The Fed has jacked up interest rates to over 5% to slow down this circus, and instead we’re getting accelerated growth.

By Wolf Richter for WOLF STREET.

We’ve been on a recession watch here for well over a year, the most-promised and most highly anticipated recession ever. For the markets — they really want that recession so that the Fed will cut rates and restart QE or whatever — it’s like “Waiting for Godot,” that infamous play of the early 1950s that was part of a movement called, “Theatre of the Absurd,” which makes total sense here. The play’s two characters are waiting for Godot, but Godot never arrives.

The Fed has jacked up interest rates to over 5% to slow down this circus, and we’ve been waiting for well over a year for this promised recession or soft landing or whatever, and instead we’re getting accelerated economic growth.

This surprising – this higher than feared – economic growth is not so surprising, actually, as the trillions of dollars that were printed and handed out during the pandemic are still circulating around out there at every level, and along with sharply rising wages, are getting spent, and are still fueling inflation and economic growth.

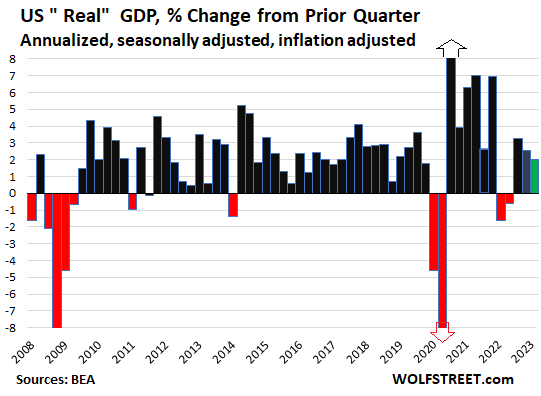

This higher than feared economic growth has shown up in all kinds of data, including today in the “third” estimate of GDP growth, released by the Bureau of Economic Analysis. It’s based on more complete data than the prior two estimates. Today’s revision, since we’ve been waiting for that recession, is special.

The GDP growth rate, adjusted for inflation – so “real GDP growth” – was raised to 2.0% annualized, much stronger than the market had feared, nearly double the growth rate of the first “advance” estimate (1.1%), and well above the second estimate (1.3%), on:

- Even stronger growth of consumer spending (our “drunken sailors”)

- Even stronger growth in government investment and consumption

- Less terrible trade deficit (“net exports”)

- Slightly smaller plunge of gross private domestic investment (buildings, machinery, etc.).

This 2% GDP growth is far above the Fed projection of 1% GDP growth for all of 2023, per its “Summary of Economic Projections” at its last meeting. These projections include the infamous dot plot where a large majority of participants see at least two additional rate hikes this year, if the economy and inflation wobble along as they expect. Alas, GDP growth so far has beaten those projections by a wide margin.

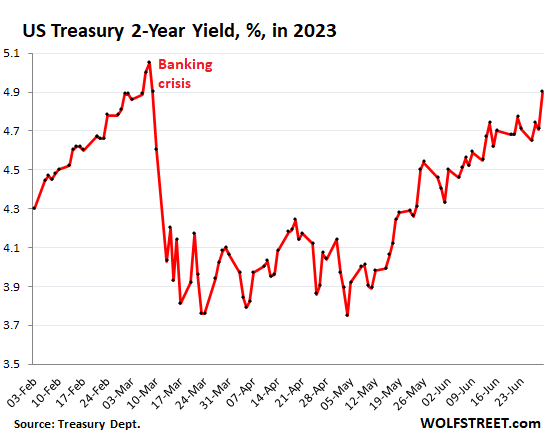

In response to this stronger than feared economic growth, Treasury yields surged as bond prices fell in anticipation of “even higher for even longer”: The 10-year yield jumped 15 basis points to 3.86%, and the two-year yield spiked by 18 basis points to 4.89% at the moment, the highest since the last trading day before the official beginning of the banking crisis:

I’ll just point at a few key items in today’s GDP data (all adjusted for inflation, so “real,” and annualized).

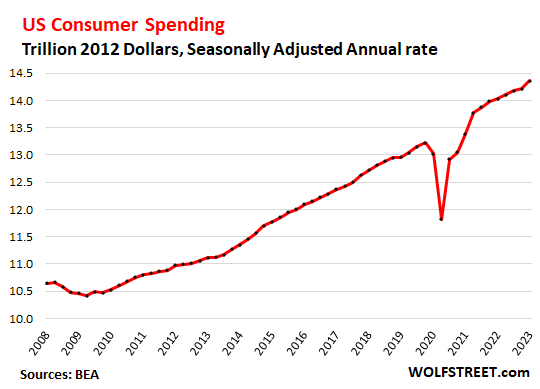

Consumer spending on goods and services jumped by 4.2%, the fastest growth rate since the stimulus checks went out in Q1 2021. I’ve been saying for months that consumers are spending like drunken sailors. And they sure did in Q1. This chart shows the seasonally adjusted annual rate of consumer spending in inflation-adjusted dollars. You can see the jump in Q1:

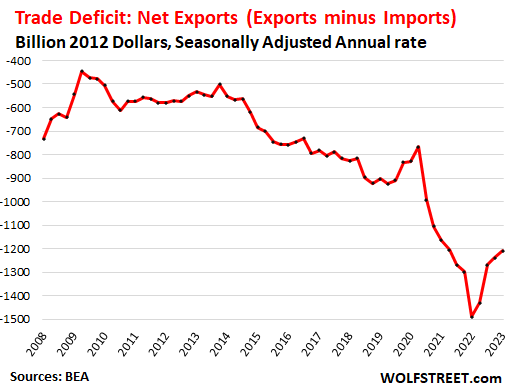

The Trade Deficit (“net exports”) in goods & services was less horrible, with exports rising faster at 7.8% (first estimate 4.8%), and with imports rising more slowly at 2.0% (first estimate 2.9%).

Exports add to GDP, imports subtract from GDP (net exports = exports minus imports = trade deficit). The ridiculous trade deficit during the pandemic was caused by consumers spending their stimulus money on imported goods, while exports had slowed. This distortion has been unwinding, and that’s a good thing, and it subtracts less from GDP, and it’s still horrible:

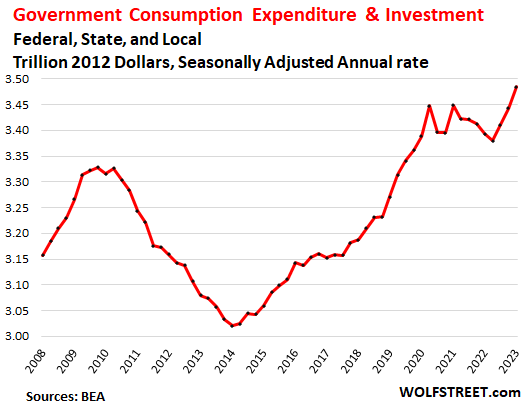

Government consumption and investment jumped by 5.0% (first estimate 4.7%), the third quarter in a row of increases, after five quarters of declines. This includes federal, state, and local governments, and they’re spending like drunken sailors too.

At the federal level, spending jumped by 6.0%, with a big increase from non-defense spending (+10.5%). State and local spending jumped by 4.4%.

Government consumption and investment does not include transfer payments and other direct payments to consumers (stimulus payments, unemployment payments, Social Security payments, etc.), which are counted in GDP when consumers and businesses spend or invest these payments from the government.

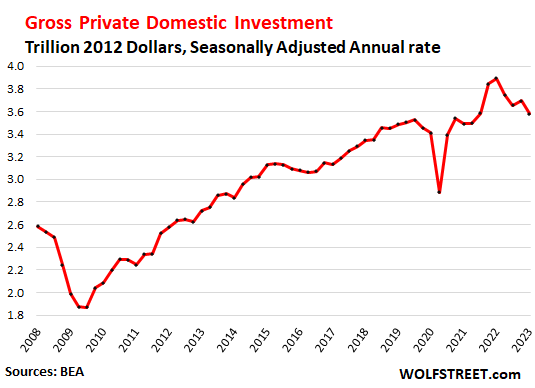

Gross private domestic investment plunged by 11.9% (a little less terrible than the 12.5% plunge in the first estimate), having now worked off the entire pandemic spike:

About a month from now, the BEA will release its first estimate (the “advance” estimate) of second-quarter GDP growth. And the figures we’ve seen so far for Q2 give no indication of any kind of recessionary decline. On the contrary. And so this modern-day absurd play, “Waiting for the Recession,” will drag on for a while longer. And that makes sense, with these trillions of dollars that were printed and handed out during the pandemic still floating around out there at every level, and still getting spent, and still fueling inflation.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks WR for this report.

Despite the rates at 5%, we see this growth basically tells us 2 things:

1. Rates are still too low. FED made a mistake by not hiking in June-2023.

2. Still too much money sloshing around the economy. Fed needs more aggressive QT.

I don’t expect much from FED as well all know by watching their actions in last few decades, they work for the elite.

What people dont understand is that the short term interest rate is almost meaningless. It is long term rates and the size of the balance sheet that are propping up the everything bubble.

It is the everything bubble, along with government deficit spending, that props up consumer spending and inflation.

Once long term rates rebound sufficiently, we will see bubbles begin to burst and then finally consumer spending start to tank and after a period of time, inflation will finally decline.

If we had a responsible group of central bankers, they would have liquidated at least 50% of the balance sheets they built since COVID. But instead we have puppets of the rich.

I largely agree that increasing the ST interest rate doesn’t reduce inflation as much as people expect. Most business and personal decisions are based on LT interest rates, which have actually declined since October 2022.

Although a benefit of high ST rates is that it takes the worst speculators out of the game. These are the folks that borrowed short and invested long. That play is not viable with an inverted yield curve. I’m surprised that only a handful of weak banks collapsed. I think there is more of that to come if the ST stays higher for longer.

If the Fed were serious about fighting inflation, it would start selling its MBS portfolio to eliminate market distortions. That would represent a real effort to reduce inflation.

“I’m surprised that only a handful of weak banks collapsed. ”

Other than the giant banks, I suggest most banks are near collapse. They are kept alive by the Bank Term Funding Program. That and the stupidity of their depositors: .01% interest rates, fees for overdrafts, fees for checking accounts, fees for checks, fees for writing too many checks (on money market accounts), fees for other stuff I do not know about. Granted, banks make most of their money on the interest rate spread, but if Powell really wants to slow the economy to get inflation to 2%, there will be plenty of foreclosures. I seem to remember this happening not too long ago.

Increasing the ST rates works just fine as long as they are not .25 increases. 2.0 and higher in one shot or two will definitely crush inflation.

jon, I agree totally that rates are too low. 7-8% (raised my estimate from 7%) may get things to slow down. It’s obvious to everyone but the fed, that 5.25% or anything close to that, isn’t having the effect they predicted.

gametv, Short term rates are extremely important. Approximately 80% of all commercial loans are variable rate loans based on short term rates. If you want to slow the economy, you raise short term rates.

The problem is simple. The FED hasn’t raised rates enough yet because they think they can create a miracle – a soft landing. Once rates rise to the correct level, businesses will face suffocating costs and lower revenues, so they’ll reduce their spending, lay off more workers. Their stocks and options will crater and we’ll finally get the major recession we need to cause widespread deflation and a reset in the economy that’s been needed for the last 15 years.

Houses will be cheap again if enough folks are out of work and can’t make their mortgage payments, but unfortunately most won’t have the jobs or the cash or the income to buy them.

Short term rates will drop. The yield curve will turn positive and voila, you’ll have your high long-term rates again – at least relative to short term rates. The spoiler in all this is the “Drunken Sailor” energizer bunny consumer, as Wolf calls them.

Government budget deficit are to continue and to be spent. Privat business supply what is to be spent on. you may not see a recession of the kind you expect.

No. High short term rates => yield curve inversion => lower bank lending => less demand => lower inflation.

Exactly. Hell, if we could have just had them honor their $95 billion per month pronouncement we’d be in a better place.

As I mentioned yesterday, from 1971 to 2022, average Fed funds rate was 4.86%. Today’s 5.07% rate is about average. It alone is not going to slow the economy, especially with all the money sloshing around. Many in the press seem fixated on the rapid rise in rates from hysterical lows (oops, I meant historical lows). That’s just a correction of an aberration. Instead we should maybe focus on the level of rates, which is about average right now. Note that today’s 30 year fixed mortgage rate is 100 basis points BELOW the fifty year average.

Much higher, much longer, which is pretty much what Jerry Powell has been saying lately. We will see if Jerry’s Kids (the FOMC) will follow their leader. They usually do.

They will also get $200,000 to $400,000 per boring speech, like a certain prior “Fed” (bank cartel) leader is getting if they can just pretend to act but secretly keep inflation going: it is reducing the value of bankers’ liabilities (your bank deposits) and their cronies’ (over leveraged companies and their ultra rich owners) liabilities by over a trillion dollars a year. The “Fed” and its banker, ultrarich owners luv, inflation long time. LOL Their banks are legally insolvent but inflation can rescue them by raising the nominal value of their total assets over their total debts.

I wonder if the increased defense spending is also pumping up our economy, not just the Chips act and inflation reduction act?

Check out John Titus best evidence latest video for why the banks that failed did.

The fed selling $50B a month in MBS would help push up mortgage rates. The economy isn’t going to roll over until housing, which always leads into a recession, rolls over.

If more aggressive QT is what’s needed, why don’t they just do it already and get it over with. Janet sold a THIRD OF A TRILLION in new debt in one day as soon as the debt ceiling was cancelled and as of Wednesday, she’s sold $799B a tad over three weeks.

Only thing I can figure is it was all short term T-bills and there’s no market for anything over a year.

i dont care if inflation goes up. my debt will be wiped clean and ill still be able to buy more useless stuff than i need. i dont understand why everyone wants the economy to crash

Nobody wants the economy to crash. But, people want inflation to recede.

I am glad you are doing fine. But, inflation is basically stealing from people who have savings in FIAT currency and those with incomes harder/slower to adapt to the inflation rate, e.g. pensioners.

Not to mention in the very long run EVERYBODY is negatively affected by inflation. Big investment projects need big savings accumulation and inflation deletes savings. So, everybody will be living in a less productive economy.

Its my understanding that the cost to service the world’s debt is on the verge of making a new high as a percentage of GDP. I expect that debt servicing will put us into recession soon enough.

Not sure how to express this. But like a NASCAR car in a 4 wheel drift, the driver, the FED, applies oposite wheel a little…a little….then a little more but the drift continues. At some point the drift ends and reacts to all the opposite wheel inputs, with a snap spin directly into the wall.

Is our ecomony like that NASCAR, just about to go into an opposite snap spin?

After which everyone realizes that the damned car (the collective society and economy) was going way too fast for it’s set-up, chosen drivers, and the entire situation…..all in the interest of “winning” this “race for the best life”…..a pretty stupid game, no?

The biggest problem with your fine analogy is that sooner or later there WON’t be a next race to get it everything right.

Like the ECO-MONEY typo. Spaceship Earth doesn’t.

The only way is for Fed to reduce balance sheet meaningfully. They need to go back to at least pre pandemic levels. Also actually sell MBS they are holding.

FED won’t do it. Treasury is selling 100s of billions in bonds/bills .

If FED is really serious and honest, they’d have been much more aggressive.

Treasury spending $2T per year (for foreseeable future) in deficit, I am not how it will help fighting inflation. At this it is beyond us simpleton brains to comprehend what is going on :-)

Politicians need to keep spending to buy votes, so I don’t see govt cutting votes.

Govt can’t tax the rich people as they are the ones funding their campaign.

Only resort then is: More and more deficit spending. It works as long as USD stays as reserve currency, which can be the case for ever or for et least next few decades.

The Fed isn’t selling anything. They’re letting all those short-term bills mature and roll off their balance sheet.

@ Random Intime –

As jon mentions and Wolf elaborated on recently, U.S. Treasury is set to issue debt at a breathtaking pace over the next 18 months.

Wolf mentioned the other day that there were $4 T in T-bills outstanding at the end of May. That’s $4 T of new issuance coming by May, 2024. Then the heightened issuance schedule of notes and bonds that are on the way to keep the maturity schedule in proper balance which amounts to an estimated $600 B of issuance the rest of this year and another $1.7 T in 2024. By my reckoning, those estimates of note and bond issuance look too low, if anything.

Fed is currently letting $60 B of Treasury securities mature each month without replacement. I agree with you however that removing the monthly cap on balance sheet runoff would go a long way to curbing inflation but the FOMC doesn’t much care. If they were serious about fighting inflation, FF would be at 8% by now.

Those who whine that this is the fastest hiking schedule in history fail to mention the fastest easing schedule when QE was rolled out and kept in place for over a decade.

Monetary policy remains incredibly loose…and inflation is NOT coming down meaningfully for a long, long while.

The Federal deficit is over 2 Trillion. Until they start moving towards a balanced budget everything the Fed is doing will fail. END OF STORY.

Howdy Mr Wolf Sir. Love your charts too

“as the trillions of dollars that were printed and handed out during the pandemic are still circulating around ”

Imagine what will happen while US old geezers spend all that interest earned???? Should have an effect also??? Fun times for the old folk….

The percentage of transaction type accounts to gated type accounts is growing. Transaction accounts turn over faster than gated deposits. So, I say the demand for money is falling (velocity rising).

Shadow stats puts it this way: “inflation pressures continued, with the May 2023 Money Supply reflecting still-extreme flight to liquidity. The most-liquid “Basic M1” (Currency-plus-Demand Deposits) held 119.2% above its Pre-Pandemic Level and was increasing year-to-year with intensifying inflation pressure”

Remember George Garvey

Deposit Velocity and Its Significance (stlouisfed.org)

“Obviously, velocity of total deposits, including time deposits, is considerably lower than that computed for demand deposits alone. The precise difference between the two sets of ratios would depend on the relative share of time deposits in the total as well as on the respective turnover rates of the two types of deposits.”

And that makes Steve Hanke wrong.

Steve Hanke is the only person I know that has been accurate at forecasting whan inflation is going to be a year in advance on a consistent basis.. I think the problem with using money supply to predict inflation is you have to use the correct lag factor for the money to get into the economy.

I think he has data that shows lagged money supply is 93% correlated to inflation. I think the challenge is there are multiple factors for inflation, but at least in his mind by far the dominant factor is money supply.

The Fed’s model for predicting inflation is obviously terrible or they intentionally lie about the forecast to steer the market to their preferred outcome.

Know what ‘funny’ bit is about all the doom and gloom predictions?

The moment that they are right the crystal ball fondlers will ignore that it took them hundreds of failed predictions to get lucky once. And they will scream from the rooftops that the Fed should have listened to them so that the one accident where they ended up right could have been prevented.

A year from now Wolf will have a post saying “we have been waiting patiently now these past 2 years for a recession”.

I remember the run up to the crash around 2000. It got very crazy at the end. I thought the bust would never come. Money managers kept getting funds and they kept driving PEs higher and higher. When the winds change all you have left are companies that can service their debt in a recession.

“The moment that they are right the crystal ball fondlers will ignore that it took them hundreds of failed predictions to get lucky once.”

Yeah, like those dummies who predicted the GFC.

That which cannot continue indefinitely won’t. There, that’s my doomsday prediction.

Guys, I don’t want to be that guy, but…

…any sort of beliefs that there is a free market in the west, it’s unfortunately wrong. Any sort of beliefs that the FED will “do the right thing” and crank up interest rates to slay inflation, it won’t happen…

Guys, “the right thing” won’t happen. They will keep printing and they will keep propping up the markets. All of them. The markets will go up again, and the vast majority of people around you will continue living in fantasy land. The FED and the politicians will do this until the currency is no longer usable, and then they will give you an offer that you “can’t refuse”…

…just sign the dotted line. You’re going to have to…

…unless you want to be the “outsider”, the “outcast”…

The show must go on…

I agree. you hit the nail on the head :-)

jon,

“hit the nail on the head”

LOL. Nail bent crooked, thumb squashed. Because:

Robin:

“They will keep printing and they will keep propping up the markets.”

LOL. For the past 15 months, central banks have been doing the opposite. And they’re tightening further. Not sure how you could have missed all that.

The bigger picture is: They printed like crazy and kept the rates too low for too long.

Now whatever they are doing in the name of slowing down economy and taming inflation is too little and too late.

I wish I have the same faith in FED like you but looking around you and looking at your articles/data, it is evident that there is NO slowdown.

jon,

“I wish I have the same faith in FED like you”

I have no faith in the Fed or in anything else. I don’t operate on faith. I’m just telling you what they already did — they “tightened by the mostest and fastest”® in 40 years — and what they may still do, based on various indications.

Robin’s statement, “They will keep printing and they will keep propping up the markets,” is effing bullshit because they STOPPED printing and they STOPPED propping up the markets last year, and instead they tightened, and denying that is ignorant or malicious bullshit. And your response to this effing bullshit was “hit the nail on the head.” I understand that spreading and wallowing in effing bullshit is a lot more fun than looking at dry complicated details. But that’s life. People need to spread this effing bullshit somewhere else.

Maybe your “hit the nail” line was about another portion of Robin’s comment, and then OK, but you need to specify what portion of the statement you’re addressing.

Before 2008 desired fed funds rate achieved differently than now. Now Fed uses IOR. With bank reserves being very high (consequence of QE), the interest generated by reserves might be acting as stimulator for economy. In high reserve regime not sure how much effective high fed funds rate are.

Random Intime:

And with that and overnight rrp, we have the fed taking on the “risk” on long duration securities while institutions are brought along to take the profit.

Correct me if I am wrong, but since rrp and ior are close to 5%, treasury now pays 5% on the portion in fed’s rrp/ior. Part of it through the security loaned out by the fed to the instution (assuming low TLT security on rrp), paid to the institution, and the rest to cover the difference, after fed accounting, directly to the fed.

Robin, while I agree that the Fed will not do the right thing at the level it should be done, I disagree that the Fed will not continue to be forced to tighten until markets fall and inflation falls.

But what will happen is that instead of allowing the system to purge itself once the “you-know-what” hits the fan, the Fed will revert to cutting rates again to bail out the rich. They do this every time.

Technology is really creating the potential for significant improvements in lifestyles. What we need is for the government to create policies that prevent wealth concentration in the hands of the few. So everyone benefits from these tech changes.

But that is a step the Fed and government wont take.

Howdy gametv

I’m confused and being a newbe here is probably part of it. Do you like Government or NOT like Government. Sorry, read your post and am confused…..

Jon and gametv continuously rant that the Fed wants inflation for the benefit of the “elite”. If that were true, then they wouldn’t be raising rates to reduce inflation at all. Plain and simple. But the conspiracies are easy to propagate. The history of the Fed – to keep the economy from overheating or undercooking – is all the Fed is doing. They don’t time it right, for sure, but it’s probably much harder to get right, because of political pressure from both sides of the aisle, and the macro threats that appear from time to time typically coming from out of the blue, than anyone imagines.

Also, if you insist on believing that the Fed actually wants greater wealth concentration (for the horrible elites), you’ve also got to be certifiably paranoid. No one “wants” that, it’s just an inevitable outcome of smart businesspeople and investors beating out stupid ones. It’s called “capitalism”. And there is a huge supply of stupid ones including the conspiracy bull shi**ers.

Look into getting therapy and spare the rest of the readers. It would be nice if you two could stop spreading paranoia and present some real evidence of your suspicions. Spreading bs is easy. Cleaning it up is harder.

Would you add your opinion/knowledge regarding the very obvious facts of insider trading by political elites and members of FRBs, etc.

That these practices by politicians and other ”EMPLOYEES” of GUV MINT are well known appears to be something you don’t know about, hmm???

Some of us have seen the local and state politicians going around and buying all the farmland for peanuts that became interstates, and especially the land around where the interchanges would become.

Others have seen every single current county commissioner put in jail by the feds for participating in deals where they were the ones to sign off on ”zoning” and other changes to county laws, etc., etc…

VVNVet: first, thank you for your service. We are indebted to you. Second, yep, there are several web sites devoted to Congressional insider trading alerts and whistle blowing. I’m highly confident that most of our govt. representatives are flat-out crooks. They may not have started that way, but they end up that way. Corruption is part of the human condition: it ain’t good, but until we no longer have testosterone and want to own everything we can get our mitts on, we’ll suffer from it.

But to think that inflation, which causes widespread problems in our country, is WANTED by the Fed is bull-pucky. And to say that the Fed is only doing what they do for the benefit of the “elites” – which have taken the place of “commies” as evil-doers – or for the wealthiest class, is a second serving of bull-pucky.

When people get angry, or hangry (hungry and angry), they are emotionally charged and give birth to a brand new, baby conspiracy. Lots of pregnancies here on Wolf St. But lots of smart commentary, too.

So why do the “stupid ones” keep getting bailed out?

There is a rumor that a big ugly bird, which has a name not known yet, will come and smash the Fed and its actions, and Washington and Wall St. too. It is very angry and wild and wants revenge and wont hold back and is ready. All I know about this bird is it is a swan, and it is black, and will come by surprise.

And that after this is accomplished, and the brave new world begins, when all men are paid for existing and no man must pay for his sins,

As surely as Water will wet us, as surely as Fire will burn,

The Gods of the Copybook Headings with terror and slaughter return!

The timeline was that the 0 rates caused a blow off top on the SPX to 4800. A lot of that profit was obviously taken and a lot of stock was also issued. SPACS went nuts IPO’ing dogshit. That money within a 24 month period went into Real Positive Rate bonds. The rate hikes are now fueling inflation because the risk free rate is on inflated money through institutions.

The bank shit is non-news and borderline irrelevant simply the U.S. banking system has been a disaster since Glass-Steagall was repealed. The “necessity” of small regionals is irrelevant when you can run your day-to-day expenses and AR/AP out of MMF’s with actual yield and better underlyings than banks.

Few understand the actual paradigm and would rather flail and whine and live in their anti-capitalist echochambers. Not that this is capitalism anyway. It’s central planning and the Fed is getting exactly what it wants: hard proof to the government that their spending is completely out of control. Powell said recently that the Fed’s job is not to buy the USG’s idiotic spending and fund its inefficiency. And the Fed damn well knows this and will keep rates up to inflate the debt away until it catches up to the current spends.

M2 may be declining but the base effect is nullified but just how enormous 2020-2022’s NIRP was and how much helicopter money was rained down.

Watch USD and JPY raise in tandem now, Gold, BTC, and NASDAQ go up because the ROW is going to get in on this parade too even more than they are.

Eurozone and China are going to get brutalized by this.

This has been posted many times…….it’s tough to have a slowdown when…

the federal budget is approximately 50% more than 2019.

If we take the 6.2 trillion spent by the feds and add local government spending of 3.5 trillion….. its 9.7 trillion spent in 2023.

9.7 multiplied by volocity of money of 1.3 is approximately 13 trillion.

So back of the matchbook numbers…..roughly half of our GDP is government.

Add the professions that go on no matter what happens to the economy like doctors, hospitals, law etc etc

Good luck slowing down this mess.

I agree. Government is far too big a component of GDP to actually have GDP mean anything in terms of “Production”. To double GDP all the government has to do is borrow $20T and spend it on a bunch of Solyndras.

Agree 100%! Add to all that the fact that there’s $93T in wealth held by the baby boomers and the silent generation, means a lot of GenX & Millennials are able to spend & not save. They have big golden parachutes waiting for them as their parents die off.

And, there was almost $2T in dividend / interest income from the first quarter alone now that the Fed has jacked up the FFR.

Like Wolf says, there’s trillions of dollars still slushing around. The only way all that tappers off is for the housing & stock markets asset bubbles to burst along with real job losses.

Otherwise, core inflation is just going to keep humming along at or above 5% for quite some time. The absolutely should not have taken their foot off the gas. It may take 25 basis point hikes all the way through the end of the year to really push the economy into the needed recession. And a mild recession simply isn’t going to cut it. Far from it, actually.

I think 5% might do it. It is just going to take time for rates to bite. I just heard Wolfspeed, an offshoot of Cree I believe, just borrowed a big slug of money at near 10%. This is a chipmaker that the government subsidized to build a multi billion dollar chip plant close to me.

I think a lot of businesses are going to be looking at having to roll debt at 8% – 10% if rates stay at 5%. That would take a lot out. It’s going to take a little time for the businesses to start axing people to try to make their payments.

Corporate Bond Market Distress readings are rising, and mostly in Investment grade. This is debt alternate to growth or High Yield, and consistent with Wilsons read on fixed costs weighing hard on corporate earnings on the backside of inflation. The same situation does not apply to growth companies. The economy is overheating while consumer prices are coming down. How long does the trend last? The Fed may not lower rates for two years.

Alfonso Peccatiello did an interview back in March or so when SI Bank went under. He said typically there’s a gap of around 6 to 9 months between an initial set of (weaker) bank failures, where not much happens on the surface, before the broader economy turns. At the time he was saying he expects a recession anywhere between the beginning of the 4th quarter of ’23 and the 1st quarter of ’24.

Feels roughly right to me: nothing’s breaking yet, just ominous creaking noises. At “some” Fed funds rate, things will break. And they intend to raise until they do break.

“Feels roughly right to me: nothing’s breaking yet, just ominous creaking noises. At “some” Fed funds rate, things will break.”

Replace “Fed funds rate” with “ocean depth” and it sounds like some recent news headlines.

That’s why I phrased it that way. :)

If Alfonso is right, he’s ignoring one glaring difference between now and the past… Today’s Fed will inflate their balance sheet as neccessary to paper over the stuff that breaks regardless of inflation. The balance sheet spiked for a little while recently when SVB and the banking sector made some creaking noises, then they let off once the depositors were made whole and the problem blew over (for now). The outcome is that the balance sheet is roughly right where it was at the beginning of March, almost like neutralizing 3 months of QT. I reckon there’s a very good chance the Fed will perform these little sort-of-quasi-QE actions every time something creaks, so the balance sheet could dance around a flat line for a while. These focused mini-QE events could make the clown show drag on for a lot longer than Q1 of 2024. Maybe years. Then when something big breaks, we’ll be right back to shock and awe money printing faster than you can type “QE.”

Most economists still believe the neutral interest rate is around 2.5%. Is there a chance that estimate might be too low?

If we’re talking nominal interest rate, the “neutral” rate would be at the rate of inflation. That would mean that the “real” rate (interest rate – inflation rate) would be 0%.

exactly !

But FF should add a little for the taxation effect

I think you can say that the Fed has at least got into a restrictive environment which to me means in the intermediate term short term treasuries and t -bills are a better alternative than stocks. In the very short term people smarter than me can play the rips and dips and maybe make money. I get tempted sometimes, but I don’t think I can compete with Wall Street gunslingers doing that.

Check the “Macrotrends” site. They have a history of Fed Fund Rates dating back to 1954. The rate has almost never been at 2%. It has fluctuated constantly. The 2% rate is a target; it’s been over that most of the last 70 years.

HSBC just weighed on recession prediction, following Deutsch Bank a week ago. DB thought 2024, HSBC thinks late 2023.

Where is von Mises when we need him?

Rand Paul has taken over as his wacky disciple.

Rand Paul has decided to go the RFK Jr route. Both their fathers were sensible men compared to their offspring. I was proud to cast a vote for Ron Paul.

Ron Paul caused all this, in a Butterfly Effect kinda way. He split the Florida vote in the 2000 presidential election, so Gore lost the national electoral vote by a handful of votes, assuming they counted right during the 15th or so recount. Maby only maby no 911 without GWB, but likely no global financial crisis part 1, leading to no ZIRP this past decade or so, no precident for Covid stimulus, etc. “For lack of a nail, a horse was lost” -Ben Franklin

NAH mol, that was Nader who split the FL vote in 2000, NOT Paul…

Was here working at that time,,, almost lost it when my bro told me he voted for Nader who was a good guy IMHO, even though he had lied a bit about corvair car, one of the funnest cars we ever did donuts on the beach in, with never any flips — as long as ya knew how to drive it…

Anyway,,, bro saw what he had done to elect bushy 2, and found some of the results when he was forced into foreclosure in bushys reign…

There is a time lag in liquidity reduction, especially after the insane helicopter cash distribution, but Truth reigns supreme.

Ludwig von Mises was crystal clear on the ultimate effect.

https://mises.org/wire/housing-prices-are-falling-reality-sinks

All good news, however long good news lasts for?

The US has never had it so good.

Despite a decade of China, Russia and Covid, the US economy continues to motor ahead in a golden age of asset wealth and GDP superiority over the rest of the world.

Inflation is coming down. GDP is going up, and everyone who wants one has a job.

The US is in much better shape than you think.

The US government is an insolvent debt disaster that is getting vastly worse every single day and there is no way to fix those problems without 1) raising federal taxes very substantially, and/or 2) cutting federal spending very significantly without any further delay.

Us govt can never be insolvent as they can print money ad infinitum.

Infact no govt who can print currency can be insolvent

Only side effect is inflation which can be hidden by manipulation

The fact that money printing is considered an acceptable solution, when history tells us that it always ends badly is a mystery to me. I do think we are in a new Geopolitical game where as long as China uses capital controls, the US is going to keep growing debt.

The US government also owns over 210 Trillion in assests

Did you forget the sarc tag?

Yes. That shadow on the x-ray will probably go away on its own. The tremors usually settle down by the afternoon and even that mild bit of gangrene at the outer extremities? — can barely notice it over the perpetual volcanoes of champagne.

Good times.

CBO: Federal debt to soar…

181% of nation’s economic output…

gull’ darn’it! I want my RECESSION! When’s that recession arriving so we can do recessiony sorta things?

All the official arm chair economists on youtube have been telling people for a year now that things were getting “really bad” and that the end of the world was upon us. It’s just not fair that our economy is doing better than ever. Things really need to get bad.

I’ve been saying it for a while now: we need rates up 10%, 12%, even 16%. ASAP.

I’m glad you’ve returned, Mr. Dugan. Great movie; great cast; great screenplay. Now, if we can only resurrect Jason Robards and few others… we could do a sequel.

But, if we did have a serious recession, the ranters would be screaming for the Gov to “give us jobs, we just need jobs”!!

In the remake maybe Matthew Broderick could play Max and Marsha Mason could revive the role of Mrs. Litke the helpful neighbor across the alley.

At the time of of the filming of the original movie mortgage rates were around 15-16% and the average cost of a home in L.A. was about $69,000. Both desirable bench marks I think we can agree.

I grew up in el aye. I was looking to buy a house in Venice when it was a haven for druggies and still had a high crime rate. But it was starting to turn.

Ask me if I regret not buying in…

I personally think the rate hikes are working… just slowly. I come here for the hard data, and try to gather color to that from what I see and hear from friends, family, suppliers, and customers. I see a mixed bag out here in flyover country. Signs of slowdown, but most things still hot.

Lumber is back to the range of sanity, with plenty of availability on the shelves. Steel prices are roughly back to pre-pandemic levels and shortages are gone. Aluminum recently peaked and is heading back down. Lead times on core components we buy at work have come down dramatically from peaks in 2021 or 2022. One or two suppliers are still way behind, but lead times on some industrial products are below average.

The large camper dealer lot down the road that was empty for almost two years is now chock full. Inventory is starting to show back up at local car dealerships, and discounting is back on, albeit from high MSRP. UTV’s and tractors are now available on the showroom floor again after an impossible two year stretch. Pricing is still high but falling slowly.

Our state manufacturer’s association data update yesterday is predicting a gradual slowdown through 2023 and they are calling for a mild recession in 2024. That said, we are still absolutely buried in work building truck equipment. Record backlog by a mile. We’d finish the year strong if we didn’t take another order from now through December.

We tried outsourcing laser cutting work during the stimulus-fueled supply chain mess of 2021 and 2022, and no one could help. All were too busy and quoted lead times of 3-6 months. We just had a laser go down, and we’ve now been able to outsource to two local suppliers with million-dollar lasers sitting nearly idle, and all others quoted around 1-month lead time on most parts. Things are softening, but it’s spotty, and by no means hitting everyone evenly.

A friend is a commercial crane operator in a nearby big city… their company is now doing rolling layoffs for the first time in a few years.

I was completely taken by surprise by how hot our market has been this year. Orders took off like a rocket starting in January and just keep coming. Orders have now topped our 5-year average for six months straight. In the last 18 years my data covers, we’ve only sold more than FH 2023 once, and it was in 2021 – barely.

In general it feels like rate hikes are working, but agree with Wolf. Higher rates for longer is in the cards. This economy got burning so hot it’s like that camp fire you keep pouring water on, and it just keeps flaring back up when you walk away.

Thanks for the perspective. A view from the bridge.

Doesn’t it prove that the Central Banks are all working in cahoot.

They all lowered interest rates and then did QE.

Then they were doing QT and now increasing interest rates.

They say that this is to reduce inflation but surely if my mortgage loan payments go up, I will ask my boss for more money so he will have to put his product and service prices up. If he has a business loan and his business’s interest rate goes up, he will also have to put his prices up.

“They say that this is to reduce inflation but surely if my mortgage loan payments go up, I will ask my boss for more money so he will have to …”

That’s option A.

Option B is that your boss lays you off to save money, and you can’t find another job, so you go on unemployment and cut back on spending, and if you cannot find a job quickly enough, you’ll default on your mortgage, and then…

While it is discouraging to constantly see the GDP roaring, job creation, job vacancies and all the other inflationary economic dismal news, there is hope on the horizon.

The sun is rising on a beacon of hope for the USA and that is Europe. Europe has lower interest rates and higher inflation, giving them much better odds of a recession. European economic challenges should reduce our GDP by enough, and put our goods into better supply and demand balance like Jerome Powell says. The Europeans also face raw material challenges keeping those factories cooled off while cheaper Chinese goods fill their shelves and with economy of scale ours too (maybe some Walmart styled rollbacks). The Chinese have construction companies that were looking into building US homes, disappeared from the news, but perhaps they are working on modular home components they could ship here, with all their youth unemployment.

These kind of economic conditions lead to trade and tariff battles that also help put supply and demand into better balance.

Those European factories need natural gas for many industrial processes and chemicals. Our LNG comes from geologic small pockets that need constant drilling and fracking to maintain the overall production. With the much increased demand the investment in production is stressed at the same time the banks are stressed (reduced or no loans). Lower production raising European prices. dropping ship demand to uneconomical, and lowering excess labor demand here at home.

Perhaps this is just an inflation fighting daydream, but it has happened before. Better odds than a lottery ticket.

Godot = unanswered prayers to a mere mortals.

The Fed has become a place of worship.

And God said, “Thou shalt have no other gods before me.” You’d think someone would have listened…

I think with all of this money circulating and the gov. spending like a drunken sailor fed funds would have to hit 9 to 10% to have any meaningful impact.

Amen!

That would take us from negative real rates to historic norms.

B

QT must step up

The Fed should let these huge auctions coming find their own level

I am in the UK where Bank of England interest rates are now 5%.

It is definitely affecting retail customers because the builders merchants tell me that sales for home extensions is down but commercial construction has not fallen.

Return to the trendline of consumer spending: it worked! The Govt bailed us out of COVID and into stagflation!

So… mission accomplished and send it to the next guy!

Maybe the old Bond Vigilantes are waking up from their 40 years in hibernation.

Anybody remember them?

Cheers,

B

I bought some fifty year strip bonds in 1981 and 1982 but in retrospect I wish I had of bought a greater sum of them.

Indeed I do but we now live in bizarro world where there is no place for the Bond Vigilantes. Up is down, day is night. Gold and silver are worthless while coded bytes are priceless.

Esclaro,

The change of your screen name has not fixed the issue. Let’s go to plan B. Can you use a different email for the next five comments (fake is OK). It may be that I cannot fix this issue. Thanks.

Makes total sense to me. Not every consumer is an idiot and when inflation rears it’s head and money is worth less tomorrow than it is today, well you buy things now rather than tomorrow.

Time to get things done before they become unavailable and/or too expensive. (go price HVAC for an example, make sure you are sitting down). If your HVAC is 20 years old, probably better to just do it rather than wait 2 years for it to blow up as you have money now and it will only be more expensive.

government spending trillions they don’t have with no end in sight (and gas/oil about to go back up after SPR drained) inflation ain’t ending tomorrow, people feel it and are acting upon it.

I replaced my HVAC with a mini splitter that I installed myself. Cost 1/3 of a roof mounted unit I would have replaced. It is far more efficient also. Also replaced the unit in my guest house with one.

Yes, that applies to me. Once I saw inflation persisting this year, Fed not hiking rates or increasing QT as fast as I’d like, and Congress continuing to deficit spend with no plans on anything else, I decided I need to do my travels and buy other things I’ve wanted ASAP as my purchasing power will continue to go down. Already spent more than I ever have in first 6 months this year than I did in last 5 years. None from stimulus money as I didn’t get a cent from that nor from ridiculous stock gains as that’s only 401k/403b I don’t touch (not much gains anyway as I’ve only had a plan and did DCA since 2018).

As far as when those with stimulus/cash run out, someone here posted a source from Wells Fargo I can’t find or remember exactly. Something with words harvest and/or matrix in the title and their outlook. It was published in 2022 and they estimated consumers will be low on cash by end of Q2 2023 so about this time. Second half of this year will be interesting. Anecdotally, I did probably 90% of my spending first 6 months and 10% left as I’ve already paid for most of 2nd half travels (flights and hotels already paid, not rental car til I get there).

I hope you’re retired and haven’t spent all your money, because when the recession hits, and it always will, you could be out of a job and out of money.

Nah, not retired, but I have always lived frugally until this year. Even now that I’m traveling and spending a lot it’s still not much. i.e. last week got a flight to Tokyo from Orlando for $1,051 on Air Canada for end of Oct. I’m not going to pass that up and it won’t affect my finances as I save way way too much of my take-home income (have been for years). My savings are enough to last me a long time without a job thankfully. Thanks for looking out, though. :)

Tokyo Tokyo Tokyo — all I hear about is folks going to Tokyo these days. New status symbol?

It’s cheap!

The plunge of the yen against the USD.

Well, of course you are going to get some ‘growth’ – I mean, the US government no longer has a ‘budget’ of any sorts. Whatever is wanted, they buy – no concern for accounting. I don’t think the man in the street even has an appreciation for the 100’s of billions of dollars poured into weapons and such in Ukraine – in just a year or so!

Think of a water balloon. Squeeze one end and you get a huge bulge in the other end. Money has to go somewhere. For example, It leaves commercial real estate and goes into areas X, and Y. There is LOTS of money out there sloshing around. Don’t think because you don’t have it, its not there in MANY forms.

I would reckon that a large portion of money for Ukrain is the equipment and supplies we send, not cash. We are getting a chance to rid ourselves of outdated gear from the Cold War. Other countries did this too- instead of pay to dispose of hazardous materials that modern countries would not supply to their own troops, everyone sent it to Ukrain. Also, the amount of heavy metals in their farmland will now poison people for generations.

As a Marine officer from the cold war era, I assure you that what’s being shipped to Ukraine is not ‘cold war’ material. Bradley’s are not cold war, MRAPS are not cold war, Strikers are not cold war, Patriots are not cold war. These are (and many more) all weapons currently in the inventories of active duty Army and Marine Corps units.

The ammo is definitely not cold war. It’s not kept in inventory for over 30 years. Maybe the NATO countries have given some old junk, but the US is giving 10’s of Billions$$ of current (and pricey) equipment.

Consumers are spending like there is still stimulus money because it’s a habit. The extra money’s gone but their access to credit is not. Consumer’s will hit that wall right around the same time. Tick, tock.

Yes it is a habit and humans are creatures of habit. Especially when the habit gives them a dopamine hit.

Raise taxes

People and businesses hurt by inflation

Now raise taxes

Now raise taxes?

Stops inflation

Once again, where does it rain?

Its a spending problem, not a revenue problem. If gov’ts at all levels (fed/state/muni) weren’t spending like drunken sailors, they wouldn’t need to raise taxes.

One of the companies I work for is an A/V supply house with an entire dept that sells to state & municipal agencies, police depts etc. I see all the crap they buy at ridiculous, marked-up prices with taxpayer $$. All the emails with POs mentioning how their FY is almost over and they have to use up their budget etc etc.

That’s what happens when you have the privilege of spending other people’s money.

The police department of every podunk town in America has more military equipment than most Third World countries. They are like modern day warlords in their little feudal kingdoms.

Raise taxes to reduce the deficit and reduce the money supply at the same time. I thought those were the things everybody agrees need to be done. Simple and obvious, but apparently too simple and too obvious for most people.

Off topic, but:

A former mayor of NYC once bragged that the NYPD has anti-aircraft weapons.

I’ve seen images of local PDs with armored vehicles, complete with 50 cal turrets.

Crazy.

In this feudal kingdom the peasants are packing heat.

Government figures…..take with a very large grain of salt. Inflation adjusted?? Lots of room for wiggle in the GDP numbers. My on the ground/in the store sez things are slowing.

I see the drunken sailors all around me. People are spending money like there’s no tomorrow — and a bunch of it is going into travel spending. It’s a zoo.

Next week, we’ll talk about Q2 new vehicle sales. And from the indications I have, they have come up a bunch from Q1 and from last year — mostly because now there’s inventory, finally, and deals are being made again, and people are buying cars again!

“I see the drunken sailors all around me.”

Calling these morons who are spending all their income and going into debt on credit cards at 29% interest rates the equivalent of drunken sailors is an insult to our patriotic navy personal who occasionally get drunk but are serving our country with distinction at home and overseas.

No, it was just a misspelling. They meant, “drunken salers”, you know, people who can’t stand missing out on a good sale.

financing cars again. most of the cash buyers on the over 10 years old/older vehicles are few and far between.

Tech has most definitely slowed since the SVB thing and the last time I checked it wasn’t making it into the numbers, so I very much take the numbers with salt.

Tech layoffs — actual tech layoffs in the US, not announcements of global layoffs — made it into the numbers just fine. And we have discussed it here many times. You just have to pay attention. This BS about something “not making it into the numbers” is just BS.

And there’s a lot of demand for tech workers in other sectors (automakers trying to transition to EVs, oil and gas drilling, etc.), and good laid-off tech workers get picked up quickly (except when there’s age discrimination involved).

Can we now conclude that manipulated yield curves do not predict anything….but merely reveal the folly of central bankers thinking they can alter reality?

🤣🧡

30 year mortgages in the USA were below 5% for 12 years. It was an anomaly due to a financial crisis. Now a reset: expect rates to stay above 5% for the rest of your life.

The financial crisis did not last 12 years

They just couldnt stop….chose not to

The 10 year Treasury was posted at 3.84% today. That’s a big jump. Only one network covered it. Why didn’t the others? Their advertisers don’t want to spoil the party. The financial news media is totally corrupt. Wolf needs to confirm this jump in interest rates as it affects mortgage rates.

Mortgagenewsdaily is quoting 7.04% for end of today. 0.13% higher than yesterday.

30year conventional was low 7’s a couple periods since fall of 2022.

You better duck and cover SC, ’cause your ass is fix’n to get acronym’d.

No one knows for sure how or when this movie ends. What can an individual do? Be as liquid and diversified as possible. Have no debt, except perhaps on your primary residence. Live within your means. Then, when the movie ends and the credits roll, while others are running for the exits in panic, you can waltz out of the theater confident and eager to pounce on opportunities at a discount. We shall see……..

Look at coin melt values of current coinage, specifically; dimes, quarters, half dollars.

It’s at 20-25% depending on copper price. At ~12% or so monetary inflation, we reach melt equals face around late 20’s to 2030. The nickel coin, we know, is already at this crossroads.

Things go unnoticed unless they change drastically. Will a rush to hoard occur, similar to 1960’s, if they change the composition to zinc coated steel? Will mentality change either way? The great inflation began in the mid 1960’s, during the previous change in coinage.

Is a discussion of CBDC in antisipation of removal of coinage by 2030? If so, we hand to the squid the last bastion of national currency that isn’t tied to the federal reserve system, our coinage.

“antisipation”: n. – a teetotaler; v.t. – refusing to take another sip

Good catch. I have no excuse, but the bottle. The irony.

This is my plan of action!

Put this together with romping stock prices, and it’s clear money is still easy. Exactly where is less clear. It’s not because rates are too low, but it could have something to do with the fact that, unlike for most of history, the Fed is actually paying them to support its lower target bound. It could also have to do with, despite its QT program, the Fed’s balance sheet is still much larger than it was pre-pandemic.

Bottom line though … money is still easy.

Loved the article. Correctly framed the obvious dislocation between expectation versus reality that is itself, almost as stressful, as an excessively reported stock market decline.

The reality is hard to reconnoiter. Increasing “real GDP” in the face of strong headwinds seems exceptional. But is it ?

Real GDP has never increased in the face of monetary duress. Is the reality that the so called “free markets” are still controlled by the Fed and are stimulative. Rather than the popular word fodder about the terrible Fed putting the markets under undue stress.

The obvious is always the enemy of the published.

Wrong.

re: “Real GDP has never increased in the face of monetary duress.”

1980-04-01 -8.0

1980-07-01 -0.5

1980-10-01 7.7

1981-01-01 8.1

Whatever, what’s your point ? To get your jollies off by presenting an example of a time period in which real GDP advanced in the face of monetary duress, without a shred of shame.

Any prior period before QE is irrelevant, comparing apples to other fruit. A coward without the gumption to offer an alternative that would resolve his angst.

Well, doesn’t raising the interest rate just mean MORE money printing?

Where does the logic of this lead? Argentina has an overnight rate in the order of 97% and their inflation rate is about 109%

Coincidence?

We are a very long way from being Argentina but if we apply ourselves and choose bone-headed policies, we can definitely get there. One day, we can sing, Don’t Cry For Me, America!

How would raising interests rates have anything to do with ‘more money printing?”

More currency is printed by the treasury in service of dept.

The treasury can’t print currency, it can only sell treasury securities.

We should report this news to the secret service. The bureau of engraving and printing is counterfeiting federal reserve notes.

What are you talking about? It may be helpful to learn something about how the system operates. The Fed manages the money supply. The Treasury has no capacity to monetize its own debt by printing currency.

The Fed determines how much currency is printed each year, and the fact a division of the Treasury actually does the physical production of the bills doesn’t change this fact.

The fed only determines the minimum. A combination of the fed’s and treasury’s decisions account for total currency in circulation. The treasury prints the fed’s portion, which is what I said above, “printed”. I don’t get why this is confusing.

From Investopedia re: Who Prints Money in the US:

“KEY TAKEAWAYS:

-The U.S. Federal Reserve controls the supply of money in the U.S., and when it expands that supply it is often described as “printing money.”

-The job of actually printing currency bills belongs to the Treasury Department’s Bureau of Engraving and Printing, but the Fed determines exactly how many new bills are printed each year.

-When it is said that the Fed is “printing money,” the reference is really to the central bank increasing the money supply in the system, such as through quantitative easing (QE), an asset-purchase program.”

If this wasn’t the case, the Fed would not control the money supply. I don’t get why this is confusing.

I am curious though, where did you come up with “the Fed only determines the minimum”?

I’m wondering if it’s something like the Treasury replacing damaged bills or something, in which case it’s just replacing currency, not issuing new currency authorized by the Fed.

From the federal reserve website:

“The Federal Reserve’s role in coin operations is more limited than its role in currency operations. As the issuing authority for coins, the United States Mint determines annual coin production.

…

Coin held by the Reserve Banks is an asset on its balance sheet and the Reserve Banks buy coin from the Mint at face value.”

The Fed doesn’t “authorize” coinage. The treasury is issuing it’s own currency using the mint.

I also don’t like the above quoted statement 100%, since the coinage the treasury mints is also a currency, the face value is generally not a weight and not equal to the metal value.

You keep providing statements and quotes showing that the treasury “prints” currency, then use such to argue that the treasury does no such thing. Just because most people, who learn a bit about FR notes, believe that Jerome Powell has a printer printing franklins in his office, doesn’t make my statement inaccurate. It merely shows a lack of deeper understanding of the process, which is fine, given that it’s intentionally confusing.

First, coins are minted, not “printed” as you stated in the comment that started this off: “More currency is printed by the treasury in service of dept.” Now you’re talking about the minting of coins as opposed to printing currency.

Second, you should have included the full paragraph from the Federal Reserve website as it relates to the production of coins since it explains how the Fed influences coin production:

“The Federal Reserve’s role in coin operations is more limited than its role in currency operations. As the issuing authority for coins, the United States Mint determines annual coin production. The Reserve Banks, however, influence the process by providing the Mint with monthly coin orders and a 12-month rolling coin-order forecast. The Mint transports the coin from its production facilities in Philadelphia and Denver to all of the Reserve Banks and the Reserve Banks’ coin terminal locations.”

Finally, you state “You keep providing statements and quotes showing that the treasury “prints” currency, then use such to argue that the treasury does no such thing.” You’re making this up. I specifically said in a comment above: “The Fed determines how much currency is printed each year, and the fact a division of the Treasury actually does the physical production of the bills doesn’t change this fact.” No, I don’t think “Jerome Powell has a printer printing franklins in his office.”

Your original original comment to SoCalBeachDude is inaccurate because you implied that raising interest rates may cause the Treasury to print more currency in service of its debt. Laws and regulations can change, but that’s not how the system currently works.

FV = PV +I …. The interest needs to come into existance

FV- Future value

PV – Present value

I – Interest as cost of money for risk

Check how interest rate work on the money from a mathematical standpoint. Interest on money generate money.

Let me suggest an alternative view of why the Fed should raise the FFR ( Federal Funds Rate) the short term interest rate that the FOMC, the Federal Open Market Committee, controls directly.

The current yield curve is synthetic and in no way comparable to the previous yield curves before QE.

There is not one currency in the basket that is correctly valued. QE is a phenomena never attempted in the course of recorded human history beside the past 15 year, worldwide, experiment in interest rate suppression.

No, in a competently run economy, increased interest expenses will force tough fiscal choices and crowd out other government spending. Argentina chose a different path, and the results are not a coincidence. America gets to make its own choice.

We can just mint the national debt away.

That hasn’t worked well for the economy of countries that have tried it.

In Q4 2021 real GDP was $20T, today $20.28T, up 1.4%, after all the “printing”.

My current thought about the distribution of residual wealth at the end of the Fed glide path, which currently seems to be to inflate the economy with a stimulative monetary regime, that supports current asset prices until they make sense.

And who loses for this inflation and who wins. Who pays.

There is a group atop our society that makes one ponder the eternal question; how much is enough, that in their sociopathy, they lose site of the roots that made their impossible journey possible.

I recently became aware of the practice of the IRS to limit the claim for a refund for over payed taxes to a Congressionally legislated period of 3 years after which the government will take any monies which they could easily have returned.

The IRS calculates your tax return all the time to the point that they could mail one their tax return and if correct sign and return, like Sweden does.

Our government has been reduced to the sheriff of Nottingham stature. Swindling the poor and disabled to pay for the massive tax cuts, delivered to the least deserving.

One of my great great grandfathers came from Nottingham and here we are. No Robin Hood and his Merry Men (and Maid Marian) to foil the sheriff.

I think your wrong about no merry men. I think there is a plethora of merry men, standing by while the world changes, that I think will ultimately determine the terms of their engagement.

Just to further advance my argument I propose the theory that, from the moment of birth until the current day,

most men long to be merry.

There’s only one question that matters. Does Jerome Powell have genuine concern about the plight of the bottom 80%, particularly younger generations?

If he does, he should be selling assets from his balance sheet in sufficient quantity to reduce asset prices. It’s not just inflation that is smothering people, it’s also the high asset prices

How would the Federal Reserve selling its assets change anything?

Fed sells the assets aka reduce their balance sheet thus making LT bonds available in the market and it’d hike the LT rates

Same With MBS fed is holding

It looks like the government is fueling most of the inflation, according to these charts.

Well it seems I picked a fine time to increase the duration of my bond holdings. But in other news, the Fed says 37% of US companies are now distressed. Fortunately this move also reduced my corporate holdings a bit.

Lynn Alden suggests the Fed’s current response to inflation is using the 1970’s playbook which addresses excessive bank lending. However, she goes on to say that our inflation problem isn’t caused by excessive bank lending, but rather excessive deficit spending. But happily when the economy eventually blows up and nearly 40% of the businesses file for bankruptcy, that should begin to tame the rate of inflation a bit.

TARP didn’t stop the RE markets and stock markets from crashing. And not everyone is too big to fail.

Can blood never run in the streets again? I say it can and it will.

Would TARP have stopped the crash if everyone had known what TARP would do, though? This time there is expectation.

makruger

“But in other news, the Fed says 37% of US companies are now distressed.”

I really hate it when people post this clickbait headline bullshit here and don’t know what they’re talking about.

1. No, that’s NOT what “the Fed” said. But two researchers at the Fed published an academic paper. Link below.

2. This is how they defined “distressed”: “Firms in distress are those whose distance to default is below the 25th percentile of the distribution of distance to default across the sample.” Got it?

Kind of a funny definition of “distress,” LOL.

3. They found that even in the best of times 10% to 22% of companies are in distress, including in 2018-2019 (22% were in distress, LOL), because a lot of businesses are ALWAYS in distress.

And this is one of the charts:

https://www.federalreserve.gov/econres/notes/feds-notes/distressed-firms-and-the-large-effects-of-monetary-policy-tightenings-20230623.html

Thank you for putting this into perspective. I was wondering what the baseline was. It still might not take much to have more businesses stressed and topple the economy.

Wolf,

When do you expect the bond vigilantes to show up? 10 year treasury STILL below 4% and credit spreads fast asleep.

WTF!!!!????

They’re packed into the short-term corner.

Do you think that we will see longer term rates rise anytime soon, and if so what catalysts could cause that?

I am thinking (1) Japan easing yield curve control, (2) longer term treasury offerings late summer (maybe some 5 and 10 year zeros), (3) more aggressive ECB hikes.

Or is the loosening from China and Japan just keeping this circus going?

Now that is an absolutely correct answer, They stay in the short term corner because whilst the FED is swinging those dukes It can be hazardous to your health. But when the Fed stops swinging those punches they have some safety to exit.

Me, I am a lover, not a fighter :)

Everyone is on wrong side of the boat ,usually doesn’t end well

I have a stupid question: does it actually matter if we are in a recession or will be in a recession soon? What should matter is the situation that most people find themselves in. If inflation keeps increasing prices (even with disinflation prices keep going up) and people can barely pay rent and food and people get laid off, isn’t that a problem? If we are technically not in a “recession” because of government spending or some other reason but 50% of Americans (I made up that number as an example) live like we are in a recession, isn’t that what is important? Maybe we need a new “Quality of Life” metric because there seems to be a disconnect between a recession and the lives of many people right now. It’s just like when people say the economy is fine because the stock market is up. So why all the focus on recession when the focus should be on the quality of people’s lives?

I think, but I am not an expert at reading chicken innards, That we are entering a World Wide recession and that has not happened in a very long time.

China, bailed us all last time but this time they do not have enough in the tank to push another building boom. EU and yes even Germany are basket cases and little Britain doesn’t have a pot to pee in. India is developing but as yet no real muscle, Japan is confused and having its Lunch eaten by Korea and China.

The only one that can do anything is the US but they have lost all Industrial muscle and Ai is not a panacea.

Be prepared for ugly and watch like a hawk, World un – employment rates. That is the Key.

The government is not responsible for “the quality of people’s lives”. That’s the individuals responsibility. This “nanny government” attitude has got to die a quick death if this country is to survive in any recognizable form.

Remember: The U.S. Bill of Rights only speaks to life, liberty, and the pursuit of happiness. Nowhere in there does it guarantee any of the above.

Happiness is relative. So is quality of life.

That’s all fine and well, but it doesn’t mean that the government should be actively trying to make people’s lives worse.

I think the fairy tale of a “shrinking money supply” ( which is mathematically impossible in a debt-based fiat Money system) can now be safely put to rest.

R.I.P.

Wolf, you talk about both ‘low rates’ and ‘stimulus money’ as the drivers for inflation. What’s your take on their relative impact? Is this inflation driven more by the Fed printing or by government programs? Thanks

Inflation (consumer price inflation) is a complex phenomenon, driven by all kinds of factors, including critically mass psychology (the inflationary mindset where people and businesses pay whatever), without which inflation doesn’t thrive. Monetary policy and fiscal policy are also big factors. Then there are supply shocks, demand shocks, etc. Once inflation takes off seriously, it’s tough to bring back under control. That has been the case historically.

Saw a graph recently showing how real wages aren’t even close to keeping up with inflation these days, so you’d think that’d eventually affect their spending, but seems the asset bubble is keeping the money flowing at the top end still.

Gonna need to induce a ‘richcession’ but with all that free money floating around looking for a place to land it’s going to be awhile yet unless some black swan shows up to crap on the party lawn.

NQ 1W Lazer log : June 28 2010 to Aug 8 2011 lows // parallel from Feb 14

2011 high. There was no monthly close below the Lazer. Options :

1) In July/Aug NQ might drop to the Lazer to form a tilting H&S.

NQ might reach/breach a resistance line coming from Mar 2000 to

Nov 2021 highs.

2) A bearish option : NQ might drop below the Lazer to test 2020 low,

or breach it.

As Wolf said “People still spending like drunken sailors.”

YET

At the same time 34% say they can’t pay their Student Loans come October?

Weren’t you just on Spring Break? Now you’re broke all the sudden?

The people that can’t afford their loans are not the same group that own assets and have benefited from the ginormous asset inflation of the past years.

My point is that the same people who “can’t afford to pay” are also pissing away tons of money.

To your point, I doubt many 40s and below own a ton of stocks and bonds. Maybe 10% of them???

Cry me a river. If their student loans were suspended, did they bank that money in anticipation of the deferment / forgiveness not happening? No? Then too bad, so sad. Failure to plan by one group of people is not the problem of the people who own assets. People who own assets have those assets because they’re not stupid enough to p*ss away their money.

A smart person, “without assets”, would have continued to live like they were making those payments and bank them as they are a potential future liability. At worse, they’d be prepared for the unfavorable ruling and, at best, they’d start building “assets”and habits that would lead them to a more financially secure life.

Nope. Tattoos for everyone!

This isn’t a failure of those “with assets”. This is a failure of the schools/parents for not teaching home economics… budgeting, savings, power of compounding (both positive and negative), how to balance a checkbook, how to handle revolving credit, and other necessary life skills.

The schools/universities who helped them set up the loans, took their money, and the student graduated with a 2.5 GPA but has insufficient income to thrive, through no fault of their own – despite the degree which has proven worthless? They should be sued out of existence.

Put the onus on those that unfairly benefit… not on those who act responsibly. My DIL had loans. A lot of them. High 5 figures. She and my son paid them off…. and they took full advantage of the time where interest wasn’t accruing to do so. Now they’re out of debt and are building assets through their responsible behavior – despite their friends telling them they were stupid for paying off the loans because “free money”.

So a stronger economy is driving rates higher. People speak of sticky inflation but it is rates that are proving to be sticky. Lower inflation is great but it’s higher rates that will slow economic growth.

High rates contributed to the banking crises, CRE meltdown, and the housing freeze. But it’s sticky rates that will ultimately bring down the economy.

State of Indiana just announced we are finalists (of two) for a 50 billion dollar chip plant being proposed near Indy.

Eli Lilly building a 3.7 billion expansion near Indy.

New Battery plant being built in Kokomo IN for 2.6 Billion.

New Battery plant in New Carlise IN for 2.5 billion.

Andretti building HQ in Fishers IN for big bucks.

Many other projects underway….I could list another 10 major projects in IN

This is just Indiana

Recession……dream on. Rates will stop non of this. This is a runaway train brought to you by a political party desperate to avoid recession during an election year.

I’ve been reading a lot about the impact that higher and stickier rates are having on Indiana’s RV industry. Glad to hear some good news out of IN

Agree that this administration will do anything to stay in power which is part of the reason that rates will eventually “un stick” to juice the economy

The US Supreme Court has just struck down the bizarre and stupid notion of any student loan forgiveness and those debtors will have to start repaying their student loans in the coming months, years, and decades for the services that they chose to purchase all by themselves.

Believe me: These student loans would never be repaid.

Biden already working on it to circumvent supreme court decision.

Also, in next 5 years, FED balance sheet would be much much higher.

“The Fed has jacked up interest rates to over 5% to slow down this circus, and instead we’re getting accelerated growth.”

Because they stopped lifting rates, and they signaled their intent back in the fall. Even the dullest of the dull can see right through the FED. They are inflationists.

DC…….

As you have pointed out many times on this site.

Powell is intent on monetizing the fed debt, transferring wealth from poor to rich and keeping his job.

He is doing a great job. Can’t wait til the day when the national oil reserve is empty……..Warren Buffet a wolf in sheep’s clothes is salivating over 150 per B oil. He just bought more Oxy.

Can you imagine what the inflation numbers will be if energy turns up.

Of course by then Powell ought to be at 6 to 7 percent…..with inflation at 10.

Warren Buffet is not a wolf in sheeps clothing. I had the pleasure of meeting him years ago when he came and spoke at one of my college classes at the University of Nebraska. He’s an extremely kind and generous person. He spoke how he raised his kids to stand on their own two feet and earn their way in life.

AAPL $3T ukulele.

1) Interesting: “this administration will do anything to stay in power”, in light of the previous administration attempts to stay in power.

2) Record-breaking government spending is typically the norm of governments everywhere, always.

3) Borrowing is a bet on the future. When your “team” does it things are great. When the other one does, it is a bad idea.

BS is in the eye of the BS’er-and it is harder to clean up than make.

If you are referring to me…….Both sides are as guilty as sin.

It’s not about sides, it’s about retaining a capitalistic country that made our standard of living the best.

When the government is 50% of the economy DC decides who does what and how much. That will not produce a good future. You do not borrow your way to wealth unless you are borrowing to build productive assets ordered by the private economy. Borrowed funds to buy warships and unearned benefits are flushed down the toilet.

I will not respond to any further comments because I have more productive uses of my time.

I can´t understand. The media say that the economy is growing, and I read a commentator who talked about the strong economic structure of the US.

Today I read this