Complicated times for the dollar. The Chinese Renminbi, a distant also-ran, loses ground.

By Wolf Richter for WOLF STREET.

The last three years were complicated for the dominant reserve currency. At first there was the Fed’s $5-trillion money-printing orgy and interest-rate repression. Then there was raging inflation, which the Fed brushed off as “transitory.” Through this period, the dollar fell against other currencies. But then the Fed got religion and began to tighten: since March 2022, it has hiked rates by 425 basis points, accompanied over the past six months by $414 billion in QT so far. As a result, the dollar bounced off and shot higher against other currencies, particularly the euro and the yen – the #2 and #3 reserve currencies.

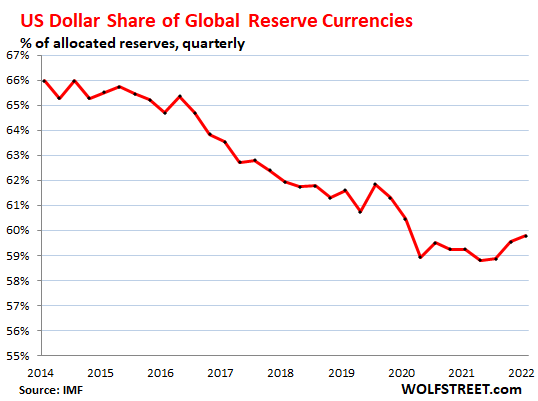

At the end of Q3, the share of US-dollar-denominated foreign exchange reserves rose to 59.8%, the third quarter in a row of increases, and the highest since Q3 2020, according to the IMF’s new COFER data on reserve currencies. Since the end of 2021, the share of the dollar rose by nearly 1 percentage point.

But this increase came off a 26-year low at the end of 2021. Note that this does not include the dollar-denominated assets on the Fed’s balance sheet, but only dollar-denominated assets held by foreign central banks and foreign official institutions:

The dollar as reserve currency means that foreign central banks and other foreign official institutions hold US-dollar-denominated assets, such as Treasury securities, US corporate bonds, US mortgage-backed securities, and the like.

These foreign central banks and official institutions also hold assets denominated in other currencies. And all those assets combined make up the total global foreign exchange reserves, which amounted to $11.6 trillion in all currencies when expressed in USD, according to the IMF’s COFER data; 59.8% were dollar-denominated assets.

The remaining 40.2% were assets denominated in other currencies, primarily the euro, and a bunch of also-rans, whose value were then translated into USD.

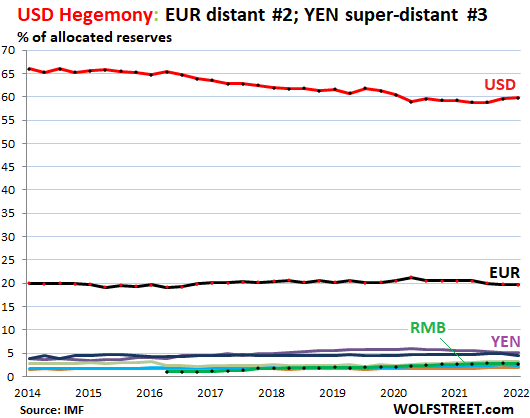

The other major reserve currency, and the also-rans.

The euro is the second largest reserve currency. The Eurozone encompasses 19 countries with a population of 340 million people. Over two decades ago, when the euro was being promoted to Europeans, they often talked about “parity” of the euro with the dollar on all levels: as global reserve currency, as trading currency, and as financing currency. This reserve currency parity made progress until the Euro Debt Crisis brought to light the euro’s structural weakness. And that put an end to this parity talk.

Since then, the euro has had a share of about 20% of global reserve currencies (in Q3, 19.7%), about as large as all also-rans combined. But it was far below the dollar (black line, red dots in the chart below).

The yen (purple line at the top of the colorful spaghetti at the bottom in the chart) had a share of 5.3%. It became the #3 reserve currency in 2018, when its share surpassed that of the British pound.

The British pound, the #4 reserve currency, had a share of 4.6% (blue line just under the yen in the spaghetti).

The Chinese renminbi, the #5 reserve currency, dipped to a share of 2.8% in Q3 — only 2.8%, despite the huge size and global interconnection of China’s economy! Given the capital controls still in place, and other issues, it seems central banks are leery of RMB-denominated assets and are in no hurry to pile them on, despite years of predictions that they would. Folks that expect the Renminbi to overtake the US dollar as reserve currency will have to have enormous patience (green line with black dots near the very bottom).

The other currencies in the spaghetti: Canadian dollar (2.4%), Australian dollar (1.9%), and Swiss franc (0.23%). There are other currencies, each of which has such a small share that it doesn’t matter.

You can have a large trade surplus and a large reserve currency just fine.

The Eurozone has had a large trade surplus with the rest of the world in recent years – particularly with the US. This demonstrates that an economy with a trade surplus can also have one of the top reserve currencies, thereby debunking the outdated theories that the country with a large reserve currency must have a large trade deficit.

But having the dominant reserve currency encourages the US to run up its gigantic twin-deficits: The US government deficits that have produced the incredibly spiking public debt; and the ballooning trade deficit, powered by Corporate America’s three-decade search of cheap labor. Both of these deficits would be more expensive to fund if the dollar were not the dominant reserve currency.

Dollar’s share gains in 2022 may be over: exchange rates and foreign exchange reserves.

Since the end of Q3, the ECB hiked rates and shed a huge €850 billion in assets, and the euro reacted, recovering some against the dollar. And the Bank of Japan made noises in that direction, and the yen bounced.

The values of foreign exchange reserves denominated in euros, yen, British Pound, renminbi, and other currencies are translated into dollar figures at the current exchange rate, so that they can be summed and compared.

For example, within the IMF’s data, the value of Japan’s official holdings of euro-denominated assets is expressed in dollars at the current EUR-USD exchange rate.

The exchange rate between the USD and other reserve currencies impacts the magnitude of the non-USD assets. To stick with our example, the magnitude, expressed in dollars, of the euro-denominated assets held by Japan fell as the euro’s exchange rate fell against the dollar.

So the increase in the share of the USD since the end of 2021 may have run its course because the plunge of the euro and yen have ended, and both currencies have bounced since the end of Q3.

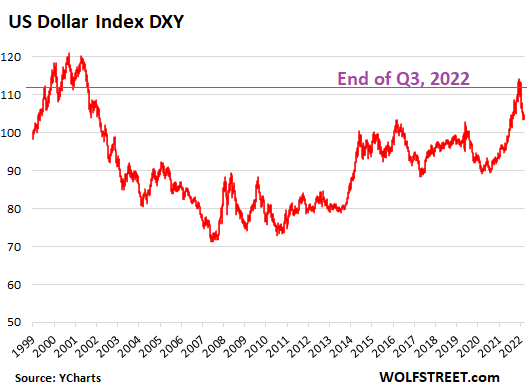

Overall, over the past two decades, the exchange rates of the major currency pairs have bounced up and down within a fairly wide band, as shown by the Dollar Index [DXY], which tracks the exchange rates of the dollar against the euro, yen, British pound, Canadian dollar, Swedish krona, and Swiss franc. The DXY is dominated by the euro and yen.

At the end of Q3, the IMF’s cutoff point for this reserve currency data, the DXY closed at 112.2, where it had been 22 years earlier, in May 2002, but there were big movements in between (data via YCharts):

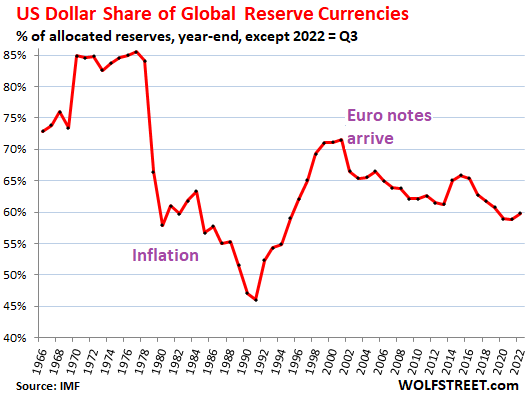

The long-term decline of the dollar’s share: not related to exchange rates.

As we have seen in the DXY chart above, the dollar’s exchange rate with the euro and the yen is back where it had been in 2002. But in 2002, the dollar had a share of 66.5%; and in Q3, 2022, it had a share of 59.8%.

So this portion of the long-term decline of the dollar’s share is not due to exchange rates, but due to central banks slowly diversifying away from dollar-denominated holdings and into securities that are denominated in other currencies.

The dollar had a share of 85% of global exchange reserves in the early 1970s. But over the next 15 years, the share plunged by nearly half, driven by an explosion of inflation that scared the wits out of holders of USD-denominated assets. One of the reasons why the Fed is now serious about cracking down on inflation is to avoid another dollar-fiasco like that:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

With a hawkish Fed, the dollar (DXY) should be able to keep its head above the water, while draining the swamp. One thing Wolf, why is China not included in the DXY?

There are other indices that include the RMB and many other currencies. But the RMB is a non-entity as far as reserve currencies. The DXY is dominated by the euro and the yen, and so is a good measure for those currencies against the dollar.

Wolf, there are also more than 28 Metric Tonnes of Gold in foreign reserves today (only 0.014% of all Gold mined).

That amounts to ~$1.8 trillion of foreign reserves now. The same amount of gold would have accounted for only $300 Billion in 2000 and there was lesser much lesser gold in foreign reserves then.

Can you also start including Gold in the net foreign reserve share because clearly it had a remarkable gain and would most likely continue this trend due to

1. Geopolitical tensions where dollar settlements can be blocked by US.

2. Rampant global inflation that is hurting all fiat currencies and can increase private holding of gold in countries like China, India and many other third world countries possibly increasing gold prices. Please note that many European countries have even higher inflation, but it’s new to these guys, so they lack the experience (or resources) to save gold privately.

3. Some Oil producers ready to accept gold instead of dollars.

I just did a quick dive and got the number to be $2.1 T. Maybe it’s all legacy of the gold standard, but I read central banks own 20% of gold that has ever been mined.

I think in reality your currency is backed by your economic vitality that can fund a superior military so you can set the economic rules of the world.

I think that is how Great Britain defeated Spanish empire. GB had the industrial revolution and Spain was too interested in plundering for gold.

one thing to remember is that master XI is moving as much trade to FRIENDLY countries

which are NOT USSA,EU,Japan,Aussie – ie non-friendly countries

Master Xi’s house of cards will collapse if the US stops importing from China — or even if the US significantly reduces its imports from China. The Chinese economy is dependent on its exports to the US. So Master Xi isn’t moving any trade away from the US, but is traying to maintain it.

Good call old-school for fixing my calculations. Central banks own 28,000 metric tonees of gold, amounting to ~14% of all Gold mined. It’s still worth about $2.0 trillion.

However, I have multiple news reports to believe that Central Banks have been increasing their Gold reserves in tonnes.

I don’t favor gold over productive work, aka real investment, that no longer exists in today’s negative real rate economy. So Gold today remains one of the best store of value (aka reserve) in the global arena!

For OS:

Britain defeated Spain due to the courage and stern resolve of Nelson, Cochrane, and SO many brave PEONs on theirs and many other ships of the British Navy of those times…

Patrick O’Brian is very very clear about that, making the actual ships logs of the times into ”Historical Fiction” in his 20 volume ”Aubrey-Maturin” epic work.

AS ALWAYS,,, ”Might makes Right” was the order of that day, and is clearly continuing these days…

HAPPY NEW YEAR 2023 to all on here!!!!!!!

Leo,

The answer to your question about including gold in “foreign exchange reserves” is NO because:

1. This article is NOT about “central bank assets,” but about “foreign exchange reserves.”

2. Gold is not “foreign” for any country — it’s the same metal no matter who is holding it. So it’s not foreign exchange.

However, gold is included in central bank assets. The Fed, the ECB, the BOJ… they all list their gold on their balance sheets. You can just look it up. It’s listed at some historic value, such as acquisition cost, and it’s not marked to market, so you can get the weight of their holdings and do your own math. But it’s irrelevant for “foreign exchange reserves” for the two reasons I outlined.

Thanks for the explanation Wolf. I guess I confused foreign reserves with assets that can be used for imports :).

Leo,

Wasn’t really trying to correct you. Wolf’s article made me curious so I punched out the value based on what I could find and then I saw you were thinking along the same lines, but I still posted.

I had an opportunity to buy various precious metals a year ago from a family member. That’s about 3% of my wealth plus a large gold stock for another 2%.

For me like China and Russia it’s an effort not to be so hitched to the dollar.

@Leo … I don’t think anyone is proposing gold as an alternative to productive work. It’s better thought of as an alternative to man-made money. It serves as a way to store the value of productive work.

Recall the three hallmarks of money are that it serves as a unit of account, medium of exchange, and a store of value. Currencies do an admirable job as media of exchange, but are wanting as a store of value, especially over the long term. It’s in this latter area that commodity money like gold finds its strong suit.

As far as productive investment goes, it depends on the opportunity set. When financial assets are excessively highly priced, gold can come in handy as a place to park capital. For instance, buying stocks at the turn of the millennium, when a bubble was in effect, has been a loser compared to gold to date. I think of it not as an investment, but a default asset … what you own when you don’t have a reason to own anything else

VVNVet……tactics.

Gold is just one of the hundreds of commodities that one has to chose from to “store wealth”….or trade.

I think it’s main attraction is that it can be EASILY stored at one’s home or under the Aspen vacation cabin, by those of considerable wealth. And it is EASILY forgotten about by everyone, including tax authorities, and can be sold to shady outfits like the Swiss and other “no tell” outfits, if needed.

And perhaps there are a few who still like to rub it, or wear it. Or perhaps buy and sell weapons or drugs with it.

Fossil fuels have much more real world value, but don’t store as neatly.

For 2-3 weeks after the 2017 fires in Fountain Grove (our wealthiest neighborhood) NOBODY was allowed up there until the immediate family were done finding it all in the ashes, and I imagine a lot was “lost”, or never there in the first place for insurance purposes…along with art, heirlooms, and such. There were constant ads on TV to help them put together “lists”.

I often think of crypto as electronic Alchemy…similar purpose to gold, but not so good in the execution, to say the least.

Coin of the Realm for me.

@ NBay: “Gold is just one of the hundreds of commodities that one has to chose from to “store wealth”….or trade.”

Indeed … I chose my words carefully in referring to “… commodity money like gold …”. But it is a standout in terms of its use as a central bank reserve asset, hence its use as an example here.

At least part for the reason you cite as being compact. Also as one of the elementary members of the periodic table, it can neither be created nor destroyed outside of nuclear reactions. This means there is for all intents and purposes a finite, fixed quantity on and in the earth. Oil, in contrast, is destroyed in the process of being used. Even if it were much more compact and rare that would make it unsuitable for use as money.

Note for example this fixed quantity property is one of the merits cited for bitcoin. On the other hand, no one will soon likely impress their sweetie with a beautiful bitcoin necklace …

DXY was established in 1973, when China was of much less significance to the world economy. It hasn’t been adjusted since then, except to account for launch of EUR.

Sure, but that isn’t as much an explanation as a recitation of mere facts…I mean, when one of two dominant world exporters isn’t included…

Wolf’s reserve share argument is a little more persuasive but in the mid to long run, the country with the best productive efficiency (of which export success is a strong-if-not-perfect proxy) will see the importance/unavoidable use of its currency rise.

(Unless the US can pull another petro-dollar miracle/scam/protection racket out of its…productive decline. But it is hard to see China going along with this for any reason whatsoever…not when China is a standalone superpower and has spent 30 years expropriating its own exporters/consumers in order to build internal productive capacity/efficiency, with an eye to dislodging the USD’s “excessive advantage” in currency use/manipulation).

80% of the world’s trade in the global oil market is priced in the almighty Petro Dollar.

But for the last five years, China has been the largest importer of crude oil. Needless to say, there is a push now for China and Russia to bypass the dollar. The ‘Shanghai Petroleum and Natural Gas Exchange’ is the umbrella organization that Xi and China are pushing to run oil trades through the yuan. Xi is trying to get the Persian Gulf monarchies on board with this.

Xi was in Arabia in December 2022, and in Samarkand in September 2022 for meetings with the ‘Shanghai Cooperation Organization,’ of which there are now nine permanent member nations. And 40% of the world’s population is represented in the SCO.

It’s almost amusing to see the names of the groups being organized in this manner, but the coalitions are forming. In Russia this May, the next ‘Supreme Eurasian Economic Council’ will meet, just before the next ‘Belt and Road Forum’ meeting takes place. The goal is to drive towards a common payment infrastructure outside of the SWIFT banking mechanism, and that is the lynch pin of the petrodollar.

Outside of oil trade, Russia and China are working on having the central banks across central Asia, Iran, and India use UnionPay, Mir cards, Alipay, and WeChat Pay instead of Visa and Mastercard; in another effort to break the dollar as the world’s reserve currency.

These moves take many years or even decades to gather steam, but the push is there.

As Washington, London and NATO have played their cards for all to see lately, it will be interesting to watch what happens with the BRICS, South American countries and African countries.

Will we see a new global alternative currency emerge? Time will tell, and perhaps a fairly long time remains for King Dollar to stay on top.

Prairie Rider,

In terms of currencies, reserve currencies, the “petro dollar” or whatever, the first thing you need to do is forget about Russia. It’s a minuscule economy. It’s smaller than the economy of Florida, it’s much smaller than the economy of Texas, it’s less than half the size of the economy of California. The US is a larger producer of petroleum and petroleum products than Russia, it’s a larger producer of natural gas. So forget Russia. Take it out of your currency equation. It just doesn’t matter.

China is another story. That’s a huge economy whose currency carries no weight. And that’s actually not a good deal for the global economy. China’s currency SHOULD carry more weight, that would be good for the global economy and for the US. But China is governed by a freaked-out government that put capital controls in place, and you cannot have a powerful currency with capital controls. So forget that one too.

Forget Saudi Arabia. Another tiny economy. They have oil but the US imports very little Saudi oil, so now they try to sell their oil to China at a discount. That’s great. Good for China. So who cares. Glad someone is buying Saudi oil or else they’d have to eat it.

US oil production CRASHED the price of oil, starting in 2014. If US frackers lose their newly-found discipline, they’ll crash the price of oil again.

I’m surprised you fell for the hilarities you referenced. These people have been pumping the same nonsense for over a decade, copy and paste.

BTW, no one outside the parties involved in the deal cares about what currency a particular oil trade is conducted in. No one cares if Russia sells China oil and prices it in yuan or euros or whatever. Russia can then turn around and buy Chinese cars and other consumer products. What’s the problem? There isn’t one, not for the US, not for the US dollar, not for anyone.

If a lot of trade in commodities, goods and services shift to other currencies than US dollar there may be an impact on the US dollar as a reserve currency. Especially combined with all kinds of political initiated sanctions on trade and money transfer.

The impact will not be on the US dollar position as the worlds reserve currency, rather the usefulness of holding a lot of reserve currency. Why hold a lot of US dollars if a trade agreement with China provides a country a stable trade with one of the world’s largest manufacturer?

With raging inflation of US dollars and now following price rises, how much goods and services can be bought for these reserves today?

The US dollar’s position as reserve currency may not have changed much, maybe more interesting is if the usefulness of currency reserves changes.

The biggest immediate risk to USD’s current reserve status is political, not economic.

The challenge is that there isn’t a viable alternative now, since the Euro poses the same risk.

This is the most sane reason for any country to diversify their holdings.

This question answers itself:

“ Why hold a lot of US dollars if a trade agreement with China provides a country a stable trade with one of the world’s largest manufacturer?”

China , trade and “stable” are not words that historically go together. China being so large isn’t an asset here – they are big enough to rewrite terms mid-deal without facing much in the way of consequences. Just look at all the trade impacted by the COVID shutdowns – with result that many manufacturers are diversifying away not adding more in China.

And the Chinese currency has a colorful history as well, which is part of why it’s not yet a major reserve currency.

#Wisdom Seeker,

China being big enough to rewrite terms mid-deal without facing much in the way of consequences is no different than dealing with the USA.

The business side with China is no better than with the USA, on the other side China care much less about internal affairs in countries they do business with.

China yuan can become one of MANY reserve currencies without the need to open their capital accounts.

China has currency swaps with more than 40 countries now. Trades occur outside the SWIFT system. So how do you know what volumes are to make any comparison. In other words, your graphs are bogus!

If you think China buying oil in yuan does not matter, why all of a sudden all the DC hawks have stopped bashing Saudi Arabia? Why the sudden silence?

Last, good luck having the Fed print dollars to ‘stimulate’ the economy out of a recession. The US can no longer export inflation to the rest of the world because, unlike in 2008,China is dumping US treasuries!

“China yuan can become one of MANY reserve currencies without…”

The RMB is ALREADY one of many reserve currencies. It has a share of only 2.8%. This was explained in the article, including in a chart.

The “China will wreck US by dumping Treasuries” is another old nonsensical trope that’s been floated to frighten people since at least 2007. I studied that issue back then – China doesn’t own enough Treasuries to make a difference – there are too many willing owners of those bonds at slightly higher rates, including the Fed and millions of yield-starved Europeans.

“These people have been pumping the same nonsense for over a decade, copy and paste” …

It’s all about perspective: the West is not capable to look forward more than 4 years, while China looks 100 years ahead. That’s why it achieved the greatest reduction of poverty in 30 years.

The formation of a powerful force in the East has began and the West is going down fast. It’s like the British empire all over again …

Not even close A,,, at least SO FAR…

While the ”Suez Crisis” in ’56 was clearly the last straw breaking the back of the British camel,,, there were tons and tons of antecedent similar events going back, at least, to the ’47 revolts of the PEONs in India led by Gandhi and others.

The clearly massive exploitations of the PEONs of India and others by the British going back many decades,,, centuries even, are now very well documented.

SO FAR, USA has not done anywhere near such a job on various and sundry ”protectorates” in spite of the propaganda… SO FAR.

And, SO FAR, China seems to be going down the same slippery slope of ALL such hegemonies, since FOR EVER,,, or at least since the Egyptians that we know at least something about….

God Bless us all!!!

To achieve poverty reduction on the scale China did in the last 30 years, it helps to start with the worlds largest and an incredibly poor population. It’s hard to believe a country which looks 100 years ahead found itself in that position. These facts don’t detract from the immense material progress China has made in the last 30 years, but they are worth keeping in mind when talking about time scales of 100 years. China is now a high middle-income country and we’ll need to see if its system can transition to a high income country over the next few decades. Thirty years ago Japan was going to take over the world, and while Japan is certainly a high-income country, that didn’t happen for a variety of reasons.

The future is uncertain. Though in a relative sense the economic dominance of the West was bound to decline as much of the rest of the world continues to develop.

Asul – hubris (i.e.: ‘folly’) is historically baked in to every nation that arises to a position of power. It can be the source of national vitality in the near-term, and, lacking sufficient and critical self-reflection, the source of national decline in the long one…

may we all find a better day.

Ha ha ha! Did the “one child policy ” work out for those geniuses? How about the “great leap forward” that starved tens of millions? The “cultural revolution” that destroyed decades of educational progress? “Belt and road” which is failing both financially and politically across Asia? They had to back pedal from their own stupid COVID policies but did so only after it became clear that the pitchforks were coming out. China’s leadership are clowns who care only for their own power.

Huh ? China has a national debt of $51 trillion, and 285% of gdp. That is no miracle, nor bringing anyone out of permanent poverty. It’s very temporary. China knows. And all of their new found debt is tied up mostly in real estate or construction of highways and buildings going unused. The worst part for China, is that their citizens have majority of their wealth tied up in real estate too. China is in serious financial trouble, and that will bleed out into the world economy. Also their demographics are horrid, with a massive chunk of elderly and not nearly enough young adults or middle age to carry the country. Hence they MUST keep exporting until basically everyone keels over from exhaustion. COVID restrictions and lockdowns, and now the real Covid hitting hard, is really going to knock the legs out from China in 2023.

Mike R,

“Huh ? China has a national debt of $51 trillion, and 285% of gdp.”

This is nonsense. Current China debt is $9.3T, which is no where near the made up number you listed.

C# Dev,

I think he referred to the total debt of China, at all levels of government, including the heavily indebted provincial and city governments, and the heavily indebted state-owned enterprises, plus some other forms of debt, maybe private sector companies, and consumers (mortgage debt mostly).

I really enjoy your site, but I find the disparaging remarks about other country’s economies a bit ‘arrogant’

Russia has above 5 times the US proven reserves of oil and gas and in many years exports almost the same volume of both.Its the 11th largest economy in the world, which may compare poorly on some basis with the largest US states, but not on others.

Saudi Arabia is and has been exporting oil mainly to China, India , S Korea for some years, its not suddenly facing ‘discounting’ because of non sales to US. Its the 20th largest economy in the world.

If the US was not bothered about SCO, BRICS+ etc , it must be very paranoid about nothing, given its recent geo-political behaviour.

Yup.

As you correctly pointed out, GDP is a very poor measure of geopolitical relevance.

These countries (Russia and Saudia Arabia) provide resources that are vital to the global economy. Who cares if the US doesn’t need to import it? If it wasn’t available, it would be felt in the global economy immediately, including in the US where inflation would skyrocket.

It’s certainly a lot more important than practically any other goods and especially services.

Wolf is a superb economic analyst, but the comparisons of Russia’s economy with those of individual American states are absurd. GDP doesn’t come close to telling the fully story of economies, and Russia’s SOTA military hardware and tremendous reserves of oil and gas set it far apart from the likes of Texas and Florida.

Furthermore, Russia is the largest wheat exporter in the world, etc.

As you suggest, JW, if, on close inspection, it were actually easy to “forget” Russia because of the size of its economy (based on GDP), U.S. foreign policy would look very, very different today.

Energy is the biggest factor in any economy. It determines industrial output, and the cost of it, determines the the economic competitiveness of the end products.

The fact that the majority of the worlds future energy reserves lie in countries that are not always on friendly terms with the US does bode well.

The fact that some of these countries are actively seeking alternatives to the dollar for the trading of this energy is equally problematic.

Everything obeys the laws of supply and demand, and if the need for dollars to trade petrol-chemicals declines, then it stands to reason the supply of dollars increases, effecting its value.

If the de-industrialization of Europe progresses into the future, the US dollar could theoretically replace some of the demand for dollars for worldwide trade due to weakened confidence in the Euro, and Europe’s declining output. This may however cause political problems itself.

I hope someone will make a comment about Purchase Price Parity. In that regard the US economy does not look very good.

According to the latest available purchasing power parity (PPP) data, China’s gross domestic product (GDP) in PPP terms overtook the USA’s in 2013, and now accounts for nearly 19% of the global economy. Five years earlier, in 2008, India’s GDP in PPP terms surpassed that of Japan to become the third largest economy in the world.

1. It’s called “Purchasing power parity” not “purchase price parity.”

2. What PPP is: From the OECD:

“Purchasing power parities (PPPs) are the rates of currency conversion that try to equalise the purchasing power of different currencies, by eliminating the differences in price levels between countries. The basket of goods and services priced is a sample of all those that are part of final expenditures: final consumption of households and government, fixed capital formation, and net exports. This indicator is measured in terms of national currency per US dollar.”

3. It’s an interesting economic theory, but very flawed. And it has been debunked and its flaws have been pointed out. From the St. Louis Fed (PDF):

Authors Michael R. Pakko and Patricia S. Pollard cited the following factors to explain why the purchasing power parity theory is not a good reflection of reality.

Transport Costs Goods that are unavailable locally must be imported, resulting in transport costs. These costs include not only fuel but import duties as well. Imported goods will consequently sell at a relatively higher price than do identical locally sourced goods.7

Tax Differences: Government sales taxes such as the value-added tax (VAT) can spike prices in one country, relative to another.7

Government Intervention: Tariffs can dramatically augment the price of imported goods, where the same products in other countries will be comparatively cheaper.7

Non-Traded Services: The Big Mac’s price factors input costs that are not traded. These factors include such items as insurance, utility costs, and labor costs. Therefore, those expenses are unlikely to be at parity internationally.

Market Competition: Goods might be deliberately priced higher in a country. In some cases, higher prices are because a company may have a competitive advantage over other sellers. The company may have a monopoly or be part of a cartel of companies that manipulate prices, keeping them artificially high.

All of that oil is locked away under the frozen tundra. They choose to spend their money invading down south rather than investing in their own infrastructure.

Have you ever talked with anyone from Russia? Outside of Moscow and St Petersburg it is desperately poor and backward. It is resource rich but lacks rule of law and entrepreneurial spirit. The population is aging and shrinking and literally hundreds of thousands of the best and brightest young people emigrated en masse since last March. Russia is a failing country and to speak about it in any other way is dishonest.

It’s also a proud and beautiful country with a rich cultural heritage and dangerous because of nuclear weapons. But it is economically shrinking and in a demographic spiral.

Wolf you said the answer so well but the crisis that does not exist is tried to be created especially surrounding Russia. I’ve worked in Moscow and Naryanmar and seen their economy in action. Traffic in Moscow at rush hour is a gridlock with commute times lasting 4 hours one way. Their metro is packed and is very efficient but cattle cars during rush hours. There is limited road rail and airport infrastructure. Just a few at the top that benefit very similar to Saudi where the average young male can’t get a decent job and we won’t discuss the lack of employment for females leaving half the workforce unemployed with some exceptions of course. You nailed the issue with China a growing economy with a growing middle class and full employment capability but a lack of capital transparency and seems to me rules that keep changing.

Moscow sounds a lot like Los Angeles…without the Lakers, of course!

I do hope that the dollar remains strong and continues as the world’s reserve currency.

It’s critical to the living standards of most Americans, the vast majority.

A noticeably lower exchange rate (below the 2008 low) means that the vast majority of Americans will be poorer or a lot poorer.

I agree that we should forget about Russia, but we are not

I wanted to make a minor correction in here. Different organizations have various estimates, but overall, Russian economy is around $2 trillion. This is larger than Florida’s (around $1.3 trillion) and similar size as Texas’. That’s still very small when compared to China and U.S. definitely.

Pinpoint LOL riposte to the Great Zoltan and Prince Pepe.

What’s for dinner?

The ruble fell 10 % in a week last month. The Russian economy is forecast to contract 5 % in 2023. With an economy ranked # 1, in a class of its own for inequality, this means pensioners will have a hard time maintaining even their present subsidence.

To think where Russia could be today…if only.

Russia is a very wealthy country. To deny that is absurd. The value of Russia’s natural resources at 75 trillion dwarfs the US at 45 trillion.

When you consider that 90% or US natural resources are in coal and timber, that comparison becomes even more one sided. The value of coal going forward is questionable unless new technology can be developed to make it clean burning.

Russia is rich in Oil, Gas, Gold, Diamonds, Metals, including rare metals. They also produce a large amount of the worlds food supply.

The future clearly lies in the countries that produce the resources the rest of the world needs, and in many cases is running out of. That is why our military are always involved in countries that have, or control valuable resources.

“Russia is a very wealthy country.” Only problem is the wealth is only in the hands of less than a 1000 of its population. Hence why it’s an oligarchy. These oligs’s squirrel the money out of Russia into various European tax havens. This does nothing for the ordinary Russian.

It is really not much different anywhere else. The big difference is the availability of credit which allows people who do not have money to buy what they want based on future earnings.

Most peoples wealth in so called developed countries is based on the overvaluation of assets which in an economic downturn can be devalued and wipe out the majority of wealth.

The oligarchs are extremely short sighted and have been plundering the wealth of Russia and not even bothering to invest in new production.

Jdog,

I must admit that this is an inane BS-larded comparison, on all kinds of levels. It’s just ridiculous.

Bogus statement. What valuable resources did Vietnam have or control? How about Kosovo? No boots on the ground but we are involved in Ukraine. What valuable resources do they have or control? Just another America hating, liberal progressive trope that gets thrown out there time after time. Get a clue.

Vietnam had huge rubber plantations and rubber was a huge military commodity prior to oil based sythetics. In WW2 rubber was in very short supply. In the 60’s rubber was still a valuable commodity.

US Dollar/ DXY is reaching a crucial technical level – both the 2016 and 2020 previous high levels– and would be a “potential” logical technical spot for it to eventually bounce (support), especially with the RSI/momentum indicator not getting into oversold /below 30. Wouldn’t surprise me , with somewhat of a “muted” Santa Clause Rally thus far, and looking at the Stock Trader Almanac January seasonality patterns (going back to 1901 with the Dow – and especially the periods from 1988 – 2021) if we don’t get a bounce here in the upcoming near term, which obviously would be another headwind for equities/growth. Purely from a technical /price perspective…Time will tell.

The Canadian peso is still low to the USD even with these relatively high oil prices. I wonder if it’s done on purpose to make real estate cheaper for speculators?

I liked it when the Canadian dollar was at par mainly during the early part of the last decade. After Harper lost the election, the Canadian dollar went to garbage rates.

The Canadian dollar was falling well before Harper lost re-election. The CAD was on parity because the USD was weak.

And yet hockey equipment still costs so damned much.

It is amazing to look at that last chart and see how the USD has moved down and up over time. When inflation was at its worst in the late 70s and early 80s, the USD share of Global Reserve Currencies went UP… but once inflation was brought under control in 1982-1983… the USD share went DOWN. That lasted until the First Gulf War and the implosion of global communism in 1991.

Then the USD went up again as a share of the Global Reserve Currencies for a decade until the Euro arrived. Since then the dollar’s hegemony has slowly eroded as Wolf says because of…

“The US government deficits that have produced the incredibly spiking public debt; and the ballooning trade deficit, powered by Corporate America’s three-decade search of cheap labor.”

Using the term ‘Budget’ brings the biggest laugh in DC where it’s still pedal to the metal. Huge debts like paying off student loans are tossed back and forth as the Right or Wrong thing to do, no worry if it can be afforded or not. It’s all about getting reelected and apparently, we love keeping their asses in office.

We all have to admit, owning the reserve currency in the U.S. has greatly enriched all of our lives in one way or another. We still have 59.8% to go. Love that Social Security raise. More stimulus coming if needed.

1) In the 70’s US was targeted, ARAMCO was confiscated, US lost it’s oil assets, but we didn’t care, because we developed new oilfields, creating a glut.

2) In 2022 US co lost it’s Russian assets, but here is no glut. The Dow misbehaved. The Dow Anti fun was May 12/17.

3) In Oct the Dow jumped above hoop and pooped on the Anti in Dec.

4) For econ101 GDP growth equal power. Tiny economies like :

Iran, Russia, Saudi Arabia and N.Korea don’t matter. When u cluster

them together, under China’s SCO, they do matter.

5) China new openness might be positive for the global economy, especially empowering oil producers and SCO members, causing inflation, paying them in devalued currency.

6) But China new openness might spread death all over the globe, including China itself. Protests against China spread in Gwadar. Oil co workers striked in Iran.

7) Europe might have learnt their lesson from it’s dependence on Russia,

applying it to China.

8) The world hate China more than US.

Thanks wolf,

Another reason to keep hiking rates!

1) DXY 10Y accumulation between 2004 and the Jump in 2014.

2) Six years in Re-accumulation between 2015 and the jump in 2021.

3) DXY is backing up, testing Jan 2017 and Mar 2020 highs.

4) Can DXY breach 2000/2001 highs and reach 140 : yes.

Have you got money riding on that bet it’s going to reach 140? I will take the other side of that bet. The DXY may challenge 120 again but 140 isn’t happening.

I’m with you on this one. I wish it were otherwise but don’t think so.

On pure momentum alone, the USD has been losing about 0.5% a year of global currency reserves for the past 50 years. If current trends continue, the USD will dip back under the 50% level before 2050.

The world, for sure, is quietly cracking apart into 2 rival monetary systems. You are either going to be with the WEST or with the EAST. You will either use Swift, petrodollar, Visa, etc. Or you will use e-CNY, petroyuan, Alipay, etc.

The big test for the dollar (and Euro) will be the national and then international rollout of e-CNY in 2024-2030. The digital yuan, if designed properly, could make international trade payments faster, easier, cheaper.

Of course, China has its own problems, too. Its population has peaked, and may halve in size by 2100, dramatically reducing its trade influence. China is not guaranteed to “win” the currency wars.

To summarize, the US dollar is approaching a crossroads in the 2020s. And China will make it or break it.

“On pure momentum alone, the USD has been losing about 0.5% a year of global currency reserves for the past 50 years. If current trends continue, the USD will dip back under the 50% level before 2050.”

Presumably, you are basing this on the decline of the USD from 85% in the early 1970s to 59.8% today. It doesn’t make sense to look at it this way and then extrapolate in a linear fashion into the future. Look at the final chart in the article. The USD portion of reserves has fluctuated widely in the last 50 years. Going from 85% in the early 1970s to just over 45% in the early 1990s, before rebounding back above 70% around 2000, before falling again to today’s level. There is no long-term trend in the chart. USD reserve status fluctuates, often quite rapidly, with changing economic conditions and the availability of other potential reserve currencies.

The US may fall below the 50% level well before 2050 if a viable alternative as a reserve currency establishes itself. It really depends on how each major economic power manages its economy and currency, but change in either direction can happen fast as the final graph attests.

Even though the percentage of the reserve currency is dropping, the amount in circulation has gone up. Populations keep growing. The amount of USD in circulation in 2014 was 1.2 trillion and not it is 2.4 trillion. 80% increase. Everybody is printing.

If the U.S. percentage is dropping, that means other Central Banks must be printing at a faster rate than the U.S. LOL

Anyway…here is the amount of USD in circulation vs average house price. I am guessing the average price will be $800k in 18 years. It seems to double every 20 years.

1980: 123 Billion Median House price: 63k | Avg = 72k

1990: 273 Billion

2000: 590 Billion Median House Price: 165k | Avg = 201k

2010: 927 Billion

2020: 1.8 Trillion Median House Price 320k | Avg = 391k

2022: 2.29 Trillion Median House Price 420k | Avg = 520k

2030 estimate: USD in circulation over 3 trillion? Median House price after a dip down to $350k and then a run to 500k and Avg = 600k.

The 1st number is USD in circulation.

Thus

1980: 123 Billion

1990: 273 Billion

2000: 590 Billion

2010: 927 Billion

2020: 1.8 Trillion

2022: 2.29 Trillion

First number is the year.

ru82,

A majority of the “currency in circulation” (paper dollars, aka Federal Reserve Notes) that you cite is held overseas, including in Russia, as a way to protect their wealth from the collapse of the local currency. Much of this currency in circulation (paper dollars) is NOT cash that circulates in the US. It’s cash that is overseas.

Currency in circulation is demand-based. It’s not something the Fed prints and drops from helicopters. If someone walks up to a bank to get paper dollars, the bank must be able to provide them; foreign banks work through their correspondent US banks to get the paper dollars for their local customers.

Banks get the paper dollars from the Fed in exchange for collateral, such as Treasury securities. This is an exchange, Federal Reserve Notes against Treasury securities, or similar. These Federal Reserve Notes are not QE, and don’t have the effect of QE. Sounds like you’ve been reading some blogger out there that doesn’t understand even the basics.

Read all about it here, including a chart on the paper dollars in circulation:

https://wolfstreet.com/2022/11/27/the-feds-liabilities-under-qt-november-update/

1) DXY Anti : July 1973 low/ Jan 1974 high, 90.54/ 109.50.

2) DXY resigned, but in Feb 1985 it popped up to 165, after the 1984 Plaza Accord. James Baker became furious when Japan had a flirt with China, destroying the love affair between US & China.

3) During the Tokyo RE and Nikk bubbles DXY slumped.

4) DXY was in accumulation between 1988 and the dot-com jump in 1999. US real estate reached nadir, in real terms, in 1995.

5) Apr 2008 nadir was a spring.

6) Nov 1982 high/ Jan 1983 low ==> 126/115 was a backbone. It built the Plaza Accord bubble.

7) In 2000/2001 DXY reached it’s middle and failed.

8) After accumulation and re-accumulation DXY might get there next time.

Great summary for the DVY and reserve currency picture. Facts vs click bait non articles without any substance causes many to push a narrative that fits something they are selling.

The USD as the world reserve currency is a boon an bane. It can be used for shopping the world and politicians misuse it and create inflation and waste. It may have smaller but similar negative effects you see clearly in oil producing countries. They don’t have to produce, they just sell crude.

As an investor, I think the USD could weaken substancially if / when Powell cuts rates in an emergency. Falling stock prices could be pretty negative for the USD.

This chart of long term USD share of global reserve currencies is interesting. In the inflationary times in the ’70s the USD share dropped a lot. I would be curious to understand that better.

The long term view of the dollar should be separated from the short term fluctuations. But this is very difficult with the huge crazy Ron Paul brigades that keep whining about the precious as the only real currency. The trade deficit funds the world reserve currency, and as long as the rest of the world’s major currencies look more unstable- well, the dollar stands alone.

Meanwhile, as Wolf points out- the massive use of the dollar in trade continually reinforces the dollar as the world trade unit. Russia hates this, but the inability to offer a better use item means that it is doomed. Russia has a huge proportion of the world’s raw materials coopted by a failed state. This will change, but the country that is best positioned to grab some of these resources is China. So, what we do is sort of irrelevant to those two countries. China has had massive wealth leakage over the last two decades, and fighting this distortion has removed any real chance the currency could be used in trade on a world basis.

I do find it curious that no other serious rival to the dollar has emerged since the Euro, and Germany’s mismanagement of the southern peripheral crisis blew that chance.

By the way, the Randian nutters totally miss the manipulation of the metals markets by Russia, they keep looking for Bilderbergs and Rothschilds instead of the obvious that Putin has been liquidating metals by the trainload to China to buy war materials. The volatility of the grey dog has been epic.

In short, the dollar stands because of the recognition of a short term value and ability to move it worldwide. You want to buy a house anywhere in the world with your fancy capital of USD- great, we welcome your funny money with open arms in Bogata, J-Burg, Madras, Peshawar, Tokyo, etc.

The strongest currency in the world is the Kuwati dinar. Another Arab oil vanity project. Meh.

A true worldwide currency would require some sort of super way of transferring wealth like the stupid bitcoin, but in much more efficient way. Now, if banks would back a dollar based parking place based on a megacalorie of food, that could be a start. But still, how to use it like a digital dollar. Even Alipay take VMC and paypal.

So nothing yet. But the Fed contracting the amount of global currency is going to be a huge minute in a huge world economy.

Someday this war’s gonna end…

For those who aren’t finance professionals like myself I can’t recommend

Ray Dalio’s ’Principles for Dealing With the Changing World Order’ (2021)

enough. There’s also a youtube video that summarizes among other things how reserve currency happens. The author seems very pro-China but that may be in part to light a fire under policy makers.

Anyway, the book is, by design, very readable, IMO.

The author is semi-Woke but not like Friar Blockrock. The Wokes think China is just special.

@No Bad Cake,

I think Ray Dalio is pushing a narrative that fits something he is trying to sell.

Harvey,

Maybe, IMO, the word “China” should be mentally redacted by the reader after the first 15 uses of the word!

However, Ibn Khaldun writes similarly in ‘The Muqaddimah: An Introduction to History’ (1377) and he’s not the only one. The past cycles of civilization Dalio describes seem to be valid.

Very interesting but if the US continues with MMT and there is no indications this will end what happens to the dollar in 5, 10, 15 years? Can a nation continue to debase its currency and still have people who believe in the value of said currency?

The US isn’t doing MMT, but QT and rate hikes, in case you haven’t noticed.

The question you have to ask is this: which major currency is being debased less than the USD? They’re all being debased, to varying degrees.

Everything you say is true but:

1) CBO is projecting a cumulative federal deficit in years 22 to 32 to be nearly $16T

2) The combination of entitlements and interest is projected to be nearly 25% of GDP by 32

Can the bond markets accommodate these levels without depending on more QE?

Now start subtracting a whole bunch from this burden because of inflation. Inflation boots government revenues, business revenues, and consumer revenues (wage inflation) — we’re already seeing this. Government debt as % of GDP has dropped a whole bunch from the peak in 2020. For example, 10% inflation in one year cuts the burden of the TOTAL government debt at the beginning of that year by roughly 10%.

Monetary Policy says tighten, Fiscal Policy says spend like there’s no tomorrow.

Please reconcile that, Wolf.

There is nothing to reconcile. Congress is in FULL inflation-denial mode. Congress is fueling inflation, and the Fed is trying to crack down on inflation. These big deficits during high inflation are just nuts.

This means: higher inflation for longer, higher rates for longer, more QT for longer.

Once the 10-year yield is at 7% or 8% and short-term yields at 6%, and borrowing is getting more expensive, then Congress might be a little more reluctant to borrow and spend. But I’m not holding my breath. There are no fiscal conservatives in Congress. They’ve all been run off. What we have left is a bunch of people from both parties who want to be fiscal conservatives with what the other party wants and spending-monsters with their own priorities. So it doesn’t matter overall who is in power: we’re going to have a big-fat deficit.

The only discipline left would be market forces, if the Fed allows them to run loose (the bond vigilantes).

And how does the big, fat Deficit get financed?

Sounds a lot like that song, “There’s a hole in the bucket….”

Thank you.

It gets financed by selling more Treasury securities that investors will eagerly buy if the interest is high enough — including me.

Right now, Congress is the chief villain not the Fed for causing inflation. Spending is completely out of control. DoD got a 10% increase in spending and the new budget bill got Republicans to sign off on it. There are no conservatives left here in the Swamp.

Concerned citizen,

I think there is a theory that once you start down the road of monetizing debt to juice the economy, you can’t stop without a calamity. I thought we might find out this year, but government is stimulating so much in 2023 that it is going to kick the can maybe to the end of the year.

US has racked up a lot of debt obligations since Pandemic with negative real interest rate. Don’t think we can service it long term with a positive real interest rate. We will know sometime in the next few years. We sure live in interesting times.

OS: ”Election Cycles = Voter Bribery Cycles” eh?

Remember clearly that every time the party in power was changed, the flow of funds was changed too…

Not so much anymore, as the fiscal conservatives that used to predominate in BOTH parties have been replaced by freaking reactionaries in BOTH parties and the results speak for themselves == fiscal insanity!!!

Raising rates higher than other countries means our currency will be stronger and is being dabased by a smaller amount, but then the government passes another Trillion dollar bill (1.7 Trillion) so who knows. We are on our way to 40 Trillion in government debt by 2040. I am guessing the government will be spending over 1 trillion in interest payments a year by 2040 too. Either they need to cut spending (won’t happen, raise taxes, or deflate the debt away). We know the debt will just always be kicked down the road. There will be a day of reckoning but that is still far off. Just watch Japan, their day of reckoning will be 1st among the G7.

“deflate the debt away”

Good article by St. Louis Fed 8/2022, “Inflation and the Real Value of Debt: A Double-edged Sword”

“I am guessing the government will be spending over 1 trillion in interest payments a year by 2040 too.”

I’d guess that it will happen a lot sooner than 2040.

Probably by 2026 the way the government spends money increasing the deficit and the FED having to increase interest rates to combat inflation.

Government has only one playback, proved time and again through different ages: inflate the debt away (soft default). Don’t like it? Buy yuan! Lol jk/

The M2 money supply is nearly flatlined from Nov 2021 – Nov 2022.

Farm fertilizer prices in $USD are down from their 2022 peak.

Oil and NG prices in $USD are down from their 2022 peak.

New auto inventory has been rising.

……..as Wolf explained, U.S. currency is dominant as U.S. Corporations have found using other Countries assets, (labor, and natural resources) to their benefit hasn’t been as deplorable as many suggest. Trade imbalance is tolerable when these proven reserves are exchanged for services that have little effect on natural reserves.

The US Dollar is equivalent to Mount Everest, neither is going anywhere within our lifetimes.

That’s not a bad concept, because mountains are worn down, facing volatile challenges from nature and the dynamics of physics. The capitalist system works, primarily because communist slaves aren’t innovative or motivated enough to think outside their doomed existence.

That’s the commies plight, but for a few years, we’ve had a small slice of noise from the crypto community, arguing about the decline of Dollar dominance — an issue being currently explored in their Crypto Winter.

If the globe is in the midst of resetting onto a new economic path, the future will be connected to Uncle Sam’s printer.

The Crypto Winter has just begun and the commies future looks like the commy past.

Here’s a crypto tip:

Voyager’s and Celsius’ chapter 11 bankruptcy filings highlight the question of whether crypto assets held by an exchange, or similar platform, may be considered property of a bankruptcy estate and, therefore, not recoverable by the customer, who would then likely be an unsecured claimholder of the debtor.

I find it hilarious to see the terms “crypto” and “assets” in the same sentence!

Crypto is like an old watch, with a huge amount of connected parts, primarily gears. The watch system has been functioning smoothly as a nice ponzi game, but various gears are breaking down and the whole system is going to break and grind to a halt.

The fantasy assets in that watch will be less valuable than rusty metal gears. It’ll be challenging to salvage value from something that never existed.

Also, everyone was happy as the prices were going up but nobody asked what is behind the curtain making the prices go up.

Eventually, the curtains falls down for some reason or another and you see the most of it was hocus pocus.

But it is getting harder and harder to reconcile the “doomed commie slaves don’t make competitive workers” trope with the actual intl performance of the Chinese economy for 25 years.

Maybe they ain’t so Commie and less slaves. The CCP may be an ever present worry for Chinese businesses and workers…but both seemed to have decided that safety lay in production and savings (even if – mainly – in coerced Yuan).

The Chinese economy has been the fastest growing (at scale) in human history.

Japan, South Korea, Taiwan all did the same growing from subsistence poverty to top tier wealth in 20-30 years. China is larger and started from a “North Korea” poverty level. They pivoted from Mao to a relatively capitalist system initially in a few cities and then nationwide from about 1990.

But they are now stupidly pivoting away from what brought them up near the rest of Asia and imprisoning their business leaders and nationalizing more of their critical industry. Growth is falling from 10% to the 4% range (per their metrics, actual growth is lower). And per capita income in China is only about 11K, it’s less than half of Japan, South Korea and Taiwan, and there are still hundreds of millions of rural Chinese living on less than 1,000$ a year.

China is the first country that will grow old before becoming rich. If Xi is the path the continue to follow, there will be economic trouble in 5 years.

” A catastrophic US military defeat”

Can any nuclear power be defeated in an external war? I’m unsure how this tech changes the cycles of civilization(Khaldun, Dalio) present since Mesopotamia.

In my lifetime, I have witnessed the dollar lose 95% of its buying power.

I have witnessed the economy go from one in which a blue collar husband could easily afford to support a family, purchase a home, and a new car every 2 or 3 years, and put his kids through college without any debt, to the debt ridden economy of today where financial independence is a unattainable dream for the vast majority.

The dollar is hardly Mt Everest, it is more like Mt St Hellen’s. It may still be there, but it sure is not what it used to be….

You’ve also witnessed companies gut unions and cancel pensions.

Union’s paid for in “innovative and creative” Capitalist Slave’s blood.

And again paid for in even much MORE worker blood during WW2, which left our capitalists with effectively NO world competition. Nice spot to be in, no? But they then fucked the workers….again.

Destroyed by capitalist’s mega-money, buying much more “democratic law” than a worker (slave) ever could even dream of. And it continues.

And of course, shipping all our factories overseas to get cheap labor. After all, they only care about themselves and (some of) their shareholders. Uncle Milty “proved” that they should, and got a faux Nobel prize for it.

All the capitalist slave workers wanted was a seat at our fascist corporation’s decision making tables…(where those “creative innovators” are)…..and still do.

Dr D, don’t you think that your stupid old trope has caused enough human suffering?

Hahaha, the ruble lost 90% of its value against your collapsing USD in the last 24 years!!! You people crack me up.

All currencies lose purchasing power over time. But the dollar is among the cleanest dirty shirts; and the ruble is among the filthiest dirty shirts. There are still filthier shirts than the ruble, such as the Argentine peso.

So what if the ruble lost value against the US dollar.

Peoples in the US don’t use rubles and it has nothing to do with those peoples.

The value of the US dollar in terms of purchasing power inside the US has fallen especially for common items where there is not what you call hedonistic adjustments such as in cars or computers.

Houses, food, energy, wages and such things all cost more in dollar terms. So does education.

Is the quality of a US university education the same as it was 30 years ago despite the huge increase in cost? I doubt it.

Perhaps privatizing education (especially K-12) is not such a good idea (except for the wealthy owners, and very wealthy clients) ? IE, DeVos, etal, and Trump U, etc, etc, etc, etc? I know privatized health care isn’t working out well at all.

Answering to profit is not the same as answering to what’s left of a democratic government.

“The capitalist system works, primarily because communist slaves aren’t innovative or motivated enough to think outside their doomed existence.”

This kind of thinking is reckless and no experienced leader would suggest such complacency or conclusory thinking–I suggest to all, never take for granted that the disgruntled masses will simply “remain passive”. Jolly Old England in 1776, Russia and France and the USA over the past 200+ years sure learned this fallacy the hard way.

I’m sorry that was a horrific statement. I meant to say:

Capitalism works, because at it’s core, innovators have an opportunity to be financially rewarded, resulting in a society that has an inclination to excel — versus — a slave-based civilization that relies on punishment and terror to demand mediocre output, from poorly trained workers. A communist society is always looking backwards versus capitalist culture that moves forward.

Sorry about the awkwardness of my last post.

There are more than two ways to structure an economy.

Capitalism or communism is a false choice. Reality is much more complex.

I do understand your point and the 2 system premise. That said, I can’t help but think about how well the “American Capitalist” system was working for the cotton plantation owner, whether he owns a “gin” or not; and how shitty it was for the slaves that work on his plantation. I think they had the same dreams and hopes, as every other sentient human being. In modern times, I think of a Tyson meat processing plant and workers being “forced” to work through COVID and sickness. I think America needs to really focus on treating Its labor force with respect, dignity and at least living wages–even if that means a bit less executive pay and shareholder dividends. If you want a Big Mac, you cant outsource that to the next cheap labor market. Might as well treat the worker making it for you with dignity and pay the extra that may cost.

I agree, Nathan. There was a time when the US concerned itself with the well-being of its citizenry to a degree unmatched anywhere else in the world, making its system an attractive example for many to emulate — “the shining city on a hill.”

Somewhere along the line other priorities appear to have emerged, to the detriment of working people in the US. I remain hopeful for a reset of priorities — a revival of sorts, if you will. But I’m not getting any younger …

Dr D,

“Common sense is a collection of prejudices, usually accumulate by about age 18” -Albert Einstein

I don’t know which post is more “awkward”……Why don’t you say “Better dead than Red” and let it go at that?

There’s a psychological as well as political component of being a reserve currency. Democracies have the edge over totalitarian regimes, because who wants to have to move to China vs US if it all fell apart, to be able to spend their cash. Even with foreign exchange possible, communists and dictators can literally take you money if they really want/need to. Yes they know it will hurt future business, but for survival even democracies will do it. Short of a catastrophic event, western democracies will prevail. But like all good things, even democracies make poor political/economic choices at some point and destroy their currencies.

“communists and dictators can literally take you money if they really want/need to.”

See: Executive Order 6102

Glenn McClendon addresses that in his next sentence: “Yes they know it will hurt future business, but for survival even democracies will do it.”

And the IRS had better do so and SOON.

See Wolf’s USA net wealth inequality charts and National Debt charts.

Recent headline from reputable source:

“Major Problem, U.S. Treasury Market Is Becoming Illiquid”

Oct. 18, 2022

Cue: Heavenly Choir singing in falcetto voices

‘Round and ’round and ’round it goes

When will it crash – nobody knows…

I have a yellowed brittle issue of NYT dated Nov 28, 1978. Biggest headline on the front page was:

SAN FRANCISCO MAYOR IS SLAIN. CITY SUPERVISOR ALSO KILLED. EX-OFFICIAL GIVES UP TO THE POLICE.

Second front page headline, not so long and not so big, announces the issuance of UST denominated in German Marks and Swiss Francs:

US REPORTED SET TO BORROW MARKS WORTH $1.25B

Brief historical intro.

On October of 1974, President Ford announced his infamous “Whip Inflation Now” campaign. In a speech before Congress, Ford declared inflation, “public enemy number one” and announced a series of measures to combat it.

But President Ford did not whip inflation…and neither did President Carter. Although inflation rates dipped back down toward the 6% range in 1976 and 1977, they skyrocketed shortly thereafter. Dollar-holders and T-bond holders both suffered mightily.

Less than a month after President Carter’s inauguration, the US Treasury issued its first 30-year bond – the 7 5/8s maturing in 2007. Over the next four years this bond lost nearly half its value, as inflation and bond yields both soared toward 15%.

President Carter responded to this dire situation by issuing T-bonds denominated in Deutschemarks and Swiss francs. In 1978, these so-called Carter Bonds came to market, with the hope of attracting investors who would not buy the Treasury’s dollar-denominated bonds. The buyers of these unique bonds fared pretty well; the buyers of traditional Treasury bonds, not so much.

I WANT MY REMNINBI-DENOMINATED, GOLD-BACKED I-SERIES US SAVINGS BIDEN BONDS !

AND I WANT THEM NOW !!!

I bought some laddered corporate bonds in October, at some of the highest interest rates seen in years. It produces some retirement income. 7% compounded annually doubles in about ten years. Since WFH local real estate prices are crazy, same as local population growth. I forget about my two vacant lots, can not short term trade those, same as my bonds. The taxes go to the county, schools, roads, police and fire dept.

Way to go my smart friend !

Even if I was burned a little during the Great Bond Crash of 1994 (to the tune of MINUS 8%) I remained adamant Boglehead and stuck with Vanguard bond funds ever since.

2 years ago I was totally nauseated by the Great Financial Shit Show & Permanent QE Fireworks IN TOTO and transferred my meagre savings into 0.2% interest-bearing BofA savings account. Let it rot away there. I simply ceased to care. This includes I-bonds too. And I was right:

VWESX – Vanguard(!) Long-Term(!!) Investment Grade(!!!!) Fund:

YTD Return as of Jan 2, 2023 MINUS 30.94% (!!!)

I wouldn’t hold my breath waiting for the end of US & USD hegemony. No other country or union of countries even comes close to real competition.

Every empire has its decline. It is prosperity itself that lays the groundwork for decline. It is simple human nature. Prosperity makes people believe they are entitled, it makes them lazy and weak, it makes them corrupt and incompetent. Every action has an equal and opposite reaction. No empire survives its own human weakness.

That’s true, but outside of something cataclysmic, the United States simply has too many advantages over all other nations on Earth. If anything, the coming era of instability will only increase the USD’s dominance, since the United States (and the North American continent) is the most stable region anywhere, by any metric.

Global warming and or loss of biodiversity is something cataclysmic, and given the complete failure of governments around the world (apart from some lip service in the form of accords etc.) to address these problems, means that these cataclysms are becoming closer and closer.

The USA – since it uses more resources and energy – than most other countries, will be affected.

Generally correct, but most of these comments are too narrowly focused on economics and related charts/data….all good but fail to take into account the flock of cataclysmic black swans flapping around the globe, too numerous for my feeble brain to list…whichever way it breaks, I’m expecting to get totally rogered…

@ c_heale

Climate change is not an economic cataclysm, and wealthy countries like the US are far better equipped to adapt. There are many things I do fear economically and politically, but climate change is at the very bottom of that list.

Why hold 1 national currency when you can own all of them in one easy package?

USD will lose it’s hegemony only if we lose a major war.

Hence the all out support for Ukraine (so far Ukraine given more money than Russia’s entire annual military budget).

Spending money we do not have, to be involved in a war we have no national interest in, and that cannot be won. That seems to be a re-occurring pattern.

No national interest? Ukraine has managed to destroy a good portion of Russia’s military.

“No national interest? Ukraine has managed to destroy a good portion of Russia’s military.”

No they haven’t.

What the Ukraine armed forces have done is to deplete a huge stockpile of western arms,

USD will lose its hegonomy due to corruption, nepotism and political malpractice. In the USA.

Maybe helped by a few hurricanes or other weather incidents.

Empires only lose wars after the innards have rotted away.

Highly, highly improbable. China, the EU, and everyone else depend on the United States for the order that lets them trade their goods internationally in peace. But even IF the US left or was kicked out of the world order, it wouldn’t matter.

Simply put, the US has THE ‘magic blend’ of advantages (geographic, political, demographic, resource, etc) that means it will remain the single most powerful country on Earth for a long, long time.

The USA losing its hegenomy do not imply that anyone else take the place.

That the world order as is break down do neither imply that a new take over.

As for geography, have you ever wondered why there are little or no relics of ancient towns in the eastern part of the USA?

In Africa, Asia, Europe, South America there are relics of ancient towns and cultures. Pyramids, temples, irrogation systems and the like.

There are a few in the US mid west, but anyone on the east cost?

I question your ‘magic blend’…I think more critical analysis could poke some holes in that…

Sams:

Maybe because the first peoples of east coast were very frugal, left nothing but footprints and TONS of shells from harvest of plentiful sea/bay/bayou/estuary foods, etc., etc.?

We teens had somewhat secret places in Everglades that were mounds of shells sometimes 3 meters and higher where we went to party. Oysters were so plentiful that we picked up dozens at a time, etc., etc.

Probably not particularly politically correct even in the late ’50s-early ’60s, but who knew, eh

Ukraine is a major war, democracy is at war, we certainly screwed Iraq, clueless in Afghanistan, didn’t have the courage to drop a bomb in Al-Assads’ lap. He produces all the meth that drives Dash and the crazies. We are supposed to fight for the underdog. No? We had early chances to nip this war in the bud but I guess we are to busy to party and getting rich. Listen to smart people for once. Want to know why things are screwed up ? Talk to the the folks looking up. This group has good insight, nice reprieve from twisted news. God dang their BURNING their hijabs !

And for Canada and it’s gold reserves? Isn’t Canada vulnerable due to earlier dumping of Gold reserves?

This isn’t about central bank assets but about “foreign exchange reserves”. Gold is not a “foreign” exchange reserve. It’s the same metal for everyone.

All these comments about Russia having all these proven oil reserves, or mineral wealth are really a bunch of exaggerated nonsense. First of all, Russia simply does not have the capital or financial resources nor financial acumen, to get access to the worlds capital, predominantly US to fund extraction of said oil. Secondly they absolutely do not possess the technology to get at majority of their oil, nor the ability to manufacture the technology. The war with Ukraine proves beyond a shadow of any doubt, that Russias military is super weak, of inferior technology, and basically running out of any reasonably d

Feasible hardware. That same lack of prowess exists in every one of their industries, including oil and gas extraction. They are no financial powerhouse and never will be as a communist ruled country. So basically Wolf is right with his comparisons, and actually being generous. Russia has really crippled and imperiled itself with this war on Ukraine. It will take them decades to recover, if ever. Eventually, the US will go in to Russia, and it will be US oil corporations extracting the oil for the world to use, as we did in Saudi for the saudis who have not gotten any further in their exploration and extraction knowledge than they were in the 1990’s. The Chinese do not possess our e&p prowess either.

Mike R, Russia can extract oil.

Russia have the most advance weapons in the world, though they suffered severe blows in WWI type trenches war.

Russia GDP is small, but they are the largest country in the world, and they own large oil assets.

US News and World Report, world most powerful nation 2022 : US, China,

Russia, Germany, UK….

Advanced weapons? Is this why the Ukraine is literally pounding the crap out of them with 1/10th the resources and manpower? Russian tanks have proven to be unusually vulnerable to drone attacks. The Ukraine war has proven conclusively that the Russian military is a paper tiger and that their war machinery is second rate.

No wonder you people in the USA has problems with that kind of post.

1) Our dollar is strong, because the Fed raised rates to fight inflation.

2) When rates rise the value of gov bonds and notes fall.

3) TY US10Y futures reached an all time high during the stock markets

slump in Mar 2020. After one year in distribution the markdown started.

4) In Aug 2021 TY tried to recover, but failed. The real slum started thereafter. Central banks from all over the world, institutions…dumped

the gov bonds and notes assets, taking real losses. The dumping didn’t stop.

5) RRP rose from zero in Mar 2021 and $1.6T in Sept 2021, sucking liquidity, providing impaired collateral in the o/n markets, as good as it gets.

6) TY slump stopped in Oct 2022, after reaching a 35Y support line from

1987 and Jan 2000 lows. RRP reached $2.55 this week.

7) The Fed and other central banks are badly injure. BOJ stayed on zero

rates. The ECB raised little. Chinese took bloody punches.

Since the U.S. is no longer an economically undeveloped nation, but is increasingly an international debtor, what evaluation should be places on our huge trade and current account deficits? For the very short run these deficits keep prices and interest rates lower than they otherwise would be and they subsidize our standard of living. But the deficits also are inexorably forcing the dollar down in terms of its foreign exchange value—and no consortium of central bankers, treasury secretaries, et al. can stop the process

With a chronically depreciating dollar foreigners will be much less inclined to invest in the U.S. on a creditor ship basis, thus pushing up interest rates. The rising cost and diminishing volume of imports will contribute to an increase in inflation, and the expectation of further inflation will also push up interest rates. This spells stagflation.

Industrial output has been given or sold off to other lands, with China being the major beneficiary of this wrong headedness. Corporate America has fashioned the rope by which it will be hanged until dead. Strong currencies follow strong production. US has been declining in both at the hands of the politicians for 7 decades. USD has nothing to sell now. Yuan does.

This topic and many of the comments are a good reminder of why the subject was called political economy before being (erroneously) renamed economics.

Here’s another reminder: the fundamental unit of life is the calorie.

Totally agree with first point.