Inflation is the bane of the bond market. And it is now demanding multiple rate hikes, starting late this year.

By Wolf Richter for WOLF STREET.

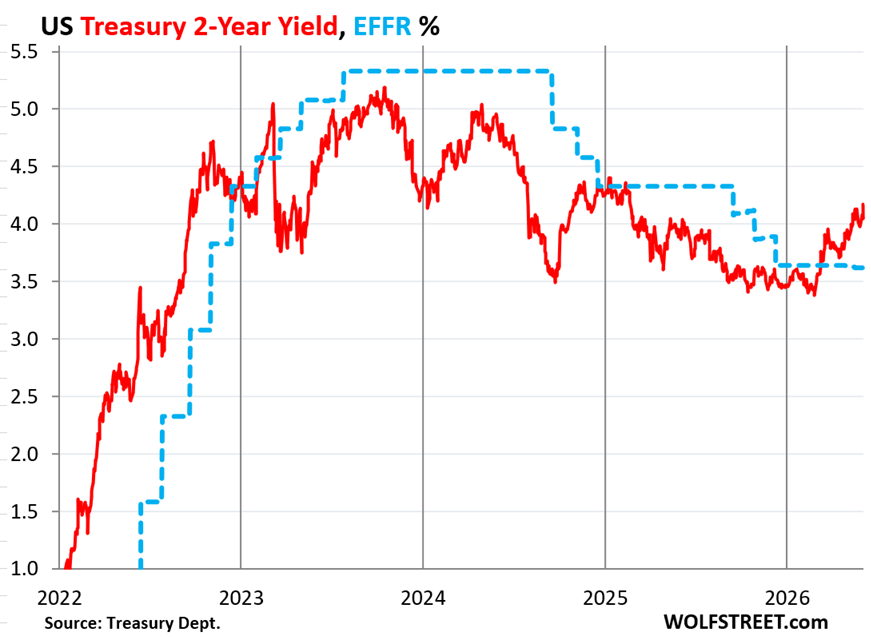

The 2-year Treasury yield jumped by 12 basis points on Friday, to 4.17%, the highest since February 2025, when it was on the way down. Back then, it was anticipating more rate cuts, which came in the fall that year, three of them.

Now it’s anticipating rate hikes – multiple rate hikes. Yields reflect the summary of the vast bond market’s diverse opinions. Since the end of February, the 2-year yield has jumped by 79 basis points, having switched from expecting a rate cut, to expecting multiple rate hikes. It is now 54 basis points above the Effective Federal Funds Rate, an overnight rate that the Fed targets with its policy rates (blue in the chart).

The trigger on Friday was the jobs report which confirmed that the labor market was fine, with three months in a row of substantial job growth, including upward revisions of the prior two months, and with the three-month average job growth at the highest level since March 2024 (my analysis: Job Growth Turns Around Decidedly after Weakening for Years). This labor market data indicates that the Fed can move inflation to the very top of its worry list.

Both measures of consumer price inflation, the CPI and the Fed-favored PCE price index, will likely show that inflation was over 4% in May, double the Fed’s target, and above the Fed’s target for over five years.

Inflation has been rising for months before the energy shock in March even hit and has metastasized beyond the energy shock to other areas of the economy.

Newly minted Fed chair Warsh is going to have a hard time over the next few months persuading a majority of voting members on the FOMC that a rate cut is needed in this environment, according to the Treasury market; and later this year, he may have a hard persuading a majority that a rate hike is not needed, according to the Treasury market.

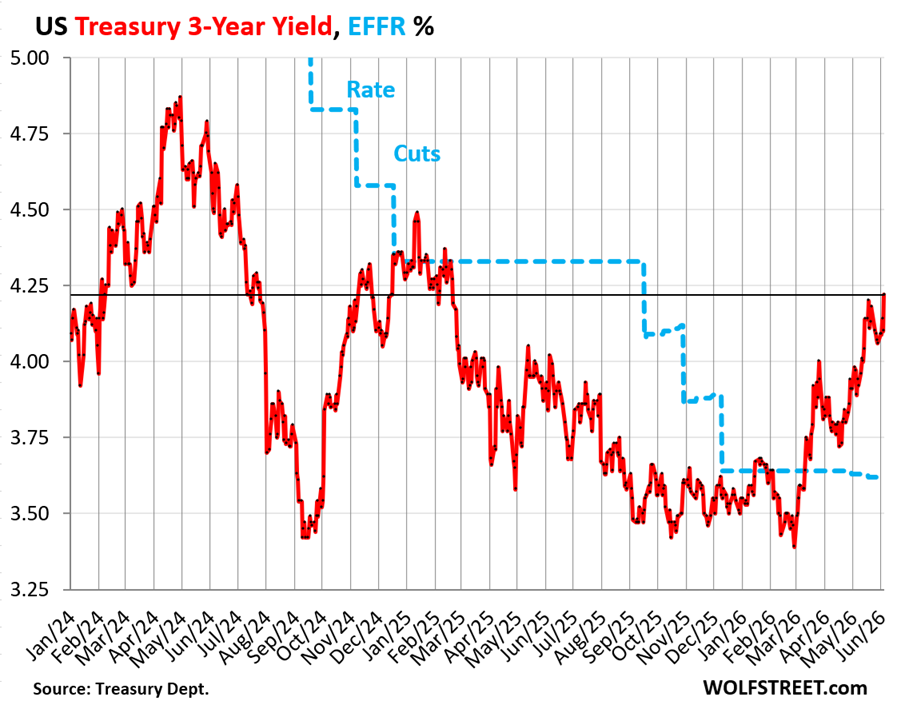

The 3-year Treasury yield also jumped by 12 basis points on Friday, to 4.22%, the highest since February 2025, and up by 81 basis points since the end of February. It’s now 59 basis points above the EFFR.

Higher yields mean lower prices – and losses for existing holders. Bonds sold off.

These movements in the yield indicate that the bond market is not only anticipating rate hikes but is also demanding rate hikes because it’s worried about inflation. The bond market can have a powerful voice.

The CPI inflation rate for May may be higher than even the 3-year Treasury yield. Inflation rates have been higher than T-bill yields across the board for a month.

Here we’re looking at a close-up.

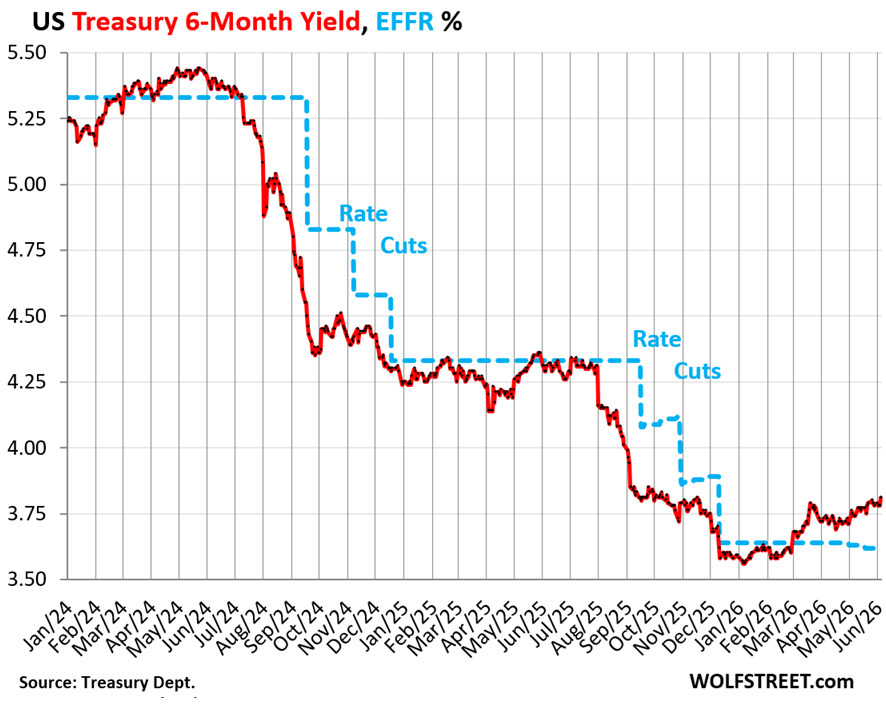

The 6-month Treasury yield, which shows bond market expectations of Fed rates over the next 3-5 months, rose to 3.80% on Friday, 18 basis points above the EFFR, a sign that the bond market is expecting the initial rate hike later this year – not next year.

The bond market isn’t just expecting that the Fed will hike rates – it’s putting pressure on the Fed to hike rates.

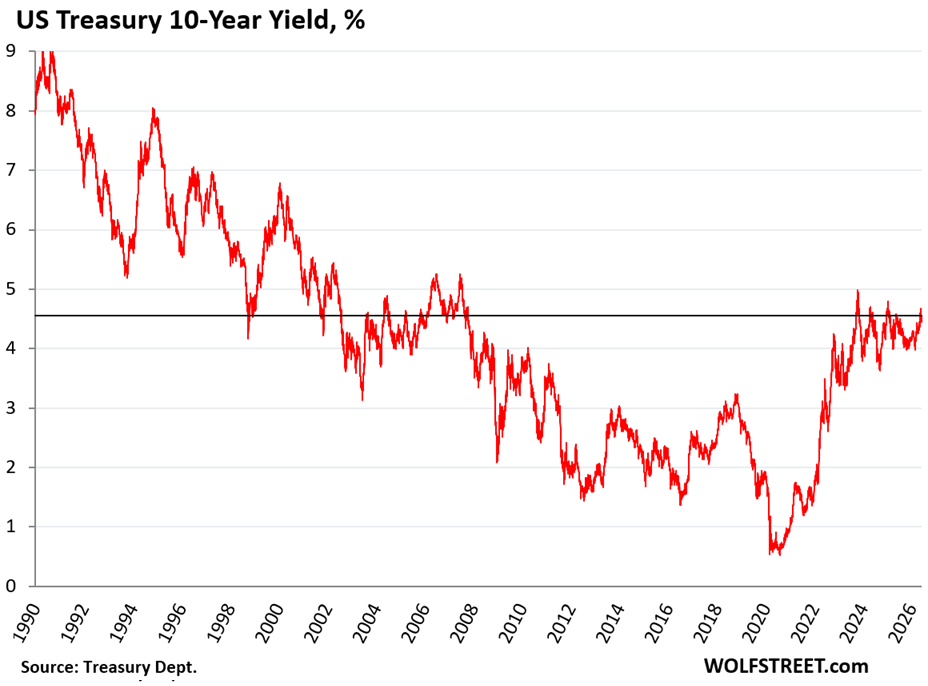

The Fed will have a major bond-market problem on its hands if inflation continues to be twice its target, or more, and it doesn’t deal with this inflation, and just blows it off, claiming that it would “look through” this inflation for a while. That bond-market problem would manifest itself in the long-term yields – particularly the 10-year and 30-year Treasury yields, and they’re already getting restless.

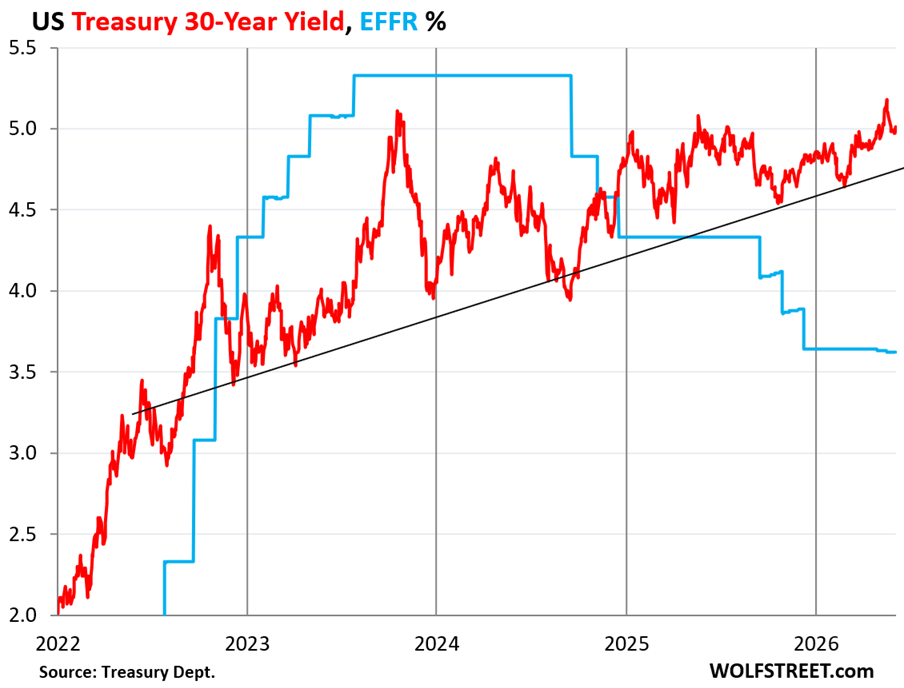

The 30-year Treasury yield rose above 5% again on Friday, after having been just below 5% for over a week. It has vacillated around the 5% line, a little above, a little below since early April. On May 19, it had hit 5.19%.

My imaginary trend line connects some of the lows along the trend of higher lows. The yield-yo-yo has been narrowing for a year as the bond market has been getting more convinced about the direction this is going: There is trouble brewing in the bond market.

Trouble in the bond market is twofold: A recognition that higher inflation, perhaps in the 3-4% range or may higher will be tolerated, if not desired, which means that yields need to rise to remain sufficiently above it. And a fear that the path of the Treasury debt, its growth of over $2 trillion a year, is not “sustainable” – that eventually something has to give, namely whatever might be left of price stability.

The 10-year Treasury yield jumped by 8 basis points to 4.55% at the close on Friday. At this level, the 10-year yield is not high for this inflationary environment — and might be low:

The bond market is still, if half-heartedly, buying the story that long-term inflation will go back toward 2.5% or so, and a 10-year yield in the current range would be about appropriate for that kind of average inflation rate.

But to get an average inflation rate of 2.5% over 10 years while inflation is allowed to go over 4% is going to be tough. And the 10-year yield remains very unattractive at this level, given that the Fed and the government apparently agree on letting the economy “run hot,” with more nominal economic growth, faster wage growth, and higher inflation rates, in order to deal with the huge and growing national debt before it spirals into fiscal chaos.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

When IPO valuations are so absurdly high, they even compete with .gov for liquidity.

wasn’t there prediction that Warsh wouldn’t raise rates

or

did bond vigilantes finally wake up

When Warsh was being talked about as candidate last year, inflation was much lower, but rising slowly. So that was a scenario that has been obviated by events. Now there’s a new scenario of surging and much higher inflation.

The algorithm that has been accepted as gospel is that price is not a reliable indicator of the cost of living as opposed to the obvious logical conclusion that …….

Good analysis of the U.S. Teasury Bond market.

Looking at your 30 year treasury trend line its seems as though a pennant is forming(if you drew a top trend line above—narrowing triangle—technical analysis). A narrowing pennant flag pattern usually points to a break above or below the pennant. I would think a break above is realistic given the current rate of inflation, unless something else happens such as a disinflationary event.

PS, if the bank reserves on loan at the Fed were to move into the US treasury market this would have a negative effect on short term interest rates(down). Warsh has mentioned this and has stated he wants to reduce the Fed’s balance sheet.

I believe Warsh and Bessent want to reduce the Federal Reserve balance to the point they are not able to function as “The lender of last resort” possibly at a time of high demand in the Reverse Repo Market.

That’s patently BS spread by people who don’t know what the Fed is and how it functions. The Fed creates money. Repeat after me: The Fed creates money. Every time it pays for anything, it creates money to pay for it. Conversely, every time it gets paid for anything, it destroys that money. The Fed does not have a “cash” account. If it wants to lend $10 trillion this afternoon, it creates $10 trillion and lends it. Then that $10 trillion is added to its balance sheet as an asset.

The market drop on Friday is what I expected to happen earlier.

Concerns about the interest cost of the U.S. budget will keep increasing.

Buyers of U.S. Treasuries will become increasingly worried that they are going to take big losses in a currency devalution.

Repeat after me;

FRACTIONAL BANKING….

…….whether it is a loan or a nation state’s currency……..

Most busyness’s print jobs/facilities/….(and unfortunately advertising money by avoiding taxes) based on expected (and hoped for) customers……Banks print all the above in addition to loans for busynesses……and yeah, the “special cartel” Fed Bank(s) can print coin of the realm……

So….Round and Round we go, while REAL assets are used up/turned into large mammal pollution (chemical and heat)…….NOBODY CAN PRINT ATOMS…..and “unprinting” nasty molecules is often more work than printing them…….

Look at Ten year and 2 year weekly charts for 5 years. Higher for longer is clear.

You expect price of U.S. Treasuries to fall and the interest rate to break upward ?

If so, I agree.

The extent to which this will happen (rates rise) will depend on a couple things; 1) whether or not CONgress become fiscally responsible (raise taxes, lower spending) 2) how much Walsh is willing to expand The Fed’s balance sheet. Let’s all be honest, the fewer treasuries The Fed buys, the higher interest rates will go.

The massively extraordinary amount of preventable waste in government spending, including exorbitant amounts of fraud wasting tax dollars, should absolutely completely shut the mouths of anyone that says raise taxes. No offense to the poster.

Funny how some amateurs have been insisting since the Reagan era that all deficits are completely caused by “waste” but no one in the last 40 years has been able to document what specifically this so-called waste is (beyond sporadic random items that are trivial on the scale of the national deficit, and magically align with their partisan views on government priorities)

We just had Elon Musk promise to easily evaporate $2 trillion in spending, and yet despite months of chainsaw wielding, he managed to reduce spending by a few dozen billion once the receipts were totalled.

Perhaps the mistake was not getting Wolf commenters to run DOGE and find the other $1.95 trillion in “waste” that they have figured out but never bothered to tell the rest of us.

” the 10 year yield remains unattractive at this level”. Depends on a lot of things not the least of what your investing profile is. And Micron was attractive to some on Wednesday. Not so much Thursday and Friday.

“Micron was attractive to some on Wednesday. Not so much Thursday and Friday.”

It’s hard to predict the future movements of the herd with day-to-day precision.

Wall Street reminds me of the morons I knew in Junior High School who never cared about principles, but instead just cared about what their peers wanted.

The herd is being herded either into a pen or off a cliff. Not much room to manuever.

Personally, I am afraid to invest in a long term bond that is paying less than the obvious rate of inflation let alone the risk premium which is currently valued by the market at a negative 50 bpt at least

It’s still better than in 2021 when you were in a .50 % bond and the treasury raised rates to 4% in the following years.

Thats 8x what you were making.

What if you buy a 4% now are they going to raise the rates to 32%? I don’t think so. Worst case scenario a hawk gets in there next after Warsh and raises rates to 8-9%. At that point inflation would be negligible.

*Fed raised rates*

When diesel prices begin increasing further in July due to oil supply constraints, the knock on effects to prices for goods will send inflation higher. The impact on distillates and other oil related products (naptha, etc.) will raise prices and induce scarcity also.

Time will tell if the US can ride out the impact until demand destruction brings prices back in line. It’s going to be a helluva tightrope walk. I’ll be observing from the sidelines and minimizing personal consumption. Sadly, many cannot.

Can’t wait to hear the howling from the “rolling coal” crowd.

The “rolling coal” crowd is utterly insensitive to the price of diesel, just like the fatties lined up at Texas Roadhouse are insensitive to the rising price of their steaks.

When economic consumption becomes one’s identity, one is willing to work very hard, even for things that damage oneself.

Going forward, we may need to closely monitor the Richter scale for the bond markets. Little tremors – maybe ok. The Big One – not ok.

There’s rumblings in the bond markets.

That bond market sure seems to have a lot of patience. After 5 years of high inflation, the US would need 5 years of 0 inflation to get near the already ‘jimmied’ 2.5 fake target. Isn’t the key to this ‘inflate away your troubles’ a requirement that the debt to gdp drops? At some point that will require the federal government to slow their annual spending binge. How long is this going to take, if ever? I haven’t seen anyone project that; you know; shows us the plan. Maybe Wolf has done it in an article I missed. Good luck to Kevin Warsh.

That’s their way out, inflate it away.

You can’t inflate your way out of debt while you are still adding to that debt. You have to get somewhere close to break-even on current accounts in order for inflation to eat away at existing debt.

yep. this is what I am concerned about. We’re going to get the inflation without the GDP/debt reduction.

Its a classic political bait and switch. The tax increase (or cut) is today, and the spending cuts start in a few years, and never happen.

But inflation is most definitely a tax increase that hits folks who spend all of their income on necessities the hardest.

Yes you can. So here is an extreme example: If you have 10% inflation, your tax receipts are going to go up by roughly 10% too. If you also have 13% nominal GDP growth (=3% “real” GDP growth adjusted for inflation), your tax receipts are going to rise by another 13%. In other words, 10% inflation with 3% real GDP growth generates 23% increase in tax receipts. It’s this flood of tax receipts that makes that debt easier to deal with, while inflation at the same time devalues the entire outstanding debt. These relationships are fairly stable and well understood.

Wolf, that’s hardly an extreme example….

;-)

Wolf I’m having a hard time understanding how you’re not double counting inflation here. Mind explaining it to a dummy?

yes, seems to me too double counting inflation

Better to double-count inflation than not counting it all 🤣

? Of course you can inflate your way out of debt while still nominally adding to the debt, if you inflate faster than you increase the debt. Mostly people care about debt/GDP so also GDP growth reduces the debt burden.

Right now the government debt is growing at 8.5% year on year, real GDP growth is ~ 2.5%, so at 6% inflation (without corresponding increase in gov. expenditures) the real debt would reduce. 2021 and 2022 had inflation+growth > 10% which is why debt/GDP reduced in those years.

The paradox is that as the US inflates away its debts, it also becomes a more creditable borrower. E.g. as debt/GDP gets smaller due to inflation, more lenders are willing to lend at even lower rates.

The result is a sort of equilibrium where treasuries sometimes – for years at a time – don’t fully compensate lenders for inflation.

Inflation targets are not retroactive.

There will never be any concept of trying to depress future inflation below 1% to “average out” past high inflation.

No one in power is promising to produce a CPI that averages 2% per annum stretching back to the creation of the union.

Pulte future Grok prompt:

“How do I FISA the FED? Don’t make mistakes or hallucinate. Delete search history.”

Mr. Warsh has nightmares at night of some grotesque creature yelling “In -Flayyy-Shunnn”. It has gotten so bad, he is rumored to have sought out professional help for his debilitating nightmares.

Do yourself a favor: buy something when it crashes, sell it when it flys, and most important do nothing otherwise. So it is time to sell stocks they have flown. The big question is: where do you put the money because nothing has crashed. Perhaps it is time to do nothing!!

Isn’t that just “market timing” as opposed to “buy and hold”?

I bought a few hundred thousand bucks of STIP, as one side of a barbell portfolio. The other side is SPY calls, 2 years out. The most I can lose, outside of crazy economic collapse scenarios, works out to a single-digit percentage. Call me a coward, but I’m still all-in!

The AI boom is almost comically well timed..

Quick…repeat three times in a row…the Strait of Hormuz.

Lorie Logan just did an interview stating that they won’t increase rates till the end of the year. And she also said she is against the scarce reserves policy saying that the ample reserve policy has kept money market rates in the FOMC target range. If I was a long-term bond holder, I would be selling off immediately. Crazy times, it’s almost as if they want to keep inflation around. Logan worried about money market rates instead of inflation is absolutely nuts. These FOMC members are trash.

Didn’t the 10-year climb from 5 percent in late1993 to 8 percent at the end of 94? I think the situation today is far riskier for long term holders of bonds than in those times. It seems as though the bond holders of today forgot about the past.

“At this level, the 10-year yield is not high for this inflationary environment”

Couldn’t agree more. 4.53% is very low. I feel Bond market still in denial. One news here and there and Bonds prices rise yields fall. 2026 it is much better compared to 2025. Now all securities are showing no rate cut for this year.

After stopping QT, FED is influencing Treasury Markets by not only reinvesting maturing ones but also proceeds from MBS.

Reserve management purchase amounts came down a lot but they didnt unwind purchases from Dec 2025 yet. Let us see if Warsh has stones to follow what he has been shouting on all TV shows in last few years. “Reduce the balance sheet”. Looking forward to 10 yr hitting 5% and stay there for few weeks at least (unlike when it hit in Oct 2024 for not even a day).

As Buffet says when the high tide is over, we know who is swimming naked.

The low yields suggest massive demand for treasuries.

The massive demand comes from too much money in circulation.

Let’s hope KevWar’s Quantitative Tightening By Another Name reels in the money supply before the pressure to raise rates gets too high.

The “yield curve” stepping stones: the spread between 1M and

1Y is almost flat: 0.174. Between 1Y and 2Y: 0.277. A low step up between 2Y and 10Y: 0.368. A jump between 10Y and 30Y: 0.484. In Germany the 10Y is: 3.04. the spread between 15Y and 30Y is almost flat. In Japan the 40Y and the 15Y are inverted. A year ago the front end was higher. The yield curve was a curve with a bottom at 3Y. There isn’t much between the 2Y and the 10Y despite inflation fears. A global recession can invert the 2Y/10Y in the US, Germany and Japan and drag the long duration down.

Wolf, thank you for your comment above on how the Fed creates and destroys money. I am not an economist but took an interest in this subject post 2008 Financial crisis.

It took a few years to get to realization on how money and debt are two sides of same coin. Issuing debt creates money on the spot. Paying back debt will destroy money as well as the corresponding debt.

My understanding is that the interest rate itself is key as to how much debt people/businesses/governments want to take on and how readily they want to pay it back.

In general it seems like for many decades most government/business debt is never fully paid back and often rolled over into newly created debt. Thus more money is in existence with every passing year.

worth noting as a generality that fiscal policy tends to be proactive in its initiation by government , while monetary policy tends to be reactive by central banks

if one looks back at the post war history of crisis , central banks respond to financial market events first , while the governments react to economic events as a priority

if this thesis is correct , and it may well be disputed , if interest rate direction and bond prices are in dispute , it is perhaps likely that any motivation will come from a financial market event , not an economic crisis.

Brent might rise to $150/$200 and TNX drops below 3.50%.

XOM and CVX CEO: Inventories were never so low. Higher Brent and lower TNX will cancel each other.

What do you expect from these oil companies executives?

That we have full inventory and gas prices are gonna fall 😀

I am checking the grand assumption…

“the Fed will/is fighting inflation”

5 years over their manufactured target strongly suggests they are not.

The bond market must bring rates back to reality, they have been too low for too long. Speculative mania and these massive massive IPOs and all the leveraging surrounding the IPOs is suggesting we are in a cauldron of dangerous financial ingredients. Now, add in the Iran event and the likelyhood of a change of Congressional control in the fall.

Swim close to shore.

My credit union and many commercial banks here are offering lower rates on longer term CDs than shorter ones. What gives here?

They prey on dumb money. There is a lot of it out there.

I’ve noticed this shift too. More broadly, brokered short term bank CDs have starting paying higher interest rates than T-bills offered in my 401k and other accounts. I haven’t seen that in a while but am happy to take advantage for short term cash management. Might be an early indicator of stress in the banking system?

“Might be an early indicator of stress in the banking system?”

Good lordy no. Every time some banks raise their brokered CD rates a little, the same nonsense about “stress in the banking system” comes out. It means that SOME banks are paying a tiny bit more to attract new consumers and new money. Banks do this all the time. Brokered CDs, which is what you’re discussing, are sold in a competitive marketplace, similar to stocks, and the highest interest rate wins. Now banks are beginning to expect rate hikes, and all their loan rates have risen, and they feel freer to offer better rates to get some cash that they then lend out at 6.7% for mortgages or 9% for auto loans or 30% on credit card loans. All of those rates have gone up recently.

It’s called an interest rate sale. On a smaller scale, often used to attract depositors when a bank opens a branch in a new location or city .

Anyone remember when the markets waited to see what the banks would do with the Prime Rate on Friday? (1970s and 80s)

The Free Market was at work back then……

The Fed was not nearly “front and center” as they have now become.

One would hope Warsh would be more focused on improving the inflation calculation by trashing the surveys and replacing with hard data now available for housing and rent.

The so-called ‘prime rate’ hasn’t had any relevance for many decades.

So Cal.

You seem to miss the point

There once was a time when it DID MATTER …a lot.

Then suddenly it didnt.

Now, can you put your finger on what changed? What entity became MORE in the forefront, became more of a monetary authoritarian, more of an intrusion in free market price discovery”

It’s time for higher taxes especially corporate coupled with reduced spending. Rates can go up, too. If our government was treated like a indebted household, that would be the solution. Unfortunately, politicians are not prepared for austerity and prefer to juice the economy and pray that inflation is just enough to offset the increase debt servicing costs. So we are left with bonds that don’t pay enough for the risk or equities that are overvalued and in bubble territory. Great time to be a fiscally conservative investor.

All that has to be done is remove the curtain: ( The average guy pays full taxes, the super rich hide their wealth and donate to political forces to remain hiding, in plain sight.)

The U.S. Corporate Transparency Act (CTA) requires certain private businesses to report their Beneficial Ownership Information (BOI) to the Financial Crimes Enforcement Network (FinCEN) to combat money laundering and tax fraud. FinCEN has significantly narrowed the requirements, currently exempting domestic entities and U.S. persons while maintaining reporting rules for foreign reporting companies

You’re Canadian now, former USian, as per years of your comments here. Why don’t discuss the massive money laundering in Canadian real estate that has been tolerated or encouraged forever and continues to this day. Lots of excellent Canadian reports on this over the years.

Warsh will continue financial repression. Higher inflation rate than the 2% “target”; probably 3-5%. Remember, inflation reduces the debt, and it looks like that reduction has to outrun or at least equal the deficit increases each year (approximately 5% of debt)

The Fed will keep interest rates artifically low. “Someone” will be buying US bonds/bills/notes and if not shown legally on the Fed Balance sheet, probably some “unknown” entities registered in the Caymen Islands.

This continued, and unfortunately necessary, inflation is going to decimate the lower K, retirees and anyone dumb enough to put their money in CDs and/or fixed income (other than short term in MMs).

Congress is going to continue to spend and particularly now that we have a department of war. Of course, social spending will need to be increased to help the lower K survive. It doesn’t matter which party is in power. They both do the same until they can’t.

Yesterday I talked to a senior bank manager: we don’t have delinquency

problems, but other regional banks have. If SPY drops to or below Mar 2026 low and Brent will rise: DXY will rise and TNX will drop.

There aren’t any troubles in the bond markets that yield (interest rate) increases won’t very easily solve.

Correct. But that’s the trouble.

A nothingburger or…?

“The Financial Times reported that Euroclear plans to accept China #onshore bonds traded in Hong Kong (via the Bond Connect program) as collateral. If successful, this would mark the first time Euroclear allows its clients to use China onshore government bonds as collateral.”

China is the second largest economy in the world and is trying to elevate its currency and bonds to developed-country level. What’s wrong with that? Long overdue.

“Euroclear’s plan is to allow Chinese domestic bonds held by investors in Hong Kong through the programme — currently around $120bn — to eventually become eligible as collateral in the settlement of international transactions.

Urbain added that the move could potentially open €5tn worth of Chinese domestic government bonds to be used as collateral in the settlement of transactions managed by Euroclear, which would help drive up international demand for the renminbi and open up the Chinese bond market to western investors.”

I suppose I didn’t make myself clear. The concept of the US dollar as THE currency of choice is discussed here fairly often. Could $5T euros cause a dent? I also saw that China owns 7.5% of Euroclear. Thnx.

It makes zero difference to the US dollar and has nothing to do with the US dollar. Bonds of every developed economy can be used as collateral, and are being used as collateral. China has been trying to get into that club for many years and is making some progress. The issue is still convertibility of the RMB which makes buying and selling RMB denominated bonds more complicated if you want to do that from another currency base, which is why Euroclear has been dragging its feet for so long.

Thanks for the clarification Wolf.

Savings flowing through the nonbanks increases the supply of loan funds but not the supply of money, a velocity relationship. The increase in MMMFs volumes has kept rates down. So has the draining of the O/N repo facility.

Bank credit has continued to expand. The proportion of Treasury and Agency Securities, All Commercial Banks (USGSECNSA) has accelerated. The banks are monetizing a part of the deficits.

The deficits must be cut. Only the interest expense is untouchable.

How about stop replacing MBS with T’s.

Is just that much QT too much to ask for??

Sadly, bond vigilantes have been scared shitless after the Federal Reserve’s numerous 21st-century monetary interventions.

At this point, given the current FOMC composition, I find it more likely they convene an emergency bond-buying meeting on Treasury bonds to prevent “a disorderly tightening of financial conditions” (similar to BOE’s 2022 Liz Truss interventions) if 10-30 year yields keep rising, than enact an emergency rate increase.

No institution on Wall Street wants their punch bowls taken away before the SpaceX-OpenAI-Anthropic trillion-dollar IPO bonanza either, so that’s why they’re exerting enormous pressure on central bankers to hold off any rate increases until year end.

Bond vigilantes have seemingly been victim of a Treasury and Fed that keeps track of their short positions……

which when built, are ‘run in” by “announcements” or behind the scenes machinations. IMO.

Wolf, I like how your writing produces ingestible levels of informed cognitive dissonance. That’s a rare treat in 2026.

I dunno, there seems to be a consensus that inflation will rise, both among the commenters here and professional economists elsewhere.

https://econforecasting.com/forecast/cpi

Most people aren’t saying what they’re doing about it though. And some see it as a good thing, while others see it as a bad thing.

The dissonance would be to expect higher inflation and also own fixed income investments.

“This labor market data indicates that the Fed can move inflation to the very top of its worry list.”

I hope so and I hope it sends a message to all central bankers. JP/FED have pretty much let this new stealthy rise in inflation gain a foothold. If they don’t hike next meeting and/or put in some very stark hawkish comments they will be making inflation great again.

IDK, in 2022 CPI inflation had exceeded 8% by the time the Fed made its first rate hike in March of that year.

https://fred.stlouisfed.org/graph/?g=1WPnO

They gave everyone 6 months notice ahead of the rate hiking campaign to prevent market disruptions, and apparently this worked because we didn’t immediately go into a banking crisis. All the more reason to think KevWar will use his June and July press conferences to start giving the next 6 month warning.

The only question is whether an increase in QT-By-Another-Name begins immediately or if we get a warning period on that too.

Is 23% the right increase in tax receipts? I think 13% makes more sense. If tax rates also increased then there would be a compounding impact.

I own lots of long bonds and have no desire to sell. You can calculate inflation all you want, but people who own bonds don’t need the cash, which is why they own bonds. So whether inflation is 1% or 5%, the bond pays better than the cash you would otherwise hold. If rates go down, that’s just gravy. The question is whether sitting on the cash would get you a better rate than the current rate a little bit down the road — I just don’t know. All the time that you *don’t* own the bond, you’re *not* earning interest on the cash. A lot of this depends on your time horizon and your view of what *other* asset you might hold other than a bond. Do you prefer stocks at this level? Real estate? Perhaps there’s something obvious, but if it were really obvious it would be bid up to prices that might make it unpalatable.