April was another bad dud for spring selling season as supply continued to pile up.

By Wolf Richter for WOLF STREET.

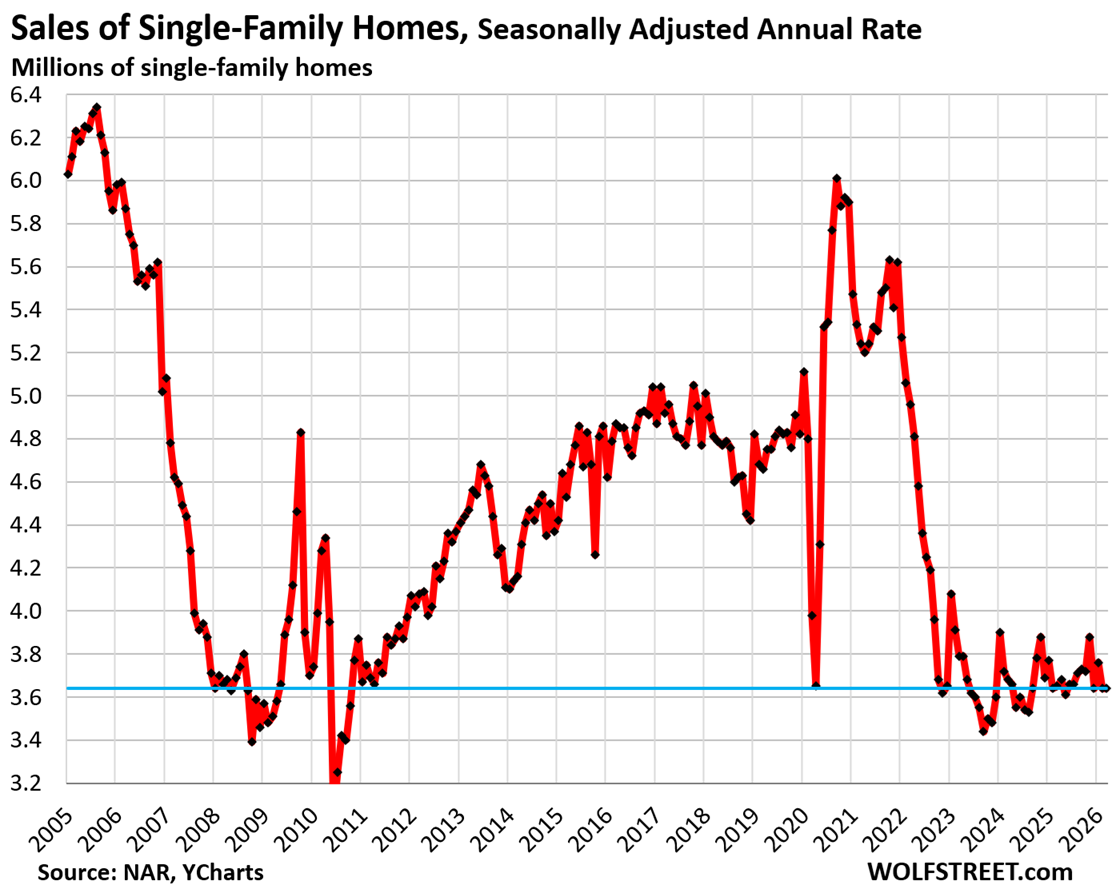

Sales of existing single-family homes that closed in April seasonally adjusted were unchanged from March, at an annual rate of 3.64 million sales, near the very bottom of the deepfreeze range that has existed for the past three-and-a-half years, according to data by the National Association of Realtors today.

Compared to April in (historical data from YCharts):

- 2025: -0.3% (year-over-year)

- 2024: -1.1%

- 2023: -4.0%

- 2022: -26.6%

- 2021: -30.5%

- 2019: -21.9%

- 2015: -19.6%

- 2009: +3.7% (Housing Bust)

- 1996: -7.4%

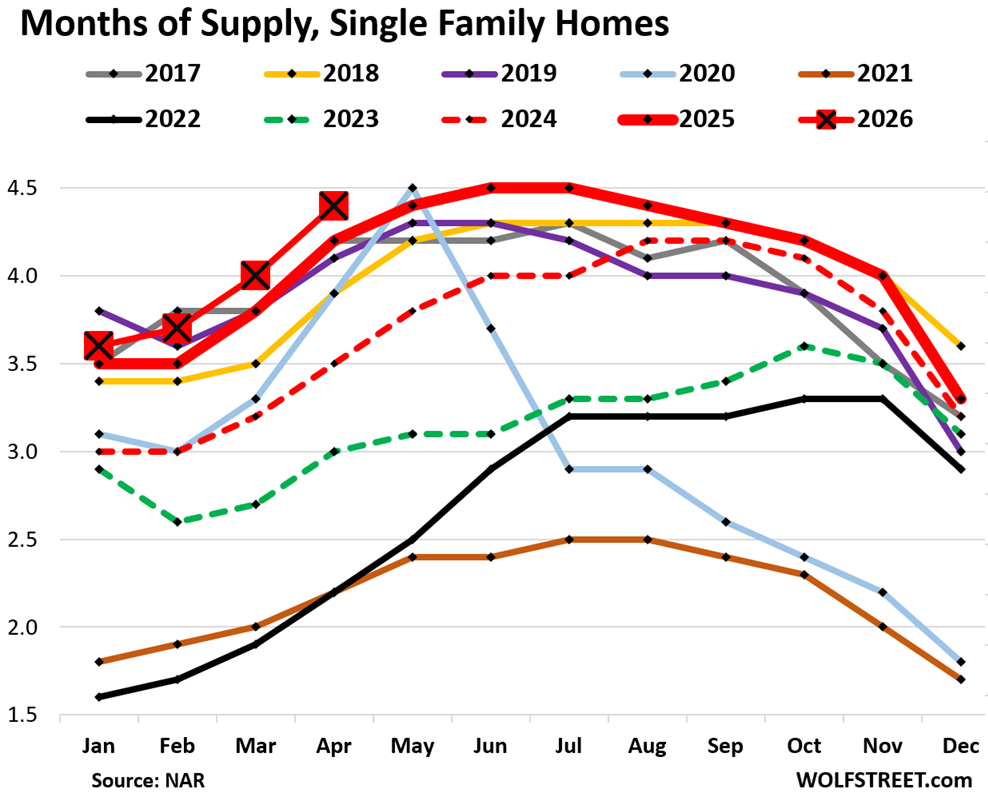

Supply of single-family homes jumped to 4.4 months in April (red line with big red squares in the chart below), the highest supply for April since 2016.

Supply is a function of inventory and sales (demand). Inventory in a vacuum doesn’t matter all that much; what matters is how much inventory there is in relationship to sales, and sales have plunged while inventories have been rising (historical data from YCharts).

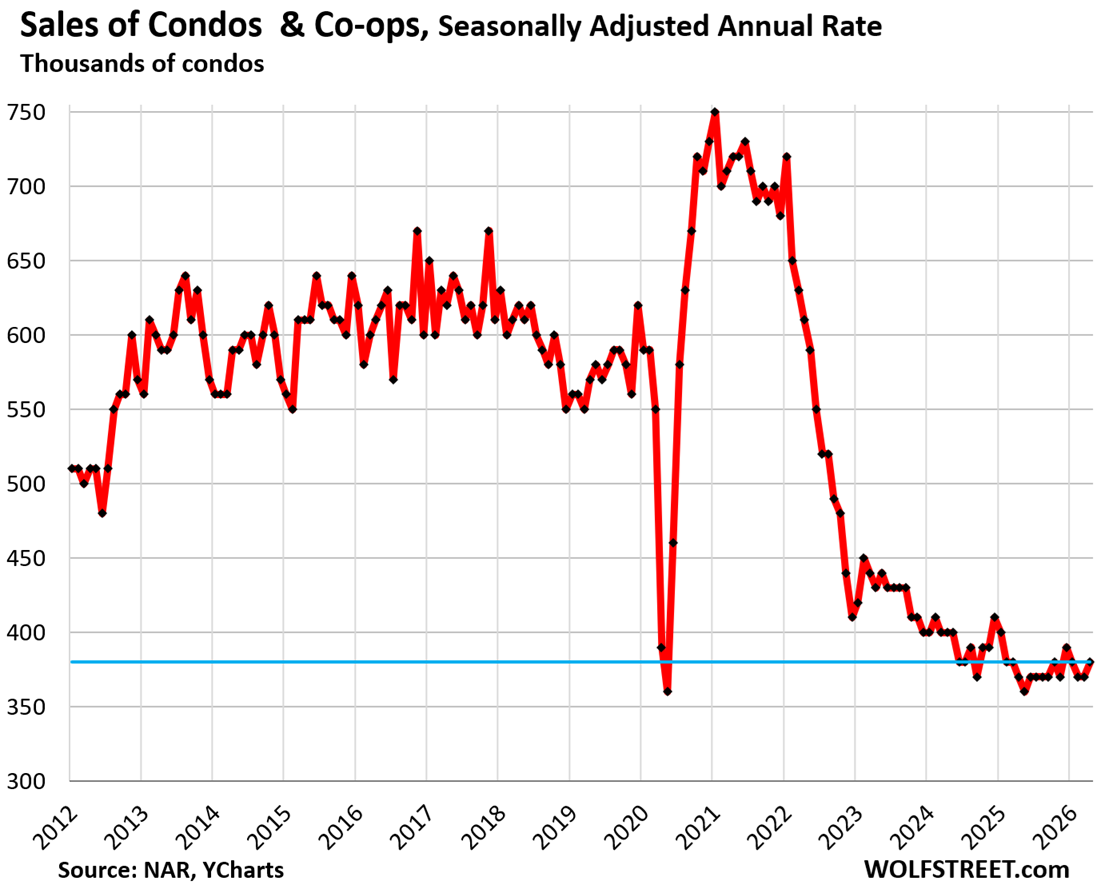

Sales of condos and co-ops ticked up seasonally adjusted in April from March to an annual rate of 380,000, near the very bottom of the data, which go back only to late 2011:

Compared to April in:

- 2025: +2.7% (year-over-year)

- 2021: -47.2%

- 2019: -33.3%

- 2012: -25.5% (first April in the data series)

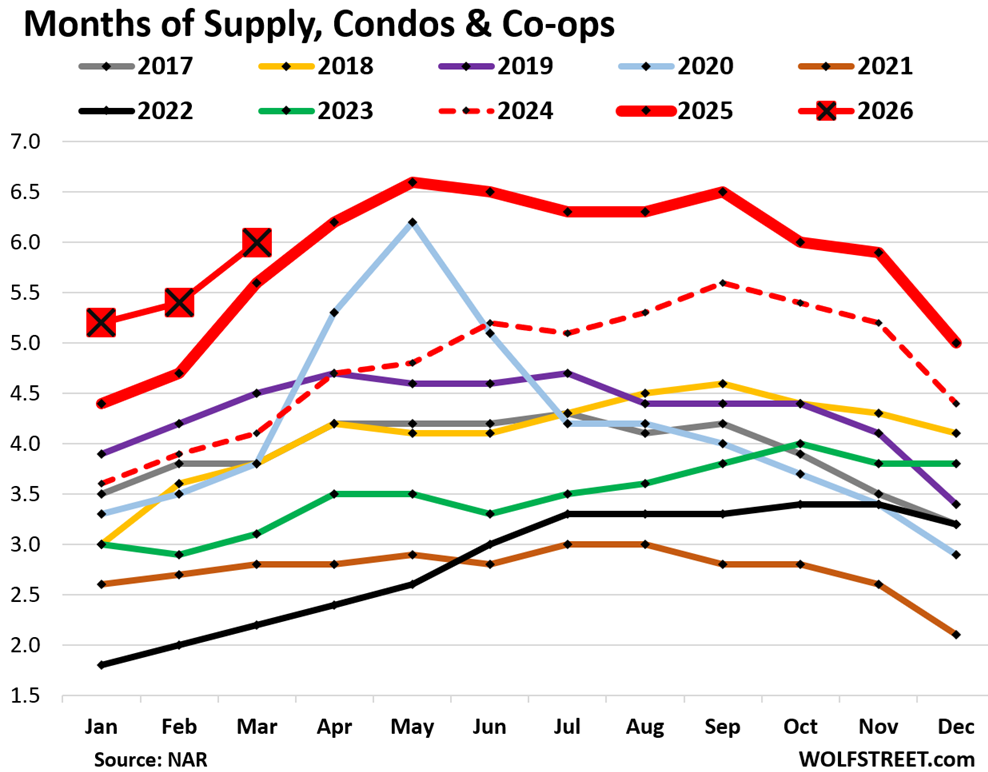

Supply of condos: The NAR has had a data issue with its condo supply figure that started this year. The originally reported figure has been much lower than the prior figures, but then a month later, it gets massively revised higher.

For example, a month ago, NAR reported supply for March as 4.3 months, a total outlier in the figures. Today, NAR revised March supply up to 6.0 months’ supply.

This has been going on for the past few months, with revisions adding close to 2 months each time. So I stopped reporting the original figures because I don’t want to look like a goofball a month later, but only report the revised supply figures.

So March, condo supply was revised up to 6.0 months, the highest for any March since March 2012, the first March in the data series (red line with big red squares in the chart below).

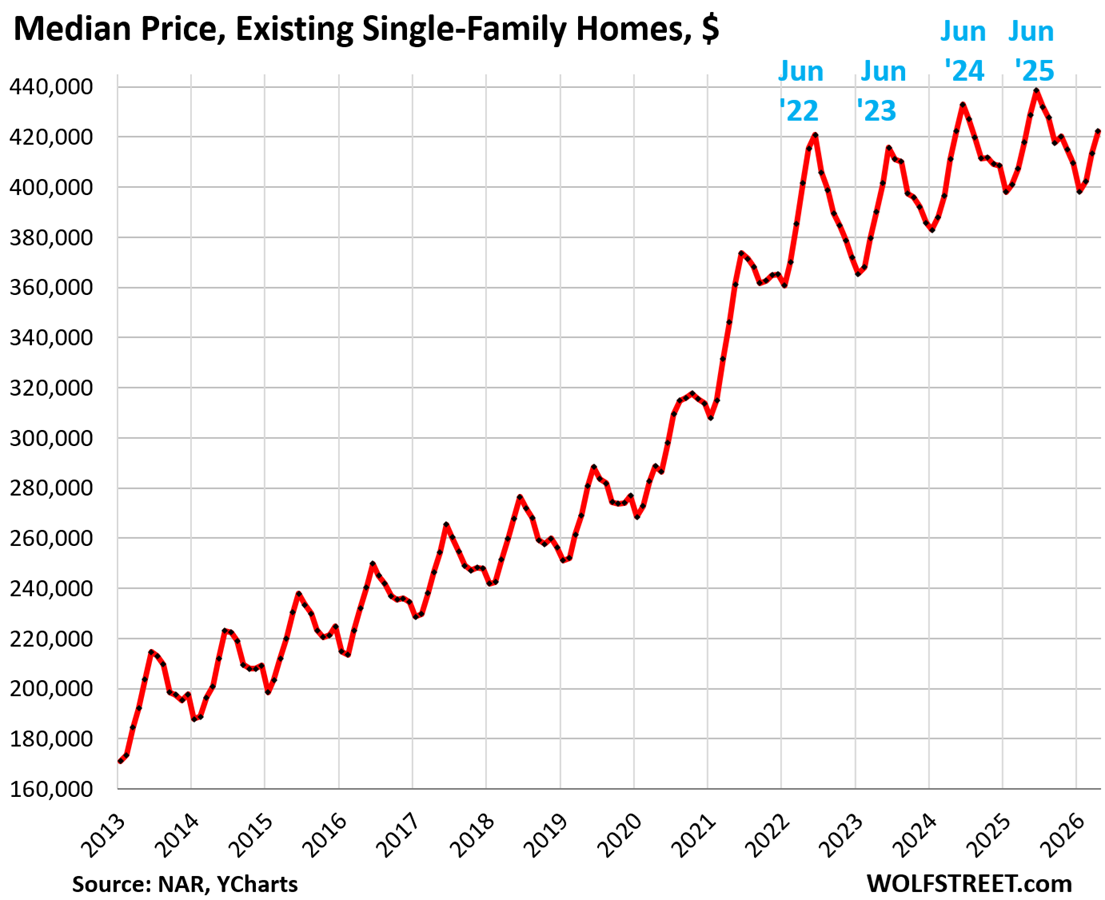

National median price v. local prices.

The national median price of single-family homes inched up year-over-year by 1.0% in April, not seasonally adjusted.

The median price of single-family homes had exploded by 41% from June 2020 through June 2022, from already high prices. Those now too-high prices form the core of the “affordability issues” that are dogging the housing market and are one reason home sales have remained in the deepfreeze.

But the national median price is irrelevant for people buying or selling homes, though they’re an interesting data point from an overall economics perspective. What matters to buyers and sellers are local markets.

Since mid-2022, prices of single-family homes have dropped in some cities, for example:

- Oakland: -25%

- Austin: -24%

- New Orleans: -20%

- Fort Myers: -15%

And in some other cities, prices of single-family homes have continued to rise, for example year-over-year:

- New York City: +5.3%

- Milwaukee: +3.7%

- Chicago: +3.9%

For more, see my city-by-city analysis of home prices in 33 big cities.

The national median price is very seasonal, rising and falling with the shift in inventories and sales, as a larger portion of expensive homes comes on the market and sells every year in the spring, thereby changing the mix of what sold, and shifting the median price up through June. In the second half of the year, the mix reverts, and the median price drops and bottoms out in January.

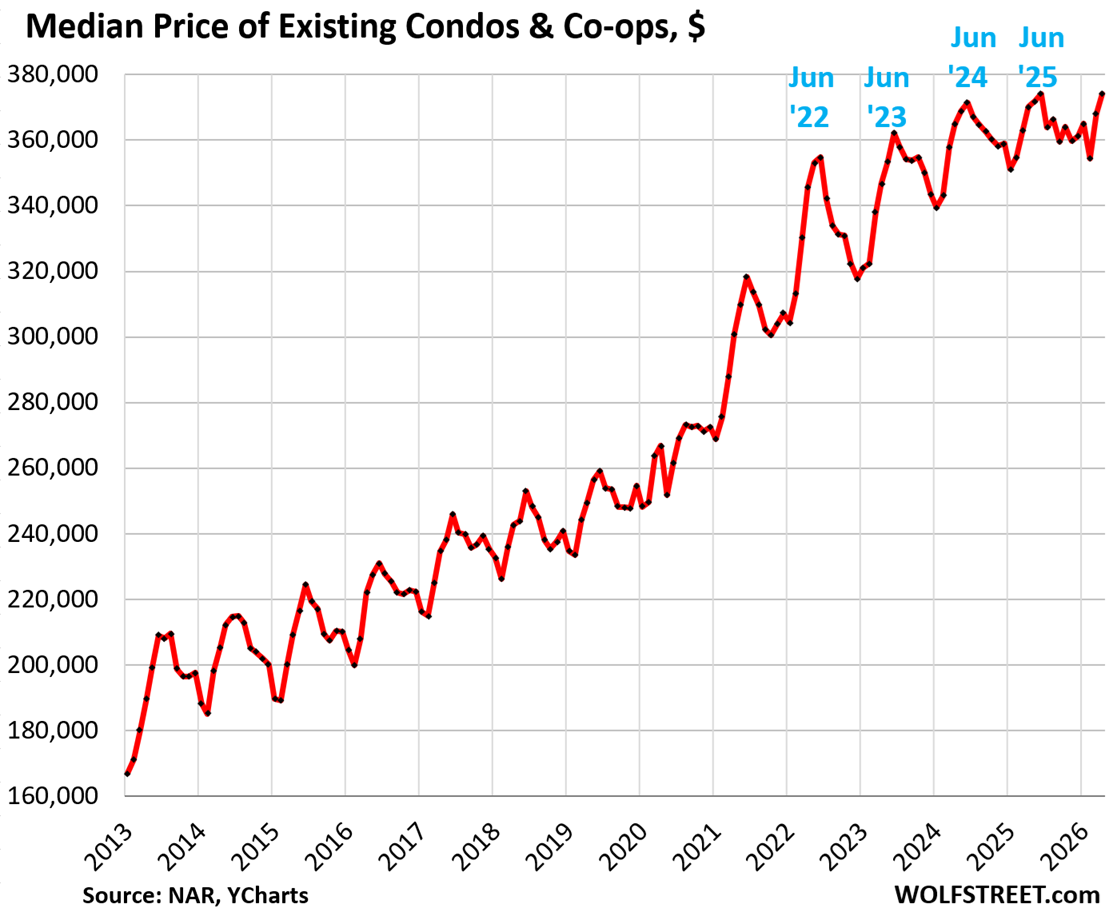

The national median price of condos and co-ops inched up year-over-year by 1.1% in April, not seasonally adjusted.

By local market, condo prices have plunged by 12% to 31% in 31 bigger cities or counties, topped off by:

- Oakland, CA: -31%

- Petersburg, Fl: -28%

- Austin, TX: -26%

- Sarasota County, FL: -24%

- Lee County, FL (Cape Coral, Fort Myers): -23%

In 51 markets, condo and co-op prices dropped by 7% or more, such as in Houston (-13%), Dallas (-11%), Manhattan (-17%). My report on these condo markets is here.

The national median price of condos and co-ops had exploded by 40% mid-2020 and mid-2022,

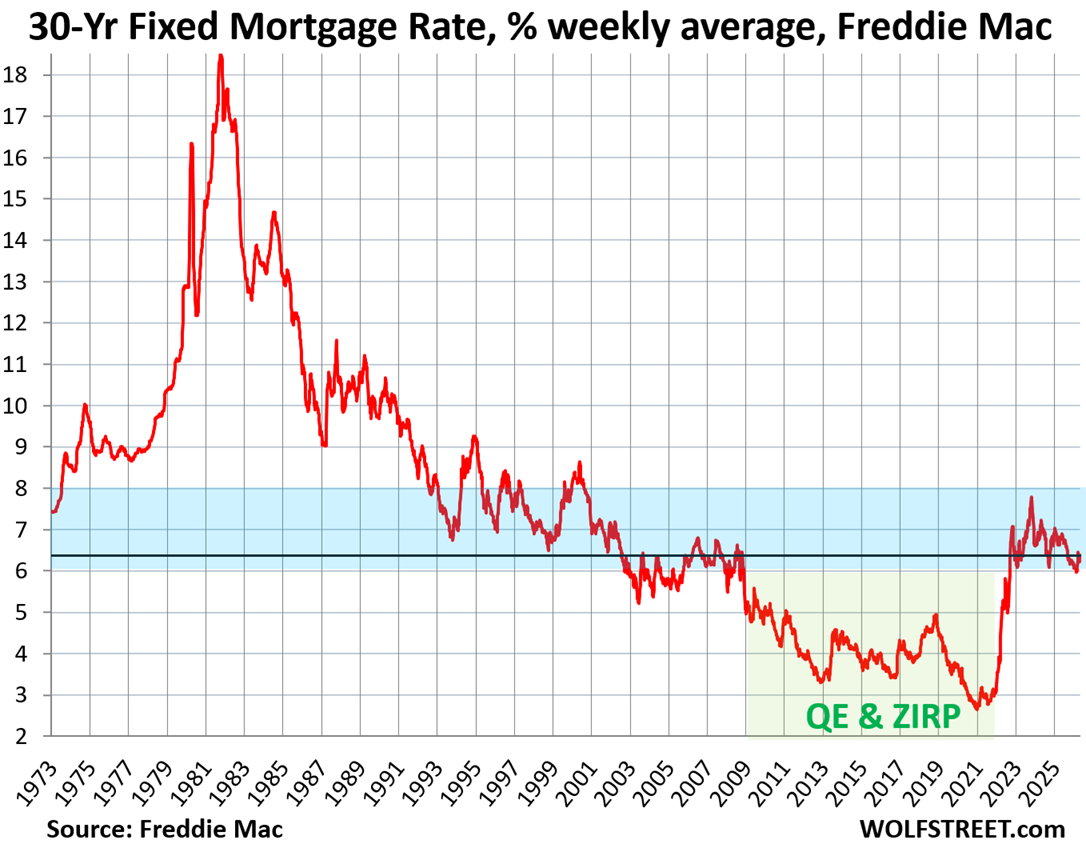

The average 30-year fixed mortgage rate ticked up to 6.37% as of May 7, after dipping barely below 6% for just one week in late February, according to Freddie Mac’s weekly measure of mortgage rates.

Mortgage rates are a product of the bond market. They roughly track the movements of the 10-year Treasury yield, but are higher, and the spread between them varies. The 10-year Treasury yield rose to 4.41% at the moment, and the bond market is on edge.

These mortgage rates are at the low end of the range in the decades before the Fed’s QE, before the Fed bought trillions of dollars of mortgage-backed securities and Treasury securities with the purpose of repressing mortgage rates. Powell’s QE during the pandemic was the primary trigger for the explosion in home prices from mid-2020 to mid-2022 that is now causing the “affordability” issues, and it also helped trigger the worst inflation in 40 years.

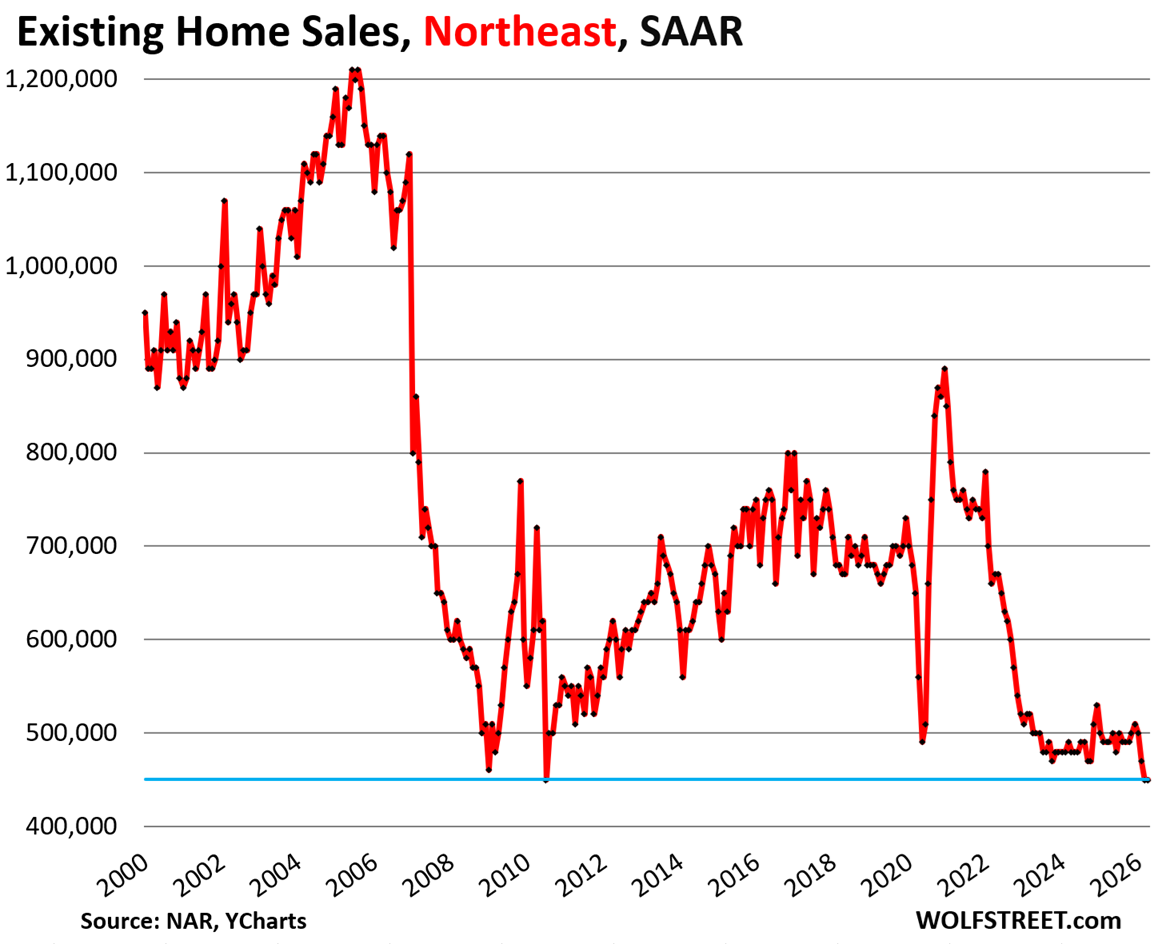

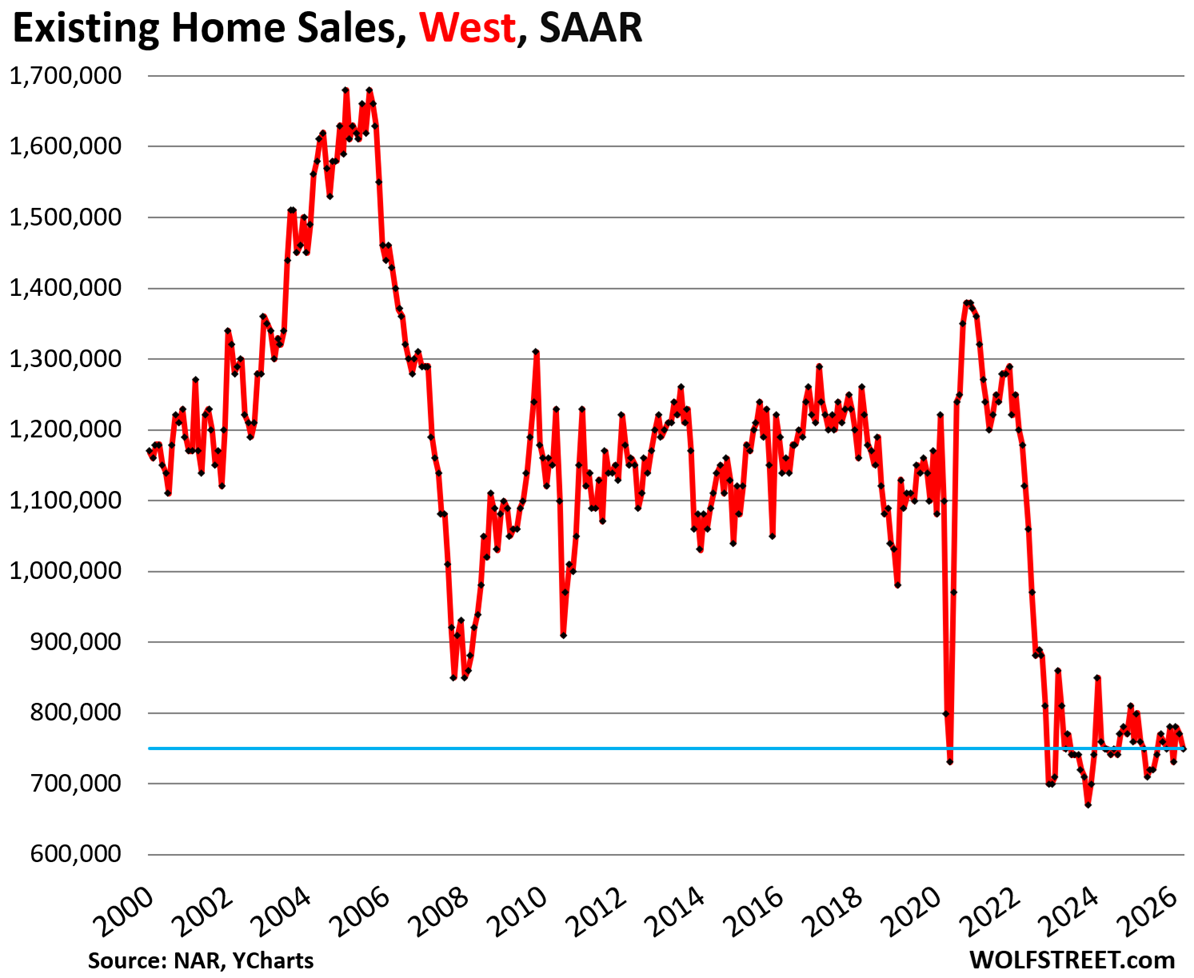

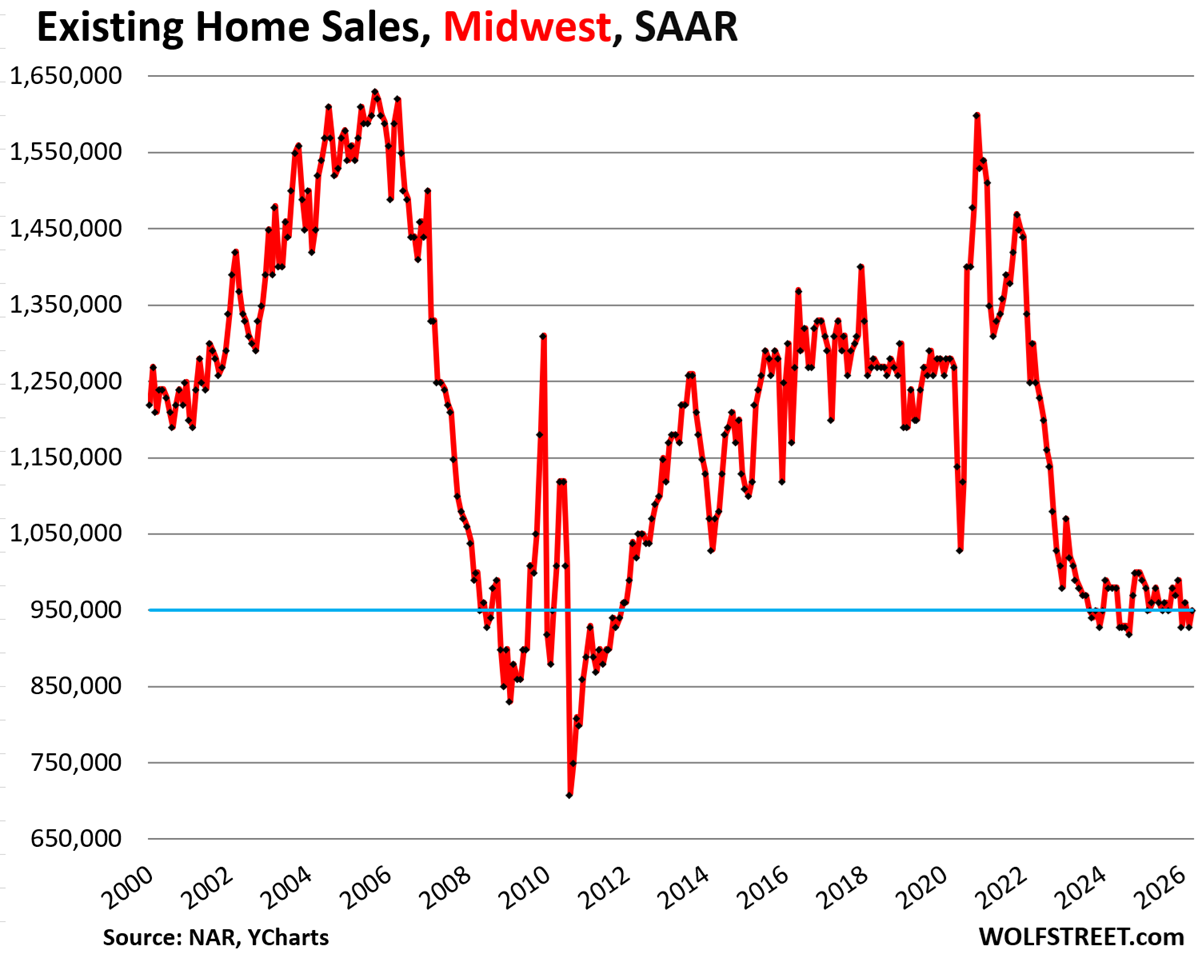

Sales of existing homes of all types by region.

On a month-to-month basis, sales of existing homes (single-family, condos, and co-ops combined) dropped in the West, were unchanged in the Northeast, ticked up a hair in the South, and rose in the Midwest, seasonally adjusted.

The charts below show the seasonally adjusted annual rate of sales (SAAR) in the four Census Regions of the US. A map of the four regions is below the article at the top of the comments.

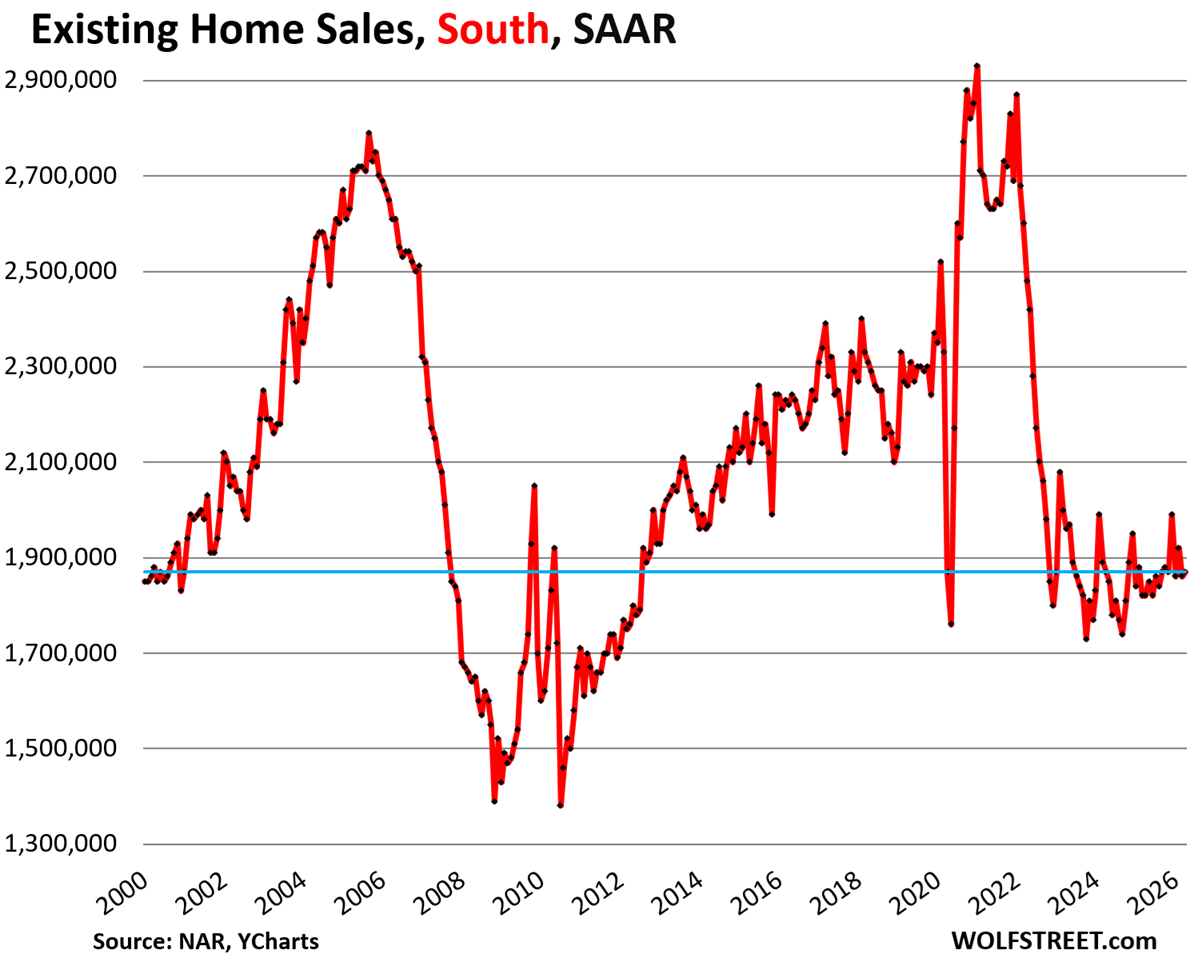

In the South, the seasonally adjusted annual rate of sales ticked up by 0.5% in April from March, to 1.87 million homes.

Compared to April in:

- 2025: +2.7% (year-over-year)

- 2024: 0%

- 2023: -4.6%

- 2022: -24.6%

- 2019: -17.3%

- 2018: -19.2%

In the Northeast, the seasonally adjusted annual rate of sales in April remained at 450,000, unchanged from March at the record low level of sales in NAR’s data, which goes back to 1999, after two plunges in February from January.

Compared to April in:

- 2025: -8.2% (year-over-year)

- 2024: -6.3%

- 2023: -10.0%

- 2022: -32.8%

- 2019: -31.8%

- 2018: -32.8%

In the West, the seasonally adjusted annual rate of sales fell by 2.6% in April from March, to 750,000 homes.

Compared to April in:

- 2025: 0% (year-over-year)

- 2024: 0%

- 2023: 0%

- 2022: -33.0%

- 2019: -32.4%

- 2018: -36.4%

In the Midwest, the seasonally adjusted annual rate of sales rose by 2.2% in April from March, to 950,000 homes.

Compared to April in:

- 2025: -1.0% (year-over-year)

- 2024: -3.1%

- 2023: -5.9%

- 2022: -26.9%

- 2019: -20.8%

- 2018: -25.8%

In case you missed it: Housing Market’s Crucial “Spring Selling Season” Is in Tatters

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Looks good, can only go up with inflation

Fed helicopter money destroyed the market, it is that simple, there is no tools to fix it, nothing is free, mistakes have a price, and the price is housing market destruction.

Housing market destruction would be the best case scenario at this point. The other option is housing market stagnation and prolonging the affordability crisis, which the fed seems hellbent on pursuing.

Here is a map of the four Census regions of the US:

There ‘ain’t no more jobs’ to support SFH on a mass scale anymore, let alone beach condo’s. You have downsizers from huge homes moving into luxury apartments, and then kids at 30 living at home looking for their first real jobs. The Apartments being made today themselves tell this tale.

This is also known as a declining living standard. And it’s very likely just at the start. Maybe I’m wrong.

You’re not wrong, but there is the upper arm of the K shaped economy that is buying new real estate, new cars, new boats, new fashion, iphone whatever they’re on now, etc. The lower arm fights over their worn out scraps of old houses, used luxury cars with 200k miles, and declining neighborhoods.

@SomeGuy when you wrote “kids at 30 living at home looking for their first real jobs.” It reminded me that I seem to be the only guy that thinks it is a bad idea for a kid to never have a “real job” until they get a grad degree (when they are pushing 30 like almost every kid my kids grew up with on the SF Peninsula). I started working as a kid (I worked six days a week all through High School) but I didn’t start playing golf until I was 30 and I struggle to keep my handicap under 20. I started my kids working when they were super young “and” I also started them playing golf when they were young and they are good at “both” working and golf (both have low dingle digit handicaps).

Flat prices for another 6-8 years around that June 2022 price peak will do wonders for housing affordability and maybe let tiund people in the door again. Maybe the Fed will have sold off their last MBS by then too. 25+ years of a broken housing market due to Fed meddling.

What flat prices?

House sold near the GF’s condo in January 2026 for $1,050,000 and is back on the market for $1,600,000.

I’m trying to escape the insanity that is California and I just looked at a property in MO that was $275K in 2023 and it’s on the market……..for $480K

Where’s the flat prices? Everywhere I look RE has doubled since 2020.

“sold near the GF’s condo in January 2026 for $1,050,000 and is back on the market for $1,600,000”

Someone is hallucinating. “On the market” means zero about the market or prices, but reveals the sellers state of mind.

True…and the fact that it remains on the market (and for how long) reveals *buyers’* state of mind/ability to pay (under anything other than ZIRP).

That’s why tracking *closed* sales over time matters so much (the whole pt of your chart).

The general media, though, have for a long time primarily pimp’ed out the “sales price” numbers – completely ignoring *how many* sales.

Fed’s ZIRP “wealth effect” necromancy kinda relies on the US public systematically thinking that their highly leveraged homes are worth substantially more than if any sizeable pct of US homeowners actually tried to sell them in a reasonable period of time.

With 80-85 million SFH homes, it would take a lonnnggg time to roll-over the whole shooting match at a rate of 4 million sales per year. And, yet, solely reporting “sales prices” cultivates that misleading mindset.

(Hell, even at 7 million homes per year – peak sales volume – it would take a long time to work through 80-85 million SFH).

Same dynamic applies to stocks and market cap hype.

https://x.com/Barchart/status/2053810202454221186

This does sound like the classic turn in the markets where sellers are not getting buyers, volume dries up, but eventually, sellers starting discounting, or are forced to discount because of layoffs.

But your article on May 8 is titled “Supply of Labor Shrinks Further while Private-Sector Jobs Grow”.

So, the layoffs aren’t here yet. . . . .

It looks like the median price chart got put in twice for condos and coops?

Also the seasonal adjuster for the sales data in the South looks like January’s past adjustment doesn’t apply any more!

Can someone explain how it’s possible demand has cratered, supply has spiked, and we still haven’t seen halfway decent reductions in price? I get we’ve dropped a hair from ‘22 but that last little spike unwound then has flatlined for 3 years.

Sellers are in no need to sell now. They just want their peak’ish price hence not budging from their aspirational/asking price.

Prices wont go down but for recession.

These sellers also have locked in very low mortgage rates.

“Sellers are in no need to sell now”

I get what you are saying, but have deaths, divorces, retirements, or job losses ceased?

Those are traditional drivers of home sale inventory.

Perhaps people are white knuckling it through in order to preserve their maximalist fantasies (although why now if not historically?).

But even if true, all that means is that latent future sale pressure builds and builds – likely making future price falls faster and worse.

On balance, it *is* fair to wonder at long delayed price sell-offs 4+ yrs post-ZIRP (the turning point for the Fed’s demented ZIRP goosing of home sales prices post 2002).

Prices going up still in Europe, I think we’re ready for a rally. /S

Cem-

It depends on the market; New vs. Existing are different.

New home sales (NHS) are doing rather well, because home builders cut prices and provided incentives to move their inventory. As Wolf has said previously, home builders are a business and they do what they have to to make sales happen. BTW, I don’t think incentives – including mortgage rate buy-downs – are included in the headline price reductions. Wolf has spoken to this also.

As far as used/resale/existing home sales (EHS) go, well, and as Wolf says in this article, sales are in the “deepfreeze” because used home sellers still want 2022 bubble peak prices, but those are gone, because mortgage rates are now more than 2x higher. They’re even pulling their listings if they don’t get their aspirational (read delusional) wish price. This is the current “rage” delisting. I’m guessing that NHS are maybe 20-30% of the market currently, while EHS are the remainder, so if EHS are frozen, then overall sales are going to be low, and they are.

As in Housing Bubble (HB) 1.0, prices are “sticky to the downside” due to said used home seller reluctance to cut prices. However, home prices are set at the margin, and sooner or later, some will have to sell due to the “3 D’s”: death, divorce, distress. For example, demographics indicate millions of baby boomers will pass on over the next 20 years, and ~70% of these properties will be sold by the heirs (children). That’s a lot of inventory coming soon to a market near you.

Anyway, expect prices to drop, as HB 2.0 deflates, but it will take probably 3-5 years. I’m expecting ~35-40% price drop, just due to the difference in 2-3% pandemic rates vs. current 6.49% (MND today) rate. P&I only. All of the other carrying costs went up also… Remember, the Fed and .gov did this.

Homes are mostly unaffordable to shelter-buyers. Neither are mortgage rates going back down to the 2-3% artificial pandemic range, nor are wages going up 35-40% anytime soon. That leaves price decline as the most likely option.

Finally, we’re in HB 2.0, as part of The Everything Bubble, aka The Central Bank Bubble. History shows that asset bubbles always burst; an inconvenient truth. Reference Tulip Mania, South Sea bubble, Mississippi Bubble, HB 1.0, Japan Real Estate Bubble, Dot-Com Bubble, etc. BTW, AI is also a bubble. Not a good way really to run an economy, but here we are…

@Double Bubble you wrote “For example, demographics indicate millions of baby boomers will pass on over the next 20 years, and ~70% of these properties will be sold by the heirs (children). That’s a lot of inventory coming soon to a market near you.”

Keep in mind that most Boomers just have a couple kids and after they die and their “kids” sell the house and other assets there will “kids” with pockets full of cash to “trade up” for a nicer home or buy their kids an overpriced home. At 65 most of the “kids” my age have already lost their parents and many have used the millions they inherited to buy nicer homes, SF condos, Tahoe cabins and overpriced homes for their kids to live near them.

If the kids are just going to blow the wad on nicer housing, cars, etc., why leave an inheritance?

I’ll leave my inheritance to kids/grandkids/trusts for education, medical, and charitable purposes only.

Bobber.

Interesting that you have more faith in the judgment of unrelated trustees and financial managers than you have in your own offspring…

AI-

They say that demographics is destiny, and not all boomers, or their children are wealthy. Just check out retirement savings, including housing equity in the U.S.

Fertility/birth rates are way down in the U.S. and in the OECD – and China – in general. Ditto for immigration, at least in the U.S. for now.

Who’s going to buy all the McMansions? Too big and too expensive for both price + carrying costs. Younger generations want starter homes, if at all. Econ 101. Supply and demand. It’s estimated that 15M boomers will pass on in the next 10 yrs. Same est. for the next decade as well. Ref.: The Silver Tsunami.

Ref.: Japan’s housing market, or the lack thereof. 15%/9M vacant homes. The U.S. currently has 15M vacant homes, already, but that’s an allocation problem in the U.S due to financialization/commoditization of shelter.

In the U.S., housing is too expensive. Sales are in the “deepfreeze.” Sales volume leads price. Mean reversion is a thing.

IMHO, the stock markets are keeping the U.S. economy afloat. AI/Semiconductors is part of this. Housing is highly correlated with stock prices. I’m expecting a mean reversion event in stocks as well, which will bleed into the housing market. There are consequences to blowing asset bubbles; an inconvenient truth. Bubbles as far as the eye can see…

Inflation. The housing market absorbed newly printed QE $$$. The big question is if wages can inflate to match in a timely manner. It would be nice to see a correction, but it’ll take years. The fed ruined some stuff after 08 and covid.

Many things are possible but a spike of wage inflation seems unlikely in the near term with the wave of white collar layoffs. Why do we think places like Oakland and Austin seeing price declines?

The economy seems stagflationy except for the AI capex. If that seizes up…uf for everything.

SFH price doesn’t look so high when compared with inflation. The lack of sale may be due to lack of wage growth and mountain of taxes. I certainly can’t afford my own house if I have to buy it again. I can barely afford the property tax, which has gone through the roof.

A lot of accidental landlords must be muddling through with low vacancies.

There are only so many housing units, so the people waiting for the market to crash are paying rent in the meantime, keeping the accidental landlords from having to cut their prices.

But paying rent saves them lots of money — thousands of dollars a month in expensive markets — and they don’t have to worry about property price declines and being stuck in an upside-mortgage. Accidental landlords have the carrying costs and the risks of property price declines, plus all the substantial risks of landlording.

Yea, the standoff is between owners who can break even charging lower-than-mortgage rents but don’t want to sell their wood and brick lotto ticket for a too-low price, and the potential buyers who are comparing lower-than-mortgage rents to possible high mortgage payments.

The irony is that the standoff is stable because owners can just sit on their high prices and wait indefinitely as long as the rent pays the note, and renters can rent indefinitely as long as that’s cheaper than buying.

The equilibrium will only be broken during the next deep recession when the renters lose their jobs and must consolidate households with roommates or parents. That will create a vacant rental units, which will force the owners to lower prices to escape negative cash flow situations.

But then prices will have to keep falling because the number of qualified buyers will have gone down, and because the remaining buyers will be both scared for their jobs and caught onto the idea that prices will have to fall.

But rising ownership expenses and falling home prices should drive some selling of vacant homes and vacation properties in the short term.

In my neighborhood

People are buying homes and paying 10k per month to rent out the homes at 5k per month

In so cal it’s crazy

They can make it up with volume 🤣

There are JUST enough Buyers today. Any more reduction of Buyers and we will see prices start to really slip. My listings have for 2 years been underwhelming as far as showings but still sell. In the old days you would get 2 or 3 times the traffic and about the same amount of offers. Buyers must still think it is a Sellers market but from my observation it is clearly a Buyers market still buyers are behaving like they are going to miss out if they don’t act fast. Also the ” Spring Buying Season ” has moved up to February-April in the last 5 or 6 years as Buyers can look at listings on their phones with no need to call an agent along with the same thinking that if they look before June they will get a better deal. The reality is that this market is hanging on by a thread.

We’re studying our Orange County market intensely as we expect to list in two weeks. Well appointed turnkey homes in great school districts are still selling for list. Takes a little longer, but buyers for premium properties are still active. Fixers are wallowing and taking multiple price reductions. The buyers that are out there are choosy.

The sellers who are hallucinating are the ones who dump their dog of a house with no updates on the market and expect 2022 pricing.

I eagerly await the incoming Fed chair and the midterms. Seems an awful lot of the future of the US will be decided after that period. I wonder if Warsh will cook up some new theory to sell out more of the poor and middle class to the rich or do a lazy about face and cut rates with the potential help of Trump firing voting members should the midterms go his way.

Nothing of any significance will change at all with a new Chairman of the Federal Reserve. All interest rate policies are set by the 12 member FOMC and the Chairman just has a single vote. How is the Federal Reserve in any way even involved with the so-called ‘middle class’ which its job is simply to be the central bank to bankers in the US?

J Powell will stay on the Fed board and be a shadow Fed Chairman for as long he can stay on.

@SoCalBeachDude is correct that the chair is just one of the votes on the FOMC. However, I think there are several members who could be persuaded that the combination of QT and lower rates can be used to reduce inflation (through reduction in money supply) without harming the economy (by not raising or even lowering rates). Warsh has already said he wants to reduce the Fed’s balance sheet, which would be QT.

I’ve advocated for this strategy before. I’m no monetarist, but QE/QT is powerful stuff, and should be considered the main policy tool, with interest rates in second place.

The issue is that when the Feds and Congress increased M2 by 41% between 2020 and 2022, a lot of that money ended up bidding up the value of investments such as real estate, stocks, and crypto. The market even retained enough capacity to absorb a massive increase in treasuries, without the 10y yield ever going too far above 5%. Inflation got under control when the cash moved off of Main Street and got parked in Wall Street investments.

If Warsh reels back in some large percentage of the money supply by reducing Fed assets, will the reverse of 2020-2026 happen to asset prices? There’s no reason to think it won’t.

When the treasury is issuing fiat money and increasing M2, the offset is issuing treasury bills. And the new money is available to absorb the growth in treasuries.

That’s complete BS all the way through, from the W to the s. The Treasury Dept can do no such thing.

I having been leasing a SFM for the past 3 years south of Seattle and every time I look at what I can buy for the price of my rent it isn’t even close. Just re-upped for the 4th year. I figure if I had bought 3 years ago, I would have paid at least $70k more in mortgage than I have in rent. I also would have had to make repairs and lost out on the interest on my money during that time. Total opportunity cost over the last 3 years is probably right around $100k. I don’t think the appreciation and mortgage buy down would touch that. I hate renting, but will continue to do it until the math makes sense again. Just keep saving.

Same, but in the Raleigh metro area. SFH rental about to be re-upped for the 4th lease (did own a home until 2022 though). Getting locked into ANY kind of loan seems like a suckers game at the moment. Having long-term monthly obligations in a sea of change just strikes me as dangerous.

I’m not sure when being essentially 100% liquid actually starts to pay off again, but I intend to have the most dry powder in the storm (comparatively) — even if that means I just get to keep a roof over my head.

Historically, the payoff was about not being tied to a specific area. One could pursue jobs in other states and make career leaps every few years in pursuit of higher salaries, as long as one didn’t get bogged down in one place with a mortgage and a bunch of house problems to solve. Job hoppers tend to snag double digit percentage increases every 3-4 years.

I think maintaining job growth and mobility is key to making it work as a renter. If you aren’t getting this benefit in today’s low-unemployment environment, you’re wasting an opportunity.

Saving $3,000 per month (in my case), investing and saving the difference (or spending if large one-off expenses happen), and not having your time eaten up by home repair & maintenance are enough to make buying a really stupid thing to do right now (in my opinion). No moving required.

If (when?) the next crash happens, anyone who didn’t get caught up in the FOMO will be sleeping well at night, instead of sweating bullets.

I personally know a ton of people who bought during 2021-2025 and they’re barely surviving. Their 20-40 year old $750,000+ homes all have needed massive repairs that weren’t budgeted and these houses have become anchors sucking away savings, vacations… having a life.

A mortgage is the least you’ll pay in a month. Rent is the most. A lot of people are starting to learn that the hard way.

Treasury pays $3B a day in interest on national debt

How much does it get in tax receipts a day on average?

The US federal government collected approximately $5.23 trillion in total revenue during fiscal year 2025. Individual income taxes remain the largest source, accounting for over half of this revenue ($2.66 trillion), followed by payroll taxes ($1.75 trillion) and corporate income taxes ($452 billion). To get the per day tax receipts revenue, divide $5.23 trillion by 365 days. It’s a bit of a problem and issue that Congress is now spending around $7 trillion a year causing a nearly $2 trillion a year deficit to be added to the $40 trillion of federal debt.

The U.S. Treasury has paid $628 billion in net interest this year to service its borrowing, according to the the Congressional Budget Office (CBO).

The latest monthly budget update on the national debt and its interest burden, shared on May 8, breaks down the government’s income and outgoings for the fiscal year so far, which began in October.

The report demonstrates the government’s largest outlays: $953 billion so far this year for Social Security benefits, $588 billion for Medicare, and $409 billion for Medicaid. Net interest on public debt is a larger figure than both Medicare and Medicaid, totaling $628 billion for the seven months between October and April.

Looks like the CEOs of all the major corporations will be going to China with Trump to sell out the middle class once again, going against all the BS from the Treasury Sec about helping Main Street vs Wall Street. The likes of Blackrock, Blackstone CEOs all globalists to the core will be there making deals with China.

Good lordy. That’s to sell more US products and services in China, and have freer access to China and fewer Chinese tariffs and restrictions on US products and services, not vice versa.

Wouldn’t a deal to reduce tariffs be a more effective way to achieve this goal, rather than sending in one’s top campaign donors and cronies to make one-off deals with special tariff exemptions to be granted by the president?

I’m guessing selling more US products and services in China or freeing up access is not the goal at all.

The idea is to sell more high-value US goods (not ag stuff) and services in China and import fewer goods from China.

Bought a 1947 Cape Cod back in 2013 in Ohio in our late 20s – other than conceiving our only child this was the best timing of our lives. Now, how to get over that financially independent bridge??? Working on it, but investing in real estate is not part of the plan!

Seems like logical solution is for all rents to go up so high that buying a house by comparison is the right choice. Having two kidneys is overrated anyway so plenty of down payment options.

I don’t know if I can fetch enough money for my extra kidney or my first born, or both.

“I picked a helluva day to stop drinking”

-Independence Day, 1996

Got to preserve that kidney or else be homeless.

I’ve been watching those documentaries where the South Koreans are paying like $700/mo for what can only be described as a pod in a high-rise, and I’m like, you know, in the US you don’t even have the option of living in a pod. The cheapest option is to pay double that for a one-bedroom apartment, and if you can’t afford that, then it’s the cardboard box for you. As usual, the Asians are way ahead of us, well on their way to living in the liquid-filled pods from The Matrix, where they receive “food” and “shelter” in return for allowing the billionaires to harvest their DNA, and we over here in the US are out in the cold.

We may have one trick up our sleeves, however. The homeless here appear to have an unnatural ability to conjure up ancient RVs out of thin air. I watch the city bulldoze a whole lot of them, and a week later they’re all back. None of these things appears to be in operable condition, so how did they get there? It appears to be some form of witchcraft, which I hope to learn from the homeless when I eventually become one at this rate.

Matt B

There are $700 a month pods available in the US, but they’re not very popular apparently:

“A company that went viral for offering $700 a month sleeping pods as a solution to San Francisco’s high rent prices is now accused of failing to pay rent itself.

The startup is facing eviction as the tiny, dorm-like living quarters have been the center of a years-long fight with the city of San Francisco.

Tucked away in a corner of Mint Plaza sits what was supposed to be a revolutionary way to help fix San Francisco’s chronic housing crisis.

“Our idea was to turn these empty office buildings into housing in a way that isn’t too expensive so we can charge lower cost rents that people can afford that need to be in the city,” said Brownstone Housing CEO James Stallworth.

Brownstone Housing is the startup behind 12 Mint Plaza.

The unique location has 26 so-called sleeping pods — spaces people can rent and live out of for only $700 a month.

But now, 12 Mint Plaza could be on the verge of shutting down after Brownstone was hit with a lawsuit by its landlord for more than $150,000 in unpaid rent.

https://abc7news.com/post/brownstone-housing-ceo-faces-lawsuit-unpaid-rent-700-month-sleeping-pods-san-francisco/17508385/

It used to be the ‘American dream’ to own a home, have a car or two and a stable life. Now, it would be a nightmare or sign of complete failure to rent a ‘pod’ – how embarrassing and demeaning; a sign of slave status. Is it better than sleeping on the streets? One would hope so.

I guess an entrepreneuring person could open up a building full of them and call it the

Wolfs’ Dens.

Matt B,

We have 350 sqft new studios will small cook stoves, pull down beds and stuff but nowhere in the $700 ballpark! No parking either at all so best to not a car due to limited street parking.

I should have figured SF would have something like that. You would think that idea would work. Do people still rent out individual closets over there too? Where I’m at you can’t even get a studio anywhere. Old 1-bed apts go for $1600. The only way to get anything below that is to split it with a bunch of roommates.

Just need to find a roommate and split a two bedroom apartment. Lots of cities in the US where you can do that.

House prices set to plummet across country…

Spring Shaping Up as Bust…

Come on America. 6.37% 30 yr interest rate isn’t expensive – just market rates. Need to bring back the “ no money down” guys. Why can’t America market themselves out of this conundrum. Everybody wants a house not a pod.

Nobody can afford any of the houses they build today, and yet despite this, they continue to to build more homes for more money.

The only way to even qualify to buy a new $600k+ home today is to ensure both people are working. And that is just to meet the qualification, your mortgage is probably between $2k – $3k per month, and taxes, utilities and maintenance add another couple hundred.

Buying a newer good quality home today is a financial house of cards. If one person loses their, their financial support could collapse at and point and lose the house they just spent all that money on.

Stop build new houses and start moving people into the ones that already exist, or at least tare down the old houses so the land can start growing back.

“Nobody can afford any of the houses they build today,”

🤣 but those new houses are selling at a brisk clip — unlike used houses. You should read some of the articles here, including this one from May 5 about new house sales… it has a chart of those sales that “nobody can afford” – see below

And they lowered prices and piled on incentives, and that’s good.

https://wolfstreet.com/2026/05/05/new-single-family-home-prices-drop-further-amid-inventory-glut-but-lower-prices-beget-higher-sales/

It’s interesting how the national median SFH is down to the 2012 level even though the US population is about 35 million higher in 2026.

Frozen market …stubborn sellers and buyers … buyers waiting for a recession (rate cuts) and sellers waiting for a specific minimal price.

Unfortunately for buyers seems no recession in sight even with all the chaos in the middle east. Suppose there is still time for a nice juicy recession lol.

It is a golden time in the housing market right now, people have lots of time to look around and can get a proper inspection. If you want to rent there’s no rush either. Rates will back into the 5’s one day , maybe 5 or so years from now .

I agree with that view. However, we have friends and family members who “missed out” according to them. They get split into two camps at the opposite end of the spectrum.

Camp 1 “We will never own a home”. They have given up and have told themselves it’s not possible to buy.

Camp 2 “We’re wating for prices to come down.” They are diligently saving and waiting for something or someone to tell them it’s time to buy.

Neither group is actively looking out there, seeing if there are deals, watching some homes that go under contract and then get re-listed because of inspection, appraisal, and financing issues. In my opinion, we are returning to a more normal market and the prices still have to come down.

The right home could be out there for them, but they have just given up on finding it. Fast forward 10 years, some will still say “I missed out…again!” Hindsight is 20/20.

Buying at these prices is honestly insane.

I am in so cal where prices are gradually coming down. For a 1.5 mill home, if it goes down by say 3 percent in 1 year then they are losing equity of 45K per year or ~4K/month. ON top of that by renting they’d say ~$5K/month.

In essence, by not buying and renting the same home, they are saving $10K/month at least.

The math changes if home prices go up but difficult to go up from these insanely high prices.

Much smarter to wait then buy at these prices in my hood.

rates are not a problem but high prices are

Houses in San Diego are selling…when the seller is reasonable about the price.

Lots of homes closed near me because the seller realized that the covid mania run up was over four years ago. Homes are still expensive, but they are less than they would have cost in 2022.

Are homes way more than at the start of 2020? Yes. But people need to remember that Jan 2020 was over six years ago.

home today are cheaper than what it was in 2022.

Would it be cheaper in 2028 than today ? I think so.

Also, by renting n waiting, you save a lot per month.

In 1986 when I bought my first house, the mind set was that real estate would almost always go up in value, and that it was usually best to buy the most house you could afford because a bigger house would eventually mean a higher profit when selling. That is obviously not true right now. Today where I live there are an amazing number of apartments being built with a lot of people asking why so many. We will see if they fill up. I guess somebody knows something the rest of us don’t. My guess is that a lot of the apartment people will eventually be buying homes here. It is too bad about the pandemic and the decisions made. If I were a young person wanting to buy a house, I might try to find a job in a smaller town than the big cities. Homes are probably cheeper there and life might be better than living on the ant hill.

In the Southeast region, sales exploded due to people from the North and West making a killing on their home sale, and then moving here and buying either a much larger home or two homes and renting one of them. Since Tennessee does not have an income tax, it has attracted a lot of out of state retirees. Needless to say prices have gone up due to this influx.

In the last 2-3 years, this illegal immigration (LOL) has been sharply curtailed IMHO due to several reasons:

– home sales in these areas are decreasing along with selling prices,

– less people changing jobs and decrease in work from home

– Our prices are no longer as attractive, and the number of rental apartment complexes have exploded as well, resulting in a glut. Hence a second home as a rental or air bnb is not as attractive.

-A lot of companies offered buyouts during Covid, and people close to retirement took advantage of them and moved here. That wave has peaked and subsided.

Asking prices are still outrageous. When I see a literal hunting shack in the woods with a couple acres of land going for 150k – 250k, I know we are still in the Twilight Zone. Rod is going to show up any minute and say “Submitted for your approval”.