Ground beef, steak, chicken, fruit & veggies, coffee, dairy, eggs, other foods, and total.

By Wolf Richter for WOLF STREET.

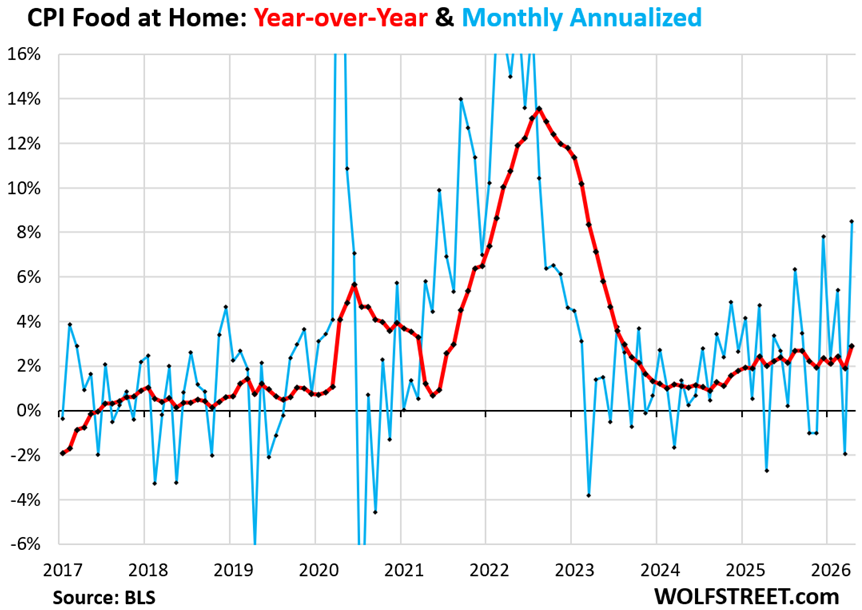

Prices of food and beverages purchased at stores and markets jumped by 0.7% in April from March, the worst month-to-month jump since August 2022 during the period of red-hot food inflation. And it pushed the year-over-year increase to 2.9%, the worst since August 2023, according to the Consumer Price Index. Food inflation was one of the factors why the overall CPI for April was so hot.

Prices of some major food categories spiked in April – actually, continued to spike – such as beef, fresh fruits and vegetables, and coffee. Price increases in some other major food categories were muted. And prices of eggs continued to implode after their stratospheric spike that had topped out in March last year. And overall, it added up to re-accelerating inflation on top of already very high prices.

Ground beef: The average price of ground beef, 100% beef (excluding round, chuck, sirloin, and preformed patties) spiked by 3.0% in April from March, and by 18.9% year-over-year to a record $6.90 per pound, according to the detailed CPI data from the BLS. Since January 2020, the price has shot up 78%.

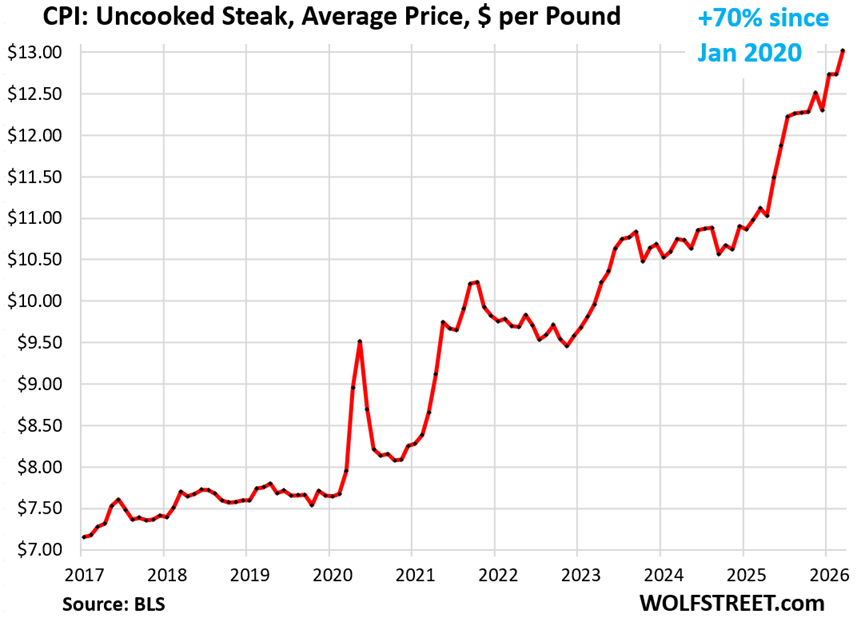

Steak: The average price of uncooked steak spiked by 2.3% in April from March, and by 17.1% year-over-year, to a record $13.02 per pound, according to the CPI data from the BLS.

Since January 2020, it has shot up by 70%, or by $5.37 per pound.

Beef prices started soaring in early 2021 for a laundry list of reasons, including that the US cattle herd has dropped to multi-decade lows, causing tight supply, and including lots of profit opportunities for the industry, such that the Department of Justice has launched an investigation into price manipulation and collusion by the meatpacker oligopoly of Tyson Foods, Cargill, JBS USA, and National Beef Packing Company that controls about 85% of the US beef processing market.

Demand destruction, as consumers revolt against getting ripped off and stop buying beef, would have caused those prices to collapse. Consumers could have let the beef rot on the shelves at supermarkets and switch to the innumerable other delicious animal and plant proteins. Consumers could have shut that circus down. But that didn’t happen. Americans wail and gnash their teeth about high beef prices but keep buying beef and keep paying those prices, and beef isn’t rotting on the shelves.

The price index for beef and veal in total, all subcategories combined, shot up 2.7% in April from March and by 14.8% year-over-year.

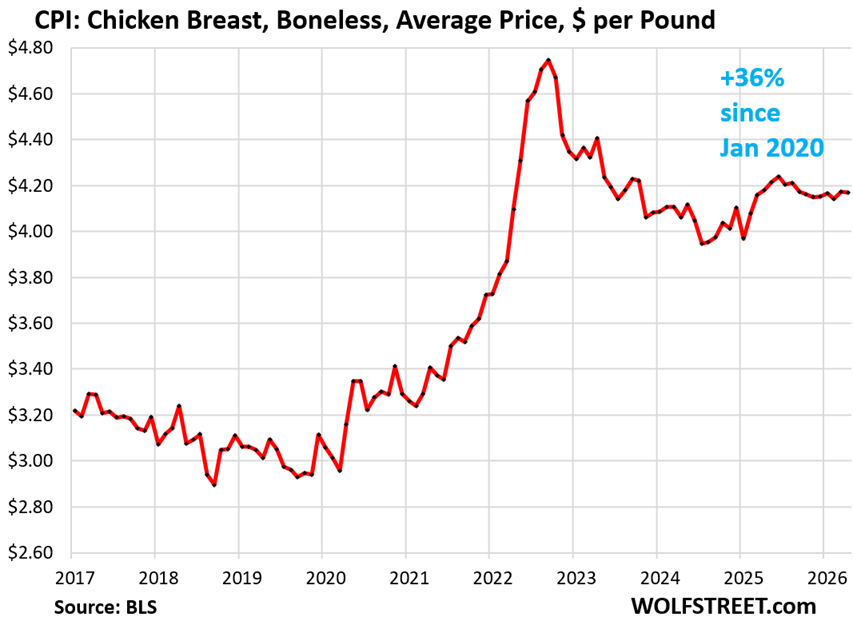

Chicken breast, boneless: The average price of boneless chicken breast was unchanged in April from March and was down a hair year-over-year, at $4.17 per pound.

After the two-year 58% price spike through September 2022 to $4.75 per pound, prices began to skid. Now, though lower, they’re still very high, up by 36% from January 2020.

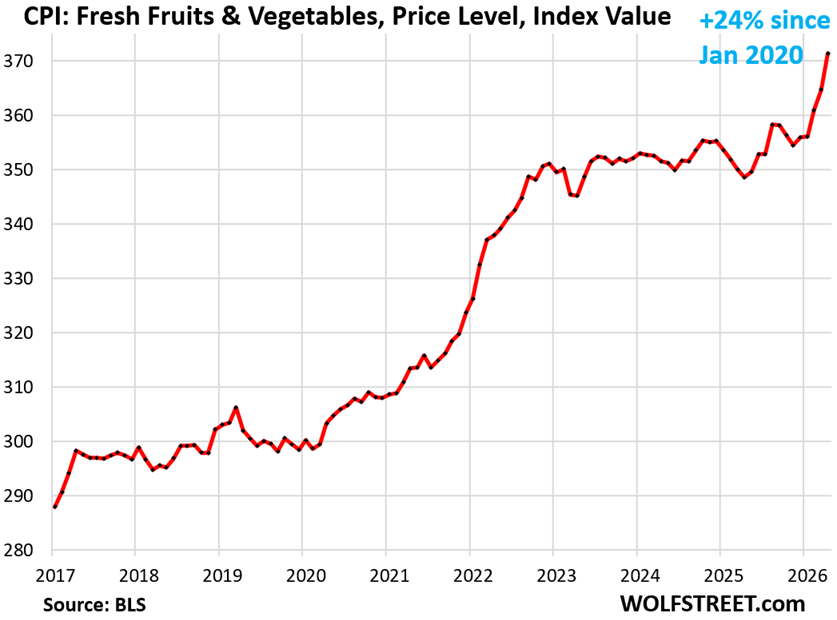

The CPI for fresh fruit and vegetables spiked by 1.8% in April from March, the third such spike in a row. Over those three months, it has spiked by 4.4%, breaking out after several years of relative calm.

These increases pushed the year-over-year increase to 6.6%, up from unchanged late last year. Since January 2020, the index increased by 24%:

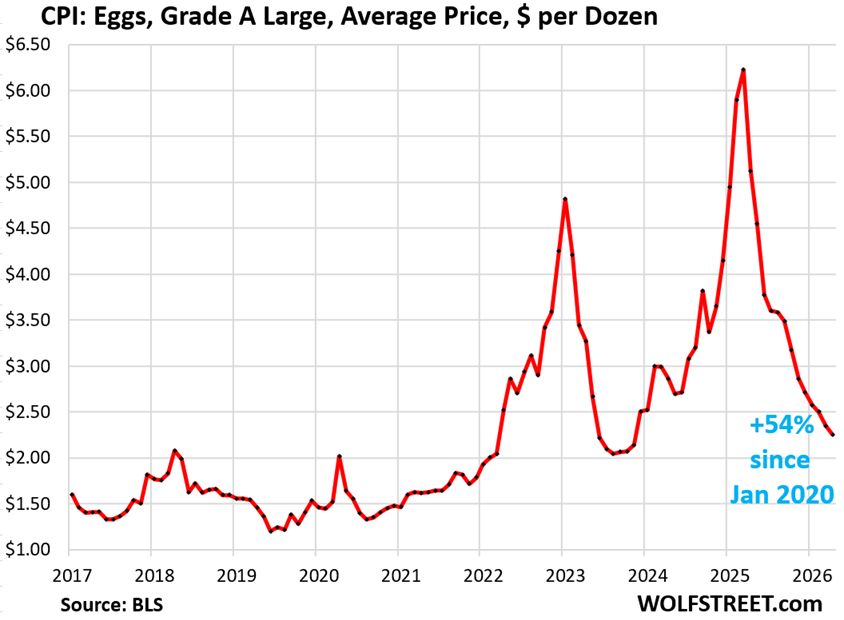

Eggs: The crazy price spikes through March 2025, amid two waves of the avian flu, continued to implode in April.

The average price of “Grade A Large Eggs” fell by 4.2% for the month and by 56% year-over-year, to $2.25 per dozen, by according to CPI data.

Since the peak of the spike in March 2025, egg prices have collapsed by 64%. But those prices are still very high, up by 54% from January 2020.

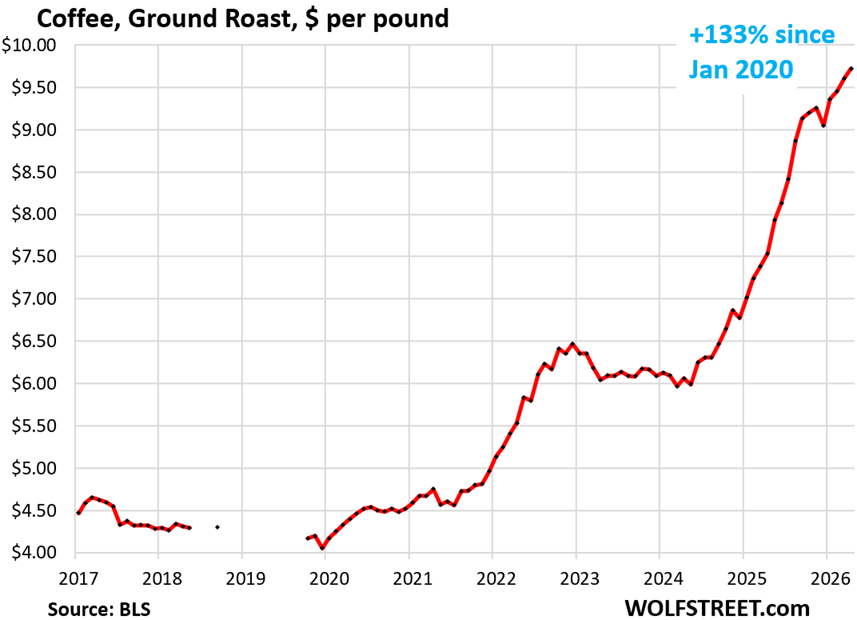

Coffee is another product that Americans won’t crush with demand destruction. For many people, coffee is not optional. It’s required, regardless of the price.

The average retail price of Ground Roast 100% Coffee spiked by 1.2% in April, and by 29% year-over-year, to $9.72 per pound, according to BLS data.

Since January 2020, the price of this type of coffee has exploded by 133%.

Coffee rocketed higher in two waves, roughly following with a lag the two waves in the coffee futures market: The first wave started in mid-2021, the second wave in September 2024.

But now futures prices are plunging while retail coffee prices are still soaring because Americans are still buying coffee and are still paying those crazy prices, me too. Eardrums are blowing out from the deafening sound of Ka-ching at retailers and roasters.

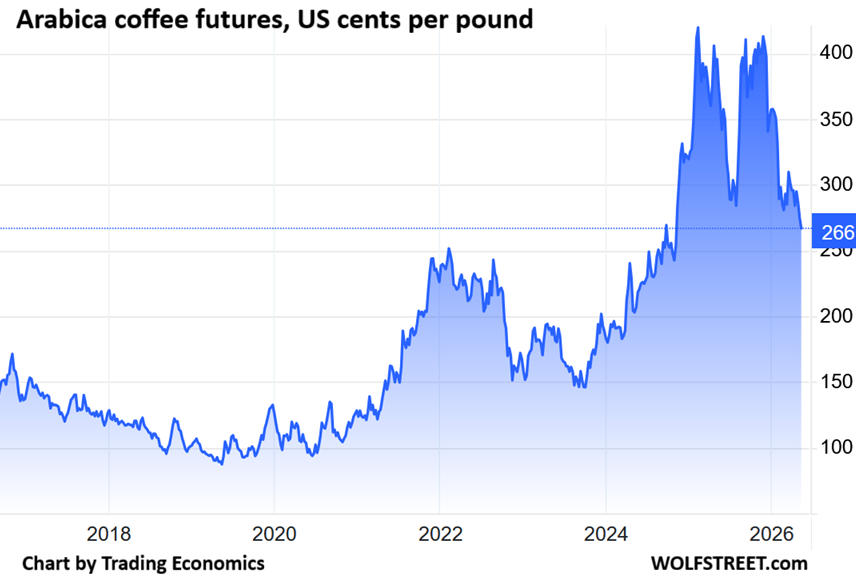

Coffee futures prices plunged recently. Prices of green coffee beans, a global commodity product, can fluctuate wildly, driven by trading algos, fears of droughts, bad harvests, market forces, tariffs, or whatever.

Futures prices for green beans of Arabica coffee have plunged by 35%, to $2.66 per pound currently, from $4.13 a pound at the peak in December 2025, on talk of larger harvests and what not (chart below via Trading Economics):

But the cost of green coffee beans as a commodity is only a part of the retail price of ground roast coffee. The current green-bean price of $2.66 per pound of Arabica compares to the average retail price of $9.72 per pound for ground roast coffee.

The difference between the two is pocketed by roasters, retailers, and transportation companies, which have to spend some of it on labor, rent, fuel, and the like, and the rest goes to profits, bonuses, and share buybacks, because consumers pay these prices and refuse to shut down the whole circus by imposing sudden demand destruction on the industry, which would be a hoot, having tens of millions of Americans driving to work without coffee, and struggling through work without coffee, day after day, month after month.

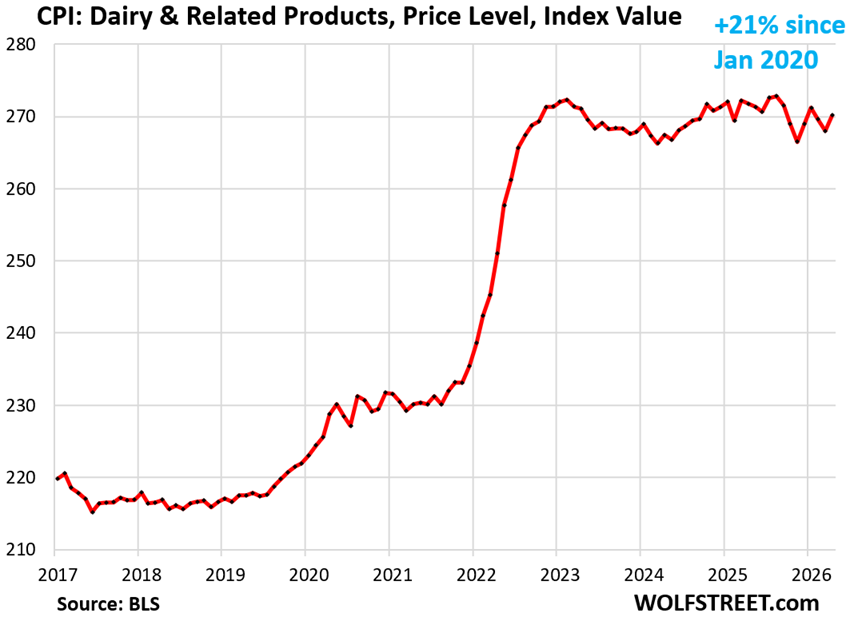

The CPI for dairy and related products rose by 0.8% in April from March, after two declines in a row. Compared to a year ago, it was still down a hair.

Dairy prices are high, up by 21% from January 2020, but the annual rate of change (inflation) for dairy prices has been around the unchanged-line for a year.

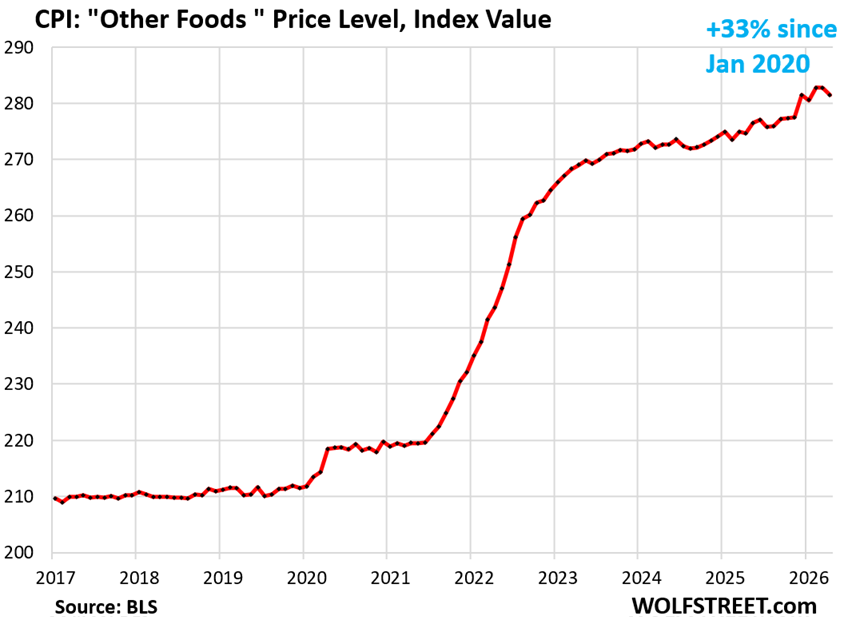

The CPI for “Other foods” dipped by 0.4% in April, and was up by 2.5% year-over-year.

It combines the sub-indices of many food items and categories that the BLS tracks separately. They include sugar, sweets, fats and oils, salad dressing, peanut butter, soups, frozen and prepared meals, snacks, spices, olives, pickles, baby food and formula, etc. So a substantial part of what is mostly in the middle of the grocery store.

Since January 2020, it has soared by 33%, most of it in the two years between mid-2021 and mid-2023.

All combined, the CPI for food at home jumped by 0.7% in April, the worst month-to-month jump since August 2022 (blue line in the chart).

Year-over-year, it rose by 2.9%, the worst since August 2023 (red).

It covers food and beverages that people buy at stores, markets, or online.

Food prices are very high after the massive inflation outburst in 2021 and 2022, followed by mild increases in 2023 through mid-2024, and the accelerating since then. The spike in April added on top of it all.

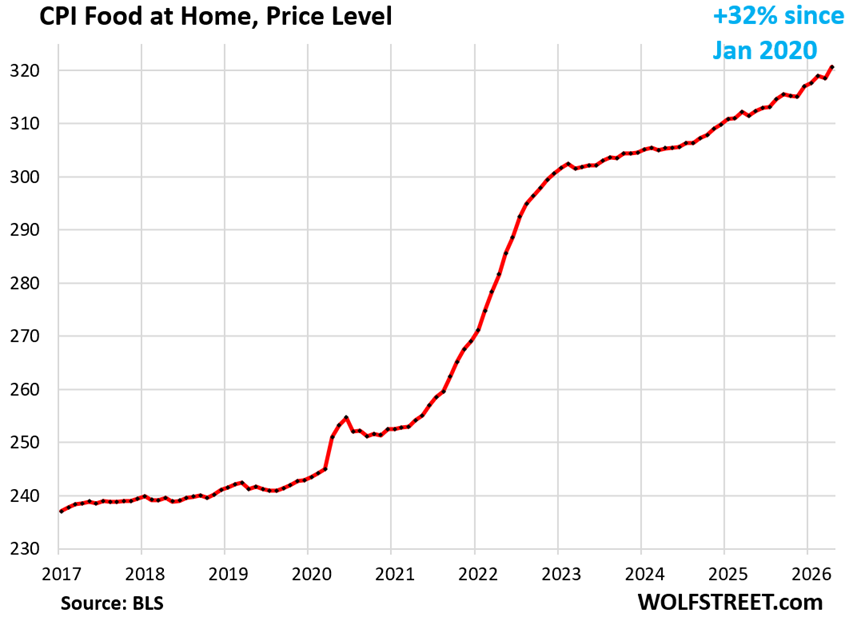

Since January 2020, the CPI for food at home is up by 32%.

In case you missed it: CPI Inflation Blows Past Fed Rates as Core Services, Gasoline, Electricity, and Food Spike. Fed’s “Real” Rates Are now Negative

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Plantation America mentality !

This too shall pass.

Strauss-Howe explains our current situation.

here’s idea – today some 40% of contents of refrigerator end up in trash

I keep telling my wife, either buy smaller amounts or start freezing

and please we don’t have kids at home so quit cooking for 5

then we have massive leftovers and only 1/2 get eaten

fruits and veggies – my wife puts them in frig and no one knows they are there

Where does this lead us? There’s still affordable land, and they don’t make that anymore. I’ve been urging the family to gather and create an estate for self sustainable food production. Noone thinks it’s the end of the world, as if that’s the only reason to congregate and combine resources. I’m not panicking. I’m concerned. I like my growing capability and the 100 free range or so eggs I gather per week. It helps.

IMHO, by beef ranching, I think the days of cheap beef are long gone because the uber-wealthy have been buying up ranches at high speed for 30-40 years, such as by Ted Turner.

The Uber-wealthy have been buying ranches for generations. They are not a major cause of the decline in the cattle count. A likely bigger effect is a reduction in the herd size of small operations due to drought and the decline in the interest of current working generations in livestock production.

Lol it is not Ted Turner. He sed and used some of that land to produce a substitute good, bison.

Instead, cattle farmers cut herds due to drought and never got them back to previous levels. Plus costs more for feed.

Expect this to get worse with climate change. We were told we would get more droughts. We got more droughts.

I know a few cattle ranchers. It’s a tough business because packing houses and feedlots capture most of the profits and will always squeeze the producers.

The only ones who survive are those who have avoided a lot of leverage and expansion in “the good years”. Many are 2nd or 3rd generation who have managed to keep their acerage together without hanging a lot of debt on it. They don’t get rich, but they have a good, comfortable life and tend to be very adaptable and able to resist the temptation to “reach”.

1. Wealthy family buys ranch subdivided from ag land.

2. Wealthy family leases hay fields to local beef rancher (whose family may have owned the land before) just to get an agricultural exemption on taxes, not because they need it. Small farmer pays for water and all maintenance.

4. Wealthy family complains about pets eating cowpies, dust, truck traffic, and mud from irrigation.

5. Small beef rancher gives up and scales back to own land, reducing profits and saving the headache of leased land.

I like beef as much as the next person but not exactly a resource efficient protein source.

I’ve tried to do my part with coffee. Stopped buying bad cheap coffee (Folgers, Maxwell House) and started buying store brand. It’s brutal stuff. Sour and bitter as though it was roasted as an afterthought from some other industrial process like smelting radioactive aluminum. But, it gets the job done.

Trader Joe’s my friend. The German’s are a force in the US grocery scene….

Pete,how is Joe’s price wise,have one I pass once every couple of weeks but never actually went in.

James, in my experience, Trader Joe’s is well priced for numerous items and can compete with the regional supermarkets. For instance, in the Trader Joe’s stores in San Diego, chicken is $3.49 per pound, 80/20 ground beef is $5.49 per pound, and fresh salmon is $10.99 per pound. It’s much tougher to compete with Costco prices, but bananas, for instance, are cheaper at Trader Joe’s ($0.23 per banana) than at Costco unless you find a bunch of bananas at Costco that have at least nine bananas. Trader Joe’s also won’t be able to compete with the likes of Aldi or local ethnic stores for the majority of produce. Having said that, for my family, we’ve found that a combo of Costco and Trader Joe’s is nearly perfect for convenience (I’d rather not haul my toddlers to more than two stores) and prices.

As long as you know TJ is actually owned by Aldi,,, you’re good to go to either and, of course, in keeping with the illusions of ”free choice” blathered every day by the propaganda machine AKA ”mainstream media, etc,”

YOUR choices will be completely YOURS,,, and not the result of advertising, etc…

For any and all having any kind of challenge affording food,,, please keep in mind the vast markups between ”real” foods and those prepared or processed in any way,,, even without consideration of the poisons used to preserve P&P foods.

Trader Joe’s is owned by the Albrecht family, who are the founders of the German discount supermarket chain Aldi. However, the grocery chains are completely separate businesses. While both chains trace their roots to the same founding family, Trader Joe’s and U.S. Aldi stores operate as entirely distinct companies with separate leadership, sourcing, and store strategies.

Fantastic German products,

The Brie with wild mushrooms….😀

After the third cup, you tend not to taste the bitterness.

Try adding a pinch of salt to the grounds. I’ve found it takes the bitter edge off cheap coffee grounds

Start roasting your own. You’ll never go back to commercial coffee.

For the past yr I’ve only bought coffee @ Costco. Starbucks usually puts coffee on sale twice a yr. Last purchase was Pikes Peak, 36oz bag for 13.99

Bought 6

I simply can’t compromise on coffee. I will work an extra hour a week for it. Like the methead I see motoring around the local plaza raiding all the recycling bins, the bean has my by my very soul and will not let go 😢

I scored a 1 bag of Peets last week for $3.70, and $6.75 at Safeway.

Some of these chains are starting to gouge. Although Kroger owns North Carolina based Harris Teeter, they insist on portraying it as some upmarket place. Good luck with that Cincinnati! In competitive markets Harris Teeter will be destroyed in this environment

It is remarkable the lengths that large supermarket chains (looking at you Kroger, etc.) will go to preserve acquired chain’s names/obscure the fact there are significantly fewer grocery store chains in the US than it appears.

Most acquirers in mergers *want* to slap the parent company’s name on the acquiree for branding purposes.

Supermarket acquirors are notorious for doing the opposite.

One summer we experimented with eating snails from the garden.

They tasted just like escargots, which is to say they tasted of butter, parsley, garlic, and rubber.

No ill effects at all. We had taken the precaution of confining them in plastic buckets, feeding them for a few days on lettuce leaves from the garden, and giving them plenty of water, regularly renewed. Naturally the garlic and parsley came from the garden too.

And today, Herself is about to bring in the first of the year’s crop of strawberries and the first “baby” broad beans. They go awfully well with bacon. The beans, I mean.

Given the choice of no beef or no bacon I’d bid farewell to the beef. But then I expect we eat more fish than most Americans do so beef isn’t a predominant part of our diet anyway.

My chickens used to eat the yard snails when I lived in California. Their eggs tasted great. The chickens were eaten once they got too old to produce. New chics were their replacements. It’s a cycle.

As Wolf says: unless, and until the consumer balks and stops buying – these prices will stay elevated. Same for cars, houses, etc.

Anecdotally, we have definitely cut back on steak in our house and have traded to pork tenderloin and chicken.

Amen on chicken and pork.

Eggs at local Aldi were $1.47 last week… a protein bargain (even after spike and retreat), if you appreciate the convenience and deliciousness of the egg sandwich!

And our president goes to China and wants them to import more American beef.

And the real baloney, we are setting records of exporting gasoline, diesel, jet fuel and other fin8shed distillates and the Republican Congress will not embargo these exports to lower the domestic prices.

MABA – Make Americans Broke Always

There is always one who only sees through the lens of their political rage.

I guess it WOULD all make more sense if I picked up a copy of The New England Primer and mastered it….so to speak.

And his name is Trump.

Unfortunately, him being President means the rest of us need to see the world through the same lens if we want to understand what’s going on.

The President is clearly the one who has TDS…I totally am confused about how that all got twisted and spun..but, like I said….I never mastered the New England Primer…..or watched “reality” shows…..

alan,

I see the export of LNG to be especially short sighted. While we have significant reserves(proven) and resources (best guesses) it isn’t that much in context potentially struggling to have enough easily accessible supply post 2030 if we ramp exports to the degree possible (not what is tweeted). That and liquifying natural gas takes about 10% of gas as expensive to liquify. That said, oil companies care about next quarter only so expected.

alan – congress or the pres will start limiting exports assuming inflation continues to spike in the next few months. Be patient!

Unfortunately it’s not that easy for 2 reasons.

First, oil isn’t exactly fungible. Shale oil is light and sweet. But our refineries are built to process heavy and sour grades from Canada, Venezuela, and the middle east. Refineries can process different grades, but it won’t be optimal, meaning less efficient and therefore more expensive end-products. So restricting exports of shale oil won’t help much.

Secondly, exports are currently up because production is up: drillers see the prices LNG is getting in international markets and have started ramping up. If we restrict exports, they won’t all of a sudden sell it to us for less. They’ll just stop producing from some of the higher cost wells that don’t make financial sense without high prices. So while prices might decline somewhat, it won’t be as much as you expect because production will simply go back down.

People need to quit regurgitating this stuff about refineries from 15 years ago. Refineries invest all the time to maximize their profits. Many refineries have been around for 100+ years, but the equipment is new. It’s not static.

Wolf-

Yes but no one is going to invest in changing their refinery for the long term because of a temporary disruption. Ironically, many of these refineries used to be optimized for light sweet crude like WTI but as we started importing more from Canada and others, the refineries moved towards heavier grades. So I agree that refineries aren’t set in stone. But neither do they change on a dime.

Most likely what is happening now is what I mentioned: that refineries optimized for different grades are being more opportunistic, taking whatever barrels they can get, even if there will be some inefficiencies from processing them, and selling the output. But those inefficiencies do add up to meaningful costs, not to mention unbalanced supplies (eg lighter grades tend to yield more gasoline while heavier grades yield more diesel).

I as a paranoid prepper stock up a lot(also have relationships business wise with small/local farmers)but they do NOT grow coffee beans,a life necessity!The smaller guys are expensive but the meats great and just use more rice/pastas etc. to help stretch out meals.I also like that folks have a reason(farming)to keep lands open and as the deer hit on their crops they are happy to have me hunt there!

I stock up on beans vacuum sealed that are good 2 years down the road(perhaps longer but have not gone much by the use date. I pay about 9 bucks for 22 ounce bags and could save more but like the smaller bags to keep beans fresher as opposed to opening a 25-50 pound bag,I do see them in me future though soon.

You have the land and desire growing veggies can be tiring but rewarding work,get heirloom seeds and see what grows happily in your neck of the woods.

I watch a few friends properties when they are away and thus as both have flocks get fresh/local eggs free,lucky to have good friends who also happen to have chickens.

James,

We grow at least 75% of our produce, and this year concentrating on what freezes best for the winter and what is the best value for required work as we age. Green beans and peas freeze very well as do raspberries and blueberries. Grow enough garlic for 10 families and spuds are up. Went to raised beds for most crops two years ago so that makes it much easier. Greenhouses produce tomatoes, long english cukes, celery…..stuff like that. lettuce in garden and early in greenhouse. Corn will go in the first real hot spell. Supply neigbours with eggs and that covers all feed costs. Today I planted some tomatoes for my 99 year old neighbour. It keeps him going.. Save our own seeds except for hybrids as they revert. It is very satisfying. Used to raise sheep for lambs but cougars kept coming and coming. Our base protein is salmon caught from my dock and/or chicken and pork. Beans. Nothing like a good burger but beef prices are crazy.

For a lark I planted some very early potatoes in layers in a 5 gallon bucket with drainage holes. It should give is new potatoes very soon. Lots of fun. Seed saving is done after pods dry. My wife shells them while we watch a movie…evenings.

Won’t ever give up coffee. Just make it at home….even pricey beans works out to pennies a cup.

regards

Paul,you have the lands I seek out but do to buyers strike do not have!

I feel one does not have to be 100% food self sufficient(though would be great).Specialize in what you are good at to a degree and trade with others specialties,makes sense and as you point out builds community<i.e. your tomato neighbor and chicken eggs fans.

I would unless directly threatened learn to live with/avoid cougars,threatened directly while me handle covers that!

The developed world is quickly learning that you can’t land, housing, food, oil, or water the same way you can create “financial products.”

I understand not giving up coffee. It’s a drug addiction, but there is nothing that replaces it, Don’t even suggest tea. Hey, and if you afford beef, go for it. I won’t blame you. In a couple of years the effects of the drought will be history and prices will come down. But chicken and pork are a lot cheaper right now, and better for the world. Order the McChicken and stop whining.

I’m a long time black coffee drinker. I had a stomach issue recently that thankfully was temporary, but for a few months I couldn’t tolerate coffee, or anything acidic or spicy. I found that tea didn’t bother me. I switched to drinking hot unsweetened tea in the mornings. I had to use a lot of tea bags to supply the requisite caffeine, but it did the trick, and my working abilities were not impaired. However, it tasted like dirt, and I’m back on coffee now. For those looking to give up coffee, tea is an option, if your taste buds can stand it.

Do you know that dark coffees like French Roast might be a lot easier on your gut than light or medium coffees?

I had issues with coffee until I made the switch. Like night and day difference for me.

Thanks, I didn’t know that. I’m a regular Folgers drinker, so I don’t know what kind of roast that qualifies as. But someone gave me a bag of french roast they didn’t like, and I’m about to give it a try.

Chicory sometimes works for me.

(Black tea sometimes screws up my stomach)

Marvin,

With the dark roast I don’t put too much coffee in. I use about 70-80% of what I would otherwise use because the dark coffee flavor is stronger. Some like it strong (Europeans and Seattle folks) but I prefer less dense flavor. Try it both ways.

During the Civil War, most southerners couldn’t afford coffee. They drank a brew of steeped yaupon holly leaves instead. I’ve never tasted it myself, but yaupon is native to the south (and is North America’s only caffeinated plant), and is grown mostly for ornament. Haven’t tried it myself, but the usually exuberant comments section’s rather dour mood here has me thinking I might should grow some. Maybe get a little chicory while I’m at it.

If I ever want an economic analysis of an industry, I strike up a conversation with a ma and pop business, in my case a small coffee roastery in Canada. Thankfully it wasn’t busy because I got an earful! They never dreamed that they would start the day analyzing socio-economic and weather events at breakfast time. The middle east war has diverted more ships past Somalian pirates who have realized that every container of coffee is around $200K and they are holding it for ransom! Plus serious organized crime has become involved in stealing coffee containers once they hit the port. Plus, as Wolf mentioned, the draughts and wars interfering with coffee production. Anyway, I too am held hostage and will pay almost anything for coffee. Cheers!

The CPI for food may well be up 30% according to that metric , but

the US must have some sort of magic food store , because in Canada, post pandemic , the price increases for most food products have increased on average 100%.

Putting in a request that this magic store be tariff free access in the upcoming trade negotiations and we will forgive all and become winter tourists once again

It’s got to be a rare occasion / need for me to buy beef.

The one item at ALDI that’s defied the significant price drop of eggs is their egg substitute. It hasn’t budged one cent, since Trump took office. In fact, it went up $0.10 in the past month.

It’s interesting to see how many food products have inelastic demand. Kinda makes you wonder why producers didn’t increase to these prices a long time ago. People could switch to alternative producers that undercut the other ones. But that hasn’t happened much. It’s almost as if our food complex has monopolistic pricing power. Oh, um, yeah….

This. We need to _reinforce_ antitrust law, and then _re-enforce_ antitrust law!

All critical markets should all have at least 10 competing suppliers, and no single supplier with over 20% market share. Split up anything larger and get the pieces competing with each other.

Similarly, companies that win in the stock market should be broken up as well, so that no single stock is more than 1% of the total market cap.

What we have now on supermarket shelves is mostly fake competition, with just a few primary suppliers hiding behind a dozen fake brand names.

So socialize supply through law making and what happens when it isn’t profitable? Do you then force them to set prices at specific levels, hire specific numbers per store and quotas of goods purchased per month for a store? Can the owner escape through bankruptcy or do you move up the supply chain and mandate goods prices to the stores? Where does it end when profit and loss are not allowed to be considered? Do we start asking “Who is John Gault”?

Enforcement of antitrust law is not “socializing supply”. Nothing I wrote said anything about mandating prices or profits. Just making sure customers have choices and don’t get gouged.

The entire classic definition of capitalism assumes marketplace competition among many suppliers, not monopolistic domination by a few.

Where suppliers deliver well they should profit. There’s nothing wrong with profit … but that profitability should also attract fresh competition.

Put another way, your freedom to profit from trade does NOT extend to the freedom to deny someone else the chance to compete with you.

You think they were just giving the meat away at a loss before? Or accepting lower profits out of the goodness of their precious hearts? Pricing usually adjusts to suit demand. If everyone had so much money before and they could have just jacked the prices up I think they would have, they aren’t stupid, they are in business to make money. The difference is money fell into a lot of people’s laps and prices then adjusted accordingly. In fact some even predicted they would….crazy. but I highly doubt they never once thought of this crazy idea to raise prices long ago. Peoples wealth changed, not the business leaders mindsets

Howdy Youngins. Inflation could be worse and was worse before and probably will get worse…Go on a diet if it bothers you…

Keep on Sailing Sailors. I will never stop…

Listening to a great song about a hearse and no trailer hitch…

Even if the body didn’t tightly regulate fat percentage, 10% body fat is only a month of food bills. Not really a long term solution.

Howdy Jdavis. If a person can control their appetite, imagine just how much more one can control. When we control our own futures life is good.

When Debt Free Bubba wrote: “Go on a diet if it bothers you…” it reminds me that starting in college and until I got married, I spent as little as possible on quality food so I could invest more money. In addition to having more money to invest not having any junk food or processed food around the house is probably why I never put on weight and have remained so healthy. After getting married it was a lot of work to get my wife (who was raised by a Mom that loved Trader Joes heat and serve meals) to cook everything from scratch (it got easier once I taught the kids to peel potatoes and chop vegetables when they were young so they could cook entire meals for us by the time they were in Junior High).

I definitely have stopped eating as much beef but you are right, the coffee is where I draw the line. At least for now. But I am old enough to remember when beef and seafood was a luxury.

I have had pet chickens for 30 plus years and no longer can eat chicken without feeling sick. Not by choice. But I have been eating more of the eggs rather than giving them to neighbors and charity.

I am certainly wishing I was shorter and had smaller muscles at this point. Ha ha. Dang my Scandinavian German genes. Luckily the old age slower metabolism will kick in soon.

This is a real problem. The 30-40% inflation and permanent price level changes from January 2020 to January 2024 was painful and ugly, and hopefully taught the lesson that an extreme panicked overreaction to a health scare and massive money printing was a stupid idea.

Now, after what appeared to be a slow return to 2% price increases we’re back up to double that and more.

The Fed has to administer some very painful medicine before it’s too late. The ten year is going to 5% then 6, and maybe 7+ before it’s all done. The Fed can try to keep the short end anchored at 3.5% or so but they need significant $50B a month QT and stop all hints of rate cuts for a long time.

Rate cuts used to help employment. Now they seem to allow faster capex and replacement of thousands of higher paid workers with a-i. See Metas big layoff plan for this week. People lose jobs and face higher inflation with low rates.

If you find fresh-brewed coffee too acidic try doing cold brew at home. If you like your coffee hot, put it in the microwave for a couple of minutes.

WARNING: cold brewing can be very messy

We buy our beef by the quarter. All ground – steaks, roasts and prime all to burger. Due next week is another quarter of stew meat chunks with a bit of burger. That’s how we eat and cook and from scratch.

Our neighbor raises grass fed Jersey beef, through a private butcher and delivered to our door. There are no sick, medicated cattle or questionable hygiene questions. No questionable employment problems. Just neighbors doing business together. Yup, it’s more expensive than store bought. But the amount of meet left in the pan after you cooked it and no water or fillers or excess fat. Oh, yeah, it tastes really good. More than you can imagine.

And we are supporting our local economy directly. From the producer to the butcher – all the middle stuff is gone. But I understand some folks don’t have access to those trustworthy resources let alone freezer space for a quarter. Gee, that sucks.

There are solutions to the food distribution systems but you have to do something different instead of complaining and doing the same thing over and over. And you just might be for the better doing so.

Zohran Mamdani said my coffee and beef will be free in NYC. And I will get to the city run grocery store on a free bus ride.

I love that your response to reading this report for the whole country is to get mad at Mamdani.

Bob B is just being silly with internet BS. He is in Texas and Mamdani has nothing to do with his coffee and beef.

False. Why put up totally false nonsense?

Mamdani promised lower prices on essentials. I expect by offering limited options, buying in bulk, and subsidizing the store overhead. He never promised free food, that sounds like a misinterpretation that may have been spread on social media. I doubt they’ll be selling beef for less than wholesale, likely a bit more, which will still be pretty expensive.

There is always one who only sees through the lens of their political rage.

You should get better sources of information that do not make you look foolish. Why not educate yourself and become a better person rather than continue to use sources that just feed you what you want to hear?

I always thought the egg spike was just ridiculous. You had politicians claiming they could help bring prices down, but in reality it was just avian flu that was allowed to propagate without intervention from the very same politicians overseeing the FDA. Once the culling got the epidemic under control, prices dropped back to earth. Who needs regulations?!

As for beef prices, I grew up in central Kansas where the stench of manure from feedlots is synonymous with money. The industry is no longer the same as when I was a kid. Large alfalfa and corn fields have replaced wheat, but require irrigation and pesticides. There are more cows than humans in Kansas. But, heat waves and fires changed the dynamics and led to the death of herds. These losses don’t help with prices.

LOL, so glad I’m not a coffee, soda or alcohol drinker… and good clean water is still practically free.

This seems like a good thread for a friendly reminder to any younger readers (does Wolf have any younger readers?) that every $5/day “lifestyle habit” costs you 1-3 years of retirement!

$5/day, x 365 days/year x 30 years = 1 year of middle class living expenses. And if you invest the savings wisely, you can make that 2-3 years.

Mild stimulants like coffee might be the only exception, since you feel like you “get more” out of your available time-on-planet?

P.S. Unhealthy habits are even worse. Those are a double whammy because, first, you can’t retire as early, and then second, you don’t live as long either.

P.P.S. Even if you love your job and never want to retire, the sense of personal freedom, peace of mind and reduced stress that come from being financially secure are priceless and add years to your life expectancy.

1. Read up on the now large body of research showing that regular coffee drinkers are much less likely to suffer from dementia, such as Alzheimer’s. I don’t know if they understand the exact mechanisms, but regularly drinking coffee seems to provide significant protections. And your brain’s health does matter.

2. Coffee offers other benefits as well. Alcohol offers no physical benefits (other than pleasure and social lubricant) and is a toxin, which is why it is an effective disinfectant, because it kills stuff. So don’t lump coffee and alcohol into the same sentence.

3. It’s only $5 a day if you go to Starbucks et al. If you buy whole-bean coffee ($20 per 3-pound bag at Costo, delicious), grind it yourself, and make coffee yourself by whatever method, a cup costs maybe 25 cents, depending on the kind of coffee, the strength of your coffee, and the size of the cup, one of the cheapest pleasures out there.

4. Obviously, you can overdo anything, even coffee.

A single cup of cost-efficient coffee is a reasonable deal, but that’s not how a lot of people approach it.

Personally I doubt the health benefits are real. Dietary “science” is rife with fad research pushed by vested interests. So much of what was “proven” 40 years ago has been proven wrong.

It’s very hard to measure what people actually do vs. what they say they do, and even harder to establish causation rather than mere correlation. But it’s very, very easy to write something persuasive when it validates people’s pre-existing preferences.

I think it’s reasonably clear that coffee doesn’t do tremendous medical harms or benefits. If it was like, say, smoking or alcohol, the consequences would be a lot more obvious. And although I’m skeptical, I do hope the research on mental health benefits is real, and the calcium-loss data (osteoporosis risk) gets disproven… because although I don’t drink it myself, my spouse loves that daily $0.25 home-ground Costco coffee too!

But I’m gonna retire first. :)

A friend of mine basically said the same thing about Starbucks twenty years ago. His logic was simple: forgoing a Starbucks coffee every day of the week saves enough for a vacation. I buy local roasted coffee beans from Sam’s Club, and many great tasting cups of coffee for a fraction of the price. It takes five minutes with an electric kettle to make a fresh drip cup of coffee. Even if you must have espresso or a cappuccino, doing it at home is cheaper and probably quicker than going to a coffee shop and standing in line.

$5 a cup? That’s a bargain! Lol. My daughter and friend ordered Starbucks via Uber delivery one day last summer. I almost had a heart attack. Inconceivable!

This. Paying $3-$6 for a coffee or latte out each day is a choice.

Also, even if you’re too lazy to buy ground coffee and brew your own, you can get a Keurig for under $100 on sale, and you can get the Kirkland brand K-cups for under $30 on sale for 120 pods, so same under 25 cents that you noted.

Are K-cups amazing? No, but it’s decent enough.

I just looked and the 100 pack of Litpon Tea Bags is on sale for just under $5, so $0.05/day so a lot cheaper per day than going to Starbucks.

There’s a ton of phytonutrients in coffee which are antioxidants, anti-inflammatory and immune-boosting.

I have always enjoyed coffees. A few years ago I did a paper for Biology class (refresher, decades after finishing college) about the proven benefits of coffee.

Cleveland Clinic, UC Davis, others have studied the benefits of coffee and generally conclude that it’s really good for you. As long as it’s fresh (doesn’t sit burning/heating in a carafe, or percolated).

Been drinking it since I was 8 and I’m quite healthy.

Starting next week, WolfStreet is raising its online

access by 50% due to rising inflation pressures.

Wolf cited the rising cost of driving his gas guzzler to work as one component of his rising costs, as well as the numerous lattes he drinks throughout the day to keep him hyped up. He assures his readers there will not be another rate increase until at least 2027.

He added that living in the most expensive city in the WORLD adds to his cost of doing business. He also said he may relocate to Stockton, CA which offers a lower cost structure and is (in Wolf’s words) “the most beautiful city in the world.”

OIL SUPPLIES ‘DECLINING RAPIDLY’…

GAS PRICES UP 56% IN USA…

I too keep reading about oil supplies dwindling yet I don’t see any type of hoarding or rapid increases in price to 200 plus . The oil market is extremely mature and oil traders globally know their business . The dwindling supply must not be that big of deal but higher for longer will persist

There is no oil supply dwindling in the US. The US is awash in these products, being the world’s largest producer. When we get solid production data a few months from now, we’ll see that US production and exports rose during this time.

I drink Mount Hagen freeze dried coffee and it has gone up from $11 to $16 a jar. 45% increase – gasp! , but that’s 20c a cup so I’m not hurting. I’ve switched to condrnsed milk instead of half & half for diet reasons also the cans don’t go bad. I might tell a difference if I think about it.

Beef and pork are local from food co op. I like meat from happy animals. With inflation the price isn’t much more than feedlot beef now. Produce is where I see the inflation, but at the supermarket more than fruit stands.

Let’s just say that because of certain current events prices have nowhere to go but up.

Can changing some government policies at least stabilize prices? Maybe. But you have to care. If you don’t care or you don’t get that it’s important…you’re out of touch.

It’s inflation,stupid.

The cheapest meat we enjoy is chicken livers. You eat lots of chicken in the US so your supermarkets must presumably sell chicken livers. Yet I’ve never seen them mentioned in online discussions.

Lambs’ livers are even better but more expensive.

Loaded in fat and cholesterol. I’ll pass, even if I could get it for free.

You are a generation behind with your food taboos. Catch up – cholesterol is not evil but necessary. Enjoy the new conventional wisdom until it too is cast aside in favour of a new one.

You really could fill hours with this sort of stuff. Cow farts cooking the planet is another.

For all the CO2 we spout, don’t the plants just get fitter?

If you are in a field/profession that has had wage increases proportionate to inflation this may not be so bad. However, those in fields that have stagnant pay or below inflation this is definitely becoming tougher to absorb. I do wonder how inflation in these items in the US compares to places like Canada, Europe.

Just my own observation, but a lb of lean ground beef here in Toronto, bought from Walmart, has gone from $6 to $9 over the last couple of years. Chicken inflation has been noticeable. You rarely see a good deal on meat in the supermarket these deals. Like the comments from others here, there is a lot of concentration and increased profit in the supply chain in Canada. But most farmers and esp beef growers are making more money too. Supply management keeps the cost is dairy and chicken permanently high. And for much of the year our veggies come from California and Mexico.

I lost 50 pounds by not using oil and by only eating 1 pound of meat per week instead of 3. I’ve read that the average American eats 4 pounds per week! Get a vegan cookbook, find 4 dinners you love, make a stack of them for the fridge and eat as much as you want. Then once a week have a steak dinner. Great Chile does not need meat. Black beans are pure, ultra versatile protien

Incomplete protein though, never mind the other important stuff your body needs from meat.

Of course a vegan diet can provide those missing parts, but then those foods aren’t exactly cheap or ecologically optimal to farm either.

Followup on the prior articles about rising interest rates:

The charts for the Total Bond Market ETFs, such as BND and AGG, are in process of retesting the March lows.

If the March lows don’t hold, that triggers a lower-highs/lower-lows downtrend pattern. Very similar to the start of the 2020-2023 bear market in bonds.

On a total return basis (including dividends) the March lows are barely holding, and the Total Bond ETFs are breaking down from the same general level as the 2021 top.

It’s not just the total-bond-market funds, either. The standard intermediate-term funds (IEF, VGIT) show the same pattern.

It’s like a crash occurred, but the value of USD vs assets.

All that QE devaluation, the elephant in the room, was suddenly recognised, the Covid shock made people acknowledge it.

Same with stocks and the inflation trade.

Now the question is does a future business cycle end correct a lot of this, or will assets be front-run by people expecting QE/easing again heavily subduing any dip in USD prices of assets?

Beef vs gold for example doesn’t look too bad.

There is no “market” for true price discovery. We’re all Chinese now. Completely managed eCONomies. The Fed’s balance sheet has already begun growing again. Welcome to the centrally planned world…

Hedge accordingly.

Voters: We want higher GDP and higher wages too!

Politicians: Hmm, I know how we can engineer that.

US Dollar: Falls like the Turkish lira.

A hungry man is an angry man…

Hedge accordingly.

SSRI’s are anti-angry pills. The world would be a better place if we all took ’em. Seriously.

I kind of think it’s a good thing beef has gotten so high. Less cows getting killed which is pretty sad, though I eat it on the rare occasion, so I’m guilty too. I just read beans and rice make complete protein, and they are still pretty cheap, so that is a good healthy option for people.

I was thinking as a single person shopping for myself, that food is a relatively small percent of my budget. Was wondering if for some people, food is a lot more of their budget, and Google said yes, that a family of 4 might spend $1,200 to $1,400 monthly. Now that surprised me because I spend substantially less than $300 per month on food (dividing the cost for 4 by 4). So I’m wondering what are these folks buying that is so expensive, maybe beef still? Because it seems they could save a lot by choosing cheaper, but still very healthy, maybe even more healthy options. And Google agreed with my recommendations, saying they could save a lot by buying whole-food staples. Such as:

Oats: A large canister provides breakfast for around $0.15 to $0.20 per serving.

Rice and Beans: Buying dry beans and large bags of rice drops dinner costs to about $0.50 per serving.

Potatoes: A 10-pound bag provides versatile, calorie-dense meals for roughly $0.30 per pound.

Canned Tuna: Provides affordable, lean protein at about $1.00 per can.

Some other very cheap ones healthy foods are carrots, apples, some chicken, papaya, bananas, roma tomatoes, cabbage, lentils…I’m sure there are plenty more. So folks have options here, as opposed to some other types of inflation that are more unavoidable such as electricity.

Bananas are what, like 29 cents each? At Whole Foods I pass on the $10 boxes of cereal (HOLY MOLY) and go for their $3.99 store brand. But $20 for a freaking Chipotle bowl and $60 at Chic-fil-A for a family of four? My pre-teen ordered $62 of food at Cheesecake factory a while ago. A steak and two sides. Wuuuut?