Housing construction has split in two.

By Wolf Richter for WOLF STREET.

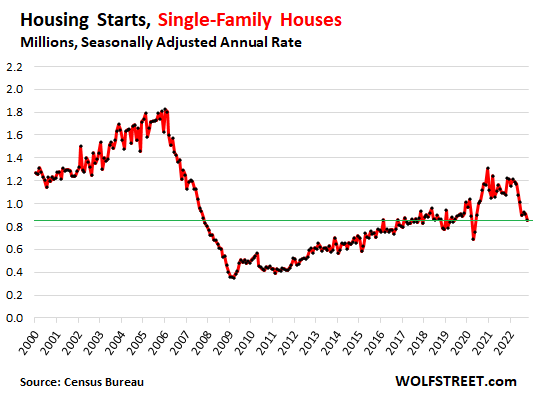

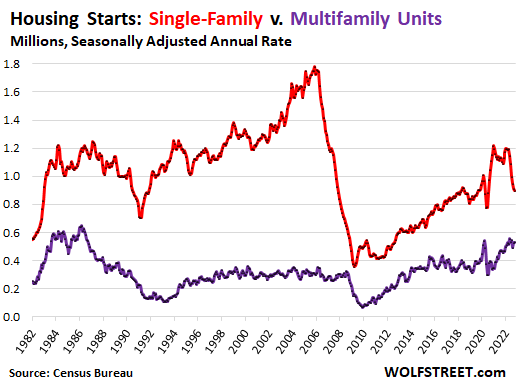

Construction starts of single-family houses have been dropping all year as homebuilders are trying to unload a huge pile of inventory while sales have plunged and foot traffic to view new properties has collapsed. In October, single-family construction starts dropped further.

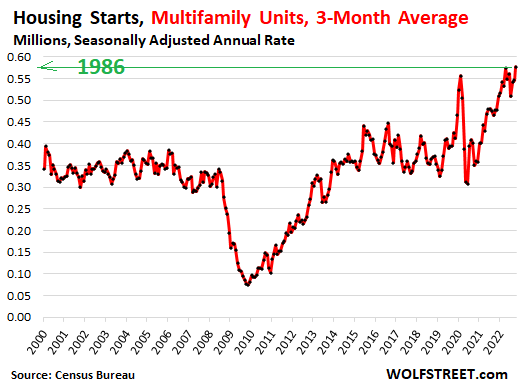

Construction starts of multifamily projects – condo and apartment buildings – continue at the highest levels since the multifamily boom in the 1980s.

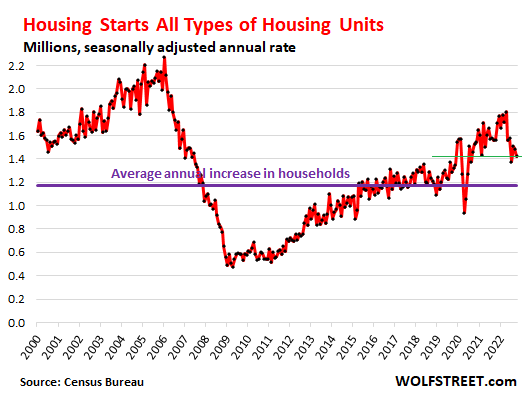

Combined, construction starts of all types of privately owned housing units fell by 4.2% in October from September, and by 8.8% year-over-year, to a seasonally adjusted annual rate (SAAR) of 1.42 million housing units, according to the Census Bureau today.

During the period from 2000 through 2020, the number of households increased by 1.17 million per year on average, topped off by a decline in 2020 (purple line). It sheds some light on the so-called “housing shortage” and “underbuilding.” But this equation doesn’t take into account housing units that are being used for non-housing purposes, such as vacant properties that are held off the market by their owners to ride up the price-spike all the way; and such as housing units being used as short-term vacation rentals.

The plunge in single-family construction:

Construction starts of single-family houses plunged by 6.1% in October from September, and by 21% from a year ago, to a seasonally adjusted annual rate of 855,000 houses. Since the free-money-fueled peak in December 2020, construction starts of single-family houses have plunged by 35%.

But even the peak remains far below the Housing Bubble 1 peak in 2005, infamous for rampant overbuilding and the subsequent collapse of the industry.

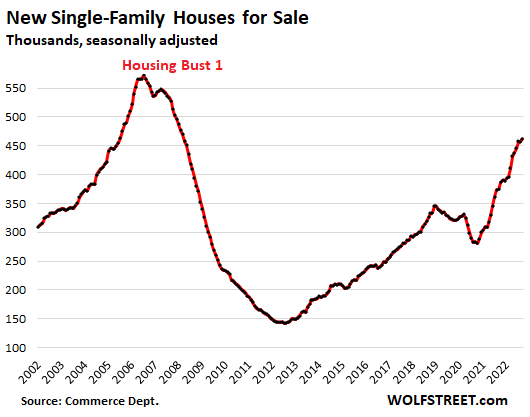

Inventories of houses in various stages of construction have been piling up in massive numbers and in September, at 462,000 properties, reached the highest level since early 2008, according to separate data from the Census Bureau released last month. Mortgage rates have returned to the normal-ish levels before QE, but house prices have not, and that’s a toxic mix, and it killed demand.

The boom in multifamily construction.

Construction starts of multifamily buildings of five or more units, such as condo and apartment buildings, dipped just a tad in October from September, but surged by 17.3% from a year ago, to a seasonally adjusted annual rate of 556,000 units.

In many densely populated cities and urban cores, multifamily is just about the only type of housing that is getting built, such as in San Francisco, Boston, Manhattan, etc., while single-family construction takes place further away from urban cores.

These initial estimates of multifamily construction starts are volatile from month to month. To show the long-term trends, I converted the monthly data into three-month moving averages (3MMA), which rose to the highest level since 1986.

The current rate of construction starts is up by over 50% from the middle of the range in 2000-2008; and it’s up around 40% from the middle of the range in 2015 through 2019:

Over the four-decade horizon, we can see the booms and busts in construction of single-family houses (red line in the chart below) and multifamily units (green line in the chart below). In the 1980s, there was a giant boom overall in construction. Construction starts of multifamily units tripled over the period, leading to a long downturn afterwards, while single-family construction continued to ramp up to finally blow the top off in 2005.

Lead times are a lot longer for multifamily projects and are measured in years for big towers. Once a project gets rolling, it’ll generally keep rolling. But homebuilders can cut their construction plans fairly quickly. And that too is visible in the chart: During Housing Bust 1, single-family construction started declining in early 2006. But multifamily didn’t drop until the Lehman bankruptcy blew a financial-system fuse, which put funding for big projects in doubt, and everything came to a halt:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I am about to pivot!!! $5 bucks straight from my pocket to anyone who buys a house right now! For reals!

JP, I appreciate the $5 offer, but I’m concerned about your depreciating dollar. Can you pay it in Bitcoin instead? My account is at FTX. Thanks!

$5 or $1,000,000 FTX!!! Your choice!

J-Pow, why $5 only? Why not print $5 trillions and hand it to each of us so that we can each buy 5 million homes?

Aren’t you the all powerful Fed that Noone can fight?

Deep thinker. Thank you for your contributions.

“Multifamily Construction at 36-Year High”

The raging mania continues. Powellbucks have proven to be goddamn stubborn (big shock). Wall St. is still partying, the roads are packed, restaurants have waiting lists, car lots are empty, mortgage rates are plummeting (with buyers rushing back in if you listen to the media chuckleheads), retail sales are surprising to the upside, etc. Meanwhile, those with the least are getting destroyed. Enjoy.

2007 2.0

but this one will be worse.

It’s already worst, thanks to the inflation outpacing wages. And it has not even started.

I know several people who jumped in to buy a house as rates went down a bit. I also noticed several house with asking price $1.5M+ which have been sitting on market for a while now suddenly lot of them went contingent in last week (if this was a coincidence then it is a crazy one).

People are acting irrationally.

Only high unemployment is the cure.

Reducing the money supply big time is another cure that isn’t happening fast enough.

The Fed TGA account is dipping and sending liquidity into the markets. I expect the Treasury to flood the markets with money until year end. This ensures all the day traders at the Fed will make their profit targets! (the real reason for the Fed)

Would not be shocked by 4500 on the S&P. Bullard pushing for 7% interest rates is pathetic. Everyone knows the Fed will cave.

Danno:

Yes. Raising taxes on the limousine class fights inflation.

Not a huge difference between 6.6% and 7.1% mortgages.

I’m not seeing anyone tempted by this dip.

Why rated are suddenly down?

Rates are suddenly up, then they’re suddenly down, then they’re suddenly up, then they’re suddenly down… That’s what markets do. Same as your stocks. But beyond these ups and downs, there are longer-term trends that are not hard to miss: up for rates, down for stocks.

Can’t say “nobody buys a house in November/December” but it always is the slow season

First time home buyers are stuck and those moving to different bigger house tend to do that in spring do works out best with kids (and thecreal move in summer)

And for them it is just a mortgage to pay the difference. A mortgage that will be refi-ed once the rates come down again.

And if the rates do not come down, it means the inflation is still high and real value of the principal is coming down

But that is only for those that can pony up a good equity % in the new house to qualify. So we are talking people that already have a house (and use a bridge loan as well) and first-time buyers are stuck

CG, if the behavior is irrational, and I agree that it is, then this is indicative of some final death throws by the latest housing bubble. Like all manias, it will end by virtue of its own stupidity.

I saw lowest priced condo in Alameda, CA go from 700K to 480K (after remodel). Pretty significant drop. People may be jumping on unique “good deals”. HOA fee was very steep still. I could rent it for half the price of owning.

Maybe those still with some resources are figuring that $1.5 million house is going to look like a cheapie in year. Sort of like buying on the price inflation upswing. ? I personally don’t like to gamble like that and my real estate is bought for desired location and fitness of purpose. If it’s value goes up, or goes down, doesn’t really impact either purpose. Still enjoy a nice place that keeps me out of the weather so to speak.

And homebuilder profits are still high & mighty. When you can build 3-4 more houses per acre that share walls, go up instead of out and don’t have yards but still have high prices, then builders live high on the hog.

The ONLY way this gets sorted out is through a real housing recession that leads to at least 30% declines in home prices. A piddly 10-15% reduction won’t cut it. As the economy softens, 30YFRM are likely to wan. Once they reach 5% with a modest 10% drop in price, housing WILL reignite to some extent, assuming the recession is shallow.

It’s always been about housing. The only question is will Uncle Sam step in with rent & mortgage relief again if unemployment moves up towards 5%.

15% price drop? Yeah that takes us all the way back to 2021 when houses were hmmmm ……. Cheap?!?!

Oh no a 15 percent haircut on assets that increased by 39% over the past two years. It’s a crash I tell you!!! JPow save us!!

Depth,

““Multifamily Construction at 36-Year High”…”The raging mania continues.”

Did you expect the mania in multifamily projects — projects that have no trouble at all renting up — that take 2-3 years to plan and get approved, and involve lots of investors to coordinate and tens of millions to build, to just freeze up? Check back in 2-3 years. Sheesh.

BTW, plenty of MF and related deals that haven’t closed are getting repriced. Construction costs are under pressure as investors see their expected IRRs shrink. So settle down.

“So settle down.”

GFY. If you don’t like what I post, ignore it. Got it? Good.

DC, I usually do ignore your posts, which are invariably pointlessly vitriolic non sequitur rants. But sometimes your posts distract others from paying attention to the *actual point* of Wolf’s thread. Now see what I wrote in my post. Actual useful information on how multifamily development works, hopefully countering your b.s. and getting the thread back on track….

Anyone ever experienced a beautiful day before a forecast terrible storm a few days away. Mentally it’s hard to have an urgency about preparation when your senses are telling you everything is ok.

Fed is turning the screws to the economy hard, but the consequences are still out there aways. We shouldn’t wait til average consumer stops spending to get ourselves in a good place. We had a decade of free money. Might be a decade to mop up the bad policy.

All the retirees that I know, have increased their rate of spending! They are in the right position, and don’t respect the dollar’s power in the future. They are not, I repeat, not haphazardly getting into debt. The One, Two, Step works.

New Privately-Owned Housing Units Authorized but Not Started: Total Units (FRED Monthly Data): 290,000 units. This is the highest number since 1974.

New Privately-Owned Housing Units Under Construction (October): Total Units: 1.72 million units. This is the highest number in this series since the series began in 1970 (FRED – Federal Reserve Economic Data, Federal Reserve Bank of St. Louis).

Are there labor and parts shortages?

The rental vacancy rate (FRED) is 6%. In 2007 the rental vacancy rate was 10%.

“Not started” because homebuilders have pulled back from starting construction. They’ve all said that in their earnings calls. They don’t want to sit on 200,000+ competed spec homes in this market with no buyers. The financial commitments could sink them.

Plenty of buyers…. if the price is right. Same for used car market.

Yes, if the price is right. That’s the crux. “Right” means low enough.

Here in flyover land, the prices are still not right. SFHs are sitting on the market for longer periods, and price reductions are more common. But even the reduced prices continue to be highly inflated.

The standoff between buyers and sellers that Wolf described in an earlier article is evident in this area. The agents and sellers just aren’t giving up the pricing disconnection from economic reality that resulted from Fed overstimulation. It may take large scale and widespread layoffs before the “party is over” message gets through.

Cold in the Midwest, I just got a “newsletter” from a R.E. agent who had a house I looked at quite a while back. Basically it said reductions are coming. Of course, reductions in selling prices have been happening for quite some time.. She is trying to prepare sellers to lower prices. This is a first. Aside from my (actual) friends who are RE agents, this is the first time I’ve seen agents putting “news” out to try to get sellers to reduce prices. Interesting..

I’ve been saying for a while that SFR’s won’t take the same beating as multifamily. There simply aren’t enough houses made or being made (the kind leave it to beaver grew up in), and I’m referring primarily to California. Who wants to be stuck in a box the next time chairman whoever screams lockdown? People want houses, especially couples with a bunch of snot nosed rug rats running around. The market will correct but it will be disproportionate.

Please…. At least look at the title.

You got it BACKWARDS. It’s the SFR that IS TAKING THE BEATING and the multifamily is still riding high.

Wolf, The Bob is referring to the future, that MF prices will get whacked harder than SFR.

The Bob, you’re likely very wrong. Multi-fam are large investor owned, enjoying rents for years/decades/sometimes forever. They’re often traded via 1031 at their convenient leisure. Of course there are forced sellers at times. Of course there are motivated sellers at times. But nothing like SFRs. MF owners don’t lose their jobs, get transferred, blow their mortgage payments at the craps table, get divorced, etc.

In the last crash, which dropped more, SFR or MF? I think SFR dropped by 2-3x as much as MF.

You’re right in my reasoning as it relates to the future. There aren’t enough being built and many of those already built are being converted to duplexes via ADU’s or more with sb9 and 10. It’s a matter of time. People want houses and they’ll be in high demand as multifamily is all that’s being built.

As I’ve said many a time in the past, though, I could be wrong.

Reply to Bob below:

“People want houses and they’ll be in high demand as multifamily is all that’s being built.”

I dont want the homes they build today. Or have built the last decade.

Unlike most posters here my income is quite modest. I dont want to and

won’t buy a 2500 ft² home. Not even a 1500 ft² home.

Dont want to heat, cool, maintain all the extra space. Dont want to pay an extra $500 to $1200 per month to rent a house.

I’m in a 570 ft² apartment that is perfect size for me.

Single people exist as do childless couples.

I owned a 1650 ft² home for 10 years in the 80s and 90s. I dont miss it.

Honestly. Its not that I love my apartment either, its just the best solution for me.

Agree with Randy on the subject of houses too big and costly to maintain pushing folks into rentals of appropriate size.

We, in this case the family we, got tired of chores of the never ending kind, and went to a SFR on a city lot with less than 25% of the maintenance time and efforts…

Suspect many folks will be doing either the smaller house or the apartment of appropriate size as soon as this crazy stimulus situation and other funny money is gone.

So give it a few years, likely mid decade for the opportunities IMHO.

Also, Gattopardo, thank you for seeing my point of view. I tend to say things here and get flamed pretty quickly for having a differing opinion or alternative viewpoint.

I’m in Multifamily and I agree with Bob. Anyone who has bought or built multi in the past 18 months is underwater right now. Give this a year and all hell is going to break loose. Recession will mean job losses on top of an already weakening apartment market. There are no exits at the moment with rates where they are. The herd is going to be slaughtered. There is a very high percentage of multi loans that are short term floating rate.

Bunch of my friends bought sfr last year citing that come what may sfr prices won’t go down.

Now in my hood sfrs have come down in price

People who has stake in sfrs would say that sfrs won’t be impacted.

This time it is worse than HB1.

I didn’t say that sfr prices won’t go down, just saying that when it all goes to hell folks still want a house with a picket fence and a swing in the tree and not a cube in a building. I can’t speak to every city in California but here in San Diego you can’t go more than 500 feet before tripping over a three stack of concrete with a 5 stack of wood on top, all housing of some sort, whether it be apartments, condos, subsidized, rehab, homeless, you name it. No new single family of any consequence is being built here. I suspect most other cities in this state are the same.

In my hood sfrs are taking a beating.

If there are more sfrs it pressures the sfrs as well.

My neighborhood is down 10 percent plus from peak. Never saw such a fast drop.

@Jon,

What region of the USA?

San Diego CA.

San Diego went up huge the last few years. 10 percent drop is like nothing. Especially with current rates. Total monthly payments are up almost double in some areas now in a matter of two years.

Let the good times roll.

I see no stress out there.

My favorite steak house doubled their price, now it’s $50 and you pay extra for any sides. Yet the place it’s full, can’t book a spot, help wanted everywhere.

People are being lied about inflation, it’s much more than official figures.

Let’s see how long it will last.

People are being lied but it’s not really impacting people’s lives in any way.

Look at the spending. There is no slow down.

America media needs more distribution charts.

Simple distribution charts.

“it’s not really impacting people’s lives in any way.”

Begs the question “which people ?”.

Of course (!) this inflation is not affecting the rich. Or the upper middle class. Nor many middle class if they are confident of their future.

But surely it is affecting many poor families even some lower middle class.

Its amazing how the US media in general avoids stats altogether or just provides the most basic ones… averages and medians.

Subclasses of populations can, of course, believe and act differently than the population as a whole, on average.

Somehow that conveniently is overlooked by many authors in this country.

There’s something called Simpson’s Paradox. While I’m no statistician I bring it up because its the sort of thing that only comes to light with more than simple analysis.

Not that this is an example of Simpson’s Paradox (see the web, plenty examples) but while it may appear Americans prefer new homes that are 2500 ft² and larger… after all that’s what they typically buy… many would be quite pleased to buy a much smaller home if only 1) they built them, 2) they were affordable.

Appearances can be deceiving.

Inflation is affecting people’s lives, some more than others. I feel wierd stating the obvious.

Anectdotal, but every time I try to seek out something about economy of people in the USA I get statistics sorted by colour.

Not by wage, education, net worth or any other economic size. I wonder if that is by purpose to conceal that class matters.

Honestly, I don’t really see people tightening their belt.

I hear you but when I look around: restaurants are packed, cara selling above msrp, hotels booked, airlines booked etc.

‘I wonder if that is by purpose to conceal that class matters.’

Reply to Sams. Ding ding We have a winner. Income and net worth assigned and sorted stats purposely do not exist in USofA.

by sex/sex orientation/left handed/right handed/color/ethnic origin/age/marital status/ on and on.

But not by either income or net worth. We can’t have a class war here, can we….Much better to divide into tiny groups jealous of each other, than by class: upper and lower.

One anecdote. The wealthy were never impacted by inflation on the same level as the rest of society. Somehow, I don’t think people making less than median wage are frequenting 50 dollar steak houses.

Yeah, I keep reading about how the Sizzler’s all booked up & running outta steaks — ON A TUESDAY AT THAT.

Maybe I’m just not looking hard enough or maybe (definitely?) I just run with a low-lived buncha scum, but none in my circle are running amok in silk shirts or ordering designer lobster stuffed with another lobster or drinking Chivas from ice luges or partaking of whatever other big jazz-handsy spendy doings everyone else seems to be witnessing. There is no big discernible swing from the status quo to conspicuous consumption. People are the same idiots with their money as they always were.

I get concerned that there is a missing piece in all the analyses of the data. “Time” and its impact on money and the economy.

For example, the Gov’t has pumped about 6 triliion into the money supply since early 2020 give or take. All of it couldn’t have been instantly absorbed. (Although FTX has “absorbed” a lot. Sorry, couldn’t resist). How much spent and where, and how much is left to be spent on what and when.

Savings shot up, now coming way down, credit cards tanked then shot up again…people exited the work force, 5 million or so didn’t come back,.. inflation constantly eating away at higher and higher rungs of the income ladder. Seems like there are still a LOT of things up in the air that have to come back to earth so to speak.

It is Wolf who is expertly charting the journey, there is no actual destination.

And just like that, the Great Reset was upon us.

Never Fear the Banks are here. First homebuyers keep wishing that nightmare will end.

J.P. Morgan and Haven will be looking at buying 50 to 200 homes per transaction, with floor plans ranging between 1,500 and 2,500 square feet. Most of the houses will be two to four bedrooms with two-car garages in Atlanta, Ga. (Net spend over $1billion dollars).

Other markets the two firms plan to target include Nashville, Knoxville, Chattanooga, Charlotte, Phoenix and Las Vegas. The JV will use the funds to double what is already in Haven’s current portfolio of 3,500 homes across 35 developments, according to a spokesperson.

JP Morgan is planning on buying rental homes, built as rental homes, from home builders. Build to rent is the only thing that is moving for homebuilders.

Wolf,

will you write about Masayoshi Son of SoftBank? Was there ever a worst investor? His latest loss was in FTX apparently. The guy just can’t get any break.

Hi had a few HUGE wins, and his entire investing career is founded them: he was early investor in Alibaba (he just sold that stake for something like a $20 billion gain) and an early investor in Yahoo Japan. I think there were a couple of others. But those two were gigantic wins.

Anecdotally I was reading on Twitter that corporate buyers were backing away from built to rent in the Phoenix area. But it was several weeks ago so I can’t remember the details. The opinion, I’ll say opinion bc I don’t know if it’s fact, of some is that build to rent model only works when home prices are appreciating. Maybe that was just the case for the corporate buyers in this one case I recall.

Yes, some of the corporate buyers (publicly traded REITs) of built to rent are pulling back and have said so in their earnings calls. But the JP Morgan deal is a fund they’re setting up to buy in the future. So they may not be buyers now either. Also, there are always investors who disagree, one is a seller, the other a buyer, which is what makes a market.

“JP Morgan is planning on buying rental homes”

ought to be illegal ………………

Why? Landlord sells a portfolio of rental homes (usually occupied with tenants) to another landlord. What’s wrong with that?

Ask the tenants

@ Wolf –

Because JP Morgan is a bank with FDIC insurance and a FED to backstop them. And a corporate charter giving them limitless life and limited liability protections for their stockholders.

Repealing Glass Steagal was a travesty. Allowing corporations without tight charters is detrimental to individuals. Fomenting concentrated wealth and power destroys individualism and freedom of the common person. Allowing corporate institutions to compete with citizens for the purpose of making those citizens renters or debt slaves is government sponsored feudalism. or facism?

(Why do corporate investors get to use depreciation when they rent out a house, but not an a buyer occupant?)

You know it’s sick that JP Morgan could buy houses and get into the rental business. You could add many additional reasons to the ones I’ve listed. I mean the very thought ………. These bankster bastards get to lobby for lending laws (interest right offs, etc.) to encourage debt slavery, then get to pump and dump markets with government agency and FED cooperation, then get bailed out if the going gets rough, then get to pursue the property accumulation and rental business, with the advantage of being a Corporation against common citizens. That’s almost as stupid as letting non citizens compete with citizens in buying houses.

I agree that first watering down and then repealing Glass-Steagal was a travesty (tragedy?).

But you’re going overboard. This is a FUND that is jointly owned by a FUND of JPM and another company. FDIC insurance doesn’t apply. If that fund blows up, it blows up. No Fed intervention, no FDIC intervention, no nothing.

It’s like saying a bond mutual fund or a Treasury money market fund sold by JPM to investors should be illegal.

@ Wolf-

“It’s like saying a bond mutual fund or a Treasury money market fund sold by JPM to investors should be illegal.”

———————————————–

There is another issue. It probably should be illegal. JPM is subsidized by FDIC insurance, the FED, governments bailouts, government sponsored tax incentives for investors to funnel money to packaged funds, Government allowed corporate protections and an overall government and FED created “cover of security.”

Didn’t Glass Steagal keep banks out of the mutual fund packaging business?

A lot of big banks and institutions made big mistakes.

Just don’t think blindly thsy they are smart.

I have heard from a fairly reliable source that 50 percent of consumption in USA is from the wealthy (top 10 percent or so) hence the talked about Fed wealth effect. Also the equity markets have risen 40 percent the last 36 months or so and plenty of wealth is felt. Not to mention cash out refi etc for housing increases. So until asset prices and stock equity prices drop significantly ie a flat stock market for 36 months I don’t think we will see PCE drop much. The spx would need to come down to 2600 from the current 3900 to get a reasonable PE of 12. Probably the 4th inning of a long baseball game. Oil prices will remain stubbornly high as long as Saudi supports price with production cuts.

P/E is one of the worst measures of value. Earnings are also absurdly inflated due to the fake economy and asset mania.

Try near 1200 to get back to “fair value”.

“The spx would need to come down to 2600 from the current 3900 to get a reasonable PE of 12. Probably the 4th inning of a long baseball game.”

The history of the most recent super bubbles support your statement. Historically, the Earnings denominator declined and at the bottom many enterprises were selling at a P/E in single digits on depressed earnings.

Those who fail to study history are doomed to repeat it.

Was just doing that. (getting kinda sick of that old saw, too).

Hope Wolf lets me post a 2400 year old play. Plot is just a real short read and funny as hell. And good example of repeating history. Sounds like South Park episode to me.

file:///Users/network/Desktop/The%20Clouds%20Aristophanes.webarchive

And thanks for good WS update on current situation, Can’t say I didn’t expect it, though.

Sorry, posted my own ref copy, but just look up The Clouds by Aristophanes. I SWEAR it is short read and a good laugh.

Not a recommendation just observation:

the forward looking and trailing P/E of one international mutual fund is just below 10.

The company that offers it is from Wolfs current home and been around since the 1930s.

I imagine its not the exception.

While I can appreciate everyone wanting to realize the American dream of owning their own single family home and spending 2 hours or more in heavy traffic every day to realize it, endless suburbs of car dependent single family homes are clearly not the answer.

The USA needs far more multifamily housing and far less single family housing and zoning changes to encourage the former while discouraging the latter. Furthermore, it’s the city centers paying the lions share to property taxes to help subsidize all that car dependent suburbia.

Or a smaller population. No population can increase indefinitely.

That’s the other solution to the problem you describe.

Yep…imagine California with the population of 1940.

…or even 1960… (pre-Interstate highway build out…).

May we all find a better day.

The problem with your solution is that, believe it or not, PEOPLE get to make their own choices as to where and how they want to live…

“PEOPLE get to make their own choices as to where and how they want to live”.

We the people are given options…government and companies decide what these options are. At best we get to select from these choices if we have sufficient $; at worse we don’t.

Either way the people don’t decide what kind of cars or houses should be built.

Car manufacturers and homebuilders do.

Consumers merely provide positive or negative feedback w.r.t. these options.

I consider this a shortcoming in our society.

“Freedom” in this country is oversold.

Car manufacturers no longer sell things like the Edsel. Others are long out of business for the same “consumer choice” reasons.

Home builders could push a square box divided equally into bedrooms, living area and kitchen, nothing but plain siding. That would be the lowest input cost for them. Yet, look at homes that are actually built and sold. It is what the consumer will buy when they are able.

Try to open a business and disregard customer’s wishes. It won’t be around long.

Randy, YEP!

CGB….you gotta be kidding me……what are mobile, prefab, “tiny” and kit houses? Even the 500sq ft 3 story hotel style apt I’m in? (5ft hallways). What a lame “rebuttal!”

“Freedom is an illusion created by those with power (&$$s) for those that don’t”

-The Merovingian in The Matrix

In response to CreditGB’s response to my previous post:

“Try to open a business and disregard customer’s wishes. It won’t be around long.”

…but I didn’t suggest otherwise.

That aside…

Companies can make different errors w.r.t societal desires… 2 obvious ones:

1. They don’t provide the products, services society wants (in a particular industry). For various reasons noone fills the void. Those making a good profit from the status quo may stymie new entrants that might fill the void.

2. They force consumers to buy products they’d rather not buy. Many consumers like 2500 to 4000 ft² homes.

Some undoubtedly are pleased with a tiny home. But my guess is that some people refused to buy a home they felt was overdone… too big, too pricey for their needs. And, they felt the tiny home was just too small. They continued to rent.

Other people did buy a home that was bigger than they desired (or smaller, tiny home) but wished they could have bought a new home, say, 600 to 1200 ft² in size. There are undoubtedly some builders that built new homes in that size range but I never see them.

Clearly problems 1 and 2 (above) are related. The second problem can be, perhaps usually is, a direct result of #1.

My main point though is: what DO consumers want in housing and how could their desires necessarily get reflected in what builders build.

Builders build what works out best for them… many consumers are pleased with what they offer but some consumers, maybe large numbers of them, perceive holes in the offerings.

They have no recourse to get the businesses to provide what they want…unless they can start a business to provide the product/service.

I rent in one of your ‘awesome’ townhome type places your advocating we need more of… it’s great.

I pay double what I paid for my last house to live sandwiched between a couple of shut-in girlfriends and weed 24/7 smokers who had 3 cop cars outside just yesterday. It’s supposedly a desirable community.

Lease it up in 5-months. My plan is to burn as much gasoline as I need helping Exxon, Shell, and the rest to record profits (stock tip, everyone) as I burn up and down the highway from long distances to live far, far away from here.

I’ll be in the 1981 dilapidated double-wide on 5 acres but not here in the shadow of the evil Mouse.

Lol. That sounds exactly like our previous condo townhouse. I got told by the neighbor that the weed smoking is legal in this state. HOA board wouldn’t enforce nuisance rules either. Sold the townhouse and bought a new build in 55+ community, best move ever. No riff raff here.

Your point is very valid and significant.

Apartments need better soundproofing and bad tenants need to be dealt with.

“Code enforcement ” in the city i live says tenants need to use an attorney to deal with such problems (whether with other tenants or management shortcomings). This gives government a bad name.

Regulations not being enforced is just as problematic as over enforcement or bad regulations in the first place.

That said, I’ve lived in 8 apartments (or equivalent) in various states. Most neighbors have been pretty decent but there have been exceptions.

Also homes can have problems. The home I grew up in in a very middle class neighborhood got broken into. Many items stolen including guitar and amp. House I owned decades later also broken into… it too was in a very middle class neighborhood.

You go ahead and enjoy your multifamily utopia. I’ve never lived in an apartment in my life, or shared a common wall, and I never will. That’s the stuff of nightmares.

Thank god we all like different things or else we’d all try to live in the same place :-]

Buying a house at these prices/interest rates are the stuff of nightmares.

DC

I agree

Ms Swamp’s hairdresser lives in a townhouse with a shared wall with her neighbor. The tenant/owner moved into the townhouse and started cooking Indian food for her whole extended family. They cook all day and all night, and the fumes from the hot food go right through the wall. I like Indian food, but who would want to put up with this 24/7???

F that. Just stop all forms of immigration for a few decades.

Heck no. Take a look at the priorities of your masters. I guarantee that “Cheap labor” is way above “The ability to house the proles”

K-spot on. Can recall a (possibly) Thos. Nast cartoon circa 1870’s – ’90’s referencing the same issue in the Gilded Age. Am beginning to get the impression that (similar to that period’s) ‘reformist’ sentiments are coalescing in our younger generations-a bumpy road ahead, as it was then, with more and more asking: ‘What Is To Be Done?’ (…among other titles…).

may we all find a better day

I think many people agree, until they have a child. It is much easier for a child to play outside in your yard, than it is to take them to the park. With the right window placement, parents can watch a child on his swing set or playing with his dog, and still multitask. Remote work should make the suburbs more livable and lessen traffic. High density housing is the dream of urban planners, not most Americans, and certainly not those with children.

Maybe this means that the dream of the American Dream is finally dying.

LK-

On the contrary, our vibrant free market system allows for the best upward mobility on the planet as intelligent, hard working risk takers redeploy assets and capital. This web site is dedicated to disseminating the truth, uncovering the underreported, and shepherding understanding and interpretation with a tolerance for dissent and an intolerance for untruths and misinformation. Wolf Richter has earned our respect and deserves our support. The contributors here are an eclectic group of mostly sincere, usually virtuous and often entertaining individuals to help you succeed. This is the heart of the American Dream.

Agree with you HH, far damn shore, and in SO many ways:

My late 70s life as well as my sibs is MUCH better than our parents and their who partied through the Great Depression on trust funds OR sweat depending on which side.

Our mid 30s-early 50s kids are ALSO much better off by virtue of hard work.

IMHO, ”THE” American Dream is alive and well for those whose parents continue to choose to ”raise their kids” instead of ”letting them grow up.”

Why else would half the people of the world WANT to come to USA any way they can, including through incredible hard ships???

I could be wrong but I would guess more people look to immigrate to Australia (and NZ), Canada, Scandinavian countries and perhaps a few others than the US. But its probably harder to get into those countries.

Just guessing.

OK. I think George Carlin put it better, but if I was comfortably successful in my twilight years, I’d probably believe that mythological BS too.

About a year ago, you never saw a for rent sign in my area, now they are all over the place, something is changing….. But that is not stopping the building of new apartments…. It will be interesting to see how fast rents start dropping.

Have rents ever dropped much?

In every recession…..

I see local townhomes listed for sale on redfin (available in early 2023), with list price going up on a weekly basis (instead of going down).

I was familiar with the area and its not far out of my regular drive, i decided to check that location out. As of now, it is a big lot, surrounded by a temporary fence. They at best moved some dirt to level the lot. I highly doubt it will be available in 2023, not to mention there is not even a model townhouse to physically see. If i was in a market for one, i would be seriously worried about giving them any money.

If that’s how they build multifamily properties around the country, then it is just another sham bubble.

I own a trucking company that transports cement to redi-mix plants. Concrete in my market averages $130/yd delivered. This price is double from two years ago. Concrete is the first to slow down and I have parked four trucks and laid off 4 drivers. The business expense of diesel, road use tax, maintenance, tires, insurance and equipment is crazy.

Two of my clients are delivering concrete to several multi-family

low rise apartment projects. All of the projects were designed in phases so that as demand softens, only a phase will be built and finished. All of these projects are shutting down being 1/3 to 1/2 built. Relentless construction cost increases are causing the shutdown. Demand for concrete from SF construction has died. SF uses a significant amount of concrete for foundation walls (basements), floors, driveways, sidewalks, curbs, etc.

All of my equipment is paid off, and I anticipate that by Spring of 23, all residential construction will be shut down in my market. Industrial and highway construction will still be ongoing, but this is not enough to take up the lack of concrete demand from SF construction

Not going to be fun times. At least this time around it feels good to be

debt free business/personal.

I remember the start of the GFC, and the talking heads saying that

the housing market & construction wouldn’t take the rest of the economy

down.

Will be no different this time around. I have friends in manufacturing.

Their orders are tanking. Back to traveling & visiting clients.

In Arizona we are seeing SF builders pulling way back, and MF and industrial developers walking from new deals. Lots of land sales falling on of escrow. No relief on concrete or general construction prices yet as there is much to be finished and some very large multi year projects, including the TSMC plant and Intel expansion. Right now a concrete delivery has to be scheduled 6 weeks out, and you take it when you can get it. Electrical service sections are still a 48 week lead time! For a small commercial project I have to order before the full construction drawings are even complete .

Huh, it’s still going strong on industrial projects. MF developers are trying to to get Scottsdale council to buy off on huge projects by enticing them with use of grey water and other water saving features. Obviously these projects haven’t broken ground yet and I’m astounded they would want to looking at the housing market. If someone can explain that to me I don’t understand.

TSMC is already planning on a $12B expansion of the chip fab when the first phase is still under construction. I can tell you that infrastructure costs are going up in some cases over 20% just in the last 6 months.

I’ve seen concrete quotes at $220/yd on some projects. Contractors are asking for whatever they want, which is normal, but in some cases they’re getting it bc everyone is so busy.

I found Fed’s Bullard research graph on Taylor interest rates a good visual. It shows how late Fed was to get off of zero and how Fed is still below what it’s going to take to kill inflation.

By being late I think they doomed us to a hard landing especially the housing market.

The good thing is as rates go up the gamblers/shysters/crooks are being exposed.

I think there is a good case for having a good balance sheet and investing in firms with a good balance sheet. When the Fed has to put the squeeze on the economy, they are not going to kill everything, just those that took on too much debt.

Great comment ! The Taylor Rule (interest rates should be 2% above the inflation rate) has withstood the test of time repeatedly. Some have even expressed an opinion that the Fed should be replace with the Tayor Rule.

1) Our economy is strong : single family and multi units start are below

the eighties. New single family houses for sale might make a new all

time high. The housing market liquidate itself.

2) The weekly Dow futures : Trading range #2 : Jan 13/27 2020,

29,362/ 28,105. // Trading range #3 : May 10 2021 h/lo, 35,000/ 33,200.

3) The Dow dropped from TR #3 to #2 and bounce back to #3.

4) But a line coming from Jan 22 2018 high to TR #2 is blocking it.

5) TR #1 Jan 22/ Feb 5 2018 is waiting for the Dow. If so, we don’t know, an uptrend channel from the 1974 and 1982 will meet yo mama p*ta Dow, for fun and entertainment only.

Median price still going up. Paging Mr. Powell.

Actually no. Today’s NAR median price fell for the fourth month in a row and is down 8.4% from the peak. It’s still up year over year, but only 6.6%, as each month the yoy gains shrivel.

Yeah, what we need now is a nationwide Proposition 19 for single family homes.

It’s kind of amazing how things have changed. My grandfather got married about 110 years ago. His family who was poor like everyone else helped him build his home without a mortgage and with hand tools. From then on it was pay as you go to add on, electrify and add indoor plumbing as times and life changed.

Now we have to finance granite countertops for the guest bathroom to be happy.

In the 50’s and 60’s 10, 15, and 20 yr mortgages were common. In the more rural areas, many people just borrowed enough to do the work they could not do themselves, and did as much of the work building their house as they could, with the help of friends and relatives. They grew up during the depression and avoided debt as much as possible. I remember most of our neighbors all had their homes paid for before their kids graduated high school.

I totally agree we are ridiculously spoiled these days. But debt has its benefits.

We mostly like to focus on the downsides, especially here on WS. Too much debt at the heart of a lot of society’s ills.

The benefit is that debt allows us mortals to own things earlier and enjoy them longer. It also creates demand for products and industries that otherwise would struggle to exist in a purely pay-as-you-go model. This system helps to create jobs whether we like it or not.

My grandfather, of very modest means, spent his whole life wanting a camper someday. And as a miserly child of the depression, would only pay cash for it. By the time he bought one, my grandmother was sick and he cared for her for nearly a decade. After her passing, he was too frail to use it himself. Still has never used it.

His camp ground is filled with financially irresponsible younger blue collar guys sleeping in $80,000 fifth-wheels. Who is the smart one? Maybe there is a balance somewhere in the middle? The clock only moves one direction.

There is a big difference between having possession of something, and owning it. A lot of people are going to learn that over the next 5 years…..

Those granite countertops in the guest bathroom receive government guaranteed financing. What’s next?…government guaranteed plastic surgery loans? Government guaranteed vacation loans?

Government guaranteed Corporate profits. Actually, that was step one in the sequence…..I got it backwards…….