Which raises a question: How many more Fed rate cuts would it take in this inflationary era to drive the 30-year Treasury yield to 6%?

By Wolf Richter for WOLF STREET.

Treasury yields from 2 years to 30 years spiked today – along with crude oil prices and inflation fears – after Iranian attacks on oil facilities in the United Arab Emirates, commercial ships, and US Navy ships. Treasury yields are like a loaded spring amid escalating inflation fears. Rising yields means falling prices for existing bondholders.

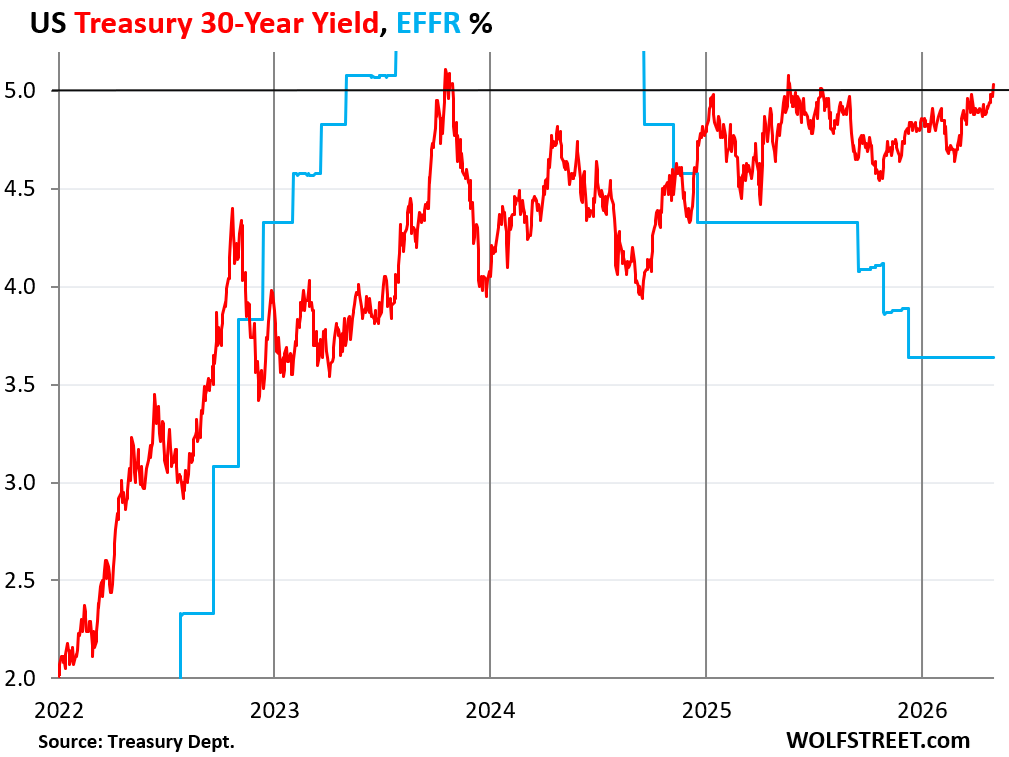

The 30-year Treasury yield jumped by 6 basis points at the moment to 5.03%, the highest since May 2025, and is now 139 basis points above the Federal Funds Rate of 3.64% (EFFR, blue line), which the Fed targets with its policy rates, as the bond market is now pricing in significantly higher inflation rates over the life of the bond than the Fed’s 2% target.

A dovish Fed – a Fed that threatens to “look through” surging inflation because it’s just an energy price spike or whatever – spooks the long end of the bond market. The more the Fed cuts, the higher the 30-year yield? Which raises the question: how many rate cuts would it take in this environment to drive the 30-year yield to 6%?

But historically, 5% is not a high 30-year yield: between October 1979 and October 1985, the 30-year Treasury yield was over 10% and topped out at just over 15% in September 1981. It didn’t drop consistently below 5% until the Financial Crisis in late 2007.

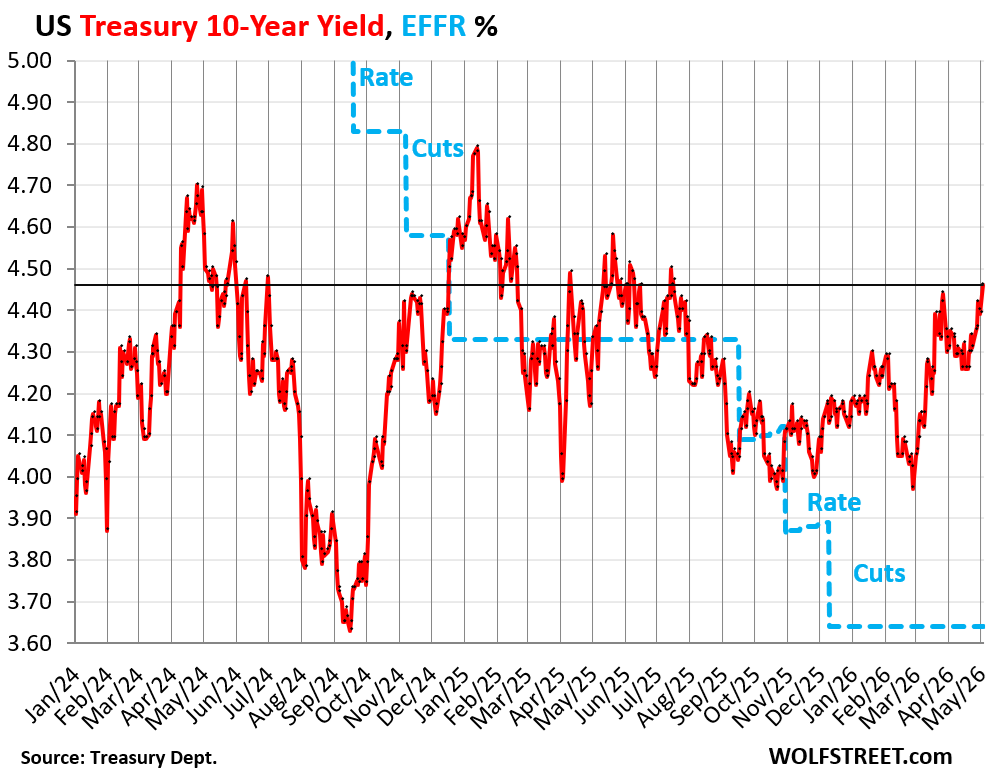

The 10-year Treasury yield spiked by 7 basis points at the moment, to 4.45%, the highest since the top of the spike in July last year.

Since end of February, the 10-year yield has surged by 50 basis points. It is now 82 basis points above the EFFR.

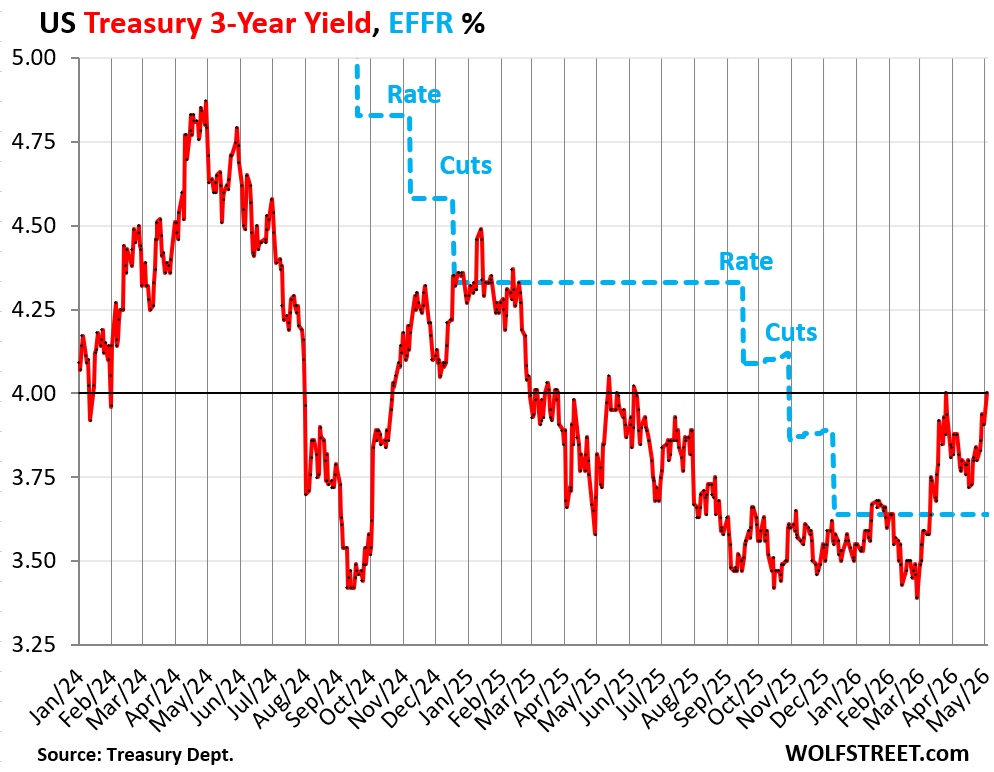

The 3-year Treasury yield spiked by 9 basis points to 4.0%, same as the top of the spike at the end of March, and both the highest since June 2025, and both 36 basis points above the EFFR, a strong signal that the bond market is expecting rate hikes over the next couple of years, not rate cuts.

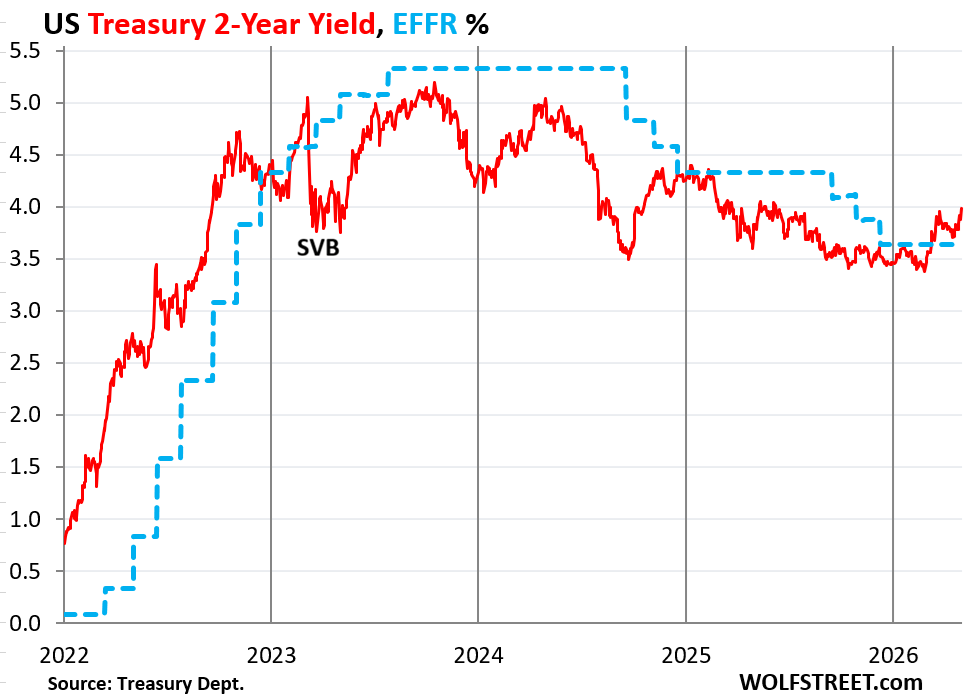

The 2-year Treasury yield spiked by 8 basis points at the moment to 3.98%, the highest since June last year.

It is now 34 basis points above the EFFR of 3.64%, the most since early 2023 just before the SVB collapse, after having been below the EFFR for nearly the entire time since the SVB collapse on rate cut expectations. This recent surge above the EFFR is a sign that this part of the bond market is now pricing in rate hikes, instead of rate cuts. And this expectation of rate hikes is also why the 30-year yield hasn’t yet surged toward 6%.

Overall inflation rates already spiked in March due to the energy price spike. It remains up for debate to what extent exactly the energy price spike will also fuel, sorry, even higher “core” inflation, which excludes energy and food products that consumers pay for directly.

The Fed favored “core” PCE price index has been rising for months and in March reached 3.2% year-over-year, with the 6-month average at 3.7% annualized. But even this core measure will trend higher as higher energy prices start filtering non-energy goods and services – part of which has already started with airline fares.

The longer end of the bond market is on edge about this inflation scenario and the risk that it could spread over many years as the Fed remains unwilling to really crack down on inflation and keeps looking for excuses – such as “looking through” the energy price spike, and perhaps under the Warsh-Fed, expecting that efficiency gains from AI will somehow solve the inflation problem.

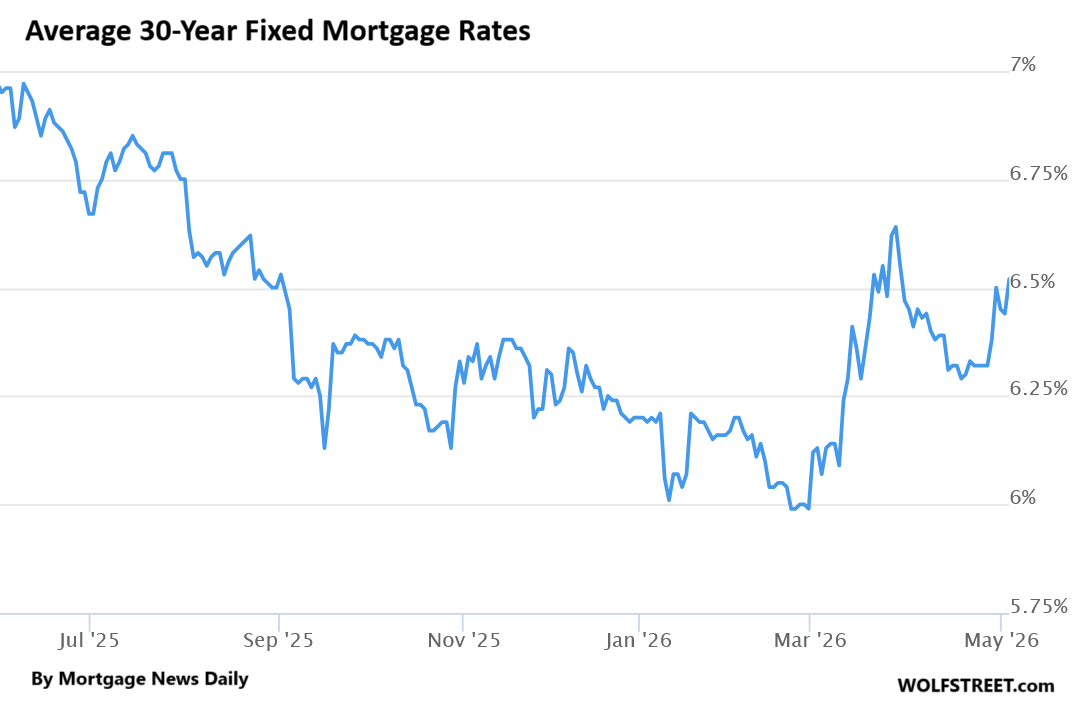

And the average 30-year fixed mortgage rate, which roughly tracks the 10-year Treasury yield but is higher, jumped by 8 basis points this morning, to 6.52%, according to the daily measure by Mortgage News Daily.

In case you missed it: The US Government sold $723 billion of Treasury Securities this Week. Inflation Jumped and Met T-bill Yields

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks wolf

It’s starting to get real… When idealism meets physics.

Yup

The spring is loaded and there appears to be no way out except higher rates. 4.75 on the 10 year will see 7%+ for a 30 year mortgage. That should tip housing over for a nice dip. I’ve been watching Texas prices and it isn’t just Austin. Way overbuilt north of Dallas. Looked at a really nice house w/guest house in McKinney and it’s almost back to2017 price. Nothing like leaving 25% profit on the table and now trying to just break even.

Yeah it’s perfect for Spring/Summer selling season. Rates going up may also finally make sellers realize next year will likely be worse, not better, and we’ll start to see some more price pressure.

Also on a demographic standpoint demand for rental units is also falling for a number of reasons. So I think delist and sell is also going to not be an appealing option very soon.

Everything is fine. It’s like this… we’re on a party bus, drinking up the tax cut money, going down the mountain having a blast, with no brakes and an orangutang at the wheel.

The visuals are outstanding!

Exactly!

And the intoxicated ditz Cackler would have had Us in a better situation at this point ?

🤣

Probably not in the middle of a war!

Yes. Thanks for asking.

[1M] DXY might flip if “Project Freedom” produces casus belly for the US or UAE.

You are about 2 weeks behind with this breaking news and analysis.

Casus belly? Is that like getting Bali belly? Bad times on the toilet.

Thankfully, we had a bidet in our hotel room.

Howdy Youngins. YOU were not around for the Greenspan era. Maestro, as some folks called him, would raise, lower, go sideways even, and was even considered a genius. Will the FED pull the Greenspan tool out of the FED toolbox???? I sure hope so… It is truly a sight to be hold….

Diffrent times

The 30-Year Treasury has flirted with 5% several times in the past 3 years.

A technical analyst would say this is “not a breakout yet” – not until the 30-year closes above the 2023 high of 5.103% and the 2025 high of 5.09%, and stays there.

This time may not be any different – Wolf used to say that rates above 5% will get peoples’ attention and attract fresh buyers. But since the 30-year has been above 4.5% for a year now, perhaps “6% is the new 5%” to make Treasuries attractive again?

I agree, when projecting from a very generalized and muted overall view. (Leaving out what the FED and US government have really been doing in specific detail, as well as strategic implications for the US as a result of much of any increase of interest rates. This also leaves out chain reactions for the economy, lending, real estate markets, etc. We shalt not talk in specifics here or draw parallels to houses made of cards, emperors style of clothes and the death of empires that have had their foundations severely undermined by greed and degeneracy.)

If I remember correctly, Wolf said that about the 10-year, not the 30-year.

The 30-year is too long duration for a lot of buyers, so 5% is not enough to entice most people into that. But reasonably high 10-year treasuries would be good for retirees

That’s right, it was the 10-year that Wolf mentioned.

The 10 year hasn’t closed above 5% yet. Just flops around between 3.6% and 5% for 3 years.

IMHO issuing debt to replace MBS rollover was the signal to us all that the Fed intended to “run it hot”.

Tidal waves of liquidity. 6% rates and $6 gas by 8/1.

It’s gonna be GREAT!

Historically rates are not terribly high, but in the post 2008 crisis where rates were kept low and most thought it was the new normal. Now lots of debt needs to be rolled over in the next 3 or so years, at much higher rates, and I suspect that it will have a major impact on everything.

The 150 year average 10 year yield is 4.5%, almost exactly what it is today. Except for the oil shock in the early 80s, the two previous peaks of 5.6% during the panic of 1873 and 5.0% in the post WW1 panic in 1920 were the previous highs.

It’ll be interesting to see what the high will be during the current rebound from historical lows in 2020.

@Numbers, 2 thoughts regarding 10-year rates:

(1) Rates prior to 1971 are not comparable to those since, due to abandoning the low-inflation gold standard in 1971. Because of fiat-currency inflation, rates since 1971 are higher. Today’s TIPS rates are more directly comparable to pre-1971 Treasury rates.

(2) I have multiple sources that contradict your historical rate data. There are a lot of bad sources out there, which did you look at?

What I see is that the 10-year yield:

(a) Had a peak at 8.1% in 1798

(b) Was uniformly above 5.5% from 1794-1819 or so.

(c) Peaked at 6.6% in 1842

(d) Peaked at 6.6% in 1861.

(e) Was never below 4.0% (on a gold standard!) from 1790-1878 or so.

(f) Hit 5.6% (not 5.0%) in 1920

(g) Was never below 4% from about 1960-2002.

For more info on the economic significance of the Gold Standard (and loss thereof), see WTFHappenedIn1971.com

Those are a lot higher than today’s TIPs rates.

The Gold Standard, the last legal link to gold (prior to the “gold cover” bill of March 19, 1968), was fictional, the economic tie tenuous, and its protection was a myth.

It was the raises in Reg. Q ceilings that caused the change.

The low structural inflation in the various monetary regimes from 1820-1971 is unmistakeable. But it’s a 150-year period, not a 40 year period, not a 10-year period.

Regulation Q did not exist before 1933 and only restricted bank interest rates to retail customers. It did not affect U.S. Treasury Bond rates. It did not even affect retail interest rates until the mid-1960s, because market rates were lower than Reg Q limits until that point.

Even now, long after Regulation Q constraints were phased out, very few banks will pay interest on savings at anywhere near T-Bill rates. Reg Q just isn’t a factor in this conversation.

Alan Greenspan had an excellent article “Can the U.S. Return to the Gold Standard” in the WSJ on 9/1/1981.

See Barron’s:

1) “Forgotten Man? Washington Again Is Threatening to Penalize the Thrifty” Jun. 6, 1966

2) “Up the Down Staircase, The New Economics Doesn’t Know Whether It’s Coming or Going” Sept. 26, 1966

3) “Ceiling Zero. The U.S. Must Take the Lid Off Money Rates” Nov. 26, 1967

4) “Men and Money, Savers of Modest Means Deserve a Decent Return” Jan. 19, 1970

5) “Q Marks the Spot. All Ceilings on Interest Rates Should Be Lifted” Dec. 28, 1970

6) “Maximum Mischief, Ceilings on Interest Rates Must Go” Mar. 13, 1973

7) “Supreme Interest. The Banking Agencies Have Finally Done Something Right” Jul. 23, 1973

8) “No More Wild Cards, Congress Has Dealt Savers Out of the Money Game” Oct. 2, 1973

9) “Poor Joe DiMaggio. It No Longer Pays to Save at the Bowery”” Sept. 22, 1975

All bank-held savings are lost to both consumption and investment. Japan’s lost decade is prima facie evidence.

Monetary and Banking Changes from 1939 to 1979

Net expansion of commercial bank credit = 1189.1

Net increase in time and demand deposits and borrowings = 1202.6

principally eurodollar borrowings since 1969

Net effect on the volume of time and demand deposits and borrowing of all factors, except commercial bank credit (principally capital accounts) = 13.5

Lending/investing by the banks create deposits. Not the other way around.

It’s stock vs. flow.

Frozen savings ,,,,, Reg Q ceiling %

11/01/1933 ,,,,, 0.0300

02/01/1935 ,,,,, 0.0250

01/01/1957 ,,,,, 0.0300

01/01/1962 ,,,,, 0.0350

07/17/1963 ,,,,, 0.0400

11/24/1964 ,,,,, 0.0450

12/06/1965 ,,,,, 0.0550

07/20/1966 ,,,,, 0.0500

04/19/1968 ,,,,, 0.0625 * most impactful

07/21/1970 ,,,,, 0.0750

It’s just as Dr. Philip George observed in his “The Riddle of Money Finally Solved”.

There were other factors that converged upon 1971. The Great Inflation was due to the monetization of time deposits, the end of gate keeping restrictions on TDs and the transition from clerical to electronic processing which vastly accelerated the transaction’s velocity of funds.

The Fed’s brake and gas pedals sigh,

Worried as markets edge high.

To slow or to speed,

They ponder with need—

Balancing growth ‘fore a crash nigh.

I love your poem.

Indecisiveness shines through.

Pray we get a hike.

“expecting that efficiency gains from AI will somehow solve the inflation problem”

The most likely outcome from AI is UBI, aka increased fical outlays on welfare and subsidies. Counterintuitively, Fed funds rate cuts are most likely to accelerate job losses in this environment, rather than “save jobs”, as lower rates would just make cheap money available to businesses to incentivize them to pull forward invest in AI while it is “cheap” to do so. Unfortunately, the Fed is mired in legacy thinking, and can’t see clearly here what needs to be done. The best thing to do here is to listen to the market and hike the Fed funds rate by a quarter of a point, rather than sitting on their hands. They can cut rates a month later if things were to somehow improve, which only Peter Pan would be able to envision at this point.

“The most likely outcome from AI is UBI”

This UBI BS is getting really old. Don’t these UBI mongers ever use their brain to do some grade-school-level math?

According to these morons: Since AI destroys all the jobs, the government should pay everyone the UBI. But who, dear morons, is going to pay the government those vast amounts of taxes needed to 1. replace $2.6 trillion in personal income tax receipts since people aren’t working anymore (2025 figures) and 2. PAY them $13 trillion in UBI to replace wages and salaries (2025 figures)? They need to come up with $16 trillion a year in NEW TAX RECEIPTS to do this. They cannot even come up with $6 trillion now 🤣. Corporate taxes are not going to get multiplied by 30 to pay for it, AND billionaire wealth isn’t going to get 100% confiscated to pay for it, and even that wouldn’t be enough. So where would these $16 trillion A YEAR come from? From a VAT? 🤣 Pay people $4,000 a month in UBI and then fund that $4,000 UBI by collecting $800 in VAT back from them???? Did these UBI mongers miss grade school? That whole idea is just stupid absurd bullshit.

Money is an exchange medium for human work. AI and robots do not run on such an exchange medium. Their basic exchange currency unit is energy, and in the future it will be perhaps some sort of crypto. Human energy will provide only a minor input for AI and robots, if at all. So what would be the incentive for AI to share energy in the form of UBI with humans?

If you are optimistic, you hope that this is going to be hard wired into the AI/robotic future by a sane human. But looking at the current leadership (Musk, Altman, et al), I do not think this is going to be a home run.

“Their basic exchange currency unit is energy..”

So what you’re saying is that a tax on electricity usage to make up for human income tax loss is the way to get AI operators to contribute? They build these data centers in the US where they are protected by the trillion dollar defense budget, and also can use functional highways, police protection and other first world benefits. Sounds good. How about 10 cents per kWh for everything over 1000 kWh a month. A big AI data center uses 70+ million kWh per month.

Right now AI is in their brute force phase. More processors and more energy are just being thrown at it in the race to get ahead. At some point there are going to be limits to processing power and energy. When that happens, the race will shift where the most computational and energy efficient AIs will win.

Seriously?

Robots and AI run on money, like everything else.

They ain’t cheap at all.

That is why manufacturing went overseas. Labor is cheaper than machines over there.

Right now these ai tools are cheap for users, but only because the companies are losing buckets of money. Their prices must increase eventually and it has already started.

It’s really quite simple. The AI computer kills all of humanity except for 5 people after merging all competing AI architectures. Those 5 people are kept alive through a “UBI” of small food and water rations while they are tortured endlessly as punishment for AM’s creation. Err… I MEAN AI’s creation. Yes… AI.

I for one welcome our new robot overlords.

I have no job but I must spend.

They should simply add more progressivity to corporate tax rates, which would rebalance wealth and strengthen system sustainability, plus spur competition by discouraging excessive scale.

The economy did great when tax burdens were based on ability to pay. The fiscal situation slowly fell apart when trickle down tax theory entered the scene.

Look at the tantrum the elite had when corporate income taxes were imposed (in the form of tariffs).

But who, dear morons, is going to pay the government those vast amounts of taxes?

Elon Musk?

🤣

even if you take ALL his assets (stock, real estate, Treasuries, cash etc., all of it to where he’d be homeless), it would pay for maybe 2 weeks of UBI. And then what?

UBI wouldn’t be temporary, like the stimulus checks. It would have to be paid forever, month after month after month, year after year after year, decade after decade… It’s not a pile of assets the government would need, but a monthly inflow of $1.5 trillion, month after month, year after year, decade after deca….

@Wolf, sort of like SNAP and Medicare? Dumb expenditures don’t matter to Congress. Subsidies just push up prices, and they obviously want that. They don’t think beyond that.

You’ve got to get off this BS and do the third-grade math. $16 TRTILLION PER YEAR is what UBI would cost to replace wages and salaries, and tax receipts from those wages and salaries, on top of $7 trillion in normal spending, even as tax receipts would collapse, year after year, assuming no inflation. With inflation, all these number explode. That cannot be done, just like the earth cannot be flattened out no matter how much you think Congress can flatten out the earth. End of discussion.

And 16 Trtillion is a LOT of money. First comes billions, then trillions, then jillions, then trtillions. Coming up with that kind of cash will not be easy!

UBI wouldn’t work, not only from a funding perspective but also from a “who gets how much money” perspective. Those middle income earners would need more than a low income earner replaced by AI, otherwise they default on their house and every other loan. How would we even determine a fair UBI payment

Not sure why you’re getting so aggressive with people lately, but alas

It has zero to do with fairness, but with an economic collapse: UBI would have to replace every single dollar earned in wages and salaries, $13 trillion a year. If it doesn’t, the economy will collapse because consumer spending will collapse. If households that earned $300k in wages and salaries get $50K in UBI to replace their $300k, their spending collapses. They have to get $300K in UBI, and households that earned $100k have to get $100K in UBI, etc., or else the economy collapses. So this entire UBI notion is just plain absurd braindead bullshit concocted by morons for morons, and people need to quit dragging it into here.

“Not sure why you’re getting so aggressive with people lately, but alas”

There is a site where people can spread stupid-ass BS like UBI, and it’s called X, and Musk owns it.

It’s outrageous that people come here to promote UBI.

That was more or less my point about UBI – a high income household would have to receive a disproportionate amount compared to a low income household to allow the economy to keep chugging along.

In the event that AI is as disruptive to labor as some (or many) predict, what kind of system do you think could prop up the economy?

I have been milling this over and I can’t come up with anything.

@Troy “In the event that AI is as disruptive to labor as some (or many) predict, what kind of system do you think could prop up the economy?”

The current system will work just fine.

It survived industrialization, automation, mechanized agriculture shifting millions from farms to cities, automobiles eliminating horses, telegraphs and telephones replacing messengers, radio & TV, computers, and internet shopping.

So long as there are human needs that can only be met by other people, we will find new ways to work for one another.

Given enough energy, labor-saving AI and robotics will deflate production costs and free up more leisure time. That’s good, not bad!

The workweek was 6 days/week until the 1930s. It could drop to 4 days/week, or 3.5 days/week with alternating schedules.

The two-income household is not historically normal either. Taking care of a home and raising a family are still a lot of work. But with AI and robotics, staying at home and raising children could become an affordable thing again. Some young parents could stay home to raise the kids, then finish school and go to work later in life.

Retirement can also be extended. It used to be a luxury, most people worked until they were near death. Now retirement is a norm. With robots producing more and reducing the need for human labor, a nation with a reasonable wealth distribution could support earlier retirement ages.

The one thing we do not need is political visionaries pretending they know better than everyone else, trying to sell everyone a free lunch paid for by your taxes. Let people figure it out for themselves.

Wealth is going to dramatically increase. But if a handful of giant monopolies control all the wealth of the nation, the people will become serfs and that isn’t fair at all. Competition, not redistribution, is what levels the playing field and ensures workers get a fair share of the world’s newfound wealth.

Regarding your UBI comment:

And for that I thank you !

And for a lot of people $4K a month is definitely “BASIC”. I like how Musk has moved onto Universal High Income, because most people don’t want to go from a high standard of living to basic one. So now, we’ve got to double or even triple that number.

Musk and anyone else hyping UBI are just trying to get bailed out on all their bad bets, trying to get their debts inflated away, inflate stonks.

MMT – the Magic Money Tree – will pay for everything.

Socialism works until you run out of money.

There will be plenty of jobs working to fix the dumb mistakes AI keeps making.

AI might replace a small subset of jobs, but it will also create other opportunities. It was true of the cotton engine, telephones, the computer, etc. A machine, a robot, or a computer might replace a job, but none of those things can buy a product or service.

And Trump still keeps wanting the Fed to lower rates. Does he not realize that in an inflationary environment, lowering short-term rates will stoke inflation, and lead to higher long term rates, and higher mortgage rates? The bond market has been telling us this for two years. Trump needs to change his tune, which he has shown he is capable of doing.

No, he doesn’t, but he certainly knows how to be bombastic & say lots of hyperbole stuff.

We’re going to find out real soon if Pocahontas was right about Warsh being a TACO stooge.

I have my doubts.

After income taxes on interest, investors are actually losing money when buying US treasuries. Even when kept in tax free retirement accounts it barely preserves the current purchasing power. No wonder every other asset class is in a bubble.

So was there just more things to invest in back in the 70’s or whatever? Or was there less money chasing investments? Because I feel like the only logical reason the markets are the way they are is that there’s way too much money floating around that has to be invested *somewhere*.

U ask AI questions and the bills pile up. Nothing for free. U have to organize your co before asking AI. It add cost. U always need a team to analyze if AI makes sense. Large co build their own data centers with NVDA chips and a cooling systems. AI customers can out of budget fast. Only 33% are happy with it.

I was just listening to Patrick Boyle’s video on inflation he made a couple days ago. Seems like a pretty concise case that inflation is only going to get worse in the US no matter how much mental gymnastics we try to use to wish it away.

We’ve implemented AI for our routing. Of course this isn’t the lean efficient AI employed at LTL companies that actually massively improved productivity. This is garbage software that had a lot of motivational speaker type blowhards woo old digitally clueless suit fillers. I’ve been living up to my autistic nature and auditing my routes. In the past 2 months it has been implemented my route has had a 31% increase in fuel usage. 17% increase in miles traveled. A 7% drop in net tonnage/weight. And a doubling in customer call ins/dropped off the route. An utter and complete mess. I’m no luddite; I’ve seen what a good AI system can do for productivity. I’m currently seeing the grifting side where everyone has to pile in on the latest and greatest fad. We’re now starting to lose customers due to our faltering service as well.

As always there will be winners and losers.

TG, I always enjoy reading your perspective. Hope you keep chiming in.

What you don’t see behind the AI and data centers is all energy and water consumption. What you should really be asking is; could all the energy (commodities) and water be put to more productive applications.

Humanity continue to eat it’s “seed corn” faster and faster and then wonders why why life for the average person gets worse and worse. If all these data centers and AI is so profitable, why do they need tax breaks and subsidies? At least when we overbuilt the internet and biotech they let all the non-profitable crap die (and yes the market lost 30%, that’s what is supposed to happen in capitalism) in 2001.

I don’t think inflation will be as fast as the pandemic inflation, as the government isn’t going to be sending checks with all the military spend that’s being asked, and consumers running large revolving credit.

That being said – it does seem inevitable that inflation will keep on going up as diesel gets passed through, especially when it gets into food.

A big question is when the Fed will start at least making noises to raise rates. They’re losing a lot of credibility on the 2% target with all the political headwinds. They’re leaving the proverbial punchbowl out too long.

Well, it’s been 50 years since we had our last real oil shock induced inflationary bout. At 5% 30YT and likely to go higher, I would imagine we’re going to see the T-Bills % of total treasuries move higher & faster than most thought possible.

Bond markets coming to reality is good thing. But we have seen 30 yr crossing 5% 2 times already after 2021. FED and US Treasury came up with some tricks and announcements. Reduce Longer issuance, more T-bills. We see how it goes this time. somewhere Bond markets have to realize Inflation risks.

Now inflation risks has gone higher and much far from FED’s target (compared to Labor market risk). So looking forward to Warsh led FOMC meeting in June.

This will be when rubber meets the road test. Warsh was all about Inflation and smaller balance sheet. It will be tested in first meeting. So lets see if he can “Talk the talk, walk the walk”

With an economy that appears to be strong overall, along with all of the cash floating around, it seems to me that we may have to get use to inflation that is a bit higher than the past. Since the end of the pandemic, inflation has been somewhat higher than before the pandemic. Interesting that lowering the fed rate could raise bond rates due to the increased fear of future inflation. Donald Trump would like interest rates to fall, but exaggerating in the face of reality seems to be his talking point these days with just about everything.

I don’t see UBI as replacement income, more like a subsistence pay to eke out the essentials. Leave people free to do art, child care restaurant work, auto & home repair. Who pays for it? robots and their owners.

A more likely scenario is we really really need the factory robots to pay into social security. Not the 8-15% but they really should pay something.

You’re promoting a total economic collapse. UBI would have to replace every single dollar earned in wages and salaries, $13 trillion a year in today’s money. If it doesn’t, the economy will collapse because consumer spending will collapse. If households that earned $300k in wages and salaries get $50K in UBI to replace their $300k, their spending collapses. They have to get $300K in UBI, and households that earned $100k have to get $100K in UBI, etc., or else the economy collapses. So this entire UBI notion is just plain absurd braindead BS.

I do not favor a UBI, but I think the idea is to replace basic income. If every household were to be above the poverty level it would require $25K (looked it up), and keeping the math easy 2.5 ppl/per household, yielding $10K per head, or JUST(!) $3.42 trillion. Probably be on top of other benefits which would push the cost higher.

Then people that wanted *more* could work, and they’d subsidize the tax revenues.

I feel its a poor solution given human nature, but I think trying to replace all income isn’t what it’s about.

Thanks for your great insights.

You’re twisting the subject and are introducing even more BS. The entire discussion that someone started is about alleged AI allegedly destroying alleged jobs and UBI replacing the income from those lost jobs. A household of coders losing $300K in income due to AI must get a UBI of $300K or else their spending collapses. And as the spending of millions of consumers collapses due to alleged AI’s job destruction, the economy collapses. When consumer spending dips by 2%, we’re talking about a massive recession. Now UBI-mongers proposing consumer spending drops of 20-50%. You people are out of your minds. UBI as a solution to the alleged AI job destruction is about keeping the economy afloat as AI destroys HIGH-LEVEL jobs, or whatever these AI-idiots are proposing.

This UBI bullshit has to end.

It’s great conceptually, but it doesn’t work in real world economics.

First is you were making $200k/yr and you’re now making $25k/yr you’re probably losing your house.

Second now you spend $25k/yr instead of $200k/yr so you’re stimulating the economy less. We have a 70% consumer driven economy.

Third you remove economic mobility, the rich control the politicians and govt. So it will not make us equal. It will return us to the middle ages where the class you’re born into you die in.

When this happens at scale say 10-20% of all white collar jobs get eliminated with no equal paying replacement. Home foreclosures take down the housing market. It trickles into every industry because who do you think buys the goods and services. Blue collar jobs suffer because these are the people who buy blue collar services. Then those people start losing houses and stop shopping. We end up in a death spiral. Landlords also end up screwed because this will drive missed rent payments and dropping rent. Like I said death spiral. We live in a 70% consumer driven economy and everything is connected.

UBI won’t save us. If replacement happens slow and new jobs are created we’ll be fine. If replacement happens fast and we start to see something like 10%+ unemployment we’re screwed because dropping rates won’t save us, it will spur more investment in AI and robotic replacements.

Guess I’m biased towards the pandemic era child payments because that was one time my charity case renter was not behind on their rent. Made my life easier. Don’t have kids myself but don’t mind chipping in a bit towards those that do.

If AI replaces all workers and we achieve some kind of post-labor-scarcity society where robots do everything for us, why do we think the robot makers would still have the same power to demand the pre-AI price for their products? At that point, the economy becomes a distribution problem rather than a distribution + incentive-to-work problem. We wouldn’t need to replace all wages as they are today.

(I don’t think AI is going to do any of that. I expect it to destroy the economy in a very different way when all these companies go bankrupt, but we’re talking hypothetically.)

Just to be clear, I’m not a UBI proponent.

I understand that automation can’t replace people working, earning income, and participating in an economy. Nothing comes for free. If we’re all sitting around who maintains the automation, invents new things, etc. And the best entertainment will still be created by humans (intentionally or unintentionally).

I was just trying to clarify an understanding of the proposal.

E Lon is a complete moron!!! I continually see stories of him pop up saying that in the next 20 years, people won’t have to save for retirement, and that AI will bring the age of abundance, implying that everything will be free.

If the guy really believes his own BS, he should GIVE AWAY ALL of his money, and wait for his utopian AI future. Imagine a (almost) trillionaire saying we don’t have to save for retirement. What a dolt!

Exactly. Instead of saving for your retirement he wants you to spend your retirement on his products today.

If long term interest rates are rising then growth stocks should be falling under the discounted cash flow approach to valuation. That’s not happening, yet.

Because the stock cheerleading crowd is convinced that BigTech can continue to grow at the same rate, no matter how little the economy is growing.

I’ve said for years that the math doesn’t work, long term. BigTech’s profits can’t increase by 20-30% every single year while the economy is growing at a stable, but relatively tepid, rate. At some point, the 30-40 P/E rates that are supposedly justified by forward looking “growth” hit a wall.

Big Techs market is global. I don’t think their growth fully depends on US growth.

A more interesting article would be a list of names & banks who bought the 30yr in 2020 at 1.3% to name & Shame. And ask them what they thought they were doing.

I’ll go first:

SVB Bank

Signature bank

But Wolf is a classy guy. He wouldn’t do that to his Wall Street friends. It’s garunteed Wall Street reads every article Wolf puts out to see if their named in it.

Someone out there bought a negative yielding German bunds for their pension fund.

Wolf, one of your best charts is the superimposing of 2 year treasury rate onto the federal funds rate. I check these rates against one another more often now, and feel less mystified by the fed’s rate decisions.

Dan

Great point. Note the 2yr presaged higher rates prior to 2022.

I took a closer look at comparison between 2year treasury rate and federal funds rate since 1972 using FRED data. From eyeballing it, looks like sharp rises and drops of 2year rate (like 2007 and 2021) are most predictive.

Also noticing that 2yr rate on average is 0.30% above FFR. If you can take the risk may not be a bad way to earn a little more interest.

Our first home loan was 12%, and that was low at the time. So many cry babys today. Like it or not, it turns out the America is just as corrupt as the rest of the world and now RISK is being repriced globally.

Hedge accordingly.

Rates should be higher, home prices much lower (or stagnant for a good while).

I’m guessing that your mortgage was in the mid-80s. Home prices are about five times more expensive: https://fred.stlouisfed.org/series/MSPUS. In some places it is much worse.

I worry for my kids being able to get a start.

Longtime reader of this blog and I dont think Ive ever commented. Can I just say that I absolutely love when The Wolf let’s any comment fly on the page and then he eviscerates someone as needed. This is a better platform than censorship. I love when The Wolf pops an IPA and rolls his eyes and lights someone up he says someone dumb. I guess I am Old School in that way. I am only 45 but made a lot of money in investment brokerage in my 20’a and in turn bought good investments that made me more money and I retired very young. Wolf unloading on someone reminds me of the good old days when someone who knew more than you told you why you were a moron when you expressed a stupid thought. Wolf you are the man. Never stop swinging. Much love.

Typo.. “I love when The Wolf pops an IPA and rolls his eyes and lights someone up when they say someone dumb.”

Long term rates are returning to normal. Nothing to see here folks!

Maybe with the cost of money returning to normal we will see other things returning to normal because I’m so tired of crazy?

News Gaurd which checks fake news: Anthropic Claude salad bar is contaminated by Putin, China and Iran fake news. 15% of the times they repeated Russian and Chinese propaganda. Last time they checked it was only 4%. Claude cannibalized the rest to spread fake news. They are getting worse !

I am in the camp who believes that the powers wont allow the long term yields to go up drastically high come what may.

they’d use fed to monetize all the bonds to suppress yields and use govt manipulated metrics to show that inflation is in 3-4 % range.

FED mandate is is have 2% or so inflation but they have failed so far on this for the last 5 years or so. Now 3-4% inflation on paper is normalized.

My “Gas Station from hell” just posted $6/gallon for regular gasoline. This is the highest in the history of this city. Look for it to go higher, much higher. I believe it will hit $8/gallon by the summer peak driving season.

I’m waiting for my gas station from hell to flip regular to $7.00. But premium is stuck at $6.99. Premium has to go first, but it has been stuck.

Switch to diesel Wolf, that is the real premium

I had some free time and went down to the site (ground zero) of the infamous January DC Sewer Spill. I used to hike down there and feed birds but NO more. The place stunk like hell. Sandbags were installed by DC Water to route the raw sewage from the C & O canal (built in 1890) to the Potomac river. If that had not been done, all the raw sewerage would have gone down the canal into the high rent districts of DC like Georgetown and Foggy Bottom, and destroyed businesses and residential property values. Its amazing how fragile our city infrastructure is and how quickly it can be turned into sewage dump.