Month-to-month, durable goods prices rose again, on price spike of motor vehicles, after steep drops; services might be cooling a little. Energy plunged.

By Wolf Richter for WOLF STREET.

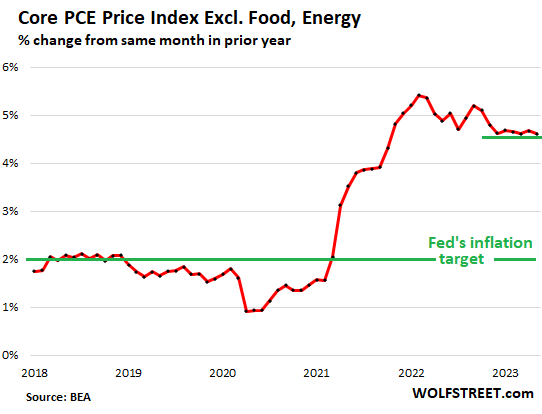

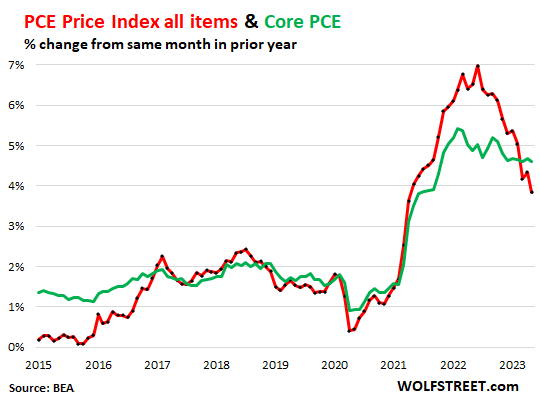

The core PCE price index, which excludes food and energy products and is the inflation measure favored by the Fed, dipped in May to 4.62%, from April (4.68%), but was above March (4.61%), and was exactly where it had been in December (4.62%), and has essentially gotten stuck in this narrow range and gone sideways for the sixth month in a row. The Fed’s target is 2%:

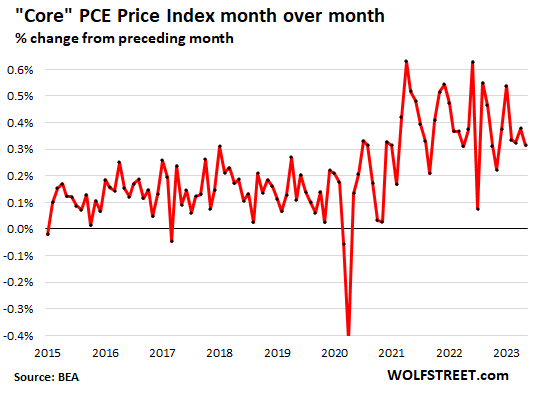

Month-to-month down trend, or not? On a month-to-month basis (green in the chart below), the core PCE price index has oscillated in a dizzying manner since 2021. The oscillations now appear to settle down somewhat. In May, it rose by 0.31%, a slightly smaller increase than in April (0.38%), but roughly the same as in March, and right back where it had been in October (0.31%), according to data from the Bureau of Economic Analysis today. Core PCE has been in this range of 0.3% to 0.4% for the fourth month in a row.

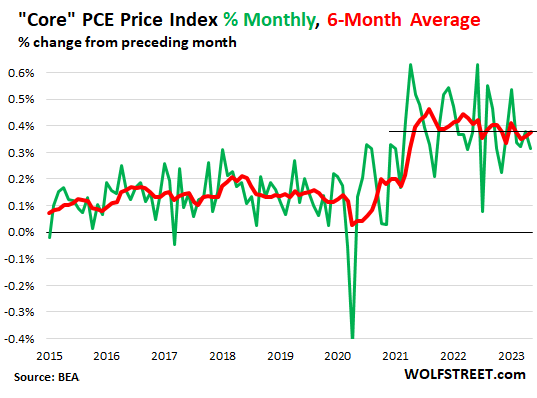

The six-month average of Core PCE (red line in the chart below), which smoothens out the wild volatility and gives a better feel for the trend, was 0.38% in May, same as in November. You can see how it trended down through late 2022 and has then remained roughly in place since then. The six-month average of core PCE priced index in May of 0.38% translates into an annualized rate of 4.7%.

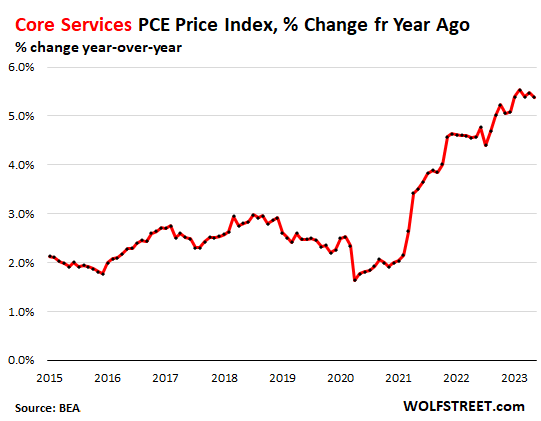

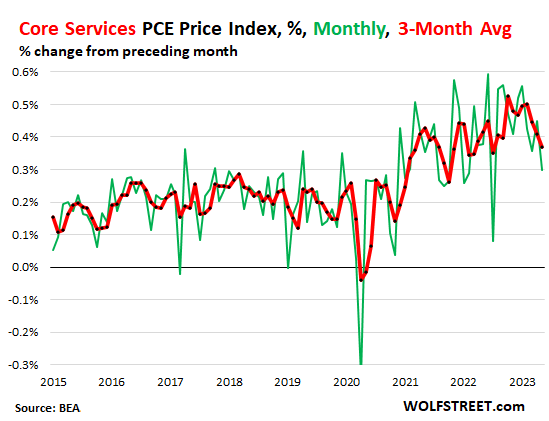

Core services inflation (without energy services) rose by 5.4% in May, year-over-year, a hair lower than in April (5.5%), but same as in March (5.4%) and in December (5.4%). It has been stuck at roughly this level – the highest level in four decades – for the fifth month in a row:

Month-over-month, services inflation appears to be cooling off a little. In May, the index rose by 0.3%, a smaller increase than in the prior months. In April it had spiked by 0.45%. The three-month average came in at 0.37% (red line), showing a three-month cooling period. But it remains very high. That three-month average of 0.37% is 4.5% annualized.

But then, inflation is a weird thing. For the three months through October 2021, there were the same kind of hopeful downtrend of the three-month average, only to reverse and turn into a long uptrend.

The game of inflation whack-a-mole.

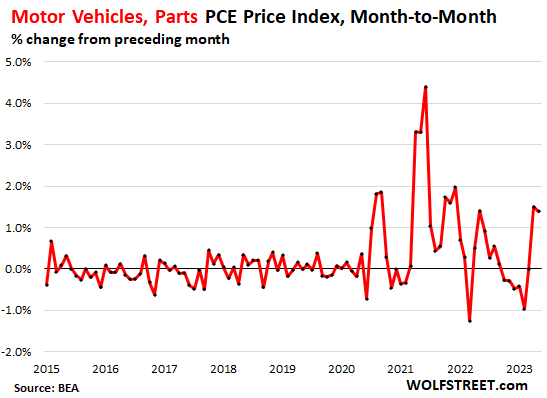

Prices of durable goods, which had been plunging, with negative month-to-month changes, rose again on a big spike in motor vehicle prices.

The index for motor vehicles and parts spiked by 1.4% in May from April (18% annualized), after having spiked by 1.5% in April from March. So that’s not good. This spike might not last, but who knows, prices have done strange things over the past two years:

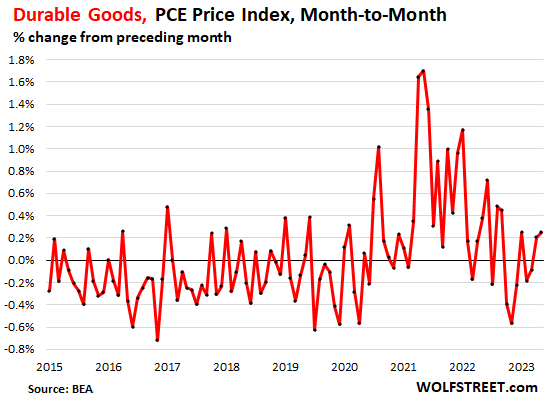

The index for durable goods rose again month-to-month, after having been largely negative since last fall on a month-to-month basis. In May, it rose by 0.25% from April after the 0.20% increase in April from March.

The drop in durable goods prices over the past 12 months – with actual negative readings – had been a big contributor to holding down core PCE inflation. What we saw over the past two months is that this episode of price plunges appears to have ended.

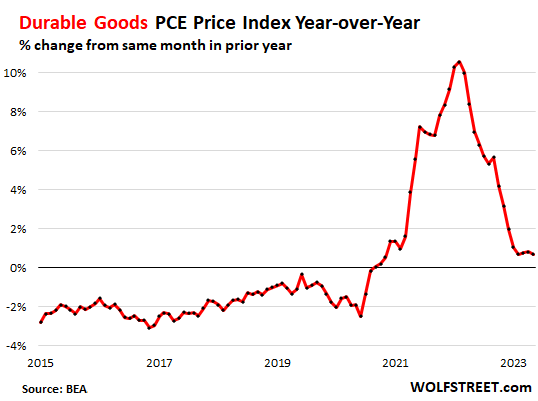

In normal pre-pandemic times, the index for durable goods – manufactured goods that are intended to last a while – was negative year-over-year, driven by improvements in products (hedonic quality adjustments), manufacturing efficiencies, offshoring, and competition.

After the huge year-over-year spike in durable goods prices in 2021 and the first half of 2022, the index now seems to be stabilizing at a positive rate, rising 0.7% in May, roughly the same over the past four months, rather than reverting to pre-pandemic negative rates:

The PCE price index for gasoline and other energy goods plunged by 5.6% in May from April, and by 21.9% year-over-year. This plunge in energy prices pulled down the overall PCE price index.

Food prices, after dipping month-to-month in March and April, rose a tad in May. This reduced the year-over-year increase further to 5.8%, the least bad increase since December 2021.

The overall PCE price index, pulled down by the plunge in energy prices, rose by 3.8%, the lowest since April 2021.

The overall PCE price index was below core PCE for the third month in a row, the result of the plunge in energy prices. Core PCE shows the underlying inflation trends beyond the volatile food and energy components.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Seems huge disconnect between market and Fed. Market thinks Fed will go back to ZIRP and QE.

Random Intime – Yes, a major disconnect. I am scratching my head as to how the S&P 500 can be up 1.3% today as I write this comment and the NASDAQ is up 1.6%. Inflation is not under control, at least not compared to the Fed’s 2% target for Core PCE. The only way to make the market valuation math work is to assume that interest rates will decline in the near future because the Fed will give up the fight to bring inflation back to anywhere near 2%. As Wolf has pointed out repeatedly, this is a bad assumption if you believe what Jerome Powell has said over and over again. I cling desperately to the hope that the Fed will do the right thing and not capitulate to the politicians, both Democrat and Republican, who want the gravy train of low interest rates and overstimulation to keep on rolling.

Its simple, nobody believes the FED…the recent pause in rates represents ineptitude of the highest order…or its part of the plan for the rich…

And everybody blames the markets for not believing the Fed, but if the Fed hadn’t set its own credibility on fire this wouldn’t be a problem.

And they shouldn’t believe FED. Its almost comical how people expect FED to fix the problems that arose as a result of their own actions.

Then there are arguments such as “well FED was under political pressure”, if that was the case than FED is even less capable to fixing anything, because the minute political pressure arise again they will turn on a dime.

I agree with Larry, if Fed were serious, they wouldn’t have paused.

Market thinks Powell is bluffing, Fed is using tough talk instead of rates to bring down inflation.

I think Fed wanna give banks some relief. Banks probably begged Fed not to raise rates any further.

Treasury isn’t enjoying high rates either.

5 trillion dollar covid stimulus is probably enough to keep the economy going for several years.

fed needs to keep raising rates

should be 8% today

of course real problem is GOVT SPENDING

only the 1% of the mic/neocon or big corporates like chip makers get the big $$$

then they buy everything at whatever price it takes

I don’t think it’s the FED is the issue here. The main issue is US GOV spending like a drunken sailor. If you have 2 Trillions deficits then you are spending too much. All that money ended up in the eCONomy and are pushing stocks up to atmosphere. Until Uncle Sam reigns in its spending, all hope is lost. That is why the FED is saying “higher for longer” b/c they KNOW Uncle Sam is full pledge drunk.

It could be that government spending will continue without slow down ever. Federal, State, and Local govt expenditures are over $10T/yr per FRED St Louid Fed data series SLEXPND and FGEXPND. That’s a huge percentage of GDP. So that money will get spent and probably buying overpriced goods/services and contracts from large corps (not mom and pop). Also productivity will go down from more government spending and payrolls.

Eventually with enough inflation and currency devaluation owning a productive asset (company) is not a bad idea. Stocks are still down quite a bit from all time high and o/n RRP has come down a couple hundred billion that is helping with keeping liquidity going in the short term. You will need to bring liquidity down more to bring stocks down as then they sell stocks to get liquidity to cover their issues in the real economy.

so I needed back brakes on my f350

brakes, 2 rotors and 1 caliper

mechanic rate was $135 hr

total cost $1,666

These pivot-mongers and squawkers are the definition of delusional stupidity, especially at this point. It’s exactly that sort of thinking that led to the worst bank failures in the US since 2008 earlier this year with SVB and the other pivot-fantasizers who failed to prepare for the higher interest rate environment. The Fed simply can’t afford to throw in the towel on inflation as that’ll wreck whatever’s left of affordability for basics like food, rent, healthcare and vehicles, Wolf’s had like a dozen articles on this. (And worth noting that a big reason for the upward GDP revision yesterday was due to healthcare costs getting more expensive and a burden–not a good thing for Americans in general and another red-flag on how useless GDP is in some ways for actually measuring things of actual value in an economy) Not to mention making the US dollar even less attractive as a store of value at home and abroad–already much of Asia has fast-pivoted to using alternative value stores (and not just other currencies, their own and others, but whatever they can use other than a depreciating dollar), Bloomberg and Forbes even had articles on this.

All the inflation in housing, basic goods and services was bad enough but it’s even less affordable now with so much of the pandemic stimulus and massive government fiscal stimulus expiring basically this summer. Whatever it’s underlying merits, the Supreme Court’s recent decision striking down student loan forgiveness will throw a lot of oil on the fire economically, that’s a minimum 45 million American adults who now have a big hole in their monthly budgets starting in late July with high student loan repayments returning (even earlier for a lot of graduates re-starting the payments early). But then also the multiplier effect with all the shops, services and businesses that will have less money each month too. And then expiration of the eviction moratorium, Medicaid help, food stamps benefits, higher household debt to begin with (plus the Treasury having to raise money to cover so much of that extra debt from the deal earlier this month) and Americans are going to be absolutely crushed even worse by all this inflation. They simply can’t afford these prices, and the Fed cannot afford to let the foot off the gas of interest rate hikes and much more aggressive QT.

Agree 100% with what you said and what the FED should do…problem is they have taken their foot off the gas…they are allowing this narrative to continue by not being aggressive…inflation isnt 5%, we all know that..its more like 10% easy…

Larry, no matter what the Fed does, the pivot mongers will say it’s dovish. If they raise by 0.5% next month, they’ll say it’s “bullish” for stocks because it wasn’t 0.75%. There’s nothing the Fed can do to make these people get the picture other than stay the course.

Be patient. 5.25% interest rates WILL cause bankruptcies of many zombie companies. It just takes time for their debt to rollover.

There is still plenty of stimulus from higher government spending and above longer-term trend deficits. Government spending = someone else’s income.

I would say that the Fed is waiting on raising interest rates for two reasons. First, student loans will soon begin to be repaid. That is an average of $393 a month on 32% of the 25- to 34-year-old population, which are prime consumers. For people earning $75K a year or even $100K a year, who have high fixed expenses, like housing, that is going to be a big drag on their spending.

Second, the Fed is waiting to see the impact of much larger Treasury issuance on long term rates. The supply-demand side of Treasury issuance will be enough to push higher rates, which will cause asset prices to fall based on discounting calculations.

Earnings calls this quarter will have some real caution in forward guidance, because companies know that demand will be weakening.

Apple is so overpriced right now that it is insane. The company is definitely one of the companies that will feel the impact of lower consumer demand. It is easy to just keep your iphone if it works properly. It is the definition of a discretionary expenditure.

“believe what Jerome Powell has said over and over”

You’d be nuts to believe what Jerome Powell has said! Better to pay attention to what he has done. He tucked tail and pulled a u-turn back into QE earlier in his tenure, a move from which his credibility never recovered. He farted out $5T at the drop of a hat to ignite inflation, then sat idle on that “transitory” inflation for at least a year too long. He has cautiously favored allowing inflation to run hot with mostly .25% hikes over the risk of startling the super-wealthy (for whom he works, not us peons). He has stood behind a relatively tepid cap on QT, the one really meaningful inflation fighting tool he has. Then when a failure pile of a high risk investment bank (SVB) sneezed a little too hard, the fed jacked their balance sheet back up with 400 billion of not-QE (nothing to see here) before resuming weak QT so that the Fed’s balance sheet is right where it was at the beginning of March as we go into July. And they’ll do it again the next time some other institution cries uncle.

We shouldn’t believe a single word out of Powell’s mouth. He doesn’t work for or care about you and me.

But the people who refused to believe Powell since September 2021 have gotten tangled up in their own underwear: They said he’d never end QE, he’d never raise rates, he’d never do QT, he’d never-ever take rates to 3%, LOL, because he’s trapped, etc., etc., and for a year these people have spouted off just ridiculous BS and have been proven wrong by Powell every step along the way.

People should do the believing in church. People who say that Powell isn’t serious after he raised from 0.25% to 5.25% in 14 months, the biggest and fastest increase in 40 years, are just silly.

Last time the Fed raised to 5.25%, we ended up with a Financial Crisis. So not serious?

So far, he took down only four major banks — rather than the whole banking system, as last time. And instead of printing trillions and doing QE infinity to undo the damage, as Bernanke had done, he bailed out depositors but wiped out the investors of those banks, and that bailout spike on the balance sheet has already been worked off in less than four months.

Perhaps the discussion shouldn’t be strawman’ish.

“Some people said JP would do X and then he didn’t. Joke’s on them haha”.

Instead discussion should be in what JP actually did or didn’t do.

Despite what some people strongly feel, QT has been in name only and hasn’t reduced total Fed assets in any significant way.

” QT has been in name only and hasn’t reduced total Fed assets in any significant way”

BS. The balance sheet is down by $625 billion. $625 billion is a huge amount. It unwound 13% of the QE done since March 2020 (despite the bank bailout measures, LOL). I hate this kind of QT-denier BS.

This is precisely what the market is pricing in. Not an imminent return to QE or ZIRP (though certainly possible in a recession), but a de-facto abandonment of the 2% target as it’s far politically easier to tolerate ~3% inflation with a booming economy than raising rates to 6%, 7%+ for 2%. They won’t say it explicitly as it destroys their credibility, but they’ll take their time & skip rate increases like they did last month.

The 10-year yield is pricing in 2% inflation long-term. If they wake up to 4% inflation long-term, the 10-year yield will jump to 6%, corporate AA-rated 10-year money to 7%, and mortgage rates to 8%. Are markets ready for that kind of bloodletting? I think it would be kind of fun to watch.

The economy isn’t booming. GDP growth may not be accurate but doubt it’s that inaccurate.

Wolf’s comment here is quite interesting. If the market does start to believe that higher inflation is going to be allowed, then long term rates go crazy. That is far worse for the economy.

gametv

the interesting thing is that the wolf repeats this in almost every article of his.

I’m starting to think that most people here only read the title of the article and some don’t even read the title. Otherwise, I can’t explain how they miss all the basic things said several times by the author.

Saw a article by maneco 64 who studied rip going back to 1913 to present inflation has averaged 4.6% right on target

Russell Napier has a few interesting interviews. His thesis is that we are in for a long period of financial repression. Inflation will run at 4 or 5 but interest rates will not be allowed to rise. Like between 1939 and 1979. This will be achieved no longer so much through QE but through other gimmicks such as captive bond purchasers (eg financial institutions that are required to invest into gvt bonds regardless of yield) and through gvt loan guarantees and state pressure applied to banks to keep lending at below market rates.

Sustained high inflation is vicious especially for the working class and poor the world over

May be no. May be Fed is overselling the meager QT and the market can see all the liquidity they need:

1. Fed Reverse Repo over $2 Billion.

2. Long term interests still below core CPI => Negative real rates => Hyper liquidity.

3. Govt printing trillions.

4. Total Fed balance sheet has not budged in 4 months. Any treasury sale is made up by bank bailouts!

5. Even Bitcoin crap above $30,000.

6. Nasdaq rallied 30%.

System is FUBAR, sorry to crush your hopes.

“Total Fed balance sheet has not budged in 4 months.”

Nonsense. The entire $390 billion bank bailout spike that you people (yes, YOU Leo) hyped as “QE” all over again has now been worked off, and the balance sheet dropped by nearly $400 billion from the peak of that bailout spike and is now back where it had been just before it. It has been dropping at a rate of about $115 billion a month from that bailout spike.

What effect does the endlessly loose conditions in China and Japan have on inflation here? It seems like this is major factor as to why stocks refuse to go down (and long term bond yields refuse to go up).

Thoughts on when this dynamic might reverse?

Does anyone really expect balance to go back to pre pandemic levels. Fed at this point has hard time meeting MBS targets. As soon as there is a smallest trouble Fed will start some sort of QE. They might even do CMBS QE this time.

Random Intime,

Four major banks imploding is not “a smallest trouble”– that was the potential beginning of a financial crisis. And less than four months later, that bailout spike on the balance sheet has been worked off. Compare that to Bernanke who did QE infinity.

The Fed isn’t going to do anything with CMBS because there are no banking issues involved. Their holders are spread far and wide across the globe. No one really cares except the holders — and many of them don’t even know they’re holding them. You have them in your bond fund.

The bank bailout spike has been “worked off,” but is meaningless for the population that is neither in the banking industry or in the Federal Reserve’s slow rolling facade of fighting inflation.

The fact is undeniable that any inflation fighting economic effects of QT have been stalled for the 4 month breakeven, from an already tragic snail’s pace.

The Fed’s balance sheet would be (should be) below $8T, if not counting the ‘inconsequential’ spike, following the curve of the graph. I guess time is inconsequential.

So if we’re not calling that QE – IT WAS – then there has been ZERO QT since Feb/March. The FED is a joke. That balance sheet is a joke. The whole thing is smoke and mirrors BS. All of the tough talk by the FED about QT turned out to be, again, BS.

Depth Charge,

I was just going to say, “You’re joke too, Depth Charge.” But I’m not going to say it because you might take it wrong. You’re funny, for sure, in an aggrieved sort of way.

The way I see it, while that spike has been worked off, that was 3 months ago, so for it to truly have been worked off, the balance sheet would have to be around $210-$270 billion ($75-$90 per month * 3) below the point at which the SVB spike happened.

So it’s good that a lot of it has been worked off, it certainly hasn’t been all of it.

Looks like its almost time for more “bailouts”. :)

I think the point is the balance sheet is at the same level as 4 months ago. That is obvious from your chart and it isn’t nonsense. Pumping it up bigly and then letting a little air out isn’t going to do the job.

“I was just going to say, “You’re joke too, Depth Charge.” But I’m not going to say it because you might take it wrong.”

But I haven’t done anything to harm anybody, Wolf, while the FED has destroyed millions of lives. Shelter has become a luxury. Autos, a luxury. All due to their reckless money-printing. But I’m the joke? I don’t understand. Why have the people who criticize the FED on your site suddenly become a lightning rod for your criticism? I don’t get it.

Depth Charge,

Criticize the Fed for the right thing. There was a time when the Fed watched inflation spiral out of control while it repressed interest rates to 0% and did $120 billion a month of QE. I called it “the most reckless Fed ever.” And it was.

But the Fed has made a U-Turn. This is now the most hawkish Fed in 40 years. It has raised rates by the fastest in 40 years, and it’s doing the biggest ever QT.

Is it not hawkish enough? Maybe. Is it too hawkish? Maybe. We’ll find out. But it is the most hawkish Fed in 40 years. All kinds of things are already blowing up, including major banks and CRE because of high interest rates.

Banks blowing up because of high interest rates is a scary thing. The S&L Crisis started out that way. Then came the second leg of the S&L Crisis, when credit turned bad. So now we have the first leg, much higher rates; and we’re going to get the second leg, credit going bad. Some of that second leg is already happening.

You’ve got to acknowledge the Fed’s U-Turn and what it is doing, or else you’re just a jokester. Lots of people hate the Fed and they hate whatever it is doing, no matter what it does. And that’s fine, but I get tired of seeing this nonsense here.

“You’ve got to acknowledge the Fed’s U-Turn and what it is doing, or else you’re just a jokester.”

No, they f**ked up and paused, Wolf. That’s my whole point. They continue to f**k up so I will continue to point that out. All of their bold talk of QT was a bunch of horsesh!t. Remember when they were talking of selling MBS outright and you were talking about that here? Wha ha-ha-ha-happened with that, huh? Convenient to gloss over.

“Most hawkish FED in over 40 years.” Yeah, after the most disgustingly reckless display of money-printing in the HISTORY OF THE WORLD, yet they paused at a measly 5% and change FFR with CORE CPI stuck at a 38 year high of 5.4%.

And you accuse me of “wanting to burn it all down” because I wanted them to continue with a 25 basis point rate hike last meeting. Something’s not adding up with any of this, Wolf, and you are acting like when I criticize Jerome Powell that it’s a personal attack on you. IT’S NOT.

Wolf:

IMHO, as well as your very clear former articles, the following is not correct:

”All kinds of things are already blowing up, including major banks and CRE because of high interest rates.”

1. ”major banks” have blown up because of bad management and cronyism.

2. CRE has blown up because of the WFH, AKA WFA trend taking place due to pandemic.

3. Clearly, every metric of financials, money, investments, etc., has been distorted in new and unique ways by the trillions of USD given since 2019.

After consideration of those 3 foundations of the current crazyness, then I agree FRB is at least trying to bring situation down without the major crash that almost certainly would have happened and still may take place.

“No, they f**ked up and paused, Wolf.” What makes you think a pause was a mistake, and what makes you think you know the future? What are your credentials on the subject that give you this insight that Wolf and the Fed don’t have? What analysis have you done?

Learn from Wolf. “It not hawkish enough? Maybe. Is it too hawkish? Maybe. We’ll find out.”

There’s a lot of wisdom in those words. When someone says they know the future they’re either lying or ignorant. Hitting the breaks could be preventing a bank meltdown. Patience dude.

There is STILL about $4 Trillion too much out there…..COVID spillage and QE…IMO

QT and huge auctions coming….it will be interesting.

AI seems to be a “tout”….. get into some AI stocks now before its too late!

and the ramping up of indexes for the quarterly window dressing….

Wind power, windmills, water power, stemcells, dope stocks et al. all of them virtually went to zero with AI next in line. Don’t get suckered into the ponzi.

AI is real, but the winners are not so obvious. Nvidia already saw the big boom in its valuation.

There will be lots of companies that were positioned at AI companies that really go nowhere.

Think of each time the Fed raises rates as hitting a glass ketchup bottle. Though it was delusional to think that ketchup will come out on its own (transitory inflation) it’s perfectly reasonable to think one of these hits will eventually get a big ol’ blob of ketchup out.

That blob could be big enough to mean actual deflation, back to 2% or just down a bit of disinflation and still need more hits.

The lack of linearity and control over the situation means it’s entirely possible the Fed does have to go back to ZIRP and QE faster than it anticipates.

Deflation is what we need. Czech Republic used to be a boring but stable country with a stable price level. Price level is now 50% up since 2019. That’s a wealth tax of 33% on money. If price level was 100 in 2019, it should be at 120 in 2029. We need 20% deflation between now and 2029 for the central bank to restore its credibility. If this does not happen, I will see it as proof that Czechs are scammers and Czech currency is nothing but an emanation of hyperinflationary Czech genes (unless I can come up with a better insult by then).

Recessions and depressions bring deflation. IMO until we have one of those, we will have inflation, regardless of what the fed does.

The Federal Reserve needs to quit running frontman and try to protect the Joe Biden Administration the party is over the money has been spent it’s now coming home to roost, we should have never pause raising the interest rate just two weeks ago these interest rates need to be around 8% to tame inflation and to slow down employment

Powell says keeping rates up till 2025. Personally, I think rates stay around this level forever. It’s actually better for people to have a savings rate around 4.5- 5.0.

Problem with 5% is $6 T of government debt is due next year and interest payments will quickly be $1T on its way to $1.5T. Then when recession hits tax revenue declines and you get close to doom loop without near zero rates or another Central Bank innovation.

There is no central bank “innovation”.

Actual USG credit is the worst since at least WWII. Since it is, it’s market psychology supporting first the FX rate and second, the bond market.

The actual long-term US fundamentals are also actually awful, regardless of how it compares (favorably or not) to the rest of the world.

The basis of EVERY central bank’s power and influence is the national currency. Other countries and their residents are stuck with the USD previously accumulated from trade deficits, but they can conduct foreign trade in another one going forward if they choose. They can also crash the USD by selling assets in the capital markets, regardless that there isn’t enough real wealth and US based production for them to get rid of it.

OS…

and they will blame the interest rates, rather than the debt, for the condition.

The interest rate cycle almost certainly turned in 2020. The one dating back to 1981.

If it did, the FRB can’t reverse it and rates are destined to “blow out” years from now, inflation or not. If they could, interest rates never would have reached prior (1981) levels and the same is true for other central banks.

There are no “wizards behind the curtain” at any central bank or treasury department.

Thanks Wolf,

Looks like a bullish flag on core inflation!

The market and Powell thinks inflation is under control.

Here is the proof for this:

1. Market is up and up and up.

2. Powel may something but his acts tells us something else. Powell paused and his QT is too slow and too little. if he really thinks that inflation is too high then he’d not have paused in June but have hiked by 50bp and would have been more aggressive with his QTs.

3. Although he historically hiked quite fast in last 1 year or so but it was also historical to print so much money so far and rates were kept quite low for last 15 or so years along with QE.

I think the end game is: Rich would become richer, middle/poor-class would be screwed which is happening for last few decades but people don’t feel it like boiling the frog slowly.

Market doesn’t care about inflation. Market thinks soon Fed will take rates back to zero and start new QE. Already walstreet started planting news in media why QE is needed to support $2T deficit/year for foreseeable future.

“Market doesn’t care about inflation.”

The markets delight in an inflation that is not addressed with higher rates.

Per Wolf’s last graph, overall inflation continues to drop rapidly while CORE PCE remains stuck. A high and sticky core leads to high and sticky rates. These rates that took out three major banks, helped CRE bleed out, froze the mortgage and housing market will do further damage as they “stick” to the economy.

Higher and stickier rates are replacing inflation as the biggest concern.

PCE is right where the Fed wants it right now.

Once again the elephant in the room is the annual Federal spending and budget deficit. While the financial media is laser focused on 1/10th of 1% drop in the PCE index YOY which is a change in the second derivative of the inflation index over one month, the huge Federal deficit of 2.2 Trillion is ignored by the mainstream media. You hardly find any reporting of this astronomical number. And this is after they passed the debt ceiling bill. So, I’ve concluded that it is a waste of time listening to these shills on CNBC and elsewhere. They are all bought and paid for to promulgate BS Non-stop 24/7 to the masses.

Its a pity that those who are struggling can’t vote their way out of this squeeze, with no real sensible options on the coming horizon. I guess it is like being the kids in a family with two totally fiscally irresponsible parents.

That’s why FAMILY is most important thing in life,take care of each other if possible

Perhaps the traditional French response of rioting in the streets would get through to our rulers.

Think the American lower 49% will ever be up for that? Nah.

One perception the mostly idiotic commies got right is the slogan, “Voting is the bosses game”.

Deficits and the national debt don’t matter until they do. Recent actual USG credit quality is the worst since at least WWII.

RRP $3T. Investors fight inflation by investing in the stock market for the long run.

Banks dumped $600B of assets in May. The 10Y is good for unrealized losses. They charge between 7% and 30%, no less.

Banks profit margin is low, but the good old days of mortgages between 2.4% and 4% are gone.

Is a 3 handle on overall PCE why the markets are turning into rocket and moon emojis right now? I just took a look at the PCE headlines and most of them have an “inflation is dead” ring to them. Buried in the articles themselves are slivers of the inconvenient truth Wolf so eloquently lays out here.

The problem is that we as a species have devolved into headline readers, lost in a never ending scroll of information where we seldom bother to RTGDFA, let alone actually engage with the material in a meaningful way. With our younger generation growing up on TikTok, I don’t see this problem getting any better.

My guess is that the markets are convinced that the 5.25% interest rates will cause things to break relatively soon, and the Fed will return to ZIRP and QE. That’s the only way today’s stock multiples are even close to justified.

Warren Buffett said P/Es of 30 are justifiable if you have permanent ZIRP. Right now, we’re at 5.25%, and will likely be at 5.5% in a few weeks. Something is off.

The only thing deflating at this point is Annheiser Busch’s stock price.

Blackrock pushed the agenda ,now Larry Fink is backing down ,also backing away from esg,. Keep up the good fight we the people. Shall not be manipulated

After the last FOMC it is time to place the phrase: “data driven” on the same ash heap of gaslighting history as “transitory.”

Curious how these numbers will change after the resumption of student loan payments in September/October.

I suspect a good portion of those ~$300/month payments have been going to goods and services instead of into savings or to pay down debt.

Maybe their parents will raise their allowance to makeup for the shortfall. A lot of these kids will go on a spending spree to make sure they’ve got no money when it comes time to paying back those student loans.

Biden’s got a new plan already…From NPR:

President Biden also shared Friday afternoon that his administration will create a “12-month on-ramp payment program” as part of his “Plan B” solution to deal with student loan debt.

Under this program, Americans won’t face the threat of default or harm to their credit for the first 12 months that debt repayments are due, he said.

Additionally, the Education Department will not refer borrowers to credit agencies.

This plan will run from Oct. 1, 2023, to Sept. 30, 2024. Loan payments will be due and interest will accrue during this time, but the White House said interest will not capitalize at the end of the on-ramp period.

Additionally:

Under a new repayment plan outlined by President Biden following the decision Friday, borrowers’ monthly payments will be slashed.

The Saving on a Valuable Education (SAVE) plan, which student loan borrowers have to enroll in to get access to, would allow them to make $0 monthly payments.

Undergraduate loan borrowers will only have to pay 5% of discretionary income each month — down from 10%. Additionally, borrowers won’t be charged monthly interest.

Loan balances will also be forgiven after 10 years of payments — instead of 20 years — for borrowers with original loan balances of $12,000 or less, according to the White House.

The Democrats are repelling a lot of intelligent moderates with this student loan BS, and these are the folks who vote.

Yep, I’m an independent and getting tired of this. I just read he’s now trying to still do loan forgiveness using a 1965 act even though SCOTUS said today only Congress can do that large and broad of forgiveness. This is getting ridiculous. The changes to loans he already is making will be extremely inflationary as he is only making it that 5% of discretionary income has to be used to pay loans instead of 10% (some with “$0 payments” which is a joke to describe it like that) plus all gone after 10 years. So basically we can all go to school, get it paid for with loans for housing and food, and never have to pay it back (or at most 50% of your annual discretionary income). Might as well go to school forever.

Yeah, I simply can’t fathom how the government can just pick and choose which consumer debts to forgive. People don’t ask to get sick but you have to go out of your way to get a student loan. Its a pathetically short-sighted move and does nothing at all to fix the problem. Politics in a nutshell

I think Jerome Powell is being callous towards the 90% by taking his time getting to 2% inflation, while allowing inflation to run at a steady 4-5% for several quarters now. He could clamp down on the inflation immediately by reversing out the money he printed (by selling assets on his balance sheet) and allowing asset prices and RE to significantly correct, which would only reverse a couple years of undeserved speculative gains. This slow walk of QT is allowing inflation to entrench at the 4-5% level.

Apparently Jerome Powell doesn’t think wealthy asset holders should contribute anything to the inflation fight. Poor and middle classes, as well as younger generations, must shoulder the burden and make all the sacrifices.

The student loan program should be abolished. It never should have existed.

Biden et al are just using the student loan issue as a carrot on a stick for young voters. If Republicans would bring to vote a bill with forgiveness of all student debt, while also abolishing the program, they could get rid of two issues. Republicans aren’t that concerned about the forgiveness, and Democrat voters don’t care where the future funding comes from.

Yeah, moral hazard and all, but if it could pass with both key items, we wouldn’t have this chickenshit game used every two years.

A former President made sure the first thing he did was to federalize student loans. The end game was to throw a bone to the young folk, forgive the loans in exchange for political fidelity.

That blew up yesterday.

Why dont the schools forgive the loans? Especially schools with massive endowments?

Why dont the student borrow directly from the schools themselves, like a purchaser of a car would deal with that car companies finance dept?

But no one seems to ask the big question…WHY is college so expensive? 3 lectures a week and a class run by a grad student who is getting a tuition break.

I heard the other day that the number of people in the administration at one IVY league school equaled the number of students.

AAPL $3T. A bull market or bear market rally : NDX closed < feb 2022 high : 15,196.40.

July/Aug might be red.

Whatever happens, I am considering if i need to change careers again. Mortgages is not cutting it, after 11 years in the business. After the heady years of 2020 and 2021, 2022 was rough and this year has been twice as rough. Not expecting things to improve at this point. I’m fortunate to be married to someone with a steady income.

The industry is kind of making the decision for you, isn’t it?

very possibly. Working for a credit union I like providing a service to our members and I don’t have to get in the gutter with realtors, wining and dining to get them to refer me their buyers. I am good at what I do and have a lot of repeat clients. The market has just vaporized.

Wasn’t looking to start over at 48 but maybe this is the push I needed.

Why would anyone care about the paltry little 5% returns in bonds when they can earn vastly more in US stocks?!!!

MW: Stocks end higher Friday, Nasdaq scores best first half of a year since 1983!!!

MW: Nasdaq Composite ends first half 31.7% higher!!!

MW: S&P 500 up 15.9% year to date, its best first half since 2019!!!

ALL the major indices are DOWN from late 2021 and early 2022. People forget?

The return of the Nasdaq composite since Nov 2021 = -15%.

The return of the Nasdaq composite since January 2021 = 0%. That’s 2.5 years of 0% return.

In addition, they lost purchasing power due to inflation over the same period. So add those together for your total “real” loss, if you’re so inclined.

Fair point. It’s only relevant to say that the S&P is up 16% YTD if you purchased back then. Most people didn’t.

Don’t forget Nasdaq is a price index, not a total return index. Investors will have received dividends, so return is not zero since January 2021 — though as you say it’s probably negative in real terms.

Yes. Average dividend yield of the ETF QQQM:

2020: 0.02%

2021: 0.40%

2022: 0.58%

The war in Ukraine is over according to the commodity markets. Corn under $5, wheat under $8, soybeans bouncing over $13 so traders can lock in some green before returning to the long march down. Gonna be pain in flyover soon- no new tractors next year! We will have some minor pain, but the recession will be in the Chinese rust belt- their turn to rationalize their economy and shoot the obsolete.

Nothing about this stuff is going to be instant, and those who expect inflation to moderate at the speed of the internet are mistaken. Now comes the next recession when durable goods stop selling because everyone will have enough. Just think about how many new appliances are sold with home ownership changes….

As for overpriced cars, no raise, no ability to pay, no new car- and those selling on commission become superfluous….yet again. Long time since a Fed recession was allowed to fully mature, and a lot of pain to be revealed by the outgoing tide….

Get out the popcorn as the populists once again begin railing against the Fed…and he is us.

Saved by automobile prices, up in Canada there’s a 4 year wait list for electric cars. All the car lots are empty so we have another 4 years to celebrate.

Blackrock pushed the agenda ,now Larry Fink is backing down ,also backing away from esg,. Keep up the good fight we the people. Shall not be manipulated

Plenty of cats here in America,you just have to become a debt slave to get one

There was absolutely ZERO reason for the FED to pause this past meeting. ZERO. They are reckless narcissistic aszholes taking care of their rich buddies while destroying the working class and the poor.

There is a big reason for FED to pause:

FED works for the wealthy and they had to pause. At the same time, they have this veneer of so called mandate ( full um employment and 2% inflation ).

Thus FED is walking a very thin line to show to the world that they are working for their explicit mandate but at the same time their real masters are wealthy so they need to cater to them as well.

That’s the reason for Pause and too little and too late QT.

Once we accept this fact about FED we all would see the picture clearly.

I meant full employment!

I’ll never “accept” corruption. Ever. They have a mandate. They are in direct violation of it due to corruption. Let’s arrest Jerome Powell to start.

No. Not in the least bit.

DC…

the ability to “redefine” is the ability to seize POWER.

The Fed started with “2% = stable prices”.

Then there was the ignoring of the 3rd mandate…”promote moderate long term rates.” They pushed long rates to ALL TIME lows.

They have redefined their mandates, and they are gaslighting the People to accept their own ignoring of the mandates and instructions under which they are allowed to exist and wield their special powers.

The pause was to stop bankruptcies of banks

Since Oct ’22 10 year bonds have been inching up in price. People like buying things that go up in price. So demand for 10 year bonds is solid. If the Fed had increased rates demand would have become even stronger. Prices would have gone up even faster. Rates would have moved down faster during a period the Fed would like to increase rates. By pausing the Fed kept rates going down slow rather than fast.

Europe would have had to respond with higher rates to stop the flow out of Europe into the USA. And Europe is more of a basket case than USA. The Fed is probably worried about crashing EU economy. In which case he would have wanted to pause.

It’s a different story if there’s weak demand for 10 year bonds.

In my mind the real question is do you want The USA to be concerned about Europe? My answer is yes. They are one of USA’s major trading partner. What affects them probably affects USA.

What if this is the landing? Rates stabilize around 6% and inflation 4-5%, staying in these ranges for years.

It’s a Jerome Powell wet dream.

In the scenario you describe, long rates will have to move up substantially to reflect these higher inflation expectations. This will in turn push up mortgage rates even further, eventually breaking the back of the housing market. The higher long term yields will also suck money out of equities, as longer duration bonds become more attractive than investing in a manic stock market approaching all time highs. It’s actually the recipe for a crash landing if you think about it (at least if you’re referring to housing and equities).

I agree this scenario would put mortgage rates closer to double digits. Housing would have to come down a lot more and stocks would follow. But if its a slow grind down, perhaps a crash will be avoided.

This is what I’m thinking too.

PCE core m/m falling…core services m/m falling.

Michigan consumer infl expectations falling as sentiment rising.

Fed has paused.

Bullish stocks.

…until what is happening in Europe happens here: inflation turns back up, Fed raises.

IF it happens here.

Need energy to bottom and surge for that?

Who expects a recession and is buying OIL, raise your hand.

If it does become the 70s = whipsaw city. Tons of fun all through your accounts.

“PCE core m/m falling…core services m/m falling.”

you mean RATE OF INCREASE falling, right? Still increasing.

Rate of change wags the tail.

Core PCI m/m for May = +.1% vs +.4% April.

Core PCI y/y = +4.6% v. +4.7%.

Wolf charts show services inflation rolling over so yoy may come down faster.

Add in a Fed pause and continuing bank bailout = bullish stocks.

But YES, prices are still going up.

The accummulated inflation of last few years is not going to go away altogther does the real damage. Big labor strikes of 70s will be arriving soon.

Stock market seems to like inflation for awhile: earnings are not reported inflation-adjusted. Hey great, buy. What bears got wrong this year.

Stocks become inflation hedge until they don’t. Which is when inflation spikes again from a higher low (as happened in 70s) as Wolf expects. And interest rates follow.

Happening now in Europe.

Eric:

“Core PCI m/m for May = +.1% vs +.4% April.”

That’s wrong. Overall CPI in May: +0.1%

Core CPI in May: +0.44%, up for the second month in a row:

https://wolfstreet.com/2023/06/13/for-7-months-core-cpi-hasnt-improved-at-all-stuck-at-2-5x-fed-target-services-cpi-accelerates-rents-not-playing-along-used-vehicle-cpi-spikes-but-energy-plunged/

Seems the real question is how quickly, if at all, the fed will jump back on the ZIRP and QE bandwagon when economic metrics show any sign of duress. Id like to believe Powell is honest in his statements, but I know he doesnt work for me.

The Federal Reserve will continue to keep increasing its policy interest rates as was made 100% crystal clear just yesterday in speeches in Spain by its Chairman, Jerome Powell. Didn’t you get the memo?

Powell is looking for excuses to Pivot. At any sign of weaknesses, he’d cave in to Pivot mongerer.

The people in power works for the wealthy. Let’s not forget this.

One example is: Recent incidences with Banks ( SVB et al ) and how the rich depositors were made whole using tax payers and common people money.

These banks were not systemic risk at all but FED and treasury worked over weekend to save their wealthy friends.

Many of them were political royalty & VIPs. For example, Peter Thiel (despite urging his portfolio companies to pull their money) kept $50 million of his personal funds in SVB. He was bailed out dollar for dollar using FDIC money.

Him & other big donors. Of course, in justifying the “systemic” risk, policymakers pointed to “BuSiNeSsEs CaN’t MaKe PaYrOlL” without mentioning the billionaires.

Ignorant/gaslighting comment.

Peter Thiel didn’t get bailed out. He withdrew his and his money only. He told his associate companies to withdraw their (again, their own cash) because the SVB collapse was imminent.

Royalty that was bailed out were Oprah, Pelosis, Newsoms, Royal Sussex and unnamed bunch of well connected elites.

The real world inflation rate appears to have been higher than the official numbers suggest, indeed.

Exactly. The BLS engages in what can best be described as “tortured statistics.” They’re fudging the numbers.

Could it be that high interest rates are also fueling some inflation?

Millionaires are now making an average American’s annual salary, or more, just from collecting interest. Some of that money is going into consumption, real estate, the stock market, etc.

Sure, as a percentage of income/wealth, the wealthy don’t consume as much as the working classes. But it’s still a nontrivial amount of money flooding into the economy.

Pre-tax, roughly $1.5MM to = median US household income at today’s ST rates.

I can guarantee you that FED’s balance sheet would be much much higher than today after 5 years or so.

US Govt would need to sell 2 trillion USD/year for next 10 years or so.

This would be all absorbed by FED.

Bottom line: Much higher prices for everything, booming asset market, more hidden inflation and screwed up middle/poor class.

One more example: Biden is planning to circumvent Student Load Scotus decision so basically more free money, more deficit.

1) Consumer spending might drop because the supreme court reinstated

the $1.8T student loans payments.

2) The gov cry wolf, but will charge Gen-Z and millennial student loans at mortgage rates of 5%/6%, to cut the budget deficit in the next 10 – 20 years.

3) RE loans might drop, because demand will be down.

4) In the next 2 decades the expired boomers might leave behind deflating RE assets. The C/S pairs might flip to bearish biased.

5) Gen Z will have to compete with millions of new immigrants that will

do whatever they can to survive. New immigrants will own the majority of small businesses, employing Gen Z and millennial.

The stock market goes all over the place from one day to the next, but today’s jump seems stranger than usual. I suggest:

1. The stock market seems to be only looking at the overall CPI, and not the core CPI. It is difficult to believe it can be this stupid, but that’s how it looks.

2. The market has decided to ignore Powell’s hawkish talk, perhaps because in the last meeting Powell talked hawkish while acting dovish. It’s just one meeting, but it left me a little confused. Powell has been talking hawkish lately, but based on the last meeting, perhaps this is his way of telling us he is finished raising rates /sarc.

“Don’t fight the Fed” was the usual explanation for the long boom in the stock market since March 2009. Now, ignoring the Fed’s rate increases and hawkish rhetoric are standard operating procedure. It must be that the Covid overreaction, recent bank rescues and the BTFP convinced Wall Street that any wobble deemed systemic in the economy will be met with a firehose of liquidity (and rate cuts plus YCC if need be) from the Fed regardless of the inflation rate. And so, the risk of loss in equities once something breaks (or might break) is insignificant. The Fed put and Wall Street’s belief in its effectiveness are more powerful than ever. It will probably take a very big external shock to break the spell.

If inflation remains higher for longer and if bond coupon rates for longer term treasuries and corporates need to drastically increase in order to find buyers, then holders of longer term bond funds are likely to experience continued capital losses (well beyond what they’ve already experienced). In such an environment, it seems cash held in a money market account is probably the safest place to be since banks and corporations will likely begin to default in increasing numbers.

That’s not likely to end well.

Wolf,

Thanks so much for the reporting and charts. Great work, as always. PCE truly is stuck well above the Fed’s target. No surprise given that the National Financial Conditions Index (NFCI) has been in a downtrend since last October. Monetary conditions have eased. The Fed is losing the battle against inflation despite the approx. 200 bps increase in Fed Funds since October.

Fiscal policy (if one can call it that) has also sprayed gasoline onto the inflation fire.

Monetary tightening needs to accelerate meaningfully from here otherwise we’ll be looking at worse PCE reports a year from now.

i don’t particularly like comparing YoY price indices of one month to the next or prior one, because one also needs to know what the price index had done during the same month a year earlier to judge what happened – ie, witness the recent big drop in YoY CPI when last May’s 1.0% increase went off the board…

i don’t know what one could use otherwise, though…

I used month-to-month, three-month or six-month moving average of month-to-month, and year-over-year. All of them have their issues, but taken together, they’re pretty good.