Keeping an eye on stuff, including dollar liquidity swaps and Primary Credit.

By Wolf Richter for WOLF STREET.

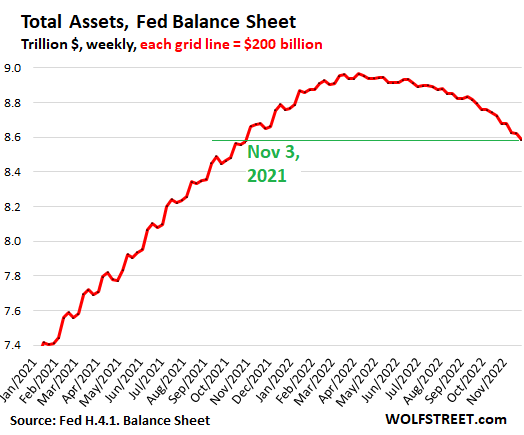

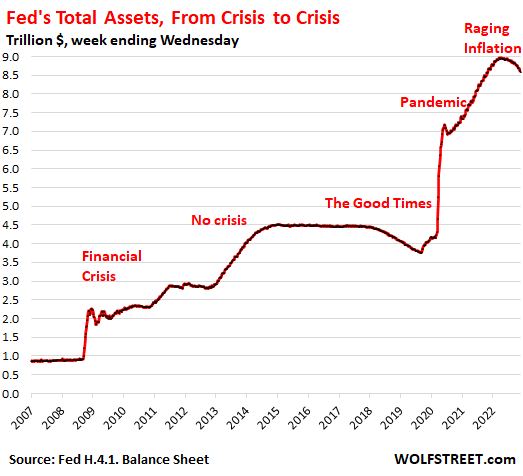

Since the peak in April, total assets on the Federal Reserve’s balance sheet dropped by $381 billion, to $8.585 trillion, the lowest since November 3, 2021, according to the weekly balance sheet released today, with balances as of November 30.

Compared to four weeks ago (balance sheet released on November 3), total assets dropped by $92 billion.

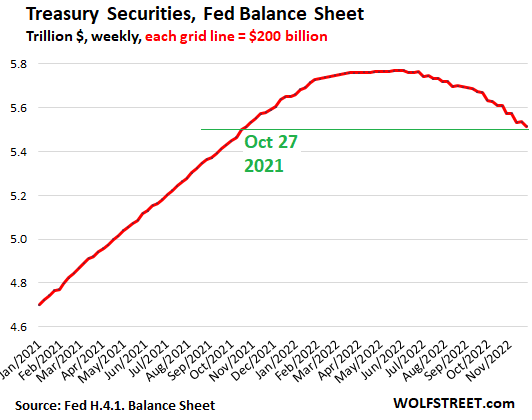

Treasury securities: Down $255 billion from peak.

Treasury securities mature mid-month and at the end of the month and roll off the Fed’s balance sheet at that time.

Since the peak on early June, Treasury holdings fell by $255 billion to $5.516 trillion, the lowest since October 27, 2021.

Over the past four weeks since the November 3 balance sheet, the Fed’s holdings of Treasury securities fell by $59 billion:

- $60 billion of Treasury securities (at the monthly cap of $60 billion)

- Minus $1 billion in inflation compensation the Fed received for its Treasury Inflation Protected Securities (TIPS). Inflation compensation is not paid in cash but is added to the principal of the TIPS, which increases the TIPS balance.

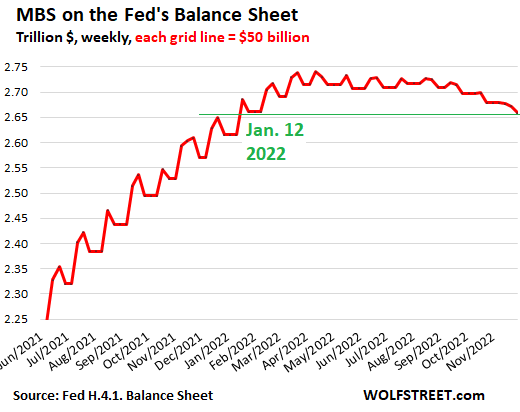

Mortgage-backed securities: Down $81 billion from peak.

Since the peak, the balance of MBS dropped by $81 billion, to $2.659 trillion. Over the past four weeks, the balance dropped by $20 billion, below the cap of $35 billion.

The problem with MBS is that they come off the balance sheet largely via pass-through principal payments, and those have turned from a torrent into a trickle after mortgage rates spiked and mortgage payoffs plunged as sales of existing homes plunged and as refinancings of existing mortgages collapsed.

In mid-September, the Fed stopped buying MBS after having already cut its purchases to near nothing. Given the delays associated with MBS that the Fed bought in the To-Be-Announced market, the inflow of new MBS onto the balance sheet ended in October. These inflows are the upward zigs in the chart.

The downward zags are the weeks when the pass-through principal payments reached the Fed and reduced the principal balance of the MBS holdings.

The resulting zigzag line has gotten ironed out, as the upward zigs have ended and the downward zags have dwindled due to the drop in mortgage payoffs.

Various Fed governors have mentioned the possibility of selling MBS outright to get to somewhere near the cap of $35 billion a month – which means that the Fed might have to sell about $15 billion a month in MBS. I’m eagerly awaiting some official mention in the meeting minutes about it, likely sometime next year.

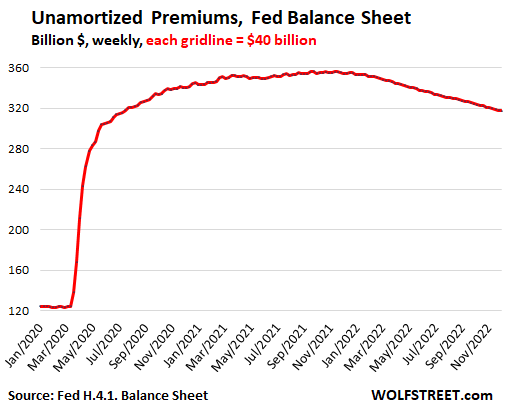

Unamortized Premiums: Down $39 billion from peak.

The Fed bought its securities in the secondary market, and when market yields were lower than the coupon interest of the bonds, the Fed, like everyone else, had to pay a “premium” over face value.

The Fed books the face value in the regular accounts, and it books the “premiums” in an account called “unamortized premiums.” It then amortizes the premium of each bond to zero over the remaining maturity of the bond. By the time the bond matures, and the Fed receives face value for the bond, the premium has been fully amortized.

Unamortized premiums have dropped by $39 billion from the peak in November 2021, to $317 billion:

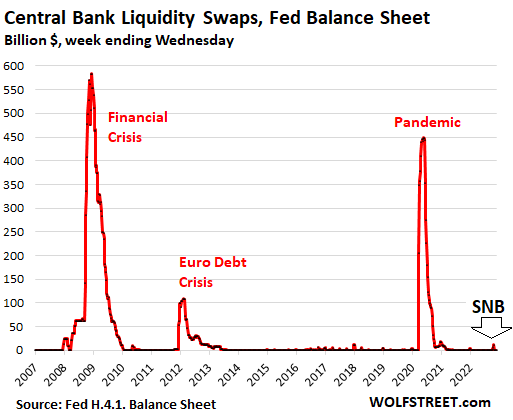

Keeping an eye on the Central Bank Liquidity Swaps

Starting on September 14, the Swiss National Bank used the long-standing swap line with the Fed for five 7-day dollar-swaps in a row. The last and largest swap amounted to $11.1 billion, which matured on October 27. Since then, there have been no swaps with the SNB, and the balance with the SNB has been $0. The SNB likely did this to provide short-term dollar-liquidity to Credit Suisse, which had come under attack by a massive outflow of funds.

We’ll keep an eye on liquidity swaps.

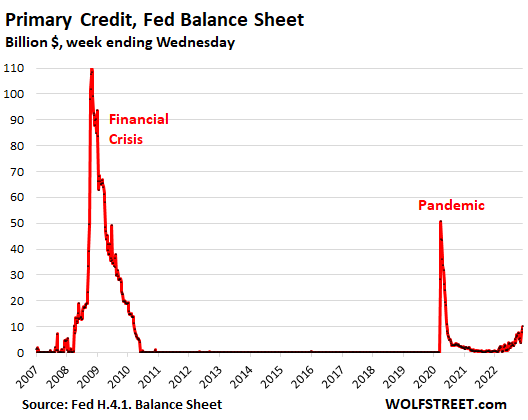

Keeping an eye on “Primary Credit.”

The Fed lends money to the banks and currently charges 4.0% interest on these loans at the “Discount Window.”

When the Fed started hiking rates in early 2022, Primary Credit began rising. On today’s balance sheet, the total Primary Credit outstanding rose to $10 billion. Keeping an eye on it:

QE created money, QT destroys money.

With QT, the Fed destroys the money that it had created with QE. QT works in the opposite direction and does the opposite of QE, but relies on a different mechanism. With QE, the Fed created money and used this money to purchase securities via its primary dealers, which then used this money to buy other stuff with, and the money began to circulate.

For QT, the Fed doesn’t sell securities to the primary dealers. Instead, when Treasury securities mature, the Fed gets paid face value from the government, and the Fed then destroys this money. With MBS, the Fed destroys the money from the pass-through principal payments.

QE caused a huge bout of asset price inflation – and finally contributed to raging consumer price inflation. QT, though it’s slower than QE, will be causing the opposite, and we can already see the effects, with bond and stock prices down substantially from a year ago, crypto imploding, and home prices starting to fall.

And how we got to Raging Inflation:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I look forward to these updates Wolf. Its time for the Fed to get creative in order to make sure the maximum Treasuries asset reduction is achieved. Perhaps a Un Twist to relieve liquidity pressures on off the run assets is in order.

Forget selling MBS, theres no need to sell anything at a loss to the taxpayer.

Who cares about taking a paper loss? They bought then with fake created money anyways, that literally was the point of buying them.

We care, because their paper loss on foolishly invested fake created money is part of what’s causing our inflation.

The more dollars get wasted, the less they are worth.

Blackstone limited withdrawal from its real estate fund. These are the greedy idiots who didn’t bother to transfer their risks from buying crap MBS or crap houses to taxpayers.

Don’t worry, the Fed will bail them out to prevent any force selling or run on fund as that may lead to the real price discovery.

Fed has been busy rewarding behaviors that are destroying the real economy. It was “BUYING” MBS until 2 months back!

Buying it led to asset inflation, selling it does not. So no, you do not care if they sell it at a paper loss.

If you still think you do care, then you just don’t understand this article.

@Leo

“Fed has been busy rewarding behaviors that are destroying the real economy.’

Good description of QE and ZIRP and Fed policy in general for the last 40 years, at least up until tightening started late last year. Savers and the frugal get punished severely, both retired seniors and young couples starting out in the workforce can’t afford new housing or other basics, while speculators and overleveraged spendthrifts make out like bandits. It’s why even with the recent falls, BTC and crypto are still the highest yielding assets over the past decade, all for “investments” on imaginary coins that anyone can start up basically out of thin air. At least with the madly overpriced tulips in the 1600’s you could get a nice looking flower to put on your window sill.

@Cyrus –

I agree that Fed print-and-buy is part of the problem, but would argue passionately that wasting money on either end (buying OR selling) is a loss for the taxpayer and a boon to someone who doesn’t deserve it.

Also, I wasn’t talking about asset inflation. I’m arguing that nonproductive squandering of money requires additional printing somewhere in the system, which generates inflation via currency devaluation. Waste and fraud generate “bezzle” (a fantastic concept) and printing to offset the bezzle losses IS monetary inflation.

Where the inflation pops out is a bit like where the lava flows show up on Mauna Loa – you can’t easily tell in advance. But for both volcanoes and inflation, once the pressure grows inside the system, you know there will be a mess.

It also allows the Wall Street Landlords to pay cash and overbid on houses. They just bundle the mortgages into MBS and push the risk to the people who buy these MBS. But wait, there is no risk to the investors who buy the MBS because the GSE agreed to guarantee these mortgages.

So really, what is stopping them from buying more and more houses?

Paying cash for a house does not generate a mortgage. So nothing gets bundled into a MBS from that sale.

“Uncle Sam may be insolvent.”

hahahaah, I hope you are joking?

Gov was insolvent in 1933 so it confiscated our Constitutional money and replaced it with irredeemable Federal Reserve Notes. Then again in 1964 when it took silver out of our coinage. The again in 1972 when it reneged on the Bretton Woods agreement. And ever since by continuously rolling over its debt and NEVER paying back even a penny. Talk about a zombie organization! True to its nature, it needs wars, overregulation and taxes, financial treachery and a great enabling Fed complete with Fed Agent flying monkeys to survive. But don’t worry, they got our backs. (Or backsides?)

So — the American Century, the most successful national experience in the whole history of humanity, coincided with all this awful stuff? PLEASE. How far from reality is it possible to depart, while pursuing these theories of grievance and blame? How much of a cartoon construct can one follow, or try to purvey to others, with a straight face?

I shudder when i think of how many Americans believe this drivel.

America going off the gold standard caused negative interest rates. Greenspan and Bernanke just made things much worse.

Umm, I wouldn’t say it caused it, but certainly cleared the way for it.

Getting rid of a standard measurement of value, which historically has been a gold price peg, is what first and foremost enables inflation. Then inflation and hijacked interest rate control is what brought us negative interest rates.

“ Uncle Sam may be insolvent.”

Very deeply scary and possibly true….the consequences are terrifying and unescapable.

Thanks for having the guts to point that out.

Ccat,

See my comment below.

BS comments attract BS comments like a magnet. That’s why I should delete BS comments from get-go because if not, we end up with a compendium of BS.

LEO,

“Uncle Sam may be insolvent.”

I should delete this kind of BS. People keep posting it, but it’s just stupid BS.

Because a government that controls its own currency can never become insolvent in its own currency because it can always print more of its own currency. Duh.

But in the process, that government can destroy the currency with inflation. And that is happening.

Likewise, Wolf. My understanding of QE and now QT were limited to generalities. In a short while you have filled in a lot of the blanks regarding this AND other subjects. This is one of the several reasons this site has become my go to site for the analytical breakdown of headlines into what it actually means and why… Thanks again!

I can’t tell if this is satire or serious (MBS)…

“I’m eagerly awaiting some official mention in the meeting minutes about it, likely sometime next year.”

satirious.

If the Fed will never reach $35 billion monthly runoff for MBS, might a better policy be to scrap the $60 billion cap on Treasury securities runoff and just have a $95 billion combined monthly cap?

I’m fine with scrapping the cap. It might cause some turmoil because in some months, the roll-off will be huge.

The Fed has been mentioning selling MBS outright after QT is “well under way,” or something like that. So I’m expecting to see some formal discussions coming our way. Selling MBS is what they should do anyway.

The treasury runoff doesn’t matter as much as the MBS. Without the Fed selling MBS, the 30YFRM is going to drop below 6% a lot sooner than it needs to, allowing housing to start to stabilize.

All running off more treasuries is going to do is get us into the liquidity trap sooner rather than later. We need bank liquidity to say high enough, long enough, so housing can tank enough.

Housing has to tank at least 25% for there to be some semblance of affordability. But even a 25% drop only means about 1 year of price increases in a lot of high demand areas.

This entire morass is about housing, but JPowell won’t admit as much. Nor will Congress who will be chomping at the bits to revive rent & mortgage relief once we approach a 20% drop in housing.

The stock market is entirely a consequence of what MUST happen with housing. We don’t come out of the back end of this with a healthy reset with housing in my area costing $250 per square foot to build AVERAGE houses.

That’s not supportable long-term and skews EVERYTHING.

From a markets standpoint, JPowell should be telling pension funds to brace for impact. Bitcoin needs to go to near zero. It has no intrinsic value and is pure speculation.

JayW-

To an extent, treasuries and MBS are fungible: they’re both federally guaranteed bonds. There are important differences that make them not exactly alike but the point is, even if the Fed themselves don’t sell MBS, private players will sell MBS and buy treasuries when the interest rate difference is high enough to make the arbitrage trade worthwhile.

The Fed wants to get rid of MBS because predicting and managing their balance sheet gets difficult with MBS which have variable payments and variable effective maturity rates.

But regarding interest rates, What matters more is the total amount of QT. The private market will take care of equalizing interest rates between the different actual securities.

“The Fed has been mentioning selling MBS outright after QT is ‘well under way,’ or something like that. So I’m expecting to see some formal discussions coming our way. Selling MBS is what they should do anyway.”

I hope you’re not holding your breath while waiting.

Perhaps the reason the Fed limited the rate hike to .5 percent is to limit its own losses on the assets it sells . Just a guess.

Maybe though the Fed’s still been non-committal at this point, they talked about a likely down-shift to 0.5 for the past couple meetings, only to push it back up to 0.75 when the 50 bp clearly wasn’t doing enough to stop inflation. The data this morning and the ongoing, maybe even worsening services inflation now is changing the picture, and now reports are already that they’re back in drawing board mode. If inflation persists like this for a few more months like this we’re looking at social unrest in the US, can’t have a functioning society when more than half the population is finding basics like housing, healthcare and even food more and more out of reach. In being fair, even Paul Volcker had bit of a learning curve and didn’t jump on the really aggressive rate hikes right away, he tried to start a bit slower before accepting he had to get more aggressive to reign in the inflation then. JPow is now being forced to take the same hard medicine, though at least he also has the tightening power of QT along with the rate hikes so we’ll see how that evolves.

It’s not just the Fed that is draining liquidity and raising rates. Were it only the Fed, it would lead to a lot of head-scratching as to why a hawkish Powell would watch as the dollar and Treasury yields have been falling over the past month.

Except for the China Central Bank (I live in China), are there any central banks that are loosening? Singapore and Korea are tightening. There are no advanced economies that are NOT hiking rates, and most of the developing markets are also.

It’s not easy to ignore the monster rallies in US equities every time Powell says he’s serious about bleeding out the inflation problem. Is it possible that his statements are taken by global investors as gospel truth–even while Americans are probably skeptical–and so are loading up on US blue chips and bonds, while US institutionals are net sellers? Seems reasonable to me. Which global funds managers would be plunking investor cash into a Europe, heading into winter with low energy reserves, or into an Asia, with the worst demographics in world history, if they can buy a Google or a Disney at 40% off from a few months ago?

The whole world is awash in too much liquidity, all sloshing around, like a swimming pool on a cruise ship in a storm. Fascinating to watch. It’s even funny to watch people jumping in with their floaties.

Disney at 40% off? It has a p/e of 56. And its theme parks are ridiculously expensive and headed into a pull-back in spending. And it’s still earning almost nothing on its streaming if not going negative – Dis+. Dunno about Google but its searches are becoming less and less tolerable with ads… You can count the reasonably priced stocks on one finger.

the middle finger

I’m not making a case to buy DIS or GOOG. But if you’re an equities fund manager, you’re usually not allowed to park assets in cash or short-term bonds, even if you wish you could–you gotta do what the prospectus says you gotta do. Ditto for everyone who is managing pension or retirement assets.

Huge chunks of the money that rolls into stock and bond markets are automatic allocations, based on whatever boxes were checked on employees’ 401k investment questionnaires.

Cheers.

Rising unemployment will be the pressure valve for this at some point.

> automatic allocations

That and deer-in-the-headlights self-managed investors just hanging in there, are the most credible reason I can find, for the buoyancy in the markets. Oh yeah, and “patriotically” ginned-up spending, and companies still hiring anxiously. Actual earnings seem more patchy. But this world hasn’t listened to fundamentals and deep value in a LONG time, why start now? Why not just let the funny money ride?

Not to mention the birth rate is heading towards zero. Disney is the next Toys R Us.

That’s a Goofy statement.

It’s because few believe the Fed any more. The institution has a profound credibility issue. They’ve flipped one time too many, so few take them seriously. That whole transitory nonsense was the final straw.

Once a central bank does crazy things, the credibility is lost forever, until they undergo structural change. This Fed kept mindlessly stimulating the economy for decades, simply because inflation wasn’t rising. Given how asset prices, housing, and debts were rising, they should have seen the CPI coming. Inflation presents first in assets, then in spending.

The Fed’s policies have been extremely short-sighted and unthoughtful for decades. Somewhere along the line, they lost all sense of long-term sustainability and risk.

I will never trust Fed decision-making and intent until Congress changes the monetary governance structure to something stable. Until then, you have to invest and operate as though the monetary system is run by whim and prayer. Invest short-term. Plan for hyperinflation and severe deflation.

I think that even the average person probably understands that:

1) The gov spends more than it takes in

2) There is no political will to raise taxes and/or cut spending

3) The gov will be stuck spending more than it takes indefinitely

4) 1 through 3 mean that the government will have to keep printing one way or another

Credibility is huge a problem, but it’s not just the trust issue that is front and center here. It’s deeper than taking the Fed seriously. It’s an understanding that the Fed’s fight is futile. Pandora’s QE box has been opened and we now live in a system built primarily on debt and printing. It doesn’t take a logical leap to come to the conclusion that the Fed’s fight won’t work. These days, pivot talk seems to mostly be built around the argument that the Fed can only stay the course for so long before something big blows up. It doesn’t matter how valiant the fed is. They’re not going to pivot because they want to. They’re going to pivot because they will be forced to pivot by the next financial crisis.

I’d steer very clear of any funds manager who talks about buying Disney, Apple, Amazon or Google (much less Tesla) “at a discount” given their valuations now, that manager is probably the type to get duped by shiny objects and not do their homework about sensible valuations. It’s like that old lesson from Econ 101 where they talk about the sneaky trick that shopkeepers can use to sucker in gullible customers, by marking up the price of an item by triple it’s rational value, then cut that price in half and claim to offer it up “at a discount” (still way above what it should be selling for).

Like the other posters here saying, it’s not the discount or markdown that matters, it’s whether the stock price is consistent with fundamentals and commonsense valuations, and the P to E for Disney and the others are still way beyond anything that would be consistent with the earnings they can actually produce. The other factors are irrelevant–again Europe’s economies are export-heavy (and they’ve been busily introducing backup sources to deal with the energy issues regardless), so even with a tamp-down in consumer spending at home, they’ve still posted solid growth from exports and tourism by basically tapping into the consumer markets of other economies. It’s why the EU economies grew well in 2022 despite the predictions (it was actually the US economy that contracted in Q1 and Q2, even if not a recession with consumer spending still strong). And demographic factors like that aren’t really relevant for short-term fund manager decisions, and it’s not like the West is doing any better than Asia there (not to mention populations have to stabilize anyway at some point, even China recently has become a huge immigration magnet even if more locally, from Korea, the Philippines and Vietnam). So what matters is the valuation of the particular stocks in the equity manager’s portfolio, and they’re mostly still at lunatic values.

Even if Disney’s 40 percent off, it’s still way overvalued–40% off a ridiculous overvalued high is still way too high and has far lower to go. Like the others are saying, it’s theme parks are an overpriced ripoff, and with inflation raging so high even in essentials like housing and food, American households just simply don’t have the spare cash to spend as much on entertainment–those sorts of discretionary things are the first things to start to hurt with inflation this bad. Same for the housing bubble. That’s the problem with the Everything Bubble that ZIRP and QE created, it’s ruined price discovery and broken price stability and is threatening the very foundations of the US economy and social stability. And it’s why for all the dumb pivot talk, the Fed simply can’t pivot if the US economy is to survive, it’s Paul Volcker Pt 2 or bust now. The market can have these delusional rallies here and there but the effects of rising interest rates, yields and QT can’t be held off for much longer. Any equities fund manager worth their fees has to be aware of that, and if they’re picking their portfolios, they simply have to do their homework and search for better values reflecting what the companies can actually sell and profit from.

I agree with everything you’ve just said. But ETF’s are real. Mutual funds are real. And the maxim is true that no FA has ever been fired for buying …… stock. (Fill in the blank with GE, GM, Coke, Ford, what have you.)

If your job is to manage the pension assets of German machinists or Toyota Motor USA (positions I actually held, in a former life)–where are you putting new contributions now? What should you buy? It’s got to go somewhere. That’s the reality, and just because I know that DIS is overvalued no matter who they just brought back as CEO and even if every child in America bought a Yoda baby doll, because their cash flows are negative until 3Q 2023 at the earliest because their streaming unit is hemorrhaging money.

But what happens after that? Well, my job was to manage the pensions of guys who are today 35, and will need the money at 65, and I’m always having new money rolling in to cost-average down. And that is a huge, huge part of the asset management industry.

I’m a PE guy now. Much better, but also much harder.

Cheers Enjoy the weekend.

Re: “It’s not easy to ignore the monster rallies in US equities every time Powell says he’s serious about bleeding out the inflation problem.”

It’s a mistake to infer direct cause-effect relationships between events and subsequent price changes. The dynamic in play is usually much more complex. The “sell the bad rumor, buy the news” scenario is one example of how a market could move up following a piece of bad news. (Or vice-versa, down on good news.) I can think of several other scenarios as well. My personal speculative favorite is that some market whales want to use Powell as a patsy, and are manipulating outsize index moves via “wag the dog” options trading.

There’s also the vicious dynamic where MBSes do not fall off the balance sheet because nobody pays off their mortgages anymore – that market is dead, no sales no refinancing. Therefore the FRB will hold onto their MBS even longer! When they’re forced to dump their holdings on the ‘free’ markets there will be carnage.

Been wondering about things like this too, even if they wouldn’t qualify as black swan events, pressure must be building in some places when the normal market checks and balances and valuation metrics aren’t functioning right, so that when things finally do correct, they do so in a hurry (and probably overcorrect, like in 2009). Still thinking it’ll take a few years for this housing bubble to fully unwind to some kind of non-bubble level for housing prices that are closer to actual incomes, but also wondering if there could be an acceleration and then a sudden waterfall drop the way some trends are pointing. A lot of potential sellers have taken their homes off the market with the falling prices, but with pressure mounting, others are starting to sell even with the lowered prices. And with so much leverage going into many of the home purchases esp since COVID started spreading and the pandemic stimulus, the dropping home prices may force panic-selling as more and more esp of the investors buying homes fear going way underwater as prices drop further.

“When they’re forced to dump their holdings on the ‘free’ markets there will be carnage.”

Lmao. Forced by whom?

I think the lag in central bank policy is 6 – 18 months. If you count back on Wolf’s chart 6 months not much runoff had occurred and 9 months ago the Fed was easing.

I don’t think the average person realizes that 2023 is going to be the year that all the Fed tightening kicks in and leveraged assets get revalued with a 5% t-bill.

“…and leveraged assets get revalued with a 5% t-bill.” Sobering.

“I don’t think the average person realizes that 2023 is going to be the year that all the Fed tightening kicks in and leveraged assets get revalued with a 5% t-bill.”

What do you mean?

Big difference in what people will pay for an asset like an apartment building or a dividend stock when you can park money safely at 5% and wait for better prices.

Right, and there’s a psychological component to this where the “transient” mindset (“rates will come back down soon”) breaks down and people start thinking off things as permanent. Just as inflation turned out not to be transient and shocked a lot of people who should’ve known better, high-rates-for-longer will also be a shock. There are many, many businesses with weak debt positions (leveraged loans, anyone?) who can string things out in the short term, praying for rates to fall, but who can’t stay in business when they finally need to refinance.

People don’t look at 1 year T-bills when deciding whether or not to purchase real estate. They look at long bond rates, and the trend there is falling yields, now that Powell has revealed his true dovish sentiment in the Nov 30 Q&A session at Brookings.

Yeah I feel like in general it’ll take at least a couple months to really feel the brunt, even when Volcker started going all in with the rate hikes esp by early 1982 (though without QT back then), it still took until the end of the year and mainly by early 1983 before things really kicked into gear and the markets and consumers felt the full effects. I’d guess Q1 or Q2 before we really start to see things happen in a bigger way here.

why be optimistic about continued QT given the last graphic? seems like QT will happen for a little bit, there will be some “crisis”, then Fed will kick QE back into gear and the total assets will jump up to a higher plateau.

That crisis is NOW: Raging inflation.

Wolf so many times you discuss the issue with raging inflation and the impact on the poor. For the longest time at least through the QE period after Lehman and banking collapse inflation has been low even with QE and few but the fed seems to understand these issues. An inflation rate CPI above 2 percent is catastrophic. Also a market crash and a repeat of 2008 is as well so the Fed has a well laid out plan to tackle the problem. Thanks for the updates and the markets still have plenty of liquidity by design to find a reverting mean value after so much misallocated QE money available to wallstreet and VC.

The poor own nothing so they have nothing more to lose. The big problem is the Fed funds rate is below the inflation rate. That’s what causes people to go broke.

TRT – always tread carefully and thoughtfully around those with nothing left to lose. (Their definition of ‘reason’ can be subject to high and not-easily damped oscillations…).

may we all find a better day.

I heard yesterday that low end wage earners we’re the only workers whose pay has been out pacing inflation. Maybe lower middle class getting hit the hardest.

@ BS – ” For the longest time at least through the QE period after Lehman and banking collapse inflation has been low even with QE”

———————————————————–

That’s not asset prices had to say. They manifested raging inflation.

“Instead, when Treasury securities mature, the Fed gets paid face value from the government, and the Fed then destroys this money.”

What exactly are the mechanics of this? Maturity implies a payment to the Fed. What happens to this? Is it simply a credit to a Fed account which the Fed then ERASES???

When a Treasury security matures, the government must pay it off, no matter who holds it, whether that’s me or the Fed. So the government in advance issues new securities to get the money to pay off maturing securities. The government then uses this cash to pay off all securities that mature at that time.

For the Fed, this means that the government sends $1 billion from its checking account, Treasury General Account (TGA) at the New York Fed, to the Fed, similar to when it sends the money to me for a maturing bond. The TGA balance is a liability for the Fed (money it owes the gov). This liability drops by $1 billion.

After payoff, the bond ceases to exist, and the Fed’s assets drop by $1 billion, and the balance sheet balances.

The cash that the government sent to the Fed vanishes, in the reverse process in that the Fed created the cash to buy assets with.

And yes, everything, like everywhere, is done via debts and credits.

For a detailed look into how the QT accounting works, check this out. It’s likely going to give you a headache:

https://libertystreeteconomics.newyorkfed.org/2022/04/the-feds-balance-sheet-runoff-and-the-on-rrp-facility/

The crisis was yesterday: raging money printing.

Wolf, do you know understand why they are going fast on rates and slow on QT? I know they had the so called “taper tantrum” back a couple years ago. To me it’s like slamming the brakes on a car… but keeping your foot on the gas. Is it because draining liquidity can freeze up markets?

Kev,

The Fed is NOT going “slow” on QT. It’s the Fed’s FASTEST QT EVER.

This “slow on QT” is the latest idiotic version of QT-denier BS, designed to manipulate markets. Hedge fund gurus are instigating this BS to support their bets.

The Fed is not “keeping the foot on the gas.” That’s ignorant twisted BS. They’ve got both feet on the brake.

The QT from Nov 2017 till September 2019, over those 22 months, the Fed reduced its assets by $710 billion. Now in the 6 months since QT started, the Fed reduced its balance sheet by $381 billion already. By the end of this month, they’ll be down by something like $460 billion. They’ll be down by $710 billion by about end of March or April 2023. So in about 9-10 months, the Fed is doing what it did in 22 months before. That’s over twice as fast.

The dollar has dropped hard recently. If QT is destroying dollars, why is DXY falling? And how low can it go?

I notice that Reverse Repo (RRP) is draining, taking USD out of SOMA and this is adding dollar liquidity — so the stock market is up hard.

As the Fed reduces its balance sheet, with RRP draining — ordinary Americans may lose yet more purchasing power as DXY dumps.

Yeah, the RRP QT counterbalance seems to have finally awaken and may help explain some of these wild upswings in the market.

Soma Definition & Meaning – Merriam-Websterhttps://www.merriam-webster.com › dictionary › soma

The meaning of SOMA is an intoxicating juice from a plant of disputed identity that was used in ancient India as an offering to the gods and as a drink of …

If you look at a long term chart of the DXY you can see that it has reached these peaks before, near 120 in the mid 1980s and early 2000s. So I expect that this move up will eventually be reversed. Most of the short term moves seem to be caused by how investors feel about future interest rate moves. If they feel the Fed is going to increase up the DXY goes, if they they feel there is going to be a decrease. down it goes.

“For QT, the Fed doesn’t sell securities to the primary dealers. Instead, when Treasury securities mature, the Fed gets paid face value from the government, and the Fed then destroys this money.”

And I would add, this money is being destroyed because the government, in paying the Fed the face value of the maturing treasury, has to fund this payment with either new taxes or new debt issuance. It’s the funding of this payment from a source other than the Fed that ultimately “destroys this money”. The new taxes directly remove money from the economy, while the new debt issuance absorbs money from the economy by adding a new asset to the market that locks up the money.

Well we are barely out of the wood. From $9T to 8.6 is a measly 5%.

Wait till this number drop to $4-$5Trillion, then we can talk.

But all of these are needed to support the “economy”, right?

How low can they go before everyone hitting the exit button.

$4-5T? No way. I don’t see the Fed’s balance sheet getting much under $8T before they deem something a liquidity crisis and turn printers back on. They are very quick to cut rates and print, but anemic at doing the opposite.

Liquidity is only needed when buying is happening…. In a severe recession there is little buying because everyone is trying to sell….

Has anybody noticed that the spread between the 30-year fixed mortgage rate (Freddie Mac) and the 10-year treasury yield has gotten worse over the last 2 months, occasionally breaching 3%? I recognize that the spread had been worsening ever since the Fed started increasing rates earlier this year, but in the last few months it appears to have gotten worse. In fact, it appears to have breached the worst spread observed during the GFC.

FYI, I’m using the weekly data series MORTGAGE30US and WGS10YR from FRED.

Because bond market has gone nuts over the Fed-pivot delusion and pushed down the 10-year yield to ridiculously low levels.

Back in the summer of 2020, the bond market believed that the federal funds rate would go negative, and the 10-year yield dropped below 0.5%. Nothing is dumber than a bunch of idiots in the markets relying on their beliefs.

Eventually they’ll figure it out. It just takes a while.

I don’t see it that way. Long end of bond market is betting Fed is going to get rid of inflation by causing a recession. Gunlach predicted top to be 4.25 on 10 year when it was rising and about 4%. He was pretty close, but we will know within a few months if it was the right trade.

Gundlach is not “predicting.” He is “manipulating.” He is a bond-fund manager and is getting killed by rising long-term yields.

He was one of the manipulator idiots back in mid-2020 who tried to pump up his bond portfolio further by “predicting” that the Fed would lower the federal funds rate into the negative. This idiot helped push down the 10-year yield at the time below 0.5%. And people who bought the 10-year or anything near at the time got killed.

He has been WRONG EVER SINCE.

He will say anything to try to stop the bleeding of his bond fund, and he relies on CNBC, Bloomberg, etc. to help him spread the word, and he relies on people like you to help spread the word, so that it then happens.

That’s how all these fund managers operate. That’s WHY they show up on CNBC.

The 10-year yield will go well above 4.5%. Look at a two-year chart. The trend is perfect: big up, a retracement, another big up, a retracement, another big up…

For example, during the summer rally, the 10-year yield retraced by 25%; during this rally since early November, it has only retraced by 18% so far. So there’s still a little room to go before it snaps back.

Ha! The FFR will hit 4.5%, 10 yr will hit 3%! Look at the CURRENT trend.

In mid-2020, the same folks said that 10-year yield will go negative when it dropped to 0.5%. And people who believed it got their faces ripped off. Look at a two-year chart to see the trend. And it’s not to 3%.

I’m with Wolf. Can we all take a moment to remember Bill Ackman crying? Don’t believe the hype from these guys. It’s like Elon Musk’s Hyperloop. Take it as entertainment, but don’t give them your dollars. QQ

Jeremy Siegal just appeared on CNBC and predicted (out loud) a 2 handle on the 10 this time next year.

We will see. Recession is most likely coming and the yield on sp500 and yield on treasuries probably going to cross before bottom is in. Currently Sp500 is 1.6% and treasures 3.4%.

I will take a guess and say they will cross around 2.5% and it will be the most inverted yield curve in a long time, because the Fed goofed up the most in a long time.

We should know within 6 months I think.

Recession might be coming, and the Fed raises to 7% because inflation is still at 8%? The Fed has said a gazillion times it won’t cut because of a recession, that it might HAVE to CAUSE a recession to get inflation under control, and that it will only cut if inflation is headed back to 2%. There is nothing anywhere in sight that would cause inflation to trudge back to 2%.

None of these new bond kings and queens have been around in late 1970 and early 1980. People have trouble wrapping their brains around this concept of high and persistent inflation, and what it means for yields.

What these charts show is the Fed is moving slowly reducing its balance sheet and MBS. Their actions will be overtaken by events still unknown. Unknown Unknowns.

Interest rates are still well below the inflation rate. They are still stimulating the economy. People are still spending like drunken sailors with money they don’t have.

And not just ‘people’. In NC, Local and state gov’ts are spending Covid relief funds, drug monies from opioid mfgs avoiding jail time, and recently passed bond issues. A lot of these one time funds are being used to pay for ongoing, perpetual expenses, which will end in disaster.

The Federal Reserve is moving exactly as they have clearly stated.

That’s my impression too. A 50 bp hike in December was telegraphed in September. Nothing has happened since then (such as a huge surge in inflation) to suggest changing course. If the CPI on December 13 is very hot, maybe they go with 75 bp, but that’s unlikely. Personally, I want them to continue with at least the 75 bp hikes, but what I want doesn’t mean they’re not doing what they said they’d do.

Under current projections when will the MBS runoff hit the $35 billion dollar cap?

As far as I can tell, that will not happen unless Fannie or Freddie call a bunch of MBS held by the Fed.

Does anyone else have any insight?

The Fed can start selling MBS — and they’ve mentioned it. So maybe in 2023.

I agree that selling MBS would be great. But will the Fed stay the course if it precipitates a drastic fall in home prices?

Destroying money while forcing up mortgage rates is sound policy. But if the Fed chokes on selling MBS, allowing greater runoff of Treasuries instead of selling MBS would at least destroy the money, and might indirectly force up mortgage rates.

(And personally, I want to see home prices go down fast. I need to make a move by the middle of next year, since my condo building is being torn down to make way for an 80-story monstrosity…)

Powell explicitly shot the idea down when he was asked about it recently.

I think he said something like “we won’t consider it until QT is well underway.”

Can’t see fed selling mbs at a loss as that sets a bad example for managing capital

DX landed on Mar 2020 high @103.96. DX is up after the job report was released.

The DXY will soon be up well over 120 and headed much higher.

Off of your lithium again?

So…. latest job report is above forecast, wage is going stronger, retail sales or Demand is above forecast too. And Inflation still at well over 7% .

Yet Powell is thinking about slowing down rate hike?!! With Fed fund rate at mini 4%, way below CPI. And Fed officials play dumb, could not understand why Inflation, Wage, and Employment is SOOO STRONG.

Let me repeat. If business can borrow at mere 6% to expand product lines and sell these products at extra 8% inflated price, they would hire and expand. DUH!!

It takes Volcker in late 1970s to do the basic economic 101, increase rate to match CPI, to kill off the un-ending greed of inflation cycle.

This is the SAME POWELL, that kept printing QE back in early 2022 and kept rate 0% when Inflation was around 7.5%, and Employment was STRONGEST EVER.

And this is the exact same POWELL, that want to slow down rate hike when Fed rate is STILL 4% BELOW CPI, when Employment + Wage + Retail sales all above forecast, pregnant with HUGE Balance SHEET of 8.6 TRILLION FREE MONEY Sloshing around.

For 2 years, he has been scrxwing Poor People, scrxwing Down-To-Earth People who make honest living and saving in cash. And he is still scrxwing these people now.

XMAS Gift for Honest America!

By the time 2024 roll around and Inflation comes down to 3%, Powell would pat his own back and declare victory.

But then, all prices would be 50% higher than 2021.

Powell should be dragged out of building !!

XMAS Gift for Honest America!

It was Bernanke who really drained my bank accounts with his zero interest rate policies.

Yes. However, the products seem to be selling at a 15-20% increase, further widening the spread.

If you were one of the people getting financially bled out by this, what would you do? That wouldn’t result in a potential conflict with the justice system? Sincerely.

To discern the truth, (always) in plain sight, is one thing. Having an effective counter is another.

Meanwhile, I sometimes wonder if Wilson had a diabolical grin on his face or if he was under extreme duress, on that fateful christmas eve.

Is the employment situation really that strong though? There is a disturbing divergence between the BLS establishment survey, and the household survey. One says employment is growing and the other says it is flat.

You have to take all government statistics with a grain of salt, many if not most, are politically motivated, and then revised latter on after they have served their purpose…..

Jdog,

You’re wrong in your interpretation because you don’t know that the household survey includes gig workers, and the establishment survey only includes actual payrolls, not the self-employed, and employers have been aggressively hiring, thereby pulling the self-employed onto regular payrolls.

READ THIS:

https://wolfstreet.com/2022/12/02/the-jobs-report-in-light-of-what-powell-said-the-fed-cannot-create-supply-of-labor-but-it-can-tamp-down-on-demand-for-labor/#comment-483857

And yet it is the establishment survey that is constantly quoted as if it were the total, instead of a partial measure of the employment status. People shifting from one type of employment to another is not job growth and any attempt to paint it as such is a deception.

Of course we are always dealing with narratives and not facts when it comes to government regardless of the subject.

Sean,

Clear reasoning. No desire to see to Powell shot though. I would enjoy seeing him separated for any unjustly earned wealth, and having to do real physical work. But he’s just a pawn anyway. There is a deep line of pawns to replace him.

A foolish person, who pays attention to what has been done in the past, will predict that the Fed manages to do about a 20-25% reduction in the balance sheet, tops, before having to restart QE. So, I predict, being a foolish person, that the Fed manages to reduce its balance sheet to no less than 7-7.5 trillion before restarting QE, at which point the balance sheet will go over 12 trillion dollars by 2027-28.

It’s difficult to discern anything from the past when it comes to QT by the Fed since QT was done only once under completely different (noninflationary) conditions. I’m guessing the experience of the current inflation will keep the Fed from engaging in any significant QE for a long time, though it may suspend QT at some point, unless there is a severe deflationary crisis. We’ll see.

When was QT ever done, and did that play out?

You’re right, but the pace of QT matters between now snd then. If we get down to the QE level at the current pace of QT runoff, then the runoff will have been for nought, with no real impact to the markets or rate of inflation. On the other hand, if they increase the current pace of QT, then even though it will last for a shorter timeframe, it will put a dent if the inflationary mindset since asset prices would stabilize or even start falling slightly if the pace of QT was actually sufficient.

This is an excellent deep dive into the Fed’s balance sheet. Thanks for the thorough explanation.

Formerly, when financial markets tended to key off excess reserves, or the lack thereof, I followed the Fed’s weekly releases closely.

But after QE ballooned excess reserves into the stratosphere, Fed watching seemed as pointless as analyzing gradations of infinity.

With QT underway, that’s changed. The Fed has no analytical basis to forecast how QT will work. They’ll simply tighten till the weakest link in the financial system breaks. Then it will be bailout time again, as in 2008, courtesy of the ever-munificent taxpayers who weren’t even consulted.

To run an eclownomy, obviously you need insane clowns in charge.

If the Fed sells MBS when interest rates are higher as they are now, compared to when it bought the MBS, will it not lose money outright, since the bonds will be priced lower now, perhaps much lower? How much slack does the Fed have if its capital base is just $42Bn? Will this not make Fed bankruptcy a real thing? Can it use interest income from Treasuries to make up for this loss of capital? I mean, how will this work? And what happens when homeowners begin sending jingle mail – what incentives do banks have to try and resell the homes at a reasonable price if the Feds bear all the risk of repayment?

Losses don’t matter to a central bank that creates its own money. It will never run out of money.

In Capitol Hill testimony this week, Federal Reserve Chair Jerome Powell was asked if the central bank would consider selling its mortgage holdings at a loss by Republican Sen. Bill Hagerty, who estimated the Fed’s current loss exposure at roughly $500 billion.

About selling MBS outright: “It’s something I think we will turn to, but that time — the time for turning to it — has not come,” Powell said during the press conference after Wednesday’s FOMC meeting. “It’s not close.” So that was in September.

I am savoring the slow liquidation and bleeding out of assets. It is so slow some dumb asses think that it is going the other way or not happening. I am a liquidation masochist disguised as a saver so as to be acceptable in civil society. QT pain, slow and steady with a calibrated touch of the rate whip on sensitive spots is my game.

I agree with everything, except the need to be acceptable in civil society.

The fact that every dip in the stock market is seen as an opportunity to buy means that inflation isn’t even close to being under control. It won’t be under control until the speculators finally give up.

Inflation has shifted from consumer durables to services and now will be shifting to wages. With this rail settlement in the works, everyone is going to want the same or better wage and benefit increases. Look for teacher strikes, transit strikes, longshormen strikes. Read “When Money Dies”. The same thing is happening here that happened in Germany and Austria in 1921 to 1923. Those with union clout in essential services came out better than those without. Retirees, savers, bond holders and those on fixed incomes not adjusted properly for inflation are going to get screwed more than they have already, if not get completely wiped out.

The people never want to believe when the entire fraud ponzi stock market finally implodes that they won’t be the bag holders. The bankers and people in the know will always be the only ones who get out unscathed as they’ll be the first ones out.

Have the bankers gotten smarter since they blew themselves up in 2007-2008?

– Mr. Powell telegraphed just 50 basis points in Dec before this labor data and soon coming inflation data on Nov. This is data driven, right?

QEs were in Billions/Trillions

QT at snail place in millions

Wonder about the reality, if ‘mkt to mkt’ accounting standard was brought back today. especially MBSs – I know, I am dreaming.

If the inflation data comes below 7.7% big rally ensues but if it is 8% are above, mkts will tank.

Perception vs reality fight continues.

Does Mr. Powell really wants see a big dive in mkts before X-mas? Strong hopium and front running are still, there under neath.

Let’s wait n See!

If there is financial crisis of ‘any kind’ in Treasury mkt, guess which one the Fed will try to bailout, between Treasury mkt vs Stock mkts!?

Did Paul Volcker really tame inflation?

Economics is not really a science as there are too many variables to make it so(IMO).

At the same time Volcker was aggressively raising interest rates, there was also a whole host of economic events happening behind the scene.

For one, the baby boomers were just begging to enter their peek spending cycle. Production capacity soared via innovation to meet the increased demand and drive down costs.

Emerging markets, well emerged, IE China etc. further increasing supply and driving down prices.

The Fed is given way to much credit for the things that they claim they can control and never really faulted for the distortions that they create.

Where would we be today if the Fed had simply done nothing.

Simple solution, wipe the slate clean and sin no more…

I agree there were other factors in play. Saudi Arabia pumping oil like the world had never seen, probably has a bit to do with inflation in the USA coming down after Volker was appointed.

I still say that the sale of assets is pathetically small. Instead of focusing on raising interest rates, why not sell a boatload of the assets as quickly as possible? That will have a big impact on long term interest rates because to sell it off, investors will demand a higher interest rate.

My theory is that the Fed does not really intend to reduce these balances because taking these assets out of the markets props up asset prices and the Fed doesnt really want to pop any asset bubbles.

The goal of the Fed is to use increased interest rates to drive unemployment higher, thereby breaking the wage-price spiral and defeating inflation, BUT they dont really want to pop the asset bubbles in real estate and debt and equities. Why? Because the Fed cares alot about rich people and they want to keep the whole “wealth effect” in place. On the other hand, the Fed is willing to piss all over the middle class and poor people with higher rates of unemployment.

Building an economy on asset prices creates a gambling economy, where people with money never had to work or produce and people without money never can get ahead. It is the very opposite of what should be done.

At this pace the Fed will NEVER get close to selling this trash back to the markets. The Fed continues to backstop the risk-takers on Wall Street at the expense of the taxpayer (middle and upper-middle classes).

I really wish that Powell had to answer the questions of real people asking real questions, instead of the soft-ball questions he is asked by the financial media who are selected to enter that room.

Lots of frustration expressed on this board by people who are sick and tired of this BS.

Inflation will be coming down. It just takes a while for everything (rate hikes) to filter through the economy.

Just go look at things that are inputs into products. Prices have dropped dramatically form this summer.

-Lumber is now below pre-covid prices and 75% down from the ATH

-Oats are down 60% in just the past few months.

-Corn is down 24% and dropping

– Soybean oil is down over 20% and dropping

– Canola oil is down -30% and dropping

– Wheat is down 40% and dropping

– Cotton is down 50% and back to pre covid levels

– oil and nat gas are down over 40% or 50% and still dropping

– Lean hogs are down 30%

– Copper is down 20%

– Silver is down

– Housing prices are dropping

– Stocks are down 20% to 30%

– Cryptos are down 70%

– coffee is down 30%

Sure, there are few commodities that are up like cattle, rice, orange juice

If you look at charts going that only start at when the FED started raising rates, you would think we are experiencing massive deflation and the economy is terrible.

Anyway, those peak commodity prices this past summer are inputs into things we are buying now and next quarter. The effects of the dropping commodities should be seen 2Q2023..

You clearly haven’t read any of Wolf’s articles about how most inflation is in services now.

+100%

The central bankers want to get back to low inflation and asset bubbles everywhere. There is no intention to disturb the business models of kingpins at places like Blackrock.

We need central banks that are committed to reducing their balances to pre-2009 levels. These central bank balances are distortions of free markets. Financial markets were capable of functioning without these massive balances, time to get back to some reality in the financial markets.

If we stopped using monetary policy to pump up the wealth of the rich, then we could start to focus our attention on the politicians who are not doing their job. We could start to see that rewarding Wall Street jerks to ship jobs off to China was a horrible policy for true wealth creation (instead of financial speculation).

J Powell

A Bankers Main agenda is to make Money

” its a personal thing and general agenda ”

That’s the whole story .

To have a Banker Mentality at the head of the Fed means unless your in on it You lose …. The Inner Circle

The QT is way too slow, evidenced by the stock market roaring to near all-time highs. Furthermore, it’s now been 9 months since the FED started raising and there have been no appreciable effects. The NASDAQ went up almost 5% in AN HOUR during Powell’s comments. That’s an entire year of gains in normal times. That alone should have knocked some sense into Powell that there is just WAY TOO MUCH MONEY sloshing around. But no, Powell and the FED are looking for any hint of an excuse to slow their rate hikes. These guys/gals are fraudsters.

Yup! Stocks are all green now. The speculators still believe that the Fed has their backs. We’ll see if they are ultimately proven right in the next few months.

“Stocks are all green now.”

You spoke a few minutes too early, it seems.

Depth Charge

He has lost his credibility after his last speech this week.

His so called ‘hawkish’ words are nothing but ‘wishy-washy’ dovish tilt, compared to his 3 his own FOMC members including Mr. Bullard are consistently hawkish.

Look at the indexes, keep attempting turning into green! Mkt is laughing at him. Does he get it!?

The descriptors – No crisis – and – The good times – on the last graph. Source? The system broke in 2008. The fix was to give banksters legal immunity – insurance to continue – not to fix the dishonest system. Bank owned media spouted illusory good times giving time to plan a big 2020 story the people should accept as ‘real’. Accounts still unaudited and missing money unaccounted for. Ask the military where its gone. Tax payers keep giving. But to what. Is the question. Tech not shared. There but for grace go I.

Sure I have read the articles. I am just making an observation on commodities prices. Commodity prices are a big input into services too. Especially energy.

If I have a painter paint my house or an auto repair shop fix my car, I think the price of the paint and the price of the car parts have increased at a higher percentage than the hourly manual labor. But the aggregate of the material (paint) and labor end up being a service? I know because I have a painter who works on my rental houses and bids out his labor and I buy the paint. In the last bid, the paint went up 30% and the labor 10% yet they are combined as a service with a 40% increase if I just bid out the complete job to the painter. I

Yes, service inflation is up but why? It is easy to see commodity inflation but what makes service inflation go up? Does a barber raise his prices because we want to earn more profit or is it because his energy bills went up and the product prices (shampoo, shaving cream) went up in price and when he goes home his food bills increased. What if those the energy costs drop, the price of shampoo drops, and food prices drop. Will he keep raising haircut prices?

I did not say we will be at 2% inflation, but I think inflation has peaked for now. I don’t think inflation will keep increasing if:

– commodity prices drop and stay down.

– If energy prices stay down. If you go back and look at the historical charts of energy and CPI. When energy prices goes up, inflation goes up. When energy goes down, inflation goes down.

– The FED keeps draining liquidity.

From my perspective, it does not matter if inflation has peaked at 7 0r 8%. what matters is, it should go down to 2% which is Fed’s target rate and for this , we have long way to to go.

It also means, more hikes and QT along with big asset price down, of all assets.

Treasuries should be rolled off the balance sheet at a pace of $90 billion/month right now, not $60 billion/month. It’s obvious in the markets and inflation figures that the current level of QT treasury drawdowns is ineffective towards accompishing desired goals.

For treasuries, is there any information about the breakdown of those rolling off – Short duration vs long duration? And if total roll off is exceeding 60 billion, is fed buying the surplus? And what are they buying? Short term or long term maturities?

And how much over the $60 billion cap has run off and is being recycled into Treasuries?

Yes, you can look them up by type (Treasury, MBS, or Agency Debt), maturity, and CUSIP number, and you can download them and sort them and bathe in them, all right here:

https://www.newyorkfed.org/markets/soma-holdings