Inflation surged past these yields, though they’ve started to rise again. Households nevertheless poured more money into them.

By Wolf Richter for WOLF STREET.

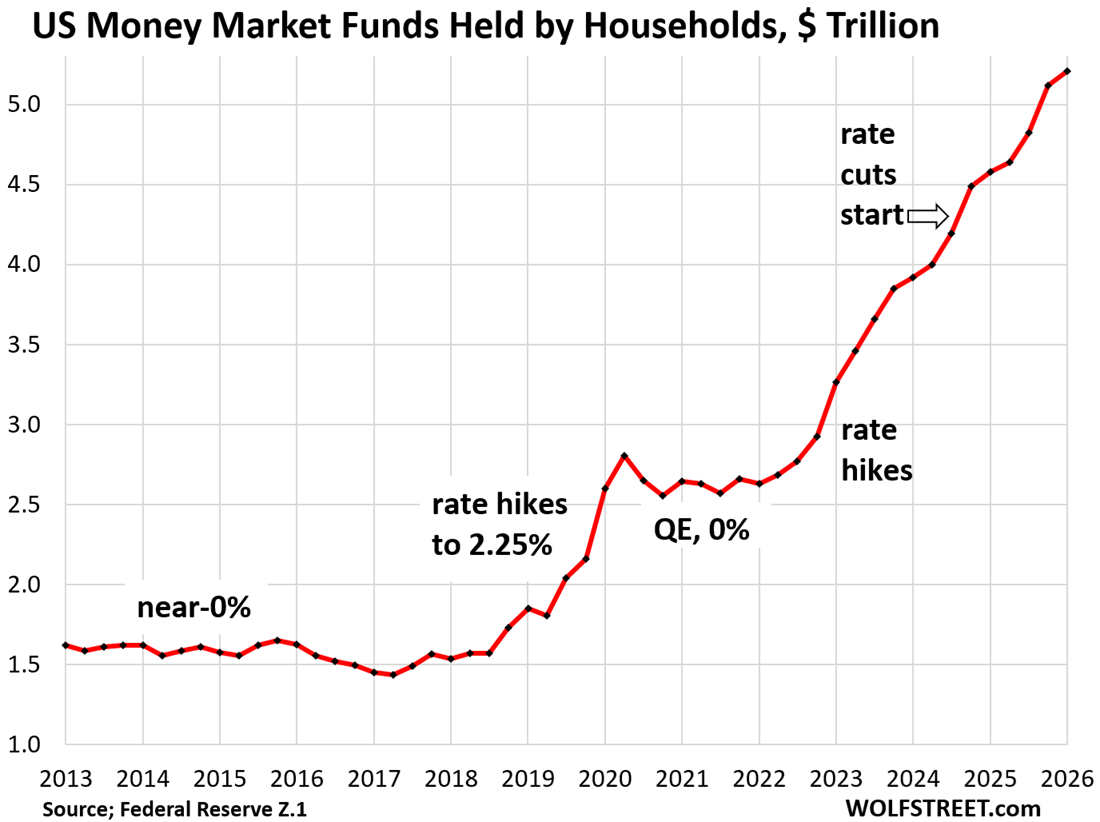

Despite inflation surging past short-term yields, households kept pouring cash into money market funds (MMFs) in Q1. Balances in MMFs held by households rose by $89 billion from the prior quarter, and by $626 billion from a year ago, to $5.21 trillion, according to the Fed’s quarterly Z1 Financial Accounts. Since Q1 2022, when the Fed started hiking its policy rates, balances have about doubled.

These MMF balances include retail MMFs that households bought from their broker or bank, and institutional MMFs that households bought indirectly through their employers, trustees, and fiduciaries – such as in their 401(k) plans.

MMFs are short-term liquid low-risk investments, a form of interest-earning cash: At current MMF yields of around 3.5% and at Q1 MMF balances, households would earn $182 billion in interest in a 12-month period.

MMFs have been earning around 3.5%, give or take a little, down from over 5% in 2024 before the rate cut started.

Treasury bills, a close alternative to MMFs, are currently earning between 3.66% (investment rate of the 4-week T-bills sold at auction this week) and 3.91% (investment rate of the 1-year T-bills sold at auction this week).

Inflation in March (end of Q1) was 3.5% per the Fed-preferred PCE price index, surged further in April, and in May went over 4.2%, and money market funds still earn only about 3.5%.

During January and February of Q1, MMFs were still out-earning inflation, earning a positive “real” yield (yield minus inflation). But that stopped in March for many MMFs, and in April for all MMFs, and further worsened in May. At May’s CPI inflation rate, “real” yields of MMFs are a negative 0.7%. They’re no longer attractive.

The Fed may eventually line up a rate hike or two, and the bond market currently expects the first rate hike to come late this year and another one next year, but that’s not guaranteed, that’s just the bond market pulling that way, and even if it does happen, real yields of MMFs would likely be negative until then, and might remain negative if inflation is allowed to stay at this rate or get worse still.

MMF yields are determined by the instruments they invest in minus the fees. Treasury MMFs stick to short-term Treasuries and overnight reverse repos at the Fed (ON RRPs). Prime MMFs invest in repurchase agreements (repos; Treasuries and agency securities with a remaining maturity of less than 1 year, but largely less than 3 months; short-term asset-backed commercial paper; certificates of deposits with big banks (lending to banks), ON RRPs at the Fed, among others.

Most of these instruments that MMFs invest in pay over 3.6% currently (except ON RRPs at the Fed, which is why ON RRPs have near-zero activity): Three-month Treasury yields are at 3.71%, six-month Treasury yields are at 3.80%. Asset-backed commercial paper is at about 3.75% for 30-day paper and 3.85% for 90-day paper. The difference between these yields and MMF yields are the fees extracted by the MMF provider.

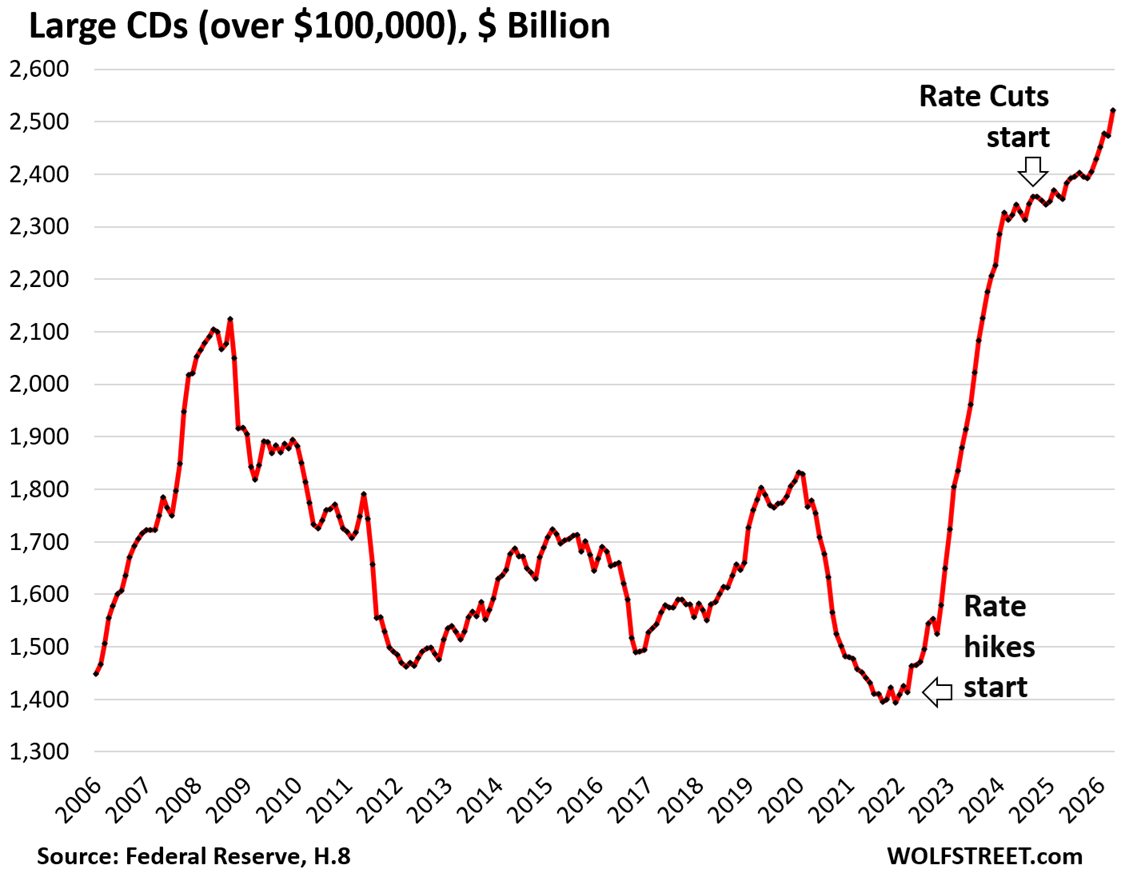

At banks, large Time-Deposits (CDs of $100,000 or more) soared to a record $2.52 trillion in April, up by $49 billion from the prior month and up by $169 billion year-over-year, as per the Federal Reserve’s monthly report on bank balance sheets (H.8). The FDIC insures CDs up to $250,000.

Since March 2022, when the rate hikes began, large CD balances have surged by $1.11 trillion. The rate cuts starting in September 2024 pushed down the yields of CDs offered by banks and slowed the increase of the balances.

The higher inflation rates that give many of the CDs offered in March, April, and May a negative “real” yield, have not stopped or reversed the growth of CD balances – on the contrary, it seems, given the spike in April.

Banks have started to offer more attractive yields, especially on “brokered CDs” (bank CDs sold through stockbrokers) where they compete directly with other banks. I just checked at my broker: The top yields offered for CDs of 9 months or longer are all over 4% APY, so a slightly better deal than T-bills. These CDs that I looked at are not callable.

What those yields show is that banks are starting to expect rate hikes, and these banks are competing for deposits among CD buyers that are looking for deals.

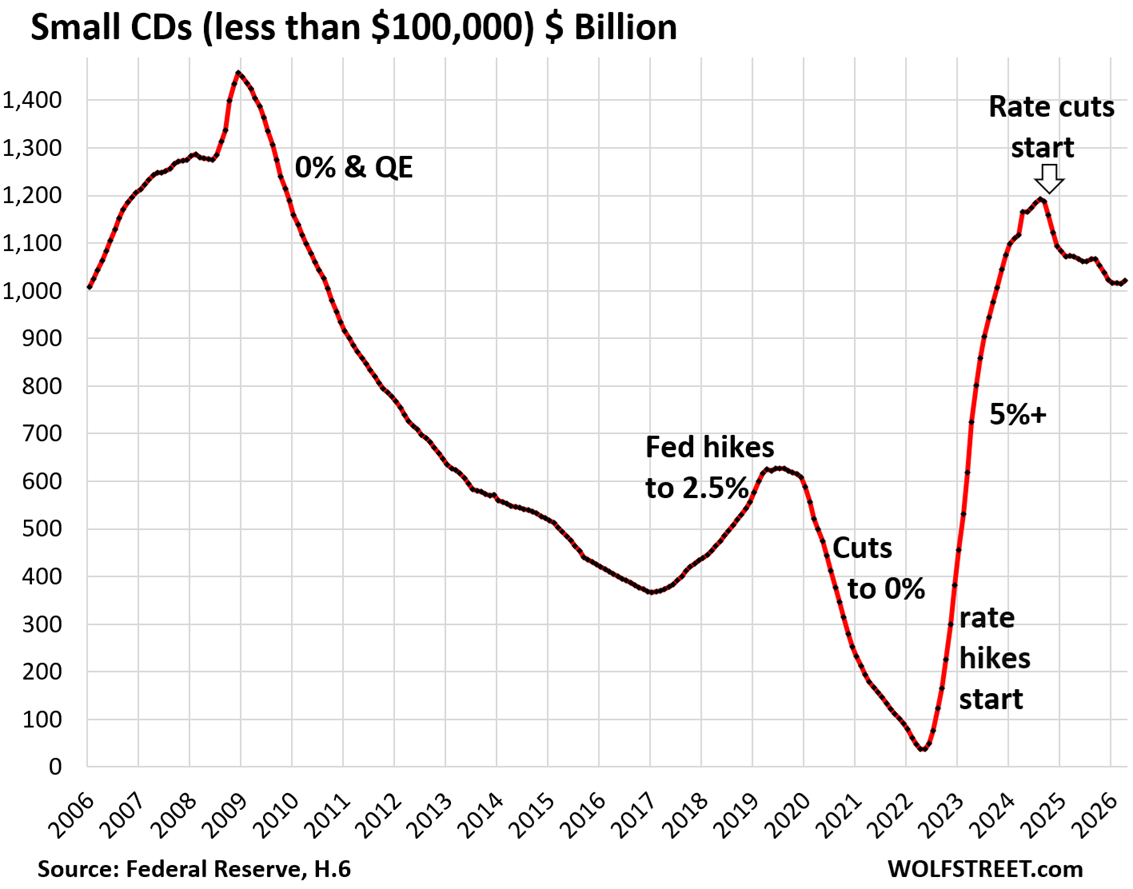

Small Time-Deposits (CDs of less than $100,000) ticked up in April to $1.02 trillion, after declining for six months in a row, per the Federal Reserve’s separate data on money stock (H.6).

Since September 2024, when the Fed started cutting rates, balances have dropped by $172 billion.

Smalls CDs react fairly quickly and strongly to interest rates offered by banks. They’re not “sticky” at all. Investors shift into them and out of them depending on yields that banks offer. They’re sort of the hot money of CDs. When the rate cuts started and banks slashed their CD yields, CD balances fell. But even the small increases in yields recently caused balances to tick up again.

Inflation will be the challenge for investors in low-risk investments, such as MMFs, CDs, and Treasuries.

Inflation eats everyone’s lunch one bite at a time, sometimes more slowly, other times faster, whether real estate or stocks or bonds or cryptos or MMFs or CDs.

But some of the other investments come with the hope of big capital gains that will – hopefully, knock on wood – outrun inflation. And that has a history of working, and of not always working. If those investments have capital losses, the curse of inflation is added to the capital losses, making those losses even harder to swallow.

Other investments come with automatic “inflation protection,” such as Treasury Inflation Protected Securities (TIPS) and Treasury I-series savings bonds, which earn an inflation protection amount based on CPI that is added to the principal as it occurs, plus a low separate yield (“base rate” for I-bonds).

And by the looks of it, higher-than-2% inflation is here to stay. Neither this administration, nor probably the next administration, nor the Federal Reserve, nor Congress is unhappy with inflation in the 3-4% range or maybe in the 3-5% range. That type of inflation makes the fiscal mess the US is in a little less “unsustainable.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Bank manager: “Sir, the hard-earned money you leave here today, will be worth less on December 31st, but your account will reflect a higher number.”

Bank customer: So more is less?

Bank manager: Exactly!

As if we had a peas chance of rectifying the extraordinarily profound amount of garbage that we generate.

Consider adding gold to the portfolio. DCA in “bites” over time. Sell a bit every time it hits a major peak. Most people are shocked when I point out gold has outperformed 10 year treasuries over the long run (1970s to present).

You know inflation is getting out of hand when trillionaires start to pop up.

He’s banking his trillionaire status on the hopium of greedy, opportunistic, short-term thinking share-holding morons, as well as continued negligence of the Federal Reserve. The latter is probably a good bet.

“Earth’s first Trillionaire”. Thank you Bernanke, Yellen, and Powel. Warsh will make it a club.

Is that net of fees? Transaction fees, holding fees. I’ve found gold to be one of the more expensive investments.

This overperformance completely disappears if you change the start date to 1980 instead of 1970.

This is in large part because of the huge readjustment on abandoning the Bretton Woods system in which gold was artificially fixed at $35/ounce, even though it was really worth quite a bit more. After abandoning the gold standard prices quickly readjusted, peaking in 1980 at a level (~$600/oz) that would not be reached again for another 25 years.

Actually, gold peaked in 1980 at approx. $850 / oz.

I think ‘not attractive’ is dependent on multiple factors. After literally doubling our NAV over the past 2 years, and being 71, I took 75% off the table and am perfectly content earning 3.5-4.1 on ST treasuries and CDs for the time being.

For now capital preservation is way more important for me than capital appreciation.

Well said! Investing is a highly individualized activity relying on many different factors unique to the needs of the investor. And besides, how many people still have large sums of money in zero to near zero interest bearing checking and savings accounts. Lastly, inflation is a statistical data point. Not everyone is affected to the same degree depending on their lifestyle, assets, and purchase decisions.

Agree i am in a similar situation, however I have the vast majority of my N.W. in physical metals, real estate, etc…., hence easy to sleep at night waiting for the next sell-off when rates blow-out.

As of now my nw is almost 40k usd with no intention to increase

All my nw is in bills and I sleep like a baby 👶

Lucky are the people who has little to lose ✨️

Without the masturbatory recitation I am also invested in short term treasuries

One of the most confounding characteristics of this stock market is that the valuations are irrational and yet “investors” continue to place bets with money they cannot afford to lose.

It’s only worth less if you spend it on something that has increased in cost due to inflation, at which time you take your loss. But not everything is going up in price, some things are lower cost than they were.

Take housing for example. As Wolf has noted many times, housing prices are dropping in most areas. If one buys at a new low, then those “Higher numbers” can be nice to have.

I’ll take those less-than-inflation yields along with the safety and no state tax situation happily, and wait for the bargains yet to show themselves, at which time I lose nothing. When the AI bubble does indeed burst imagine lots of things will be on sale. I’ll wait.

And maybe, just maybe, folks have diversified strategies in which they invest in more volatile assets (stocks) for wealth building as well as lower returning income assets (bills) – the latter to service ordinary annual expenditures ranging from vacations to home improvement projects. This, in addition to pensions, soc sec, etc, works for retirees who are looking at 10 to 15 year predicted windows.

It’s not a maximization strategy, true. But it is not irrational.

i.e., there is an inherent risk calculation to all of this.

Depends on your situation .. my fixed income 2 and 3 yr stuff from 2022 and 2023 at near 5% is coming off and is thrown in the mmf which keeps compounding along w my ss . A few friends and so on tinker for hours every day swing trading the market . That’s fine I don’t care to do it . And I’m comfortable. As simple as that .. you think older retired people need to “go buy things “ is the case for worry? I’m trying to get rid of things and countless articles how to clean out / get rid of / live simpler. Many people ( Boomers) I know are in the same situation. So it depends.

It’s all over the board. I see some 70ish folks downsizing, but I see just as many still up sizing with new autos, vacations, and second houses. There’s still lots of fun to be had in your 70’s if health cooperates.

…and 80’s.

Yes, correct! I am in my early 80’s and very active. I’m still having lots of fun.

Beware of banks and their cd’s. Most are now playing cute with call provisions earlier than stated maturities. Corporates are playing the same game as well as government agency and tax exempt issurers.

Any call provisions with bonds and CDs are clearly stated. The summary page will have a line with the word like “callable” plus some “call dates” or similar. So yes, you do need to look at the summary page that your broker provides.

Nearly all agency bonds have call provisions.

Callable bonds and CDs come with higher interest rates, which makes them interesting, even as shorter-term bets. You just have to know what you’re getting into.

Wolf I think part of the reason MMFs are rising is that technology has made it much easier to default to them over a savings account. Fidelity’s cash account for example. This is a good thing because it forces banks to be competitive.

Are MM funds insured by the FDIC? What could go wrong?

Money market funds are structurally much sounder than banks.

Banks are by definition fragile. They borrow short (deposits) and lend long (mortgages, industrial loans, etc.), and when customers want their money back, they can get a run on the bank but cannot sell their long-term assets such as loans, and so they collapse.

Money markets borrow short and lend short. Average liquidity in a money market fund may be 45 days, and selling short-term assets with 1-6 weeks left to run before maturity is easy and doesn’t involve big losses. When money market funds “break the buck,” it’s considered a catastrophe because it’s so rare, but has meant losses for holders of just 1% to 3%.

But there is a little risk of small losses there. That risk can be avoided by shifting to T-bills (and yields are higher too).

You would think that with these graphs, the government should figure out it needs to cut back on fiscal stimulus.

Still a ton better than the stock market falling 50%. Which may well happen.

Also in a regular bank account folks are earning nothing. So in this game of tug of war they are losing a good bit to inflation.

Bonds are ok except if they raise rates on you. Still better than the stock market if it gets pulverized.

We shall see!

There’s a ton of people out there that have the utmost faith in the government to protect the stock market and don’t believe a prolonged bear market is even possible.

There is an entire generation that has never seen a down market nor suspects it can happen. And with the Fed now defending the markets at every turn, perhaps they are correct. So, this becomes an arrangement rather than a “market”.

Very astute. There are tons of folks facing a world of hurt if things go south. Let’s call it ” old school”!

I-bonds have the added attraction of allowing compound interest for up to 30 years. To some degree this makes up for the fact that they don’t always quite keep up with the true inflation rate. You can pull the money out any time after 12 months if you need it, so they can serve as a cash reserve. They can be inherited and the new owner has the same time frame for owning them as did the original owner, 30 years from the purchase date, unlike the 10 year rule with IRAs. Of course like a Roth you buy the I-bond with after tax money, but when you cash them out you only pay tax on the interest.

Thanks for the write up. I’m glad to see there is so much “cash on the sidelines” waiting to buy shares of overpriced stonks.

/sarcasm

Per the figure in the article — US Money Market funds ~$5.3 Trillion. Nvidia ~$5.2 Trillion. All US money markets can buy one largest stock.

This all strikes me as FORCED behavior.

The slow to act Fed is forcing people to buy assets to avoid the taxation of inflation vs interest rates.

Fed Funds under inflation is akin to Trump pushing for negative rates a few years ago. Well, here we are.

So many of the ruling class benefit from the constant inflating, but so many of the People of this nation are constantly harmed by this inflation.

The “new Fed”, from 2009 to now, has discarded the relationship between interest and inflation. It is they who set the arrangement and it is intentionally skewed to benefit one group at the expense of another.

This is the result of interference in free market forces.

JA – “This all strikes me as FORCED behavior.

The slow to act Fed is forcing people to buy assets to avoid the taxation of inflation vs interest rates.”

This is policy; it’s financial repression. Right out of the playbook. Drive interest rates below inflation rate to cheapen the debt .gov has to pay back. It’s a stealth tax and a soft default. Nefarious, and a violation of the 5th Amendment Takings Clause, but here we are.

“The most important thing to remember is that inflation is not an act of God, that inflation is not a catastrophe of the elements or a disease that comes like the plague. Inflation is a policy.” – Ludwig von Mises

The main inflation drivers. All are unsustainable.

1) Reckless and feckless fiscal deficit spending at around 6% of GDP to juice the economy ahead of the mid-term elections in Nov. Both parties guilty of hyper-spending; it’s a bipartisan issue.

2) Insane levels of hyperscaler AI capex spending.

3) The war with Iran, of course.

Options to counteract the inflation as I see it are door #1, #2, #3, or a combination of these:

1) Buy stonks at the most overpriced levels in history.

2) Buy T-bills at negative real interest rates.

3) Buy commodities and precious metals (real money)

The top 10-20% of the economy will be fine, but to bottom 80-90% are in a world of hurt now and getting worse, since no asset ownership to offset said (high) inflation.

“The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists.” – Ernest Hemingway

Ugly Bubble

Indeed. Inflation is a tax and a policy, but not passed by our Representative governmental procedure, but by a cabal unaccountable and locked behind large oaken doors…..(now 2.5 Billion in marble)

Congress would never pass a 2% tax on holders of dollars…..its illegal.

But the Fed and their operators slipped it through as policy, and a policy even they abuse.

The widening bifurcation ….the split between those sheltered by stock and asset appreciation and those not, explains the election winners who tout the dynamic of the condition.

It may be illegal, but that is exactly what Sen. Warren just submitted. A wealth tax of 2%, for owners over $50 million.

I have a question for Mr. Richter or anyone else reading this. I regularly purchase T Bills (less than 1 year maturity) at Auction via my Vanguard Account. As there’s always a bit of a time lag between placing the order/trade and when the T Bill auction occurs, Vanguard publishes an “Indicative Yield” (and estimate of what the yield could/should be). I’ve been doing this for a few years now (T Bill and chill), but my final yield has always been a bit below Vanguard’s “Indicative Yield”.

So my question is – does anyone know if the yields quoted for T Bills are a compounded yield (particularly the under 1 year maturities)? If so, this may explain the discrepancy I’m observing.

T-bill yields in the auction results are calculated in two ways — the “high rate” and the “investment rate” — and the auction report lists them both. The “investment rate,” which is higher, is close to the calculation of the yield of an equivalent maturity in the secondary market.

I discussed this here in the article linked below and also showed both rates for that week’s T-bill auctions. Look at the table of T-bills sold that week and at the explanation beneath it:

https://wolfstreet.com/2026/05/15/us-government-sold-691-billion-of-treasury-securities-this-week-10-year-yield-spikes-to-4-6-30-year-yield-to-5-12-as-2nd-wave-of-inflation-takes-off/

Whew, for a bit there I thought I might be getting my very own RTGDFA

Thanks Mr. Richter.

With the overvalued stock market bubble that will eventually pop, negative yields of 1% especially on locked in gains are better than drops of 10-30% or more.

There might be a revolution before price discovery is allowed in asset markets. Could be a while. Need to plan on that. Sitting 100% in fixed income is risky.

A little Saturday morning insanity with coffee.

As our fixed income returns sink, the Spacex is valued at, ballpark, 100 x revenue. 1.75 trillion.

If Google had that value it would be worth 40 trillion. A little less than the total SP 500 market cap.

This is as out there as landing on the moon six times in a span of 3 years, and then forgetting how to do it. Incredibly, SpaceX figured out how to land rockets right here on Earth.

space x lost $5 Billion last year

Wernher von Braun sci fi book 1953: Elon rules Mars. If Elon $2.2T

deflates he will derail SPX

It can delay Anthrophic and ChatGPT IPO’s.

Not really any alternative to money market fund in a 401k for your current job if you don’t want to buy expensive higher risk stocks or long term bonds. But if the 401k is from a former job, best thing to do is roll it into a Roth IRA. Then you can buy treasury bills or TIPS without the tax mess.

I am going to put the proceeds of the sale of Mother in laws Condo in t bills. So this means I should buy during or around the auction? Geez I wish I understood this stuff better. I can read Wolf’s stuff 3 times and still not get all of it.

The investment rate is higher than the “high rate.” And around the time of the auction, the “investment rate” is close to the “constant maturity yield” published by market index providers to reflect trades in the secondary market.

You can buy at the auction through your broker. It’s pretty easy. You can set them up on automatic rollover so that when they mature, your broker will automatically buy the same amount of the same type of T-bill. At auctions, you buy T-bills at a discount, and when they mature, you get paid face value. The difference is the interest you earned. You can mix them by buying different maturities at different auctions. If you need the cash, cancel the rollover and sell the T-bills through your broker. That’s also easy. T-bills are super-liquid (easy to sell).

One thing to be aware of is rolling over treasury purchases differs with different brokers. I’m aware of two ways. With Schwab, you will not roll into the very next bill so that the same day your bill matures, you are owning the next one. With schwab your money will sit there earning no interest for around a week and then you purchase the next one. Fidelity however will seamlessly roll you into the very next one so you are earning interest pretty much interrupted. I’m guessing rolling over a 4 week bill for a whole year might add up to a couple of months of lost interest if doing the auto reinvest with schwab. You can buy tbills on the secondary market in schwab but you’d want to get familiar with how your taxes would deal with accrued interest and capital gains or losses if thats part of your transactions.

So in schwab you might want to put in each new auction order yourself, using a mm fund for the in between time.

“With Schwab your money will sit there earning no interest for around a week and then you purchase the next one.”

Schwab changed that a little while ago. Their new way is the same way as Fidelity’s or TreasuryDirect’s. I guess they were losing lots of Treasury auction business.

That’s good to hear they made that big improvement, thanks for the info.

Same with Fidelity. CD’s at least 9-mo are all at 4% & higher. A 5Y CD call protected gets 4.35% which is fantastic.

I’m very much a conservative investor, although I did snag 10 shares of SpaceX through my Fidelity brokerage account. Looking forward to letting those sit for years and years.

Except for those in ultra-low tax brackets, the after tax returns on money-market funds have been below inflation for a couple of years now.

This is part of what’s driving the stock mania. The speculative herd does not want to lose to inflation, and does not see anything else as “going up”.

Consider:

(1) Money-markets and Bonds earn less than inflation, after taxes.

(2) The house-price bubble has popped in most markets.

(3) The gold bubble has popped.

(4) Cryptos are still in a bear market.

So what’s a speculator to do these days, other than plow it all into cash-incinerating AI stocks and SpaceX?

But inflation applies to everything. So if you lose 50% based on price over x time, and there’s 10% inflation over the same period, you lose about 60% in terms of purchasing power. If it makes 50%, then you gain 40% in purchasing power, but risk that 50% loss. Nothing and no one escapes inflation.

But “we” haven’t seen a drop in the market for some time while inflation has been high (and in our faces) for some time. Humans seem to be designed/ conditioned to deal with immediate threats. (The average TikTok video is approximately 1.5 to 8.4 seconds.)

All this talk of T-bills, MM funds and CDs and no mention of the GOATs BIL and SGOV?

These are short term treasury ETFs that invest in various short dated treasuries and pay a monthly interest payment. They are extremely liquid, and the price does not move (technically it moves up throughout the month, and then drops by the payout at the end of the month).

SGOV is a replacement for Treasury MMFs. It’s not a replacement for T-bills.

Both SGOV and MMFs come with fees and both can go awry a little when something goes wrong. SGOV has a yield of 3.55% currently, which is lower than T-bill yields.

But nothing changes with T-bills if you hold to maturity, and you will get face value, which is not the case with SGOV and MMFs that can “break the buck.” But to cash out of T-bills before maturity, you have to sell them, and sometimes you make a little and sometimes you lose a little when you do that.

If you think rate hikes are inevitable, then going short in fixed makes sense.

If you think deflation is coming, then investors would go long on yields and invert the curve.

So, not surprising that we’re seeing some profit taking in equities and putting it in cash. I don’t think they’re there yet on inflation being a long term problem because the 10 year break even is still under control, seems to be signaling it’s transitory over the next year. My guess is the view food is f’d because of the fertilizer shortfall, oil will be a bit high for the year to restore inventories and the periodic bomb negotiations, etc. but it will viewed as transitory so maybe just a lil’ hiking.

We shall see.

I presume these @3.6% rates factor in the government definition of price inflation, but real world prices of items we all buy and use daily are almost certain to be higher than that.

Do individual “investors” in MMFs think about that? Or do they by-and-large only listen to their advisors?

Another factor that would mitigate against MMFs is oil. Oil prices are not likely to come down lastingly anytime soon, “peace deal” or not, if only because of infrastructure damage.

MMFs don’t seem to make economic sense in any scenario going forward.