not sure if that will be perceived as more safe than an office building in SF. Might work. Might not. Is it creative flexibility or desperation from what used to be Airbnb investors.

Nothing in the US is going back to normal again in my opinion Collapse of the word reserve currency will change life in the states and not for the better

Vaccination will take months at best.

And vaccines means no more free money from the government so that means people having less money so… things won’t go back the way they were before. Not everyone will get their jobs back.

2021 will be better but a full recovery is going to take time. The closest we will get to back to normal will be in 2022.

Must be some pretty deep pockets to have not only weathered the storm until now, but to be prepared for more carnage until next fall.

Real Estate is a slow moving train or ship like titanic. It may take years for things to unfold.

I was here during last bubble. I can see irrational exuberance all around which is: we are special and this time is different.

No way, SD can support median home price of $600K with a median household income of $60K but who know when would this end ?

I’d love to leave CA and looking for an exit plan.

I have many friends who lost jobs here and are on unemployment. It’s gonna be interesting to see how long this extend and pretend can go on.

But right now, real estate is hot in San Diego!

Real estate is a slow motion train wreck. Impossible to stop, but easy to avoid.

Here in a West LA mid range condos and townhouses are sitting on the market longer, things have definitely cooled down, despite still low inventory. Have seen some but not many price reductions.

“mid range condos and townhouses are sitting on the market longer”. True. But, in West LA, mid range houses are red red red hot.

“mid range condos and townhouses are sitting on the market longer”. True. But, in West LA, mid range houses are red red red hot.

Is the optimism due to the promise by Donald Trump that at the end of the COVID-19 vaccination program we will all be fast tracked back to normal ??

And what if the vaccine fails ??

Square one again or is there a loop hole somewhere ??

My daughter moved to St Kilda, VIC. this week .. she looked at all the empty apartments & said “Eny meeny miny moe”

As far as I know the vaccine suppresses getting sick but still allows people to carry and spread the ‘vid. Not sure how it’s going to open the floodgates to a return to normalcy once say 60% have the vaccine.

The mRNA bunch are thrilled at cheaper, faster vaccines, and are also talking therapeutics with dollar signs in their eyes.

That’s getting pretty deep into our basic genetic bodily functions.

I have been reading up on protein misfolding and amyloidosis.

Me too, and it’s depressing and a bit scary.

Loop hole somewhere ??

That would be Big Pharma’s non-liability agreements with the State’s blessing. That would be Big Bidness’s demands that ALL lowlymokes get the pokes — the reticence in doing doing so meaning that those ‘conspiratorial’ non-compliants get ghosted! That would be Big .Gov doing a job well done! palming those benjamins …. for the sole benefit of their Oligarchic Donors.

mRNA vaccine is safer than the traditional vaccine by design. As the paper on Immunity magazine stated mRNA allows APC cell to look at the freshest image of antigen. Also in theory, mRNA doesn’t have much ADE effect like the traditional vaccine and can trigger inner cell and body fluid antibody while the traditional vaccine only triggers body fluid antibody.

The correction mechanism in covid-19 make it mutate at half speed of other coronaviruses.

Most likely people will go back to their normal lives, just like more than a million people take flights on daily basis now.

ying,

“…just like more than a million people take flights on daily basis now.”

Yes, that happened on Friday and Saturday, peak pre-Christmas traveling days. But last year, 2.3 million people flew on each of those days. Through Dec 19, the 7-day moving average is down 65% from the same period last year. So this is VERY far from “normal.”

People designed airplanes….at it for over a hundred years….took 3 1/2 Billion years to get to eukaryotes, and then another 1/2 Billion to get to Homo sapiens and other multi celled stuff. Thats 4 Billion years of random trial and error…..BIG damned diff!

Molecular Biology is way over it’s skis and now mostly profit rather than curiosity driven, not to mention less “tangible” regulation than the FAA, including the economics/politics…you know, patents and all….and one can’t really see or change the parts, ya know?

Pretty arrogant, eh?

Here’s some more good reading for ya…..it’s theory, too, just like your “info”.

https://pubmed.ncbi.nlm.nih.gov/30250470/

If these residential buildings default, HUD will probably be the agency that buys back the property. Then they either run it, sell to non profit, or sell to investors. Usually they want a price based on historic comps which will be too high, so they will either run it or turn it over to a GSE. In the end all this “luxury” housing will land up as govt housing.

My wife ran Section 8 apartments for a RE company for years. If that’s any example of where all this stuff is going, this country is going to the dogs.

We won’t need any military to “protect our shores” as no other country will want to take this land over.

I think we are already there. Don’t let the Chinese and Russian fear mongering fool you. They have enough problems of there own. Who on earth attempts to occupy a country that is as insanely armed as the US citizenry, much less military.

There is an old quote that said: “You cannot invade the mainland USA, for there would be a rifle behind every blade of grass.”

As a rule, public housing in Victoria at least, but most likely all over Aust. is left empty, to rot, while the public linger on a 5 year waiting list.

You don’t know how tanks work.

I know how they think … and it’s generally nothing good.

That would truly be a best case scenario, but having looked into both HUD and USDA RE rules, loans and dealings I get the feeling it’s a good old boys network..

Print it and done. No difference if it comes from taxes or de-basement. We lose. The stand-off weapon of de-basement is the preferred fleecing cannon of the state. Taxes are messy and require a some what functional government and are personal. De-basement is like a drone, hit the kill button over here and let the impact happen over there. Cowardly behavior on every count.

According to the Census Bureau, the median price of a new single family home has almost doubled in 20 years. That is about 3.5% compounded annually.

Not sure how that effects vacant high rise apartments.

My county only has 8% of its ICU beds vacant.

Dr. D,

You are correct.

The G prefers to work by fraud. (Debasement).

Then implicit force. (Taxes)

Then making examples. (Individual “justified” persecutions)

Then explicit mass violence.

Internal reform is more or less inconceivable to a G…what is the point of having ascended to the top of the slippery/sh*tty pole (poll?…) if not to make your will, writ?

A fundamental betrayal of Constitutional, citizen based government but clearly the trend for multiple decades.

Actually, you have the order precisely backwards, Cas127. The state is established via mass political violence. It then exercises its monopoly over the legitimate use of force to impose taxes. Finally it issues a fiat currency which is the only thing it will accept to settle its taxes, fees and fines. Only then is debasement available, though it really doesn’t have much meaning in monetarily sovereign states which float their currency (don’t peg it to any other currency or commodity). And while there are massive amounts of unused labour due to un-and-underemployment, fiscal stimulus is wise, both economically and politically.

In theory, in a properly functioning democracy, this state power is used for the benefit of the citizenry. Of course, in the US you have a plutocracy instead, courtesy of a democratic process suborned by the “donor class.”

Good luck …

New motto same as the old one:

“Make America Inflate Again!”

Every textbook definition of inflation is that it comes before deflation, not after but don’t take textbooks at their word. Inflation has never happened after deflation in human history. Rome, Zimbabwe, and Venezuela inflation preceded deflation. What comes after isn’t inflation. End stage capitalism won’t be any different.

In five years my property taxes have increased 1400$ from 3000$ to 4400$ they will simply foreclose in none payment of taxes happened in depression inflation destroys everything like 40 trillion govt owes default dollar were all broke start over like Russia did

A lot of people are migrating because of property taxes. It’s pretty easy if you live in a high tax city and state to cut by by 75% for equivalent housing once you don’t need live in city for a good paying job.

Get some gold and you will always have the ability to pay when the hyperinflationary boogey man shows up at your door, which it will ultimately

True That!

Gold is only good for spec trading, if you are into it, and know how to do it well.

When a serious inflationary boogeyman shows up at your door he most likely won’t be selling anything.

And he’ll/she’ll/’they’ .. will demand your food to boot!

“Gimme”

You only have the ability to pay the Government it’s due if you can find someone to legally convert some of your gold into the Government’s currency. There are no guarantees.

“You only have the ability to pay the Government it’s due ”

How much do you think the G is “due” after its policies (and outright money printing) have destroyed the interest rates on savings for two decades?

ZIRP operates on short term Treasury debt as a 100% tax on savings’ interest.

Unvoted, essentially unacknowledged by DC…but transferring the economic power of those (already taxed) savings to the State…a State so incompetent that it has accumulated a debt larger than the world’s largest economy it feeds off of.

DC is due plenty.

And it isn’t another dollar.

@Cas – Gov shouldn’t be due much: manage the legal system, defend borders … gee, that’s about it. Deciding who to give to, and giving them piles of virtually and actually free money, isn’t a legitimate Gov task.

Wow, I am not a drinking man, but I am heading to the ABC store!! Just keeps getting better and better. Another example of how the Government getting involved in every aspect of private business blowing up in the taxpayers’ faces. Let’s continue to guarantee the debt of every borrower with a pulse and no business plan or ability to even execute a plan. Central Planning by another name.

And the bozo’s in the government’s employ keep their jobs, their very handsome pensions, their very generous healthcare, and us peasants eat dirt (figuratively, of course). Or maybe we’re supposed to eat cake on the way to the guillotine. Just another set of deadly “default” arrows in the quivering carcass of the U.S. economy and financial system.

The thing is that we don’t get to choose anything, they, in very poor taste build away, Melbourne CBD looks like a landfill of apartment towers, yuck man !!

The 99% should stop worrying about anything.

The Fed has a magic printing press.

Everything will turn out just fine for the 1%.

?♂️ ?

Quantitative easing (QE) is a form of unconventional monetary policy in which a central bank purchases longer-term securities from the open market in order to increase the money supply and encourage lending and investment. Buying these securities adds new money to the economy, and also serves to lower interest rates by bidding up fixed-income securities. It also expands the central bank’s balance sheet

But it all seems like a game of extreme can kickin’ with a blindfold

There is a faction of analysts who hold that QE is not money printing, among those Jeff Snider, Chief Research Officer at Alhambra Investments.

Mr. Snider holds that QE just places dollars as reserves within the FED accounts of primary dealers and that there is no effective mechanism to introduce those dollars into circulation. This is why, he maintains, we don’t see inflation that would be expected based on the FED’s huge balance sheet expansion.

The below link is to Making Sense Eurodollar University – Episode 16, where Jeff Snider makes the case. His point is made in the 1 minute 20 seconds from minute 4 to 5:20.

There is a ton of inflation, but it’s mostly asset price inflation which is what QE produces.

You have to look at what kind of inflation: asset price inflation, wage inflation, producer and wholesale price inflation, and consumer price inflation.

Inflation = loss of purchasing power of the dollar, with regards to assets, labor, producer prices, consumer prices… they’re all different. You can have high asset price inflation and no wage inflation, for example.

Wolf,

Here’s the causal chain as I see it.

1) Via ZIRP/QE, the G guts interest rates (ie, by hiking the money supply, interest rates – the “price” of lendable money – fall, as lendable money far outpaces uses of/demand for lendable money – borrowing).

This is the famous “pushing on a string”

2) As interest rates collapse, the Discounted Cash Flow formula causes asset valuations to soar…because under the DCF, existing levels of cash flow from existing assets become much more valuable.

In essence, ZIRP destroys the appeal of Treasury bond investments, forcing more and more money seeking a return into any other invt.

3) *But* once those artificially inflated (by QE) asset valuations are “bought” by subsequent asset owners, existing levels of asset cash flows are absolutely crucial…any decline is magnified due to DCf under ZIRP.

And trying to *increase* valuations is very, very difficult because the actual cash flows underlying the QE elevated valuations, may/probably weren’t equally elevated.

This might be mostly clearly seen in an apt building invt example.

QE gutted rates cause apt complex sales prices to soar (check).

But now, the complex owner is highly exposed to *any* reduction in rents (because of covid, renter job losses, etc).

*And* trying to “profit” off of the apt complex (by hiking rents) is very difficult…because whereas the Fed can destroy interest rates with a QE push button…the benefits of that QE may slowly/never flow to renters.

So you get misery in the apt mkt, as over obligated landlords try to ratify their initial valuation errors (courtesy of the Fed) by taking it out of the already stretched flesh of their tenants.

4) The exact same dynamic applies to any financial mkt asset…it only appears more benign because the valuations zoom up faster/more transparently and the “ratifying” consumer inflation operates more opaquely/slowly/ineffectively.

Any of which are bad for *somebody* – owner/shareholder or renter/consumer.

Wolf – NPR had an article that has a chart lableled “Income Growth Dwarfed By Rising Costs”. (search “NPR Paycheck-To-Paycheck Nation: Why Even Americans With Higher Income Struggle With Bills).

Where the inflation hurts the most is the “big ticket items” that include health insurance, college, and housing. Over the last 20 years, the chart shows wages increased 10.4%, yet housing increased 31.5%, college increased 55.7%, and healthcare increased 57.3%. The inflation of high value indescretionary life survival necessities is what is wiping out the middle class, and currently even the upper middle class are boarding the same inflation titantic. I own a property in an area where the average income is six figures, and I can tell you that the “property tax inflation” increases (and the $10k SALT cap) are now hurting those with six figure incomes, and it gets worse by 5-10% per year. Property taxes are relentless and never ending, never seem to go down, never seem to stay stationary, and are basically a shelter rent fee to simply exist on planet Earth. And anyone moving from “high tax” states to “no tax” states will soon realize that the property taxes are often times higher than if you paid 5-6% income tax, but only 1% property tax versus no income tax and property tax rates of 2-3% (often on inflated tax valuations, which is just as impactful as the rate of tax itself, and easy for tax authorities to manipulate higher once they have everyone at manipulated higher valuations. There is no easy way to fight inflated “COMPS” once they get everyone inflated at the same time…).

Beware anyone escaping high tax states as every state is pretty much “high tax” once you hit $75k/$150k income limits. Do your homework as once you take all the taxes into consideration, there is very little difference state to state, and it could take years to make up the cost of selling your house and the moving expenses, etc…

Yort,

You need to do a bit, possibly a ton more research into the various and sundry TAX totals of different states of USA…

Time and enough to figure out YOUR situation versus each state situation to know how best to make yourself happy re taxes…

I always keep in mind one of my best mentors comment, ”Be happy to pay taxes, it means you are successful.”

May we all live in ever more interesting times…

Wow really, look there is nothing to see here never mind worry about. I mean just look at the stock markets all at or about new highs. So many companies trading at huge multiples of earnings ah sorry I meant losses. Its all roses and sunshine and the vaccine will have everything back to normal as it was before in a jiffy.

Of course extend and pretend can’t last for ever but what possible harm and problems are there in 10’s of Millions being unemployed and homeless likely to bring?

Just in case anyone reading this takes it seriously it is made with sarcasm out the wazoo!

It is stunning to hear DC Dunces yammering on about what title to use for Biden’s wife while the whole country is facing desperation. They are arguing about sending a few hundred dollars to working stiffs instead of developing a real plan.

Dear Leaders have no ideas whatsoever except to add a bit more Bread to the Circus. A group of random ten-year-olds could do better.

These people are evil. Truly.

Babylon Bee had this do to a T, with re. to herr doktor “Jill”!

I think that there is a mind set in play & when a curveball occurs no one know what to do .. the system is the system & avoid, avoid at all costs is the reaction.

“Look Frank, a stink bomb” .. “Just don’t look at it & it will go away”

Thank you for having me.

One bad sign is value investing is nearly dead. Average stock holding is a few days not a decade or so. There basically is no investing now, only speculation. We can lay this at Congress and the Fed as speculation is getting rewarded. The Fed probably thought that they could ease us back to real investment within a few years, but once you are overvalued by 2 and 3 times it’s too far down to go without collapsing the financial system. That’s probably why the talk of a managed reset by billionaires. They know current trajectory leads us over the cliff.

Everybody knew what the outcome would be, but the FED just couldn’t contain its greed, like a gluttonous animal gorging itself to death. Despicable.

In 2012 sold for $134 million. In 2019, resold for about $85 million – a loss of nearly $50 million

This spotlights what is wrong in the world now. At this level of money dealing it makes no personal difference to the parties. They get paid well regardless of the deals. This is possible due to the Fed policy of free money – to those dealing in huge amounts so skims are possible all around and no one has their real world skin in the game.

Another example is corporate salaries. I don’t remember the details exactly but it was something like a CEO of a company with 5,000 employees got a bonus of $50M. Now which would be better for the economy and everyone; 1) the CEO buys Tesla stock because he can’t figure out anything else to do with the money, 2) each employee gets $10,000 to spend on a car, appliances, furniture, whatever.

Having dual economic structures – real world and monopoly world – will lead to undercapitaiization and depression in the real world and hyperinflation and then collapse of the monopoly world. What is the intrinsic real world value of a Bitcoin with monopoly world value of $100K? What is the intrinsic real world value of a small office building with monopoly world value of $1 billion?

We all live in the real world, though some can manufacture an artificial environment that appears substantive.

The real world now is like a freighter in a rough sea with all the cargo sliding to port side.

“In 2012 sold for $134 million. In 2019, resold for about $85 million – a loss of nearly $50 million”.

Don’t worry, they can make it up in volume.

I wasn’t worried about them. They are well paid and all busily pushing the ship’s cargo to the port side and don’t realize they also will sink.

Not much really more obvious than to see the face of a smart guy – absorbed in a specialized world – suddenly realize he forgot one very important real world factor and his angel will write him off.

Hubris works until it doesn’t.

One issue to ponder here is the relationship between things at FRED, like:

Personal current taxes: State and local: Property taxes, Billions of Dollars, Not Seasonally Adjusted (S210401A027NBEA)

and

Median Sales Price of Houses Sold for the United States, Dollars, Not Seasonally Adjusted (MSPUS)

As more people have less discretionary disposable income, in a recessionary environment, savings will go down and going forward, property taxes will rise in relationship to the increase in home values.

That increase will at some point become a barrier that will become harder to factor out, as people buy homes that will be beyond their price range. Looking forward, Biden will likely want to help more people become home owners, which will create insane supply/demand issues not unlike the pre-housing bubble/GFC.

In terms of the Fed (tax payers) owning more housing, that’s axiomatic and will play an interesting part of this WTF economy and the WTF Recovery.

One thing you can bet the farm on is that property taxes (and other taxes and fees imposed at state/local level) will increase despite stagflationary environment.

Exuberant home buyers are going to get fleeced with blunt shears when they get property tax bills going forward, since they are overpaying for houses in a frothy housing bubble.

Everyone in same neighborhood with comparable houses will share in the pain caused by overpaying buyers, since prevailing purchased house prices determine your house’s taxable value even if you haven’t bought or sold in decades.

Anyone who has owned a house through boom and bust times knows that local government appraisers are quick to pencil in rising house values (= tax increases) based on current market values, but house values are sticky on the way down as far as the taxman is concerned.

For a while cities and counties will try every tax trick in an effort to maintain their bloated governments without meaningfully cutting fat off their carcasses. Eventually taxpayers will get the message and either vote down tax increases or vote with their feet.

There are more homeless people than ever, living on the street, in cars, in RVs and every other thing imaginable. There are way too many houses for what’s coming.

Just board, but over at FRED, this mortgage garbage is broken up nicely @

Quarterly:

L.219 Multifamily Residential Mortgages

Private pension funds and REIT’s have been dumping stuff while GSE’s and other gov entities picking up stuff. ABS issuers may be interesting to watch.

The difference between the 90-day AA Asset-backed commercial paper and a six-month Treasury Bill is almost even with the 2-year Treasury yield — and that’s sort of new territory, going back to when asset-backed garbage pools didn’t exist.

That basically implies nobody wants to pay anything for future value, but I’ll leave that bone for Wolf to chew …

Just beating a (credit flow) dead horse here, hope that’s ok:

“To support further credit flow to households and businesses, the Federal Reserve will broaden the range of assets that are eligible collateral for TALF. As detailed in an updated term sheet, TALF-eligible collateral will now include the triple-A rated tranches of both outstanding commercial mortgage-backed securities and newly issued collateralized loan obligations. The size of the facility will remain $100 billion, and TALF will continue to support the issuance of asset-backed securities that fund a wide range of lending, including student loans, auto loans and credit card loans.”

Martha Careful,

TALF is among the SPVs that will expire Dec 31, 2020. And so far, TALF has bought very little.

Quoted from my article last week: https://wolfstreet.com/2020/12/11/update-on-the-feds-qe/

“Five of the SPVs are set to expire on December 31 – PMCCF, SMCCF, MLF, MSLP, and TALF – after Treasury Secretary Steven Mnuchin sent the infamous “Dear Chair Powell” letter to the Fed on November 20, where he explained that these five SPVs were no longer needed for numerous reasons that boiled down to markets are frothing at the mouth, and that those funds could be better used for fiscal support of the economy. Fed Chair Jerome Powell responded with his own “Dear Mr. Secretary” letter.”

The world is completely upside down. How can the Fed conclude that growth is better than expected when they are running the printing press like crazy? how do banks get buybacks approved with debt monetization running full throttle?

More going on here than just money printing. Trump blowing up so many regulations have put the economy in a better place than anyone expected.

What’s going on here is that the government (Trump administration, Congress) engaged in the most radical borrow-and-spend ever over the past 9 months, after having already blown huge holes into budget during the Good Times. This comes on top of the $3 trillion the Fed printed.

I have to say that I am pretty impressed by how small the State pension fund investments in this category are. I would have thought they would have been bamboozled into buying this paper with both hands. With $2.6 trillion in total assets… only holding $108 billion of this paper means that just 4.15% of the pensions are in this “asset category.”

Moreover, that assumes that ALL of the CMBS listed in Wolf’s charts are held by the pensions… while in fact some may be used to fund (if that is the right word) local real estate projects

SpencerG,

They likely hold “agency” CMBS (first and largest category) that they bought from Fannie or Freddie. There’s no credit risk involved; taxpayer has their back.

Assuming “There’s no credit risk involved; taxpayer has their back.” will always hold forever more into the future… there is still interest rate risk (and basis risk)…agency trash that no longer has any cash flows wont be available to use as collateral in repo (or be available to use in a leg in swaps transactions)…

Tax receipts are dropping, so I don’t see how the taxpayers – who only provide about 1/3-1/2 of government expenditures anyway are on any hook. Biden can whistle past the graveyard about increasing taxes, but historically that has generally reduced the overall take. Tax payers are not without intelligence.

More accurate to say MMT has their back.

Good to know if you are a pensioner I suppose. But as a taxpayer I would rather my state not buy high and sell low in its pension plans.

Agency debt and Agency derivates are used as collateral in repo markets… thats all you have to know…

Thank you so much Wolf for reporting on this. Most people would never even hear about it if it were up to the establishment media.

1) Add $2.3T to Section 8 gov debt to keep it open in 2021.

2) We don’t know who did it. We don’t know how they did it. All we know

is that someone is better than we are in cyber.

3) Sun Tzu’s advice : don’t interfere, let the enemy destroy themselves.

From: COVID-19 Handbook

Yale Program on Financial Stability

As of October 20, 2020

By comparison, the COVID-19 Section 13(3) programs have more risk built into them, as they

are accepting a wide range of assets as collateral, including accepting lower quality collateral than

the Fed has accepted in the past.

Several Fed programs will accept as collateral, “fallen angels,” bonds that were initially given an

investment-grade rating, but which have since lost their investment grade rating due, in part, to

the economic slowdown brought on by COVID-19. The following programs show the range of

collateral that is being accepted:

• TALF can buy new AAA CLO tranches

• PMCCF can buy syndicated loans, and “fallen angels”

• SMCCF can buy HY ETFs and high-yield bonds, including “fallen angels”

This is a fairly decent recourse.

I’m curious though, is there a mini-liquidity freeze headed our way to start out 2021, or will the current administration restart programs like TALF? In addition, that new level of risk, with an incoming admin, along with a massive explosion of virus cases (globally) will make for a dramatic start to 2021. With less than 1% of our population vaccinated and the new super-mutated virus accelerating transmission, it’s hard to believe that there won’t be many months of trouble ahead … and probably an entire year (+) of slower growth.

Short term interest rates are falling, BofA is worried that zero rates, and declining volume of short term from Treasury (which might drive yields down further), would put pressure on MM – read NAV. In the last MM event, 2008, Treasury paper was the firewall, this time it might be the kindling. Wiser heads might suggest the reason for dropping short term rates is the economic malaise coupled with a raging bull stock market. Then those who are piling into bitcoin at any price may prove the wiser. What does a mini-liquidity freeze look like? Perhaps the Fed can feed money into the MM system to maintain the $1 benchmark.

The new no-risk Covid economy is challenging in terms of valuation guesses, and it’s a bit uncertain as to how backstops will work within the ZIRP landscape.

Years ago, it was easy to use the Fed model to look at valuation ranges, thus, using the Current S&P 500 Earnings Yield of 2.68%, based on earnings reported Jun 2020, we can see that the 10-yr Treasury @ 0.94% is obviously mismatched.

Furthermore, the 2-yr Treasury yield is apparently a fine proxy for where the 10-yr will be a year from now — and that’s at 0.13%! Hence, once we add Tesla to the mix, increase S&P price/decrease yield — add-in a mini liquidity crisis, add-in a vaccine shortage, increase a global super virulent virus mutation, see greater unemployment, more lockdowns, bankruptcies, etc., … the markets should literally be exploding to huge upside potential, as speculators race to hit the buy buttons (before the remaining idiots run out of cash and or have margin calls).

AS for MM, the presidential transition process in the next 4 to 6 weeks will be interesting! Some have suggested that programs like TALF were not critical, we shall see …

No matter if we’re pondering cars, houses, apartments, bonds or even, God forbid, stocks, disposable income is primary — but perhaps it’s also worth pondering the supply/demand dynamics of the Law Of Diminishing Marginal Utility.

Recently lifted from the internet: “Marginal utility may decrease into negative utility, as it may become entirely unfavorable to consume another unit of any product. Therefore, the first unit of consumption for any product is typically highest, with every unit of consumption to follow holding less and less utility. Consumers handle the law of diminishing marginal utility by consuming numerous quantities of numerous goods.”

WFH is the future.

WFH cyber guards exposed us to malware since Mar 2020 and made us weaker.

1) $600 + $1200 = $1800 gov dividends.

2) $1800 : 0.02 = $90,00 portfolio. Thx US gov.

3) $900 for PPP and poor citizens. $1.4T to keep the new gov open until Sept 2021.

4) A new strain of Arab Spring virus, 70% more contagious, metastasized to Europe and US.

5) We need an Arab Spring vaccine.

Supposedly there’s new limits to the powers of the Fed. I hope someone will do an analysis on the wording to see if there are any loop holes along the likes of Blackrock acting on behalf of the Fed.

Of course there are loop holes!

Fed can do the same thing…just give the program a new name…good to go.

1) $900B + $1.4T to keep the gov open will start inflation.

2) The commodity cycle is on.

3) After a long slog down DX Aug 24 2020(C) and Dec 14(C) in a Bullish

Divergence.

4) DX downtrend is strong. DX might need Bullish Divergence #2 before popping up.

5) There is hope for 4,600SPX.

6) A correction to 3400/3500 might come first :

a) it’s an opportunity to buy at the low.

b) SPX will be in a new TR to build a cause on the right hand side of the chart.

c) use what u got : do PnF to the left, as between Feb 28(L) and Mar 3/4 2020, a cause for SPX plunge to Mar lows.

7) Rydex Assets Ratio : Bears plus MM cash divided by Bull Assets was at the lowest point on the chart in Dec 2020.

8) A deeper correction might send SPX monthly RSI to a bearish territory.

SPX will have to do a lot of work to regain the bullish territory.

Are these real posts or is this a bot?

Will anyone buy $900 billion worth of U.S. debt at 900bps. If not, is the Fed going to buy all of those tbills?

why 900bps?

Sorry was supposed to be 90bps

look at Jap. gov yield and owner distribution.

Fed just got handcuffed via $900 Billion stimulus agreement Sunday:

1. The $429 billion in unused CARES Act funds allocated for Fed lending just got repurposed (can not be used for state aid).

2. The four lending facilities have been permanently closed.

3. The four lending facilities have been “forbiden” to reopen.

4. Future clones of the Fed programs have been banned.

Wonder if this is why futures have not spiked on stimulus approval. Perhaps sell the news?

Does the new innovative lending facility only need approval from Treasure Secretary and Fed chief or from both houses?

Is the reason democrats gave up $2T package in exchange for 900B because the election shattered their dream of controlling both houses and no way to get to their number after Jan 21?

Does the stimulus v2 have any impact on future stimulus 6 months out?

Congress Strikes Long-Sought Stimulus Deal to Provide $900 Billion in Aid. Somebody doubted Mitch McConnell will agree on the new spending bill before. IMO, GOP is worse in spending money than dem. Whoever in power will kick the can down the road by all means, GOP or dem, until music stops. That’s why wall street parties on.

Damn Wolf you sure have been infactuated with the apartment complex thing. You invested in them or something? People move vacancy rates goes up and down. Nothing is a constant. So people are fleeing the crazy cities. Big deal. Real estate in Florida is booming. I have 4 new subdivisions going in within 2 square miles of my house. Can you blame people to get out of the crazy Democrat controlled lockdown states? Which is where you live. Tough luck.

Randy,

Not blaming anyone. Where did you get that nonsense? Just showing trends and who holds the multifamily debt. It would be helpful if you read the article so you know what’s in it before posting nonsense here.