What’s easier to see in this scenario is more persistent inflation.

By Wolf Richter for WOLF STREET.

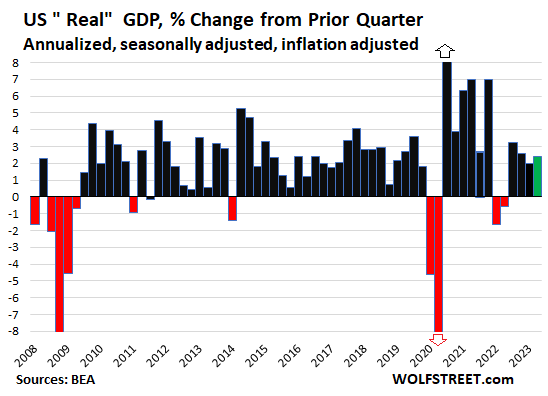

GDP, adjusted for inflation (“real GDP”), jumped by 2.4% in Q2 from Q1, following the heavily upwardly revised 2.0% increase in Q1, according to the Bureau of Economic Analysis today. All major categories, adjusted for inflation, increased:

- Consumer spending rose by 1.6%, after the upwardly revised 4.2% surge in Q1.

- Government spending rose by 2.6%, driven by surge at state and local governments.

- Gross private investment surged by 5.7%, the biggest increase since 2021, after a series of big drops, including an 11.7% plunge in Q1. That was a huge swing, driven by nonresidential investments.

- The trade deficit got a little less horrible, on a big drop in imports. So it subtracted a little less from GDP.

- Change in private inventory investment added a hair to GDP (+0.1 percentage points).

“Nominal GDP” (not adjusted for inflation) jumped by 6.3% to $26.8 trillion annualized. This is the actual size of the US economy, expressed in “current” dollars. By contrast, “real GDP” (the inflation-adjusted figures here), expressed in “2012 dollars,” came to $20.4 trillion. All figures below are adjusted for inflation via 2012 dollars.

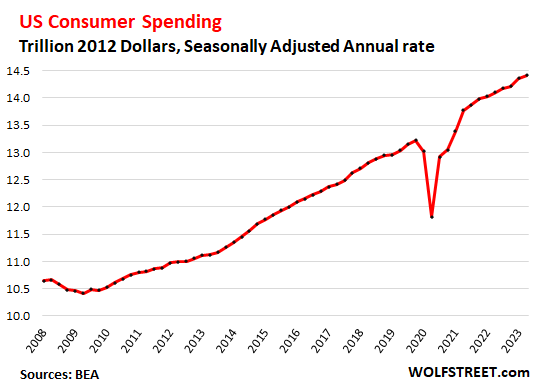

Consumer spending on goods and services rose by 1.6% annualized and adjusted for inflation, after the upwardly revised 4.2% surge in Q1. So average them out, and that’s where this is going. Consumer spending accounts for 70% of GDP.

Year-over-year, consumer spending rose 2.3%, adjusted for inflation, which is above the 2019 growth rates and right in the range of the Good Times years before the pandemic.

Spending on goods still rose at 0.7%, after the 6.0% surge in Q1, despite the massive shift of spending from goods to services.

Spending on services rose by 2.1%, adjusted for inflation, with consumers easily out-splurging inflation in services (with “core” services CPI at 6.2%!). Spending on services accounted for 62% of consumer spending.

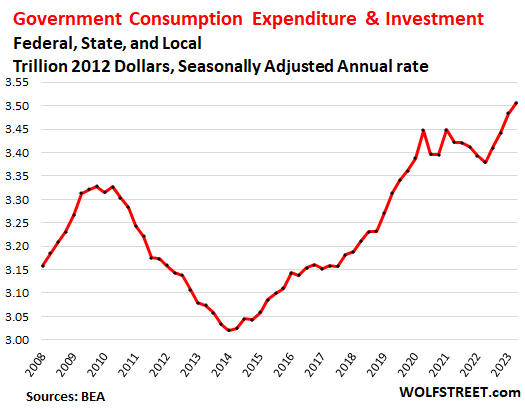

Government consumption and investment rose by 2.6% to a new record, and the fourth quarter in a row of increases, after five quarters in a row of declines.

- Federal government: +0.9% (national defense -1.1%, nondefense +2.5%).

- State and local governments: +3.6%, driven by an increase in wages for government employees.

Government consumption and investment does not include transfer payments and other direct payments to consumers (stimulus payments, unemployment payments, Social Security payments, etc.), which are counted in GDP when consumers and businesses spend or invest these funds.

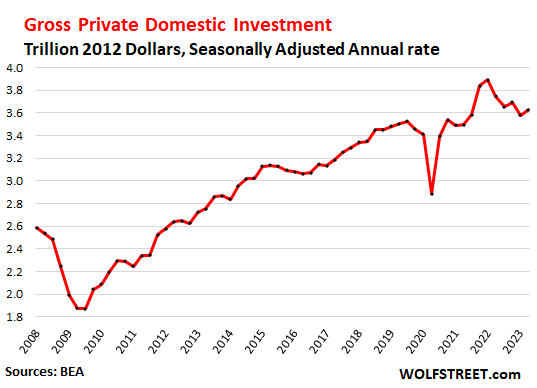

Gross private domestic investment jumped by 5.7%, after the 11.9% plunged in the prior quarter. The plunges in the prior quarters had worked off the entire pandemic spike and overshot on the way down, which had dragged down GDP. In Q2, investment perked back up, heading back to trend.

- Nonresidential fixed investments: +7.7%:

- Structures: +9.7%.

- Equipment: +10.8%.

- Intellectual property products (software, movies, etc.): +3.9%.

- Residential fixed investment: -4.2% (-4.0% in Q1, -25.1% in Q4).

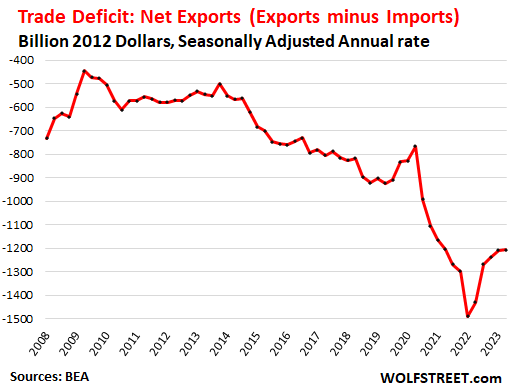

The Trade Deficit (“net exports”) in goods & services got a little less horrible:

- Exports fell 10.8%.

- Imports fell 7.8%.

Imports subtract from GDP. So falling imports in Q2 boosted GDP. Exports add to GDP. So falling exports subtracted from GDP. On net, the trade deficit – the negative “net exports” – is a negative for GDP. In Q2, it was just a tad less horrible than in Q1, so it subtracted just a tad less from GDP.

The massive trade deficit during the pandemic was caused by a historic stimulus-driven buying binge of goods in the US, a lot of which were imported, or whose components were imported. The trade deficit is now back to its normal horrible trend:

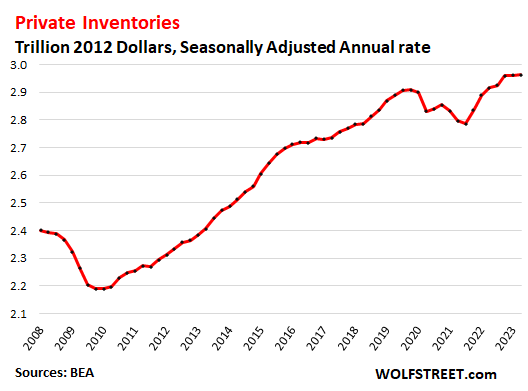

Change in private inventories added 0.1 percentage points to GDP. Changes in inventories count as a business investment. Inventories ticked up just a hair in Q2, to $2.94 trillion, in inflation-adjusted dollars. You can see the inventory shortages that had caused a spike in goods inflation and that ended in the second half of 2022, when restocking efforts began to bear fruit:

A slowdown is hard to see here. Inflation is easier to see in this scenario. When business investment takes off like this, and when government spending, particularly on government employee wages, surges like this, while consumers are still in party-mode and are outspending inflation without breaking a sweat, and are out-earning inflation, then it’s really hard to see an economic slowdown or a recession. It’s just not lining up.

What is a lot easier to see in this scenario that we now have before us is more persistent, inflation.

This is Fed Chair Jerome Powell’s reaction when he saw today’s GDP report, as captured by cartoonist Marco Ricolli for WOLF STREET:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Based on these numbers, would you say Pow Pow has failed miserably so far in taming inflation, or are we witnessing the greatest lag effect one has yet to be seen in recent history?

Or perhaps Goldielock scenario? Recession avoided, the market can absorb QT and higher and longer interest rate and still party on, and somehow asset price will come back down to earth (especially looking at housing) and inflation eventually normalize back to 2%? Such a strange time we live in, hard to make sense of what’s to come…

PPP money everywhere sitting in reserve in some cases. This is the biggest contributor to inflation I see. Tough to make real money in this crazy environment. This will last much longer based on the slow draw down of all PPP monies.

PPP was $800 billion. In terms of dry powder for consumer spending, it’s dwarfed by savings deposits (about $10 trillion), money market funds (about $7 trillion), plus tens of trillions of $ in brokerage accounts and Treasurydirect. Consumers in aggregate have a huge amount of wealth that they can spend if they want to.

Cool, guess we just have to get used to 4-5% inflation per year as the new norm…first crazy A$$ asset price for the last decade and now sticky inflation for maybe the next decade…man these new norm sure do suck for your non 1% percenters…

Wealth is real stuff. If consumers have been “given” some more bits in their electronic ledger but they can’t all exchange those bits for real goods, is it real wealth?

We have inflation because the govt allowed the rate of fiat creation to exceed the rate of real wealth creation.

Same for housing, you can exchange it for another overvalued house, but all owners cannot collectively cash out and into other real goods, because they don’t exist. This is why boomers can’t downsize en-masse.

People, even affluent people, generally have to work or take risks to acquire their savings. PPP/ERC is free money. Psychologically there is a huge difference. Many who wouldn’t think of splurging with their hard-won savings would be a lot quicker to spend a windfall that hit them as a lump sum.

Average core CPI 1971 to 2022 is 3.90%. Powell wants it down to 2%. Good luck with that.

Wall Street Journal is hiring lolololol….

Hard to get my head around many assumptions that used to make money but no more….

Got to agree with Wolf here. Here’s a personal case study that fits with the spending if coming from savings line of thinking (experience from the US).

During the pandemic we accumulated substantial savings – no daycare (closed), no commute (WFH), no traveling, dinners out etc. (all closed/canceled). My better half and I remained employed throughout. So now we have 2.5 years of excess savings and that is being spent. Vacation (first in 3 years), much needed home renovation, etc. We aren’t going into debt with this spending and I expect we won’t be so prolific next year. But I do wonder how many others are in a similar position where they remained employed during the pandemic, saved and now are spending that surplus.

So who’s gonna spend that wad anyway? Will the boomers go out in style or leave it to the millennial inheritors to blow? Maybe what we are looking at is the Mother of all Dbl Tops if boomers decide to cut back as retirees do after the big fling… Interesting times.

I think interest rates are not coming down anytime soon.

Pea sea LOTTERY

I agree that they will not rapidly fall unless there is a crisis.

But I think there is a rather excellent chance we will see a crisis and these higher interest rates *could* actually contribute to its creation.

No good choices/no good outcomes.

Recession avoided? We already had one in 2022, clear as day on the chart above.

No we did not have a recession in 2022. It’s not a recession just because YOU call it a recession. In the US, the NBER calls out a recession, and a recession is a broad economic decline, including in the labor market. The NBER has been using that definition since before I was born, which wasn’t last year.

What caused the negative GDP readings were:

1. massive IMPORTS, as companies tried to deal with the inventory shortages and meet consumer demand for goods; imports are deducted from GDP.

2. and the resulting changes in inventories, which also lowered from GDP.

This happened in a historically tight labor market, historic low unemployment, amid strong demand, consumer spending growth, and business investment.

I covered this at the time. You should have paid attention. People who say that the definition of recession was changed are ignorant. I cannot believe people still post this BS.

Gosh. It seems the Fed should be able to increase the rate of QT without driving the economy back to the Stone Age.

Good point, if normalizing the Fed’s Balance Sheet is a goal, as stated by Powell just yesterday, then why not?

What better way to tamp down “Irrational Exuberance “ as being seen this year?

BTW, their QT has remained below their “target reduction pace “ because MBs principal pay down has dried up. So at the least they could sell MBS or accelerate the Treasury drawdown to make up the difference

I agree. I wouldn’t want the Fed to hike by 5% and dump $5T off the balance sheet by the next meeting, but it seems like they could go a lot quicker. I would think they could accelerate balance sheet shrinkage by 50% and the economy would barely shrug its shoulders. Heck maybe they could double it before the economy would start to show significant signs of slowing. Our economy is barely batting an eye at the current rate of roll off. Interest rate hikes hit different parts of the economy very unevenly. If we really want to slow inflation, remove money from the system. Consumers can’t chase price increases if the extra cash doesn’t exist to chase those prices.

They won’t. For all their talk of the risk of doing too much tightening and of doing too little, they are quite nakedly terrified of doing too much. That fear is in their blood as an institution. They will always tend to err on the side of doing too little tightening.

(That they always err on the side of doing too *much* loosening when the time comes to loosen goes without saying around here, I hope.)

“they are quite nakedly terrified of doing too much”

I’m not fan of the Fed/DC (decades of unaddressed policy failures have brought us here) but the Fed knows better than anyone the accumulated, always-close-to-collapsing cumulative liabilities this country has.

They *are* scared crap-less of doing too much (otherwise they never would have choreographed essentially 20 years of ZIRP).

But the fundamental problems of the US economy can’t be fixed (then, now, or ever) by Fed green-paper-shuffling (20 years of ZIRP proved that too).

So the Fed/DC does indeed always prefer easing/slow-walking-absolutely-unavoidable-tightenings.

It is hard for DC for escape blame for huge unemployment (unfairly, ironically) but they have been successfully framing inflation patsies for *decades* (again, unfairly).

Add that to the fact that DC is the biggest debtor there is (or ever will be) and the money printer becomes DC’s only altar.

We will have another financial crisis and soon, the only question is what “crisis” they gin up to cover all their money printing.

Many of us have been arguing for this for many months. If it can be created in an instant why can’t the band-aid be removed more quickly? Hell, at the very least follow the plan and remove the $95 billion per month.

Withdrawing liquidity too fast causes a leverage financial system to collapse instantly. It’s that simple. Just the threat alone would do it. The question is: what amount is safe?

Wolf, could you please do a post on why the financial system is so vulnerable to a withdrawal of liquidity. Or have you done one already?

Absolutely it could, but they want to keep balance sheet policy in the background while rate policy takes center stage. Fed Dogma 201.

Absolutely, they should double what they are doing, it would make a big difference and would erase the stupidity of QE faster.

I dont understand the comment about business investment “taking off like this”, when gross private domestic investment chart shows a decline over the past 5 quarters (ticking up at the last reading, but still in what looks like a downtrend)?? Private inventories are also flatlined, which is actually down quite a lot from the previous trendline.

Government spending seems to be the only chart that is growing faster than previous trendlines. Isnt this what has really driven every bit of strength in this economy, government spending and Fed balance sheet?

American Express reported sales across their network was up 8% year over year versus approximately 13% for the previous quarter. I see a definite slowdown in spending here taking shape.

I saw a chart that showed the “excess savings” following the handouts and it looks like we are six months away from being back to zero in excess savings.

State and local governments are spending money from the federal government, but many will be forced to cut spending.

Just wait for the stock market to tank again, hitting a new low. That will crush all this spending. Real estate will also need to head down and that will help to kill the over-spenders.

Energy prices are headed much higher due to supply issues. Combine that with higher rents and you have a toxic formula for higher long term interest rates.

We are no more than one year away from real pain in my opinion, based on the trendlines.

“I dont understand the comment about business investment “taking off like this”

Residential fixed investment has been the only weak component, which plunged in 2022, and we saw that in other data. It still declined in Q1 and Q2 but at a much slower rates.

But nonresidential is the growth engine here. It hasn’t declined since 2020. On the contrary, it put in a lot of big quarters. And in Q2 it surged 7.7%, with structures being super-strong over the past three quarters, and equipment knocking it out of the ballpark in Q2. IP has been growing every quarter since 2020, and often at big rates.

So all it takes is for residential to be less weak, and overall investment surges (+5.7%), driven by nonresidential.

1. Concerning American Express: You’re calling an 8% increase a slowdown? Are you drunk?

Also check out Visa, which has a much bigger card business than AX. Its growth is in the double digits. You’re gonna call that a “slowdown” too? What are you drinking? Send me some.

2. These articles about “excess savings” being used up are ignorant BS, and I’m getting sick of this shit getting cited here over and over and over again (and I have wasted countless hours shooting it down). This “savings” is NOT savings, it’s NOT a stock of money, but a FLOW of money. It’s the mathematical difference between disposable income and consumer spending. And it doesn’t include capital gains.

If you want to know what consumers ACTUALLY have saved (their stock of money that they can draw on), look at the $10 trillion in savings deposits (CDs and savings accounts), $7 trillion in money market funds, trillions in Treasury securities, tens of trillions in brokerage accounts, etc. That’s consumer savings. I’m getting deadly tired of this dumb BS that consumers are poor, used up their savings, or are tapped out. People who cite this BS will never understand the US consumer and the US economy.

Wolf, those are massive savings numbers in aggregrate. Apologies if you’ve touched on this previously, but who owns the savings? Ex., is 95% of it held by the wealthiest 5%? How close to broke are the bottom 10%? 20? 30? Even if aggregate savings is massive, the distribution is also key. I’d love to hear your thoughts on it!

I cover that periodically. Wealth = assets minus debts (Federal Reserve data):

Bottom 50% hold $4.5 trillion in wealth.

Next 40% hold $39 trillion in wealth.

Top 10% hold $75 trillion in wealth

To understand the economy, you have to understand the overall wealth of consumers. The homeless people will never move the economy needle. The big spenders move the economic needle. The top 50% in the US have a lot of wealth.

Story came out recently about a bill in the works to lower fees or create competition among the credit card companies.

Can they buy their way out? Or will their stocks get dinged?

We shall see.

Here’s my 3rd comment on this article so far, so this is my last one for a while as not to overdo it.

Per FRED, both the personal savings rate (PSAVERT) and the savings rate as a percentage of disposable income are near all time lows. Only 2 times were lower since at least WWII… The depths of the GFC and the very recent late-pandemic low in Q2/Q3 of 2022. The savings rate spiked off the charts while money was being pumped into the system faster than it could be spent. But consumers are still spending their money like its burning a hole in their pockets, not saving it. This hot economy is not driven by savings spent or real productivity gains… It’s being driven by gov spending, period. Deficit spending is now the beating heart of our economy. At -$2T/yr or more in deficit spending, eventually the number of buyers willing to put their cash into gov debt will start shrink, and the gov will be forced to choose between skyrocketing interest burden or QE again. They will choose QE in the next downturn. Maybe not tomorrow, maybe not this year, but eventually they will.

“when government spending, particularly on government employee wages, surges like this”

This is where I see government debt issuance to be net inflationary in this crazy economy. When the gov issues bonds, it sucks liquidity out of the system in the short term. However, the money used to purchase bonds often tends to be money that wasn’t previously moving, not changing hands much out in the economy to juice purchases of goods and services in the first place. It comes out of pension funds, rich folks that were sitting on cash, people’s savings, and the like. The gov takes that low velocity cash, then turns around and spends it on salaries, contractors, programs, as well as paying back the debt with interest. That previously stagnant cash is being put directly back into the hands of consumers who gladly go out and chase goods and services with it (heavy on services now).

Maybe I’m way off and not realizing it, but it certainly seems like the tsunami of gov debt could be inflationary in this way.

Agree, government deficits are the primary source of inflation, and those deficits are increasing. The problem is supercharged when the Fed simply prints the money, via its QE program, to fund those deficits.

If inflation abates going forward, it’s only because we have strong deflationary forces in our economy, such as oligopolies and wealth concentration, which will ultimately destroy the system.

The Federal Reserve NEVER did that with QE as to deficits. Doing so is know as MONETIZING the Federal Debt and the Federal Reserve simply never does that at all in the US.

Your comment doesn’t even qualify as sarcasm anymore. Everybody knows the Fed is monetizing the debt.

The only question is, when will Wall Street quit pretending monetization isn’t happening? Perhaps when the masses figure out the monetization game and start revolting against the overwhelming asset and CPI inflation.

Give me a break. Powell announced unlimited QE on March 23, 2020, and Congress passed the CARES Act on March 25, 2020. The CARES Act authorized $2.2 trillion in spending, and the Fed printed more than $2 trillion in the two or three weeks after the unlimited QE announcement.

You connect the dots. Don’t play dumb.

@ Einhall –

I thought Wolf has confirmed that we are operating under QT

They’re talking about the past… 2020/21.

You 2 guys win the steak dinner. Inflation and drunken sailor spending is because of gov’t deficit spending. The gov’t sector is now close to 50% of GDP, when you add federal, state and local. Until they stop borrowing and spending with no limits, that becomes binge consumer spending.

Think about it. Half the economy. The other half is being taxed to support this monster on our backs. But it’s not that simple, because it’s also 10s of millions of make work jobs, welfare payments, etc…

And gov’t will increase their borrowing/spending as fast as they can because it’s a direct add to GDP, which makes them look like they’re *doing something*.

I’m thinking the same. I posted a few weeks ago that government spending (Federal, State, and Local) is over $10T a year. It’s a huge component of GDP. They can print/borrow and spend and make GDP go up so I don’t really have much interest in GDP anymore as a useful tool to watch. It’s basically just govt spending indicator now to me at least.

I used to believe in “don’t fight the Fed” since late 2021 when they announced QT and rate hikes, but seeing Congress spend and spend (and Biden forgive loans) I don’t think it’s as useful either as in the past. Now I will just watch liquidity flow collectively from Fed and Treasury/Congress and if that has net outflows into economy then I expected more inflation and falling productivity. A government deficit ends up as a private sector surplus…

The consumer is gripping the punchbowl with both hands, and will fight the Fed for it.

And the corrupt gov is putting the money in their hands, directly/indirectly. I believe this is similar to the late 70s early 80s. Volker, fed chair, was fighting to bring inflation down. Who was he fighting? The gov.’s spending.

But he had Reagan approval,noe fed president is a political pawn

The current sentiment is essentially whine about prices, then shrug shoulders and pay the absurd prices anyway.

The American consumer is a financial bonehead.

The only exception to this was eggs. Despite everything else out of control, people really lost their damn minds when eggs spiked to $4 / dozen. Queue massive buyers strike followed by a sharp plunge back to reality.

If only everything else that consumers are being gouged on was treated the same way.

I can’t speak for others, but I refused to buy a new car over the past 2 years while manufacturers were charging above MSRP.

I also stopped buying soda when Coke raised the non-sale price of a 2L to $3.59.

I’ve gone further than that.

I quit buying packaged drinks altogether. I drink filtered tap water now, feel a lot better, and have lost weight. Never going back.

I haven’t bought a new car in 8 years, have zero car payment, and reliably get to anywhere I want to go.

I quit Pepsi ,also no chips but they put chips on sale a lot gotta keep warehouses working and manufacturing

Oh yeah same here. At the upscale grocery where I wear a suit and tie to, ginger ale is $8.99 a 12 pack! I think it used to be $3.99.

I usually shrug at the groceries and say “I didn’t get all dressed up for nuthin’ “ but not this time! No thanks Big Cola!

42yo father with spouse, one 8yo child. Never bought a new car, never bought a house, zero debt, international professional engineer, and manage spending diligently. Until other consumers follow suit, I feel like I’ll never be in a position to change any / all of the above (out of want or necessity). How have I not been scammed?

Howdy Folks The Nobel goes too? The Cartoonist Marco.

Can we rent him for birthday parties?

The cartoonist I mean. Powell seems busy.

Don’t Fight the Ignorant Majority.

No, don’t fight the ignorant majority, take their money, Har Har Har 😛. It’s the American Way!!!

Nice move on the 10-year rate today. Perhaps the bond market is starting to worry about Powell’s inflation fighting conviction. He’s been slow-walking QT, and still refers to QE as a valuable tool.

Perhaps we should start directing our inflation complaints to Wall Street, which appears to be the head policy decision-maker.

All Treasuries from one month to thirty year are yielding over 4 percent. Today’s economic data are just too strong to ignore.

Well the Fed funds rate today is just a smidgen over the average 1971 to 2022, and the 30 year fixed rate mortgage is actually a little less than the average 1971 to 2022. I am not sure why Jerry expects to lower inflation with an average fed funds rate. Higher, longer. If he wants to get to his magical 2% inflation rate, then much higher, much longer.

Wouldn’t it be just the opposite? If the bond market thought Powell would resume QE, the yield on the 10 year would DROP.

At a time when deficits are running hot at 6% of GDP, QE is money printing. The higher money supply leads to inflation and higher interest rates because an inflation premium must be priced into LT bonds.

Look what QE did during the pandemic. Inflation went up 20%, leading to increases in interest rates. LT bondholders lost 40%.

Right, but if you are convinced QE will restart, then long term yields would drop, as you’d be able to sell those bonds to the Fed for a capital gain.

I mean one could argue it was the interest rate suppression since 2008 that caused the fever we are seeing.

12 years of damage that was uncovered by the pandemic/Covid blow.

If Einstein was correct, it will take another 12 years of the opposite policy to get back to normal.

Also what was gained during the 12 years of no inflation? You have to factor whatever that is, into the here and now.

Anywho. :)

There was a lot of good news today.

The recession never came. The inflation was never low, it was always high.

I’m broke and I’ve been missing out all my youth.

I’m joining the party.

Fire up those machines, I’m coming to the bank tomorrow. Yacht boat car house is on the menu! Max that loan out Powell! I’m going to get rich with that FED money!

Just raise taxes: This time the business, government, etc economic spending problem isn’t really Jerome Powell’s Federal Reserve fault. The problem is with an imbalance of taxation to business profit problem. The Federal government is running large deficits while the businesses are awash in cash, just look at those record profit percentages. While increasing taxes on business may not completely cure inflation it would certainly be a help with fewer treasuries being sold. The other alternative is if world economic events make US treasuries unattractive thereby forcing political special interest groups to accept proper taxation.

Howdy Gary. NO Thanks….

They can only raise tax on the wealthy, and they run the government, so …

Instead of pulling his hair in that fine picture by Marco, Powell should be pulling a Volcker.

MW: Breaking Dow falls 230 points, stocks drop as Treasury yields climbs above 4%

Month end profit taking.

Nice pump ‘n dump action today in the US stock markets!!!

Another great unmolested heart felt sermon on the state of our economy from Wolf street. It’s almost looks if Fed and congress built a monster back in March of 2020 that is now out of control. Cycles of boom and bust are just part of life. I don’t really see a slowdown in consumer spending in area of services, airlines, hotels, restaurants, entertainment venues, concerts, Disney World will continue to see high demand. My local McDonalds ice cream machine is broken again, don’t understand why they forgo revenue’s with this repetitive failure. Yet Billions Served?? Maybe AI will solve this problem.

Unusual day in the market. Lot of selling, especially into the close and on a day GDP surprised to the upside. Long bond took a swan dive (holders of long bond are wierd).

Might be one of those days where people on the wrong side of the interest rate bets are selling anything they can sell in order to pay their bills. I can’t find any systemic risk in U.S., Europe, or China so I bought and bought and bought into the close. I hope Putin doesn’t launch nukes tomorrow!…Har Har Har 😛

A lot of traders trade by the month selling to lock in gains for the month.

Thanks Real Tony,

I don’t know what was going on today but I will find out over the next few days….

The market is still surprising me so I trimmed back on the first bounce this morning to a more manageable risk level. I still expect a second and bigger bounce later today but there must be short term things going on that I do not fully understand. I am still guessing it is bond losses and fear of future bigger bond losses that is driving this ‘screwiness’ in equities.

Okay, I surrender: all the money in my mattresses is going into junk bonds and tech stocks, and I’ll whistle whenever I pass a graveyard. There’s no stoppin’ this train!

Looks like WR is the only one seeing this unbridled spending.

FED does not see this and think everything is going in the right direction.

Don’t go by what Powell/Fed said ( I think they put out Dovish statement ) but go by what they are doing.

Yesterday, instead of hiking by 50bps and creating a small shock, they decided to hike by tiny 25bps and put out a dovish statement.

FED/Bernanke used to tout about “wealth effect’ to encourage spending.

Powell never says anything about lessening wealth effect to curb spending and thus curb inflation.

Thank you WR for this report and putting up with my views despite not matching with yours!

The Fed sees it just fine. The problem is that you’re putting earplugs in your years when Powell talks and then you say that he said the opposite what he actually said. This has been your schtick over the past few months. I don’t know what triggered that. So now you keep coming up with this goofball BS.

“Don’t go by what Powell/Fed said ( I think they put out Dovish statement ) but go by what they are doing.”

Yes, we go by what they’re doing: they hiked by 525 basis points, in 16 months, the fastest in 40 years, and they slashed their balance sheet by $722 billion, the fastest in history. That’s what they’ve HAVE DONE. And they keep doing it. And you just refuse to see it, and post goofball BS here.

Right now Powell shouldn’t even be thinking about thinking about talking about lowering rates, ever. “Rate cuts” should not be part of his vocabulary, period. Not “could happen” and not “normalization” as if ZIRP is normal. Not a year from now, not ever. He should shut down all questions about rate cuts, and never leave openings for rate cuts being a possibility any time in the foreseeable future. THAT would be honorable and hawkish. But instead, he ALWAYS leaves that rate-cut carrot on a stick in ALL of his communications, which is dovish.

Just by equating the term “normalization” to low interest rates, he constantly shows his hand… He wants to return to low rates and will do so as soon as the “incoming data” can be interpreted to support cuts. That is the goal of the Fed. If the goal was truly price stabllity, then rate cuts would be “off the table” and incremental acceleration of QT with rate hikes as far into the future as needed would be the minimum measure of what is “on the table.”

I’m so gosh darn tired of Powell tip toeing around with all of this soft language signifying nothing, told by a Fed chairman with not even an iota of sound and fury.

I think Powell has to say what he has to say, which first and foremost is, we’re pursuing a 2% interest rate. Lower interest rates in the future implies that we will reach that 2%.

Can you imagine what happens if he says, “we’re giving up the ghost, and it’s going to be 5% inflation from here on out”?

Nobody is going to buy our debt, at least, not at the interest rates we’re getting on long term treasuries.

That said, my takeaway from Powell is, the Fed thinks the economy is still overheated. And GDP numbers seem to confirm that. So, they hiked.

It doesn’t matter how much people twist what Powell says. Wall Street is fighting the Fed because it thinks it can make money that way and sucker people into it, and it will lose. It will just take a lot longer, with much higher rates, and ultimately more bloodletting. Don’t fight the Fed, no?

I get really tired of all the inane bullshit that people, bloggers, and hedge-fund-manipulators on CNBC and Twitter say Powell said, when he said in fact the opposite, or that he was “weak” or “dovish” or some such bullshit. Just inane fabrications designed for morons to swallow hook line and sinker.

Powell is a political guy; that’s why he is where he is. 2024 is a presidential election year. That’s why Wall Street is convinced that rate hikes are over for now. The strong economic data this week indicates that inflation has the potential to reaccelerate; that’s bad news for the bond market. If the bond market crashes and rates spike and/or regional banks start to wobble from duration and CRE exposure, QE will be back on the table in a flash, which will be good for stocks. A big sell off in bonds might be coming in September-October, when vacations are over and everyone starts paying attention again.

Occam,

If you say, “Powell is a political guy,” you have to add that he is a Republican, first installed by a Republican President. So he would not try to help a Democrat win reelection.

I’ve been hearing for a year or more that consumers spent all their savings, maxed out credit card debt etc and yet it looks like they find ways to keep spending. Is there a way to find how far they are from the end of the line? Wolf’s comment above about tens of trillions suggests there’s no such thing in practice as the end of the line. Is it the case?

I just replied to this type of question several times. Here is one of the answers:

In terms of dry powder that consumers can spend (wealth = assets minus debts):

Bottom 50% hold $4.5 trillion in wealth.

Next 40% hold $39 trillion in wealth.

Top 10% hold $75 trillion in wealth

To understand the economy, you have to understand the overall wealth of consumers. The homeless people will never move the economy needle. The big spenders move the economic needle. The top 50% in the US have a lot of wealth.

So you’re saying we’re in ultra ultra ultra discount coach class on the “economic flight” we’re all aboard. ;)

“Now boarding ultra ultra… nevermind you know who you are. Get on the plane now.”

Why do they have to spend from just savings? People get pay raises. I know lots of people getting raises via either job change or current employer trying to retain and they are spending their higher paychecks. Wages up…spending up…prices up. These aren’t low pay hourly jobs either like fast food or retail. I’m talking about a hospital tech getting $30k raise to stay, another nearly doubling salary ($90k to $180k and they just bought an M3 for fun) going into medical sales/rep. These are not locums traveling nurse temp pay increases, but fulltime permanent. If I get a new job next year, I’ll probably spend more of what I make as well.

Prices go up faster than wages. That’s inflation. Wages have not kept up with inflation in over a decade. Every year an workers wage increases less than the inflation rate he gets poorer.

What you have is a Gov’t handing out money in entitlements that are actually increasing faster than real wages. until the Gov’t spending is constrained there will be no reduction in inflation.

It is the primary job of Congress to run the budget for the USA. They have failed this one task for multiple decades. We have not had a fiscally responsible Congress in over 20 years.

The USA has not had a fiscally responsible Congress for the entire time the USA has been a country which is now 247 years.

Me niece traveling nurse to travel been to Australia,Thailand Croatia . This is just a few when see comes home stays at moms house free . 32 years old no savings no house old car only cares about experiences. As she says I’ll inherit my wealth

I’ve seen no raises since 2016.

Sucks. My bills have gone up prob $40-60k in that time. Have been in “saving mode” since 2021. No luxuries, just trying to maintain. Used to feel like a king back in 2009-12. Now feel pretty squeezed.

I’m not seeing any pay raises around the country for the field though. But anyway maybe industry wide raises for contemporaries will come.

I read a bunch of newsletters regularly. For a long time, they all said that deflation and stagflation were going to be bad. No one is saying that any longer. To be fair to those writers, the stimulus activity was a bit too big. To be fair to the stimulators, no one knew how much to give out. We can’t go back in time and blaming is pointless. But is there any possible argument to be made for stagflation, today’s GDP aside?

Everything is cyclical and we are already seeing lots of deflation.

Mr Powell has bravely raised real rates to almost zero after inflation, with a speech that would have been regarded as highly dovish in any other era.

No wonder those with cash are trying hard to spend it before prices go up more.

This is just anecdotal evidence of the state of main street and the middle class. I recently went to my local Diner for my usual breakfast once a week. It used to be packed on weekends so I went during the weekday when it was not crowded. This time on a Wednesday it was packed. Barely able to get a table. Wolf is correct. People are spending like drunken sailors. Next time the diner will probably have a line out the door.

Lots of new money coming to savers, mainly boomers, who were getting 1% last year on savings. Now getting 5.5% in T-bills. At least $40,000 more per year for me. Well, we have been getting screwed on yields since 2008.

If you’re spending all that nominal interest, then in real terms you’re drawing down your principal by an amount equal to the rate of inflation. I suspect a lot of people ate doing that, in which case much of this drunken sailor spending is coming out of savings, in real terms.

Well, if you’re retired, you’re supposed to eat up your assets. You can’t take them with you, so you might as well. You might leave some to your kids, but you probably gave them enough already. Might as well enjoy the years you have left. That’s what retirement is all about, if you’re lucky enough to have assets (many retirees don’t or not nearly enough).

The major money center banks such as JPMC and WFC are not increasing any interest rates on accounts paid to savers. They are drowning in excess money and have very few to lend it to and they are not about to pay higher interest rates to savings accounts.

WFC offered existing customers 4.3% CDs because it wants their cash, or wants to keep their cash, and is willing to pay for it. Not drowning in excess cash. Even JPM is out there selling 5%+ brokered CDs because it wants cash, so not drowning in cash either, but it still is ripping off its existing customers with 0.1% rates.

Exactly. You should have been getting 20k a year for 12 years. But you got zip.

Who knows what that would be with compounded interest. (Cuz I do not know what you started with or added)

Is it true that the aggregate value of the US Stock Market is about $45 tril?

US Residential RE equity is about $30 tril?

I know people hold $$/assets elsewhere but I’m just saying that if we go down 20% in each of these 2 markets that’s $15 tril, wouldn’t that more than account for all the printing that has been going on?

Where do you get the false notion that there has been any ‘printing?’

QE involves the Fed creating dollars to purchase assets, colloquially known as “printing.” Of course most dollars aren’t actually “printed” today, is that your point?

Yep exactly, people always say “they printed money”

It’s some conspiracy theory thought process.

It’s QE and QT. Not printing money.

People just want to associate political thoughts to criminal activity.

If I see someone say “print money” in their comments, I know to move my eyes onto the next comment.

“When business investment takes off like this, and when government spending, particularly on government employee wages, surges like this”

Heard Biden admin has proposed a 5.2% COLA for federal employees. I’m so disgusted. Yet SS recipients will get a measley 3.1% if they are lucky. We need to cut the federal workforce by 75%. It’s a monster.

Let’s cut our wars by 75%. They are the real source of our debt.

That too, but so are salaries at many agencies. Way above private sector for run of the mill jobs.

And these idiot politicians think they’ll get re elected .Screwing the voting public.Not getting my vote

Medicare payments got cut this year. My Nurses/receptionists all got raises in order to keep them from leaving. What we get paid per unit of work (RVU) went down. I have to work significantly harder just to pay my staff more and keep my income the same.

Its a real ‘thank you’ to all the healthcare heroes out there

Oh yeah, medical ppl are def working harder and longer hours. And for some, no raises.

“You’re lucky to have a job.” That’s an old classic you’ll hear.

Canada 5 year bond yields hit a decade high of 4.06% today.

I know we are supposed to “unlearn” what we know about M2..

but, pick your money supply metric….

We have TOO MUCH money in the system…..IMO circa $4 Trillion….and until the limping along QT starts to have some impact, the punch bowl is plenty full.

Wolf said: “PPP was $800 billion. In terms of dry powder for consumer spending, it’s dwarfed by savings deposits (about $10 trillion), money market funds (about $7 trillion), plus tens of trillions of $ in brokerage accounts and Treasurydirect. Consumers in aggregate have a huge amount of wealth that they can spend if they want to.

———————————————————–

longstreet sees 4 trillion in the system. Wolf identifies at least 17 trillion in the system. M2 is currently about 21.7 Trillion. M3 is higher than M2.

Lots of confusion out there ……

Similar to homeowners using historically cheap mortgage debt to buy or refinance residential real estate, many business firms loaded up on generationally cheap debt with rates at 3% or less to finance, or refinance, business ventures. Like the fortunate homeowners, they won’t let go of their advantageous position easily. So, the economy has two major economic groups, homeowners, and business owners, who are in favorable circumstances that have not been seen in our modern economy for the past 100 years. The Fed is going to have a very hard time influencing these economic players with changes in interest rates. They will simply “sit tight”. New homeowners and new business owners will be affected, and car buyers, and credit card holders with balances, will be affected by higher rates. But this is a much smaller percentage of the economic actors than in past economic cycles. The economic effect will likely be a very prolonged economic cycle where the Fed’s increases in interest rates will have very little impact on economic activity, or inflation, for years to come. Hence the strong GDP numbers Wolfe ably describes. It will be interesting to watch it play out.

$31 billion of QT in the past week. Glad to see it.

The talking heads on the cable shows rarely mention QT…its all about Fed decisions on target FF.

I would be glad to see a positive yield curve and more QT. The BOJ shifting might be a sign the CBs cant hold long rates down much longer.

Probably more than offset by Treasury with govt deficit spending at $2T a year ($5+ billion a day so $35 billion over the past week).

Z33, government deficit spending doesn’t offset QT, because the borrowed money has to come from somewhere, and that somewhere then can’t spend the money elsewhere.

It’s not *new* dollars in that sense, yes. However, they’re converting low/zero velocity money from savers into higher velocity government spending when they borrow and spend. That’s inflationary. And it’s an amount offsetting QT at least on an annual pace per estimates ($2T deficit spending vs $1T QT per year). Week to week maybe not because of TGA and tax revenues quarterly variation, etc, but annualized is and it’s funded from low velocity sources that wouldn’t have been spent as fast as the govt otherwise as you imply it would have.

I hear your point, but I don’t know that I agree that saver money is “low velocity.” The difference is that, without the deficits, the banks that the saver’s deposits are being held at would lend it out to private borrowers, and now they’re not. So while it’s true that government spending is crowding out private investment, I don’t know that the government spending is necessarily higher velocity, in the end.

I heard a good interview with Jeremy Grantham. He mentioned that he uses a model with 3 factors that does a good job of forecasting stock prices. He said the model broke down during the last bust as it predicted the bust too early (I think he mentioned 18 months early).

He said his model has done the same thing this time saying market PE should be 17 not 27.

Hussman’s 12 year model tends to be worst at blow off tops and panic bottoms. Market tops are probably too complex for anyone to figure out but a few get lucky on timing.

If you are not a gunslinger I wonder if the way to play it is to ride money markets til 10 year yield passes money market rate and to buy stocks when dividend yield on stocks passes yield on 10 year. Bottom wasn’t in til dividend on sp500 was higher than yield on 10 year during last three recessions I believe. Of course its no guarantee this time is the same.

I cant figure out how to invest in this market so I have a lot in money market, 6 month brokered CDs, and treasury bills. Yes I’m mostly missing out on “party on” mode in thr stock market, oh well.

Im with your there. Mostly Money market and six month treasuries…Very low baseline into s and p for long term. This rally seems bonkers to me. Thats why I’ll never be rich.

It should be interesting to see if government spending slows next fiscal year after appropriations in light of the recently passed legislation….