We’re looking for culprits.

By Wolf Richter for WOLF STREET.

Let me just get this out up front: I don’t think the debacle in the stock market today had anything to do with the jobs report – Job Growth Turns Around Decidedly after Weakening for Years – but with semiconductors.

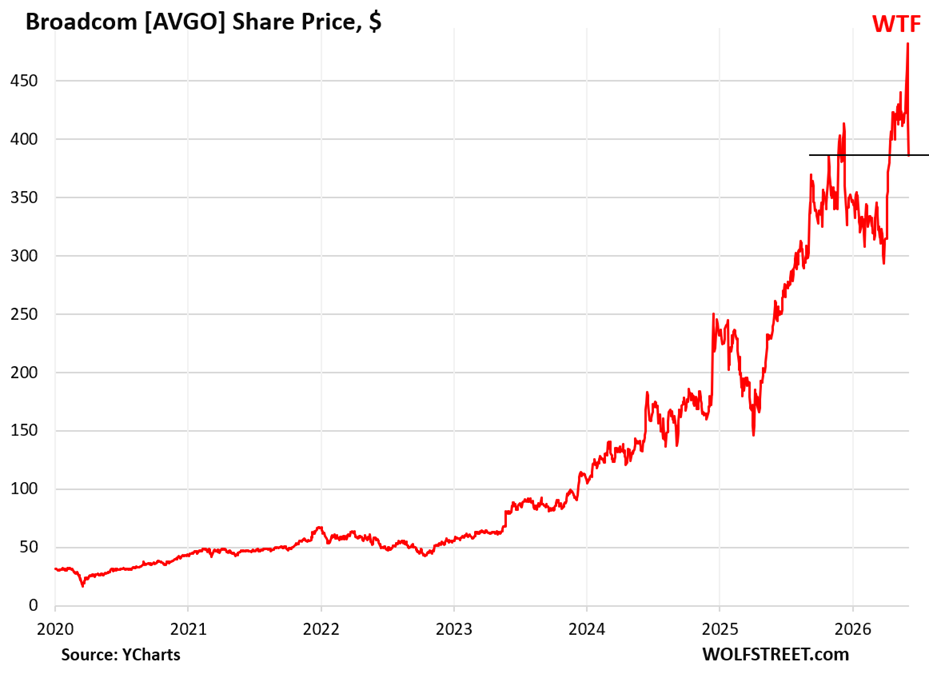

Semiconductor stocks were just overripe. And some are huge. Three are, or were, in the Trillion Dollar Club. They plunged yesterday, and they plunged further and deeper today, jobs or no jobs.

Maybe Broadcom did it. It tanked 20% in two days, $450 billion in value vanished from global portfolios. Maybe the giga-IPO of SpaceX with its $1.77 trillion valuation at 100 times revenues did it. Many have suspected that the IPO, followed by other mega-IPOs, would break the market – the mania in the stock market – as these IPOs become a gigantic liquidity suck.

Maybe the tech giants did it with their plans to also suck massive amounts of liquidity out of the stock market. They’ve started to announce plans to raise vast amounts of cash by selling new shares valued at their stratospheric valuations: On Monday, Alphabet announced that it would issue $80 billion in shares. Today, rumors spilled out that Meta is planning to sell “tens of billions” of shares. And Oracle already announced earlier this year that it would sell $20 billion in shares.

And other companies are likely to pile in, because this is one of the best times in history for a company to sell shares to the public and raise huge amounts of cash with the least shareholder dilution. Not selling shares at these prices would be a dereliction of their duties to their shareholders, so to speak. And then they can plow that cash into new projects, such as AI infrastructure, and thereby into the economy and generate growth and jobs, rather than let investors hoard it and gamble with it.

For the economy, this is a great thing. But these share sales – and the mega-IPOs along with it – reverse the liquidity flow with which share buybacks had pumped up the market for years.

Or maybe the weather did, which was unusually normal for this time of the year. Something did it, something always eventually undoes these historic spikes in semiconductor shares.

Or maybe it was just another dip for semiconductor stocks, before the spike resumes anew. Whatever. But the last two days were big.

Broadcom remains a suspect. It had an excellent quarter, doubling its AI-related revenues, and overall revenues jumped by 48%, according to its earnings release Wednesday evening. But it refused to increase guidance, and that was a bad sign, that was a sign that the magic is coming off.

Whereupon the stock [AVGO] tanked 12% on Thursday and nearly 8% today. Since its peak on Tuesday, over those three days, the stock has plunged by 20%.

Three days ago, Broadcom had a market valuation of $2.28 trillion. It has given up $450 billion of it since then.

But, but, but… the stock had spiked massively in the prior days and weeks, and that 20% plunge only took it back to where it had been in mid-April. So for people who’d gone on a long vacation from everything and just came back and looked at their portfolios, not much happened.

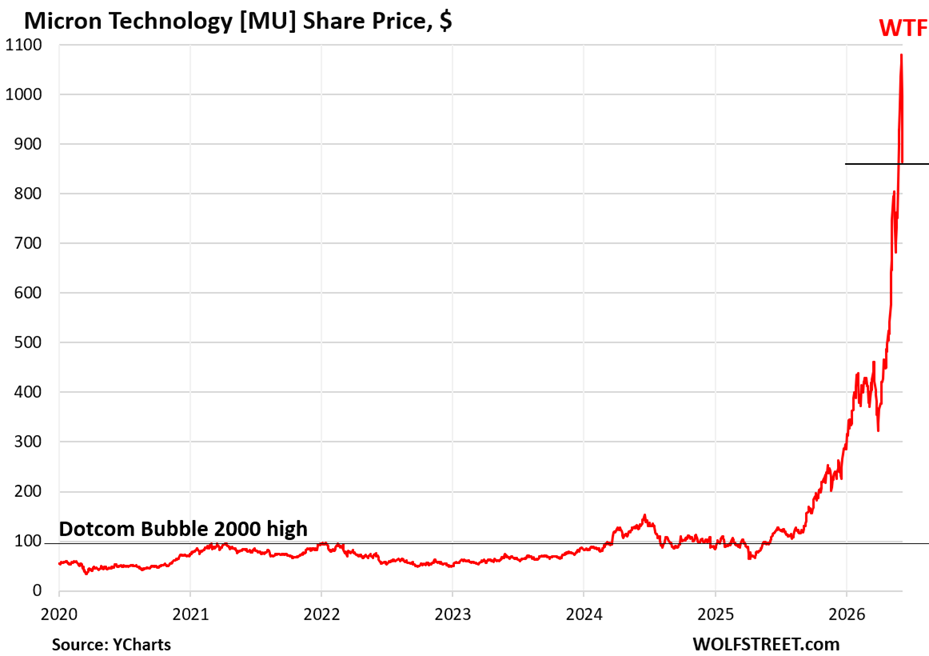

And Micron [MU] remains a suspect. It plunged 13.2% today after having plunged 7.7% yesterday. Over those two days, the shares plunged by 20%, giving up $240 billion in market cap and falling out of the Trillion Dollar Club.

But, but, but… the 20% plunge just unwound the results from the prior 8 trading days. That’s how crazy the spike has been.

We’ve been talking about Micron [MU] because it’s fantastical. Over the past 14 months through the peak on Wednesday, the share price had multiplied by 16 (+1500%) and its market capitalization had exploded from $72 billion to $1.21 trillion! Micron made history when it doubled its market cap from $500 billion to $1 trillion in just 48 trading days. No way in hell?

During the Dotcom Bust, Micron plunged by 98%, from Micron’s peak in July 2000 ($95.13) to December 2008 ($1.85). The first 70% of that plunge (to $29.00) happened in the first three months. Plunges of over 50% or 60% are the norm here.

It took the stock 24 years, to 2024, to exceed its historic Dotcom Bubble high. But then it moved with a vengeance, and the gains have been generational — and now a quarter of these generational gains vanished in two days.

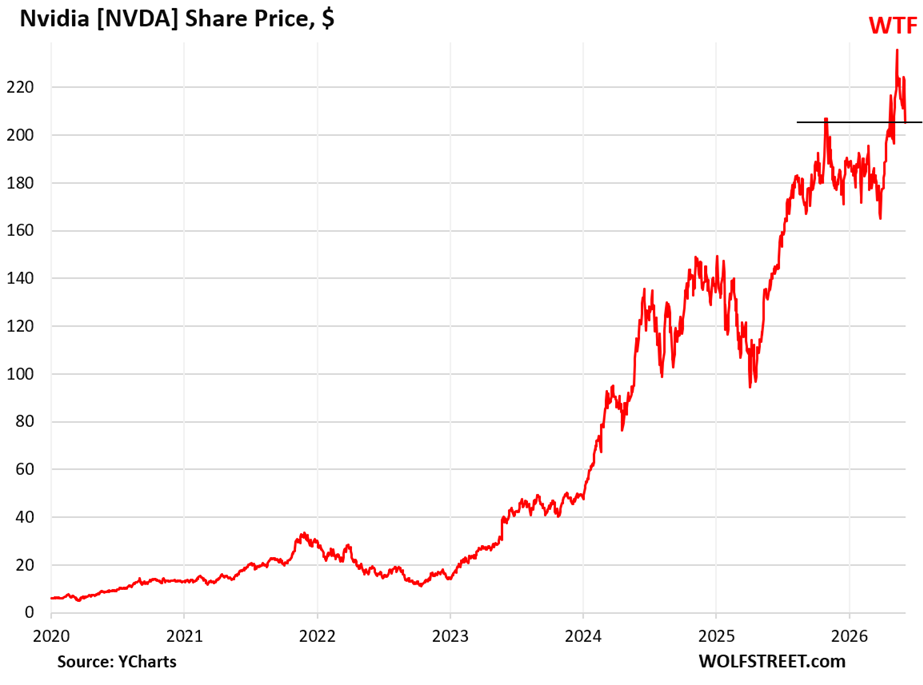

Nvidia [NVDA] is always a suspect because it’s so huge. It’s the top dog in the Trillion Dollar Club. And when it drops even modestly, it takes a lot of value out of portfolios. It dropped 6.2% today and is down 13.0% from the high on May 14. $740 billion in market value evaporated from portfolios around the world. But that just rolled things back to where they’d been a month ago.

From just these three semiconductor makers in the Trillion Dollar Club combined, $1.43 trillion evaporated from portfolios over the past few days.

Semiconductor stocks can be scary instruments – they have proven to be over and over again. Especially when leveraged. Especially after a historic spike. Especially when it’s different this time.

The industry is incredibly cyclical, where chip “shortages” and sky-high chip prices fuel a massive capacity buildout by the chipmakers, and supply ramps up, just as demand stops blowing out, and soon it turns into a glut, where chip prices reverse and collapse. This happens over and over again. Prices of most of these semiconductors act like prices of commodities. Stock prices anticipate these movements well in advance.

The dip-buyers that jumped in to take the shares off the frazzled sellers’ hands weren’t strong enough to turn around the drop at the end of the day. The semiconductor stocks just kept on drifting lower into the close of the market today.

Maybe Monday, after everyone takes a breath, the dip-buying can push up those shares.

Overall, the Nasdaq Composite dropped by 4.2% today, but is down by only 5.4% from its all-time high three days ago. So really, not a lot has happened, overall in tech land, and it’s still one of the best times in history for tech companies to sell shares to the public to raise cash at huge valuations, with the least dilution of shareholders, and plow this cash into the economy.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The story of semiconductors is nicely put. But does not explain why the software companies like NOW are also down about 18% from the recent peak only a few days ago.

Because those companies are pulling money from last resort places now with stock issuance and layoffs. It smacks of financial desperation.

‘Wikipedia has a long write up on the subject of an AI crash by a number of writers.

One estimates that based on spending and valuations the AI bubble is 17 times the size of the Dot Com bubble.’

If you look at the trends since 1850, we’re above that trend line by a lot.

Meaning sometimes we ride above the horse and sometimes horsey dunks us in the water.

Mean reversion of this on top of the horse and in a huge bubble prob means we’re getting dunked at some point.

I’m wondering if the elimination of the Pattern Day Trader rule today increased volatility? It means the leash is mostly off retail day traders who, with AI in hand, could possibly create havoc.

Or maybe not.

I posted a similar comment a while back. I wonder how many rookies got margin called today. It’s sad to see normal people get fleeced.

According to the reverse kimchi trade theory, it all goes back to perp trading on Hyperliquid driving up, then down, the price of Samsung on the Kospi 🤷♂️ whatever that means …

It turns out, if you can manipulate just Samsung, you can manipulate the entire Kospi and thus drive the entire chip market 🤔

Hilarious! Thanks for the chuckles!

“best times in history for a company to sell shares to the public and raise huge amounts of cash with the least shareholder dilution. Not selling shares at these prices would be a dereliction of their duties to their shareholders, so to speak. ”

In other words, we had to dilute the shareholders in order to save them! But it’s a modified, limited, least-dilutive dilution. (At least for now… anticipate a lot of derelict dilutions as things get more challenging…)

Layoff and dilutions are the new stock buyback.

Maybe it’s the Yen falling to 160/USD.

Do you think the recent changes with rules regarding companies being listed and amount it can float is a big deal or nothingburger with potentially 3 big IPOs coming up?

The conspiracy part of me says it is purposeful and not in a good way. Basically leaving pension and 401K funds holding the bag with requirements to buy in via index funds.

Apologies if this question makes little sense and trying to understand risk to 401Ks.

S&P Dow Jones Indices refused to change its listing rules for including SpaceX in the S&P 500. That was the biggie, and it didn’t happen. SpaceX is going to have to make a profit before it becomes part of the S&P 500, like everyone else.

Thanks.

Hold The Line.

For me this was the main reason for the Friday downdraft

Love you articles Wolf

That (non) decision left me with the faintest spark of hope in humanity. A point scored for the masses and most don’t know it.

Today’s fall is like a blip in a gargantuan rally. We will probably see another record next week. Show must go on. Until everything skyrockets and tgmhe dollar turns to trash. Welcome persistent high inflation.

Micron is truly a chip maker in that it designs and fabricates memory chips. Broadcom and Nvidia design sophisticated processors but do not fabricate them.

Like your article

Easy come. Easy Go.

Selling shares to buy spacex

The S&P holding their ground on the rules crashed the stock market.

Hehe jk /s

What I can’t believe is how incestuous all the tech companies are with each other. I’ll lease 925 billion a month of AI server space from you, when I’m already building 60 AI data service centers.

Oh and I can terminate this 925 billion dollar a month contract within 90 days. Sound ok? Greeeeaaaattttt!

This has to be bad how there are no checks and balances on how they keep investing with each other so much. House of cards?

Congressional investigations in 2029 after the economy crushing crash, “what were you thinking?!”

“No comment”

*Million*

Correction

The numbers are hard to make sense of in this economy that has been pumped full of easy money. The SpaceX IPO pricing seems ridiculous.

But then I saw this news item:

Google has agreed with SpaceX to rent computing capacity from the rocket company to power its AI capabilities.

In a filing, SpaceX said Google will pay $920 million per month to rent 110,000 Nvidia GPUs, CPUs, and memory, as well as related components from Oct. 2026 through June 2029, with computing capacity beginning to ramp in Sept. 2026.

That is $8363 per month per GPU and the support systems.

Google was an early investor in space x for $12 billion. They want their payout on the IPO just as much as everyone else.

It’s very icky how they support each other.

They can cancel that contract within 90 days too. Prob just a supporting measure for the IPO.

Why would you even invest in another AI data center from a rival who has Grok?

Are they aligning against Claude? What do Monica and Rachel think? Ross and Joey?

Haha

IMHO, this was an overdue, overall healthy sell-off….it might even continue for another few days, maybe until the SpaceX IPO gets completed. NOTHING (continues) to go up in a straight line, though the semis had been doing their best to disprove that axiom….

Wow. All this positive talk about selling shares and plowing the money back into the economy. Almost makes me think the 1999 .com bubble was a good thing. Seems to me not much of that 1999 money ended up helping the economy. Surely it did help the bankers. I suppose if all those datacenters get built before the thing implodes things might work out.

The internet the way we know it today, including broadband, came out of the Dotcom bubble. There was a huge infrastructure investment aspect to the Dotcom bubble: Laying fiberoptic cables across cities and the world, including undersea cables crisscrossing the oceans, to connect everyone and everything, and installing a gazillion servers, routers, repeaters, and what not to make it into a global network. Lots of the biggest Dotcom bubble companies, including CISCO, were involved in the infrastructure part of the Dotcom bubble.

Good point Wolf. A remaining question is whether it would be better to put that cash into alternate investments like roads and bridges, medical research, modernizing manufacturing, housing construction, paying down the debt, energy infrastructure rather than AI.

Digital infrastructure and electrical infrastructure are just as important as transportation infrastructure. It should never be “either or.” It should be “all of the above.” Infrastructure is always crucial.

The promise (hope?) is that AI will be so impactful to how we live that much of that investment would be quickly wasted. For example, autonomous driving will radically reshape housing, roadway infrastructure, etc to the point that additional lanes on a highway now is wasteful. Similarly for energy infrastructure — we hope AI will accelerate basic science (materials science, etc) such that fusion will be feasible much more quickly and supplant all other generation modes.

Makes me think of the 1873 financial crisis when the US rail industry went bust.

The rails survived though, as most likely might AI, but its builders mighn’t.

I had forgotten that the railroad buildout/bust mania was directly tied to the 1873 Long Depression. Thanks for the reminder. We spent a lot of time in one of my college history classes going over that fraud/debacle.

Of course, the problem is that fiber optic cable lasts 25-50 years while for processors there is a debate between 3 and 5 years for useful life.

Processors last a lot longer than 3-5 years. There are no moving parts, and no maintenance, and unless they get fried, they last. My first server for this site ran without any issues for a decade, and it would have been just fine for a long time. The reason I changed had nothing to do with the server, but with the data center and its management where the server was located. Originally, it was a small US company with great staff that owned the data center, and it got bought out by a big Dutch company, and then the tech support was moved from the US to India, and apparently, the cheapest most clueless people staffed it, and when they changed some settings for the data connection at their data center, my site vanished, and I had to deal with these morons in India. That’s when I changed to a US-owned data center, and while at it, got a new much fancier server – but you can’t tell the difference, the site runs as before.

The problem with chips is that new stuff can do things more efficiently, and use less energy doing the same stuff, and at some point, running a data center on old chips might cost more than replacing the old equipment with new equipment.

Look, all these big cloud guys already have data centers from years ago. They understand what happens to processors better than you and I. They’ve been living with it for years. It’s their calculus. How they depreciate it on their books is just a paper entry. It has no bearing on the reality of processors.

@wolf

Yes, while the processors can technically run for many decades, the USEFUL life is what’s relevant. I’m not an expert in fiber optic cable, but my understanding is that new fiber laid today is roughly the same as cable laid in 1999, and the backbone of the broadband net is still that late-90s overbuild with minimal maintenance and upgrades.

Compare with NVidia. The V100 (2018), used to train the original chat GPT, has ~17% the performance of the H100 (2022), which we are debating selling to China. The H100 itself has 66% the performance of the H200 (2024), the current available standard. So an 8 year old chip has 11.2% of the capability of the current standard, and market pricing reflects the non-linear value of lower-efficiency chips, with V100’s available for about $2K, H100s for $20k, and H200s for $40K. So, 11% of the performance for 5% of the price, because the physical data center space and electricity and time-to-market are at such a premium.

Modern fiberoptic cables have vastly improved over the 1999 version, both in terms of the fiber and in terms of the cable.

Modern fiber has substantially reduced signal loss (due to low-loss purer glass) and higher glass flexibility with less signal loss at bends, and therefore data speeds per fiber have vastly improved. The photons still travel through the fiber at nearly the speed of light, same as before, but that’s not data.

And today’s fibers are a lot thinner, which allows for many more fibers to be bundled into one cable.

So you get much higher data speeds and more capacity with modern fiber and modern cables. The optical-electronic hardware at the ends of the fiber has also dramatically improved.

And yet, the old fiber cables are still being used. And when more capacity is needed, new cables get installed.

But at some point, it’s not worth maintaining and repairing the old cables, and they’re replaced with new cables.

The enemy of old cables: Rodents eating through the cable armor and breaking the moisture barrier or the fiber itself; moisture getting through the jacket’s moisture barrier, which leads to hydrogen-induced signal attenuation; various environmental issues impacting cables, such as storm damage for lashed fiber cables, construction equipment for underground cables; anchors for undersea cables, etc. But if a fiber cable continues to function and generate revenues, it continues to be used. A lot of tech products are that way.

We only need recall reading how much of the internet was “dark” in the sense of unlit but connected fiber (!).

It’s lit now apparently.

That is all true. What is less frequently mentioned is that dot com enabled unexpected societal changes. Before it, it was very hard to outsource engineering or management work. Global teams did not exist. I remember meeting software engineers in 2001/2 that became high school teachers because their jobs moved elsewhere (India). When we were working on dot coms in 1999, we did not expect that. AI-induced societal changes are coming and it may not be just replacement of entry-level roles.

Greenspan didn’t own any stocks.

I loved “Not selling shares at these prices would be a dereliction of their duties to their shareholders, so to speak.”

Some of these software companoes that design AI server hardware are reporting EBIT of 50% sales. So much circular investing you start to wonder what sort of competitive capitalist environment would exist that allows that to happen? The market today took an appraisal and softened the growth curves. It’ll be back to growth until we see a few soft earnings quarters. My sense as a consumer is that a slowdown is coming. My personal rate of savings is barely keeping up with inflation, at least at 3.7% short term rates.

1W SOX: May 18 had a large buying tail. This week it has a large selling tail, after reaching #9 last week. They might cancel each other, before moving up.

1W QQQ and SPX: both flopped instead of #9. 1W DIA. Last week a new all time close. This week it closed below last week high, above Feb high, leaving behind a large selling tail, on #9.

1M QQQ: Feb flop instead of #9. It flipped in Apr. On June 5 QQQ is red after reaching a new all time high. Feb close is far below. Mar close is lower. Mar bar is half size on x2 times Apr vol.

Meanwhile, who knows what horrors lurk in private equity?

Probably drop in a bucket compared to the horrors sittng in the index funds.

Yes, look at something like an all country world index fund. The top holding is in the 2% range and the last of over 2000 holdings is like 0.0004%.

Then there’s the IBM chart with $100 per share spike ….. a result of a President’s decision to send $1 Billion to a company.

How is it that a President can do such a thing? I thought the House controlled the purse strings.

Yeah, pretty crazy, but IBM already gave up half of that $100 spike. The spike was just a crazed day-traders’ reaction to whatever Trump says. Trading on Trump’s social media posts has become an entire industry.

So Wolf, this IBM gift is not a done deal?

I would think/hope Congress has a say in this.

The Administration is buying shares from these companies. It’s not a gift, but an investment. It started with Intel last year. It was the Biden administration that handed out gift (“grants”) to the some of the biggest companies on earth and small companies alike under the CHIPS Act and other Acts. Intel, Micron, etc. got billions of dollars of those Biden gifts. The Biden administration got zero in return. Trump’s policy is to get shares in return for money. So in IBM’s case, IBM issued $1 billion worth of shares to the US and got $1 billion in cash for it.

From Reuters:

The Trump administration is expanding the government’s burgeoning investment portfolio, announcing this past week that it will award grants to nine quantum computing companies, including a new IBM (IBM) venture, in exchange for equity stakes.

With the investment, quantum technology — a sector garnering intense investor interest despite questions about its near-term commercial viability — is set to join the administration’s portfolio of investments which already spans semiconductors, steel, nuclear energy, and rare earth minerals.

The move also underlines the growing prominence of quantum computing in national security.

The Trump administration has emphasized national security in its varied investment moves over the last year. Describing them as a means to both turn a profit and support strategic industries, the administration engineered a “Golden Share” in US Steel as part of the agreement to approve Nippon Steel’s (NPSCY) purchase, as well as taking an 8% stake in nuclear power company Westinghouse.

The most prominent investment so far has been in Intel (INTC). Since that deal was announced last August, the US-based chipmaker has hit record highs and netted the US an unrealized profit north of $40 billion, which Trump has been quick to tout….

Similarities between Trump’s investments in rare earths and quantum computing. Perhaps the most direct parallels to the quantum computing awards can be found in the government’s deals involving rare earth mineral miners and refiners. The US has struggled to compete with Chinese dominance in that sector, which produces essential ingredients for modern electronics.

Over the past year, the US has taken stakes in an array of rare-earth companies such as magnet maker Vulcan Elements, mining company MP Materials, and another called USA Rare Earth.

All told, the Trump administration has equity stakes of between 5% and 15% in at least five different rare earth companies.

The return of true price discovery? One can hope. How will this occur? Slowly then suddenly…

Hedge accordingly.

I did a Google (AI) search on “How long will the computing hardware in a data center be used?” and the top-level result: 3-6 years. The Google search provided an informative breakdown of the replacement cycle for various technologies used in a data center, with narratives for each. There was a brief discussion of the lifecycle of the hardware that gets taken out of primary service, but then typically get moved to secondary service. So it could be revealing to find companies in the business of taking hardware that is obsolete in the AI race, and selling it. What does that secondary market look like, and might it be a better investment than the primary one? Maybe the people repurposing/recycling the hardware will do better than the ones making the hardware in the first place?

Ive worked in this sort of industry. At the company I worked for, the hardware didn’t move just it’s purpose. For example, new hardware gets used for the latest and greatest computation problems. But after around 3-6 years a new cluster or data center is made. The old one now is used to for other purposes such as maybe we sell compute hours on it at a decreased price. Or lower level stuff. Storing and the memory management of so many pictures, emails, documents, etc in a cloud takes processing that doesn’t require the latest and greatest processors so companies would use them for that and there is always a demand for that. Eventually the hardware does become obsolete for various reasons and will be replaced but it takes much longer than 6 years and the hardware doesn’t move. It’s just reconfigured.

“Or maybe the weather did, which was unusually normal for this time of the year. ”

So, would that make the weather abnormally normal?

Abby Normal!

Like the article points out, drop was just a pimple on an elephant’s az.

Maybe the market was feeling the Bern with the talk of the government taking a stake in the AI companies.

Or companies selling shares and investors taking profits because a dollar in the bank could be worth 2 in the bush.

MW: S&P 500 sees $1.8 trillion wipeout, while Nasdaq tallies biggest point drop ever.

Paywall guy don’t jump!

One day sanity will return. Haha

And yet Ring Cameras send your personal video of your house out to 200 different servers that anyone can watch.

People love the Ring camera though!

Consumers are Not very bright

Bitcoin, an “asset” class that is highly correlated with tech, was probably the canary in the coal mine. It was pretty down for a while while a lot of ai boomed – suggesting that there is only so much tech mania money out there and it’s starting to hit its limits.

Semis were up because they should do make a lot of money because of the capex spend from the hyperscalers. But the hyperscalers and going to need to raise a ton of money from the public market, and are competing with the AI would-be trillionaire companies.

Meanwhile interest rates and inflation are going up. Folks are seeing the potential car crash and turning off at least some risk.

As far as bubble goes. Sure, it might be a bubble. But every time a sector or asset class rips people say bubble. We’ve been in a so-called “everything bubble” for over a decade. Unfortunately, we only really know if it’s a bubble when it pops.

But does tech look like a good investment? Hell no! The P/Es are absurd, the business strategy seems stupid, the leaders all act like earned advertising con men, and none of the AI companies are making any money. Plus, the better product is coming out of China. 3 months behind at 1% of the cost and no vendor lock in as it’s all open.

I blew it on a recent Bitcoin short. Was about a week early. From my start around 72k it dipped into the upper 60s. So far so good. Then it sprang back pretty quickly to around 74k-75k where I stopped out. Only a small amount of lost money.

Then it goes up to about 82k or so, and I’m thinking I was right to bail for the time being. Was watching it to re-short, but hesitated after the recent loss and uncertainty if it was headed more immediately down.

So over the next week or so it plunges from about 82k to 60k, while I watched without participating, anticipating that it may have a small bounce in the middle of that first where I could jump on it again. It didn’t. Ouch. Easy come, easy go. I’ll likely be back at it again when it seems more ripe.

I really don’t understand why a number of large institutions seemingly got into buying bitcoin. It’s just a gambler’s coin of the realm, and the swings can be massive and come out of nowhere. Congrats to those who got in early and lucked out, but I wouldn’t want it in my retirement fund.

Still waiting for the right time to start entering some equity index shorts or puts also though. Not quite yet.

Such a long post to highlight the difference between gambling and investing. You, sir, are a gambler. Might as well just play online slots.

On Fri Wall Street worked very hard to push SPY under May 8

closed @737.62. A big red, high quality selling bar, on higher vol.

A change of character. 1D QQQ: a big red on higher vol, the biggest bar since Nov 20 2025 and Oct 10 2025 with a similar red vol. It’s just for u Kevin.

The question becomes will margin selling in any of these stocks and/or crypto cause a contagion. Let’s not forget that it was ultimately AIG that caused the Fed to soil itself, resulting in roughly a $182B bailout.

Just an FYI, for those who are convinced of the NVDA bubble…

Right now (AFTER yesterday’s drop), NVDA’s forward FY P/E is about 21-22 while last year’s revenue grew 85%. This year they are expected to earn ABOUT $9/share, w next year’s estimate in the range of $15/share, yet sits at 205

How many here are aware that Costco’s forward PE (AFTER yesterday’s drop) is about 45, while revenue grew about 11%. Costco earned $19.88/share for FY ending May ’26, with next years estimate being $22.67 and the price per share is 971 today (4.7x NVDA’s price)

The entire S&P 500 forward FY P/E is now about 25.5, while avg revenue growth is about 11%. I ain’t sayin’… I’m just sayin’ :-)

$9 out of next year’s $15/share is this year’s $9/share. I believe they refer to it as circular financing. Enron perfected this.

But yeah, Costco is pretty insane, but saner than Walmart. To paraphrase… Lehman is fine. Bear Stearns is fine. The S&P 500 index fund is fine..

Rosarito D,

Ever hear of the law of large numbers?

Unless the demand for chips grows exponentially forever, and margins hold, that oh so low p/e for NVDA is what’s going to the moon. Just sayin’. ;-)

Gatt,

Here’s a copy of a post I wrote on a previous thread from Wolf… it’s my answer to you as well… :-)

————————————

I bought NVDA in Dec 2017. My cost basis is now under $5/share. I have sold often on the way up, taking some profit off the table. Over the years, I have held thru HUGE drops (as Wolf has talked about in other posts), yet has ALWAYS come back and hit all-time highs. My belief in the big picture of the AI story (NOT just AI agents), but the unseen possibilities in ALL aspects of the the global economy. There will be applications and uses that the visionaries can see, but we can’t. My go to scenario is to think about the movie “Blade Runner”. I don’t know what, how or why, but there are always people/entrepeneurs who do see things and will have the tools, capital and vision to make things happen that will change everything and how we do it.

Many companies will fail, but the winners… the ones investing the most in this technology (with a vision), will continue to soar. The cycles will be bust and boom, but at least for now, NVDA will be at the forefront, not just for it’s GPU, but its CUDA moat and investments in so many different aspects of the AI build out. Its recent foray into the CPU field just announced (the RTX Spark) is a shot against the bow of Qualcomm, AMD and Intel.

Jensen Huang has made me a lot of money and it is not yet time to bet against him and his vision! If the stock falls 30-40%, I’ll start buying again. YMMV :-)

Good article. I have issues with “Plow this cash into the real economy”. The issue here is AI infrastructure. Building new AI infrastructure isn’t easy – it requires new power generation infrastructure and often major upgrades to power and data transmission infrastructure. That is in a sector, where the old infrastructure already needed replacing after decades of underinvestment and extending lifetimes. The “easy” bit is building the data center, as planning and permitting are generally non-contentious. For the rest, the normal timeline is about 7 to 10 years. This is dawning on the giants. I know this because I actually hear them scrabbling around the US and Europe for sensible options. We saw this unreality over in Europe last week, with Macron promising the AI industry secure power from France’s fleet of nuclear power stations. This is bull. They are ageing plants, desperately needing replacement. The last effort to build one took 20 years and came in 300% over budget. Also they are (along with Norwegian hydro) about the only baseload supply available in NW Europe and so desperately needed to balance growing solar and wind. IF, and its a big if, the power requirements of these centers cannot be reduced, very soon there will need to be announcements about realistic timelines for growth.

Yes. 7 to 10 years, when the chips they have already purchased have a lifetime of 3. And while they struggle to find any return on the massive investment they have already committed to, nVidia’s valuation requires them to continue to buy, buy, buy – at an accelerating rate.

These big data centre are just for frontier model training. Think of them as the mainframes being built just before the PC revolution. Soon all the AI a person needs will be in the local model running on their robot that they charge from roof top solar.

There’s a secret reason the hyperscalers are offloading the debt and other issues to the neoclouds. who are specializing in training, not CPU for agents, or inferencing for running models.

Just one small caveat, the baselining argument has been debunked so many times now it’s getting painful.

The answer is batteries, not nuclear. Nuclear is not, and will probably never be, the economically sensible answer to renewable energy. Batteries have been exponentially improving their power/cost ratio and are likely to continue doing so for some time. Nuclear has only been getting more expensive. SMRs do not exist yet, Thorium doesn’t exist yet, Fusion doesn’t exist and might never exist. The only real argument for nuclear is space consumtion in certain densely populated areas, which you might as well tackle with higher voltage long-distance lines to areas where it’s more feasible to put solar/wind farms.

Even in countries with high % of green energy, the days of ‘disbalance’ in the energy market can be counted on two hands per year. You don’t need nuclear to plug that gap, you need a smarter grid and some batteries.

Not sure that is right. NW Europe has all the countries plugging the North and Baltic sea with offshore wind assets. Denmark already had 70 days in the year in which prices went negative, and the number of days when it imports exceed 75% of domestic load has grown every year. A two day lull in the wind knocks out ALL the battery capacity of the nation and DK is ahead of the curve on batteries. All those countries have clear plans to increase intermittency reliant power. This is why the grid operators I speak to across Europe are literally scrabbling for real baseload. They dont regard batteries as a solution. The UK plan is to add another net 5GW of gas fired and keep it idled for 95% of the year! That is the best they can come up with… Baselining is a real problem and a painfully expensive one.