“Sternly staring at inflation until it melts before our withering gaze is not an option,” he said with a sense of urgency.

By Wolf Richter for WOLF STREET.

Fed Governor Christopher Waller is getting nervous about inflation and doesn’t want the Fed to make the 2021 mistake again of waiting too long before hiking policy interest rates, and if the core components of the CPI report on Tuesday and the PPI report on Wednesday are “hot” again, “then the FOMC will need to consider tightening monetary policy in the near term,” he concluded his speech today.

Does “in the near term” mean the FOMC meeting later this month? Or the FOMC meeting in September? The calculus had been for rate hikes to start later this year. Now the July meeting is on the front burner? If CPI and PPI readings are hot this week, will there be a majority of voting members at the July meeting to vote for a rate hike?

“Inflation and monetary policy are at a crossroads,” he said in the speech.

“Sternly staring at inflation until it melts before our withering gaze is not an option,” he said with a sense of urgency.

He explained: “There are some crucial differences now compared with 2021, and there is still a credible case for inflation to begin to fall back to our 2 percent goal with policy at its current setting. But I am concerned about the equally plausible case that data in the coming weeks will show that inflation will remain at its elevated level or even trend higher, requiring tighter monetary policy in the near term.”

Again, “in the near term.” What the heck does that mean? Does that mean he knows there’s a potential majority of voting FOMC members for a rate hike at the July meeting?

So now he has joined the chorus of FOMC members that see inflation as a bigger and growing risk and that are getting increasingly edgy about it, while the labor market is now “near full employment and stable,” as Waller said, and has recovered from the weakness last year, and has moved down in the rankings on the Fed’s worry list.

“When inflation is well above its target and the labor market is near full employment and stable, any serious policy rule calls for raising the policy rate to bring down inflation,” he said.

And he cited the inflation data and what was behind the acceleration.

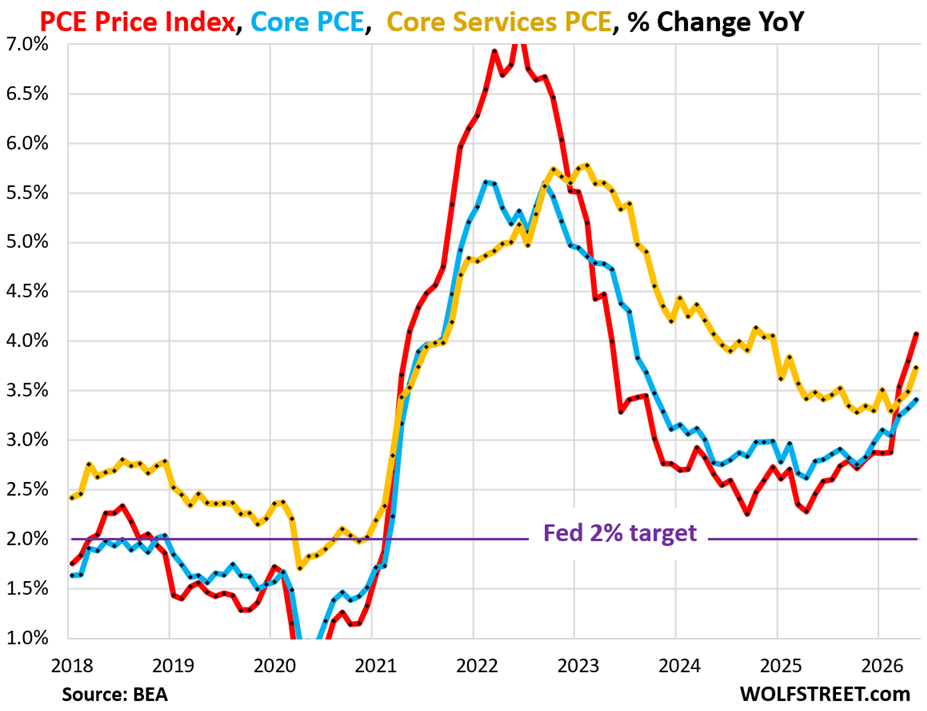

Inflation, as measured by the year-over-year increase of the all-items PCE price index (red line in the chart below) which the Fed uses as yardstick for its 2% inflation target, reached 4.1% in May, more than double the Fed’s target. It has been above target since March 2021.

Without the energy price spike, inflation as measured by the “core” PCE price index, which excludes energy components and foods, rose to 3.4% (blue line). It has also been accelerating since May last year.

The “core services” PCE Price index bottomed out at a too-high level late last year and started accelerating again this year and reached 3.7% (yellow). Core services dominate consumer spending.

An inflation hawk would have clamored for rate hikes starting last fall – when the Fed began to cut rates. But there are no inflation hawks left on the FOMC.

“So, the question is, will core inflation continue on its upward trajectory, or has it reached a turning point where it will begin to decline back toward our 2 percent target? The direction it takes has very different implications for the path of monetary policy,” he said.

“I am committed to returning inflation to the FOMC’s 2 percent goal but also determined to avoid overtightening policy and risking a recession,” he said.

While he expects the all-items inflation indexes to decelerate, as the price of gasoline has started to decline from the spike, he “will be focused on core inflation, and on that count, there are recent signs of continued pressure on goods prices,” he said.

“Core intermediate goods prices tracked in the producer price index [PPI], which may feed through to PCE prices, have increased noticeably in recent months. Also, purchasing managers for manufacturing businesses reported in June that their input prices have continued to increase, the 21st straight month they said so,” he said.

“Overall, I am monitoring price movements and am alert to the risk that the increase in core inflation is a sign that inflationary pressures are spreading through the economy,” he said.

“The FOMC has to be ready to tighten monetary policy to prevent a repeat of the 2021-to-2022 inflation episode. But there are two differences between now and then that make me cautious about leaning too heavily on that experience to make this decision,” he said.

So Waller returns to his roots as a well-reasoned centrist on inflation, after his sojourn in the dove-camp: At the FOMC meeting on July 30 last year, he’d dissented from the FOMC vote that kept rates unchanged because he’d wanted a rate cut; and he dissented again at the January 2026 meeting, when the FOMC kept rates unchanged after three cuts at the prior meetings, and he still wanted another rate cut; and during that entire time in dove-camp, he wanted to be Fed chair.

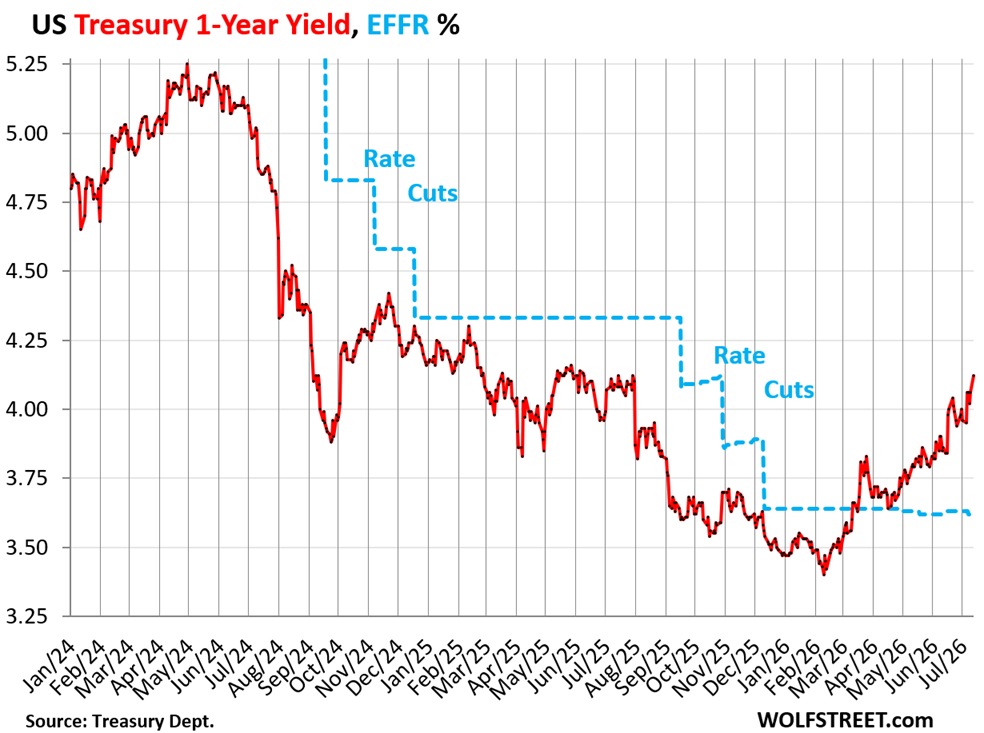

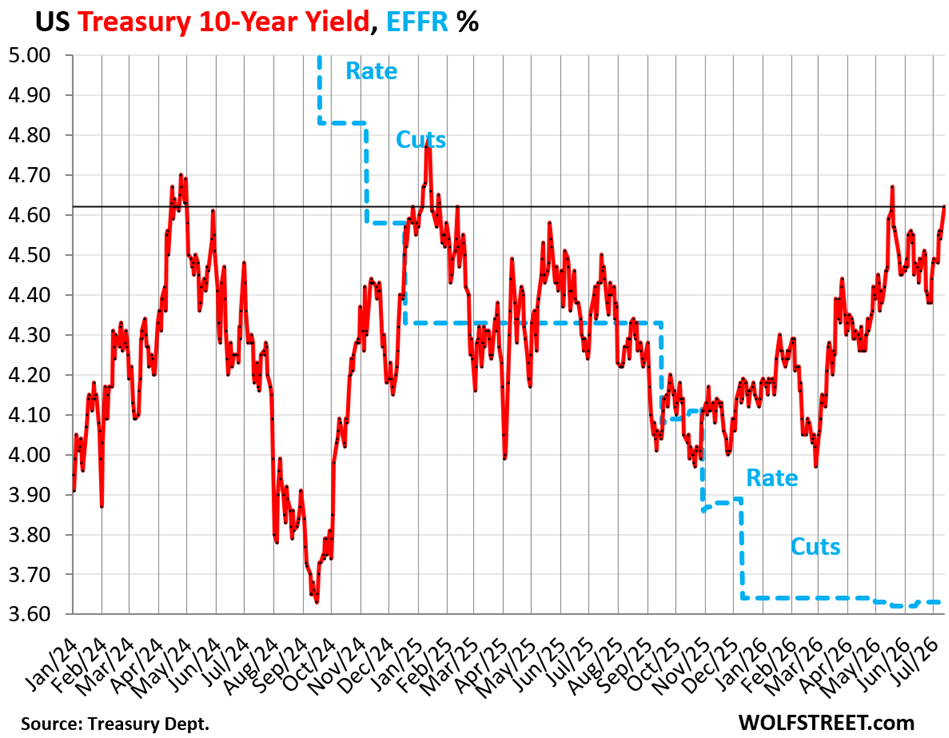

Treasury yields rose across the board today.

The 1-year Treasury yield rose by 6 basis points to 4.12% today, the highest since June 2025. It is now 50 basis points above the Effective Federal Funds Rate (EFFR, blue), which the Fed targets with its policy rates. The 1-year yield is pricing in the beginning of a rate-hike cycle:

The 10-year Treasury yield rose by 6 basis points to 4.62%:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This could be the trigger.

Hold on. It’s going to be a wild ride!

I’ll believe it when I see it.

Warsh will be Paul Volcker II.

He will overtighten.

Wishful thinking. Even if he wanted to — and he doesn’t want to — he would still have to build a majority at the FOMC, he would have find at least six other voting FOMC members to go along with his plans. And that’s not going to happen. They’ll tighten a little bit. Probably not enough to get rid of inflation, and then everyone will get used to higher inflation and higher interest rates and move on.

“Volker Shock” will never be allowed again. Our beloved rulers would rather see the system go down in flames rather than straighten out the financial morass that the USA is sinking into.

Got poverty????

My life – and that of millions of others — nearly went down in flames due to your hero Volcker. His monetary policies destroyed millions of businesses, millions of jobs, and thousands of banks. Is that what you want? If you’re a retiree sitting in your paid-off house and living on a fixed income, maybe that’s what you want. But the rest of the participants in this economy — from college students that will face the job market in a year or two, to business owners — want a functional economy, and they can live with 3-4% inflation, but they cannot live with economic destruction of the type Volcker’s policies wreaked.

In addition, inflation wasn’t today’s 3-4% in 1980. It was 14-15%. Huge difference.

Yep, Warsh will definitely trigger a recession.

Destruction of employment opportunities for the poor and asset values for the rich.

Everyone will Warsh in 2 years.

LOL, if there is a recession big enough for “destruction of employment opportunities,” then asset values are going to tank too.

I recently watched a YouTube video of one of Powell’s previous meetings with the US Senate. One Senator fawned over Powell’s engineering of a “soft landing” for the US economy.

Which reminded me of a previous observation. Politicians are terrified of having their name/tenure in office associated with a recession. They’re aware that many voters (wrongly) believe a strong correlation between economic conditions and their elected representatives. Many people “vote with their pocketbook” even though their representatives may have had little (or nothing) to do with the policies that led to current economic conditions.

Predictably, this Senator made no mention of the negative effects of Powell’s policies during Covid and afterwards. Just one example: young people being effectively priced out of the real estate market. That topic did not come up. Imagine that.

I continue to believe that Powell fully expected a large-scale recession as a result of the tightening period during his time in office. And he further thought that recession would “bail out” the substantial real estate price increases (along with many other prices) that came from the emergency ZIRP policy of 2020 – 2022. I believe he realized those price increases (inflation) would happen but expected the subsequent recession to ease and/or nullify the inflationary effects. And there is a chance he would have been right.

However, when that recession failed to materialize Powell was caught between the devil and the deep blue sea. Is it better to continue raising rates or wait until the past increases take full effect? That is where he lost his way IMHO. He should have continued increasing rates instead of the “wait and see” approach.

Easier said than done, I know. In the interim, Federal Reserve members are constantly under pressure to reduce rates from elected officials, despite the Fed’s independence. Warsh will experience the same pressure. Will he be more aggressive than Powell, or will he take the smaller tightening measures that Wolf mentioned? Probably the latter. Which, in my opinion, is not good.

How can you be cold in the Midwest?

Gotta be hot there too.

Wasn’t Warren right?

Cuz that would be strange for Warren.

Great read. The Fed’s momentum has shifted to a tightening bias, and Warsh will use that momentum to tighten 25 bps in ‘25 & 25 bps in ‘26.

CD – So you are crediting Warsh with time travel also?!?

If the markets are pushing up rates, as they have been since the Fed started cutting, how is raising the fed rate going to make any difference? Consumer rates tied to the 10 year are already way up. And one of the biggest drivers of consumer rates is indirectly tied to out of control federal spending which the Fed can do nothing about other than create a bigger debt by requiring even more interest to go to the debt. I don’t see how they have much impact with their cuts and raises.

I think quarter point rate changes matter to the largest debtor on the planet, which has $36T of rapidly growing debt.

Yes.

In addition, doesn’t a relatively ineffectual 25 bp raise lead to discussion about the NEXT raise, at which time a 50 bp raise is considered as a real possibility?

Takes time to turn the Queen Mary.

It seems to me that the rest of the committee has yet to buy into Chairman Warsh’s views of shutting up. I fear they love the sound of their own voices too much. it would be far better if they never said anything and allowed the market to price its assumptions, then act on the information in which they are confident. remember, one of the task forces is all about the data, which we all know has been substandard, at the very least.

I think they’re trying to walk the line between shutting up and not shocking the market. I would suspect this is a coordinated strategy to get the market ready for an increase.

Why commit to buy current rates when you’ll be locked into below market rates later…thats the thinking…so to sell their debt our government (all of us) have to pay buyers more…and more…

Raise the dam rates already and get on with it.

But they have avoided 102 of the last zero recessions with all of their “mistakes” so they feel justified.

I thought recessions were a required part of a healthy business cycle.

Where is it in the Fed mandate that their job is to avoid recessions? That opens so many cans of worms chiefly malinvestment and mark to fantasy accounting.

It’s a similar playbook as the late 90’s. All we need now is a flood of Asian money like the Asian Financial Crisis (half joking). So only question is can Warsh convince market there will only be a couple hikes? They did in the late 90’s. Then they cut a little, then they popped the bubble with a hiking regime. And when Jerome threatened a couple hikes in a senate hearing in 23′ markets quickly priced those in with a near 7% drop in one week. Obviously the market then went full melt up mode higher. So unless Warsh comes out and announces a hiking cycle I would think this price action is transient and could extend the bubble even more. Even spooz price action this summer looks like 96/97/98…. Anyone know if they dug out the actual binders for how to trade this. They must be dusty as heck.

The federal government spending money like they get it from the Monopoly game can only pressure higher rates to bring in the cash. Link that with the declining faith in the leadership coming out of Washington and you have a potential for real challenges in the near future.

it really is no more complicated than monopoly game. in rulebook when banker runs out of money, they are obliged to issue new currency on any piece of paper available. the bond traders are mostly confused. the FX traders used to be on the same desk as gold and silver traders. a proper perspective to money trading. i’m old enough to remember when a benjamin was baller money. now it’s chicken feed.

“But we also must avoid repeating the same mistake we made in 2021 and 2022 by waiting too long to respond.”

Perhaps he can elaborate on the cut right before the 2025 election….I mean, since they’re independent and all that and he’s now big on mea culpas. It seems to me that went a log way in defeating any realistic chance of hitting their 2% target.

Avoiding the same mistakes? I think Wall Street is fully invested in them not only repeating those mistakes, but doing so on a much greater scale.

Would love your thoughts on how the AI company bond rush might be affecting the Fed members’ thinking on inflation.

WSJ story yesterday, “The Quarter-Trillion-Dollar Onslaught of AI Bonds Is Testing Investors’ Limits”

For example, if AI infrastucture spending is a key driver of inflation, and the AI companies are price insensitive on debt, would that require higher rate hikes to have an impact on inflation?

From the story: “Typically, companies try to keep investors happy to ensure that their borrowing costs are as low as possible. But the hyperscalers are in such a heated race for computing power that they appear prepared to issue tens of billions of dollars of bonds at any moment, regardless of market conditions and whether they might need to pay higher interest rates.”

If Warsh is such an inflation hawk and he’s really shaking things up, then why did he vote to hold current rates in June, with inflation at 2x the target?

Why didn’t we at least get an announcement about QT?

And so why are we already congratulating KevWar for defeating inflation when he’s not yet done anything? What evidence suggests he is any more serious about 2% than JPow?

Committees? Sounds like a great stalling tactic / excuse to keep rates low through the midterms. What happens if the FOMC doesn’t make a substantial move for six months as inflation rises above 5%? I guess we’ll keep congratulating KevWar on his remarkable strategy of doing nothing.

“… why did he vote to hold current rates in June”

You understand nada. There are 12 voting members on the FOMC. The Fed chair has only one vote. If a Fed chair dissents from the majority during the first meeting or any early meeting, it would instantly destroys his credibility as a majority builder, and he would not be able to accomplish anything. The Fed chair’s role is to build a majority of the voting members at the FOMC for his views, and that’s a slow process.

Only one Fed chair ever dissented from the majority: Marriner Eccles dissented three times between 1938 and 1939.

That’s not my understanding of the purpose of voting. It may be how the FOMC works, and that would explain a lot, but the process you described would be considered a groupthink / toxic control situation in many other contexts where committee members vote. It strips out the usefulness of competing perspectives in favor of keeping up appearances – which is not a stated goal of having a committee like the FOMC. So maybe that’s how it actually works, but I would not say that’s how it should work.

If the longer term rates keep increasing, does the fed even have a choice?

It just seems like they are so far behind the curve with such a low rate bias that they will only make a piddly 25bps adjustment when they have no better option. Is fiscal reality creeping into the room?

Funny take in the lamestream media. I saw a couple articles twisting his comments into the idea he was not ready to raise rates just because inflation was up. Even after quoting some of his statements. Didn’t even read as a reasonable take, but their spin was “hold on, even with these numbers Waller is not ready to raise rates anytime soon”. Thanks for the factual reporting Wolf.

It wouldn’t make a dent in inflation if they hike. You think the greedy f**king landlords are going to lower rents? You think insurance companies will lower premiums? You think electricity prices will go down? You think an 8 pack of Dial soap that was $3.99 ten years ago and is now $9.99 is going to get cheaper? They want inflation. Inflation increases corporate revenues. State and local governments love inflation. It now costs $100 to buy the same groceries that cost $50 in 2016, so they collect double the sales tax now. Then the politicians give themselves raises because of inflation. I think you should get 6% on a CD now, but I don’t think it’s happening anytime soon.

A recession would lower prices in some areas. In a recession people get the smaller apartment or roommates, the get the generic instead of the name brand. As a result companies and landlords have start competing on price. I doubt we’ll get broadbased deflation but if supply were to exceed demand we’d see some in things like rent, used cars, premium products would have more frequent sales, etc

The inflation is as much a product of the consumer being willing to pay whatever as it of the feds rate policy.

“You think the greedy f**king landlords are going to lower rents”

Yes, lots of landlords have already lowered their asking rents because their units are vacant and they need to fill them. Lots of big landlords went bankrupt and lost their properties to the lenders. We covered some of this here.

“You think insurance companies will lower premiums?”

Sometimes. For example, our auto insurance premium actually went down a little last year.

“You think electricity prices will go down?”

For households? Generally not. They’re regulated and ratchet higher. But wholesale electricity prices can go to zero.

“You think an 8 pack of Dial soap that was $3.99 ten years ago and is now $9.99 is going to get cheaper?”

Quit buying Dial soap.

“It now costs $100 to buy the same groceries that cost $50 in 2016,”

That’s 100% food inflation in 10 years. That’s nonsense, unless you primarily live off beef and coffee. That’s why I post data so I don’t have to listen to this BS.

Sure they want inflation. That’s the explicit policy. Did you just wake up? Their official target is 2% PCE inflation year-over-year. And they’ll gladly accept 3% year-over-year but 4% seems to be a bit too high.

Curious to know whether you think commercial real estate rents for new buildings will decline? My meager understanding is that commercial new building loans are predicated on a certain level of rent revenue.

Here in Silicon Valley there is an explosion of empty buildings, but also plenty of new commercial construction. There have been a threat by a Russian oligarch’s progeny to build a massive skyscraper down the block from me in Menlo Park based on Proposition 9 laws (giving builders near automatic approval as long as they build a sufficient amount of residential apartments/homes, aka “builder’s remedy” for the housing shortage).

You have to negotiate with the landlord. In San Francisco, per-sf asking rents have declined. But the thing that landlords will do readily is agree to certain number of months of free rent. And they will agree to big tenant improvement allowances. That can be a big chunk of money for office space. And none of it shows up in the asking rent figures.

“Primarily living off of beef and coffee”……,hmmmmmm…..,seems a good goal!

Coffee beans have to be a carb if prepared correctly.

how about devaluing the currency by 20% that will raise the rates on long term bonds and help with the deficit i thing thats the govts end game

Israel devalued 99.90 % in 1986.

The effect of a greater devaluation would be even more than the devaluation that you propose.

That’s BS on two levels: 1. it devalued the currency by 20% after several years of near-hyperinflation and replaced it with the New Israeli Shekel; and 2. that was in 1985, and 1986 was a pretty good year after the 1985 Economic Stabilization Plan.

Vanguard Federal Money Market Fund paid out 3.57% distributions for month of June($4800/mo.) Vanguard latest stock market total returns projections are estimated at 4% to 5% over next 10 years. It would be great to see the Fed Funds rate increased to reward all the foxhole savers who are just trying to survive.

I love Vanguard but their projections have been really inaccurate. See their projections from 2016/2018.

The 3 month to 1 Year Treasury Bills are already between 4.05% to 4.25%. The work is already being accomplished in the Treasury market.

These clowns are so far behind the curve it’s laughable. Same sh!t, different day. These a$$holes are the worst human beings imaginable, just financially nuking the working class and the poor.

Agree. Lot of Ifs and Buts by Waller.

I am glad Waller has changed his tune now in terms of Inflation is real risk now and needs more focus. He was leading Doves since Jan 2025.

Wall St cry babies argument is 25 BP hike is not going to bring down inflation. Sure! but it will be clear message telling Markets FED is serious about Inflation. Otherwise its just Empty talks. Markets needs to see the Message in Action not just in talks.

The natural tendency of FED is to keep financial conditions extremely loose for obvious reasons.

So hedge accordingly.

It is incredible that he even takes the time to mentioned that he is still worried about overtightening.

Overtightening should literally be his last worry.

It is like he is driving a car that is going way too fast and heading for a cliff and he says “We have to worry about braking too fast so someone in the back seat doesn’t get surprised and get a scrape on themselves.”

There are more important pressing priorities.

RISK has not been properly priced for quite some time. The Fed has been the greatest enabler of bad behavior since Nixon and all that moral hazard is catching up with them. As the saying goes;” Full Faith and Credit”…

A finger wag and a lot of tough talk from the “fed should not provide guidance” guy.

I think he was banking on transient fuel issues. 🥹

“…from the “fed should not provide guidance” guy.”

You’re confusing Warsh and Waller.

No rate hike this month apparently given the just released inflation data.

In the past twenty-five years how often has the FFR been higher than the CPI, anyway?

And on average over the past twenty-five years, how much above or below the CPI has the FFR run, and by how much?

All in all, how accurate and appropriate have Waller’s and the other FOMC members projections been?

And what the difference between the dot plots and playing ‘pin-the-tail-on-the donkey’?

Ever been wrong before? What makes you think you’re right this time?

June inflation was back down. Nothing to see here. The sun is shining, the birds are singing,…

I think Warsh will sit chilly with rates hoping the market euphoria continues so at the same time he accelerates QT without a huge negative reaction.

(Sarcasm alert):

He will announce that the task force subcommittees have been formed.

LOL! Yep. The president is out of control, and CONgress is MIA. The market will force Warsh’s hand eventually, so why be in a hurry. The task forces are simply a stalling tactic, and quite frankly, a joke.

no matter, with the war back on, many of my energy and oil positions will be called away at very profitable strike prices…

None of this is “investing”, it is gambling, and will have consequences.

Accelerates QT? How about does any QT at all. The balance sheet has been growing since December.

I don’t care about rates – keep them steady until the election in ’28 – Bills are already paying well above the Fed target. Let’s get some real QT going – $60B a month to start.

Warsh is telling CONgress that inflation is going to be “a thing of the past”…

LOL! Go ahead Warsh, raise those rates, I triple dog dare you!!!! Stop enabling CONgress!!!

Time will tell, but now Trumpty-dumpty needs more money for more war…

…CONgress remains derelict in the responsibilities. Hold them to account already!

Hi Wolf, with inflation coming in lower than expected (again) would this be the time to go long (long-duration) treasuries?

https://wolfstreet.com/2026/07/14/gasoline-plunged-in-june-and-lots-of-month-to-month-cpi-squiggles-happened-to-drop-simultaneously-but-that-wont-last/

CNBC is cheering today’s CPI reading at “light”. I’ll wait for Wolf’s analysis!

Can the fed just work like a state machine instead of all their b.s. forecasting and fretting?

If inflation is high, and heading higher in the present state, raise rates. And so on.

Their flaw is their rapacious bias toward low rates. End that and the economy will adjust just fine, and the fed might actually achieve its goals.

IBM stock craters 24% after earnings warning…

$68 BILLION WIPED IN HOURS…

The only thing that is newsworthy here is that despite the 25% plunge, IBM shares aren’t even back where they’d been on May 13. Why did these morons pump up IBM shares so high in two months? The stock market has become a collection of lunatics.

Wolf – the F Ed knows that any meaningful increase in interest rates will TORPEDO the housing market.

Gut it, sabotage it, wipe it out, devastate it!

They know this. What magicians they are!

Tons of ‘wealth’ would vanish.

1. Mortgage rates track the 10-year Treasury yield, and the Fed doesn’t control that with its short-term policy rates. To mortgage rates down, it needs to bring inflation down.

2. The huge gains in home prices during the pandemic came in a very short time. Not many people bought at around the peak. Those would be impacted by a big price decline. But people who’ve been in their homes for years would not be impacted except psychologically. Nvidia lost $1 trillion in paper wealth in no time and nothing bad happened. Stuff comes, stuff goes. There are cities where home prices are down 25% or more already, and those cities still function.