Not much of a hangover yet. Going to see more of these frying-pan charts

By Wolf Richter for WOLF STREET.

Our Drunken Sailors have been out there spending money, and some of it comes from their surging income that has been outrunning inflation finally this year, and they’re spending money from their investment gains and from surging interest income from CDs, money market funds, Treasury bills, and savings accounts. And some are spending money they’ve borrowed. And our Drunken Sailors have borrowed heavily in recent years to buy homes at fabulous prices. So now it’s time to check in on them, to see how their credit is holding up under these conditions.

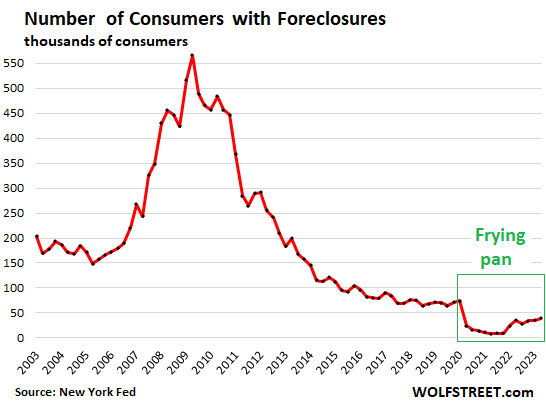

The number of consumers with foreclosures edged up to 38,840 in Q2, according to data from the New York Fed’s Household Debt and Credit Report. But that was down by about 45% from the Good Times before the pandemic in 2017-2019, and down by 75% from the Good Times in 2003-2004 when the housing market was approaching the peak of the prior housing bubble.

The fiscal and monetary excesses during the pandemic, the forbearance programs, and outright foreclosure bans reduced foreclosures to near zero. And now there’s the slow return to the Good Times normal. This combination is creating a lot of these frying-pan charts:

The funny thing is that in some corners, a big deal is being made of the catastrophic 340%, OMG-WOW spike in foreclosures from near zero in early 2021 during the period of forbearance and outright foreclosure bans. But a big percentage increase from near-zero gets to a level that is still very low, as you can see in the chart.

Homeowners are at risk of foreclosure if the market value of their house drops substantially below the loan value of the mortgage while they run into problems making their mortgage payments. Homeowners in some markets who bought over the past two years or so and skimped on the downpayment fall into this category.

But if homeowners have equity in the home and run into problems making their payments, they can just sell the home, pay off the mortgage, and walk away with some cash.

The problem arises when home prices drop by a whole bunch, and they have started to do that in a few markets, but still not very deep, and not broadly across the US, and the declines come after the huge run-up in home prices in recent years, and so foreclosures remain near the historic lows established during the free-money pandemic of foreclosure bans and forbearance.

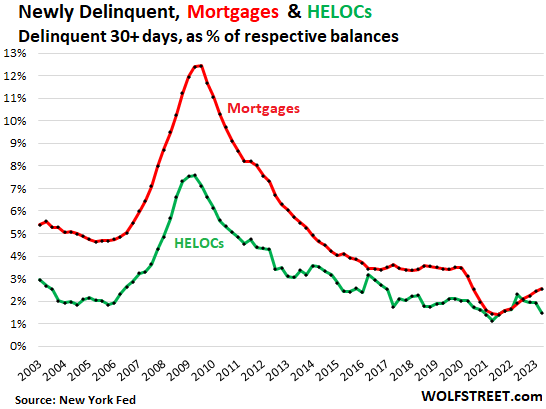

Mortgage and HELOC delinquencies have also edged up from historic lows. The rate of mortgages that transitioned into delinquencies in Q2 (30-plus days delinquent) edged up to 2.6%, but that was still down from about 3.5% during the Good Times in 2018-2019, and from 4.7% during the Good Times before Housing Bust 1, in 2005.

For HELOCs, the 30-plus-day delinquency rate dropped to 1.5%, the fourth-lowest on record (green line).

The handle of the mortgage frying pan hasn’t been installed yet. The handle of the HELOC frying pan already broke off.

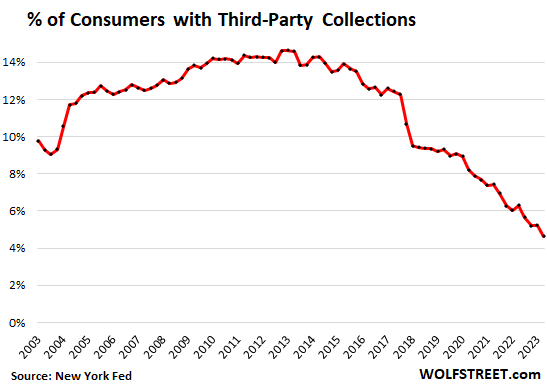

Third-party collections plunged to historic lows in Q2. The portion of Consumers with third-party collections on their credit reports dropped to just 4.6%, the lowest in the data going back to 2003.

This is where defaulted credit card accounts and other revolving credit accounts, such as personal loans and payday loans, tend to eventually end up.

Third-party collections are registered on a consumer’s credit report after a lender sold a delinquent account for cents on the dollar to a collection agency which will then hound the defaulter to obtain a settlement amount, and they might use wage garnishments, etc., in the hope of collecting significantly more than the cents-on-the-dollar they paid for the account.

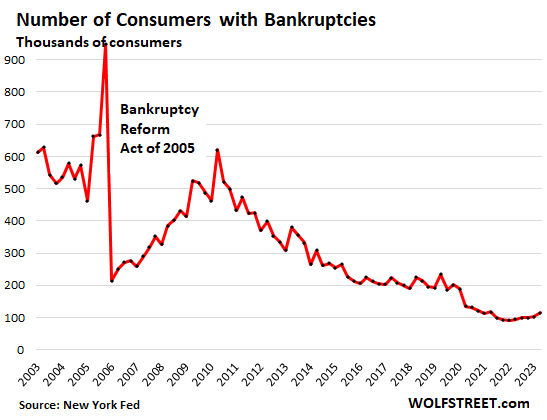

Consumer bankruptcies also hit historic lows during the free-money pandemic and have since then been edging higher but remain near historic lows.

In Q2, the number of consumers with bankruptcies inched up a tad to 114,000 consumers, still down by about 40% from the Good Times average of 2017-2019 of around 200,000, and down by 80% from the Good Times average in 2004-2005:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Still flying high. I see some hits in the used car market but they are bought up quickly.

Some people are desperate but the trough is full of piggies

If real estate prices come down then I’ll just cash flow via rental

hard to get below my mortgage ===== $0

Obviously the drunken sailors are the upper middle class and up, i wonder if there is a proxi way to track how they will be doing, maybe Tesla’s repo’s or vacations to Europe? Btw, i love coming to this site, and not seeing the annoying three bullet summary points for lazy readers, that every US news outlet sems to mandate. Beer money will be coming later this fall,

What would you put Upper Middle Class income at?

I read an economist’s paper that put 2 adults with 2 children lead a “comfortable but boring life” with $194,000. A year. And he put this as the middle class of 2023.

Earn below that and you are upper lower class?

Found it interesting.

There is no way to gauge “comfortable” or “boring” for everyone in aggregate. It’s based on individual perspective.

One person may think a $10,000 international vacation is necessary, to see and be seen. Others may find more enjoyment at the kitchen table, with family, friends, and a deck of cards.

Good luck with that one. Rents are coming down big time in AZ. Concessions galore. No one is going to rent your overpriced shack. The jig is up.

I hope so. I keep hearing “Even if I can’t sell for 2022 prices, I can always rent it out and cover my 3% mortgage.”

Based on the trajectory I’m seeing, this is doubtful.

For me, the weirdness in the essentially nationwide 20-25% post-pandemic (1 million plus killed…) rent explosion…is the fact that it was essentially nationwide (except for the historically insane metros…which maybe only went up 10%-15%…).

I’ll buy that some prime-attraction metros (FL, etc) might see demand spikes from migration, etc.

But Milwaukee? St. Louis? Pittsburgh?

I don’t think so.

As with exploding “household formation” (post 1 million killed…) I think this all merits a lot more analysis.

Cas127, that’s basically evidence for the adage post-pandemic where people have said “Things aren’t worth more, the dollar is worth less.”

….and on that note:

I live in cave creek AZ but used to live up in Prescott AZ.

The rentals numbers in Prescott / Prescott Valley / flagstaff etc are insane.

Gone up over 500%.

Prescott / Prescott valley has over 241 rentals now.

Flagstaff over 170 or so.

Months Ago there was almost nothing.

Yes, I see rental volume increasing in valley so prices are dropping (fast) but little scary how many are advertised fully furnished. As well as all the furnishings being dumped are websites like Craigslist, OfferUp, flakebook etc.

I have a bad feeling because people are distracted and not paying attention it seems.

Lala land.

Main Steam Media is currently publishing click bait stories about how 56% of Americans with student loans will have to decide between groceries and paying the student loans.

Yet with obesity approaching 50%, the glass half full take is longer, healthier lives, right?

Just asking for a friend…

Yort – time to reconsider the term: ‘…lean and MEAN…’???

may we all find a better day.

I mean, I’m not sure why anyone would willingly WANT to move to a place with 30+ days in a row of 110F weather in the summer. Would have to be a well compensated job.

I lived in Phoenix for 20+ years, I don’t miss it at all.

As I am worried there has been a non-linear climate change, they have my number and I get lots of weather articles. So this was a media outfit I had never heard about, I researched it to see if it was click-bait, and found this on wikipedia (with it’s usual refs);

On April 14, 2005, U.S. Senator Rick Santorum (R-PA) introduced the “National Weather Service Duties Act of 2005” in the U.S. Senate. The legislation would have forbidden the National Weather Service from providing any such information directly to the public, and the legislation was generally interpreted as an attempt by AccuWeather to profit off of taxpayer-funded weather research by forcing its delivery through private channels. AccuWeather denies this and maintains it never intended to keep weather information out of the hands of the general public.[34] The bill did not come up for a vote. Santorum received campaign contributions from AccuWeather’s president, Joel Myers.[35]

On October 12, 2017, President Donald Trump nominated AccuWeather CEO Barry Lee Myers, the younger brother of the company’s founder, to head the National Weather Service’s parent administration, the National Oceanic and Atmospheric Administration. It was noted that unlike 11 of the previous 12 NOAA administrators, Myers lacks an advanced scientific degree, instead holding bachelor’s and master’s degrees in business and law.[36]

NOAA has some VERY good articles on this June and July for those here who don’t hate our evil government yet.

This may throw yet another wild card into the real estate game, not to mention “climate change” opinions.

To me it’s pretty obvious….you have the less educated, the devoutly religious and those who follow Upton Sinclair’s observation on “human nature” that is probably the truest MOST significant statement ever made about how our we have. evolved mentally since the dawn of “civilization”, “specialization”, and governance.

But NOT before. We are social animals that HAD to get along or we NEVER would have survived. The fact all religions stress some form of the Golden Rule proves it is deeply hardwired in our pre-civilization brains.

Oh, Sorry,

Upton Sinclair’s observation that it is hard for a man to believe something that negatively affects his source of income….or something like that.

Guess I’ll find out if Wolf regrets teaching me to cut and paste long ago, as the above is in moderation. But I do believe it relevant to this thread and the article.

if it helps, it is pretty obvious the dems are responsible for the health care/insurance problems and possibly some banking….they have many donors there since they lost the union money and voting blocks.

“moderation” is a tripwire

Every time you complain about it, it goes into moderation, LOL

I give up. Oh well, not my site.

Oh.

Just posting here at the top.

MND says today’s 30YFRM is 7.24%. We’re almost to 10/20/22’s 52 week high of 7.37%. Woohoo!!!

I can only hope that Q3 GDP comes in @ 4%+ as currently tracking on ATL Fed GDPNow. And, I hope gas stays high and helps move inflation higher.

Recession or BUST!

Will you still take your whole crew out to lunch and give them the day off with pay like you said before?

That was for Joe diddly….seems others are beginning to notice the inconsistency in your “stories”.

Haven’t early 401k withdrawals been at a relatively high level? That’s a lot of spending money for those doing that.

Seems like we are in no man’s land as far as being between boom and bust where data sends mixed signals. Fed raised rates to where short term rates are very high yet average gold price for last quarter was highest ever. That usually doesn’t go together.

Tech stocks are priced like Cisco was 25 years ago, and Cisco has done pretty well as a business for 25 years, except if you bought at the top you have had a bad 25 years. Yet these high price to sales ratios are treated as no big deal.

The period of time when yield curve is inverted is only about 15% of the time. I haven’t seen too much discussion on investing during this time, other than stocks usually fall after Fed steepens the curve by cutting because something has broken. It might be the most rewarding or devastating time for investors because Fed seems to be tip toeing up to point of breaking things, but fiscal policy is pushing hard against that.

I think data can be pretty suspect at end of cycle and there are a lot of revisions when its a little late for making investment decisions.

Gold is the same price it was back in 2020.

And 2022.

Steadily losing ground to inflation.

If you bought gold as an investment for short term profit that is on you.

Gold is a mirror of the value of the dollar. The dollar is strong ATM, causing a slide in gold prices. When the dollar weakens gold prices rise. That is how the whole thing works…

Here are the 1year / 5 year returns on gold:

US = 6% / 60%

Swiss Franc = -1% / 41%

Canadian Dollar = 11.5% / 64%

Euro = -.6% / 67%

Yen = 15% / 110%

British Pound = 1% / 61%

Ruble = 73% / 132%

Aussie Dollar = 16% / 79%

S. African Rand = 23% / 110%

India Rupee = 10% / 89%.

I am pretty sure your statement is not correct.

Comparisons

SPY = 4% / 71%

DOW = 4.5% / 54%

Russell 2000 = -2% / 14%

Nasdaq 100 = 10% / 24%

Germany DAX = 3%

Vanguard all world etf = 5.9%

Vanguard Europe ETF = 10.8%

Franklin Canada ETF = 26%.

3 year returns

Gold is up 7.5 percent compounded annually the past 25 years.

I agree with coffee.

Think of it like an insurance policy. Hold a little and hope you never have to use it. But if you do need to use it, you’ll be glad you have it.

Yield curve analysis based on history in which the Fed was not involved at all in the long end is FOLLY.

The Fed is hiding circa $5 Trillion in long term debt from the market.

The inversion is “painted, the artist the Fed, and the fake inversion is part of the imaginary world created by central bankers, IMO

Thumbs up !!

In Europe the ecb published à estimation of the term premium supressed by its balance sheet holding.

It roughly represents :

0.4% on 2y maturity

0.8% on 5y

1.2%% on 10y

Meaning that there is no inversion in Eurozone.

FED assets holdings is roughly the same.

Exactly.

The Fed pounded long rates to FORCE investors to buy stocks and real estate, etc…

This was admitted to by former Fed Regional President Fisher in the PBS documentary “The Power of the Federal Reserve.”

FORCE? Is that in the Federal Reserve Act?

“Tech stocks are priced like Cisco was 25 years ago, and Cisco has done pretty well as a business for 25 years, except if you bought at the top you have had a bad 25 years.”

Excellent example that should be invoked more often.

Somebody needs to point a few things out to Microsoft/Apple(!)/Facebook(!!)/Amazon (!!!) shareholders holding 30/40/100 PE stocks…in companies that already sell to everyone on the planet.

You can only conquer Earth once…and you don’t justify huge PEs with GDP-paced growth…

I remember that! I was in a tech school at the time. Cisco was worshipped.

I remember my friend being bragged about in class because he got one of the first 6 figure salaries they offered. But then he burnt out in a year configuring routers. Which is mind numbingly dull.

Microsoft and Apple are bi opolies…….coordinated monopolies in a sense. Anyone notice?

Thanks Wolf. This is a great article. Best wishes to you!!

“number of consumers with foreclosures” graph: a bottom has to start somewhere, no matter how low, usually at a bottom. Looks like we have hit a bottom.

‘…out of the fire and into the frying pan…?’

may we all find a better day.

Thank you!!! Finally. I had to wait 20 hours to see “Out of the fire into the frying pan.” I thought it would be the first comment up.

…thank YOU, Wolf! I hope this doesn’t mean too-many comments are AI-generated (no sense of old-school idioms). So obvious i thought I would be late to the party…

may we all find a better day.

America household balance sheet looks to be healthy and in order, unlike to the Federal government. The Shock and Awe media platforms want us to believe the sky is falling, but there are far too many jobs and help wanted signs posted where I live. New cars and expensive new trucks are still pulling up in my neighborhood driveways, Amazon truck is noticeably here everyday. Last half will be a blow out for GDP, consumption junction nobody does it better than the USA. Great to see the raw data presented in laymen terms. All Hail Wolf!!

“Amazon truck is noticeably here everyday.”

That’s my fault but I don’t think it is due to me having too much money.

I have a number of ongoing home projects that I can do and don’t want to hire a handyman at $200/hour. I guess that means I am helping keep services inflation down.

As I planned the projects, I noticed a few things. I needed a can of water-based spar-urethane and a cable clamp. I drove the 5 miles to Home Depot, had to find someone who knew where to find these items. After 30 minutes, I found the location but they had bare shelves. It was recommended that I order from HD online and have it delivered to the store (or to my home for some larger cost).

Instead, I pulled out my phone and Amazon delivered it to my home for free within 2 days. Well, not for free, I have Amazon Prime. IMHO, it is worth it just in gas and time to find many things and have them delivered. The exception being large things like lumber, stones, plants.

For many small items, it is very convenient to order most project items from my house and have them delivered within a couple days on Amazon. Most items are cheaper on Amazon compared to Lowes or Home Depot.

This will change if it goes back to the old days and Amazon starts charging UPS/Fedex rates for delivery. I tried to send a toaster as a gift few years ago and UPS charged more for shipping than the toaster cost. Instead, i ordered it on Amazon for less than Target and had it delivered to the recipient directly for free.

I am personally keeping inflation low due to my lack of money. :-)

…re: ‘free’ shipping – as in the illegal substance trade, the first taste is ‘free’…

may we all find a better day.

You are spending on home projects or repairs? I just had 4 pool lights replaced 15 years old and had some shorts someplace in them. My contribution to spending interest on my money market . 4 lights were 500 each incandescent vs 1400 for LED. Have not seen the labor bill yet.

Retired in East Texas. That said my electric bill is 50 percent higher for my 3 year contract that expired this year . Higher for longer but I’m not poor since I can pay for pool light repairs.

Per Fortune in regards to “free shipping/returns/most of it goes to the landfill” quagmire:

In 2022, returns cost retailers about $816 billion in lost sales. That’s nearly as much as the U.S. spent on public schools and almost twice the cost of returns in 2020. The return process, with transportation and packaging, also generated about 24 million metric tons of planet-warming carbon dioxide emissions in 2022.

^^^For Reference…US citizens produce about 15 metric tons per capita per year, India citizens about 2. So 2.267 million US citizens in return CO2 waste, 17 million India citizens in return CO2 waste.

Wonder what we will get rid of first, Prime Steak or Amazon Prime’s free returns of trinkets???

The irony is that the central banks printing money is creating a perpetual loop of buying happiness which only speeds up the extinction process.

Sometimes I wonder if A.I. has already taken over and is just getting rid of us slowly. Forever low rates, endless free money printing, seems like a sneaky, logical way to speed up the process, right?

I’d type more but I have some Amazon returns I need to repackage…

This is exactly how Amazon has created impulsive customers & purchase habits. These returns do cost money even if customers aren’t (directly) paying for it.

Amazon also goes the extra mile to screw 3rd party sellers: they’ll receive our product, ship it to a customer in a thin plastic bag with no packaging, and then let the customer return it after beating it up / throwing away the packagjng etc.

And then to add insult to injury, Amazon won’t let us resell it as new anymore, we can only list it as a refurb. So now we’re forced to lose money on *their* returns, that they created with their excessively lenient return policy.

Every now and then I have a customer ask how long they have to return something they’re buying, and then ask to make sure I grab one from the shelf that’s never been opened. They want to have their cake and eat it too.

BobE,

Prime is definitely worth it to me, $139/year. I don’t use cars. I am a stubborn greenie. I have two great bicycles. One with panniers for groceries and other things and the other a monster electric off-road bike for getting out.

So, I save a lot of money and Prime helps, get my exercise, and do my bit for the world.

TC – …I’ve no doubt you’re practicing many other ‘green’ efforts, but you’re still using someone else’s trucks, etc., pretty often, nay? (Nod to Yort, above). In fairness, I wonder how much actual carbon/energy consumption reduction there has been as a result of ‘free shipping’, if any (tough to objectively quantify, in any event, TANSAAFL is always baked in…).

Remember, your bit for the world refers only to maintaining a planetary environment that allows the human species to survive upon it. Whether we do, or don’t, it cares naught…

may we all find a better day.

…add missing ‘T’ to TANSAAFL…apologies.

may we all find a better day.

I would say so much of the personal balance sheet wealth is built on asset multiple expansion. Price to sales ratio of SP500 is 3.l times higher than bottom of GFC. Multiple expansion is temporary wealth that is usually unjustified. Long term wealth is the sum of future cash flows.

The hangover isn’t happening yet, because there’s been an extensive longer than normal binge of black out, alcoholic denial, lingering as if things are normal.

I was thinking today, one thing that’s distorted the Fed rate hike shock, is the infamous Dot Plot, introduced around 2012+/-.

The dots and all the weekly Fed telegraphing and excess jawboning, has effectively buffered the reaction and impact. Everyone talks about long and variable lags — from Milton Freeman, but that was from studying economic cycles, before 1960. The process of telegraphing rate hikes, with Dot Plots, games the system.

I think one reason the drunk spending spree continues, is because the Fed has zero credibility and rate hikes have become unimportant.

Speaking of drunk sailors, the Fed BTFP is very interesting, because the 30 year Treasury yield is higher today than than during the mini-crisis in March, while the BTFP screams higher, with not so stealth QE. The banking crisis is obviously not contained, as banks attempt to buy time, hoping they can stay solvent with Fed support.

Semi-related, good thoughts from Keith Wade from Schroeders, related to the background of the drunken spree:

“ Of these four effects the low starting point for rates, fiscal largesse, and the pandemic effects have been most unique in making it harder for the Fed and other central banks to interpret and then tame the economy and inflation.

Monetary policy started from an ultra-loose level and while the Fed and others might have realised the need to tighten sooner, this came against a very uncertain backdrop of the ongoing pandemic. In addition they had to offset the stimulus from fiscal policy as well as contending with the unusual effects of Covid on spending and the labour market.

Notwithstanding the support from the Inflation Reduction Act and the excitement over AI, our view is that the tide will begin to turn in favour of the Fed as we go forward. Monetary policy is now in restrictive territory and the benefits of fiscal support and excess savings are diminishing.”

Cheers

We’re NOT going to see a recession with the amount of deficit spending we’re seeing. The FY23 deficit will approach $2T. Based on my research we are now looking at ~2T structural deficits going forward. These huge deficits are single handedly keeping a recession at bay.

By sometime next year, could GDP slip back to 1% or below? Sure but for GDP to slip that much, we’ve got see a real erosion in housing which traditionally leads the economy into a recession. Right now, housing could care less if mortgage rates continue to stay at or above 7%. And why is that? Well, that’s because home prices are going back up, the cost of materials like lumber have dropped dramatically and builders, in general, are sitting on 40%+ gross margins. The wild card with housing is what happens as these funky fixed / ARMs start to adjust in the next 6-9 months? There maybe just enough numbers for that to become a bigger deal by mid 2024.

In addition, the labor market remains on solid footing. A recession isn’t going to happen until 1st time unemployment claims move up to 300K and then towards 350K which will then push the continued claims toward 3M with them currently being at 1.7M.

We still are a ways off from the sustained levels of bad news for a recession to be around the corner.

disagree. Drunken stock ponzi investors keeping the euphoria in housing afloat imho. When stocks start going down this year(maybe this week) greed turns into panic and both stock and housing ponzies start losing trillions and trillions..and lots of trillions, much more than deficit spending debt that dont matter does anything. Drunken spending sailors sober up real quick when dreams are turned into nightmares just like that. Then it will be clear to everyone, that 60% were already broke from inflation even before the bad times started. Denial is always a tough one(to learn). nonsensual halucination… more please, money for nothin and chicks for free.

Best economic analysis,..

“of what could happen” that I have ever read anywhere.

And I follow this shit every single day.

Wolf..are you listening ?

If the pandemic wasn’t enough to sober people up for a long while, I don’t know what would be. I suppose it just made a lot of people think they will always be bailed out or it’s ok to just walk away from loans.

We’re staying afloat or above on deficit spending. The economy depends on it now. Keep an eye on the currency floats to see how long this party can go on. You have to admit, the dollar has given us a nice free long ride.

Just watch UK were usually a year behind them

“We’re NOT going to see a recession with the amount of deficit spending we’re seeing.”

Eliminating bank mark to market requirements also created billions of dollars that do not exist.

40 percent margin for homes? Is that the current large home builder margin ? My check on one home builder Pulte Homes had a net margin after cost of revenue and Opex of about 22 percent before income tax . Still healthy .

About double what it should be

I specifically stated GROSS margin. One of the big ones like Pulte said not long ago, spring I think, that gross margins were 43%.

So the MMT advocates were right ? There may be a consequence someday, but it will be after we are all dead ?

TLDR

I read all of that comment AV8R. Shame you don’t have anything of meaningful substance to contribute in the comments, besides TLDR.

I wonder if AV8R looked at the pictures…:)

Most of my neighbors are living well beyond their means especially when it comes to expensive trucks. I see these young guys commuting to work in monster size trucks…tough to get ahead while living like that.

Makes you wonder if AV8R does the same thing with his pre-flight checklist…. “Too long…. didn’t do”.

STFU

Bank failures: If people don’t default on the essentially low interest loans, perhaps the stress will be transferred to the banks that have to pay higher interest rates for the money backing those loans. Seems a bank is “bankrupt” by definition having loaned out depositors money that is represented by those loans (the actual money went years ago to whomever these borrowers bought the house, etc. from).

Absent a bank run (maybe some kind of short selling), the pressure is just going to build and build with depositors wanting a real rate of return over inflation. Investments overseas in “friend shoring” by “captains of industry” may help to remove excess private equity liquidity from the domestic financial system as well; better to be multiplied many fold in wealth turning India into China then as a boat anchor in some overpriced shack’s mortgage or clunker car loan.

For a good while now, banks have been “flipping” loans to the markets as securitized debt almost immediately after they write them. As I understand it, Silicon Valley Bank got into trouble for holding Treasuries with the wrong duration mix, not for holding bad loans.

Howdy Folks. YEP, drunk or sober lets keep enjoying life by living within your means and purchase what you want. With the captains and generals never stopping, what should we expect?????

A house near me just sold for a 76% profit over 2018 prices. 76%! Just In SA NE!!

It’s had 4 owners and the latest owners who sold it hit the friggin jackpot.

This feels like 2007 again…

From those those charts, it appears as though being an average American ain’t all that bad…

Sir, can you say something about “Bric currency”. Is the talk real or just talk?

You want me to say something? OK, here we go: “Bric currency” = blogger BS.

It’s not even a currency.

Thank you ! What I say all along ! Go USD . The dollar always gets converted to the local currency eventually .

Emil,

Anyone talking about “BRICS currency” is either trying to scam you or an idiot.

Think about this: what is the likelihood that Brazil, Russia, India, China and South Africa are going to get together in a monetary union, a la Euro?

Zero. All of them have serious debt, inflation, etc. problems, much worse than the Dollar, Euro and Yen.

Russia has been de facto kicked out of the banking system, so any adoption of a BRICS currency risks sanctions on adopters, so no US, European, etc. involvement.

China has their own currency and will never surrender authority over their domestic monetary policy to anyone, ever.

Brazil and South Africa are too dysfunctional to manage their own currencies, let alone anyone else’s (and politically things are quite touchy in both countries with major polarization).

India is the only major rising star here, and despite tons of problems, won’t carry water for the other 4 and will bolt at the first signs of trouble.

Never going to happen.

What they are aiming for is not a currency but a unit of value for clearing between currency areas. The unit of value probably a weight of gold. Reference only, therefore fiat. Whether a debt market can develop remains to be seen.

Which of above Brics countries, if any, do you want to hold the gold?

If this was going to work, then Brazil and South Africa, being gold producers, should be able to do this.

Problem being, neither have been able to pull this off because they are too dysfunctional and no one trusts the people in charge not to steal the gold.

Actually, “BRIC” currency is in making for nearly two decades with no start point in sight. But yes, it’s real, but not really real.

As mentioned, it suppose to mimic EURO union, meaning, there will be “BRIC” currency that all the members will international trade with, but all the members will have their own currency running locally. Its purpose will be only international trade.

It will have zero effect on USD/EUR/JPY. They want other currencies to work hard for them, and they want to take easy path, just to work in the shadows.

Specifically, they were thinking about “BRIC” to be backed up by a basket of commodities, but it’s too complicated, as there are quite a lot of commodities, so they are thinking about gold as a backup. But NOT PHYSICAL GOLD! They want the price of “BRIC” to be tied to PAPER PRICE of GOLD! Most idiotic currency solution ever. Another FIAT, but crazy one. Currency PEG to paper gold. Sounds like another crazy cryptocurrency.

IF they will go through with this, the “BRIC” currency will be PURE SPECULATION (one side bet against USD). If USD will fail Gold/USD will spike up, and BRIC will be the best currency in the world. But if USD will get stronger, the BRIC will fail hard and whole union will fold. If west decides to use derivatives (to manipulate GOLD/USD price) to blow up BRIC, there is nothing easier, as “BRIC” union will have very little control over price of paper Gold.

Let’s give them another few decades, maybe they will come with something even more crazier.

You make an important point. The goal is to provide an alternative to trade settlement in USD. The US propensity to impose sanctions on anyone who does not toe the line makes some alternative settlement method inevitable. How long it takes is unknown.

Russia is excluded from buying stuff they might want with USD or EUR. China sees that risk coming their way and wonder what happens to the 850 billion in treasuries they hold.

India pays for Russian oil in Rupees, but Russia is accumulating more Rupees than they can recycle. At some point Russia will offer the opportunity to Turkey to pay for oil with Lira. This will be good for Turkey and possibly good for Russia, but just provides another bit of pressure to find an alternative for settlement.

The US and it’s G7 hamsters are being very successful in convincing Russia that it has no avenue to a peace that is not just a pause to refresh for another war. Consequently Russia is slowly coming to accept that the only road to lasting peace is to confront and defeat NATO.

Russia continues to mobilize at 40k new people per month and now talk of another formal mobilization of 500k. Meanwhile NATO does nothing and prepares for nothing. Confident in their own story telling just as we are confident that USD is forever.

There are a lot of unknown, unknowns out there

The kids in the BRICS club: some can afford the movies, others can barely pay for the zoo, and one’s in timeout and isn’t supposed to be playing anyway. Gold decoder rings won’t fix the basic inequities in this club.

The dollar has appropriate problems for it’s status among currencies as the big dog tolerates a flea here and there. And sovereign nations hold gold because they don’t trust each other, not because it’s a great way to facilitate the settling of trade accounts. Somebody will get boned, the BRICS club membership guarantees that.

So the Bankruptcy Act of 2005, signed by Prince Bush, supported by Biden and opposed by Professor Warren, helped our fellow Americans out of the need for Bankruptcy.

Oh, Ho, Ho In 2005, Congress passed the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA) after heated debate. The new law was designed to deter people from pursuing bankruptcy by making filing for it more difficult and expensive, as well as less financially advantageous.

The report says it brought down interest rates, but target results were not successful overall.

https://www.ipr.northwestern.edu/news/2019/assessing-the-bankruptcy-law-of-2005.html

Who knows?

That law certainly changed debtors attitudes during the great financial crisis of ‘08. Debtors walked away ( strategic default ) from mortgages, but kept current on credit card debt since it was now much harder to default on.

Many prioritized their car payments first as “you can live in your car but you can’t drive your house”. The car is normally needed to get to work as well…..

Hehe, so handy that it was done before the crash of 2007.

It’s like heading a train off at the pass. ;)

The 2005 bankruptcy reform act had nothing to do with preventing abuses of the bankruptcy system, despite the claims of its supporters.

Instead, it was driven by the banks and credit card companies, who in the late 90s and early 2000s were sending out pre-approved credit cards to anyone who could fog a mirror, including house pets. My cat even got one (though she did have a stellar record with zero defaults).

The logic behind this was that sure, there would be more defaults, but they would more than make up for it by charging those who didn’t default 25% interest. But people failed to follow the models. While many card holders pay their bills in full every month, those who didn’t started to default in numbers much higher than the expensive consultant-driven models predicted.

Oops. So what to do if you’re the banker who made this mistake? Run to Congress and get them to change the rules, all in the name of preventing abuse and restoring honest free enterprise.

Same song, 299th different verse.

There’s no reason that people who have the ability to restructure and pay something should get the slate wiped clean so that they can blow money on cell phones and manicured nails.

Sure there is. The consumers cannot consume if they are in timeout.

Slap on the hand and back in the game!

Taco Bell needs profit. Go buy a chick Fila sandwich Missy!

1) SPX 3M (quarterly) with a cloud : T&K clamp is too wide. SPX prices are too far above the cloud.

2) Senko B, the lagging line is resting between 2009 and Oct 2011 lows. Within a year Senko B will lose the 2011 low and move up all the way to

the 2020 low.

3) The Cloud front end will flip. T&K will flip.

4) The last deep red flatbed was between 1939 and 1951. 1981 and 2016

are a blip. SPX might form a new deep red that might last until the 2030’s and the 2040’s.

1) NDX 3M, Tech analysis, skip : price is too high above the cloud. T&K

clamp is too wide. Equilibrium and sanity far below.

2) NDX is rising on a Lazer : Oct 2011 to Feb 2016 lows. Parallel from Nov

2014 high. NDX formed a double top.

3) The lagging line, 52 quarters to the left, will lose it’s lows and rise nonstop. Senko B will rise and flip. A new all time high might delay the flip.

4) NDX big red cloud was between Oct 2008 and 2019. NDX might turn

around and become red again.

5) The cloud is thin. NDX might reach/breach a support line : Oct 1987

to Oct 1990 lows.

6) SF might…

Your comments seem random

Jack – stick around this, Wolf’s most-excellent establishment, long enough and you’ll get a feel for Michael’s ‘Engelish’…

may we all find a better day.

how long does that have to be…. I’ve been here a number of years now

curious – I didn’t mean to imply you can necessarily follow it!

may we all find a better day.

Jack,

From what little (might as well say NOTHING) I know about chartist indicators, I think each numbered item is a complete observation in itself.

So, of course course it’s random, but together a current picture is supposedly painted, not a sequence of events, ie, it’s random.

It’s an attempt to mathematically organize the supposedly “real economic reality”. People get Nobel prizes for it, also in Physics and Medicine/Bio, or Chemistry. But it has to be in the language of Math…….which also gets a prize……no layman understands any of it.

And it all changes. EX; Doctors were still bleeding people in 1900 and several years after. “Fact” and “truth” are VERY elusive SOBs

And yeah, I can only follow it on very rare occasions, and even then I’m not sure I truly am.

Oh, and colleagues judged “best” in the field (by other colleagues) vote for who gets The prize…..kinda like the academy awards.

The further we go into the “managed for private profit” world the more it ALL becomes corrupt BS.

I still am pissed about the lady who finally took photograph 51 not sharing the Nobel prize with asshole Crick…..but that technique is looking doubtful (fudged, perverted) to me now, anyway, especially in Bio-chem.

Side note; Einstein and his gang’s theories were not required to build the bomb or reactors….just good old Newton (and the Curies), who is also applied to Maxwell to make fancy electronic motors…..like solid state stuff, it was just trial and error….as a kid I had a “cat whisker” radio….solid state…years before jerk Shockley…..along that line, I kinda think life is “electronic”….and that makes us just doped water. Took 4.5 B years, though, which we don’t comprehend any more than what “electrons” really are.

Must have a quark up my ass today, sorry for rant.

Guess it would be a “bottom quark” from the theory…..yes?

Fun thing.

Look up the first atomic pile at Univ of Chicago. Fermi had a REAL Dead Man Switch in case his “calculations” were wrong. Would have really Fd up that stadium…..and the “dead man switch” would be really dead.

Always enjoy Mr Engel comments and insight. Definitely don’t know all the lingo but some I do. Like T&K. No idea what T&K are .

T&K = Tidbits & Kibbles (a brand of cat food)

Google to the rescue; TK-profit means cash flows after taxes received by the TK Investor as the economic benefit after providing TK investment under the terms of a TK Investment ..

Got that? There is more, too…….

After being out of work from 2020 to 2022, I finally landed a job (paying much less… but it is steady income) and was able to make use of the Covid Forbearance programs to stave off foreclosure. It was a pretty interesting process. I thought that it was unique to the COVID situation but instead I found out that most banks have a routine forbearance process for a routine problem in America… DIVORCE

It turns out that the banking industry would be up a creek without a paddle in a nation with a 50 percent divorce rate if most of those houses ended up in a distress sale or foreclosure. So they have a process in place to protect themselves… who’d have thunk it? They just transformed it into their COVID Forbearance Program (with a little help from the Feds).

In my case I was eligible for about 20% of the refinance to be done through a federal program at 0% interest… DEFINITELY a pandemic-era program which seems to account for all of the interest that the bank would have eaten if the house was foreclosed on. For the rest of it the bank simply extended my 30 year mortgage into a 40 year mortgage at about half a point higher than I had been paying since 2010 when I last re-financed the house.

My actual monthly note is slightly less than it was before. That is because the “revised” mortgage is on the BALANCE of the principal left over after a dozen years of payments. What is NOT dealt with is the small HELOC that I had prior to the revision… I am dealing with that separately. Obviously if I refinance OR sell the house then I have to repay the government, the revised mortgage, AND the HELOC before I can see any profit myself.

Also obviously I will take a real bath if I let this loan go on for the whole 40 years… not that I expect to live to see 100. But with interest rates where they are at the moment… this is NOT the moment to refinance. Nor do I think that I would qualify for a conventional loan at the moment. Of course I can also eliminate ten years of the mortgage by paying an extra $125 per month for five years.

So basically I am back to where I was in 2010… about $110,000 mortgage on a 1400 square foot 3-bedroom ranch-style house. Hopefully the house is worth considerably more than when I first bought it… but a lot of repairs have been delayed due to my difficulties finding work over the past seven years.

All-in-all, not too shabby of a program that was pretty well thought out. I get to stay in my house… the bank and its investors are protected, the Federal Government is protected… and the only part that is at risk is whatever the Feds lose to inflation until I sell the house or refinance it (and the Federal Government is the responsible party for determining inflation rates). It certainly beats the alternative of millions of people looking for housing amid a banking crisis which was the situation that the pandemic almost certainly would have brought on if not for this forbearance program.

“Your Mileage May Vary!”

If anyone still has questions why the housing market is dead, you just gave the perfect answer.

How does anyone survive without work for 7 years

I thought he said 2 years?

How can you have 1 payment for an 80% mortgage thru your bank, a 20% payment thru the feds and a HELOC tied to your 80% mortgage?

Also I had not heard of 40 year mortgages until 2023.

Perhaps you can use your social security and retirement funds to help pay off the 110k. Like when you are 66 (bigger SS paychecks).

It was sort of both two years AND seven years. I probably should have said “due to my difficulties finding STEADY work over the past seven years.” I posted a response below that is more complete. Let me answer your other questions now.

First Question: The basis of the loans is a house that appraised for $122,000 in 2010. The total value of the loans has NEVER exceeded that amount. Meanwhile the value of the house has increased by about 50% in 12 years. My guess is THAT is why the forbearance went so quickly and smoothly once I had a job and could make the monthly payments again.

Second Question: I had never heard of a 40 year mortgage (in this country) either. In fact the bank didn’t even tell me that they did that. I noticed the date of the expiration was 01/2063. I reviewed the paperwork again last night and there is nothing in there that says “Term: 40 years” … and somehow the bank never brought it up when I spoke with them.

Third Question: To pay off the house I won’t have to wait until I turn 67 for “bigger SS paychecks” although I intend to do that too. My military reserve retirement will kick off in eighteen months when I turn 60. At that point I will truly be alright… especially if I can find a job more in line with my past education and experience. I have said before in a WolfStreet comment that I view a paid-off house as one of the pillars of a SECURE retirement plan.

In the meantime I have found a buyer for all of the inventory for my side business of 20 years and this job that I have is fine for now. But thank you for your concern. Truly!

How is somebody out of work from 2020 to 2022 in the easiest job market in history? Seems self-imposed.

“Long Covid”…

Age discrimination? It’s a thing, even in the hottest job market ever, especially in some sectors (tech, social media, some others).

Bing Bing Bing… we have a winner. With Wolf’s permission let me post a response I made back in July of last year to an entire article Wolf had about ageism in the job market.

I am living proof of the ageism problem right now. I am 57 and have an MBA from one of the top business schools on the planet… “Hook Em Horns!” Retired from the Navy Reserve as a Commander. Used to teach Business Management (mostly Marketing and Entrepreneurship) at two different universities.

After my last management position ended in November of 2020 (I was a Recruiting Manager for the 2020 Census which ended) it was time to look for a new position. In the space of a year I applied for 208 jobs… I got FOUR interviews… and ZERO job offers.

Then I read this quote from Wolf in November of 2021…

“Ageism trumps everything. 35-year olds don’t want to hire 65-year-olds. Simple as that. I didn’t do it either when I was 35. And now, three decades too late, I feel bad about that.”

That is the kind of insightful comments we see at WolfStreet that keep bringing me back here. It explained so much that I was just shocked. For instance, why was the computer system rating me as one of the highest acceptable applicants (based on my resume and application answers) for well over half of the positions but I wasn’t getting any interviews once the humans took over the process? In my job search I wasn’t wasting time applying for positions that I wasn’t qualified to fill.

In March of this year I went to a weekly Job Fair at a local casino. I thought I would find out how to get my resume into their system and hunt around for a Marketing position of some kind. Instead their HR people instantly brought two managers down to interview me on the spot… one wouldn’t make an offer because he said the other would make me a better offer… which she did. It pays exactly half of what I was making at the Census Bureau when I was a manager there but I am grateful to have some income flowing in now… it may help me save my house from foreclosure.

That said, because of Wolf’s comment it did occur to me that the HR people in their early 30s didn’t steer me towards managerial jobs. They steered me to the call center jobs booking hotel, flight, restaurant, and entertainment ticket reservations.

Reading the comments to THIS article also highlights what Wolf meant when he said “Ageism trumps everything.” The number of people who post some story (on an article warning of the dangers of ageism) of how old people (or young people) lack computer (or work) skills is both funny and weird. Two words people… CONFIRMATION BIAS.

This job I am in now is challenging because you have to juggle literally a dozen different computer programs while being engaging on the phones to the top 10% of the casino’s customers. Out of the seven people who started this training cycle, so far we have lost the 52-year-old and the two 21-year-olds. Holding on are two people in their 50s and two in their 30s. The point is that it is not wise to assume that old or young people are going to be a bad fit for a position because you remember some story from the past.

https://wolfstreet.com/2022/07/08/i-want-to-add-a-word-about-ageism-in-this-bizarre-labor-market-and-how-it-hits-labor-force-unemployment-numbers/

PS: In the end my employer was only able to hold onto me and a 35-year-old woman. The next class of seven hires also only held onto 2 people. I don’t know their ages. The job is a difficult balancing act of skills… and (like so many others) age has absolutely nothing to do with who will be successful in it.

PPS: I really want to thank Wolf for both his insight on this issue (and so many others) as well as his personal encouragement to me over these past couple of years.

Age discrimination. I made it Senior Professional Staff at JHU Applied Physics Lab with an A.A.S. as a computer programmer. Resigned after being physically assaulted (7lb hard drive thrown at me by tall guy waving arms, advancing rapidly, and cursing). and HR and management looked the other way. HR gave my boss a book to read and called done. Went and finished my B.S. in Information Assurance. Applied for 30+ jobs and not one interview. White man in his late 50’s, not hard to figure out based on resume dates and surname. To hell with this country.

“I am living proof of the ageism problem right now.”

Walmart was hiring the entire time. You could have taken the Walmart job while you still looked for a better job. But that was “beneath you” I’m sure.

Cmon depth charge. I don’t even want to shop at Walmart, let alone work there. Walmart is a hobo rest area.

This is why I bought my house alone, with only my name on the mortgage and deed. One variable I don’t have to worry about.

I need to find out what these people are drinking where they feel fine the next day…

It looks to me that Congress has basically transferred a huge chunk of private obligations and debt to the government balance sheet. So now it’s all dependent on the U.S’ ability to borrow, which at current rates, seems unmatched.

…keep on socializing all that risk…

may we all find a better day.

I think that statement is averse to Carpe Diem!

Lol

…financial risk, that is…

may we all find a better day.

Maybe this narrative of drunken sailors is more a story of perception.

It’s fairly challenging to dance around the alcoholic metaphor and to also walk on political eggshells, but I think we’ve all been exposed to a very long period of social changes, which layer by layer, have resulted in widespread malaise and shell shock (PTSD).

A great starting point is to at least identify the GFC as a break from reality — then fast forward to the period of trump chaos — then, accept that the pandemic acted as a supercharger for amplifying social and economic distortions.

The magnitude of changes and shocks are ongoing.

Maybe it’s as if we’re in a PTSD recovery mode, and for many, there’s a desire or need to believe everything is normal, and then believe in the safety net of Fed helicopters, and bailouts and ignore the actual cost of reality.

Wolf often refers to a consensual mass hallucination, and there’s probably a lot to that, and the power of group dynamics.

Within that framework, maybe it’s easier to pretend that grocery prices are falling, wages are climbing, GDP is booming, housing is booming, banks are fine, inflation is dropping and that Prozac pablum that helps some people tune out uncomfortable vibes.

The most alarming aspect related to this phase of the consensual hallucination, is the extremely sad fact that we’re racing towards an election year, that will mix together, polar opposite hallucinations with polar opposite realities, then use the media to amplify the collision, into a circus event that ultimately has no meaning.

The PTSD economy and society we live in, requires drunk sailors, and as we move away from anything real, it’s almost funny how the American Dream, is entirely compatible with life in China, Russia, North Korea, etc…. We’re basically allowed to vote for the best corrupt oligarchs and accept illusion.

Damn’d good.

Yet another layer of impending illusion/collision is the political risk of so many vast dynamics and outcomes in our political economy wobbling atop super thin bases of 1) quirky top politician and oligarch individuals, and 2) so much of the matter being shoved square-peg style into the poorly matched forums of courts and jury trials. One very ignorant juror in any of several cases (now enveloping both parties) can tip multiple huge outcomes in this situation. A society can only be stable and persist if people keep agreeing daily to not go for each others’ throats, full tilt. This bargain is now in question. Thank goodness (I think?) the world ex-USA is floundering, perhaps holding up our credit ratings (and cards). What could go wrong? Better keep spending on that vacation or granite countertop or whatever, to stay ahead of these dust devils ….

KRON, channel 4, re: American Dream: “To keep a house payment below 30% of your income after putting 20% down, a person would need to earn roughly $16,693 per month or $200,316 per year – just to buy a median-priced home in California.”

ancient Chinese curse: May You Live in a Time of Change

In Canada a small canary in the spending coal mine was Canadian Tire reporting declines in both revenue and profit in the second quarter. They also revoked their 3 year financial forecast. Presumably our shorter term mortgages here mean that interest rate pressure will be transmitted earlier to debtors than it will south of the border.

Canada is a different world than America. America doesn’t flood the country with ‘international students’ who work 40 hours a week for minimum wage, or a Minister who gaslights Canadians, and tells them that Canada needs more newcomers to build houses. The truth is that many newcomers aren’t allowed to work in the trades upon landing, because they have to join a construction union.

Wolf, thank you for pointing out that the panic hyped recent increases in the number of consumer foreclosures are possibly comparing panicdemic “oranges” in the dip, to post panicdemic “apples”.

Excluding the “artificially created dip” (if I may call it that), these latest foreclosure figures appear to be the lowest of the chart since 2003. And if I may also ignore the dip of the frying pan, the present foreclosure figures are still below where they appear to have been trending prior to the frying pan’s dip.

Also, thanks for yet another term for charts, “fying pan”. I’ve added it to “consensual hallucination” one of the best descriptions of market activity I’ve heard, love these!!

Here’s a thing that’ll be part of the glorious pandemic hangover, regardless of how much money have flowing in:

“The number of protests filed with Colorado’s 64 county assessors increased 300% in 2023 compared to the average number of protests from the previous three assessment cycles.”

Eventually, cash burn will increase and there will be less play money, and over leveraged speculative bozos that haven’t factored that into a budget, will be extremely vulnerable.

Between the Employee Retention Credit and John Podesta’s Clean Energy Innovation budget of $370 billion, I think the U.S. economy is doing just fine.

Bubble up the assets

then have people borrow against the new “wealth”

What could go wrong?

“Extraordinary Dillusions and the Madness of Crowds”

History is a lesson and precursor

…and demonstrates someone, somewhere, is always in a pickle…

may we all find a better day.

When the goblins come and you are stuck up a tree. That’s when you know you are out of the frying pan and into the fire. Pray for the Eagles to save you.

all this doom and gloom commentary is not reflected in the charts. hey maybe one day you’ll be right and can venture out of your ‘end of world’ caves and marvel at that yellow object in the sky. in the meantime there’s plenty of opportunity for those who understand that humanity spends more time muddling through changes of all sorts despite a long history of disasters. true alpha dogs are making lot’s of money right now. but being a doomer is a lot easier.

Re: all this doom and gloom commentary is not reflected in the charts

The chart that really, really confuses me today, is to look at the 30yr treasury price with the 30 year yield overlay, going back to about 2005.

We’re in a very precarious and super dangerous, volatile, risky period. Forget inversions or the delayed recession, the 30 year price dropping, is something that is very rare — which is happening as we speak. There’s not a lot of room for error here. I’m super aware of the delayed, lagging recession, but this is now!

I’m thankful to be in a ridiculously safe money market, licking my chops, while the alpha dogs are gorging themselves on AI risk exposure.

You have a point. 20 years ago when I was 50 I realized that trying to outdo the neighbor or so called friends with new cars, and big house was more misery than joy. Raised 4 kids in a real nice suburban home that had a lot of appreciation over 36 years. Room to borrow on HELOC for college help,and pay off the orignial mortgage. When I retired, realized that happiness is a ranch in the country, which is exactly what all that equity bought without a mortgage. This is the life, no debt and some country peace and quiet.

At this point, I strongly believe that there won’t be any significant foreclosures or delinquencies, because inflation eats it all away. In early spring under one of articles here, I’ve commented on here that based on what I saw on a local housing market, we would see a big spike in terms of Home Prices. And we did, in many places it established new historical highs. On national level it nearly did.

I strongly believe that official inflation figures are BS and part of the reason is so people don’t start hanging themselves, when realizing the seriousness of a situation. Within last 10 years, Imo US dollar lost 50% of purchasing power. As an example UPS Drivers will end up earning $170K salary by the end of their contract. Union asked for it, because people no longer have the same standard of living when they earned $85k per year just few years ago.

Heck, even congress no longer operates in millions territory, it became billions of dollars, whenever they fund any type of project. Even when hearing trillions of dollars being spent, barely anybody blinks an eye anymore. That shows me that government even got accustom to realities on a ground and see nothing wrong with it.

People simply don’t know how to properly define unsustainable, much less to begin to quantify the ramifications of such to its equilibrium. It’s possible many dont even care. My objective observation is the Fed has replaced organic Capitalism using its tools to create its inorganic business cycles starting lets say when we crossed the Rubicon to unpayable back debts maybe say around the Greenspan era lets say. And what do we observe? Every business cycle plays out in a boom/bust and every cycle is larger than the last. Nothing will change my view that this time will anyhow be any different. We have done things so ludicrous now no one back then would have believed what would come. The one thing I am unsure of is…are these boom/bust business cycles all planned and all that the Fed does now(their new mandate of precision maximized wealth transfer) or do we have such inept people in the Eccles building that our entire working population is at complete risk to this ineptness. I lean to the former, and expect a soft landing from their unpresedented everything bubble. Not.

Steve:

Start with the stone cold fact that NO ”observation” is or can be objective.

From that basic error of understanding, it is likely IMHO that you can begin to change your view(s) that nothing other than your increased understanding CAN change…

Good luck and God Bless,,,

I was referencing observing something objectively to draw unbiased conclusions, just to be fair. I should have said was not is. I assumed the reader would understand that point. There are always those that will point out semantics and grammar as faults but when I rant its just how I roll. Passion over perfection. Nonetheless thank you.

The trillions they printed – it was A LOT of trillions. They permanently distorted the US economy and the entire system.

Maybe not permanently, but at least roughly two more years of “above target inflation”. If they bring QE back, then they will have to adjust the inflation target higher.

””Long term”’ YES DC,,,

but nothing in the realms of the economy(s), finance, and money that Wolf’s Wonder doth describe and decipher for us SO clearly, etc., is or ever will be permanent…

Wolf, I have a question about our drunken sailors: How are they paying for these ridiculous student housing rental apartments in Florida and elsewhere, that look more like luxury vacation rentals? Is student debt sustainable and is the student housing industry in a bubble?

1. Student housing is a form of CRE, and it had its own bubble, and it’s not going to be spared the CRE downturn. Most of the student housing mortgages have been securitized into CMBS, CLOs, or are held by specialized firms, mortgage REITs, etc. and so the losses will hit investors, not banks.

2. I don’t even consider federal student loans “loans” anymore, because no interest has accrued in three years and no one has made any payments, and a bunch of them have already been forgiven in various piecemeal programs — and I’ll stick to that until I see actual payments being made in large numbers. And then, only those loans that payments are being made will be “loans” in my book. The rest will be grants.

3. I have no idea how students pay for this type of luxury housing. I mean I kinda know: student loans, boomer parents that spoil their kids, grandparents…. We used to live in unspeakable dumps if we lived off campus (which I did), and dorms were spartan. So this whole thing about students being relatively well off, and living in a cradle of luxury, rather than being steeped in abject poverty, is fascinating to me.

…sounds like there are a lot more ‘trustafarians’, or similar these days…

may we all find a better day.

Student housing reminds me of Olympic villages, built by governments to house super cool athletes who require the very best conditions— Greece, Russia, etc, build magnificent structures, which eventually fall into ghetto like state.

The investment games and excessive corruption in building fantasies is absurd, wasteful and at the heart of student debt and the excessive illusion being sold as investment opportunities.

The vast majority of students are living off parents, who have seen excessive stock market gains during Zirp. The lesson here is to invest in stupidity and ignore reality.

One of the reasons that foreclosure statistics *look* fairly low is that mortgage issuers Fannie Mae and Freddie Mac since 2015 are selling their NPL (non-performing loan) portfolios at auctions. And charging the losses against the profits/dividends that FNM/FRE would otherwise have to pay to the US Treasury as part of the 2008-era bailout.

Here is a link to the Fannie Mae version of this process, Freddie Mac has a similar one (just d a search).

https://capitalmarkets.fanniemae.com/whole-loan-sales

Nope. Zero to do with foreclosures. Selling nonperforming loans is routinely done to get them off the balance sheet. Banks do it all the time. It doesn’t change anything about foreclosures because the buyer is going to foreclose on the property if the delinquency doesn’t get cured.

Foreclosures happen when the holder of the mortgage — regardless of who that is — cannot see any other way out than to take possession of the home, sell it at a foreclosure auction, and hope that the proceeds will cover most of the outstanding mortgage and interest.

Housing credit is pristine. 90-day delinquent mortgages — after which the lender starts to entertain what to do next — are just a hair above record lows, at 0.46% of balances, which is why the next step, foreclosures, are near record lows.

I will correct myself:

“One of the reasons that DELINQUENCY statistics *look* fairly low …”

I agree, it was wrong of me to say “foreclosures” when I meant delinquencies. Most of the stats being bandied about are delinquency stats, not foreclosure stats.

What is not so clear is why the NPL/RPL auctioned loans have lower foreclosure outcomes than control groups. Maybe it is that part of the discount provided to the NPL mortgage buyers must be passed on to the debtors as a reduction in mortgage balance. I could not figure it out. There is some more info at

https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Releases-Latest-Report-on-Non-Performing-Loan-Sales_12212022.aspx

I’m going in circles, probably posting too much, but it’s fascinating looking at mortgage rates, 30 yr treasuries and various spreads. A mortgage is now about 7.62 and who the hell knows what Prime is?

The drunken sailors, and all their blessed resilience and extended QE magic tricks and denial, resistance, stupidity — are going to have to accept that the train, is off the tracks. We are in a recession that’s being managed by statisticians, who are working tirelessly to create an illusion of extraordinary prosperity.

If history is in any way useful for looking at stress in the economy, it’s useful to look at relationships with treasury prices and yields. There’s no way an AI groupie can explain away the current level of risk, other than pointing to statistics that suggest, food prices are low, unemployment is low, wages are screaming higher, rents are falling, home prices going up, income heading higher and of course, deficits don’t matter and we’re in a strong recovery, with resilient consumers, who don’t have debt — because pandemic stimulus has goosed the economy into an amazing state, just before an election year. Furthermore, banks are super strong, because all their long term treasures, like the 30yr, aren’t going down in value …

Frying pan pattern with a broken handle?

I thought the head and shoulders pattern was silly.

When did broken cook ware enter the economics charts?

Is Tupperware next? Is there a “lettuce keeper” top waiting for us around the next rate hike?

I’m starting new trends here all the time. This is one. You’re going to see a lot more frying pan charts here. And if I’m lucky, they will spread, as have some of my other trends.