The collapse of a currency is nothing to be trifled with. But the BOJ’s pussyfooted rate hikes & QT are too little too late.

By Wolf Richter for WOLF STREET.

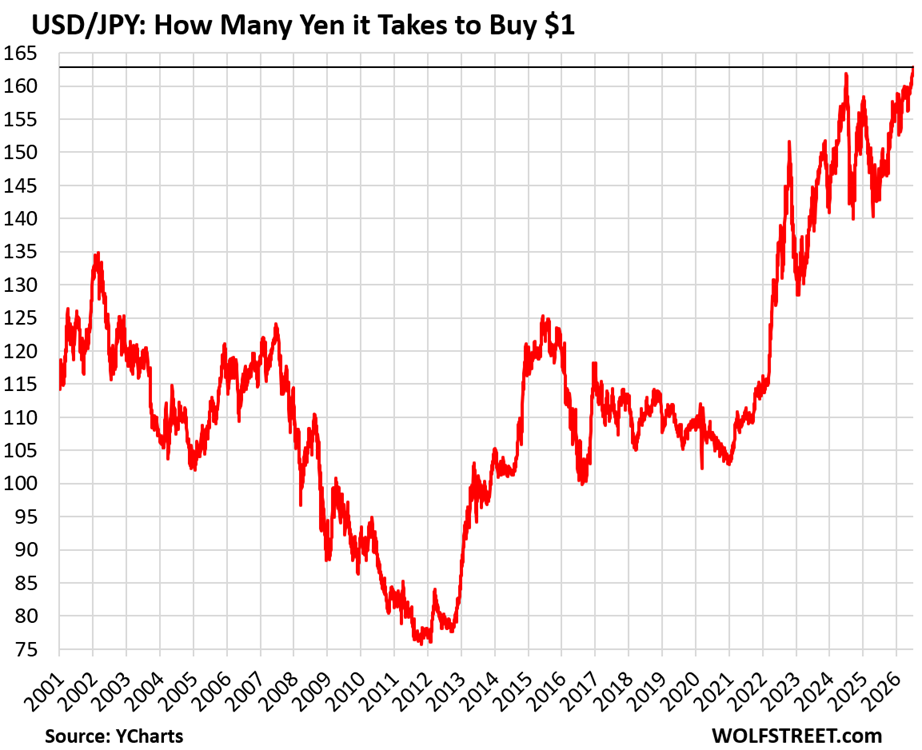

The yen has declined to a new four-decade low against the US dollar, to ¥162.8 for $1 USD, not seen since 1986, amid speculation that the Ministry of Finance would step in again by selling dollars and buying yen, plowing even more of its exchange reserves into another futile effort to put a floor under the yen by market intervention.

According to its latest monthly reports, the MOF had already engineered a record market intervention of ¥11.735 trillion ($72.13 billion at today’s exchange rate) in the period from April 28 through May 27, which only briefly put a floor under the yen, before the yen skidded further.

Since the beginning of 2021, the yen has plunged by 37% against the US dollar. Since the beginning of 2012, it has collapsed by 53%. The collapse of the currency of a developed economy is nothing to be trifled with.

This type of collapse of the yen has led to a surge of the wrong kind of consumer price inflation, not stemming from rapidly growing demand and salaries, but stemming from soaring import prices of fuels, foods, and consumer products – despite massive government subsidies at the wholesale level to contain those effects.

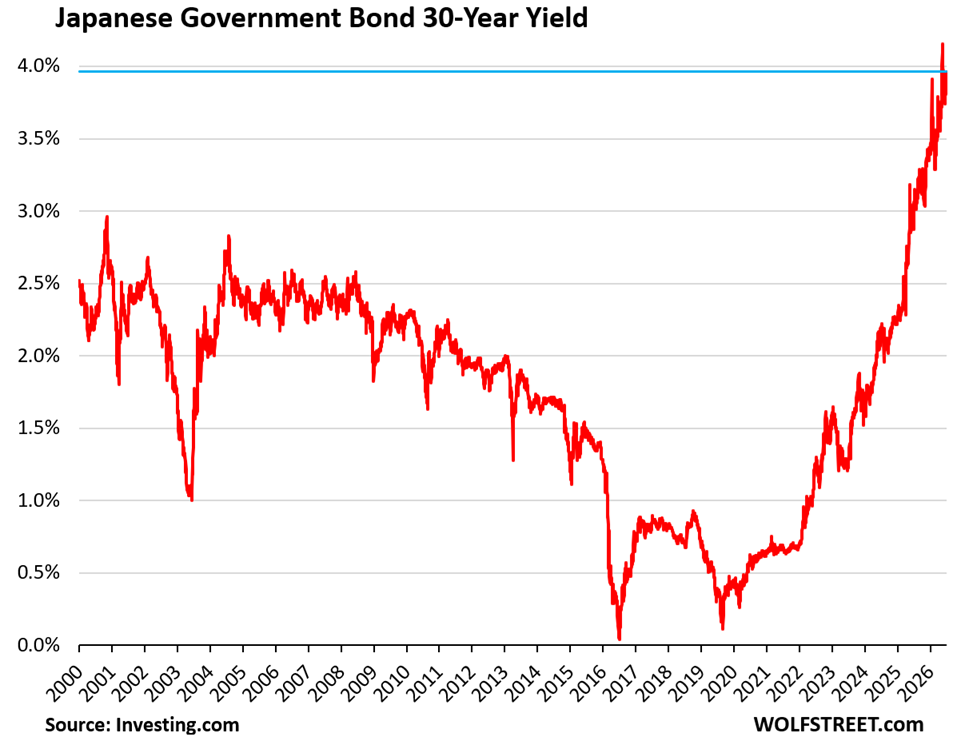

And it has also entailed a massive spike of long-term yields of Japanese Government Bonds (JGBs), thereby raising the borrowing costs for the government.

The 30-year yield of JGBs has been in the 4% range for over a month, sometimes a little over, sometimes a little under. It currently is at 3.96%.

A year ago, the 30-year JGB yield started setting record levels in the life of the 30-year bond which was introduced in 1999.

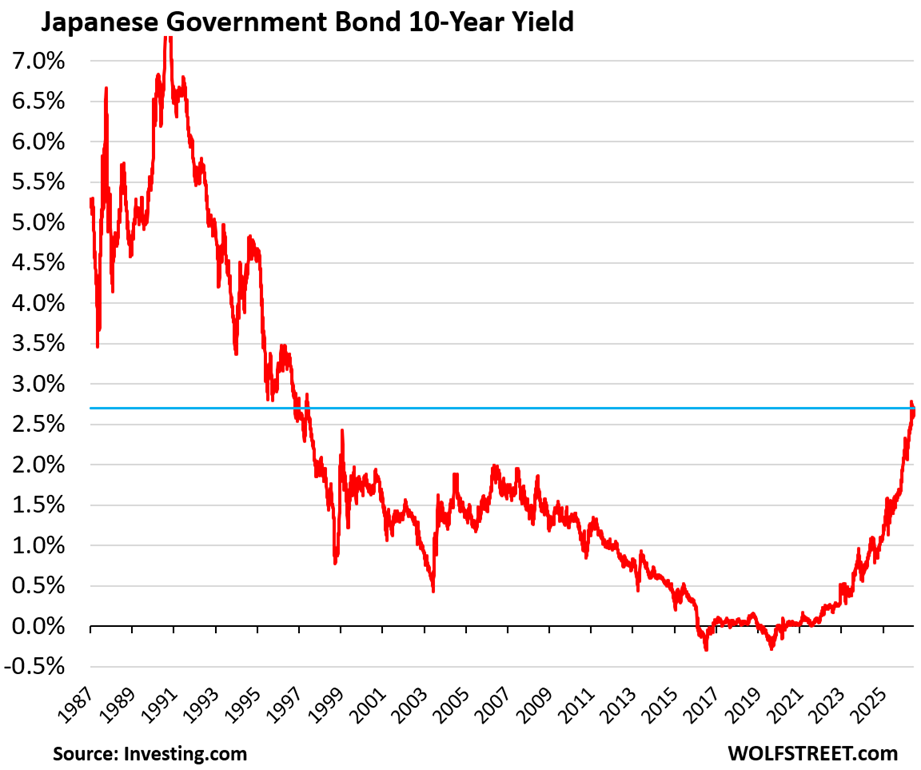

The 10-year JGB yield rose to 2.70% currently. On May 26, it had gone over 2.70% for the first time since May 1997.

Over the period from mid-2016 through mid-2021, the 10-year JGB yield traded at slightly negative yields to slightly positive yields, and absurdity that the BOJ engineered with its Yield-Curve Control (YCC). And now it’s surprised that the yen has collapsed?

Given the collapse of the yen, and inflation in Japan, YCC is now totally off the table. To the stem the slide of the yen, the BOJ has been forced to do the opposite of YCC: Quantitative Tightening, which has contributed to surging long-term yields, and rate hikes. There is no easy exit for the BOJ. What is needed is much more QT and substantially higher policy rates.

Projections of debt issuance by the Japanese government over the next few years, including to fund rising interest costs, have been ratcheting higher. New investors in this paper – including Japanese households – may have to be enticed with even higher yields to wade into Japan’s fiscal morass.

Not that it has ever mattered, but Japan’s credit rating by Fitch (‘A’) is five notches below ‘AAA’ while S&P’s rating (‘A+’) and Moody’s rating (‘A1’) are four notches below their respective top ratings (my cheat sheet of bond credit ratings by rating agency).

The yen has a Bank of Japan problem: Decades of the most recklessly dovish central bank in the world with its zero and negative interest-rate policy and massive QE. All monetary sins ultimately lead to the currency.

To put a floor under the collapsing yen, the Bank of Japan began a couple of years ago in a pussyfooted manner to raise its policy rates in minuscule steps once every blue moon, to a whopping 1.0% currently, the highest in decades, which is a bad joke for a currency during inflationary times.

In addition, it started trimming its gigantic balance sheet, and through the quarter ended March has shed 12.6% of its total assets since the peak (the quarter through June balance sheet data will be released in a couple of days, so stay tuned here).

But these pussyfooted rate hikes and QT have been too little and too late to protect the yen.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Warsh says: “We are not turning Japanese!”

Bond market says “We will see!”

“Federal Reserve Chairman Kevin Warsh doubled down on the central bank’s commitment to bring down inflation in his first comments since his inaugural press conference two weeks ago.

“We’ve all looked around, and we’ve seen that prices are too high,” Warsh said on a panel in Sintra, Portugal, at the European Central Bank forum on central banking.

Ask Yahoo Scout

“If there were people in the household or the business sector and the financial markets who thought that this central bank was going to be comfortable with an inflation objective above 2%, well, I guess they’d be disappointed. We’re going to deliver price stability in the US.”

When asked whether the Fed will do what it needs to rein in inflation regardless of President Trump’s desire for low rates, Warsh said, “We’ve been an independent central bank for a very long time. We’re going to be an independent central bank at this moment, and you’re going to see no changes on that.”

Talk is cheap! Rate cut hits in September, Gold confirming now noting too many Bears on board with this obligatory sell off.

Yep, they all talk a good talk. Don’t they?

That rate-cut by September stuff is just promo-hype being spread by internet trolls to pump up whatever. It’s beyond silly. But I’m glad you’re buying it lock, stock, and barrel. I hate to see promo-hype go to waste.

Lots of discontent in China. For example, someone flew a single engine plane into China’s tallest building 5-6 days ago.

The CCP tried to keep it quiet by confiscating all local security camera footage, and censoring photos transmitted on the Internet, but it got out anyway.

I’ll take the under on that.

I doubt the Fed will be able to fix the problem by itself.

At some point the government is going to have to step in and raise taxes, preferable on the Super Rich like the guy with his $500 million dollar yacht.

The Super Rich, at the very least, should be taxed at the same effective rate as someone working at minimum wage.

You posted this under the wrong article. You meant to post your comment under yesterday’s article on US debt, deficit, and Fed:

https://wolfstreet.com/2026/06/30/inflation-nominal-economic-growth-to-the-rescue-the-us-governments-ugly-fiscal-mess/

Please repost your comment under the correct article, and I’ll delete this one here because it doesn’t belong here.

The slide in Japan is just beginning. As older JCB debt rolls over (primarily Japanese government debt) at higher than zero or close to zero rate, the interest expense in Japan’s budget will grow dramatically and continually.

This growth in interest rate expense will be compounded by proposed tax cuts, increased defense spending, and a failure to address the reality of Japan’s aging population and failing export economy. So it will be a slow motion collapse, with only a US reserves to slow the decline. This scenario is obvious to any financial perspective that looks beyond the next year or two. I would appreciate any “optimistic” challenge to my slow doom scenario for Japan and the Japanese Yen.

Isn’t something around 90% of BOJ debt is held in country? So what happens or more accurately who benefits if/when the BOJ is forced to raise rates?

Back of the envelope (made up) numbers; with $10T in outstanding debt, just a 1% increase in the rate will result in an additional $90B in interest income, won’t it?

It’s impossible that raising rates will actually increase demand driven inflation in the short term, isn’t it? At least for those individuals and entities that currently are and will remain solvent eben ad the rates rise.

Let me ask a stupid question of the smart people on this board:

Who besides the ~120 million Japanese people uses Yen for any substantial transactions? I’m guessing that the US trade deficit with Japan results in them piling up US FRNs which are then used to purchase oil and raw materials? Do the Japanese buy things from Thailand, Australia, etc in Yen – which then come right back home for new Toyotas?

The point is so what if their internal currency and bond rates go haywire. In the end the rapidly dwindling number of Japanese citizens will own the whole island, all the companies there, all the BOJ bonds, and all the Yen debt.

The yen is a big trading and financing currency. Lots of countries and companies issued yen-denominated bonds (“samurai bonds”), including Mexico and Buffett’s outfit.

I see a supermax trade in plain sight. Sell Samurai bonds to buy US Treasuries. Lather, rinse, repeat.

That already happens. The Yen carry trade (which basically these samurai bonds are part of) is so huge and widespread for the past few decades that even Japanese housewives do it (the so-called Mrs. Watanabe trade): borrowing in Yen and buying US stocks and bonds to take advantage of the interest rate differential.

As long as yen interest rates are low and the exchange rate is stable or with depreciating yen, it works great.

The real question is when will the trade unwind, which could be a violent reversal. My suspicion is when interest rates exceed US interest rates. At that point, there’s no benefit to borrowing in Yen, and as those loans come due, they’ll be repaid in Yen and rolled over into dollar-denominated bonds again.

If this happens enough that the Yen appreciates substantially, then you could see panic as people get margin-called out of their carry trades as the exchange rate spirals higher. This uncontrolled rewind is unlikely (the govt can intervene by selling Yen) but the long-term rebalancing of the yen carry trade will have significant global effects, since currently, Japan basically subsidizes other countries’ loans.

Wolf, how do you see this ending?

It won’t end. At some point, way too late, the BOJ will do enough to stabilize the yet. Eventually the yen will regain some altitude from very low levels. This show will keep going long after we’re gone.

Historically (but very much less so now), Americans never really had to think very much about/understand FX rates and macroeconomic policies’ impact thereupon.

With an overwhelmingly domestically sourced product base (with rare exceptions like oil 1973-2013), the US Congress/Presidencies were largely free to indulge their pathological spending kinks, knowing that the Federal Reserve was there to service them and sand the ugliest edges off – so long as your domestic real economy is local-dollar-based, whoever can print the local fiat can…get away with bloody, perpetual murder vis a vis savers in that local scrip.

But…the more a country becomes internationally integrated/dependent (as a massive importer or exporter) the more that nation becomes circumscribed by the terminally jaded eye of trading partner nations (who intimately understand the fiat-dilution scam…because they deploy it against their own savers when the desire/need arises.)

Japan – being very natural resource poor (especially compared to places like the US) – built its entire post WW 2 wealth upon transforming foreign sourced raw imports into higher valued exports to foreigners.

It was deeply and inescapably integrated into international trade – making things like the FX rate have an existential importance.

But…as China has drained Japan’s milkshake as exporter to the world (compare Japanese export growth from 1964 to 1994 vs 1994 to 2024), the Japanese made the deadly error of having way, way, *wayyyy* too much faith in Keynesian game playing (vs. earlier real economy monomania) and fiat “stimulus”.

(Side note, even in pop culture, Japan has long had a sort of delusional admiration of all-things-UK (birthplace of Keynesianism) – perhaps because Japan saw in the UK a sister island nation astride the globe…until of course the UK imploded…and it is hard to understand why Japan never seemed to notice *that* macroeconomic postscript…).

Has the Yen carry trade largely already unwound or is that yet to come ? if so, what does that mean for Treasury funding ? Will it really make a dent or is the trend simply that a larger portion of Treasury Debt gets funded domestically.

For those of us in the U.S., now is a fantastic time to travel in Japan. I just got back from a 12 day trip with my family, and our meals for a family of 4 were typically $60 to $70, and I ordered anything and everything. Even our amazing hotel in the heart of Tokyo was $210/night.

Yes, Japan has become THE target for budget travelers. I’ve never seen so many tourists in Japan as we did in May. Asakusa Temple was like an ant colony. But what makes Japan a target for budget travelers (collapse of the currency) isn’t necessarily good for the people who actually live and work there.

Looking on the bright side, their exports will be cheaper and more competitive.

Yes, but all Japanese automakers produce a large portion of their overseas vehicles overseas — and the weak yen is of no help there. Hondas and Toyotas are consistently in the top of vehicles with the most US content. All Japanese automakers that sell in the US have plants in the US. They also have plants in Europe, China, etc. And plants in Japan import materials and components from other countries, and those have gotten very expensive.

Japan has promised Trump investments in US. So they need to raise USD somehow. Selling US assets? Or borrow in Japan and by USD? :)

I think an under reported happening (and reason for the lethargy and dithering of the BoJ) is that the biggest beneficiary of the carry trade is the Japanese public sector and the many financial institutions adjacent to the public sector.

Japanese savers have been getting f***ed over for decades with 0% deposit rates, whilst banks own JGB’s at some kind of positive carry.

The proceeds of those JGB’s are spent by the public sector into US treasuries etc and as long as the carry is positive and the fx is relatively stable to declining, the public sector makes payroll.

So whilst the media likes to talk about the mythical Mrs Watanabe, IMO it is the government that is getting paid off the asset side of the balance sheet more than anyone else. The BoJ will need to feel significant populist pressure before they do anything to upset the apple cart.

Bessent undoubtedly is across this better than anyone and will exerting a significant amount of pressure for them to do as little as possible.

But tourism is doing great.

Japan is becoming the new Thailand for tourism.

Currency is like a US election you want to vote for the least bad candidate. You want to hold the least bad currency. You want to lose the least amount to inflation.

Is there any non-speculative thing you can buy and make a profit. Seriously, is there anything you can buy that you can not lose money on and always get a return in excess of inflation, guaranteed. Treasuries and CD returns do not cover inflation.

Been trying hard to figure out Japan. It’s a mess.

The U S should encourage and make it as easy as possible for Japanese companies and manufacturing to move to the U S.