The big divergence of asking rents in 14 big metropolitan areas by single-family rentals and multifamily units.

By Wolf Richter for WOLF STREET.

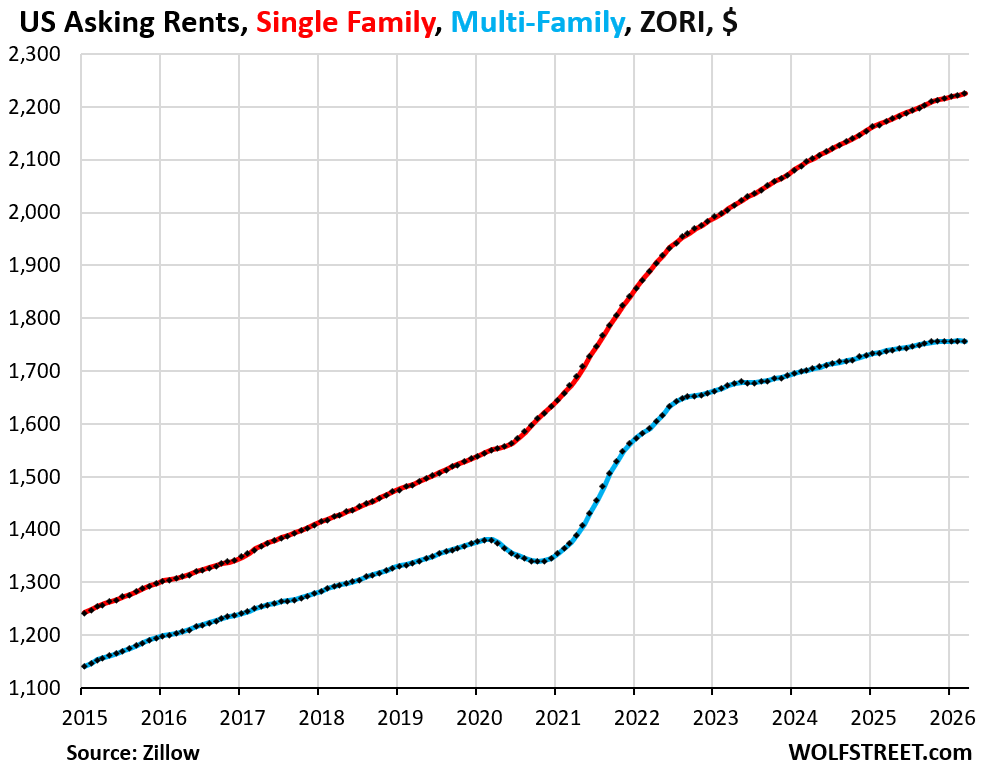

Asking rents – the rents that landlords advertise for their vacant rental properties – soared during the pandemic. But not in lockstep across different markets. And in some markets, rents have started to decline, while they continue rising in others. And asking rents for single-family homes have massively diverged from asking rents for units in multifamily buildings.

Since January 2020, mid-tier asking rents across the US for units in multifamily buildings have surged by 32%; that’s bad enough. But for single-family homes, mid-tier asking rents have exploded by 51% over the same period, such as by 69% in Miami, by 58% in Atlanta, or by 56% in Phoenix, according to the Zillow Observed Rent Index (ZORI).

Year-over-year, mid-tier multifamily asking rents rose by 1.0% in March, and on a month-to-month basis were essentially flat for the eighth month in a row, seasonally adjusted (blue in the chart). But single-family rents were still up 2.4% year-over-year and have continued to tick higher in recent months, but at a slower rate, seasonally adjusted (red).

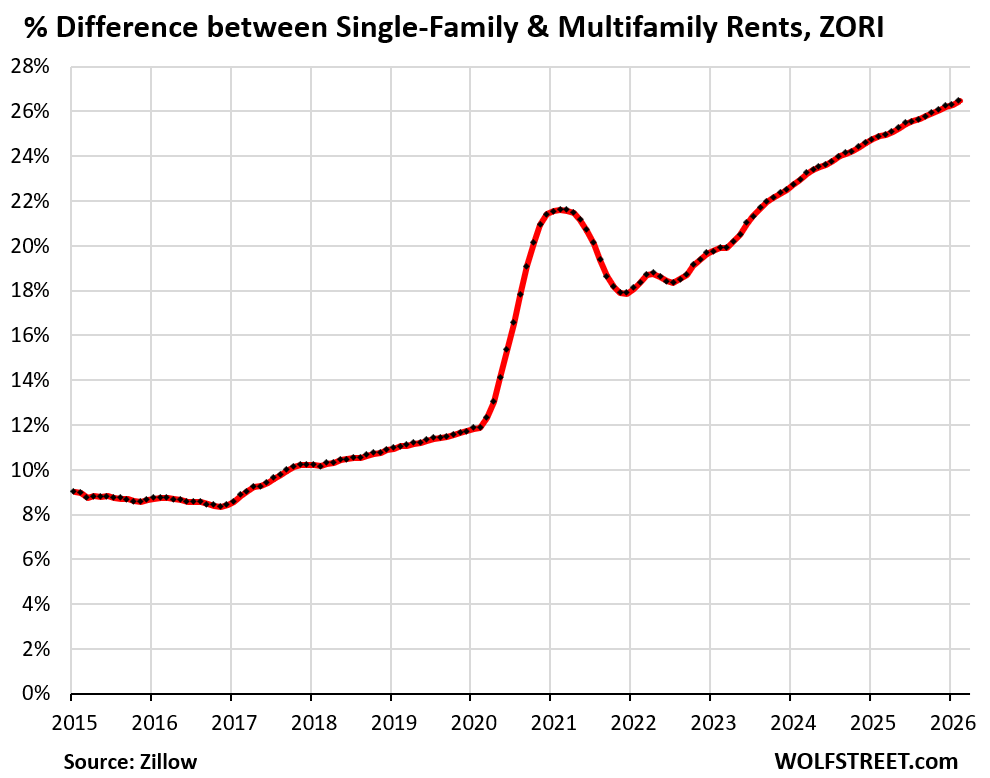

And the difference between multifamily and single-family asking rents has widened to 26.7% in March, the highest in the data, over double of what it had been before the pandemic.

By metropolitan area, the gap between multifamily and single-family rents ballooned to 71% in the Denver metro, to 66% in the Los Angeles metro, 54% in the Dallas-Fort Worth metro, and 51% in Phoenix. At in some of our 14 metros here, the gap was relatively narrow: 20% in Boston, 17% in Chicago, and 13% in the vast New York City metro, where Manhattan is mostly very expensive multifamily.

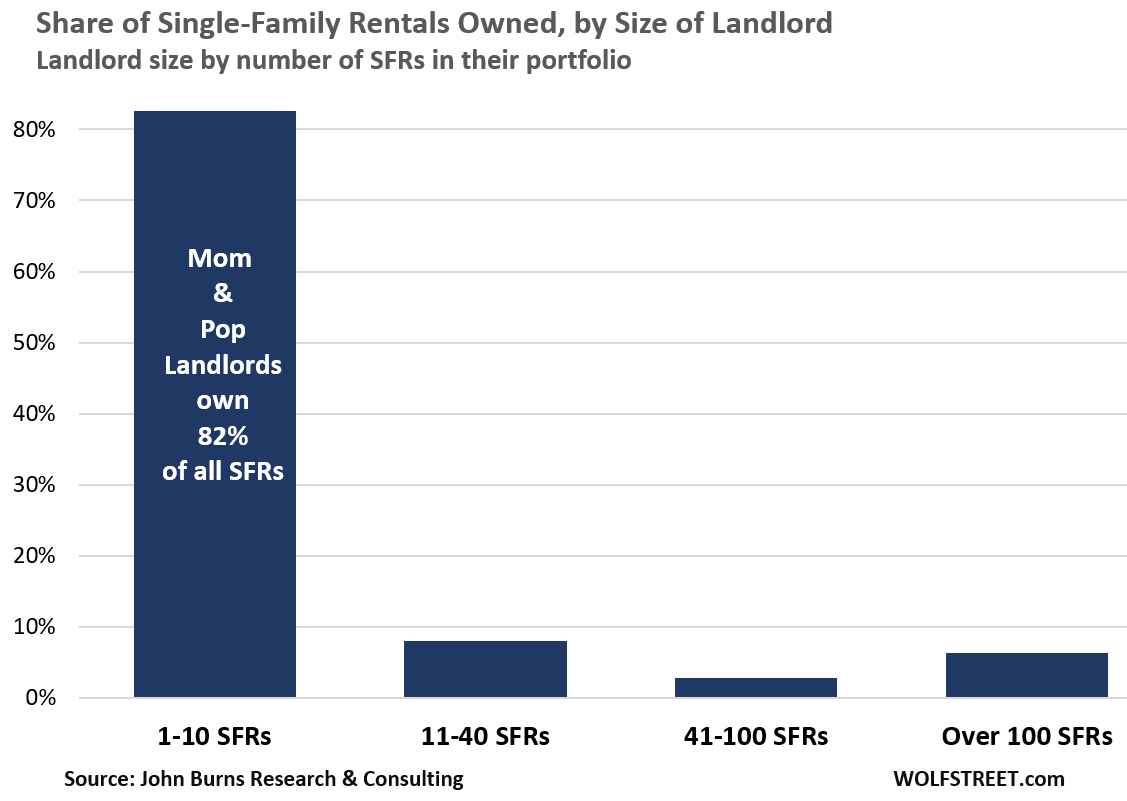

There are about 50 million rental units of all types in the US. About 15 million of them, or about 30%, are single-family rental homes (SFRs), of which about 82% are owned by mom-and-pop landlords with 1-10 rentals, and the rest by larger landlords, including a handful of giant landlords.

Asking rents are not actual rents that current tenants pay.

Asking rents are advertised rents on units that landlords have not been able to rent out yet and that are still vacant and advertised as for rent. These are not rents that current tenants are actually paying.

When rents come under downward pressure, as they’re now, after the huge surge, current tenants might be paying higher rents than asking rents, and might even agree to a small rent increase at renewal time in order to avoid having to move, while new leases might be signed at lower rents.

Invitation Homes, one of the giant single-family landlords, provided some details on these dynamics during its earnings report yesterday. Year-over-year:

- Renewal rents: +3.7%

- New-lease rents (close to asking rents): -3.0%.

Single-family and multifamily asking rents in 14 big markets.

The US rental market is not monolithic. Each market is different. Here we’re looking at 14 big metropolitan areas by asking rents for mid-tier single-family and multifamily homes, per the seasonally adjusted ZORI.

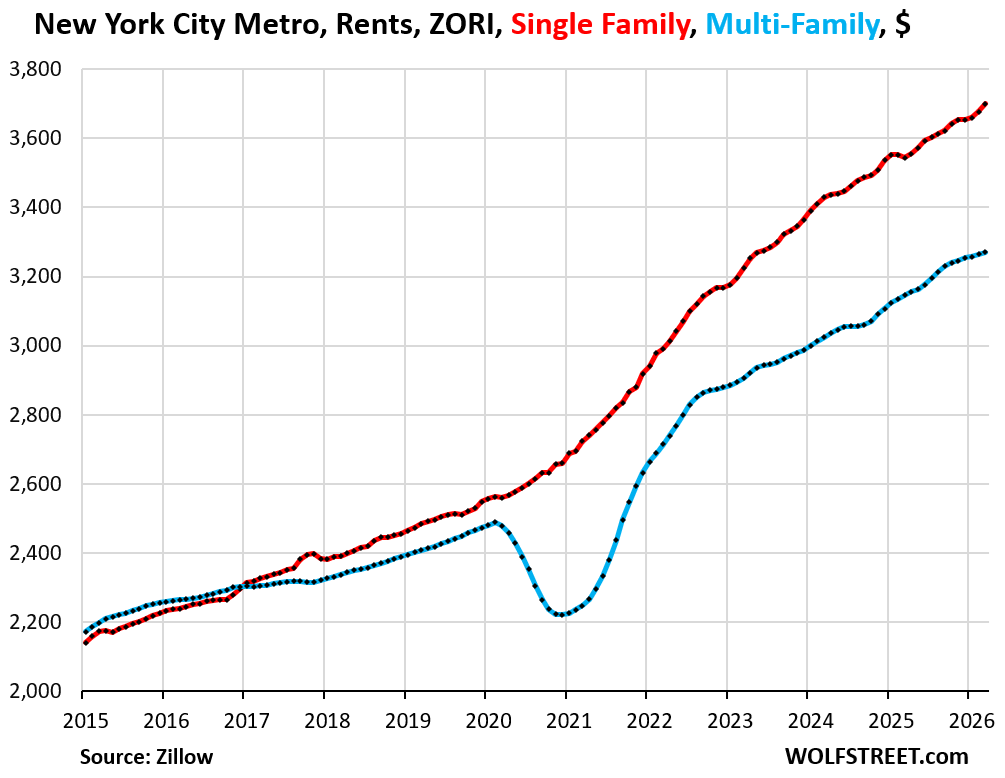

New York City metro:

- Multifamily ZORI: $3,271

- Month-to-month: +0.2%

- Year-over-year: +3.9%

- Since Jan 2020: +37%

- Single-family ZORI: $3,700

- Month-to-month: +0.6%

- Year-over-year: +4.4%

- Since Jan 2020: +50%

Difference between multifamily and single-family rents: 13%.

Note the drop in multifamily asking rents during the early part of the pandemic, as people were bailing out of the city, and the surge afterwards, as they returned and scrambled to rent a place.

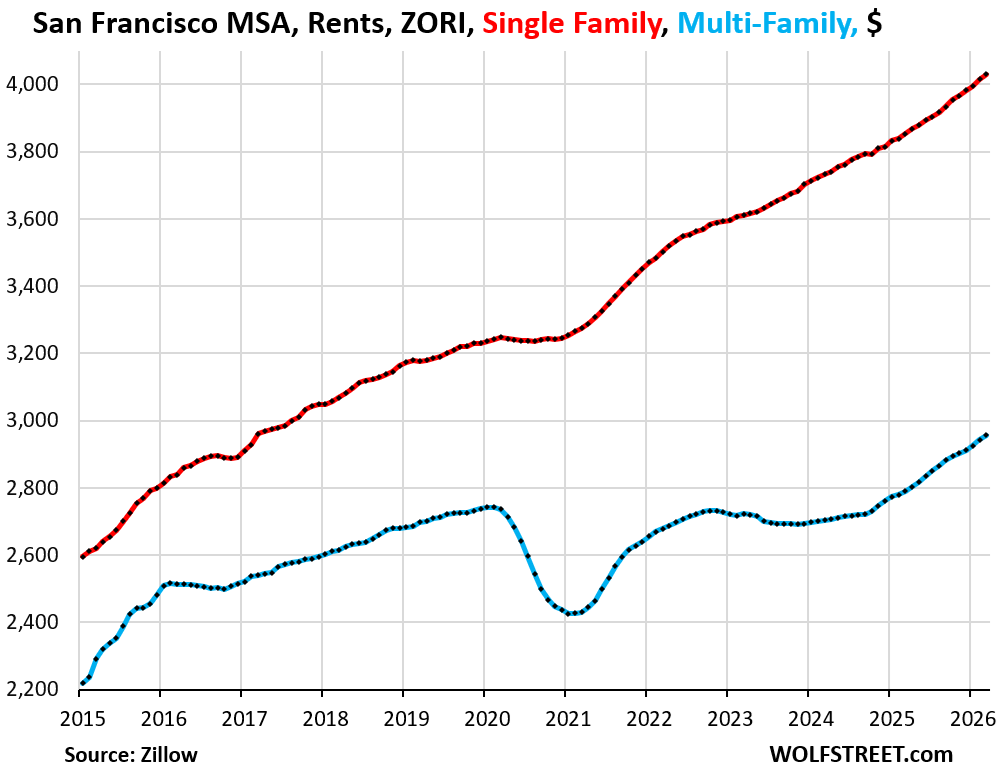

San Francisco metro:

- Multifamily ZORI: $2,957

- Month-to-month: +0.5%

- Year-over-year: +6.0%

- Since Jan 2020: +10%

- Single-family ZORI: $4,300

- Month-to-month: +0.4%

- Year-over-year: +4.6%

- Since Jan 2020: +27%

Difference between multifamily and single-family rents: 36%.

Also this drop in multifamily asking rents during the early part of the pandemic, as people were leaving the city to work from home somewhere else, and the surge afterwards. In early 2021, asking rents had dropped to the lowest since late 2015. While single-family rents soared.

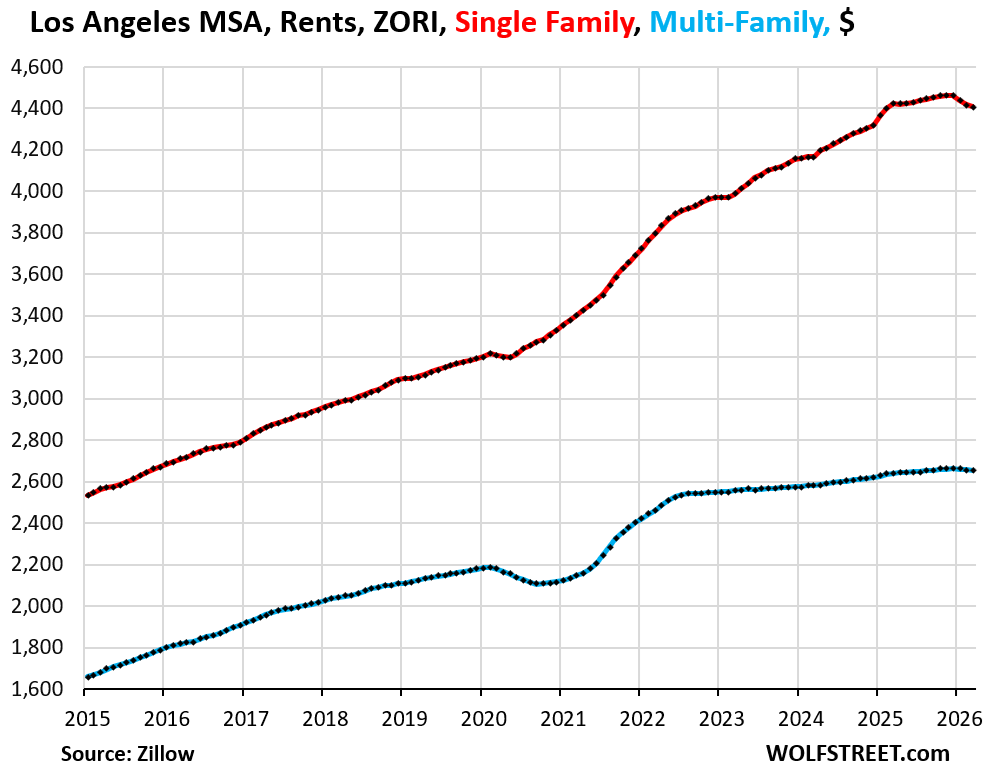

Los Angeles metro:

- Multifamily ZORI: $2,957

- Month-to-month: -0.1%

- Year-over-year: +0.5%

- Since Jan 2020: +42%

- Single-family ZORI: $4,408

- Month-to-month: -0.1%

- Year-over-year: +0.5%

- Since Jan 2020: +26%

Difference between multifamily and single-family rents: 66%.

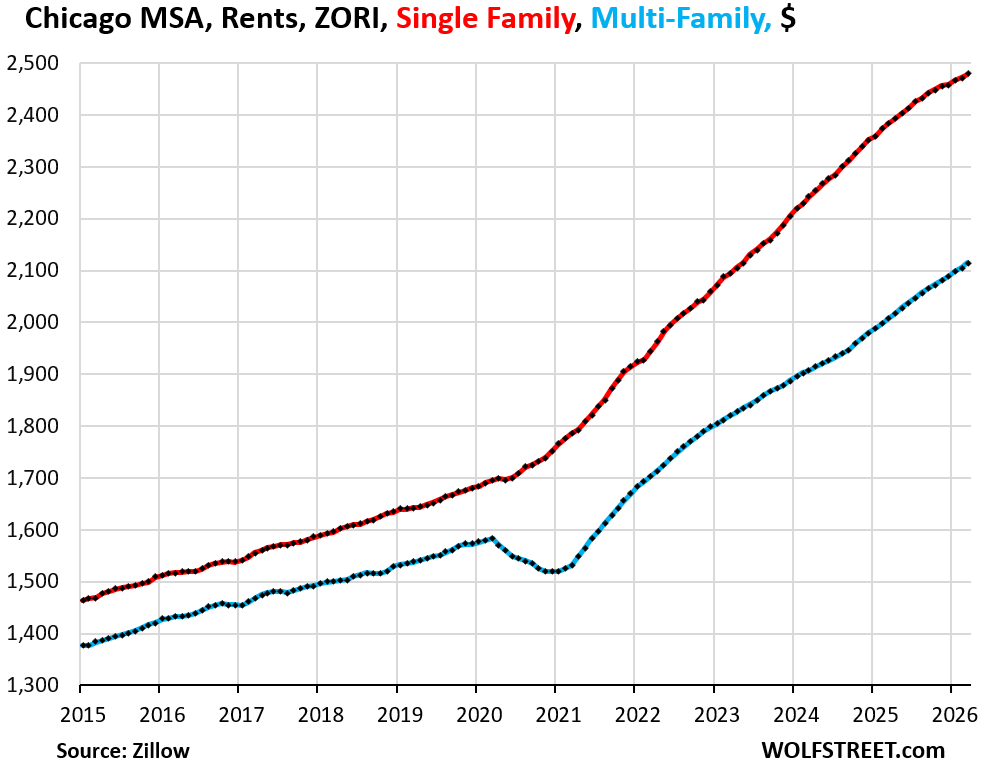

Chicago metro:

- Multifamily ZORI: $2,115

- Month-to-month: +0.5%

- Year-over-year: +5.4%

- Since Jan 2020: +38%

- Single-family ZORI: $2,479

- Month-to-month: +0.3%

- Year-over-year: +4.0%

- Since Jan 2020: +51%

Difference between multifamily and single-family rents: 17%.

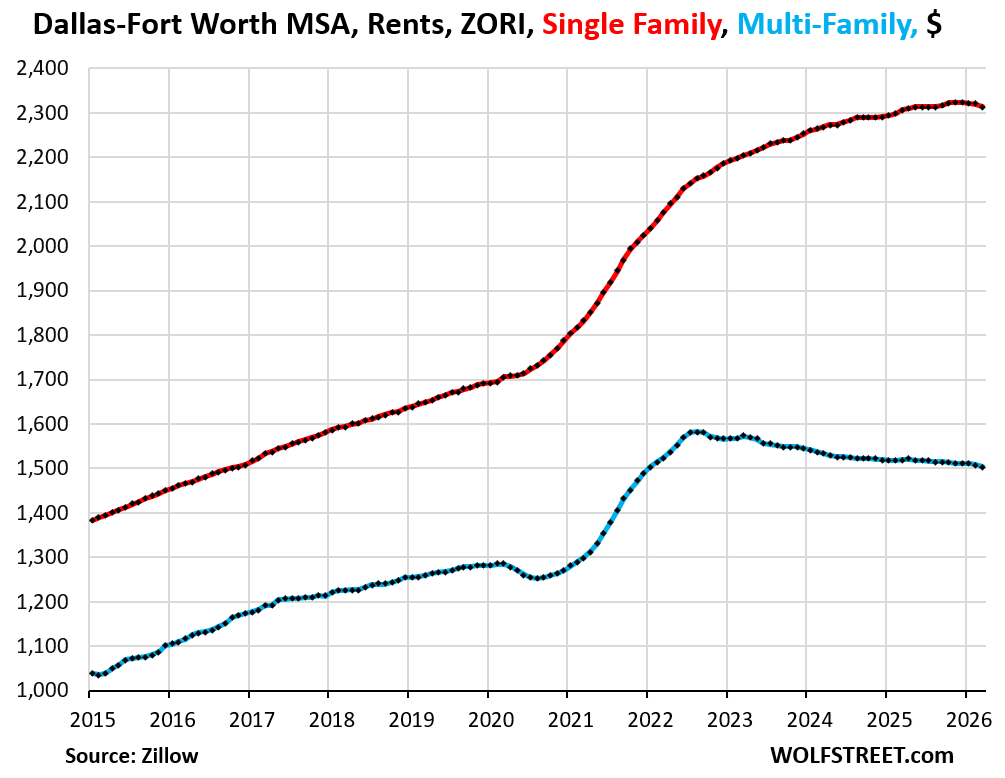

Dallas-Fort Worth metro:

- Multifamily ZORI: $1,505

- Month-to-month: -0.2%

- Year-over-year: -0.9%

- Since Jan 2020: +20%

- Single-family ZORI: $2,313

- Month-to-month: -0.3%

- Year-over-year: +0.3%

- Since Jan 2020: +41%

Difference between multifamily and single-family rents: 54%.

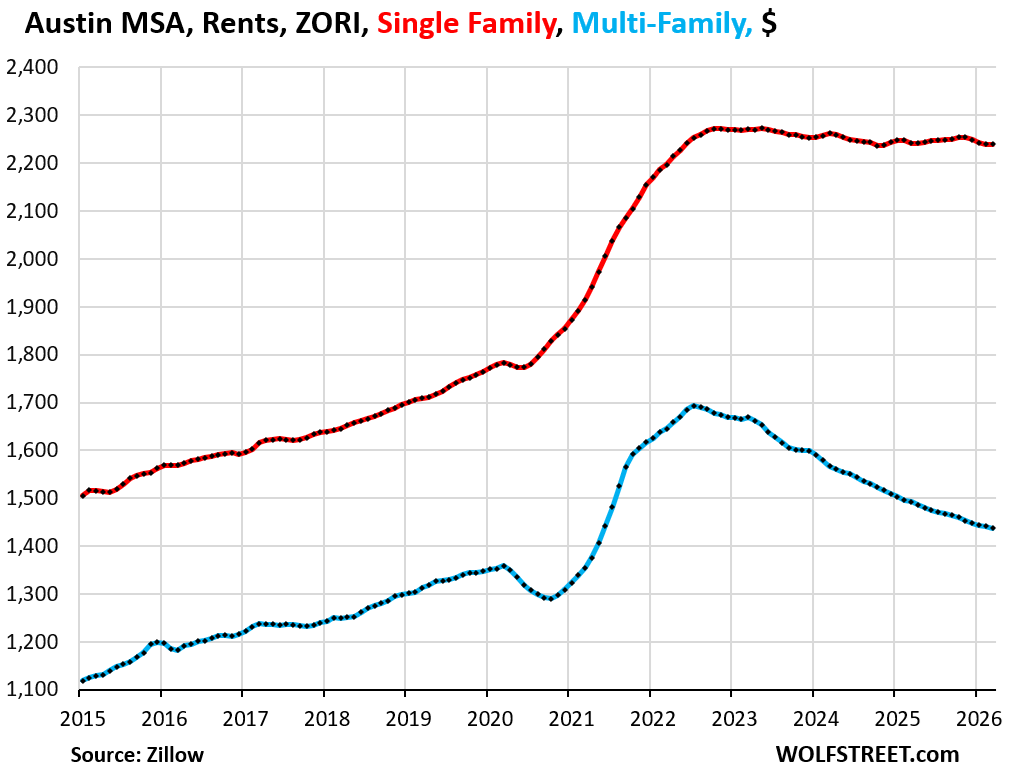

Austin metro:

- Multifamily ZORI: $1,437

- Month-to-month: -0.3%

- Year-over-year: -3.7%

- Since Jan 2020: +10%

- Single-family ZORI: $2,313

- Month-to-month: -0.3%

- Year-over-year: +0.3%

- Since Jan 2020: +41%

Multifamily is under serious downward pressure amid an onslaught of supply, while single-family rents are easing only gradually, and the difference between the two has exploded to 56%.

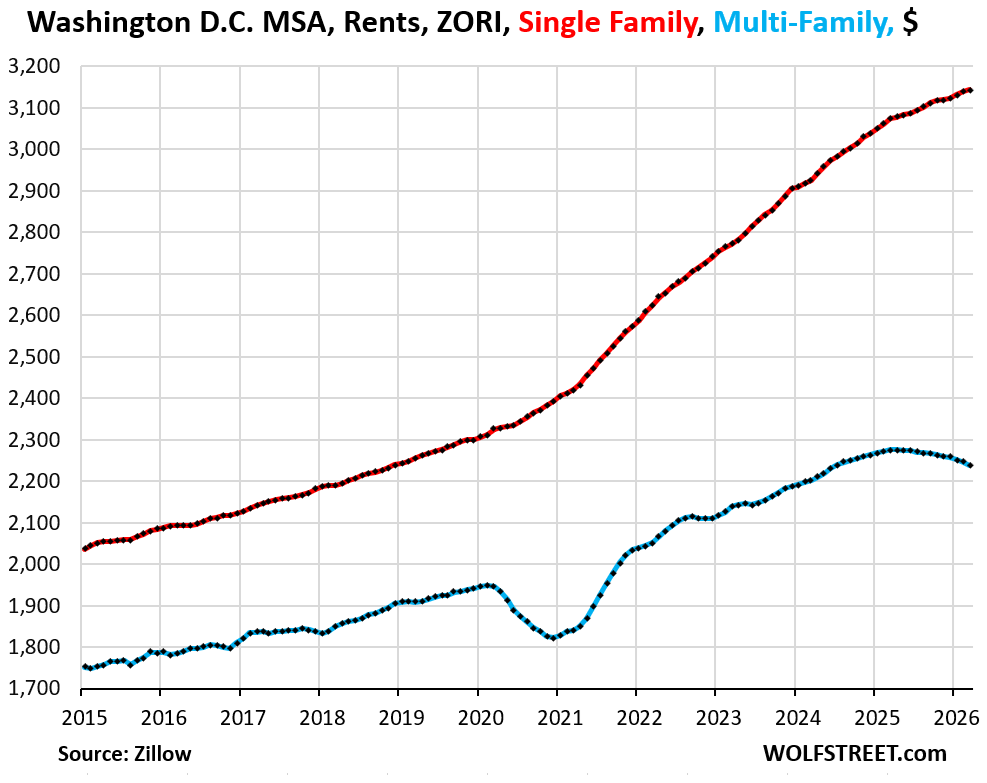

Washington D.C. metro:

- Multifamily ZORI: $2,238

- Month-to-month: -0.4%

- Year-over-year: -1.6%

- Since Jan 2020: +17%

- Single-family ZORI: $3,144

- Month-to-month: +0.2%

- Year-over-year: +2.3%

- Since Jan 2020: +40%

Difference between multifamily and single-family rents: 41%.

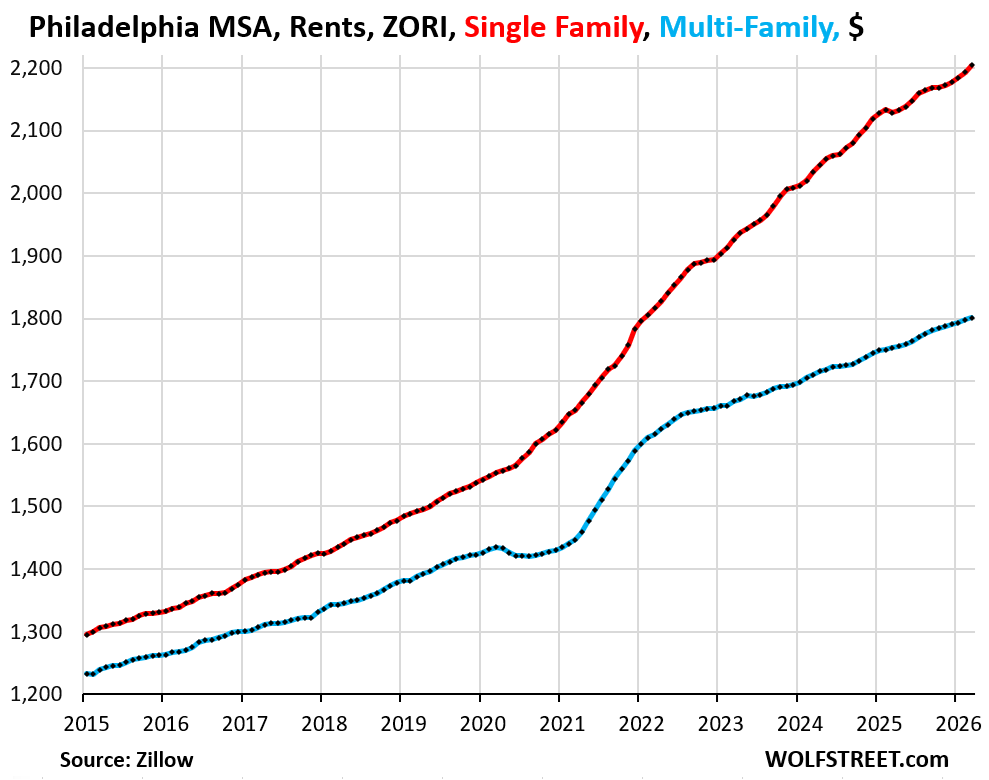

Philadelphia metro:

- Multifamily ZORI: $1,801

- Month-to-month: +0.2%

- Year-over-year: +2.7%

- Since Jan 2020: +30%

- Single-family ZORI: $3,144

- Month-to-month: +0.5%

- Year-over-year: +3.6%

- Since Jan 2020: +49%

Difference between multifamily and single-family rents: 22%.

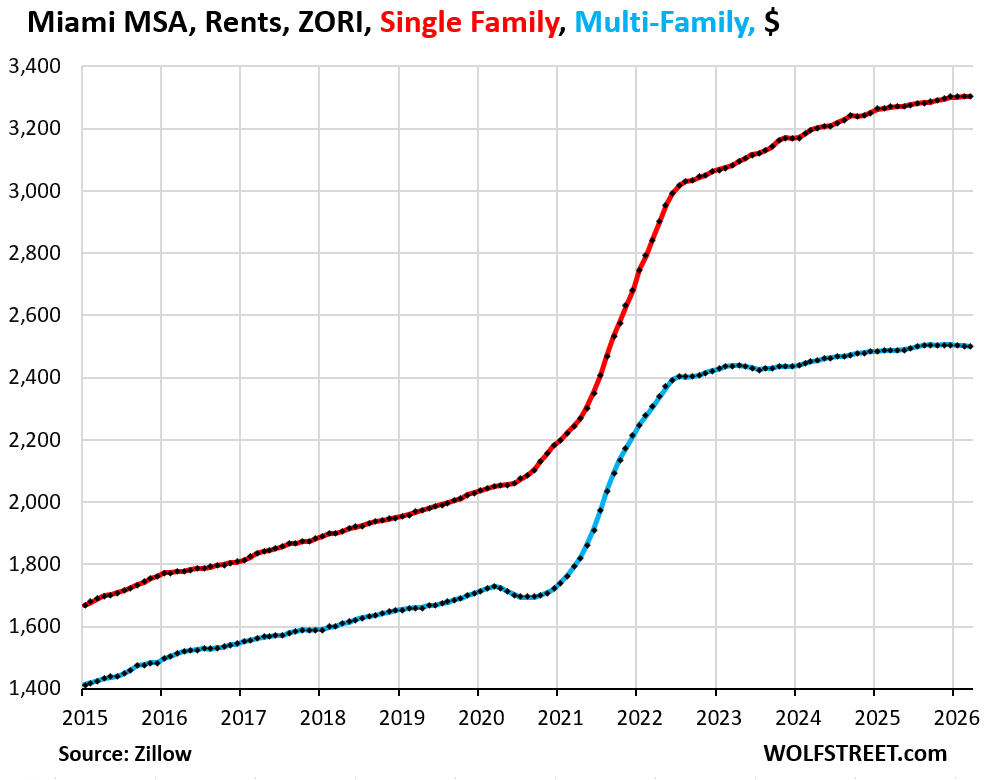

Miami metro:

- Multifamily ZORI: $2,501

- Month-to-month: +0%

- Year-over-year: +0.5%

- Since Jan 2020: +51%

- Single-family ZORI: $3,303

- Month-to-month: +0%

- Year-over-year: +1.0%

- Since Jan 2020: +69%

Difference between multifamily and single-family rents: 32%.

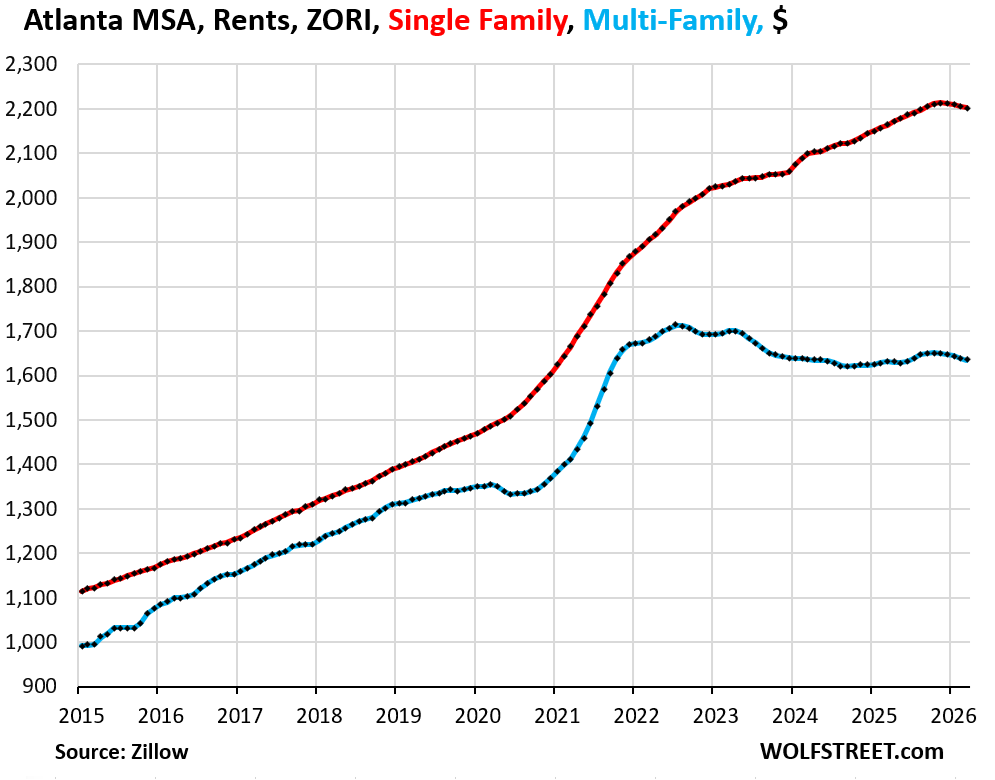

Atlanta metro:

- Multifamily ZORI: $1,635

- Month-to-month: -0.3%

- Year-over-year: +0.2%

- Since Jan 2020: +25%

- Single-family ZORI: $2,204

- Month-to-month: -0.1%

- Year-over-year: +1.9%

- Since Jan 2020: +58%

Difference between multifamily and single-family rents: 35%.

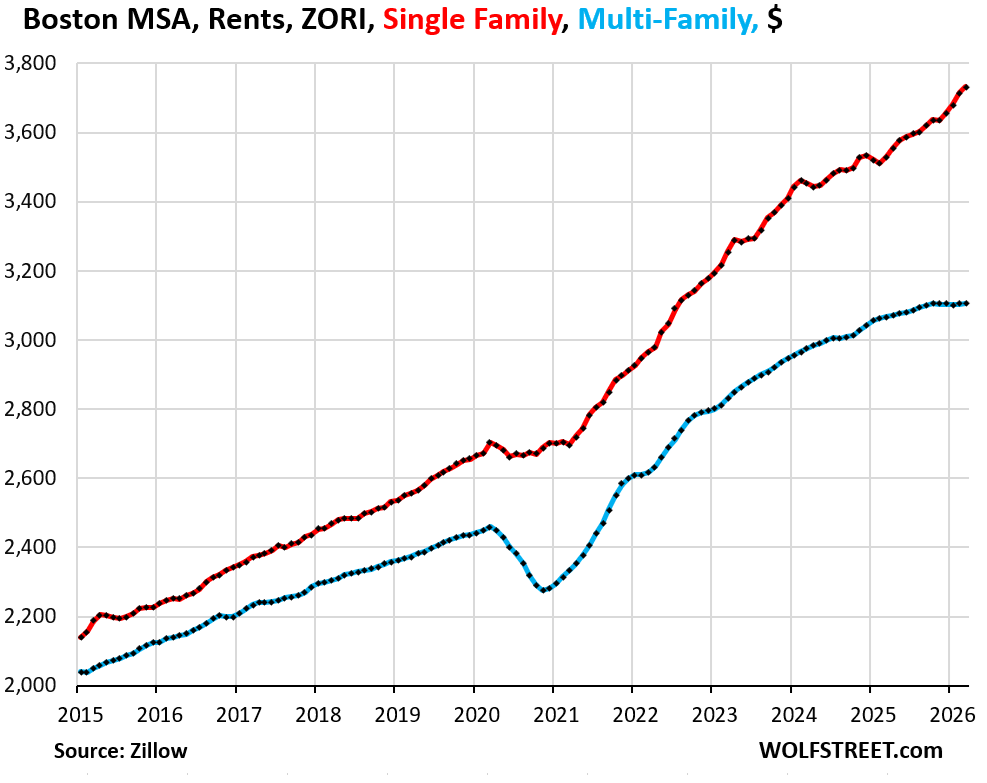

Boston metro:

- Multifamily ZORI: $3,105

- Month-to-month: +0.1%

- Year-over-year: +1.2%

- Since Jan 2020: +31%

- Single-family ZORI: $3,733

- Month-to-month: +0.5%

- Year-over-year: +5.7%

- Since Jan 2020: +47%

Difference between multifamily and single-family rents: 20%.

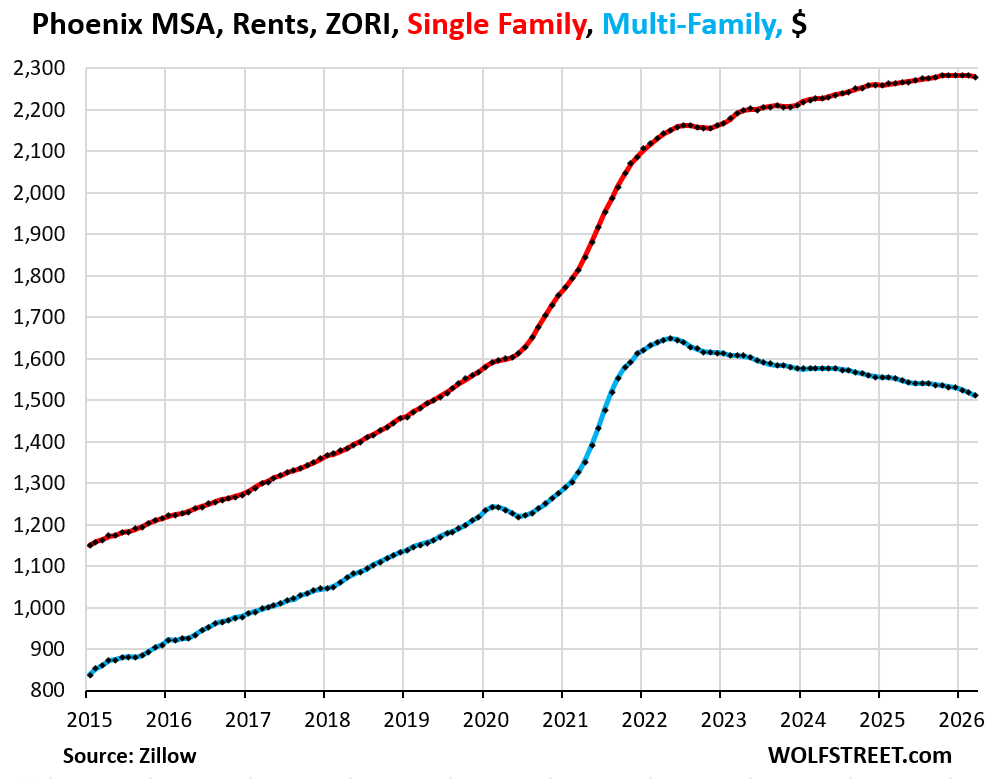

Phoenix metro:

- Multifamily ZORI: $1,513

- Month-to-month: -0.4%

- Year-over-year: -2.6%

- Since Jan 2020: +33%

- Single-family ZORI: $2,280

- Month-to-month: -0.1%

- Year-over-year: +0.7%

- Since Jan 2020: +56%

Difference between multifamily and single-family rents: 51%.

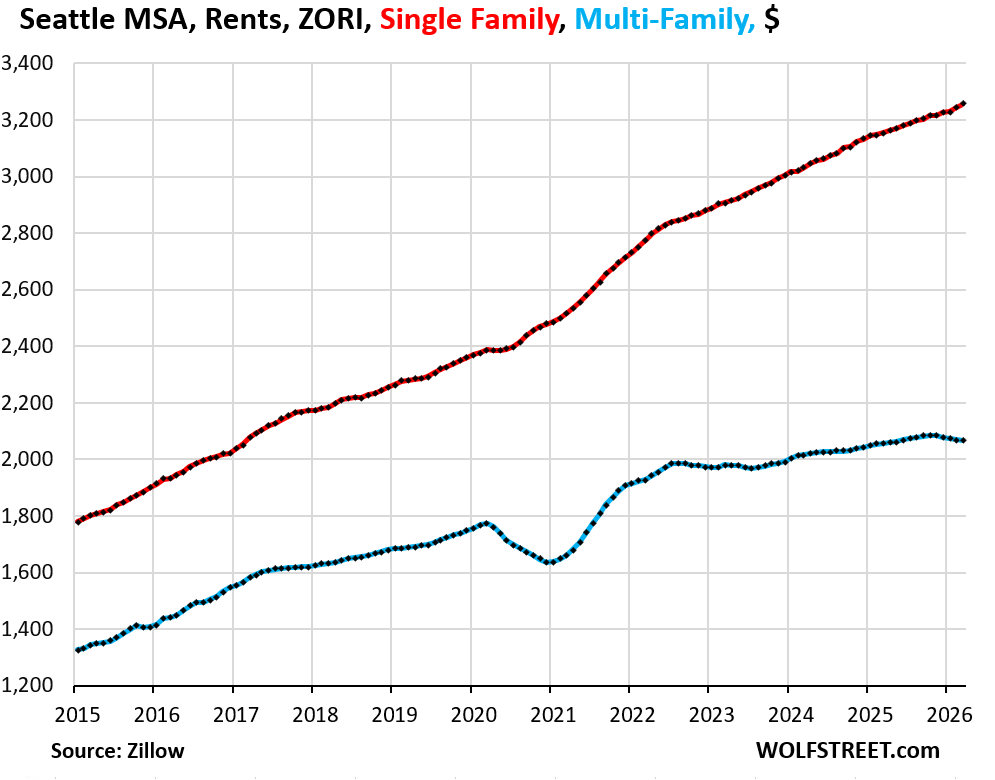

Seattle metro:

- Multifamily ZORI: $2,066

- Month-to-month: -0.2%

- Year-over-year: +0.5%

- Since Jan 2020: +23%

- Single-family ZORI: $3,256

- Month-to-month: +0.3%

- Year-over-year: +3.2%

- Since Jan 2020: +44%

Difference between multifamily and single-family rents: 58%.

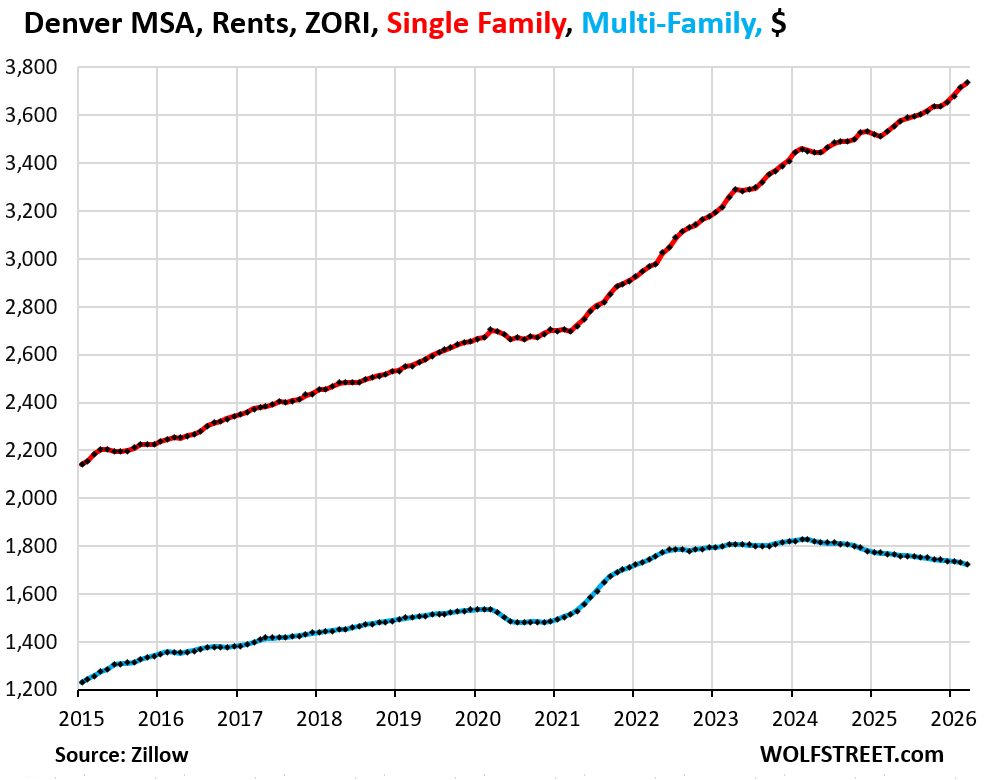

Denver metro:

- Multifamily ZORI: $1,725

- Month-to-month: -0.4%

- Year-over-year: -2.4%

- Since Jan 2020: +16%

- Single-family ZORI: $3,256

- Month-to-month: 0%

- Year-over-year: +0.9%

- Since Jan 2020: +37%

Difference between multifamily and single-family rents: 71%. Mid-tier single-family rentals in the Denver metro are nearly as expensive as in San Francisco. Multifamily rentals are over $1,200 cheaper than in San Francisco.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thank you Wolf. This is helpful. Where would a townhome show up in this data? SF?

A typical townhome would be single-family. They should be called single-family attached, which would clearer. The Census Bureau has a definition: a single-family that is attached but separated from neighboring units by a ground-to-roof wall.

Modernish codes are in place and enforced to require the wall separating units to be a four hour fire wall…

Not to sure when this requirement started, and it has been clear that some of the older rehabs we have done did not have any fire separation, both residential and commercial.

Vintage…

Fire wall upgrades are a pain in the ass for owners, but they are very helpful for fire fighters and the neighboring residents.

It is kinda like paying for a pseudo insurance.

The Fire Codes have been formulated due to past fire accidents.

Granted it is a pain for owners…

But in the long run, the “intention” is to prevent catastrophe for all.

If you rent out a home in coastal California, you re renting ar a discount to purchase price, high taxes both income and property tax, sky rocketing insurance costs, laws favoring tenants in any non payment ir other litigation. If you decide to sell landlords must pay to get tenants to move. So profitability depends on which state your in, a socialist state or a state that values property rights for the people who invested heavily in their homes. We’re mainly talking about single family homes vs apartments which are primarily income rentals. Single family homes should rent for a much higher cost relative to apartments. California landlord of both.

I wish CA were a socialist state. Then the hyper rich capital holders would actually be paying higher taxes than us lowly W-2 employees. Alas, maybe someday.

“The rents are just too damn low!”

Google AI quoting Wikipedia: “Elizabeth “Lizzie” Magie invented the precursor to Monopoly, called “The Landlord’s Game,” in 1903 to demonstrate the negative aspects of concentrated land ownership. While Charles Darrow was credited for decades as the inventor after selling the game to Parker Brothers in 1935, he actually popularized a version derived from Magie’s original concept.”

This is such an interesting KPI wolf.

Clearly shows the people holding onto houses cause they can’t “get the right price” then deciding to rent them out are getting absolutely knee capped by the folks who’s job it is to be in the rental business.

Foothills Denver here. One of my staff just switched apartments earlier this year to the nice cherry creek area. They gave him 6 months free and it was cheaper than his renewal by 200 or 300 in arvada.

Vacancy’s piling up around…

I lived in Lakewood, CO, about 7 years ago and I had friends who lived in some of the brand new apartment complexes in that area. Friends were able to get ok prices because they negotiated but for the most part the complexes were only a 1/4 full with almost empty parking lots (it was weird to drive up to) and still asking outrageous prices. Doesn’t sound like much has changed

Wolf, that would be like moving from Concord to Tiburon:)

I sold my home in Cherry Creek north in 2024. I keep up with it on Zillow. The sale estimate is still dropping thru 2026..

Yeah everything in Denver is dropping. The big complexes lots of free rent deals and they kinda look like ghost towns. The single family you see them list high and slowly drop the price as it doesn’t rent. Still a ways to go before it matches local incomes.

@wolf I’m curious with those metrics what is being compared, is it 2 bd multi family unit vs 2 bd sfh? Or is it just a multi family unit typically 1-2 bd versus a sfh which is typically 3bd or more.

Single family rentals are scarce relative to multifamily, and it’s a different clientele seeking single family than multifamily. A lot of the single family renters are people who otherwise would buy a home but perhaps sitting on the sidelines. Many of these people have assets and good jobs and even children. One thing I’ve noticed about single family homes is that renters in them can be displaced easily by the owner wanting family occupation. A lot of the multifamily units are seeking long-term renters and less risk of being displace for family use. Just my observations.

When you rent a SFH for your family and want some stability, you usually can insert options to renew in the contract for no extra fee. If a landlord won’t do it, it says a lot about the landlard’s intentions and your risk of lease termination.

From my observation (sample size 4 different landlords who each own several rental homes), the majority of tenants who rent homes are financially irresponsible. They have the income to qualify for a mortgage, but they have negative savings, i.e., zero money for a down payment.

Sounds like you need to check out higher-end rentals.

You might be right. My observations are rentals in the expanded Silicon Valley area mostly 2500 square-foot, four-bedroom, tract homes homes being rented to lower-middle management employees at places like Intel, Nvidia, Apple, Gilead, etc. They are definitely not the Palo Alto, Ladera, Portola Valley, Atherton, Woodside, Los Altos Hills locations.

… Or they’re just renter’s by choice.

We are renting a SFH, after selling our house and moving in 2022, because it’s vastly less expensive to rent than to buy in my locality at current prices and interest rates.

I have AT MINIMUM, $1,000 extra per month to invest, spend, save, whatever. Factor in repairs/upgrades and there is easily $2,000-$3,000 back in my pocket each month by NOT being a homeowner.

I have zero debt and will never own a house again if prices remain where they are currently. At this point, why would I want to put a whole bunch of cash into an illiquid asset? My kid is eligible to leave the house in 11 years. If we want to move to a location with cheaper property taxes and a lower cost of living due to crappy school systems — because at that point I WON’T CARE — why would I ever want to try and sell a home into the tsunami of boomer homes due to be coming on the market and probably not getting my investment back?

Unless you can really, truly say you’re going to be in one location for 20-30 years right now (how could you ever know?!) the math in most places favors renters.

Is Uncle Buffy still big in the trailer park market?

Berkshire Hathaway owns Berkshire Hathaway HomeServices, one of the larger real estate brokerages. It also markets US homes in China to Chinese buyers through a partnership with Juwai.

Berkshire Hathaway also owns Clayton Homes, which is a producer of manufactured housing, including manufacturing mobile homes. I don’t think Berkshire Hathaway owns the “trailer parks,” the real estate that these mobile homes sit on.

The big money for Buffett and BRK is not owning trailer parks or selling mobile homes, the major profits are from financing the mobile homes. Their financial practices would make the Genovese crime family envious. The entire business is built on low-IQ employees exploiting even lower IQ customers. It’s amazing to me to see how many of my grade school and high school classmates become frat-boy alcoholics and eventually end up in the various parts of the subprime debt business. Alas, many died in their fifties after long stretches in rehab.

All subprime lenders get accused of the same stuff by the braindead clickbait media. But they’re lending to people who refused to pay prior debts and obligations, which caused their credit rating to get cut to subprime, and they’re very high risk with huge default rates, and many of them don’t mind stiffing their lenders and landlords. So when someone lends to them, they have to ask for massive interest rates, prices, and fees so that they can stay in business despite the huge credit losses. Many subprime lenders blow up — several big subprime auto lender-dealers blew up last year. We talked about it here. It’s a risky stinky business, not for the squeamish, and these dealer-lenders need to be compensated for taking those risks inherent when 15% or more of their customers default. If people take care of the debts, and have a credit score of 800+, they can buy a trailer home with enough money down, and finance the rest with a decent rate at a credit union. Many people do that. But subprime lending is a specialized sordid business. So let’s stop subprime lending, and then these people cannot borrow at all, neither to buy a home nor to buy a car or get a credit card or whatever? And then the braindead clickbait media would wail that oh these poor people are cut off from borrowing and cannot even buy a house or a car!!!

Good points. One of my clients was a national repossession services company. It was a sad business all around. Everyone was sad/mad. The debtor lost his car. The bank lost its loan and incurred large expenses for repo and auction, and the courts hated the paperwork. I used to be laissez-faire about lender-borrower agreements, but having witnessed the collection/recovery process, I can see that this is a dead-weight loss on the economy. Let’s face it, irresponsible people shouldn’t have credit, and neither should people who don’t have the mental capacity to understand contract obligations. If people couldn’t get loans for new cars, then they would be forced to buy lower priced used cars. And if there was less money available to loan to borrowers for used cars, then those cars would cost less. Plus, fewer new cars means fewer tons of CO2 emissions. Finally, fewer tow trucks trolling the streets trying to find repos also reduces greenhouse gas emissions.

Interesting that Austin’s MF prices seem to have dropped below their long-term growth trend.

It is funny how people treat housing (and a small number of other very expensive industries) the *exact opposite* way they treat 90%+ of industries.

Rapidly developing technology is expected in 90% of cases to **make things cheaper** due to increased efficiency.

But the most expensive (and arguably abusive) industries (like housing, health care, and education) get a mystery pass – their relentless inflation has been internalized as “normal”.

Whither tech improvement/increased efficiency? Apparently the worst industries are magically immune from the benefits of increased human knowledge…

Small landlord here. I don’t believe existing SFH or existing small multi family rents have even begun to catch up with the increase in costs of ownership and maintenance. Roofs that were 20K before the Covid over reaction are now 35K. I just got a quote for exterior paint on a small house, 17K. There is just no way to recoup these costs in the form of a rent increase in a ten year time frame, they are just too high. I now say to my tenants, “if you think renting is expensive, wait until you try owning.”

Looking at the cost of construction of new SFH and/or small MF, I can’t see how they are renting for what pencils out to be a short term profit. A lot of existing rents are stuck at 3 yr old or longer prices with long term tenants, well below current market prices and below hidden costs of ownership. A lot of small Mom and Pop landlords are going backwards, and don’t even know it by failing to raise rents fast enough. Raising rents on existing tenants is hard, and having them move out and turning over units is expensive. No where to go but up.

The line between landlords and general contractors is blurring. In other words a landlord can be more successful if they hold a contractors license and can hire subcontractors. Buying the materials first, like roofing shingles and and drip edge flashing, then hiring a sub to perform the tear off and install can be much cheaper, if you’re willing to learn that skill.

Yes, cost of maintenance is way to high. It depend on your location.

What city are you located?

Jim, you’re saying “There is just no way to recoup these costs in the form of a rent increase in a ten year time frame, they are just too high.”

As a veteran owner, I’d like to offer some wisdom.

First, I bet you can get a much cheaper paint job. We just repainted here in a high-cost area for <$5/sf. You can also get a 10-20% discount by waiting until the painters are in their slack season, not the busy summer selling season.

Next, the roof: that's a 30-year item, not 10 years. $35K over 30 years, with interest, is about $200/month. Just raise the monthly rent by $50, every 2 years, for 5 cycles and you're fine.

Finally, let's talk about maintenance reserve accounts. Now that rates aren't zero anymore, it's more profitable to set up a reserve account for maintenance and replacements. Paint and roofs don't last forever, and it's not that hard to forecast – to within a couple of years – when they'll need replacing. Ditto for other items that wear out.

Many property owners set aside some of each month's revenue to cover those expected future expenses. They're earning interest on that money until they need it, instead of having to borrow for repairs.

So we should add $50 a month for a roof, then whatever else monthly for everything else, and where exactly does adding to our profit come into the mix? We didn’t buy houses so that we could make sure roofing companies stay profitable.

Older buildings are money-sucks. Which is why many rentals have endless amounts of deferred maintenance, where only the absolute minimum gets fixed, if that. The price you pay for an older building is the purchase price plus the cost of deferred maintenance.

Yeah, being a SFH Landlord right now is a lot like being a condo owner in Florida. There are lurking large deferred maintenance items. Appreciation used to make up for that but the good days could be over. Ghost makes a number of good points but remember a lot of landlords aren’t in construction management and really can’t get on a ladder or replace a water heater themselves. My mom just got smoked for a $35,000 sidewalk bill to be ADA compliant. This would have been a $1500 DIY repair or $6000 with a legit concrete contractor. The city got involved and the price literally went up five times that. No way to recover that in rents in her lifetime (plus the roof, plus paint, plus property management etc.) Tenants howl like scalded dogs when you raise their rent 35 bucks. See where this is going?

@Tina if you don’t keep the place up it won’t command a decent rent (and might not rent at all in a down market), so your income drops.

And without upkeep, the resale value plunges too.

Profit is always secondary to preservation of capital. When things get tight, your choices are to hang on for now – and wait to make big money in the next boom cycle – or to pull your capital and invest it in a better opportunity.

Most of the profit used to come from appreciation. However if you bought the property before 2022 and locked in a 30 yr rate at 3%, you’re still profiting.

Let me give you an example property I purchased in mid 2021. Class B neighborhood 15 year old home purchased for $650k, ~60k spent on rehab with entire interior replaced(flooring, cabinets, counters, appliances, shower doors, etc), HVAC replaced, repainted, low maintenance landscaping. The only thing that wasn’t touched was the tile roof, which is probably good for another 15 years or more.

I put 20% down, so my total cash outlay was just shy of 200k. 30 year non-QM(agency loans would’ve been cheaper but I had too many loans already) interest only loan at 3.5%. Hard costs are $1500 a month mortgage, $100 insurance, $700 property tax, $150 HOA, plus a repairs capital reserve of $400 for a total of $2850. So far, I’ve needed to repair nothing except a broken sprinkler head after 5 years.

I’ve rented to the same tenant since 2021, their current rent, which is still below market, is $4500 a month. So I’m netting $1650 cashflow with the repair reserve and $2050 without.

While my costs are lower because I like to find value add and I know subs who do quality work without the contractor markup, your math buying that property fully rehabbed but at a lower rate of 3% wouldn’t be too different from mine.

This is why there are so many accidental landlords who are comfortable and seemingly refuse to lower their price and sell. Their rates were so absurdly low even luxury homes that are normally terrible rentals are still in profit. A 2.5m home bought 5 years ago with a 2.5% mortgage is currently costing about 6700 a month in mortgage interest, insurance & taxes. I see these renting for about $8k a month. While they’re cashflow negative, principal pay down is building a lot of equity every month.

And this is with COVID home prices. If you bought the home before 2020 and refinanced, your cashflow is even higher. Idk about other parts of the country but here, the rental math is still very strong and why homeowners are refusing to lower prices and just turn their homes into rentals if they can’t find a buyer.

@John

Your cash on cash rate is about 10%. That same money put in the S&P would have earned significantly more. So there’s an opportunity cost for accidental landlords.

Also in many cities here’s why accidental landlord doesn’t work:

1. Falling home prices. In Denver a $650k home would have lost ~$30k in equity last year offsetting any income and then some.

2. Falling rents. If you haven’t had tenant turnover you may find a very different market now for what people are willing to pay depending on the market you’re in

3. Not applicable to you, but someone who bought awhile and has a lot of equity is giving up their capital gains deduction which could be a 6 figure loss. And yes you get deprecation but that’s recaptured when the property is sold. If you have no appreciation nbd, but the more appreciation the more of a choice that is.

Tina: your profit might come from adding value to the property. Maybe that’s through tasteful renovations that make the place more livable, and stand the test of time. If the extent of the investment is calling the first large contractor outfit on Google or Homeadvisor, you can’t be too surprised when the contractor pulls all your equity into his bid.

Also property taxes and insurance has skyrocketed. It used to take 2 months of rent to pay. Now it’s 3 1/2 months of lost rent for both. I make a better return in the SM and haven’t invested in SFH’s since 2020.

If your roof replacement costs $35k and exterior paint costs $15k you’re heavily overpaying. You need to cultivate relationships with subcontractors, it’s much cheaper that way.

I just got a house painted both interior and exterior for 8k, and this is in southern california with correspondingly high labor costs.

John,agree,this is coming from a carpenter.

You want a even better deal while not able to write off without some finagling you pay contractors cash/pull homeowner permits if needed you can get some good quality work for a fair price.

Yep the subs are happy and you’re happy. The contractor is paying them 1/2 as much as you are and taking all the profit.

For the painting job I mentioned it was 2 guys who spent 4 days taping and spraying. I bought the paint(it was roughly $1k) and they made $1k per day, far more than they make working for a contractor.

Respectfully, in the growing area where I live, there is no “finagling” on price. Legit guys have jobs in the pipe, if you offer them less they walk back to their 90K diesel truck and drive away . Marginal guys do marginal work, and you are left with shitty work, and a fight. If you pay cash it’s a 15% premium on you because they don’t want a 1099 NEC. I do all the work I can myself, but I can’t hang gutters 40 feet off the ground. Pay up, rents up. I’m still raking it in because my cost basis is mostly 20 years old. My point is, it can’t last. A few small creative landlords can work the margins and be proud of it, otherwise no where for rents to go but up.

To the people who don’t have any concept of cost regarding painting and roofing are just plain stupid. It costs miniaml 22k to cover a small roof here in pdx

Right. Or get a fly by night guy to do it and watch the paint come off in 5 years, or your no inspection roof starts leaking and they are long gone. Increased costs lead to increased rents, or your just working for your tenants.

I’ve heard that median and mean can diverge when there’s higher prices. What are these numbers? I searched the article for mean, median, average. Just curious

These data here are neither median nor mean. I hate those two methods for real estate. Mean (average) is worst, because it’s distorted by outliers; median is second worst because it’s distorted by shifts in the mix.

This data here is based on repeat-rent data which tracks the same property listed for rent at different points in time, and compares the differences of those repeat listings. It is then weighted to the rental housing stock to ensure representativeness across the entire market, not just those homes currently listed for-rent. It then chooses mid-tier of this resulting data, so the 35th to 65th percentile range which avoids outliers and shifts in the mix, and computes from that the mean dollar-denominated index.

Landlords are getting butt kicked. Every expense line item keeps going up, insurance, prop taxes, rates, materials, labor, list goes on and on. With no real rent growth since 2022. RIP cash flow.

I think the trades are raking it in. These fuel prices are prob killing them right now though.

I agree that expenses(taxes + insurance ) and future expenses( roof, appliances, HVAC, painting, etc) have risen dramatically since 2020.

Rent also increased dramatically from 2020-2022 before now flattening.

However, if someone purchased a rental before 3019 and refinanced at <3%, they had a huge rental income windfall. They are probably still making a profit every year but smaller. I hope the landlords saved some of the windfall for a rainy day when the roof leaks.

Anecdotally, that is the majority of landlords that I know. My son is paying 1/2 in rent of what it would cost to buy the same house. The landlord bought in 2005 so is still making a nice profit even with increased taxes, insurance and maintenance.

Looking at Wolf’s excellent charts, rents have to go up or house prices have to go down to restore some equilibrium in the Mom and Pop landlord market growth. I doubt many bought a house to rent out between 2022 and now. It wouldn’t make sense in most areas.

No reason to feel sorry for land lords. Especially those that purchased prior to Covid. Feel bad for all the kids that can’t afford to buy a home.

You didn’t expect costs to go up after we adopted a zero-tolerance policy to immigration? This was inevitable.

In the saltwater cities rent is rising. Landlords: where can they go. In the flyover areas demand destruction sent the multi down. Some multi have townhouses. Turnover is rising in the 1/2 BR and the townhouses.

I live in a sfr

If given an opportunity id happily rent a condo

Sfr has too many expenses if I count mine in the last 15 years

If I had to guess on a reason, it is because they were building apartment buildings like there was no tomorrow for a while but not houses. At least where I live.

So you’re telling me I should build SFH – off to the permitting office.

What are the average sizes of the homes and apartments? For example, are they both 3 bedrooms / 2 baths around 1200 square feet?

They’re “mid-tier” (in the middle third) by price in their market, as explained in the article. Same with single-family rentals.

I once had an 1,800 square-foot high-end condo, with 1 huge bedroom with big bathroom and walk-in closet, 1 smaller bedroom, an additional bath, 1 great room with open kitchen and big counter and a dining area for a table that sat 8. So a “2-bedroom 2-bath.” Meaningless. But it was not mid-tier.

So are two categories evaluated separately for tiers?

I mean I’m not surprised Denver’s middle third of sfh would be priced significantly above the middle third of multi family units. There’s an insane amount of large suburban houses that can’t get what they want when they’re trying to sell, so now they’re trying renting. We’re likely comparing significantly different bedroom counts and sized units….

As more houses don’t sell and get turned into rentals I’d expect that middle tier of sfh to keep getting pulled higher, despite actual dropping prices. If you look at specific sized homes in specific neighborhoods rents are dropping significantly. Over the last year as friends have moved out of their rentals I’ve watched their landlords not be able get the same rent and repeatedly cut. For sfh one friend paid $3500 for a lease signed in 2021 last I saw the landlord had dropped the asking rent to $2800, not sure if it rented. Another paid $2200 and that one rented for $1800. Another was paying $3000 and that rented for $2800.

Thing is in 2019 the first place would have rented for 2200-2400, the second place would have rented for 1800, and the third would have rented for $2000-2200. So there is a very long ways to go pricewise.

I can’t reply to your other comment for some reason, so I’ll put it here.

Regarding stock market returns, most of that is in appreciation. You can’t compare that to cashflow from a rental – especially given the tax deferred nature of rental properties using the depreciation schedule.

On that property I have $180k in gains from appreciation. Now there’s selling costs involved, so call it $130k. That’s still better than the S&P. Yes appreciation is not guaranteed, but clearly that’s true for the stock market as well.

I have a lot of dividend investments as well and the closest comparison to this are BDCs which pay around a 9% yield. Except I pay extremely high taxes on them(top marginal bracket+state tax+NIIT) and there’s practically no appreciation.

1. Regarding falling home prices, surely you will agree the stock market is also subject to falling prices. We can’t have a bull market forever. I only buy in markets with high income growth and a high proportion of NIMBYs that block new construction. In my local market almost all construction are apartments, with very few SFRs.

2. SFR rents are not falling, that’s kinda the point of this article. MFR rents are falling across the nation but SFR is a different market and there’s far less availability in most markets. As I said I’m still charging under market because the tenant has been great.

3. No idea what you mean by capital gains deduction, you mean the homeowner exemption? Let’s be honest, there are many ways to reduce your capital gains exposure selling a SFR.

It’s interesting, but these aggregated figures can also be misleading. As an obvious example, they don’t tell you anything about the underlying mix of property coming onto the market.

For example, in Austin 3-4 years ago there were many large luxury towers that came online in the downtown core with much higher prices. This pushed up the averages irrespective of underlying changes in supply/demand dynamics.

Similarly, the MSA definitions themselves change meaningfully, especially in rapidly growing/declining areas. In Austin, many outlying areas (with lower rents) were added to the MSA in June 2023 as the result of census 2020.

Nonsense.

1. The article tells you that they are mid-tier rents (the middle third) in every market to reduce the impact of shifts in the mix.

2. The article tells you that they’re repeat-rents, so new buildings coming on the market don’t directly impact it. They impact it only indirectly, when these new towers cut their rents to fill their units, the older buildings below them have to cut to remain competitive.

3. In every market, new apartment construction is ALWAYS focused on the higher end. People who want to pay lower rents have to look at older buildings. That has always been the case everywhere. Builders have to target the higher end with their towers because that’s where the money is. These projects don’t pencil out at lower rents.

I am looking at the break down of landlord types and I am curious why the decision was made to split the quantities of homes owned. Im look at the “Mom-and-Pop” (a term which itself evokes certian feelings about the group) being 1-10 buildings. Then the next group is 11-40. Are these standard in this type of housing policy academia?

If you own 10 rental properties, I dont think thats a mom-and-pop style. Im curious to see the numbers more granular, but especially the 4-10 crowd.

Mom-and-pop is a standard expression for small-scale investors. These are standard dividing lines. Data and dividing lines provided by Burn Real Estate, as pointed out in the chart.

I saw a news segment from LA with a so-called expert discussing the housing market. He said many people can’t sell for the prices they think they are worth and possibly have ARMs. They are now trying to rent instead of selling. This is definitely true in Florida where the market is crashing. Most markets for single family homes need a major correction. I know some people will lose money and others will lose paper equity, but that’s the nature of markets. Easy come, easy go.

Anyone have a recommendation for a location that is reasonably priced and for either a condo or SFH … leaning toward condo … some areas that might have corrected a bit but good quality of activities/quiet (not Miami)…

thanks.

If you make your money elsewhere and can live anywhere, and don’t mind living anywhere, look for a cheap city in the middle of the country, such as Tulsa. Condo prices exploded by about 80% from mid-2019 to mid-2024, but have flattened out over the past two years, and are subject to declines, but are still pretty low compared to the big coastal cities. The Zillow ZHVI for a mid-tier condo there is $120,000. Wages are a lot lower too, and there are fewer opportunities, but if you don’t have to work locally, you don’t care about that.

In general, make sure you spend a couple of weeks in the city where you’d park yourself to make sure that’s what you want, such as 100°F-plus in the summer, restaurants, entertainment, etc. In a place like Houston, which is starting to have lower condo prices (mid-tier condos now in the $135,00 range), check if you can handle the swelter, which is not for everyone, especially if you come from a northern climate and like to do stuff outdoors.

https://wolfstreet.com/2026/04/20/condo-prices-dropped-by-12-to-31-in-31-bigger-markets-some-are-where-theyd-been-20-years-ago-such-as-oakland/

Thanks Wolf!

Deportations and self-deportations are increasing, and in-migration is decreasing. This will force rents lower, probably affecting multi-family units more than single-family units. Bovino says there are 100 million illegals in the US. I doubt there is that many, but just removing say 10 or 20 million from the country will put significant downward pressure on rents. It’s a bad time to be a landlord, worse in some areas than other areas.

Hopefully it will force maintenance costs too.

I own a couple of rentals and it seems every maintenance event eats up my entire year of profit or more. The only way I will be making a profit is when I sell and capture the appreciation. There are no loans on these rentals either.

During the past 10 years there has been lots of Luxury Apartments built in my area. I keep thinking there will be a glut soon and wonder how this will effect SFH rental.