Mortgage balances barely ticked up, but HELOCs soared.

By Wolf Richter for WOLF STREET.

Mortgage balances barely inched up as sales of existing homes remained in the freezer and sales of new homes – while decent — occurred with big price cuts and incentives that kept a lid on the mortgages needed to finance them. And new home sales accounted for only 17% of total home sales.

But HELOC balances soared.

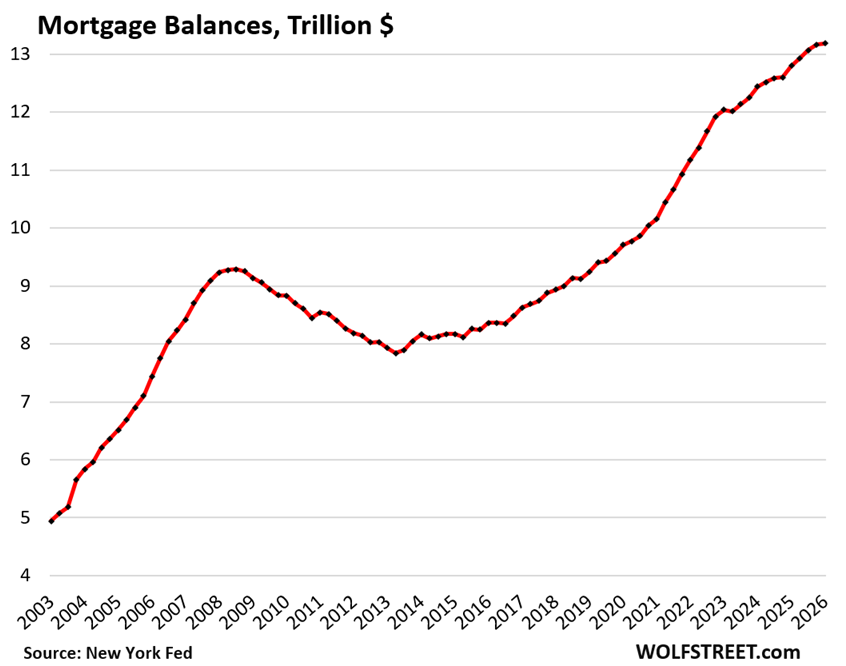

Mortgage balances inched up by 0.16% (by $21 billion) in Q1 from Q4, to $13.19 trillion, according to the Household Debt and Credit Report from the New York Fed, which obtained this data via its partnership with Equifax. Year-over-year, mortgage balances rose by $387 billion (+3.0%).

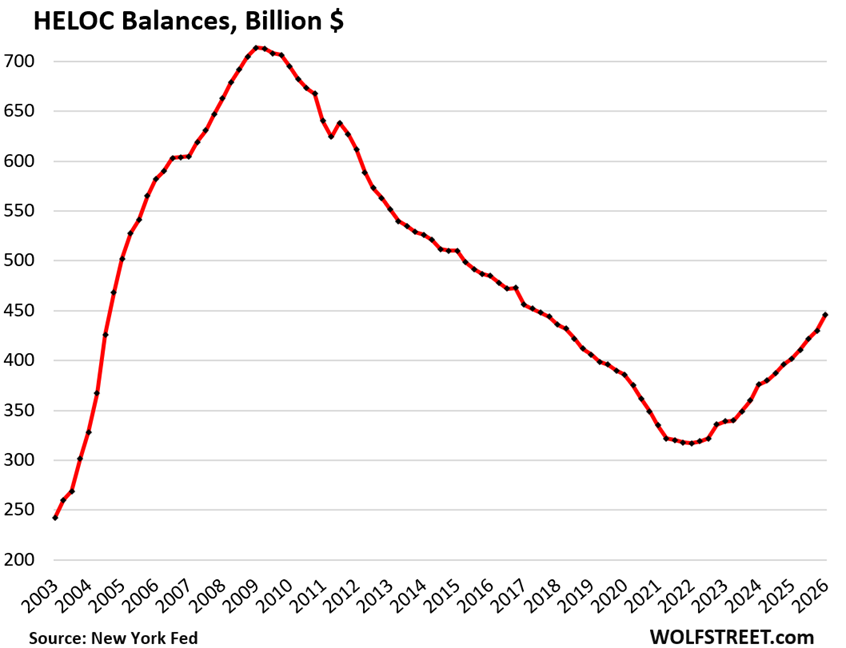

Here come the HELOCs: +41% since Q1 2021.

Balances of Home Equity Lines of Credit spiked by 3.7% in Q1 from Q4, and by 10.9% year-over-year, to $446 billion.

Since Q1 of 2021, the low point, HELOC balances have surged by 41%.

These are actual balances drawn on HELOCs and do not include the unused portion of those lines of credit.

A HELOC is a second-lien loan on the home that increases leverage and that, if defaulted on, can lead to foreclosure and loss of the home, even if the first-lien mortgage is current, which is why HELOCs add risk to the mortgage market and did some additional damage during the Housing Bust and Mortgage Crisis.

HELOCs and mortgages grow for different reasons:

Why HELOC balances are now soaring. If homeowners want to draw cash out of the home’s equity, thereby adding leverage to the home, they have to choose between refinancing the existing 3% mortgage with a larger 6% mortgage; or keeping the 3% mortgage and adding a much smaller HELOC at 8% or 9%. And that math has been tilting in favor of HELOCs for more and more homeowners, and HELOC balances have surged.

Why mortgage balances are still rising though sales of existing homes are in the freezer:

- Growth of the housing stock: buyer finances the purchase of a newly constructed home, and no mortgage gets paid off, and the total outstanding balance increases by the mortgage.

- Reshuffling the existing housing stock: Buyer of an existing home gets a big new mortgage to finance the purchase, while seller had only a small or no mortgage (40% of the homes are owned without mortgage) to pay off. And the total increases by the difference between the new mortgage and the payoff, if any.

- Increasing leverage: Homeowner cash-out refinances an existing mortgage, ending up with a larger mortgage on the same home. And the total increases by the difference of the two.

But mortgage balances are reduced by the principal portion of mortgage payments and other mortgage paydowns and mortgage payoffs; and by foreclosures that cause the remaining mortgage balance to be written off after the sale of the home, which was one of the factors behind the drop in mortgage balances during the Mortgage Crisis.

Measuring the risks of default.

Some definitions: For this debt-to-income ratio – a standard metric to evaluate credit risk – we use “housing debt” that combines all mortgages and HELOCs. For household income, we use “disposable income” (Bureau of Economic Analysis).

Disposable income consists of after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.

But it excludes capital gains, which is where the wealthy make most of their money. Excluded are thereby income from stock-based compensation plans and capital appreciation where billionaires make their billions. And this upper crust of income is excluded here and doesn’t skew the data.

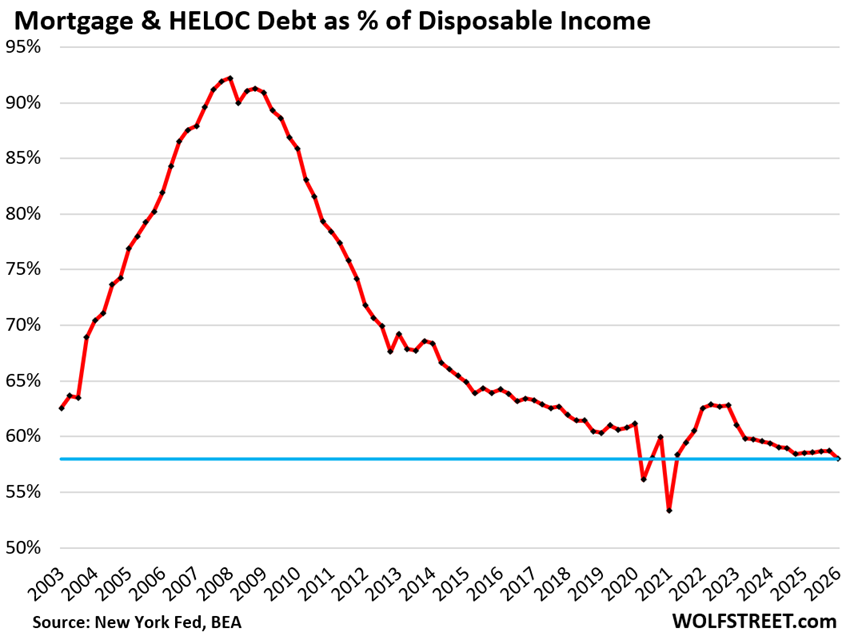

The housing-debt-to-income ratio in Q1 dipped to 58.0%, the third-lowest on record, behind only the two freak quarters Q2 2020 and Q1 2021 when government payments rained down upon households and distorted disposable income out of all proportion.

The chart shows the foundation of the Mortgage Crisis: Consumers were way overleveraged with housing debt because home prices had exploded, and households kept chasing after them with ever bigger mortgages, and they made it worse by taking equity out of their homes via refis and HELOCs, and so housing-debt balances had exploded far beyond the growth of disposable incomes.

The serious delinquency rate started surging in 2007 with a lag of about two years to the debt-to-income ratio which started surging in 2005. The surging debt-to-income ratio was a warning sign – one of many – of things to come.

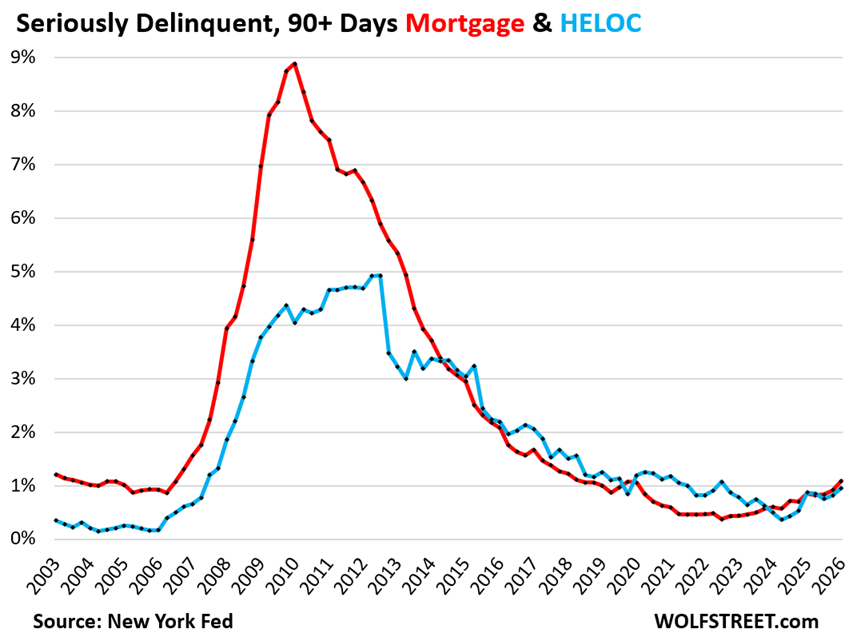

Delinquencies and foreclosures are low, in line with the low debt-to-income ratio.

The 90-plus day delinquency rate for mortgages and HELOCs edged up from the near-0% levels during the pandemic’s forbearance programs, when almost nothing counted as delinquent, but remained low in a two-decade context.

For mortgages, the 90-plus-day delinquency rate in Q1 rose to 1.09% (red in the chart below); for HELOCs it rose to 0.95% (blue). Both are roughly back where they’d been during the Good Times in 2018 and 2019.

The rates = balances of 90-plus days past due divided by total balances outstanding.

Looking forward: what could drive up delinquency rates on a large scale are the two factors that drove up delinquency rates during the Housing Bust:

- Home prices that plunge back to earth, after having exploded, when people, especially mom-and-pop landlords, including accidental landlords, strategically default on a property that would sell for far less than the outstanding mortgage balance;

- An unemployment crisis. But during the Housing Bust, the unemployment crisis started a couple of years after the Housing Bust had begun and was a result of the Financial Crisis that was in part a result of the Housing Bust.

But those two factors are not playing out on a large scale at this point.

On a micro-scale, every default has its own reasons, including a strategic default and unemployment. The legal system and lenders are equipped to deal with those, and they expect a small number of them and have built them into their business models. And so that’s not a problem for the economy until the process takes on a very large scale, as it did last time.

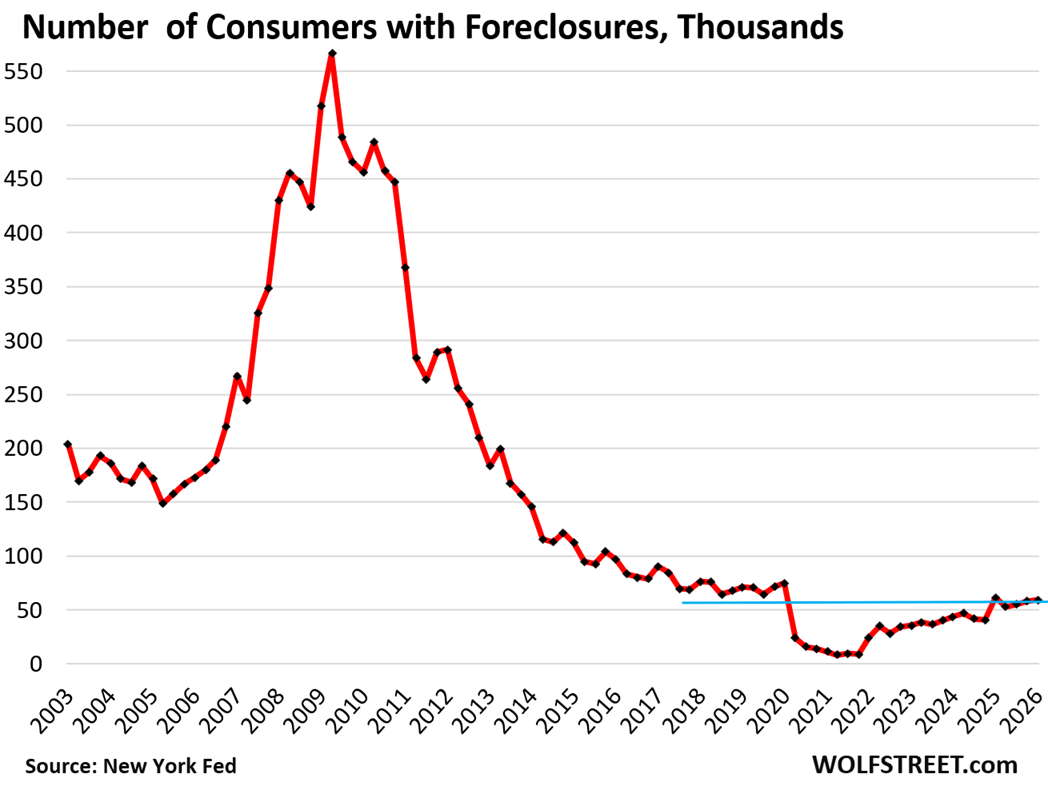

Foreclosures edged up to 59,160 consumers with foreclosures on their credit reports in Q1, but that was down by 4.1% year-over-year.

The number of foreclosures is still below the low points of the Good Times in 2018-2019, and far below those in prior years.

The increase over the past serval years comes off the near-zero levels during the era of mortgage-forbearance and foreclosure bans when foreclosures were essentially impossible.

In normal times – defined here as times without foreclosure bans and government-imposed general mortgage forbearance programs – there will always be some foreclosures.

But the surge of foreclosures that occurred during the Housing Bust won’t happen unless there is a widespread sharp decline of home prices that makes it impossible to pay off the mortgage with the proceeds from the sale of the home.

Reminder: the taxpayer is on the hook this time, not the banks.

The majority of mortgage risks, including nearly all subprime mortgages, have been transferred from banks to taxpayers – that was one of the most fundamental changes coming out of the Financial Crisis.

These mortgages are guaranteed or insured by the Government Sponsored Enterprises (GSEs such as Fannie Mae and Freddie Mac); or by government agencies, such as Ginnie Mae; or the FHA which insures subprime mortgages even with low down payments; by the VA, etc. They account for about 65% of all mortgages outstanding.

The investors are on the hook for the mortgages that didn’t qualify for government backing and that were securitized and sold as “private-label” mortgage-backed securities (MBS) to bond funds and pension funds around the world. They account for about 15% of the total.

The 4,000 banks and over 4,000 credit unions hold only about $2.7 trillion in mortgages and HELOCs (Federal Reserve data), less than 20% of the total. If there is another mortgage meltdown, banks will feel some pain, but it won’t threaten to take down the financial system, like it did last time; it will take down the taxpayer, and the taxpayers doesn’t care, that’s the tragedy.

And in case you missed it: Household Debts, Debt-to-Income Ratio, Serious Delinquencies, Foreclosures, Collections & Bankruptcies in Q1 2026

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“ Mortgage balances barely ticked up, but HELOCs soared.”

This is a sign of two things – homeowners being desperate for cash. It’s also a sign that the housing market is a ticking time b0mb. It’s going to make the housing crisis and housing crash much more severe.

I knew I shouldn’t have put that in the subtitle, because someone who didn’t bother to read the rest of the article, or prior articles, was going to spin a whole new the-consumer-is-collapsing-crisis theory out of it, and sure enough, fist one.

Wolf, serious question here, why the increase in HELO’s? What are people doing with the cash? Investing in the stock market while the house sits?

Now, if I were cash straped with a bunch of rental houses or ‘flippers’ that weren’t working out, if I took out a HELO and then went into foreclosure, I assume the HELO is still a debt on my books? But what happens to that in bankruptsy?

The increase in HELOCs is because the rates available are higher than the existing mortgage on the home. Wolf explained the math at play. People always tap equity to feed their appetite for things. 5 years ago, they did cash-out refi, as the rates were low.

Article too long. Verbage too complex to understand. We are dumber than you :)

A sign of two things: owners have equity, lenders are trying to drum up business.

I have been getting calls from my lender: thanks for being a great client! You can put your home’s equity to work!

The reasons vary from: daddy needs a new toy, to the deferred maintenance (our building is due for a roof), to maybe I’ll get one of those new builds, and expand my rental properties (short/ long term) or start a business.

Really anything one can imagine, as borrowing against your own equity is cheaper/ more accessible than going to the bank. It’s on-demand liquidity once opened (as I understand? Never used one, but I have had a line of credit for a business with a bank).

Using leverage is nothing new. Just look at uncle sam.

I have heloc, but haven’t used dime for 2 years already

currently 8%

just got offer for 5% for 12 months on new draws

I will ONLY use if it’s home run of 30% ROI or MORE

and then I’ll either flip or payoff in 1 year(not many can do that)

to us it’s all about cash flow and VALUE improvement(sweat equity)

I think it’s more that people are choosing to stay put in their current home and do an addition, add another bathroom, etc instead of moving to a new house, losing the 3% mortgage and paying a price 40% higher than it was 5 years ago. A HELOC makes more sense.

Excellent article, Wolf. After reading closely, and the definitions more than once, I am uncertain of exactly what the 58% housing-debt-to-income ratio really means. Per the definitions, “housing debt” combines all mortgages and HELOCs. ($13.19T + 0.446T = $13.64T)

But, is “disposable income” the total income (no cap gains) of ALL households, or just those with mortgages? If it is total income for ALL households, then the declining percentage could mean that fewer households have a mortgage, and a fraction of those who do, have a sub-4% mortgage. It would be interesting to see the graph using disposable income of those households with mortgage+HELOC debt.

It actually doesn’t matter because we’re looking at the aggregate risk in the housing market, not at individual risks. More homeowners without mortgages, and more homeowners with only small remaining mortgages, contribute to the reduction of leverage and risk in the housing market. Existing mortgages with 3% rates contribute to the reduction of risk in the housing market because their payments are relatively small.

I have heloc(wish it was bigger)

current balance $0 – pay $50 year for it

when I use it it will be because ROI will be 30-50%

Wolf, do home equity loans fall under the “mortgage” balances since it essentially becomes a second “mortgage”?

“Mortgage balances” here do not include HELOCs. I then also added them up to get total “housing debt.”

HELOCs are not mortgages but lines of credit secured with a lien on the home. That lien would be junior (2nd lien) to the lien of a mortgage (1st. lien).

@Wolf, I think @Nunya is asking how your analysis treats an actual “Home Equity Loan” (HEL or HELOAN), e.g. a second-lien loan, often with fixed rate and term, rather than a variable-balance, variable-rate, variable-term HELOC?

An HEL or HELOAN is more like a mortgage than a HELOC, which is more like a credit card, though both are secured by the borrower’s home equity.

If the HELOANs are treated as mortgages in this analysis, then some of the increase in mortgage balance outstanding could be from similar demand for equity as HELOCs? But the HELOAN increases from some homeowners would be offset by principal payments made by others…

Second-lien mortgages (not lines of credit) are included in “mortgages.” Like first-lien mortgages, there is a fixed amount outstanding and monthly payments, and borrowers make two payments every month.

But 2nd-lien mortgages are only a small part. They’re not popular. HELOCs provide more flexibility.

1) U have no equity in your house in the first five years. U have no

equity in your multi multis in the first five years. Either their tenants

or Uncle Sam will pay.

2) Personal spending is higher than income. Real wages lurched down.

Gen Z and millennials have to pay: mortgages, student loans, car loans,

before food, utilities and gasoline at the pump. No HELOC for them.

They have to pay realized gains after trading bitcoins and selling the

mag 7, bc SPX went vertically up since Mar 30 reaching 7,500.

3) The mag 7 cut payroll, before cutting capex, bc AI is changing too

fast even for them. They have to be re-educated. Gens alpha and Z will

teach them a lesson.

4) Within a decade or two they will inherit what gen X and the boomers

left. The gov will salivate.

Well… that depends. When I bought, I did a 20% down payment. Then one year later put another 50% in on a cash in refi. Currently I have a $375/mo payment and owe about 40k.

Doesn’t really matter what happens to home prices in my market. I don’t care whether they go up or down. A house is just a place to sleep, cook food and store stuff… I could easily pay off the mortgage, but haven’t done so as I have been, (cough) using the funds *elsewhere*…

I suspect I’m not alone.

The tipping point will be when folks pay for gas to get to work and food to eat before making their mortgage payments.

Nothing new to report here.

Heloc’s will be the only game in town, and not a bad idea, for the next decade or until the housing market collapses like it did in 2007/2008. Like Wolf said in his article, no one wants to swap a 3% mortgage for a 7% one just to get some cash to buy a car or do a major home improvement. No one wants to move under these conditions unless they have to. The market is frozen. Realtors are SOL (S$it out of luck) to get listings in this market.

I think another financial instrument is brewing – Home Equity Agreement (HEA). I see advertisements for these. It is enticing for the homeowner that wants to withdraw equity, but it doesn’t increase their monthly payment. Seems like a bad deal for the homeowner to me.

Here is what it is as described by Redfin:

“A home equity agreement or HEA – sometimes called a home equity sharing agreement, shared appreciation agreement, or home equity investment – allows you to unlock some of the value in your home without taking on a new loan or monthly payments.

Instead of borrowing money from a bank, an investor gives you a lump-sum cash payment today in exchange for a share of your home’s future value. You remain the homeowner and continue living in the property, but an investor places a lien or stake in your home’s future appreciation.

The agreement usually ends when you sell your home, refinance, or reach the end of a fixed term (often 10 to 30 years). At that time, you repay the investor based on your home’s market value at that point. Basically, an HEA lets you unlock cash today in exchange for giving up a portion of your home’s future gains.”

I don’t know if its a good idea to use a HELOC to buy a car. Just get a car loan with the car as the collateral and leave the house out of it. If you have any other way of borrowing, wouldn’t you use that first before choosing a heloc? I’ve never used one; are there tax advantages or something; I probably need to RRTGDFA. (Re-Read the GDFA)

The housing collapse is always 3-5 years away.

I read this late last night but one comment I have is this:

In my area HELOCS have mainly been adjustable. Looking at headlines and bond action today,HELOCs for some folks just might become a nuisance.

My 30 yr refi churning along at 2.5% is adjustable but caps at 6.5% in another 3.5 years so manageable.

Wondering how the mortgage rates going up will affect whether the fed starts to actively sell MBS, and what that selling does to the mortgage rates. I’m secretly hoping the plan is to get housing prices down to affordable levels and maybe force some investors out of the housing market.

Ok, not force them out, they are free to stay invested. You only lose money when you sell after all. But underwater for 5 years isn’t a great investment and wont attract new money to the trade.

Inflation is going to make a big poopy mess out of all this.

at least you’ll have WORTHLESS fiat $dollars to pay for it

Inflation works for personal debt too!

I am one of those who still has student debt (quite old too!). I don’t even remember the balance. I could easily pay it off, but the interest rate is literally less than 1%!

My wife has student debt, more recent, from her masters’ degree. The over 5% rate means that we’ve put more effort into reducing that.

Same can be done with a HELOC. Adjustable rates can impede the strategy, however if you can invest the money and make a better rate of return than the interest: Winning!

“and the taxpayers doesn’t care, that’s the tragedy.”

I believe some taxpayers care,tis just get out of the way of the hit as best as possible is all we can do.

30-year Treasury yield tops 5.1%…

Theee-year Trading range not broken … yet.

10 year not close to breakout yet.

Market is murmuring but not crying out yet.

MW: Dow, S&P 500 and Nasdaq set to tumble, gold and silver dive, as 10-year Treasury yield breaks above 4.5%; oil prices jump after Trump-XI meeting

Those HELOCs are going to be painful when housing prices come back down to earth (somewhere between 60-80% drop, or more).

What I’d suspect those HELOCs are is a representation: homeowners who own their homes outright that want to monetize them, but can’t sell them because they can’t admit to themselves that 2022 pricing was inflated to begin with and is not here to stay.

I do still think you can have a debt/financial crisis because of this. HELOCs are not guaranteed like mortgages are, meaning that if defaults happen, banks are on the hook for them. Furthermore HELOCs wouldn’t be given out if banks were convinced that home prices would fall, so banks’ lending is vulnerable.

I don’t know if this data exists, but it would be more than a little interesting to see how many of those HELOCs are borrowed by those who don’t have a mortgage. I suspect most of them fit in this category. If so, then any hits to stocks, Medicare, or Social Security are going to make the housing market nasty for anyone who has an interest in keeping prices up.

This might be the beginning of the end for the housing bubble.

I think maybe a more accurate way to state it is “the voter doesn’t care” because half or more of the voters are not tax payers.

Or homeowner.

If you purchase anything at a licensed business, you are a taxpayer. If you earn any sort of wage or salary, you are a taxpayer. Stop with the horseshit political talking points.

Corporations have taken on debt, that turned to shit. Rather than allow these people (remember, we gave them person rights) to actually go bankrupt and allow real deflation and the bad debt to clear, we transferred it to the public (US government). It continues, unabated.

This is SO TRUE, but the only option we have is to bitch about it. Change will only come when the USA is totally bankrupt, and people worldwide quit taking the US dollar, because they know it’s worthless!

In addition to complaining, people can also vote Libertarian, the only party for a balanced budget.

It’s a transfer, really. Those people may not pay income tax, but they sure do pay sales taxes – which props up local governments. By eliminating their federal tax burden, the money then flows locally.

The biggest tax the “low income” folks pay is the INFLATION tax.

U.S. stocks fall in tech-led selloff as rising Treasury yields and inflation jitters rattle investors

Howdy Youngins. The HELOCs are here Beware… Not really, HELOC loans are fantastic for building wealth. Its what I did and worked very well.

YOU should know how to add and subtract before applying. MOST do not.

What is missing from all this is how these loans are being repackaged and sold to “investors” as collateralized debt obligations. Wall Street and the big banks are at it again folks. This is the moral hazard that was unleashed by NOT prosecuting the perps in 2008 and letting the BAD debt clear, come what may. Private equity is at it again as well and the taxpayer and anyone with a bank account will be on the hook again…

Hedge accordingly,

Howdy WB. YEP, and what we need again is

NO money down home loans

NO income verification loans

Lets go ZIRPing again too.

LOL!

Wanna discuss how distorted the AI capex trade has made “markets”?

I am sure that “this time is different”…

Just that same, we better hedge accordingly.

Your article misses one major structural change since the GFC: foreclosure laws and servicing rules are nothing like they were in 2006–2008. Back then, if you were 90 days delinquent, the bank was legally required to start foreclosure. Today, servicers routinely rewrite, re‑age, and modify loans long before they ever show up as delinquent. That means a huge amount of stress never appears in the data at all.

Because of these post‑crisis rule changes, comparing today’s foreclosure or delinquency numbers to the GFC is impossible — they’re not measuring the same thing anymore. The system now masks early‑stage distress through mods, deferrals, and payment resets, so the headline numbers look calm even when borrowers are struggling underneath.

No, those mortgage protections have now ended. What is different now is that home prices still have not widely collapsed, and in many markets home prices are far higher than most mortgage balances, and in that case, there cannot be many foreclosures because the borrower can sell the home and pay off the mortgage with the proceeds, and walk away with cash.

This is the most fundamental principal you need to wrap your brain around: you need a largescale decline in home prices before foreclosures will begin to surge.

There cannot be any real “distress” in the housing market unless home prices decline a lot across many markets. That’s what all these figures also show.

Someday, home prices might plunge across the US, as they did last time, and that is when you will see a surge in foreclosures. But that has not happened yet. Home prices have plunged in some markets, and it’s in those markets where the foreclosures are happening.

A simple way to put it may be that foreclosures are a symptom, not a cause of price declines.

What tends to lead to price declines is a mismatch between demand and supply. But demand with housing is often driven by the ability of would-be buyers to pay the monthly mortgage payment, where the interest rate and insurance costs are very important.

I think some of the big declines we’re seeing is the tech & white collar layoffs, which are hitting the grinders and the wfh’ers harder than the execs. A lot of the highest valued property is still behaving pretty normally – it’s the condos and starter / mid homes getting some pain.

Not sure what happens long term to unstick the overall market. Interest rates have to go down, wage inflation, and/or prices have to decline either with more supply or sellers reducing asks, maybe from distress or fear. May be housing crisis…but for the reasons laid out I think it will probably rhyme better with the 60s-80s where house prices sort of meander.

Not great for building wealth but unsure we see another collapse. If you held during the bubble that’s your gains. If you bought during the bubble enjoy paying off a leveraged “investment” that will not earn you much.

Foreclosures do play an eventual role in pushing down home prices as those homes are sold by banks into an already distressed market, which can push down home prices further. It’s sort of a self-feeding process. Big price declines lead to foreclosures, and a surge of foreclosure sales can push prices down further, which leads to more foreclosures… But it starts with widespread big price declines.

If the real estate market crashes this time, private credit will be in trouble, not the banks.

The result would end up being similar, just another pathway.

No, private credit has very little of this debt. Taxpayers have most of it. Read the article. I gave you some numbers.

Hi Wolf,

This might be a stupid one but if GSEs hold 65% of the MBS risks compared to private label investors who hold 15% and banks/credit unions holding 20%, if a crash had to happen and the risk has been transferred to taxpayers, isn’t that a good thing?

I mean if the risk is distributed amongst taxpayers, I don’t think an individual taxpayer would feel any pain, right?

Thanks

Yes, that’s the thinking: All taxpayers combined won’t notice that they’re getting ripped off because they’re too busy watching Netflix videos. And that’s precisely how we got to $39 trillion in Treasury debt, which is the problem now.

The other part of the logic, the way it was pitched during the Financial Crisis when these two companies got bailed out by taxpayers, and were taken into government conservatorship, was that if mortgages blow up again, then banks would have to get bailed out all over again, and so to taxpayers, it wouldn’t make any difference anyway, because one way of the other, they would have to bail out the holders of these mortgages.

A lot of sick logic like this was invented during the Financial Crisis, and I’m still angry about it, but OK, life goes on.

Wolf man, I think you may need to do a reappraisal of your ‘everything is A-OK in the housing market and foreclosures are too low to be a concern’ message. I just saw an article on DailyMail saying that 42,430 homes in the U.S. were foreclosed on in April, 2026 (that would be approx 509K homes/year). This number is not as high as the housing bust of 2008-2013, but it is a major red flag suggesting the situation is changing for the worse.

I look forward to your updated article reflecting this new reality, and as always, I will read the #%*@!

RTGDFA.

The number I gave you was a lot higher than that, it was 59,160 🤣 but that’s extremely low in the 2-decade context.

The DailyMail is tabloid that is trying to pollute your brain, and it has succeeded.

This has long been the story in Canada and as long as the market kept rising it worked well for Canadian homeowners. It will be interesting to see how things will change with stagnating or falling home prices in Canada.

One huge advantage the US has had with mortgages is the 30 year fixed rate, where Canadian mortgages generally reset every 3-5 years. My understanding is that HELOC’s are at a variable rate, which Americans may not be as comfortable with if rates were to suddenly rise.

…with respect, Mark….I Would like to change the wording just a bit.

One big advantage home buyers have in the US is a 30yr fixed mortgage (if you choose it). Unfortunately, for the Country/Market, it keeps housing prices propped up far too long as there is no day of reckoning when rates actually do rise. People just stay put as opposed to moving on with a sale which would allow RE prices to adjust to the higher rates. If rates for borrowers actually rise, housing prices will drop. High interest rates produce lower RE prices. Fixed mortgages at low rates keep prices stuck.

Anecdotal warning: having said that prices are still slow in decline on Vancouver Island, (pop approx 900K). This is mainly due to the climate bringing in retirees with equity. While prices our are very slowly in decline, they remain far too high for young buyers. A friend just listed in order to move closer to family and the agent priced it at least 25% too high.

Quick search produced this:

“Approximately 60% of outstanding mortgages in Canada are set to renew by the end of 2026, marking one of the largest renewal waves in decades. According to the Bank of Canada, about 60% of these renewing borrowers (roughly 40% of all outstanding mortgages) are expected to face higher interest rates.

The high concentration of renewals is due to the prevalence of 5-year fixed-rate terms that were initiated during the pandemic-era when interest rates were at historic lows.

Breakdowns for this period include:

The “Renewal Wave”: About 60% of all mortgages are up for renewal between 2025 and 2026, with an especially heavy concentration hitting in 2026.

Rate Shock: Research indicates that around 60% of these renewals face payment increases, as they originated when interest rates were near zero.

Arrears & Delinquencies: Despite the payment shocks, the national mortgage delinquency rate remains low by historical standards. In early 2026, the national 90+ day delinquency rate sat at 0.24%, according to the Canada Mortgage and Housing Corporation, though regional stress has increased in major urban centers like Toronto and Vancouver.

Borrowers navigating this landscape are utilizing strategies like extending their amortization periods or shifting to variable rates to manage the payment jumps.

I wonder how long the handle on the frying pan will be…

Could the low debt to disposable income ratio be skewed by the fact that people are buying homes later in life, when they are higher income earners, and so the young low earners now avoiding or priced out of home ownership drive that ratio further down?

I just read something that Trump ended or changed the FHA foreclosure rules – that previously the federal government would cover up to 1/3 of the payment and then role that payment back into the principal of the loan at 0%. If that’s true, no wonder foreclosures have been super low…. supposedly this change impacts about 250k properties.

There are two things that Trump changed, both of which could ultimately increase foreclosures. But this has nothing to do yet with the foreclosures in Q1, which predate those new policies.

1. The foreclosure protections from the Biden era were ended. And we may see foreclosures rise from that on homes whose value is substantially below the outstanding mortgage amount (if it’s higher, people can just sell it and pay off the mortgage). Those protections affected about 250K homes, as you said, and some of those homes might now head into the foreclosure pipeline.

2. Changed the disclosure rules of mortgage terms which could lead to borrowers taking on mortgages that they ultimately cannot handle, which could lead to more foreclosures years down the road.

If that happens it would increase supply of homes on the market substantially and increase downward pressure on home prices….

Which could in turn result in more intentional defaults.

These things can snowball

Everyone relax. Just fire up those 100 year adjustables, add pick a payments, on the refi’s and wha la everything all better now!

Oh, add interest only payment too! Party must go on!

Today at 9:48 AM CDT

Grace O’Donnell

The 30-year Treasury yield just reached its highest level in almost 20 years

Surging Treasury yields amid a sell-off in global bonds sent the stock market a warning on Friday.

The 30-year Treasury yield (^TYX) rose 10 basis points to reach 5.12%, its highest level since June 2007. The 10-year benchmark yield (^TNX), meanwhile, climbed 11 basis points to 4.57%, its highest level since May 2025. Bond yields and prices move in opposite directions, meaning that when yields rise, prices fall.

Both bonds broke above the key psychological levels of 5% and 4.5%, respectively. As Yahoo Finance’s Jared Blikre has written before, the 5% zone for the so-called long bond represents a danger zone that has tightened financial conditions in the past.

Cboe Indices • USD

Treasury Yield 30 Years (^TYX)

5.13 +0.12 (+2.31%)

At close: 1:59:55 PM CDT

^TYX ^TNX

Advanced Chart

Concerns about rising inflation and hawkish Federal Reserve policy appeared to be behind the move in bonds on Friday.

___

I love the in depth analysis.

“Concerns about rising inflation and hawkish Federal Reserve policy appeared to be behind the move in bonds on Friday.”

This is hype for which “Grace O’Donnell” (or his/her/their AI) should be ashamed.

The 30-year has been above 5% several times since 2022. The intraday range over that period is wider than today’s range. Today’s close is insignificantly above the prior high close, and could easily have been manipulated by a whale interested in seeing “Grace” write such a story.

If the bond market were really worried about current inflation persisting for more than a few months,, the 2-, 3-, 5- and 10-year yields would be much higher than they are.

This “long end only” yield surge feels more like a bond market still rediscovering a healthy normal yield curve after years of inversion.

I wouldn’t brush it off so quickly.

1. compared to the EFFR, the 3-year yield (along with the 2-year yield) broke out massively starting in early March, and that breakout has continued. See chart in the coming article.

2. The 30-year sold at auction on Wednesday with a yield above 5% (5.046%) for the first time since 2007. In the secondary market, it has traded above 5% a few times in recent years, but this was the first time that it sold at auction at over 5% in 18 years. That’s a big thing. Auction yields are manipulated down, not up, by the biggest whale of all, the government, and that’s all they could do, is 5.046%.

I view the 2- and 3-year yield moves as a modest unwind of the prior rate-cut meme, not a “massive” move. Prior to this week I wouldn’t have touched either one for the bond ladder, it was all T-Bills. Now they might be tempting. But it’s not a market in panic over what looks to be a sustained wave of >4% inflation readings – not yet – not like 2022.

The 30-year could still be a bear trap. Not disregarding it – it needs attention – but I feel it’s premature to hype “rate panic” like that poor journalist was doing.

Modest unwind? Bonds are not stocks. Yields are not stock prices. Yields are in relationship to something, such as to the EFFR.

Right, the graph says the 3-year bond is now 0.4% above the EFFR, after running below it for 3 years.

It’s a meaningful change, coming out of inversion, but it could mean 2 things: (1) end to the rate-cut cycle or (2) start of new rate-hike cycle.

It’s normal for the 3-year to be 0.25-1.0% above the EFFR (see 2011-2018), with or without rate hikes.

If we’re in for a rerun of 2021-2022, then the first rate hike would be in 6-9 months. (The 3-year/EFFR spread crossed 0.4% in June 2021, but the Fed didn’t hike until March 2022.)

1) The Gulf States oil export is down 20 mn barrels/day. We control

Malacca and Hormuz straits. Argentina, Brazil, Venezuela, the US

and Canada export more oil, LNG, jet fuel, petrochemicals than ever

before. It’s all about Power.

2) Shi insulted Trump. Thucydides: After beating Persia Athens

suffered from high inflations and multi plagues. Many people died. When Athens was comatose Sparta beat them. During the plagues Athens suffered starvation and sedition as Cuba and Iran today.

3) Thanks JP for saving us from falling apart during the plague. Without u China could beat us and be #1.

So for this to all end well…

rates need to never go up,

inflation needs to calm down,

and home prices need to never drop,

and AI needs to not cause unemployment,

…all to ensure there’s no recession (deflation) and that equity valuations and home prices go up forever.

Am I missing anything? What are the odds?

The way I see it, either the above scenario plays out perfectly or a whole lot of people are in for a whole lot of pain.

Wolf, slightly off topic (maybe) I read on Mortgage News Daily that Fannie and Freddie are now buying MBS to keep mortgage rates down. This seems similar to what the Fed did previously. Have you written any articles on this and is this purchasing of mortgage debt by Fannie and Freddie your read as well? If so this seems like potentially a bad idea.

Fannie and Freddie have been doing this for over a year. They have some cash on their balance sheet, and they can borrow some, and they buy MBS with the proceeds. This does NOT involve money printing — and bloggers out there who claim it’s like QE are idiots.

But it increases the risks for these two companies. And these two companies were doing the same thing in the years before the Financial Crisis, and when MBS blew up, the two companies blew up and were taken over by the government. Now they’re doing the same thing again because a young goon that doesn’t know anything is running these two companies.

What they’re trying to accomplish is marginally reduce the spread between mortgage rates and the 10-year Treasury yield. So the 30-year mortgage rate rose to 6.65% today.

TLDR – Homes are not going to be affordable again for like next 5 years. Supply wont improve much to help the incumbents. Monthly payments are so low due to sub 3% mortgages that most will not end up having to sell their Nth (1st, 2nd or 3rd) home for a realistic price.

I just got an email from Progressive. They wanted me to know they could give me a HELOC. I’ve only ever used them for auto insurance. Have insurance companies always issued loans to policyholders? Seems a little odd

I don’t think Progressive is the underwriter of the HELOC. It sounds like a marketing agreement with a HELOC provider, where Progressive gets paid to send its clients promo materials from third parties, such as the HELOC lender. If you read the small print of the ad, you will likely see the name of the provider.