BOJ tries to put a floor under the yen and a lid on inflation through QT, rather than with rate hikes.

By Wolf Richter for WOLF STREET.

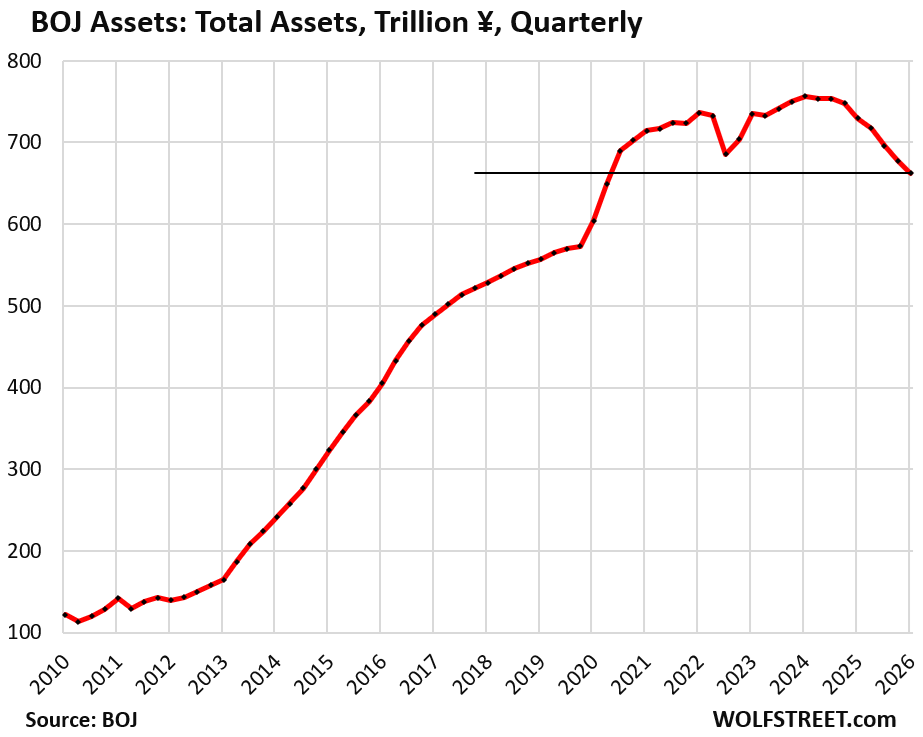

Under its QT program, the Bank of Japan reduced its total assets by another ¥15.6 trillion (-$98 billion) in the quarter through March 31, and by ¥67.6 trillion (-$423 billion) year-over-year, to ¥662.1 trillion ($4.14 trillion), the lowest level since Q2 2020, according to the BOJ’s balance sheet data on Tuesday.

Since the peak in the quarter through March 2024, the BOJ has shed ¥94.3 trillion (-$590 billion), or 12.6% of its total assets.

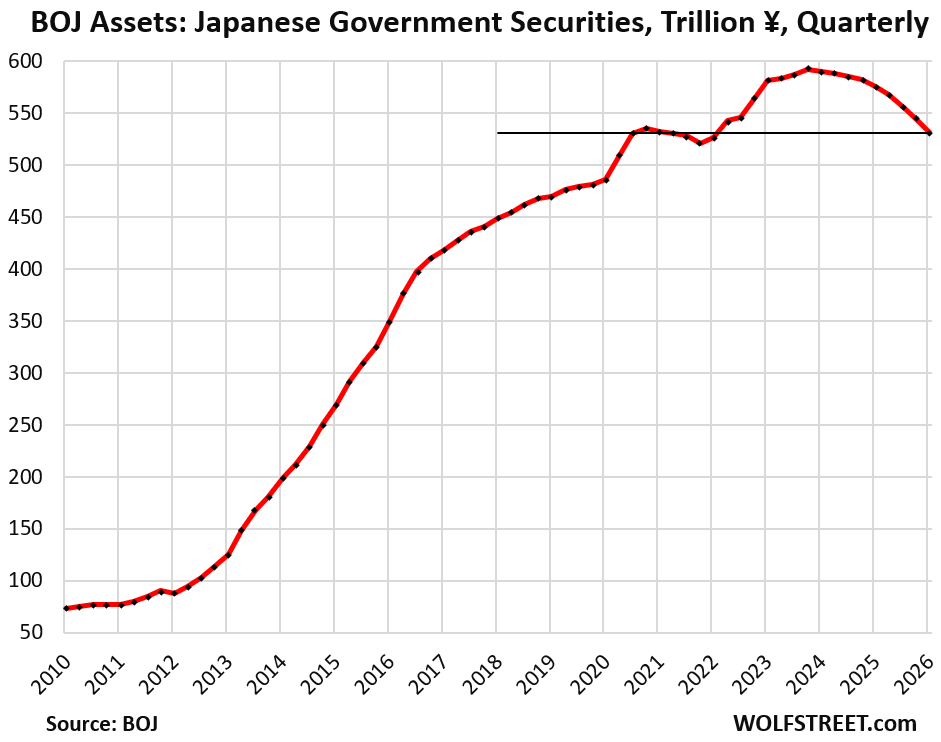

Japanese government securities on the BOJ’s balance sheet declined by ¥13.5 trillion in the quarter through March (-$85 billion), to ¥531 trillion ($3.32 trillion), where they’d first been in Q3 2020.

QT continued to accelerate: That quarterly decline of ¥13.5 trillion was the biggest quarterly decline yet since QT started.

All of them are Japanese government bonds (JGBs); the last Treasury bills (terms of one year or less) matured off the balance sheet last year and were not replaced.

Since the peak in 2023, holdings of Japanese government securities have dropped by ¥61.4 trillion or by 10.4%.

QT instead of bigger rate hikes. With this quantitative tightening, instead of with steeper rate hikes, the BOJ is attempting to put a floor under the yen, which has been plunging for years against the dollar.

The BOJ is also trying to deal with inflation, which rose by 3.4% in the overall economy as measured by the GDP deflator.

It has only minimally hiked its policy rates, in tiny steps spread far apart, to only 0.75% currently.

But QT has been more assertive, though with a late start. And it has allowed long-term interest rates to rise sharply: The 10-year JGB yield has soared from 0% in 2023 to over 2.4%, the highest since the 1990s. The 30-year JGB yield has soared to record highs near 4% (which I discussed here on Monday).

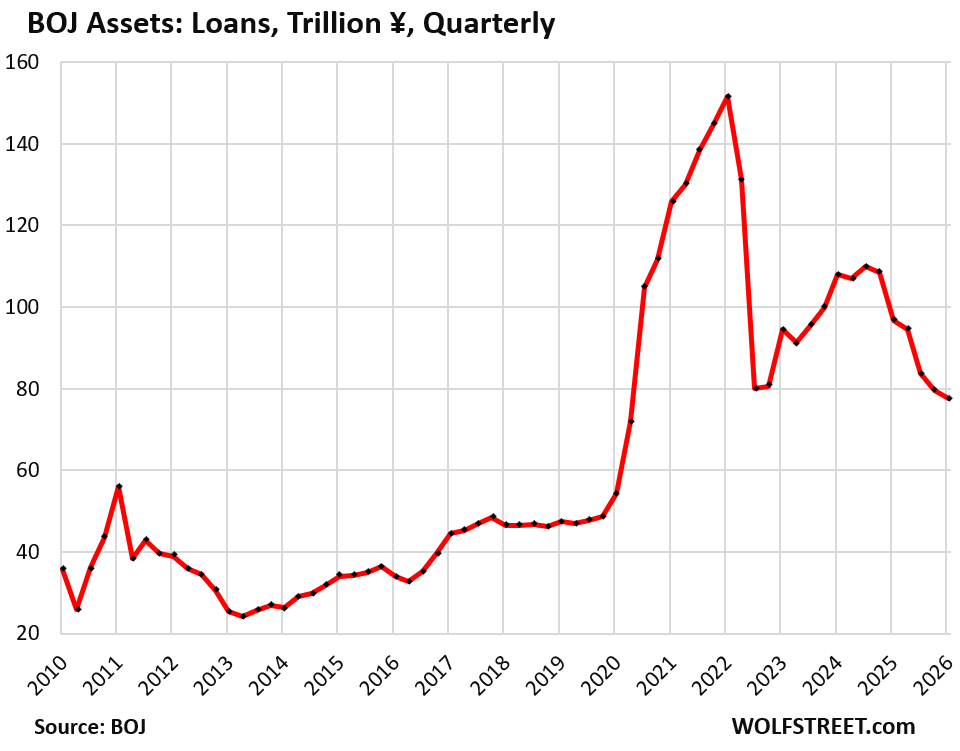

Loans declined by ¥1.8 trillion in the quarter, and by ¥19 trillion year-over-year, to ¥77.7 trillion ($486 billion).

Since the peak in Q1 2022, the outstanding loan balance has fallen by ¥74.0 trillion, or by 49%.

These loans now account for 11.7% of the BOJ’s total assets. The BOJ provided loans to banks and other entities under several programs, including the pandemic-era loans that had caused the total amount of loans outstanding to more than triple in two years:

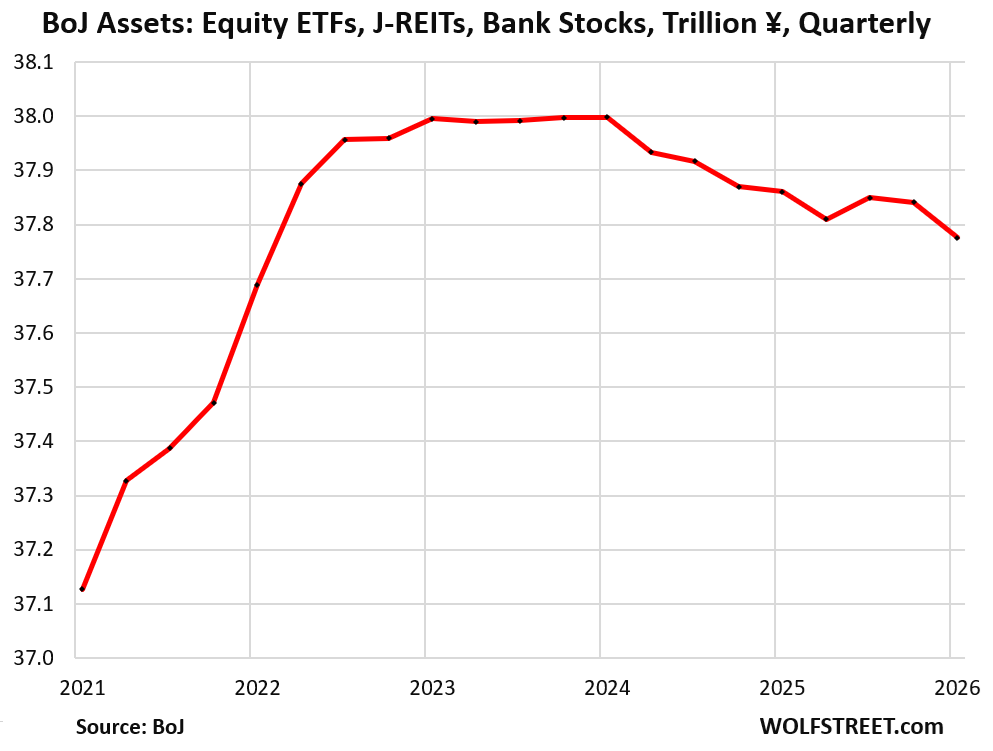

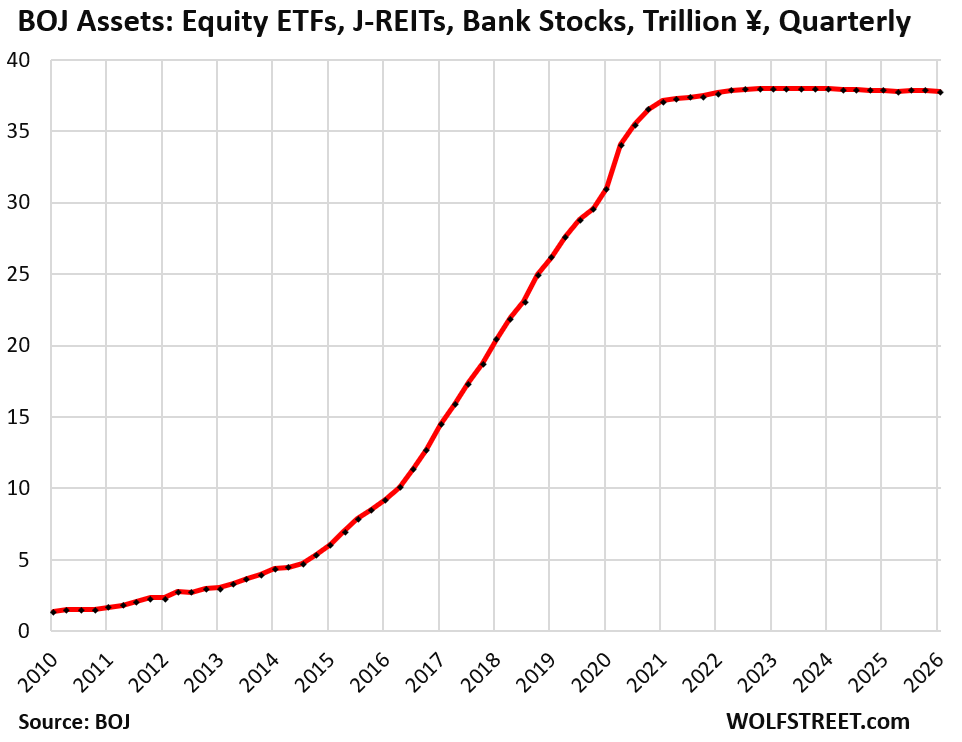

The BOJ started selling its equity ETFs and J-REITS.

The BOJ started selling its equity ETFs and J-REITS by minuscule amounts in the quarter through March, after announcing in September that it would do so, at an initial pace would be glacial: ETFs at a pace of ¥330 billion a year ($2.2 billion) and J-REITs at a pace of ¥5 billion per year ($33 million).

In Q1, it reduced its ETF and J-REIT holdings by ¥66 billion to ¥37.78 trillion ($236 billion).

But that pace of sales is faster than it seems: The BOJ carries ETFs and J-REITs at acquisition cost and has not marked them up to market since it started buying them in 2012, while the Nikkei 225 has soared by 500%.

The pace of decline is shown at acquisition cost, but market prices of its holdings are far higher, possibly two or three times higher, and in actual terms, that pace of sales at market prices is far faster than the stated sales at acquisition cost.

The BOJ sold off its last bank stocks in the September quarter. It had purchased them in the early 2000s and again in 2009-2010, and started selling them in 2016.

So the decline in the chart through the September quarter was due to the sales of its last remaining bank stocks. Sales of equity ETFs and J-REITs began in 2026.

This chart looks at the situation with a magnifying glass, or otherwise the declines wouldn’t even be visible:

In the zoomed-out version of the above chart, the declines in 2024, 2025, and in the March-quarter of 2026 are so small that the line appears nearly flat.

But these holdings account for only 5.7% of its total assets.

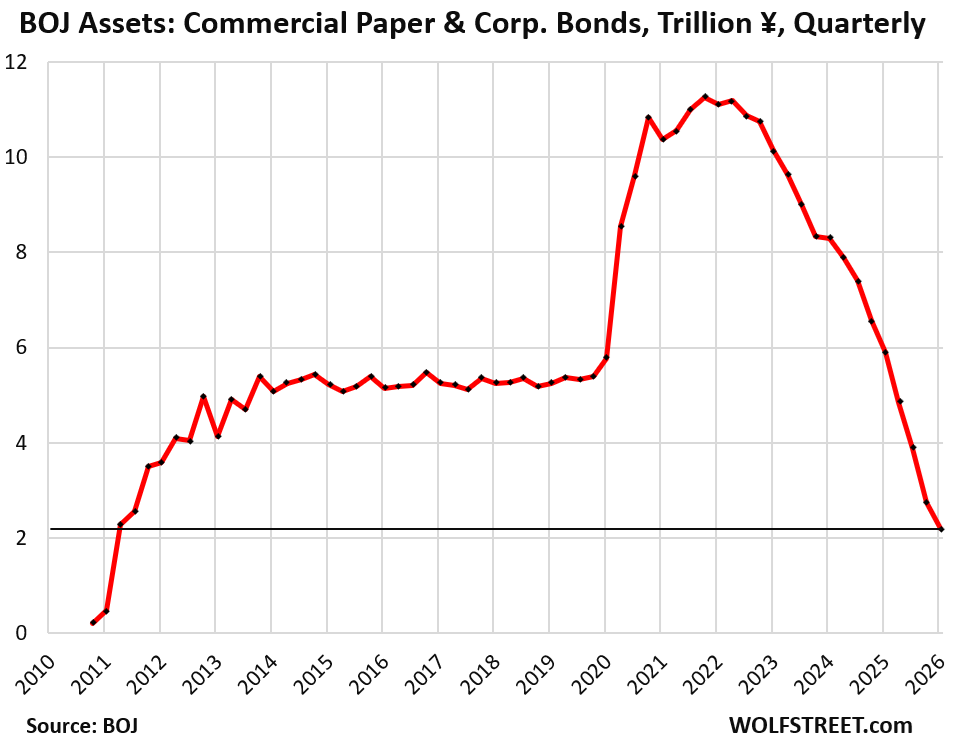

Commercial paper and corporate bonds fell by ¥550 billion in the quarter to just ¥2.2 trillion ($14 billion), all of them being corporate bonds; the BOJ shed its last commercial paper in the quarter, and they’re down to zero.

They were always just a tiny part of the BOJ’s QE operations, at their peak accounting for only 2.2% of the BOJ’s total assets. They’re now down to just 0.3%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If the tightening was accomplished by BoJ roll-off of 1 year Japanese Treasuries previously bought (and held) that is kind of interesting.

You wouldn’t think that the earlier BoJ purchases of such short term Japanese Treasuries would have had much of a restraining effect (then) on longer term Japanese interest rates (kinda the whole point of “quantitative easing”).

This is sort of an important basic question now that Central Bank money printings (QE to buy Gvt Treasuries) are becoming more and more common (if not respectable) around the world.

Namely, just *how much* Central Bank QE printing (read, inflation) is necessary to keep an artificial cap on market interest rates (by acting as a non-economic purchaser of Government Treasuries) – and what term Treasuries do such CB purchases have to target in order to keep the desired interest rates (presumably long-term) under the desired artificial ceiling?

You would think the QE would have to buy long term Treasuries to artificially restrain long term rates – but is that what the BoJ did? Can CB’s influence/control *long term* rates by buying short-term Treasuries?

Nonsense. You’re making up BS theories based on nonsense. I said in the article: “the last Treasury bills (terms of one year or less) matured off the balance sheet last year and were not replaced.” The amounts were already minuscule before QT officially started. The BOJ never held more than minuscule amounts of bills. The purpose of QE and YCC had always been to buy long-term bonds to bring 10-year yield down to 0%. In mid-2024, before QT started, the BOJ held just ¥2 trillion ($12 billion) in bills, compared to ¥580 trillion ($3.65 trillion) in JGBs.

Just another observation surrounding Japanese long term Treasury rates – from Feb 1999 to Dec 2025 it looks like they never got to (never were allowed to, due to BoJ intervention?) above 2% – despite the relentlessly worsening debt-to-GDP ratio of Japan.

And the main point really isn’t about Japan.

QE (money printing) isn’t just a about “suppressing interest rates”. Whenever a country is running a budget deficit, QE/printing is just a much about cutting taxes for the wealthy, as it is about keeping interest rates down, but most people are naive and think low interest rates make their lives better. In reality you get inflation TWICE: First from rich people front-running buying assets (houses, stocks) with their tax savings, and then again when the poor people try to catch up on the already risen house prices by loading uup on “cheap” debt.

Some interesting points.

1) I’ll definitely agree that the US G is getting mighty comfortable with money printing rather than/in addition to explicit taxation. DC is terrified of raising anybody’s taxes – but is also a complete crack addicts when it comes to spending on its priorities.

That leaves money printing and hoping that inflation can be hidden/lied about/blamed on somebody/anybody else.

2) The front-running is possible but risky unless you are really, really sure a) the fresh print fiat is definitely coming, b) you are getting it first, and c) demand for your speculative investment is going to continue. All are possible but not 100% certain (except at the more rarefied levels of US decisionmaking)

3) Sticking it to bagholders is similarly possible but also somewhat risky – demand can shift and new supply will (slowly) come on line.

Still and all, worth thinking about.

Wolf, can you deliberate or shoot down the talks I’ve heard about Japan buying less US debt as “a method of pressuring the United States in some manner or another”? I understand that this is purely speculation but I’m genuinely curious, because the picture you paint is more of a contracting budget with necessary slashes across the board.

But still the thought lingers on my novice mind, could it be that they are slashing more US bonds than they otherwise would for political reasons?

I really resent it when people drag stupid internet bullshit into here. That stuff gives you brain rot, which is incurable. And it’s infectious. It infects your family and your dog and your house and causes it to rot. It’s not my job to treat brain rot. It’s not my job to clean up the internet. I’m too busy, there is too much of this shit out there. I’m now old enough to understand that my time on earth is limited, rather than unlimited, and I don’t want to waste whatever time remains on internet bullshit. Don’t go to places that pollute your brain. This is a recommendation as basic as: Don’t drink from the sewer. And if you do go to these websites, and you get brain rot, take it like a man and cry into your pillow, but don’t spread it here and make me deal with it.

That comment is awesome, I am going to treasure it as Wolf’s Law of Internet Sewage:

“My time on earth is limited, rather than unlimited, and I don’t want to waste whatever time remains on internet bullshit. Don’t go to places that pollute your brain. This is a recommendation as basic as: Don’t drink from the sewer.”

Thank you Wolf.

Have they said anything about slowing down QT?

Yes, considering it for the June quarter. We’ll see what they will actually do, how much they will actually dial back on QT. They say all kinds of stuff, in part to confuse markets. And they start doing stuff they didn’t announce too. For example, they started letting their JGBs roll off (QT) for more than a year, starting in late 2020, and never said anything about it. You can see that in the #2 chart, and I wrote about it at the time. But there was nothing about it in the media anywhere. They reversed course when markets began reacting to it by pushing up the 10-year yield a little, and then they kicked off YCC again to get the 10-year yield back down. But that was under the Abenomics/Kuroda leadership. Kuroda exited in April 2023. Under Ueda, the BOJ has slowly moved away from Abenomics.

“The BOJ carries ETFs and J-REITs at acquisition cost and has not marked them up to market since it started buying them in 2012, while the Nikkei 225 has soared by 500%.”

Isn’t carrying at acquisition cost what resulted in all those Japanese banks collapsing back in the early ’00s, as a result of still having bubble era assets still on their books? I guess it worked out for BOJ this time, but I would’ve expected the whole country to rethink that practice.

The accounting rule that the BOJ follows is that it marks the ETFs down to market if the market price falls substantially below acquisition cost. As far as I know, that has not happened. However, it does not mark up them up to market. It just takes the gain when it sells them, which is now happening.