Sellers are struggling with denial: Priced “right,” a home will sell, but “right” is where the buyers are, and they’re a lot lower.

By Wolf Richter for WOLF STREET.

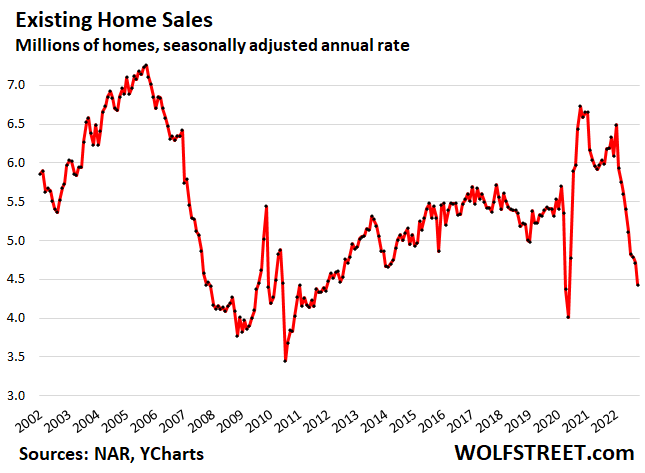

Sales of all types of previously owned homes – houses, condos, and co-ops – fell by 5.9% in October from September, the ninth month in a row of declines, to a seasonally adjusted annual rate of sales of 4.43 million homes, just a hair above the lockdown-month of April 2020, according to the National Association of Realtors. Compared to the recent free-money peak in October 2020, sales were down 34%.

Year-over-year, sales fell by 28%, the 15th month in a row of year-over-year declines. Beyond April and May 2020, this was the lowest rate of sales since December 2011 (historic data via YCharts):

Sales of single-family houses plunged by 6.4% in October from September, and by 28% year-over-year, to a seasonally adjusted annual rate of 3.95 million houses.

Sales of condos and co-ops fell by 2.0% in October from September, and by 30% year-over-year, to 480,000 seasonally adjusted annual rate.

Investors or second home buyers purchased 16% of the homes in October, down from the 17%-22% range in the spring and winter. In other words, their purchases plunged at an even higher rate than the purchases of regular buyers, as investors too are losing interest in buying at these prices.

This plunge in sales is a sign that potential sellers and buyers are in a standoff. Many potential sellers refuse to accept reality and lower their prices to where the sellers are; instead, they’re thinking, “and this too shall pass,” and they’re hoping or praying for a Fed pivot or for a miracle or whatever and don’t even put their home on the market, or pull it off the market after not getting any traffic at their aspirational asking price. And buyers have lost interest at the current prices.

Homes that are priced right – meaning priced down where the buyers are – are selling. But sellers don’t like to go there. And we see that in the active listings too. But there is some price-cutting going on, as more sellers figure this out.

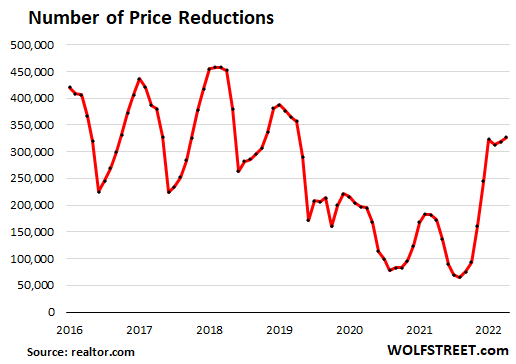

Price reductions: In October, the number of homes listed with price reductions rose to 327,184 homes, the highest since October 2019, and just a tad below it (data via realtor.com).

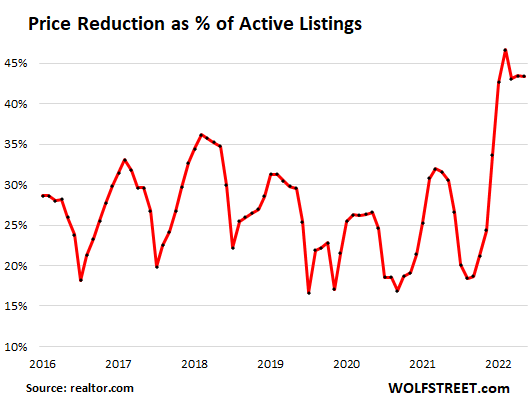

But the proportion of active listings with price reductions has exceed 40% for the past five months, by far the highest in the data that realtor.com makes available, which goes back to 2016:

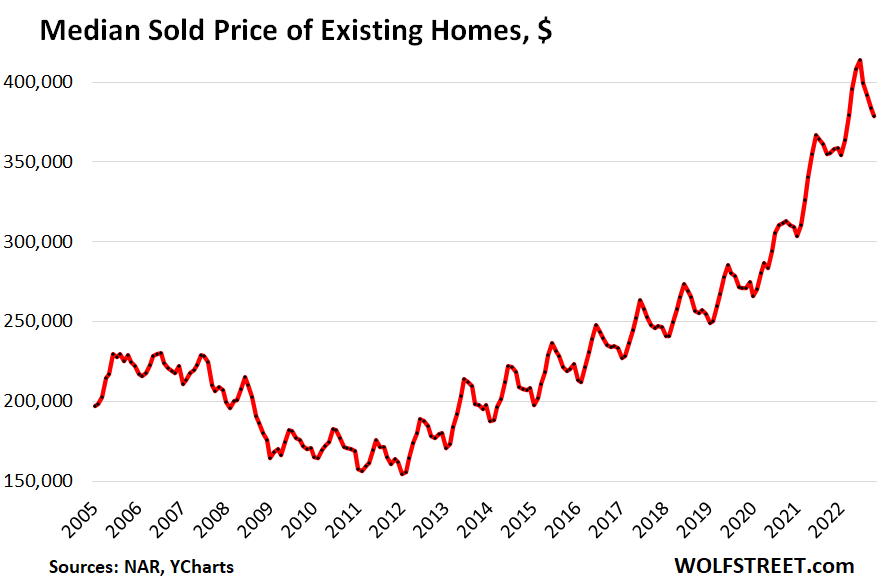

The median price of all types of homes whose sales closed in October fell for the fourth month in a row, and is now down 8.4% from the peak in June.

This whittled down the year-over-year gain further, to 6.6%, down from 8.0% in September, and down from year-over-year gains in the 20% to 25% range at peak frenzy last year, indicating that seasonality is only responsible for a portion of the price drop, and the rest of the price drop is some sellers getting more realistic (historic data via YCharts):

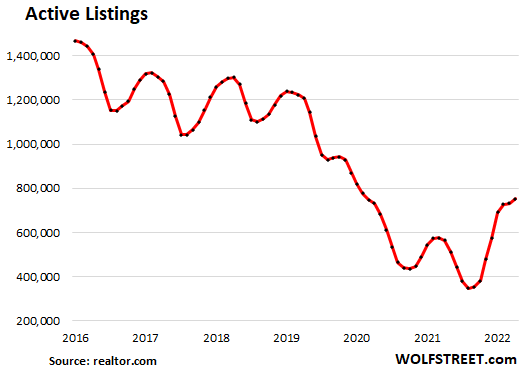

Active listings (total inventory for sale minus the properties with pending sales) rose to 754,000 homes in October, up by 33% from a year ago, and the highest since August 2020. They remain relatively low, another sign that potential sellers are still hoping for a Fed pivot or a miracle and don’t put their vacant home on the market or pull it off the market after a short while (data via realtor.com).

Days supply of total inventory increased to 3.3 months of sales, the highest since June 2020.

Sales by region: Sales plunged in all regions, but plunged by the most in the West:

- Northeast: -6.6% mom; -23.0% yoy.

- Midwest: -5.3% mom; -25.5% yoy.

- South: -4.8% mom; -27.2% yoy.

- West: -9.1% mom; -37.5% yoy.

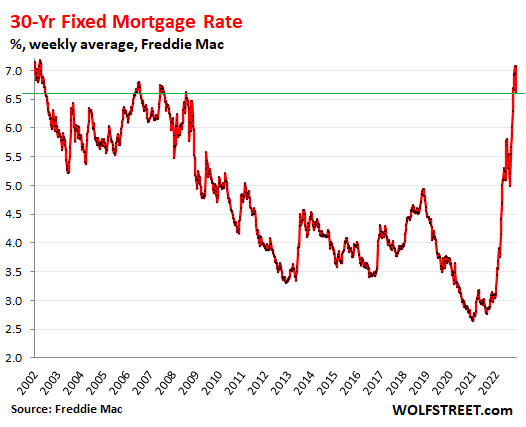

As mortgage rates jumped to the normal-ish range of the pre-money-printing era:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I wonder how much of this drop in sale is related to people finally settling down. In my area, almost all the growth in new homes has been generated from out-of-staters moving here for various reasons. Has this sort of thing finally ended?

Well, if they moved in from out of state, they’ve got to be leaving that state, and selling their home there, so one home comes off the market over here and goes on the market over there — unless they didn’t put their now vacant home on the market and are just praying for a Fed pivot or are trying to rent it out or whatever, which is a common affliction.

We should not blame sellers for this mess. They have a right to be greedy and have been led to believe that their extra house is an investment that will gather value and grow in size.

Only J Pow is the real scumbag behind this mess. J Pow has ensured that future generations, of this once great country, will become slaves to his cronies and will have to slog for their entire lives to get shelter. Most Kings and Monarches gave a much better deal to their commoners, than what we are getting in this idiocracy.

Wait 20 years and all homes will be owned by our big banks. They can print trillions with the press of a button, so we have no chance in betting against this casino.

Yeah, I fear that flag with Corp logos instead of stars is not far away. (I probably won’t see it, if lucky). But if I remind myself that dying is supposed to be a real bad thing, I don’t feel quite as guilty for being part of the generation that finally screwed things up beyond repair, when they had plenty of chances to change things (Carter’s career ending warning….only scientist we ever had as a prez). Especially since I’m kind of an expert on what agonies the “health” profession will put the very worst ones through, just to give them extra time to enjoy all their “hard earned stuff”.

“We should not blame sellers for this mess. They have a right to be greedy”

“Only J Pow is the real scumbag”

———————————————————–

to be greedy at the expense of others is scumbag behavior, no matter your size or position.

when scumbag behavior is accepted or condoned, you have or develop a scumbag culture.

Though many scientists state[196] that life extension and radical life extension are possible, there are still no international or national programs focused on radical life extension. There are political forces staying for and against life extension. By 2012, in Russia, the United States, Israel, and the Netherlands, the Longevity political parties started. They aimed to provide political support to radical life extension research and technologies, and ensure the fastest possible and at the same time soft transition of society to the next step – life without aging and with radical life extension, and to provide access to such technologies to most currently living people.[197]

Silicon Valley[edit]

Some tech innovators and Silicon Valley entrepreneurs have invested heavily into anti-aging research. This includes Jeff Bezos (founder of Amazon), Larry Ellison (founder of Oracle), Peter Thiel (former PayPal CEO),[198] Larry Page (co-founder of Google), and Peter Diamandis.[199]

I doubt such programs will be part of Medicare….but it illustrates the extreme degree of their mental illness. Being less sick is still sick….Carter’s point.

Which is also why my driver’s license says they can’t part me out, even though at 75 my parts are pretty worn out, anyway. The ONLY time I will ever set foot in a hospital again is after serious traumatic injury……where I am unable to or can’t talk my way out of it.

I don’t even like the MANAGED clinic my Doc works at (he doesn’t either), but I have a seriously trashed back, and can’t function without a couple weak pain pills…Tramadol.

My core muscles are really strong now……doing therapy as I sit here now……no more spasms, sciatica, and ambulance rides, thankfully.

Is your problem with Powell that he raised interest rates? What was he supposed to do, keep rates at 0% and inflation get more out of control than it already is? I don’t think future generations (or even this current young generation) is served well by a never ending housing bubble.

I kind of disagree with this. Anecdotally, many (especially older) people keep their main houses. This is supported by numbers as well. For instance Vacation homes went through the roof during the later part of the pandemic (https://www.nar.realtor/sites/default/files/documents/2021-vacation-home-counties-report-06-15-2021.pdf). In your above numbers you mention second homes along with Investors. I keep seeing sensational headlines about “Housing Shortages” (Fannie Mae[https://www.fanniemae.com/research-and-insights/perspectives/us-housing-shortage], WSJ etc.) all the while an estimated 7-10 million homes are vacant vacation homes. 5-7% of homes are empty most of the year (I had trouble finding solid numbers). People just have enough cash to not care. Many older (Boomer age) adults I’ve talked to have multiple homes. Sometimes up to 4 and they’re almost always underutilized. “I didn’t even go to my ski condo last year.” -Andy (Retired, Florida) “I’m going to rent from my Bunko friend. She has a house that they let their nieces and nephews stay in when they visit.” -My Mom. “We’re going to keep the condo so that my daughter can stay there when she visits from Italy.” -Barb. I have many other examples. There are also many cases of people inheriting homes and just leaving them vacant to rot. I’ve personally seen and tried to buy such homes in the past. Perhaps a recession, liquidity event or death of an older generation will free up some of these homes.

Where are u located?

Idaho panhandle…

I live in Eastern Washington… have for 22 years. I wonder what all the newbies to Idaho thought about this summer.

There were like 60 fires middle of the state to the CA border based on the AQI now website I frequented August thru October.

The last 6 or 7 years we got wildfire smoke here in Eastern Washington from all directions. No joke.

From California and Oregon. Idaho.

British Columbia. And every single year north central Washington plus a few other places in state.

AQIs maxed at 220 or 230 this year…most between 60 and 120.

It still irritates my sinuses at 100 or above.

But at least no toxic smoke as we had 2 of the last 5 years.

And no I’m no climate alarmist but another bad summer or two and I will be moving east…way east like across the Mississippi.

What’s amazing is that despite the rapid decline, houses are still up 6% yoy. IOW someone who bought last year would still be sitting on price appreciation far higher than a normal housing market , which is usually 2-3%. Shows you how much prices have to come down to reject the new reality of high interest rates. A 33% decline would barely come down enough to erase the past 2 years gains and last I checked housing was still considered unaffordable in 2019 and that’s with lower interest rates than now.

That’s why I’ll stick to my assertion that there’s a good possibility (though not a probability, yet…) that prices this time around will drop below the 2011 lows.

It’s not amazing. They were up 20%+ yoy. It takes a while to whittle that down. The last housing bust took 5 years to play out. Home prices are not like crypto prices. They move slowly. If they drop 1%-2% a month, that’s a lot already, as a national average. You don’t get instant gratification; you don’t get a 70% overnight rug-pull as you do in crypto.

“You don’t get instant gratification; you don’t get a 70% overnight rug-pull as you do in crypto.”

Why not? Some markets got instant gratification with 40%+ YOY gains. Jerome Powell and Co. showed up on the scene in 2020 and hammered rates to zero in one fell swoop while also unleashing a grotesquely revolting amount of liquidity.

That’s the scam. Quick with stimulus and stoking inflation, slow with fighting inflation. It would be much healthier for the market if it was a rug pull. Then we can more quickly get back to a more sustainable model which works for the masses, not the current corrupt model which skews everything towards speculators and the wealthy.

Depth Charge …..

+ 1000 % well said

depth charge…….. the vast majority of mortgages held today are below 4% interest rate. A big chunk of those are under 3%. Rates that low make it an asset. So if you have a very low rate and you can float the bill would you hold on to it and ride the storm out? I know I would.

So demand has been crushed and supply is still historically low. It is a buyer/seller standoff

I just heard from potential seller last week that he had full price offer.

very little down and would ‘assume’ their mortgage

ROFL – after I settled do we went 3 rounds why this was REAL BAD and likely cost them for years to come

when I mentioned the alienation clause – ie due on sale he said he asked his mortgage lender and they were ok with it

UNTIL THEY AREN’T

then it’s foreclosure, ruined credit and so many other ills that bad credit is

Dave:

No they aren’t. The volume of houses sold in the past five years is small compared to the entire market.

And life events happen. Houses sell. Things will change based upon payments.

Yeah, when something has intrinsic value blah blah blah… straight lines.

The storm was the asset bubble inflating — not the present correction.

the ‘deflation’ happening is like the back side of hurricane

looks for pretty right now

but soon they could be blood in streets

—

not that I believe powell will pivot, just hoping he doesn’t

right now I see lots of central banksters selling their treasuries in large quantities – ie fiat $dollars coming home to roost

china/japan??? more

This is not a logical argument. If housing is slow moving market and prices take time to come down they should also take time go up. But prices did go up rapidly. In some market almost doubled in 2 years. That’s breathtaking gains. The fact that they are not coming back down at the same pace as they went up implies that they will not come down to your forecasted levels. Sorry to break your heart on this but all other costs are up and there is no logical reason that home prices will be back down to even pre pandemic levels let alone 2011 levels. If material cost, labor cost, permit cost, energy cost all falls down to 2011 levels then I will believe you but these costs will only go up in rising inflation environment. Its simple logic.

If the cost of producing something goes above the price that many people can pay then only logical outcome is that those people will be out of the market, and volumes will decline. That is exactly what is happening, fewer listings and fewer construction starts. In the long run, this will make houses even more rare and scarce and valuable. Common sense.

Oh Kunal, what would we do without you to amuse us???

1. The funny law of percentages: You said: “In some market almost doubled in 2 years.” Which means +100% in 2 years (but OK, I’ll run with it). So to go down at the same percentage as they went up, house prices in those markets would have to go to $0 (zero), because that’s what -100% means??? You’re funny, Kunal.

You see, Kunal if prices go up 100%, they only have to go down 50% to wipe out all of the gains.

2. It took four months of declines to wipe out the last three months of gains nationally, so that’s pretty close to going down as fast as going up. Look at the chart, you’ll see it.

3. “… that they will not come down to your forecasted levels.” It slipped my mind. What levels did I forecast? Could you point at it? thanks.

4. Concerning your stuff about “costs”: Prices are NOT set by costs. Prices are set by the market. And the market doesn’t care about costs. And builders collapse if their costs are too high and they cannot sell their built spec homes for more than they have in them. That’s what happened during Housing Bust 1. Maybe you weren’t paying attention back then.

5. Companies lose money if they cannot get the price that covers their costs. Happens all the time. Lots of money-losing companies out there. After a while, they go out of business or file for bankruptcy protection. This is routine. COSTS DON’T SET MARKET PRICES. That’s one of the most fundamental rules, and you’ve got to try to get a grip on it, or else you’ll never understand markets.

6. Costs of materials, labor, and supplies are even more irrelevant to prices of existing homes (the topic here) because they were built years ago, and those costs are simply irrelevant.

Look Kunal, you’re really funny. In October 2021, right here in the comments, you got on this tightening-denier treadmill, and you said the Fed can never taper QE and it can never raise interest rates. And then when the Fed began tapering QE, you said that it can never end QE. And when it ended QE, you said that it can never raise interest rates. And when it raised interest rates, you said that the Fed will pivot and cut rates as soon as it gets to 1% or whatever, and that it can never do QT. And it raised rates, and now they’re at 4% and QT is proceeding just fine, and so a few months ago, you got on the housing-bust denier treadmill, running as fast as you can. What treadmill are you going to get on a year from now?

“Sorry to break your heart on this but all other costs are up and there is no logical reason that home prices will be back down to even pre pandemic levels let alone 2011 levels.”

This is what delusional greed looks like.

“What treadmill are you going to get on a year from now?”

The bankruptcy treadmill?

I’m sorry Kunal…

Maybe dig deeper into your analysis?

I might start tracking the price of 10 foot length x 1/2 inch diameter, Type L (medium thickness, blue stripe designation) of copper pipe at the wholesale supply houses.

Sure is trying hard to be next Lawrence Yun…from what I can see here, you’re doing pretty good so far. Too big he is not going anywhere anytime soon, he lasted since the last bubble/bust, likely will be around for this time around too.

“What treadmill are you going to get on a year from now?”

Buy now, or be priced out forever!

Sorry Wolf, but costs do matter if nothing else than limiting supply. What you and Kunal both overlooked is that land also has a cost and the residual value is the finished home value less replacement cost new including profit.

We are looking in a market where we get a beautiful, very good quality home (20 yo) home at a price that is half (or less) what the cost to build is where we live now NOT including the land component.

Cost may not be a primary driver, but it influences the market. If you doubt it, what would happen to values of existing homes if you could build a new home for less?

As we’re already seeing, the relationship is the other way around. When house prices fall amid this huge pile of inventory, homebuilders have to either cut prices to keep building and sell their inventory, or cut back on building. From what I can tell, some builders have chosen the first, others have chosen the second, and some do both. What this means is a large drop in housing starts (see here), which removes demand from materials and supplies, and then those constructions costs drop — and they’re doing that now. So if anything, a drop in market prices for new houses, amid lack of demand, is triggering a drop in construction costs. That’s the relationship.

So looks like whatever Kunal denies comes to pass sooner or later. Now that is a pattern worth following.

Wolf: “…COSTS DON’T SET MARKET PRICES.”

I took a class on the history of economics at UCB, (89?), and had the unfortunate task of reading Marx’s, Capital, among other difficult tracts. (Adam Smith was Great!) Though full of preaching and prognostication better labeled as philosophy, at best, I eventually dug out the nut of his, “economic,” argument, which boiled down to a single paragraph in a huge work, which I vigorously circled.

It stated that, to paraphrase, (I looked for it, but Marx is buried in somewhere in boxes), that, “…any price for a good over total costs of production is a function not of markets, but of exploitation.” That’s the whole point of Das Capital…

Wolf’s, “…COSTS DON’T SET MARKET PRICES,” is exactly the opposite of the key thesis of Das Capital! I mean precisely the opposite of the basis of Marxism! In Five Words! Brilliant!! I wish Marx would have been as concise as Wolf!

I argued in class relentlessly, and I believe successfully, that market prices reflected many valid social, economic, weather, and political forces, as well as, sometimes, exploitation. Though I still believe my arguments were valid, easily destroying the crux of Marx’s, “theory,” the majority of my fellow Cal students in my class and outside of it were not convinced, and that was in ’89…

Ignorance is much more sophisticated today, it has evolved modern post modernism to attack experience and reality themselves. It’s user’s beliefs dictate what are proper, “facts”…

To our great misfortune, these tools have been picked up and are being used by many social/political/economic groups in America today…

The current post-modern Marxist analysis requires no facts. In fact, it requires the denial of facts, of accurate percievable reality across its many frontiers, merely requiring the substitution of some aspect of, “social justice,” or “equity,” to establish, “correct,” behavior. In my example above, of market pricing.

Used slightly differently in advirtising these same technics typically validate experience based on ego and desire. In politics, they are used to generate & justify violent discord while suppressing any differing, “experiences.”

Fine times we live in…

“Facts,” have had little weight for quite a long while now, making them all the more dangerous when they ultimately reassert themselves, as we are now, “experiencing.”

Specific quasi-religious post-modern Marxist, “beliefs” are now considered as the ultimate authority for setting economic and social policies by a huge segement of our population.

“Equity,” and “social justice,” are the swords swung by our post-modern Marxists, but it is desire & open greed guiding the policy paths of our economic and political elites who promote them, if not the majority of our, “consumers,” while all are spouting their, “equity and social justice,” “rhetoric.” I want to say, “BS,” as our Black Lesbian Marxists buy mansions as our political and economic “leaders,” steal everything that’s not nailed down, painted, or saluted! Wolf sees through the salesman’s line…

Here on Wolf Street is one of the few places that reality and facts are the basis of analysis, and maybe, ultimately, conclusions and beliefs, rather than about every other analytical site, which typicall have it exactly the other way around. A breath of fresh air & clarity you are, Wolf my man! Thanks!

AlexW-

Actually, both Marx and Wolf are right.

Marx is right in the *long-term*: prices can’t go below costs. And also, prices *in the long-term* that are significantly above production costs are exploitation.

In fact, most economics theories agree, although they use a different term than exploitation. The difference between cost-based pricing and value-based pricing is exactly that: in a market where consumers have ultimate pricing power, markets tend to cost-based pricing or commodity markets. For example, selling a $2k laptop nets Dell ~$100 in profit because computers are an intense commodity market. Markets that remain above commodity or cost-based pricing for extended periods of time are taken as prima facie evidence of a poorly functioning market, with sellers able to command significant rents due to exploiting (there’s that word again) structural inefficiencies in the market’s structure.

Where Marx and non-Marxist economists disagree is the nature of those structural inefficiencies. Marx views them through a political lens (the inefficiencies are created by politicians and can only be solved by creating new political / power structures), while non-Marxists view them through somewhat less political lenses (until you get to the delusional free market absolutists who think there can be no such thing as an inefficient market, ever).

Meanwhile, Wolf is right in the short-term: due to rapid market shifts, people can be caught with their pants down and engage in forced selling (or buying) at non-economic price points. After all, leftover Christmas wrapping paper is sold for pennies on the dollar on Dec. 26th…

In this case the market is turning so rapidly that developers stuck on multi-year projects will often sell their inventory at below their costs just to avoid several years worth of carrying costs. And builders / contractors / etc with high fixed costs will often take jobs below cost if the alternative is no income coming in at all (just like airlines sell seats below cost because it’s better than nothing).

At any rate, it’s not that hard to understand Wolf’s meaning (and Marx’s, for that matter), and the fact that in all your ranting you so misunderstood both of them leads me to ask: exactly what grade did you get in that class you say you took?!

It really only took 3 years, Sep ’05 – Sep ’08, for housing to bottom, but the point is well taken that it takes time. We’re really only in about the 2nd inning here.

Jay,

According to NAR (shown on the chart in the article), two methods of counting:

1. From highest high month to lowest low month: June 2007 (record Jun) to low in Jan 2012 = 4.5 years

2. From highest low month to lowest low month: Jan 2006 (record Jan) to Jan 2012 = 6 years.

According to Case-Shiller (shown in the CS chart in the CPI article a little while ago):

Jul 2006 through Feb 2012 = 5.5 years.

This looks more like a typical seasonal downturn, which was essentially absent in 2020 and 2021. Active listing inventory is well below pre-pandemic levels, and this is what determines pricing at the end of the day.

JeffD,

“This looks more like a typical seasonal downturn,”

Nah. For example, from June 2019 through October 2019, the seasonal price drop was 4.9%. This year, the June-October price drop was 8.4%.

Since Housing Bust 1, there has never been a four-month 8.4% price drop.

In the article, I told you that the year-over-year price increase in October narrowed further, as it has been narrowing in prior months. If it were just seasonal declines that occur every year, the year-over-year price change would remain the same.

From the article:

“This whittled down the year-over-year gain further, to 6.6%, down from 8.0% in September, and down from year-over-year gains in the 20% to 25% range at peak frenzy last year, indicating that seasonality is only responsible for a portion of the price drop, and the rest of the price drop is some sellers getting more realistic.”

“Active listing inventory is well below pre-pandemic levels, and this is what determines pricing at the end of the day.”

You comment speaks to supply. But doesn’t mention demand. Sales prices are set by both. Not one or the other. And right now there is no demand.

I agree with you, but I would like to hear the peanut gallery’s thoughts on why SFH listing supply has been so slow to rebound.

Regardless, there is a ton of apartment supply on the way that will also apply downward pressure to prices.

I only wish my sources of supply data could tell me month by month when that apt supply will hit.

Also, there seem to be some mismatches between apt starts and ultimate apt completions (beyond the logical timing lags) that I don’t fully understand and would be interested in learning more about.

Reply to Cas127:

“…I would like to hear the peanut gallery’s thoughts on why SFH listing supply has been so slow to rebound.”

From the article:

“Many potential sellers refuse to accept reality and lower their prices to where the sellers are; instead, they’re thinking, “and this too shall pass,” and they’re hoping or praying for a Fed pivot or for a miracle or whatever and don’t even put their home on the market, or pull it off the market after not getting any traffic at their aspirational asking price.”

Note, that’s at the national level. At the local level, the story varies. For example, in Austin, inventory levels have risen well above normal, pre-pandemic levels. According to AXIOS, Austin’s inventory levels are at their highest levels since 2011 (article from October 21st).

You would think, right? But look at how out of whack Canadian housing prices are. With such easy financial conditions, you can no longer count on reason.

Granted, it’s lagging two months, but the Case-Schiller index for August was still up 13.1% YoY. Get back with me in January and let’s see what the CS index says then. I’ll perk up and pay attention when it gets to a 15% YoY decline.

My house doubled in value in 4 years. There are a decent number of houses that doubled in three years. We’ve got at least 9 months before it starts to get interesting. And as I always say, none of the price declines matter one bit if Uncle Sam swoops in with rent & mortgage relief when the going gets tough.

Modern Monetary Theory at it’s finest.

“We’ve got at least 9 months before it starts to get interesting.”

Hmm…look at the slopes of some of those lines.

Re savior pivots…

Uncle Sam may (after decades and decades of warning) be financially checkmated – he can’t pander politically by printing money (SOP) so long as printing money fuels politically poisonous inflation.

This isn’t 1979 where DC can gin up some economic horsesh*t about villainous suppliers creating inflation while shoving their forearms up MSM sock puppets to drill the only-DC “narrative” into the skulls of hundreds of millions.

Today, the internet will immediately call them on every ounce of their BS.

The internet can call them on their BS all they want, but the Fed, Congress & the Biden administration, IMO, are all in MMT-based running of the economy. This means that rent & mortgage relief will return at some point. They’re all in favor of stepping in and NOT letting markets decide winners & losers.

I realize I’ve never provided the reasoning why I think there’s a significant chance that prices will go below the previous lows, so here goes:

The main point is that the only reason house prices stopped dropping in 2011/2012 is because the Fed aggressively dropped interest rates until housing was finally affordable again. So if we assume that 2012, when housing stabilized, was when lower prices + lower interest rates finally hit an acceptable level of affordability during a bad recession, then we can calculate from that base to see where equivalent affordability would be in an equally bad recession.

Median house price in 2012: $238,700

Average interest rate on 30-year fixed: 4%

Monthly payment assuming 20% down: $911.67

From Statista:

https://www.statista.com/statistics/200838/median-household-income-in-the-united-states/

Median household income in 2012: 53,585.

Median household income in 2021: 70,784.

Percentage increase: 32%

So we can assume that the average household’s ability to pay has risen by 32% to: $1203.40

So what’s the average home price, given an average interest rate of 7.5% (Which, IMHO is quite conservative; we’re almost there already and the Fed is still raising rates) that this monthly payment will cover: ~$215,000, which is ~10% lower than the lows reached in 2012.

If interest rates level off at 8% instead, the average house a person, even with the elevated income of the past 10 years, can afford, would be: ~$205,000.

The key here is that, unlike 2008-2012, the Fed will not be lowering interest rates when house prices fall. Not when inflation is still raging. And interest rates have already risen enough to more than wipe out the increased buying power that Americans accumulated in the past 10 years.

So fundamentally, Americans can buy less house now, than they could 10 years ago in the depth of the last recession. That, to me is a stunning statistic.

Now one criticism might be that we won’t face as big a recession this time, so people’s balance sheets and ability to pay will be better. I’m not so sure that will be true. The Fed’s QE and lowered interest rates sparked a boom in *all* assets. By 2012 the stock market had already nearly doubled from its low in 2009. What’s more, inflation was modest, so even though people didn’t have much wage growth, inflation wasn’t eating into their earnings either.

Right now, people are “affording” much higher housing costs than this analysis might indicate, because their balance sheets are much better: they used part of the pandemic stimulus to pay down other debts, they have stable jobs, and savings from stocks, cryptos, etc. to afford the down payment. And despite this, we’re already witnessing rapid declines in house prices.

Cryptos have already imploded, and the stock market will go down significantly. The Fed will not stop its rate hikes and QT until the job market “cools down” which is codeword for higher unemployment and job uncertainty. IOW, people’s balance sheets will degrade significantly and this will further drag down affordability beyond just what the interest rates would imply, and, I personally see no reason why this affect will be less this time around than in the last housing bust, with massive job losses, underwater mortgages, wiped out equity, and skyrocketing personal bankruptcies, in addition to the new misery of inflation. I have no faith in the Fed’s ability to engineer a soft landing, and even the Fed has said as much now that inflation has become a harder beast to tame.

The main reason why this may not come to pass has nothing to do with affordability, and everything to do with if/when the Fed caves. IMHO, prices *have* to come down to previous lows if not lower for houses to truly be affordable for first-time buyers. But if inflation finally comes under control, there will be lots of temptation for the Fed to ease again and let the good times roll. And if it succumbs to that pressure, then prices may rise again regardless of the fundamentals.

But assuming that it will take at least a few years for the Fed to get inflation under control, and that it will pursue that course even if we have a hard landing, then I wouldn’t be surprised if house prices test and cross 2012 lows.

Anyway, that’s my attempt to prove I’m not crazy :-) Feel free to post your objections.

I see property listed in the most expensive parts of San Diego dropping by 400k or more at time of sale. So yeah, we have long way to go.

Great stats, thx Wolf!

House flipping has gone from a big growth industry with over 300k flips in 2021 (US) to a real hot potato now … despite a very strong Q1 2022.

And the big elephant imo are the STR’s with over 1.5MM in the US. Negative carry costs can no longer be justified by future home price increases.

“House flipping” shouldn’t even exist.

Are you blaming the flippers for doing the work the previous owners would/could not do or vise-versa?

I am not a flipper but people move to a new house to get away from the problems they never tended to in their prior home.

There’s a difference between rehabbers and flippers. Learn it.

The flippers usually don’t tend to the problems, either. But who cares about the foundation when there’s all that dazzling gray paint and gray plastic flooring?

Ahem — luxury vinyl.

Fine Corinthian Wood.

Sorry, I’m dating myself.

“luxury vinyl” cracks me up.

Hey, don’t knock the new Grey paint…it is the only thing holding that “rehab” up.

(It is actually mind boggling the almost non-existent actual rehab work that I have seen on some properties I drove by for a mere two or three years…I’ve seen very, very worn down apt complexes try to double rents by doing little more than painting exterior walls white with a shiny red stripe. They are near a college campus so I suppose the new owners – who vastly overpaid – are trying to mitigate their own screwups on the backs of naive 18 yr olds…just like our Congress creatures)

LOL.

I will never forget the showing of a house I went to, where I swear the kitchen floor was slanting at a 5 degree angle. Brand new granite counters, brand new appliances, brand new cabinets, but the whole place was about to collapse. Hilarious.

The U.S. housing market reminds one of that character of the “black knight on the bridge” in Monty Python’s “Monty Python and the holy grail”.

When housing becomes unaffordable, I look for innovation. Maybe innovation is already here in the form of multifamily structures. They seem so much more efficient to build than single family and I would assume most households now consist of only one or two people.

Single family dwellings may be a bit of a legacy from when people had large families and many were farmers.

I am helping my parents stay in their home as they are in their nineties. It is a modest 1000 SQ ft home. It served them well for 70 years. It was a little small while we were teenagers, but it has been an excellent life choice for them. Staying put for 70 years is mostly a thing of the past.

Tradition, family, simplicity, good genes and health-Awesome!

It’s just a flesh wound!

Waiting for comments on my area is still getting asking or over and house still selling like hotcake…I am expecting people in SoCal, especially South OC and West LA to still say the same thing. I do need some good laugh to go with my Thanksgiving turkey next week.

All markets are local. I saw two sales close in one condo complex nearby in the past month at historic records for that complex. Of course this does not translate across the entire market. They’re are still buyers looking in certain markets with a FOMO, but the pool is much shallower. I’m in a town that has become newly desirable in the past 10 years, which was before that a sleepy declining industrial town, so our results do not indicate anything. Real big houses are only marginally down here.

All markets benefitted from low mortgage rates. Hence, home prices went up all the places.

The same should be true in the reverse direction, right ?

I proffer a new acronym: FOTAL.

The Fear Of Taking A Loss.

Phoenix, Wolf sort of nailed my region when he wrote, “Homes that are priced right – meaning priced down where the buyers are – are selling.”

I’m in SoCal and houses priced in-line with comps at the low to mid range of the market are still moving pretty quickly at their asking prices. Houses priced way above comps are sitting. Sales are still happening waaaay above prices from a couple years ago. Inventory is still pretty sparse compared to normal, so it’s unsurprising that sales have hit a wall when you add higher interest rates back into the mix. Homeowners that I talk to are largely locked-into (more like stuck in) low interest mortgages… It’s going to take a lot of force to pry them out of their rut.

This article generally jibes with what I’m seeing. Number of price reductions have come up from peak craziness, but have flattened out still lower than normal (just like the graph). Median price dropping a touch, but still mostly in-line with the usual seasonal drop (we’ll see how that graph moves later in the spring). Active listings are up from peak craziness, but flattening out and still way lower than normal.

You may get a laugh this Thanksgiving, but with trillions of spare dollars still floating around and being removed very slowly, you may find yourself with a big frown a few Thanksgivings from now if this housing monster doesn’t go where you think it’s going. With a high rate of inflation, prices can stay stable or even go up in nominal terms while still losing value in real terms… Not all crashes look the same on paper.

I needn’t go any further than my own family. They all drink the Kool-Aid. In fact, one of them said last night “my house hasn’t gone down” when in fact they happen to live in a place which is ground zero for screwed iBuyers and crashing prices.

Phoenix?

I still mourn for Tucson – a reasonably priced option, very recently obliterated by the rightfully panicked hordes abandoning CA.

There are a few in my area that have sold over asking, but the majority of them are selling well under asking. Lots of price reductions. Still too high though- not selling very quickly.

In my neck of SoCal the buffed-out homes are selling about 10% below peak Spring ’22 prices and the others are selling closer to 20% below peak. This is no surprise. As with the last downturn, the most inferior properties will get hammered the most, the gems will hold up better. But make no

mistake there will be nowhere to hide, all classes are going down. Based on today’s closing prices, I estimate my area of coastal SoCal will see further reduction in the range of 25% as the market bottoms out in 2025-26.

I’m in SoCal OC and want to downsize and get to a quieter area so am warming up for buying/selling this summer when I turn 55 (in CA you can lock in your current property tax valuation when you bought, which is very valuable now after the last few year run ups).

I’m looking to move in a 20 mile radius and if my house price goes down so will my target, so I’m a immune to price changes, plus know what my tax bill will be no matter what. Interest rates are not a factor for me at so don’t care what they do.

I’m starting early research and I am noticing houses staying on the market a lot longer and definite price declines. I expect that to accelerate when I get serious in the summer.

As always, love your insights Wolf. One piece of feedback though: charting the number of price reductions on an absolute basis is fairly misleading, as it is highly contingent on the number of listings. Looking at it as a percentage of active listings will be much more telling, particularly in this restricted inventory environment.

Good point. Added.

This current situation is simply a move for the big guys (Blackrock et al) to pick up the unsold houses held by home builders at fire sale prices. In the process they will bankrupt these builders, so when these houses go on the rental market at artificially high rents, there will be very few home builders remaining to alleviate the “shortage” that is causing the high rents.

Prices go down because of high interest rates, these guys buy for cash at bargain prices.

I have to admire the brilliance of this move.

The big rental guys can ask for any rent they want, but they have to take the best offer or carry the expenses. The last time I rented in Florida my credit was terrible and they took my lower offer. The following year they jacked up the rent and I moved out, forever. There are limits.

You are correct. The premise in the prior post is wrong.

Landlords, corporate or otherwise, cannot keep raising rents continuously as their tenants continuously become poorer.

This is what has been happening for at least a year for the US population as a whole, longer for many.

I consistently read posts claiming or implying that because everyone has to live somewhere, that there is no practical limit to rent increases.

Wrong and I am not referring to more homeless or even living in cars.

People will double or triple up creating a huge glut.

If this type of reasoning was correct, then rents would be much higher worldwide. There is a huge shortage of housing in the third world.

It doesn’t matter that the US isn’t categorized as third world (yet), it isn’t exempt from basic math.

There is one factor you are overlooking. As real estate gets concentrated and consolidated into wealthier hands, there is less need for them to actually make a profit. These people would of course like to, but oftentimes they just hold vacant land and buildings for decades. I can show you commercial properties which haven’t been leased for 20 years, but they’re paying taxes on them.

You may ask “why would a wealthy person want to hold a non-performing asset for so long?” The answers vary. They can use them as losses to offset capital gains, so far as I’m aware. Another answer may be simply “because they can.” Some of these entities have so much money that they literally just buy things, real estate being one of them.

I know long time land owners who will never get their money back on what they have spent in taxes alone. Why are they holding this land? Because that’s just where some of their money is. It may not be the best use of it, but it is what it is. Never underestimate wealthy people just parking money in places that don’t pencil out.

Augustus, rents can increase nominally as long as the dollar exists. I dug back through the “Housing Bubble 2” category here on Wolfstreet, and the earliest article that I could find mentioning “Housing Bubble 2” by name was written on March 19th 2013, effectively a decade ago. In the concluding paragraph, Wolf writes, “At some point, not being able to make money on rentals, investors will try to bail out.”

The writer is a sharp and logical guy, and his prediction was totally reasonable in the context of the couple of decades that preceded it. Yet here we are a decade later. Rental demand is high. Investors didn’t bail and they have largely made a killing… Now they’re a huge force driving the build-to-rent market. A reasonable person looking at nominal prices could assume that something must give. But one focused on real value in the face of massive money creation would understand that all of that new money backed by no value-added work would have to go somewhere.

Don’t fight the Fed, and just as importantly, don’t trust the Fed. They are not looking out for you and me. This is an aging empire, well past its rapid growth period. Our government is on the irreversible path to inflate our reserve currency until it is replaced by some other currency. Given the lifespans of past reserve currencies, and the current lack of a solid competitor, that could still be decades away. At the end of each decade, rents will most assuredly be higher than they were at the beginning. The average American will be nominally wealthier, but poorer in real terms.

Not Sure,

Re-read what I said in that article about house prices from 2013 that you cited: “At some point, not being able to make money on rentals, investors will try to bail out.”

If you cannot make money with a rental property because rents haven’t kept up with home prices… that’s what this is about, not declining rents.

Rents dropped 25% in Bay Area following the dotcom bust and didn’t recover until money-printing started a decade later.

Rents dropped by 40% in Tulsa when I lived there. Even my own landlord dropped the rent by 40% of the 3-year period that I rented there, before I bought a condo. And you bet, investors bailed out by sending the rental properties back to the banks, and the banks then collapsed, and the FDIC then sold rental properties to new investors. That’s how that goes.

There are lots of markets were landlords bailed out by defaulting on their mortgages and send the rental property back to the lenders. Investors set up their rentals in an LLC. So if the bank wants to go after the LLC, fine, let her have it…

Landlords defaulting on rental properties and letting the properties go back to the lender was a pandemic during the mortgage crisis — and was in part responsible for the mortgage crisis.

In San Francisco, asking rents peaked in mid-2019, according to Zumper, and have dropped quite a bit since.

Rents drop in all kinds of markets. So rents can and DO drop, and by a lot.

For people people like you who don’t look at the market-by-market rental data, it gets confusing because what hasn’t happened yet is that rents drop in enough markets simultaneously to push down the national CPI for rent. So it looks like rents are never dropping. But that’s BS. Rents do drop. And landlords get the rent in their market, not the national average rent. The national rent changes are irrelevant for landlords.

To Depth Charge and Not Sure,

There are always exceptions. Example being old family money that is not interested in maximizing current or near-term returns. I get that.

Second, we’ve been living in an era of cheapo money and the loosest credit standards ever. The interest rate cycle from 1981 is over. (2013 was during this period.)

That’s the environment both of you are describing.

When rates “blow out” later which is exactly what is in store later though not in this first leg of the new interest rate cycle, many real investors will go broke or their investors will force them to sell or cash out.

Unemployment is going to soar where renters won’t be able to pay today’s inflated rents. Some investors may choose to leave their properties empty, but most won’t.

If inflation is consistently high (something I acknowledge is possible but don’t expect until later), today’s nominal rates may not decline much or at all but that still doesn’t mean high (or any) rent increases from today’s levels either.

I am about to get a tiny insight to the new real estate market – my brother/sister and I jointly own a home in northern wisconsin near lake superior in city of roughly 10k in the nicolet national forest . gorgeous area with 5-6 months of winter ! real estate has been red hot for the past two years and values are ridiculous – it will be an interesting real time experiment

My family is from Minnesota. They generally have less positive reaction to 5-6 months of winter. ;-)

Yeah, here on the northern Prairie, it is now -8C with a 26 k.p.h. wind out of the northwest. Sixteen days ago, it was 24C. All four seasons definitely take their turns as the year moves by.

Hell, the gravel bike is always good to go, but the sports car, the motorbike and my favorite road bike are now out of commission til spring. The roads have had a few days of snow falling down on them, and of course, they’ve been salted up with ice melt.

Oh well, last week I put the Blizzaks on the daily driver, and it’ll be spring again in no time, eh?

My Dad texted earlier today that the wind chill is supposed to drop below zero tonight. I’ll visit, in the summer.

In Houghton the college students make igloos. Helps the ESG scores.

Keep them Cash Cows a moving from California. $1.4 Million(SF) to $950K (LA) sales prices these folks must have lots of equity left over in there pockets after selling. Lots of Tech jobs and companies hanging their hats in Denver Metro.

San Francisco homebuyers searched to move into Aurora, CO more than any other metro followed by Los Angeles and Boston. #1 goal is to make money and STOP the bleeding. It’s like watching termites eat away at your equity and waiting for the other shoe to drop. I might as well be happy for my new neighbors

It’s not just house prices. It’s about the quality of life. California is a dreadful place to live. There no sanity here nowadays, if there ever was. I could go on, but I’m getting out, also.

No sanity anywhere. None. After 70 years here I’m totally batshit crazy.

Too far gone to even know I should get out.

Flee, flee…….before you end up like me!

A lot of that wealth will disappear. Even with that equity in their pockets, a tech layoff will burn most of it away. Just saw Carvana was laying off a ton of people. Right now employees laid off are finding jobs quickly, but eventually the job market will be saturated.

If prices fall to reflect current interest rates, shouldn’t the market loosen up a bit? In particular, I thinking of move-up buyers who have a low interest rate on their current mortgage. The incentive to keep a low interest rate on your current home declines as prices of other homes decline to reflect higher interest rates. You may also be able to refinance in the future and if applicable save more on taxes. Why not move if it makes sense for you and your family?

Of course, price drops on your current home may make coming up with a downpayment difficult. Otherwise, as long as prices reflect interest rates there should be some activity in the market. We just need further price drops to find the “right” price.

Ok but what is the “right” price reduction when interest payments have more than doubled in less than a year? Houses have not even begun to come down enough in price to make up for that.

It’s not too hard for an individual to do the math and figure out what the “right” price is, depending on the person’s current interest rate and the potential sales price of the home they’re selling to move up. My main point is that people should be willing to move from a lower interest rate to a higher interest rate mortgage once prices drop to reflect higher interest rates. Falling prices should unlock that part of the market.

People moving around and selling ONE house to buy ONE other one does not increase or decrease the absolute inventory. Wolf covers that off and on.

What increases the inventory is new homes and also sales of investor’s homes. New homes have declined, but we should expect to see a lot of vacant and second homes and AirBnBs back on the market as the real economy declines further.

Lynn,

I agree that inventory will not increase if people are selling one home to buy another. I just think that at a certain point people will be willing to trade a low interest mortgage for a higher interest one if the price is right on the home they want to purchase. I’m thinking that all the low mortgages out there won’t necessarily be an impediment to turnover in the housing market if prices drop enough. Though I think “drop enough” is more than many people can imagine right now.

Ok but what is the “right” price reduction when interest payments have more than doubled in less than a year?

Nearly half! :)

My upper-middle income family member who wanted to move up decided to remodel. New kitchen and all 3 baths, the kids got new beds and room decor. The playroom for the kids got an overhaul as they are older now.

They have a 2.5% mortgage rate, easily affordable payment even if one person becomes unemployed. If things get really bad, they would put the kids in Charter school instead of private school. I doubt the twice monthly housekeeping service would stop.

I know what you mean. If things get tough enough we just may have to take the kids out of school in Switzerland and put them in some east coast private school. Maybe sell the smaller boat in Napoli.

What I can’t understand why so many houses are still selling at these prices, which clearly have a ways to drop over the next year. Who is buying?

I guess if I am trading houses, moving from one place to another, it’s a wash. But what about people buying their first home?

Here’s a thought: it might make financial sense to sell your home (if you have the career/retirement latitude to do this), assuming you have a significant equity gain, and take back the first TD with a rate lower than prevailing rates (and reducing some of the “garbage fees”) for a 5 or 10 year term, amortizing or interest only. With a 20% down payment! There is a huge tax incentive for equity gain if the home has been lived in for 2 years or longer. And a 5 – 5 1/2% loan rate for 5 years is a decent return. The risks are: 1) inflation worsens, 2) the property value goes down more than 20%, 3) you have to repossess the house. 4) you can’t find a better place to live.

A quick review of rentals will help answer that second question, particularly in metro areas where rents are absolutely bananas, around $3k/month or more asking rent for a 2-3 Bedroom apartment, even more for houses (utilities not included).

Wolf often points out asking rents don’t necessarily mean actual rent agreed upon. Rents go for highest bids in my area. And with leases not being renewed because of rent increase restrictions on current leases, a lot of people are looking at buying in an insane market as an even trade. Myself included, unfortunately.

Mitch we see almost no first-timers in my neighborhood, it’s all traders rolling $$ from one property to the next. People keep repeating this mantra of “all real estate is local” which i never understood. If Bay Area expats are rolling to SoCal and bidding up neighborhoods and Bay Area values go down they have less to roll which directly impact SoCal bidding wars/prices, doesn’t sound local to me but what do i know.

I’m seeing signs of that in my area. One investor selling bulk to another more optimistic investor- those houses might not even go on the market. Price seems down a bit on those.

Some are home owners but also a good percentage are investors who are in denial and not doing their math. There are a lot of people who have recently bought investments with no experience. There is still some foreign investment going on and it would not surprise me to find out some of that money is offshore money fleeing Russia.

The RE investors’ forum I lurk on is only now starting to come out with articles on being careful when buying in this environment. Most of their articles have so far just been a marketing cheer lead for buying R.E.. Just, well, just because.. The smarter ones are looking for other avenues to invest in.

I would not be surprised to see some developers taking advantage of any gov funds they can find to build low income multifamily housing soon. If they can find any..

Now is a great time to buy.

Just ask a realtor.

In fact now is a great time to buy stocks.

Just ask a broker.

In my horrible little enclave here in Canada, prices peaked a bit earlier in January this year at a shocking 1m-ish for the average non-waterfront/non-acreage house, according to VIREB data, and have since dropped to around 800k according to September statistics. October showed very little movement, which surprised me, i.e., prices were pretty flat but sales were still way off. Is that a bit more calm before the next storm? I think so, but can we appreciate for a moment the accuracy of American hand-wringing when it comes to overpricing in the US, when Canada is sitting at averages almost twice as high? We are THAT crazy up north, in other words. Lots of listings piling up here with ridiculous price tags, so what Wolf said is completely correct: the only sales that happen are at levels that buyers can handle.

I try to tell my friends, who are house-blind and rate-challenged, that any pricing above basic replacement costs for a house are purely emotion. To me, it’s pretty obvious what happens when you combine cheap money with short term thinking, i.e., loan a million fools a million bucks, they will: 1. not think about any scenario where rates will go up or real estate prices/sales will go down, 2. will outbid each other to the point of maximum loan carrying capacity. It wasn’t investing acumen or actual value that FOMO’d them all into houses, but a game of financial Twister played by the recklessly indebted.

That said, I am still astonished by the traffic some open houses are getting here (I go out of morbid interest if I have nothing better to do and want to waste an hour of my time), but it’s definitely a certain demographic that very much does not fit in with the redneck-ish population here.

TEMPLE

Great data Wolf !!

Monthly declines are notable whereas annually, we are still in a “boom” market. That whole “statistics” thing is a crazy science.

This does reflect on how long the unwinding process is going to take. 2025 sounds about right.

Beardawg,

If your stocks are down 15% from the peak six months earlier, but are still up year-over-year by 5%, you’re NOT still in a “boom” market. You’re in a “correction.” And if it keeps going, you may end up in a “bear market.”

Once you get enough monthly declines together, the price will be down on a 12-month basis. But there is nothing magic about 12 months. The price can be down on a four-month basis or on a 24 months basis or whatever. Declines are measured from the peak. Like the S&P 500 is down 18%. It’s not still in a “boom” market because it’s still up from where it was 2 years ago or whatever.

BTW, if the NAR’s median price drops for another three months at the average rate of the past four months, the median price will be down year-over-year. And it will be down 13% from the peak. There is no magic to it.

In the Bay Area, for example, the median price, after a series of month-to-month declines, turned negative year-over-year some time ago, and it’s still down year-over-year. Just a little ahead of the national median.

Math is hard

Leave it up to Beardawg to completely misinterpret the data that you spoon fed him. Falling down drunk so early on a Friday?

Sorry DC, you misinterpreted context, as usual, but it made your Friday night fruitful. ;-)

You guys must be friends, or should be.

WOLF

I understand the YOY vs MOM (month over month) stats. I was just remembering the old saying “Statistics lie and liars use statistics.”

A realtor or other speculator could cite “6% higher than last year” to a gullible 1st time buyer…and they would be correct, but MOM tells a whole different story.

The unraveling is beginning for sure and as you state, the trajectory is reflecting a few more months for national stats to reflect “flat” YOY. 2025 is prolly the bottom.

Got it. Thanks for clarifying. It flew completely above my head. I agree with you. That’s exactly what the industry is saying out loud. More quietly, they all know what’s going on.

All-cash sales accounted for 26% of transactions in October, up from 22% in September and 24% in October 2021.

Yes, people with cash are paying cash instead of borrowing at 7%. It’s like earning a 7% risk-free tax-free return on your money. Where else are you going to get that? I know people who did that. If you want to buy a house, you sell your stocks and use the proceeds to buy a house, and make what amounts to a 7% tax-free and risk-free return. Best deal in town.

If mortgage rates drop a lot in a few years, you can then take out a mortgage and plow the money back into stocks at a much lower level, no?

Lots of people sit on a lot of cash, stocks, and bonds. They’d be STUPID to take out a mortgage at these rates. They can be their own banker. And that’s exactly what they’re doing. That’s why mortgage applications have collapsed a lot more than home sales.

“Yes, people with cash are paying cash instead of borrowing at 7%. It’s like earning a 7% risk-free tax-free return on your money.”

Why do you say it is tax free return on your money?

If you put $1,000,000 into junk bonds that pay 7% in interest, you pay taxes on this $70,000 in income a year. Plus you have lots of risks.

If you buy a house for $1,000,000 and instead of getting a 7% mortgage (= $70K in interest expense per year) you pay cash, investing that $1 million in the house, you save 7% in mortgage interest = $70K in savings. Saving $70k = earning $70k. But you’re not taxed on the $70K you saved.

Agree Wolf, and why I have so much hope for the younger folks!!!

SO far, IMHO, these younger folks, probably including YOU, have a ton more knowledge than I did at their ages now…

ONLY thing this old boy would ask is to INSIST that each and every school at each and every level would make it impossible to get any degree without a full and clear ”TEST of Financial Knowledge”…

And then, I would ask every ”jurisdiction” to make it equally imperative that EVERY ”drivers license” be required to pass a ”FINANCIAL LITERALLY” test,,, including at every renewal.

VVN – I’ve felt for some time that college applications should have, in addition to the letter about all the great non-academic stuff, a business plan outlining how the education will provide sufficient cash flow to retire any student loan debt incurred. There would be a lot of lies, but at least it would force prospective students to think it through.

He who panics first panics least

Hugh Hendry panicked his way to St. Kitts.

He who panics first panics best, is my preferred version :-]

Hopefully you didn’t panic least (or best) in 2020. Probably not gonna see a better opportunity to make a ton of money on the market or with RE like that again in your lifetime.

The chart I would love to see is the median monthly payments based on home price at current mortgage rate. That char would be through the roof.

Redfin posts a number of good housing focused charts weekly with one of them being what you’re looking for.

I google redfin market tracker to get to the right part of their website.

then 10 year treasury has fallen in yield about 3/4 of a percent which should translate in lower mortgage rates. As Wolf states ” nothing goes to heck in a straight line”. We may get a bump in prices for awhile. Maybe rates come down to 6.5 from 7.25

We were at 6.6% in early October and lower in September, when these sales were made! We haven’t even seen the impact on prices of the 7.2% mortgage rates yet. That’ll come in November.

During the last boom alot of people either cash-out refied or HELOC’d against the soaring value of their homes thereby reducing equity headroom from the bottom up, then got their heads smashed in when values came down. Compression fracture. Can’t see why at some level this won’t happen again given the ’20-’21 MEW boom.

If lending standards are what I keep on reading here (stricter but still very lax), the difference is that they won’t qualify for comparable size loans.

Their incomes won’t support it.

Hoomers in Canada are already complaining that their variable rate mortgage payments are rising every month.

This bubble wants to be too big to fail, but something’s gotta give. The younger generations are wondering what’s the use to work hard just to pay extortionist rent and price gouging groceries.

I’ve been watching a cross section of the Phoenix market very closely. Recently, of the tiny number of homes that do sell in relation to the # listed, it’s only the best of the best listings. Anywhere between 0-25% less than the original listing price. Some sitting months before selling. There are PLENTY of other listings in the same price range.

I’m also watching some homes come on the market, wait, then come off only to be rented when they don’t get their super high asking price. The rent is also high.

I believe the frozen market has pressure building behind it. When prices start to fall at the margins when the pressure on sellers finally increases enough… it will be interesting to see where things settle. I think the rest of the year will be quiet, Q1 or Q2 next year should be interesting.

I love the “I’ll just rent it out at a loss until the market turns around” people. This is how you lock in massive losses. Hello foreclosure.

It gives you something to do with that extra money you’re getting from the second job you had to take.

I was in PHX during all of HB 1. My former roommate listed his house at $575K and ultimately sold it for $350K, with multiple reductions all the way down until it finally sold.

New supply might be curtailed for lots of reasons, including the increased costs of building new homes relative to what buyers’ can afford.

Home prices will likely go down in real terms for reasons already cited, though in the aggregate, a new home is the cost of the home and financing costs, so cash buyers may find some ‘bargains.’ On a nominal basis, homes may not go down that much, especially in certain markets, so that might affect the psychology of those markets, in which part of price reduction is camouflaged in inflation.

I also suspect that buyers are now able to negotiate more repairs after the home inspection than months ago, and this is another camouflaged price reduction.

Going into this time of year,Thanksgiving and Christmas etc,people are starting to delay any major changes in life’s,until the new year…By then,sellers and buyers should have a better view of how the upcoming Spring will unfold,mainly interest rates and housing prices…

The opposite applies in “resort” areas. This is when the fish are in the pond. The come “for the season”, get bit by the “I gotta buy one of these”, and the rest is history.

The “gloom and doom” about PHX is greatly misrepresented. Maybe in a tract whack subdivision properties are languishing, but in areas where you have views, stuff to do, and dark skies…. it doesn’t (yet) appear to be happening.

What do I base this on? Houses in my hood (one on my street included) are selling quickly…. the one next to me was cash (geezer, of course I’m a geezer too) and sold in two days. Closed in two weeks. Full pop.

Even houses with crappy locations in the community (as long as they don’t back to the busy roads) sell…. at a bit of a discount… but if you look at what they paid and the zero investment they subsequently put into it…. they did well.

Every situation is different. That’s what “real estate is local” means. Go a few miles in either direction and their fate is different.

Will our ‘hood change? Probably. But it ain’t happened yet.

My sister is in a rehab hospital. Believe it or not, some shark contacted me and told me he had a buyer for her digs. $1.3M cash. In Floriduh.

Sorry, she still might need it.

I was recently looking at the population pyramids of USA, Canada and Australia, and how these pyramids include the gender-by-age difference by calling it Surplus.

Check it out if you think RE is driven by surplus female over 50, or Crypto by surplus male up to age 40.

Layoffs and recession will change everything. RE prices declines are set to accelerate soon.

Up to this point, nobody had to sell. Going forward, they will.

Many of the lost tech jobs were held by H1Bs who must return home if they can’t get another job quickly. These people are heavily invested in real estate in tech centers. When they can’t find their next job and can’t sell at a profit, watch out. I’d be looking at San Francisco and Austin for signs of H1Bs walking away from houses.

Interesting hypothesis which should be subjected, at least the first three questions asked of a new hypothesis:

1) Are there any statistical data available that support your hypothesis.

2) Have there been any peer reviewed papers published that would support your hypothesis.

3) Please describe, in detail, your potential financial gain that would accrue to you as a result of certification by this committee.

I don’t think those locals will collapse in the “hair on fire” manner you suggest. They are more likely to decline in a more orderly fashion. After all, we are ladies and gentlemen.

I sincerely doubt that the chaos you suggest is likely. I could be wrong.

dang

I know of large tech employers in Austin who are firing all contractors and also large numbers of staffers in India. The staffers in India are a lot cheaper than H1Bs located on site in the states, so it’s a no brainer those H1B contracts will not be renewed.

I was in Austin recently and saw the for sale signs which were non existent last year. While many of those houses are priced at or above last year’s prices, many are actually in the 300-400K range, something which hasn’t been the case for a few years. Check out Zillow.

David Eby new premier of British Columbia, sworn in today. Former housing minister, he’s witnessed an enormous bull market.

Wolf – I saw couple of days ago Daly and Brainard mention something to the effect that the FFR rate increase will slow down and it may be much smaller going forward.

But then yesterday I saw a article about Bullard saying the FFR rates higher range needs to go to 7% to tame inflation (and I am guessing even higher mortgage rates ~10%). Do you think there is any merit to it? And will this speed up the price declines in housing market?

Slowing down the rate increases will just prolong the inflation fight.

They both said hikes may slow from 75 to 50 but keep coming until “sufficiently restrictive.” Williams and Waller said the same thing. It only takes 2 x 50 to get to 5% from here. The key for the Fed — they all said that — is the endpoint, and the projected endpoint is now much higher than projected a few months ago. From what they said, it sounded like 5.5% as an endpoint. We’re going to get the next Fed projection in mid-December, and you will see that the projected endpoint will be higher than they had projected the end point to be in September. And they will project to hold it at the endpoint for longer. Both Daly and Brainard and everyone else is now on the same page on this. Bullard too. His range was 5%-7%. Daly and Brainard sounded like 5.5%. This is a moving target, and it’s moving higher every month.

Wolf

I have to disagree.

Adjusted for the real inflation it ain’t moving higher every month. It’s just following inflation upward a few points behind it. William Miller, the Fed chief under Carter, (golf cart manager and entrepreneur), tried this in the 1970s. It didn’t work then, and it won’t work now.

Well, what I heard Bullard say was that the Federal Reserve Bank of Saint Louis, a lovely place, modeled the financial response to an ascending ladder of interest rates. The multiple, independent studies indicated that inflation will only decline when the FFR is above the current rate of inflation.

He gave a nod to Stanford prof John Taylor who proposed a similar argument for the necessity to have a non-discretionary policy that automatically set the FFR at a minimum level above the rate of inflation.

We fools assume that an economic plan is a desirable commodity, without realizing it is a game plan.

Developed during a stimulating thanksgiving dinner party of relatives. Larry Summers is a close relative of our favorite whacky Uncle Milty.

Economics may be the most dangerous impediment to equality.

Historically, only stopped by a world war. The architects of disaster presenting themselves as a solution.

Starting to see quite a few homes for sale, available fully furnished. Several with bunkbeds and pool tables, which makes me think that some of the AirBNB crowd are exiting their oversaturated markets.

All of this real estate talk gets me thinking about credit ratings. Specifically: do we believe them based on what we know about consumer behavior? During the pandemic, credit ratings soared due to a combination of government relief and forced consumer savings. Do we really believe a 650 score consumer has suddenly developed the fiscal conservatism of a 750 score consumer – just because they weren’t able to go on a cruise for a year? The credit score mix of new mortgages looks wonky to me – because I don’t think we change consumer behavior so easily, or so quickly. Certainly we have blocked many of the excesses of the last real estate bubble, and have gone back to robust income verification, etc. But what if all the consumers who saw a 100 point pop in their scores during 2020, go back to their profligate ways? Can we assume higher default rates than what the numbers would otherwise suggest based solely on credit scores? Particularly if home equity takes a hit?

You describe one factor.

A bigger one for most individuals is that their supposed creditworthiness is entirely contingent upon an artificial economy and an asset mania. That’s why they have a job, their job pays the current and prior compensation, and it’s the source of most of their wealth.

The biggest lesson of the GFC wasn’t the supposed consequence of low lending standards (these have “sucked” for most of my adult life back to the 80’s), but what happens when credit and debt stop increasing during “risk off”.

All it took was a minor decline in outstanding debt and the whole financial system nearly collapsed.

A bigger version of “risk off” is in store and probably not that far off.

One wonders how the Fed will respond to a risk-off shock in the presence of persistent inflation. I see weakness in many asset classes, but the financial markets seem willing to battle the Fed to the end…

Yeah, I’ve wondered how the financial markets have demonstrated such remarkable stability within the same envelope of dark predictions that we find ourselves. I come to the same conclusion the Fed is telegraphing;

that there is still far too much liquidity by any but the most radical theories of monetary policy. The financial markets are being buoyed by the trillions of dollars of excess bank reserves that can be deployed to bolster prices when advantageous.

It makes the market refractory to the normal signals that are supposed to drive the market up or down according to a computer bidding process.

The QE Reserves are still relevant for at least two more years.

My first memory about credit ratings was, ” If you have too worry about credit ratings your trying to borrow too much. How naive I was with my engineering degree, less than 3 billion people on the planet, a white, union family, what’s the problem.

Credit ratings are based on ones ability to repay short and long term loans based on a number of criteria including income, educational level, and other things.

I’m with Wolf.

If I may assert a premeditated statement of apology if I wrongly thought you may have indicated or said outright, you felt strongly that there are many buyers when the price is right.

I sometimes think my relationship with the economy is like marrying a beautiful woman.

Complicated, irresistible, and dangerous.

@dang – you forgot to include very expensive.

See Steve Keene and the second derivative of interest rate change.

Residential real estate prices increase more rapidly than they decline because the entire political-economic housing sector is financially incentivized for this dynamic. .Gov gets more in taxes for a more expensive house, the seller gets more $, the real estate pimp gets more commission, the bankster’s loan books look bigger/healthier, so their bonus prospects look LARGER. It is the same reason why the entire policial-economic system is rigged for price inflation – targeting 2% nominally. It’s the ‘life keeps getting better every day’ narrative. It complements the debt-based fractional-reserve bankster system.