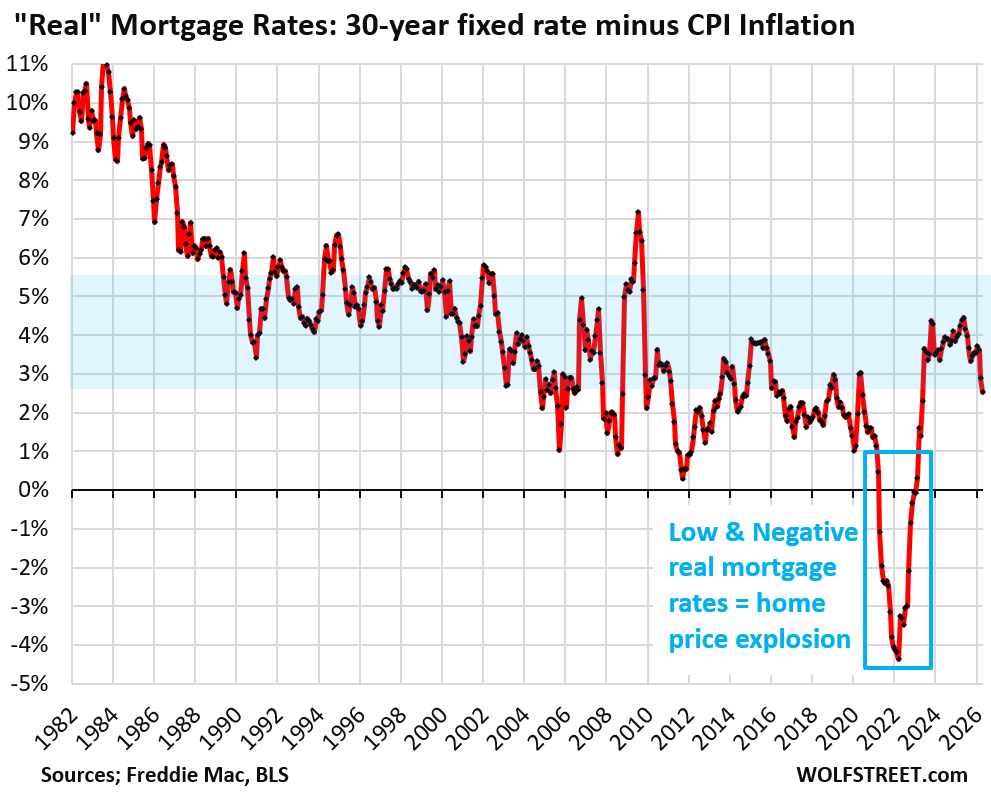

But mortgage rates are not high historically, and “real” mortgage rates, amid resurging inflation, are relatively low.

By Wolf Richter for WOLF STREET.

This spring selling season, which is now wrapping up, has been one heck of a disappointment for real-estate brokers, mortgage lenders, and mortgage brokers, after all the hype it received late last year and early this year. This was going to be the spring that pulls the housing market out of the freezer with below-5% mortgage rates and a flood of buyers unleashing pent-up demand or whatever.

But the opposite happened. Mortgage rates have remained in the historically normal-ish 6.5%-range, give or take a little, as the 10-year Treasury yield has risen amid resurging inflation now approaching 4%, and lots of talk about Fed rate hikes, instead of rate cuts. And home prices in many markets are still too high, after the price explosion from mid-2020 to mid-2022 and don’t make economic sense. And so here we go again…

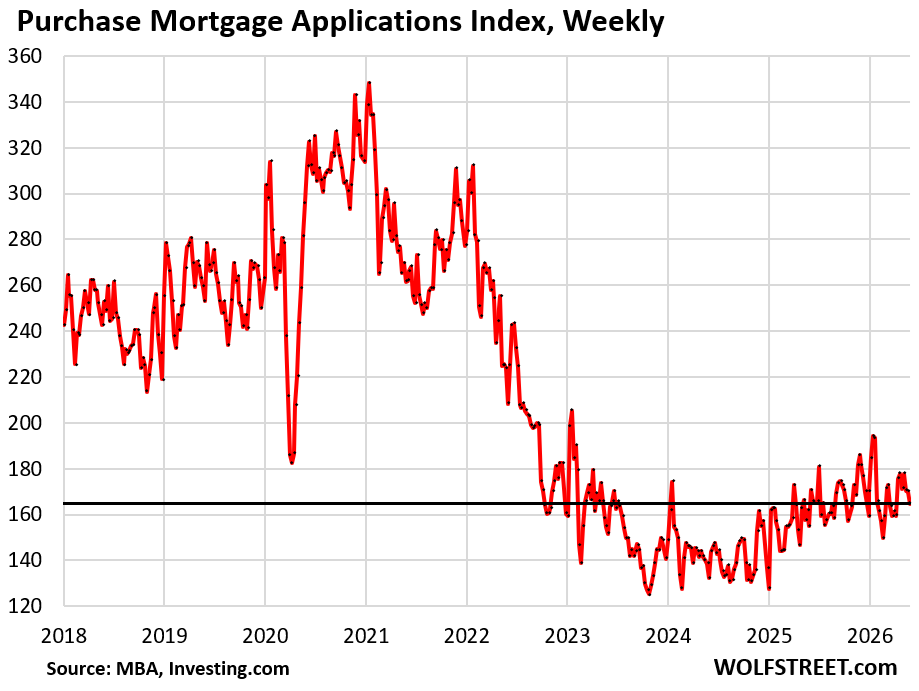

Mortgage applications to purchase a home – a forward-looking indicator of home sales – fell further in the current survey week, the third week in a row of declines. It has been wobbling along near rock-bottom levels, down by 35% from the same week in 2019, according to data by the Mortgage Bankers Association today. The market is now in the fourth year of collapsed mortgage applications.

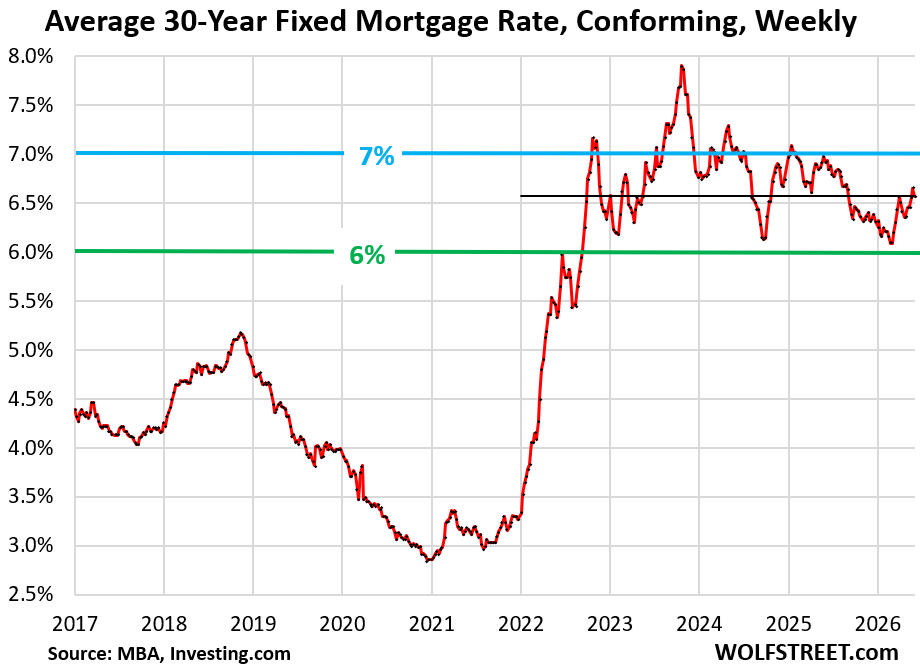

The average weekly mortgage rate for conforming 30-year fixed mortgages eased a little to 6.57% in the current reporting week, from the prior week (6.65%), which had been the highest in nearly a year, according to the MBA today.

This measure of the average 30-year fixed mortgage rate has been in the 6-7% range, except for some breakouts to the upside, since September 2022. This is not high.

With inflation currently at 3.8%, the “real” 30-year fixed mortgage rate (mortgage rate minus inflation rate) is only at about 2.8%, which is relatively low compared to the periods before 2009, before the Fed’s QE began forcing down long-term interest rates.

Between 2009 and 2022, the Fed bought trillions of dollars of securities, including mortgage-backed securities (MBS), with newly created money, which repressed mortgage rates below 3% during the pandemic era mega-QE.

But this massive amount of reckless money printing contributed to the worst inflation in 40 years. By 2021 and early 2022, with mortgage rates below 3% and inflation heading toward 9%, “real” mortgage rates (mortgage rate minus inflation rate) fell deeply into the negative. At the end of 2021 and in January 2022, “real” mortgage rates were -4%, better than free money, and when money is free, price doesn’t matter, and home prices exploded – and are now too high. We can thank the Fed for that.

And that inflation, which has refused to go back into the bottle, is now resurging again.

Also take a look at “real” mortgage rates in 2004 and 2025 (chart below). The Greenspan Fed pushed its policy rates down too far, for too long, as a result of the 2001 recession, dragging mortgage rates below 6% by early 2003, at the time the lowest in Freddie Mac’s data going back to 1971, and inflation resurged.

These below 6% mortgage rates, along with resurging inflation caused “real” mortgage rates to fall below 3%, and as low as 1%, which triggered what would become Housing Bubble 1, which then imploded spectacularly.

Low mortgage rates lead to high home prices, and affordability collapses as insurance, property taxes, HOA fees, and other expenses surge with home prices. Too-low mortgage rates have turned out to be very costly.

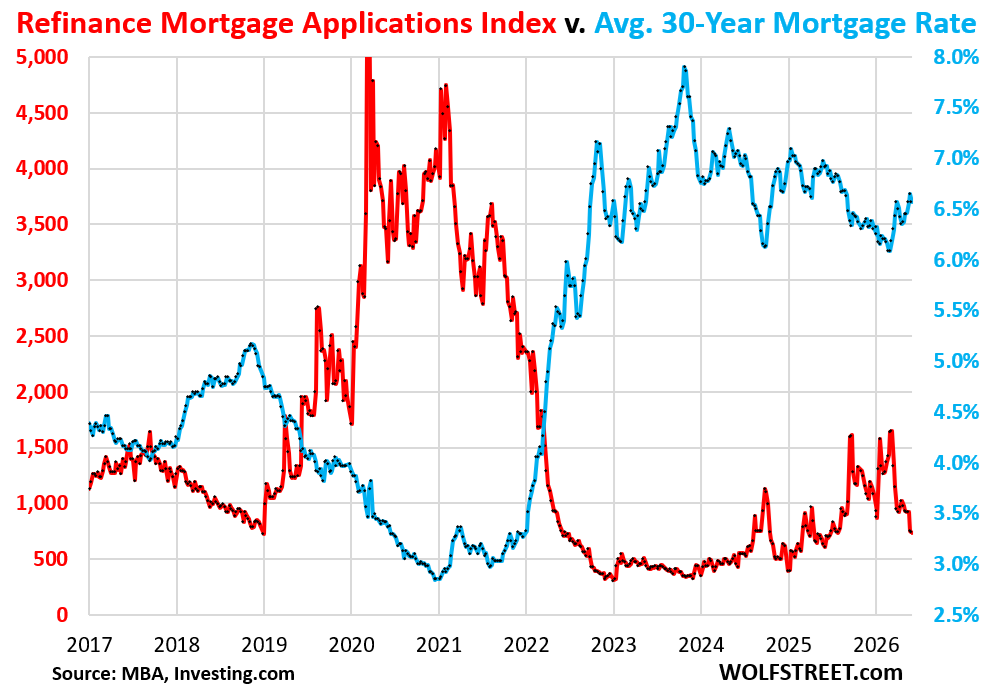

Mortgage applications to refinance a home react to changes in mortgage rates: When mortgage rates dip, homeowners – eager to refinance and doing online refi breakeven analyses on a daily basis – pounce. And when mortgage rates rise after that dip, demand dries up again.

Refis have no impact on the housing market per se (though the substantial fees, which are added to the new mortgage balance, have a substantial impact on the income of mortgage lenders and mortgage brokers).

But refis may have a positive impact on consumer spending when they lower the mortgage payments or provide cash that borrowers can spend on other stuff.

Some of the cash-out refi demand has shifted to Home Equity Lines of Credit. Amid higher interest rates, HELOCs may be the less expensive route to go for many homeowners that want to get some cash out of their home, and HELOC balances have surged.

This longer view of mortgage rates (blue) and applications to refinance a mortgage (red) demonstrates the inverse relationship between them:

In case you missed them:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Unless mortage rates drop below 4% or prices substantially drop, expect more of the same paralyzed sales volume.

It is kinda amazing that sales volume didn’t fall *considerably more* once decades of of ZIRP were unZIRP’ed.

ZIRP allowed home prices to double (or more) from 2002 to 2022, during decades when the US/US worker got the crap kicked out of them by China in international competitiveness terms.

Call it artificial reality leading to real foolishness (to go along with artifical intelligence…and real stupidity)

Lower priced homes will be more unaffordable to ordinary Americans when the oil shock hits, interest rates rise due to inflation, and higher food and other prices make consumers have less disposable income. Correction incoming.

Higher priced, luxury homes will also face some issues if AI job losses, lower demand from consumers due to oil shock hurts employers, higher interest rates, and limited populations,in some generations lower demand for them The Strait will NOT reopen unless there is some US retreat, which will not be acceptable to our dear leader. Iran fought an 8 year war and only ended it very reluctanly.

“when the oil shock hits”

it already hit. Did you miss it?

hey Wolf, I didn’t see that oil hit $150

coming soon enough

gotta thank joey the biden though for emptying SPR for us

EXXON and Chevron CEO predict July to Aug spike

$8 gas coming soon enough

and if CONgress passes war powers act I hope President Trump just leaves in 10 minutes and lets everyone figure out how to resolve it

like biden did in Afghanistan

Exxon and Chevron CEOs are NOT “predicting” – they’re “manipulating” people into accepting higher gas prices, but it’s not working, demand destruction has set in, and gas prices have started to decline, which makes sense because the US is a huge gasoline producer, is awash in gasoline and diesel, and is a huge exporter of both, even California, and the price spike was based on pure speculation and price gouging. Gasoline consumption in the US has been declining for years due to more efficient ICE vehicles and growth of EVs, especially in places like California. So what else are refineries going to do with their excess capacity? Export. The folks at Exxon and Chevron are just worried about their bonuses and share prices (both stocks are down from the March highs).

Just wait two months.

When? Is this a AI bot?

Wolf, please correct me on this, but my gut tells me that we’re overall ~30% overvalued on home prices.

Clearly, those sellers that don’t need to sell….aren’t. There will always be death, relocation, divorce, etc., but the rush of sellers willing to lower prices isn’t as great as we’d think (or like).

That said – here in NE Ohio we’re seeing prices accelerate. Scuttlebutt is that a lot of investors are looking at property here because it’s reasonably priced.

The holdout (non)sellers are gradually losing equity. The party’s over, but they don’t realize it.

“please correct me on this, but my gut tells me that we’re overall ~30% overvalued on home prices.”

I’m going to correct you on this: some markets are not “overvalued” in terms of price in relationship to local incomes, or not by a lot. But there are other markets that are massively overvalued, maybe by 100% or more overvalued. A property that is 100% overvalued (double the price of what makes economic sense) would have to drop by 50% to get back to an economically feasible price (for example +100% from $500k to $1M, and -50% back to $500k. In a market where a property is 200% overvalued, the price-drop back to reasonable would have to be -67%. There were some of those markets during Housing Bust 1. We already have some markets with price drops of 25% or more.

We talk about national home prices all the time, even here, and that’s fine in terms of the overall nationwide economy. But at some point, it just doesn’t make a lot of sense. Which is why in my housing coverage, it’s all about local prices, and if I discuss a national price, it’s with lots of references to local markets.

The problem is that people who complain about the $1.5 million shack in one of the most expensive cities in the US don’t want to move to Ohio, Missouri, or Oklahoma, where they could buy something decent for 80% off. That’s one of the reasons why expensive markets remain so expensive. If they just emptied out because people left, and no one moved in, like in the Rust Belt or Tulsa at the time, the prices would collapse and stay at collapsed levels for decades – see single-family prices in Detroit. But I totally get that: people want to live where they want to live, not where it’s cheap to live.

based on incomes, housing prices are 30% to high(maybe more)

we’re still living in 4% mortgage pricing arena

So true on the people not wanting to move away but complain about high prices.

Funny story I purchased a junk home in Detroit way back when on a whim from a friend that saw a photo in the home ad that had an old mustang sitting in the garage.

Thanks, Wolf. Good clarification.

Somewhat along these lines (how home prices can go down and actually stay down for quite a while)…housing is a bit unique in supply/demand terms because it is so very, very costly to build/buy (in relation to every other broad-based consumer product).

Almost every other consumer bought product (cars are a bit of an exception but still nowhere in the same league as housing) is much, much, much less costly (to produce/buy) – so supply and demand tends to respond fairly quickly/with sensitivity.

Because there is less money at risk for the decisionmaker (producers *and* consumers).

But a decision to *build* a new housing unit is *costly* (even if end-buyer prices from the last 20 years of ZIRP were phoney-baloney inflated) – so true new supply is evaluated very, very cautiously (especially after Bubble 1).

It may not look like it when new builds go from 500k nationally to 1 million to 1 million plus…but that growth has taken years and years and years. And those numbers could have been doubled and/or greatly compressed in time.

So that accounts for the long lags in supply -> high build costs = higher risk = more caution among housing producers.

Building a house just ain’t like letting the mass production machine produce another 10k incremental units of a widget. (And…the mass production machine is a sunk cost anyway).

On the flip side (demand), contemplate just how fast (and how ugly) housing *demand/prices* can get in a negative growth locale.

With rare-ish exceptions – most buyers have little/no desire/ability to “own” (er, incrementally…with a big ass mortgage) a *second* home.

So if local population actually goes *down* by much…that marginal house may be worth much, much less than supposed – since 85%-90% of potential buyers…are just not interested/capable of acquiring that very high dollar purchase. Landlords/speculators maybe…but that ain’t 85% to 90% of the entire population.

So if a locale with 100k houses and 250k population, loses 12.5k in population (aging, migration, employment dislocations, etc.) that means 5k homes might come on the market – that’s a lot for locally-focused speculators/landlords to absorb without *big* declines in prices (to offset the high dollar risks).

This may be one (unspoken) reason why local governments tend to slow walk new housing supply developments (via bureaucratic hurdles of multiple stripes) and have been amazingly tolerant/positive about illegal immigation (which would otherwise seem to impose a ton of incremental costs on local authorities).

Basically, local governments live in a sort of silent, mortal fear of dramatic home price declines…so err on the side of inflationary errors (excessive strangulation of supply, excessive promotion of demand),

I’m getting ready to sell my house and buy a new house since I relocated. I understand I won’t get what I would have in 2021. And that’s ok. I just want a place to raise my kids.

Homes with reasonable sellers seem to move. Homes where buyers think they are owed a bidding war end up sitting. It’s always the price and for some reason people can’t figure out that it isn’t 2021 anymore.

I think what a lot of home owners miss is housing is often a 1:1 transaction. If you sell when the markets not hot, you’re also buying when the markets not hot – so it’s a wash, otherwise you’d be paying more for that new house

What actually matters is non 1:1 transactions or differences in interest rates.

not if you move from a big house on .5 acre in MD to a small house on 5 acres in TN, reducing property taxes by 78%, and increasing quality of life 1000%.

TN,you forgot to add your state is full…..,look elsewhere!

What an excellent article.

I tried putting myself in the mind of a current buyer and simply would not know what to do with current rates and RE market in conjunction with today’s instability and change? No crystal ball. Darn. Even in the volatile late 70s early 80s the formula was get into a house as soon as you can, pay it off as soon as you can, then plan your stable economic future….and watch it unfold. And the monthly mortgage nut was never higher than comparative rent. Taxes were included with the mortgage. Clearly, today’s house prices have a long way to fall but I don’t see how they can? I’ve been building off and on for 50+ years. Sure, a few major developers are floating some financing solutions to stay operating but the price of everything continues to rise. I just renewed some insurance policies yesterday and could not believe what I am expected to carry for replacement coverage. Then, I compared these replacement prices using modular pre fabs as advertised and it is in the same price ballpark. I buy lumber weekly and it is pricey. Finishing materials are outrageous. Luckily I can buy many materials direct from a mill and plane it up myself which saves tons.

Past articles about major builders being able to offer reductions to buyers are very interesting. But more and more, and I’m retired now, more and more I believe the problem for mortgage financing and/or rent affordability is more of an income inequality issue as opposed to building and development costs. When I bought my first home(s) I was a blue collar guy working for an hourly wage. I saved a down payment, went to the bank with a letter of current employment from my employer, some pay stubs, and was told my my mortgage limit there and then. Age 24. None of that applies any more. Now, it would take two breadwinners and in many markets they would laugh you out the door.

In 1970 I was in grade 10 high school. I had a friend whose dad managed an appliance department at a small department store. It was a decent job, but nothing spectacular. The mom stayed at home, they owned a house, and owned one car. The trajectory on affordability is pretty apparent. I hate to think it could get worse, or stay the same.

Regards

Yet big builders have cut their prices by 30 percent plus from the peaks despite prices of all things going up.

They are still making tons of making after price cuts

It basically means margins were quite high for them

Austin once hot market is down by 3p percent from peak despite price of all things going up and up

In the same way other places would come down in price

I certainly hope something with prices breaks a bit in the next year or two… would love to buy when my fiancée’s student loans are paid off, but at current prices it is downright depressing to think about. In our area there are not many SFHs within a 30-45 min commute in the $500k-$600k range, let alone under. You would think that with a household gross income of $260k in Pennsylvania (fully acknowledge we are very fortunate) we would have our relative pick of the crop, but when near future daycare costs are factored in the picture changes significantly.

My mom sold the house I grew up in in 2021 for $~410k after buying it for $225k in 2001, with the house needing $80k in renovations. Houses in the development (50’s split levels) are going in the $600k-750k range. In 2026, as an engineering manager with a partner in medicine, it would take both of our incomes to afford the house my single, public school teacher mother was able to afford.

It his BLEAK for first time buyers that do not have 20% to put down. It’s no wonder why less people are having kids. Sorry for whining, I am tired.

Check out some of those markets:

Oh Dear, Condo Prices already Dropped by 15% to 33% in 24 Bigger Markets, Some Back to Where They’d Been 20 Years Ago

Prices of Single-Family Homes already Down 10% to 26% in these 15 Bigger Cities: Every Market is Different

Wolf,

I am an avid reader. Here in the Philly metro things seem to be softening a bit with price cuts becoming more common, but as your articles have shown the market here is being fairly resilient price wise in comparison to other markets.

Moving across the country is not really in the cards for us :,)

Of course the homes in your area are unaffordable, it’s due to the run up from people willing to buy homes in your area at any cost. That’s what causes these issues and stupid prices.

Time fixes these issues….

I met a ton of these folks when we were unloading our portfolio of real estate during the 2021 – 2023 craze of fomo buyers. I still laugh at the people who bought our SF home, my old neighbor down the street asks me if I know someone like that who’ll buy their home as they listed and are looking to unload and retire.

Look for opportunities elsewhere if your profession can demand it which it seems it can Engineer + Medicine = anywhere work.

@ Kracow

Theoretically yes, I could move to another role in the company in Alabama. But I am an only child and my parents are aging, plus they live hours away from each other.

It is already going to be difficult, but you have to pay to play around here.

The FED is responsible for destroying the House and Condo markets with artificially low rates. Rates were near zero off and on for over 12 years since 2008. People refinanced at 2.8% in 2020-2021 so they’re trapped in their dwelling because they don’t want to take on a 6.6% mortgage to buy a different home. There is some activity but this is the slowest housing market in decades. Not much sales activity. It’s classic inflation. 12 political appointees are deciding the cost of money in a period of fiscal and monetary madness. Markets are supposed to set the price of borrowing, not political appointees. I’m amazed the 30-year treasury isn’t yielding 10%, because in 30 years, this country will be in a 2nd Great Depression. The first Great depression was largely a debt liquidation that started in 1929 and continued into the 1950s.

With a partner in medicine, you may well find you can avail of a doc loan, i.e., with no mortgage insurance required for as low as 0% down.

If not, shop around and not just for the house. With application rates this low, mortgage sellers are begging for customers and may well work with you on less than 20% down, especially if your credit report is solid with that income level.

It sucks having mortgage+daycare go out the door on day #1 each month, but it is doable.

^^^This housing was at one point affordable for the middle class on one salary.

Statistically looking at median income, I’d be considered upper middle class (also acknowledge I’m fortunate) and housing is still unappealing at these prices.

You can afford more than you think, if you make it your priority.

With a household income less than you currently have, my spouse and I ponied up our entire lifetime savings to pay 20% down, together with a $1M mortgage, to buy a house in 2005. Mortgage was 30Y fixed with same interest rates as then as now. We already had kids, in daycare.

(We weren’t crazy, the mortgage payment was around 25% of our income. Some people went to 40% or 50% and then paid the price. Google “Two Income Trap” to learn why.)

Here are some tips:

(1) You have to make “own the house” your top financial priority. You don’t need to save for retirement or dump spare change into a college savings plan until later in life. What you need to do is beat down that mortgage, so that your monthly payments are building equity rather than paying interest.

(2) Either choose quality, or build sweat equity. In your early years, your budget is going to be tight, that’s how life is. If you want to upgrade your place, best to do it yourself. We chose to buy a well-built, well-maintained house that wouldn’t have any issues for several years. We budgeted a maintenance reserve just in case, then put the unspent maintenance money into paying down the mortgage faster.

(3) Strip your household budget to the bare minimum. Track every expense and minimize it. Daycare is a cost you pay to have a second income, and you take care of the kids, but everything else gets careful scrutiny. No credit card balances that you don’t pay off each month. Live simply, it’s healthier and less stressful too. Basic clothes, cook your own food, brown bag lunch, no fancy cars, no expensive new furniture (finding cool stuff on Craig’s List is more fun anyway), no big vacations for a few years. No fitness clubs – just play with your kids, go hiking, go swimming. (This phase only lasts a few years, because as professionals your income will advance with inflation, and your daycare costs will drop as your kids get bigger, whereas your mortgage payment stays fixed. Mortgage costs can even drop, if rates dip low enough along the way.)

At your income level, a reasonable budget balance would be roughly 25% for taxes, 25% for mortgage, 25% savings (see #5 below) and not more than 25% for monthly living expenses. Daycare is separate from this – that’s a cost you pay to have a second income. Living on $50K/year might seem challenging, but when you’re young and creative it’s actually a fun challenge. Once frugality becomes a friendly habit, you actually feel uncomfortable wasting money on things your teenage self used to consider normal, like soda or fast food.

(4) Don’t bother keeping up with your neighbors, half of them will go bust and have to downsize in the next recession, and you don’t want to join them … among other things, selling-and-moving is a bloody expensive hit to your wealth-building process. Instead, teach your kids what you’re doing and why, and immunize them against wanting things they don’t need. We pointed out retired folks who are still juggling credit card balances and doing cash-out refis to “manage their debt”, stressing constantly about finances and downsizing because they can’t resist paying for stuff they don’t really need… they’ve earned every bit of their current unhappiness. We talked about others, more fortunate to not have debt, who have “more money than brains” – so they blow their earnings on transient pleasures, instead of building lifetime wealth. Would you rather have a week in Hawaii now, or retire 2 months earlier with no stress and complete freedom? Yes, that’s a legit trade for a $10K vacatin.

(5) Stash 6 months’ of after-tax income in a money-market fund. This is the house-maintenance fund, but it also protects you in case of a temporary job loss. We rode out the housing crash, negative equity for a couple of years, and job scares. Things got tight sometimes, but we never, ever skipped that mortgage payment, and we never took on any more debt. Not even for a car, definitely not for anything else. That mortgage was the only debt I ever wanted to have, and I hated having it because it meant we did’t really own our house yet.

You can’t find SFHs in Philadelphia under $600k? I see tons of townhomes in that range on zillow in the city itself and this says the avg is under 250

https://www.zillow.com/home-values/13271/philadelphia-pa/

What’s the disconnect here?

The federal reserve suppressing rates resulted in exploding housing valuation because cheap mortgage money chased limited (for the most part) supply. Inflation has forced government debt sale rates up, which kicked mortagage rates up. Homes sales languish, housing prices down to flat across the country. So why should we complain, the market works.

“The federal reserve suppressing rates resulted in exploding housing valuation because cheap mortgage money chased limited (for the most part) supply”

For more or less 20 years.

The FED bought mortgage securities to lower mortgage rates during COVID, but rates were artificially low since 2008. I think they’re low even now considering what could go wrong. The risks are huge. And the FED over the last 18 years has shown us they’ll do practically anything to make sure we avoid crashes in stocks and housing. During COVID they sent checks to 300 million people and forced rates down to zero again. Mortgage rates were 2.8%. There are no zero rates in capitalism. Capital is valuable and markets should set the rates, not political appointees. The FED ruined the house and condo market.

During COVID, Congress and 2 different Presidents, but not the FED, sent the checks.

When does Beenanke give back his Nobel Prize ? He sure has faded into

the woodwork.

We will know we are in recession if the Fed starts buying MBS again. As a Realtor I tell my Buyers they may want to hold off buying until prices come down a lot. Another possibility is we just limp along till inflation moves up wages enough to make todays prices affordable. one way or another the current monthly payment just doesn’t make sense.

Fannie & Freddie have blown up the housing market. They have put in regulations that have made it impossible to close a Real Estate transaction. About 50% of the Appraisers have quit, including Ms Swamp. No one will be able to get a loan. Trump fired the heads of both agencies but left in the Obama regulations in place which now go into effect. The replacement, Pulte, has left Fannie Mae, to go work at the head of the DNI. He’s left a mess there and left to get away from the disaster which is about to unfold and which he helped create. You are going to see a repeat of 2007 or worse including massive foreclosures.

Specific details constraining new appraisals would be valuable.

My guess, though, is that basically all that is really happening is a marginal reintroduction of reality into a home valuing/buying marketplace that 20 years of ZIRP turned into an artificial reality doomed to unwind with the reintroduction of macroeconomic reality.

Macro imbalance is when home prices double (or more) at the same time US employment distorts/stagnates/erodes – for 20 years.

A good old fashion depression would finally make the consumer live within there means. I still carry the value of a dollar handed down to me from my Dad and Grand Dad.

Pulte hasn’t left. He is still in his old job, but now he also has a second job (he now is one of those infamous “multiple jobholders” that are constantly cited is reason why the labor market is collapsing 🤣), and that second job is “acting” DNI. That’s a temporary gig.

Wolf should do a complete rundown of all the unreported shenanegans at Fannie Mae and Freddie Mac. This includes their volume of purchases of Mortgage back securities (MBS) and offloading of these to investors. Who is buying these? What are the risks? Who gets to eat the losses if they occur? What is the taxpayers liability if any?

Pulte is a criminal. He’ll never be confirmed as the head of Intelligence. Trump destroyed a few Senators who won’t be voting with Trump anymore. Most Republicans in the Senate hate Trump but fear what he can do to their careers. They won’t remove him because that will end their Senate or House careers. The political extortion is shocking. They care more about their seats in the Senate and House than they care about America’s future, which looks pretty grim to me.

Id read about that, what specifically changed?

*hadn’t read about that.

MM

The new regulations introduced by Fannie Mae created an Appraisal form (URAR ver 3.6) that makes it completely unaffordable to work in this profession. It creates 70 pages of needless paperwork plus added legal liability. Trump and Besson promised to remove burdonsome regulations, yet they presided over the implementation of the worst regulations in the history of the housing finance process. Most of these were born in the previous administration but have been carried over and will be implemented in November of 2026. The real estate market will be deader than a door-nail as a result. No one will be able to buy or sell a house using the traditional financing methods. RE Agents will quit, Loan Officers will be out of work. Foreclosures will rise to 2007 levels.

Ouch, sorry to hear that.

If the regulations affect the whole industry, doesn’t that just cause prices to go up?

Can AI be used to accelerate the paperwork?

They are integrating AI into the Appraisal Form which all appraisers will have to start using. They will have to do regression analysis on many of the fields in the form which is now over 70 pages long. Most if not all appraisers will be quitting the profession. Their fees are already not keeping up with inflation and now the workload has tripled. Goodby housing market which is already frozen and has zero chance of recovery. Ms Swamp worked over 35 years in the profession and handed in her resignation a few weeks ago. She did not even get a courtesy call from anyone she worked for. She was terminated by a computer at 3AM in the morning. Fuck Fannie Mae and Freddie Mac

Swamp creature, Can you talk about what Fannie and Freddie are doing to gum up the loan process?

With inflation increasing again are the mortgages with < 4% rates basically back in the negative "real" mortgage rate territory again?

A member of my extended family has recently taken out a mortgage in an EU country. For the first 4 years the interest rate is fixed at 2%; thereafter it will be a floating rate but with no penalty for early overpayments of capital.

I’ve suggested that they pretend they’re paying 6% and put aside the buckshee 4% to use to reduce the debt in four years time if it seems worthwhile.

Bubble #2 isn’t a bubble. Houses will stay high, but inflation will take care of the real value.

Some examples of home prices, and there are plenty of others:

Those are horrifying charts. There are so many bubbles. The crypto bubble is finally cracking….lots of money wasted there in obscene speculation. Stocks are still in a bubble, Gold and Silver in a bubble. Houses and Condos are in a bubble, cracking in some places. But the biggest bubble is total debt in America, along with Federal debt. The Great Depression was largely a debt liquidation that went on for over 20 years. What’s coming will be terrible.

The old “permanently high plateau,” eh?

Yeah, no kidding. History says otherwise – it’s happened before with housing, always a similar build up with different twists on the crackup each time.

I don’t always know exactly what to believe that I glean from the internet in areas of interest that I haven’t worked in or don’t have expertise, but an ex-hedge fund guy i listened to who seemed to have a deeper insider perspective of what’s going on in the stock market now pointed out that some margin requirements for retail investors were eased in April, and claims it’s part of what caused the silly stock market run up from early April through now.

That stock market thang is going to crack big in the coming year IMO – could be next week, could be months from now, but it’s coming. Crypto is finally getting a dose of reality it seems, but its actual price value (ie speculation frenzy outcome) is still WAY down from here. Also IMO.

Jobs and the economy will get hit eventually too.

From what I’ve read, they’ve just off loaded the last tanker from overseas in the US that had pre-war oil prices — the next batches will start reflecting the higher prices. How domestic production will counter that is not something I’ve dug into, though Wolf seems to be saying it’s pretty flush. Interesting times, for sure, not being helped at all by the DC clown show.

The housing price collapse around the GFC was a result of low interest rates and ninja loans sliding into a down turning job and stock market. Lots of selling pressure from job loss, relocation and foreclosures brought prices down.

Todays sellers are not pressured to sell and the job and stock market look not to apply any such pressure anytime soon. So existing homeowners can wait. The question becomes if sellers hold out long enough in this environment does everyone get used to and accept higher prices?

Maybe apples to oranges here but here goes. Government decided to help with child care and those costs subsequently increased. People adapted and deal with the higher childcare cost. Government decided to help with college cost via loans and college costs subsequently increased. People adopted and deal with a higher tuition.

Government helped with mortgage loans and housing prices increased. The question is will people get used to and accept the higher prices of housing?

There was also a “not-insignificant” number of strategic defaults. Once people saw their home go underwater, and saw a better home than the one they were paying for, go for cheap.. they went and bought a newer cheaper home and just gave their old overpriced home back to the bank.

Those folks didn’t face the life events (job, relo, div, etc) they just made a rational business decision.

The house bubble was what caused the GFC.

The “down turning job market” was led by loss of construction and mortgage-industry jobs as housing supply exceeded demand. As prices started to fall, shadow inventory was put in the market causing prices to fall and killing off the entire real estate industry.

The stock market went into decline as it became clear that millions of people were losing their jobs but it didn’t really crash until the papered-over losses in the entire financial sector could no longer be hidden (Lehman). The banksters had shot themselves in the face by lending money they didn’t really have on properties that were no longer worth the mortgage value. They spread the pain to the world by selling bogus mortgage bonds that weren’t worth their ratings, and multiplying the damage by creating synthetic investments based on the performance of the same bad bonds.

But what you really need to understand is that house prices in the leading markets had rolled over 3 years before the GFC. House prices didn’t fall because employment slid or the stock market went down. They went down all by themselves just because of supply and demand. The pain rolled anll over the country eventually but all that writing was there on the wall for everyone to see. California, Florida, Arizona, Vegas. Wolf saw it and wasn’t alone. But we were in the minority.

The writing is on the wall now as well, it’s just a question of time.

We think we’ve been clever by federally guaranteeing the mortgages this time, but that just means the crash will be deeper because unlike in 2008-2099, interest rates aren’t going to go down with the economy. They’ll go up because the only way out of the imminent fiscal crisis is currency devaluation I.e. inflation galore.

“They’ll go up because the only way out of the imminent fiscal crisis is currency devaluation I.e. inflation galore.”

Yes and no. I lost all confidence that the US government would do the right thing by watching the reaction to 2008. Few truly understood the actual implications of their actions then. Over the last two decades its slowly started to filter out by repeated betrayals to others. All they’ve been doing is devaluing since 2008. But like hemmingway said, very slowly and then all at once. I think we are very close to the all at once phase. Inflation after 2020 was a warning. Rest of the world doesn’t want to absorb are endless debt anymore.

If the govt had just let housing prices collapse in 2022 we’d be out of this mess but this gradual trickle up of wages as prices stay flat plan ultimately is financially more dangerous for the following reasons:

1. More and more buyers at these prices

2. Legislatures dependent on these high property taxes

3. False sense of (illiquid) wealth impacting spending and financial decision making

A rapid rise and fall people would have adapted to. Yes some people would have suffered, but non flippers should be buying a property to live in and at 3% mortgages buying at the top was still cheaper than buying at current rates after a pull back.

Now people are used to these prices which is more dangerous

I hear stories of California shacks going for a million dollars. How did they get to and hold those price levels? Why did buyers not strike and wait for prices to come back down to shack level? Will other built out areas with good business bases follow suit and reach higher prices for shacks yet buyers buy them at elevated prices?

If there’s a buyer strike but also a seller strike doesn’t it become a Mexican standoff and the seller wins what time on their side?

Actually, the SHACKS ARE FREE. and what is going for $1,000,000 is a tiny postage size piece of land as values explode to around $5,000,000 per acre even in mediocre areas!

That’s how a currency collapses. That people become accustomed to higher and higher prices.

The other problem I see is that stocks’ valuation is based on profits, which ran up tremendously during COVID. But that also means that during a recession, the profits will drop more dramatically as customers cut back in spending.

And what dry powder will you have left when you’ve been running in the red to the tune of 1.5 ta 2 trillion during the “good times”?

Of course, there is that great tidal wave of baby boomers who are now in the 62-80 year-old range. Housing only holds its value as long as there is someone – anyone – around to buy the McMansion that you built 20 years ago at the peak of the LAST boom.

I saw a stat that 70% of kids who inherit housing from their parents sell them. The number of boomers, the main owners, who will be passing on in the next 20-25 years is pretty massive, so supply will eventually increase this way too.

I imagine a lot of people are waiting for some important IPOs before they start buying.

Since we are talking about collapses, bitcoin enthusiasts will be interested in seeing the price of BTCUSD: 11-1-2021 $64,381; 9-22-2025 $122,032; 6-3-2026 at 8:21 pm EDT $64,181. Looks like timing is everything.

Trying to comprehend house prices in those markets Wolf correctly said overpriced by 100%. If they drop 50% to rational relationship with local income…..are not the same houses there, the total same square feet in the market? Yes, chaos on some home owners, chaos for the lenders losing collateral value and suffering loan losses, may break/ close some banks, chaos for local governments losing valuations and thus tax revenues. Buy the houses are still there. The local stock of shelter is still there.

Now just move to a couple tech stocks whose price up 10 fold . Now what if the entire stock market valuations or price dropped 50% tomorrow. The come, plant, equipment, technology, employees and managers still there. Yes chaos. Yes, individual losers and winners. But companies still there.

Next, for every bond, or debt, there is a debtor and creditor. What if every debt extinguished over night. Chaos, winners and losers, but the houses, and land and commercial facilities, airplanes and all cows still there.

So, besides chaos, and huge paper wealth shift, are not all the people still there? So why does it matter what a house price is or NVIDIA share worth?

Do not chew me out, please explain why these crazy prices matter.

It’s always been a power struggle between significant asset holders and the rest of the population. The economy grows at a real rate of only 0- 2% a year, so it’s largely a zero sum game.

If the average man or woman has to work twice as many hours to afford that house, or that pound of beef, I think that’s pretty important. Overall society is poorer when that happens. It matters.

Things are way distorted, and that causes problems with what individuals are trying to accomplish near term…..

With that said…. I believe people today lack patience…..

I don’t particularly like patience either….

But it is useful in investing and life… and has worked pretty decent for me over the years.

It appears that opportunities will maybe start appearing. Waiting…. Patience…

Maybe !!

At this point in time it’s clear that if you don’t own stocks and other assets you’re never going to catch up as there will not be a crash, or a correction, or any other way for you to catch up. As much as people hope for another 2000 or 2008 the government has learned all the ways to ensure that never happens again.

Yes, see cryptos. OOPS. Bitcoin investors are already down 50% from the high in October.

I should have said real world assets not fairy dust unicorn farts. Those speculators get what they deserve.

They are rapidly increasing the debt to GDP ratio and rapidly increasing the degree of wealth concentration. Neither is sustainable.

They are experts at delaying a crash, not avoiding one.

The government could not prevent stocks from melting down after March 2000. Their attempt to mitigate the fallout caused housing bubble 1.

They could not prevent housing bubble 1, nor the subsequent housing meltdown, stock meltdown, or high unemployment that followed. At the time in 2009, much internet chatter I was reading was either “don’t fight the fed” or “OMG dollar collapse hyperinflation!” Both were wrong.

They could not prevent the housing melt-up that occurred in 2020-22. Do you think the government wanted housing to double in cost? Pardon me if I say I don’t think so.

They could not prevent housing from crashing post 2022, thus far in select markets, as shown by Wolf right here on this site.

Yet somehow, somehow, they will keep all remaining overvalued assets at a permanently high plateau going forward? I don’t think so.

Also, don’t ascribe to malice, that which can be explained by incompetence.

Cash buyer,looking for 20 acre min. with a home….,still on strike.

I did get screwed by a realtor on one place,yet,my life moves along.

Forgive me, but while Fed policy doubtless “contributed” to Covid-era inflation and more than contributed to housing price inflation, there was also a distinct benefit: namely, no depression. and an economy, we were told, which was the envy of the world, which also saw inflation.

And is a period of 9% inflation really all that worse than, say, sustained unemployment and/or mass penury? Would the U.S. have gladly and sensibly traded its post-Covid economy for a lesser one without housing price inflation, in favor of high unemployment and collapse of low end wages collapsed instead of the inflation-adjusted increases American workers saw, however briefly?

Why do you assume a return to 2% inflation would create a depression? The goal was 2% and the Fed failed miserably with 9%, and continues to fail with 3-5% over five years later.

There never was a choice between high inflation and depression. The choice was between panicking or not.