For the 4th year in a row: Normal-ish mortgage rates, too-high prices, and the “lock-in effect” from the Fed’s reckless interest-rate repression.

By Wolf Richter for WOLF STREET.

Late last year and early this year, the story was that dropping mortgage rates, powered by big rate cuts from the Fed, would unleash demand in the housing market in the spring – the key spring selling season – and that sales volume would take off and that Realtors’ commissions would rocket to the moon.

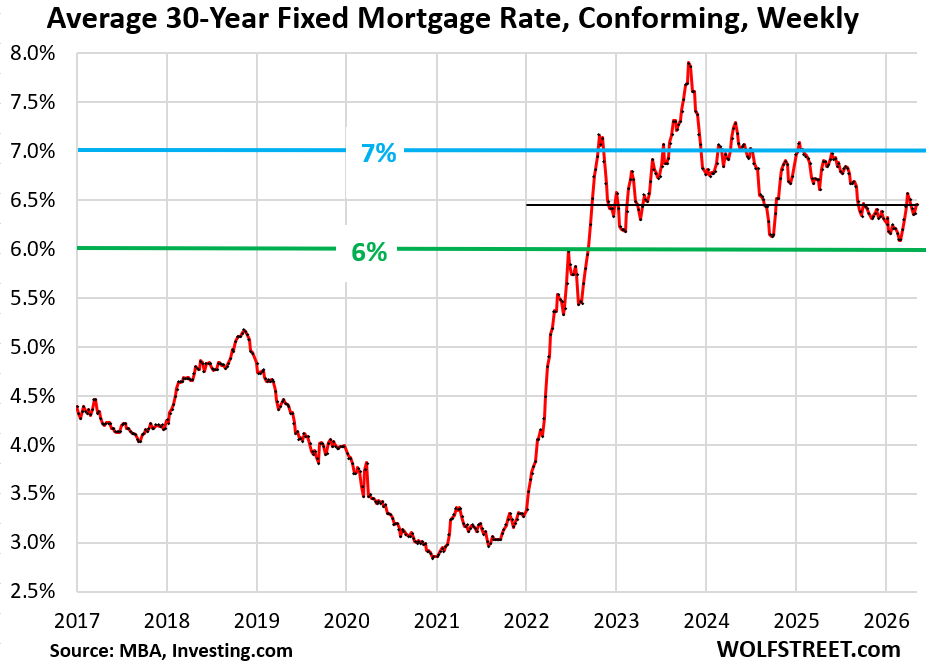

And so that didn’t happen. Inflation has been reheating for months before the war and before the energy price spike. The energy price spike in March and April then added to that resurgence of inflation. The Fed is now talking about a possibility of rate hikes as next move. And longer-term Treasury yields, such as the 10-year Treasury yield, rose in March and April in response to inflation fears. Mortgage rates, which track those Treasury yields but are higher, rose back to the 6.5% range. And the housing market remained in the same-old-same-old frozen pattern that it has been in for four years after the price explosion from mid-2020 through mid-2022. And it continued in the latest week.

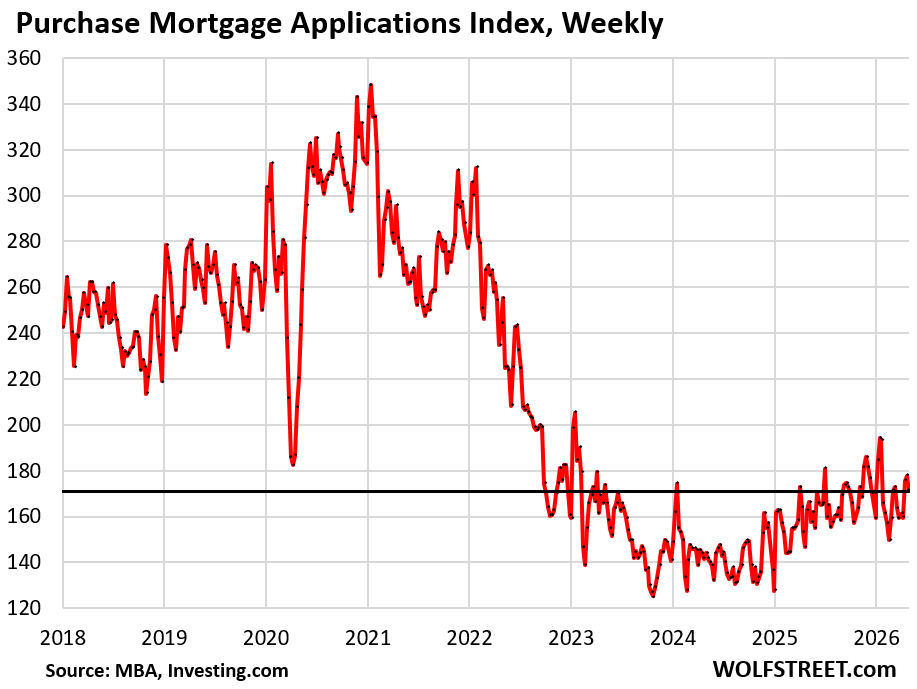

Mortgage applications to purchase a home – a measure of demand that may become actual home sales in the future, so a forward-looking indicator of home sales – dipped in the current survey week and remained near rock-bottom levels, down by 34% from the same week in 2019, according to data by the Mortgage Bankers Association today. That level of mortgage applications is below even the collapse of mortgage applications during the lockdown in the spring of 2020.

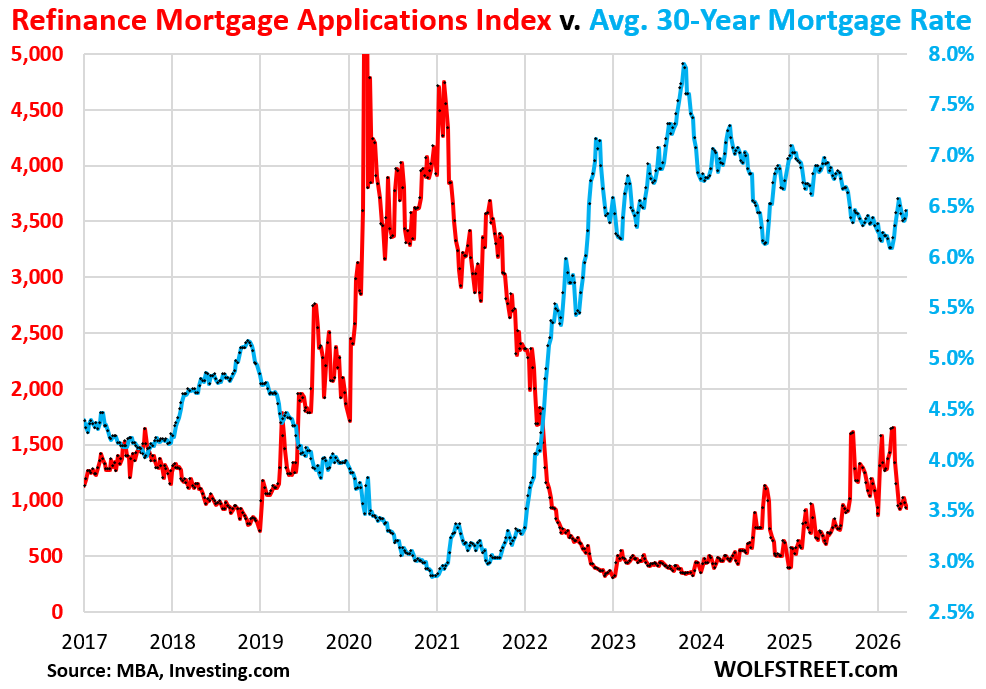

The average weekly mortgage rate for conforming 30-year fixed mortgages rose to 6.45% in the latest reporting week, according to the Mortgage Bankers Association today.

For the past 7 weeks, this measure of mortgage rates has been back in the middle of the 6-7% range, the range it has been in since September 2022, except for some breakouts to the upside.

These mortgage rates are not high in a historical context; they’re only high in the context of the Fed’s QE which started in 2009 and took on mega-proportions during the pandemic.

Under its QE programs, the Fed bought trillions of dollars of securities, including mortgage-backed securities (MBS), which repressed mortgage rates below 3%. But this massive amount of reckless money printing was part of the toxic mix at the time that triggered the worst inflation in 40 years. With mortgage rates below 3% and inflation at 9% – negative “real” mortgage rates, better than free money – home prices exploded and are now too high. And that inflation has refused to go back into the bottle.

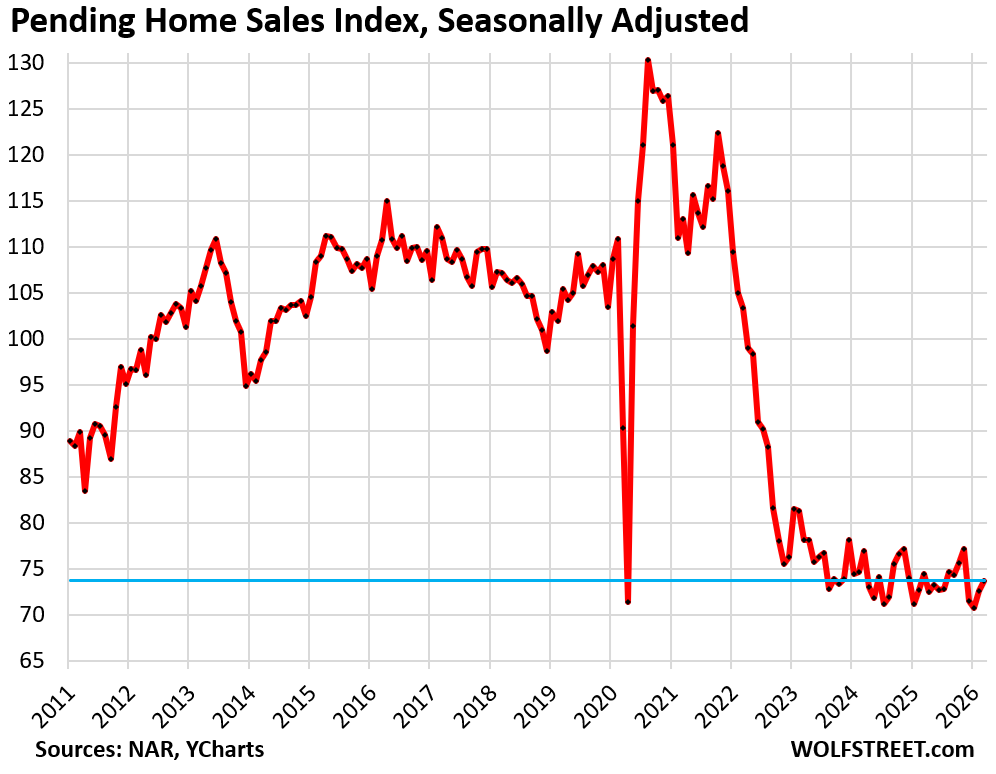

Pending home sales for March – deals that were signed in March but haven’t closed yet – also remained at rock bottom, down by 30% from March 2019. In January, they’d dropped to a record low in the data by the National Association of Realtors going back to mid-2010, and in February and March, they inched up from that record low.

And the much-hyped spring selling season has turned into the fourth dud in a row: 2023, 2024, 2025, and 2026.

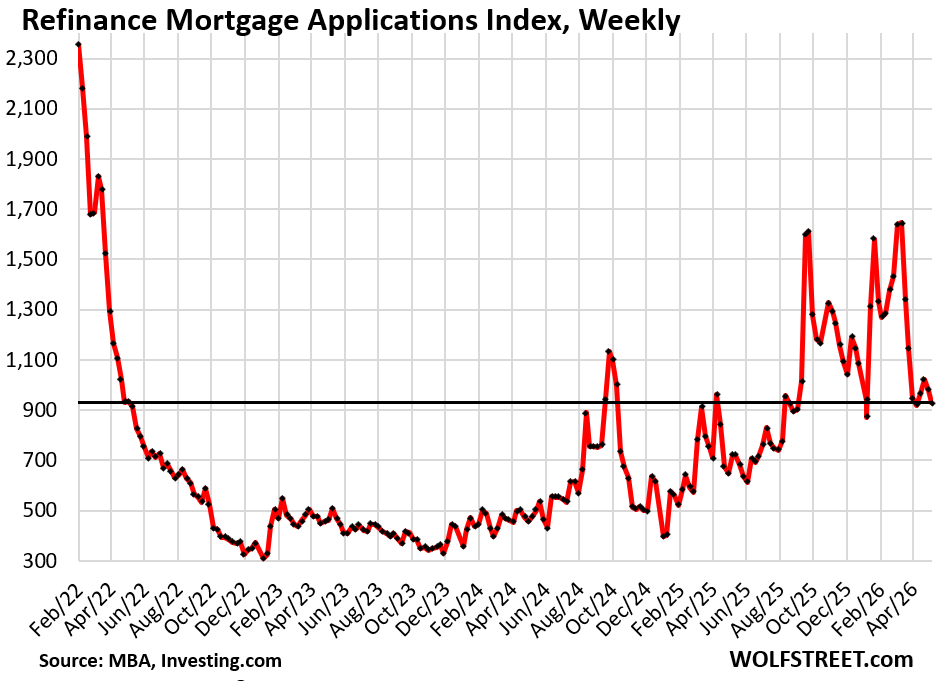

Mortgage applications to refinance a home instantly react to even small changes in mortgage rates. A dip in mortgage rates unleashes homeowners like a coiled spring to refinance a mortgage at even a slightly lower rate. And when mortgage rates rise after that dip, demand re-fizzles. These dynamics have been repeated several times since mid-2024.

Refis do nothing for the housing market, though they’re crucial for the income of mortgage brokers and lenders. But they may have a positive impact on consumer spending when they lower the mortgage payments and leave borrowers more money to spend on other stuff; or when they’re cash-out refis, the proceeds of which might then be used to pay down more expensive debts, or might be used for spending projects.

The up-front fees to be paid by homeowners when they refinance a mortgage – typically 1% of the mortgage balance – are generally added to the loan amount where they’re largely out of sight but increase the payment, which reduces the advantage of lower mortgage rates.

Homeowners can do a breakeven analysis with online calculators or through brokers and mortgage lenders, to see if refinancing a mortgage is worth it. When mortgage rates briefly drop and the breakeven analysis tilts their way, they pull the trigger, thereby creating these curious spikes in refis.

But even these spikes in refis since mid-2024 were relatively low compared to the two-year refi boom from early 2020 through 2021 when the Fed’s QE repressed mortgage rates below 3%, and everyone and their dog refinanced into these low-rate mortgages.

And now they’re part of the “lock-in effect,” when these homeowners avoid buying a new home, and thereby selling their current home, because the new home’s much higher price would have to be financed at a much higher mortgage rate, and that math doesn’t work very well for many people. But life does happen. My analysis: Update on the “Lock-in Effect” in the Housing Market: Below-3% & 4% Mortgages Fade Very Slowly

This longer view demonstrates the inverse relationship between mortgage rates (blue) and applications to refinance a mortgage (red):

In case you missed it: New Single-Family Home Prices Drop Further amid Inventory Glut. But Lower Prices Beget Higher Sales

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

When people rush to refinance after a measly 1% drop in mortgage rate, it tells me many people are financially squeezed and they think rates are going up, not down, in the future.

Generally, it’s beneficial to hold off refinancing until there is a significant benefit, so that if rates keep dropping, you don’t refinance multiple times. The costs of refinancing are somewhat hidden but costly.

It just makes financial sense in terms of cash flow if you can save $200 a month, so $2,400 a year — You expect to sell the house in a few years at a profit and pay off the mortgage with the proceeds. That calculus has been going on forever. What’s different now is that it’s easy to calculate the breakeven in real time and that refinancing a mortgage is much faster than it used to be.

For example, if the mortgage = $500,000 and rates drop by 50 basis points to 6.0% from 6.5%, and the refi fee = 1%, the mortgage balance goes to 505,000, your payment drops by about $133 a month, or by about $1,600 a year, every year for the term of the new mortgage.

You’re obviously still in the hole for 3+ years due to the fee that was rolled into the mortgage, but that’s on paper, not cash, and the hope is that you can sell your house for more a few years later and pay off the entire mortgage from the proceeds.

But if home prices drop enough in your market, a lot of these kinds of calculations don’t work anymore.

Obviously, you could save a lot more by not borrowing at all, and lots of people do that, but that’s not an option for the majority of people.

What drives me nuts are the people that start their 30 year amortization all over again every time they refi vs keeping the maturity date consistent.

Thanks wolf

“…too-high prices, and the “lock-in effect” from the Fed’s reckless interest-rate repression.”

It’s the gift that just keeps on giving 5 years later. The FED absolutely destroyed the housing market, and all shelter prices. I know of a handful of personal friends and acquaintances who did cash-out refis under 3%, substantially lowered their monthly, then took that cash windfall and poured it into another house as an “investment.”

These people act like geniuses, and they are living large. They took the gift the FED gave them and ran with it. They are asset rich (also heavy into stocks and crypto) and are spending like crazy, propping up this economy. What’s so obscene about it all is that their prolific spending is also continuing to hurt those who have no assets. And the current administration wants to continue this “wealth effect.” We have a president cheerleading the stock market daily. Trickle-down eCONomics is a lie and a scam.

A good part of the world cheer leads the stock market daily. Give it a rest.

Not really. The stock market benefits the top 5-10% for the most part. While you might think the whole “world” is cheerleading based on media coverage, that doesn’t really reflect reality on the ground, where the average Joe doesn’t care about the stock market one way or the other.

If the stock market requires trillions in bailouts every time it crashes (2008, 2020) then what is the difference between welfare and gains in the market?

Many people lack wisdom and will sell you the rope you hang them with.

Fed con game inside consumption bot numbers game. The history books we read something like the ‘penny became useless’ and ‘the flu killed millions of people’ ignoring any connection that government crisis actors and various non sense programs caused financial destruction on massive scale. There should never be an agenda like ‘maximum employment rate’ especially when ‘maximum housing inflation’ agenda is ram’d-in in parallel. Proof is in the pudding. Massive waste and corruption fueled by those in power, thank your politicians. Same can be seen of the ‘boys in blue’ surveillance systems. No privacy, no shelter, and worthless pennys and nickels. Reset the money! Shut down the programs! Stop government supply and production destruction! Figure it out in your community and know that it will ripple out to the world. In god we trust.

What a mess…

I’m waiting patiently to see how this massive waive of inflation that is about to arrive on the shores of America impacts RE. Not just the fincial impact that potential buyers experience but also the psychological impact as the war drags on and becomes far more impactful on a personal level, especially if mortgage rates continue to rise.

Thanks WR,

The prices are still too high and it needs to come down by 40% or so in my socal city.

But in socal, real estate is a like a religion. People would die before selling homes they have horded.

The FED did a criminal act by buying MBS when the housing market was on fire. By doing this, FED have locked out a generation of young Americans from the housing market.

All the ranting and raving about prices needing to come down. If it costs a dollar to produce a gallon of milk, how do you expect it to ever sell for 60 cents? The price is a conglomeration of all the things needed to build a house vs. the cost of an existing built house. I bought a small box of deck screws (like the size of a pack of cigarrettes) the other day, it was $20. Unless the government starts giving people money to buy houses, which they kinda are with these giant income restricted developments where no one wants to live, and they did with artificially low rates over the last 20 years – both bad ideas IMO- I think we’re stuck with it.

Maybe you missed Wolf’s article right before this one. Apparently Lennar can build and sell them at 2017 prices, and still make money.

That only matters for new homes. The price of a previously owned home is what people are willing to pay for it. In accounting we call that fair market value.

It can sell well above of well below replacement value.

Also in a lot of areas a lot of the cost is land value. The same home in terms of materials might be $1.5M in CA and $300k in the Midwest

The free market is under no obligation to allow people to make money doing things.

Lots of businesses go under all the time, as do investments. Housing will go under too and people will have to sell below their costs.

Long delayed price capitulation (from all time highs, albeit!) is all the more weird when US demographics are taken into account.

The Baby Boom ran from 1946 to 1964 – so let’s say 1955 was the birth year of the median boomer (truth probably skews a little more towards 1964 but 1955 is pretty close).

That *median* boomer was 60 in 2015 and 70 in 2025 (not to mention the 50%’ish, pre 1955 boomers).

I think it is safe to say that a *lot* of analysts in the late 90’s thought that the great boomer home sell-off (spiking inventory supply, dropping prices) would have started a long, long, looonggg time before now.

Plenty of intervening factors (frequently crappy US economy, ZIRP, pandemic, etc.) but demographics tends to outweigh almost everything.

And, yet, here we are, with the oldest Boomers hitting 80…and still not seeing that demographics-driven SFH supply spike.

People generally want to stay in their homes until the end. Getting shuffled out of their homes and off to PE-firm owned assisted living centers is not what boomers always dreamed about.

Those PE-firm owned assisted/independent living centers are mostly scams.

My dad passed away in an independent living facility in Salem Mass run by Erickson’s Inc in 2003. I was the co-executer of his estate and couldn’t get his deposit out ($150K) . They kept his deposit and re-rented the condo efficiency to another retireee, and kept billing his bank thus double dipping. I had to hire an expensive Mass Lawyer and pay him $2,500 to confront the management of that crooked company and stop the monthly billing and get the money back. It took over a year after he passed away to get his deposit back. I never recovered the rent paid after he passed away. Erickson’s is building a massive retirement center here in Bethesda, Md and all over the country.

The United States of Scamerica

“….shuffled out of their homes and off to PE-firm owned assisted living centers…”

Those places are absolutely terrifying. The level of care is shockingly bad, and all sorts of horrors and atrocities take place there. I’ll march off into the woods and say goodbye to myself before I ever enter one of those facilities.

Or…you could just rent an apartment somewhere where January lows are 25 degrees higher.

Selling your over-priced, 4 bedroom SFH in the frozen north does not constitute a blood-contract to enter assisted living.

If a Boomer is even remotely healthy and of sound mind, they aren’t selling $#@! — and even if not in good health, they’re still most likely not selling. Where are they going to go?

My father-in-law is 76 with Alzheimer’s and the mother-in-law, 73, has her own host of issues. They have no where to go and we won’t support them (based on previous life choices). They will claw and fight tooth and nail to stay in their home until there is no other alternative — either grave or Medicaid facility.

I wonder how the price of assisted living factors into the equation. When Dad and stepmom needed AL in 2017 it was 3k for step mom + 1k for dad. That was good for the ALF as Dad was able to help out some. I got the impression there was a shortage of customers at that time.

As boomers age the supply and demand will flip and costs will rise. Wondering if that will tip the scale towards staying home and hiring help. Not full time of course. That is always far more expensive than an ALF.

We had mass immigration.

Just wait until people are locked in at 6%

In Oct 2008 the Fed saved the banks, before saving the RE market. Without the Fed it would take decades to rise from

the ashes. Home builder can save the RE market by starving

supply. Trump saved the oil market, the dollar and LNG terminals by starving Iran. So, good things can happen. Iran, a pariah state, might benefit from being less hostile to her neighbors and by accepting basic rules of international civility. The media, seeking headlines, is so short sighted and stupid stupid, Trump tortures them 5 times a day, for fun. Yes, stupid !

Trump didn’t “save” the oil market. If there’s no significant long term structural damage prices will fall. If there is, then we’ll ramp up development i.e. drill wells that aren’t profitable at 60-70/barrel and a certain point hit oversupply again and prices will plummet. Oil hss always been boom and bust like that.

Also most E&P companies debt covenants require them to hedge a certain percentage of their production, so likely the profits aren’t as extreme as the media is making them. Sales at recent prices are likely partially offset by hedge losses.

She’ll just reported a windfall.

Yeah they will make more, my point was if they hedge 50% of production at $60-70/barrel they’re taking a loss on those hedges that offset SOME of the gains. That also depends on the debt level and convenants. A lot small shale drilling E&P companies had covenants requiring them to hedge 70-80% of their production.

Similarly the airlines should have hedges some of their fuel costs… but then again we’re now in a risk on environment where nothing bad can happen so maybe that’s only in the before COVID times

The media loves attention grabbing headlines but often the financial details are more nuanced.

I didn’t know Michael Engel was MAGA. Aside, there’s a difference between saving the oil companies and saving money for the consumers of that oil. With some kinds of policy you could probably have both, but with a war that just cuts off a substantial portion of the global oil supply, you really only benefit the producers, and only temporarily. The result is the opposite of what the president campaigned on.

Love the inverse relationship graph!!! Great job Wolf!!!!

SingleMaltScoth, something to think about.

After a certain age, our parents slowly become our children. They ask simple questions, repeat stories but depend on our patience the way we once depended on theirs. Very few understand this role reversal when it most matters. What looks like innocence or inconvenience is really time coming full circle. Don’t correct them harshly. Don’t rush them. Simply care for them the way they once protected us. This isn’t a burden. It’s repayment quietly wrapped as love.

Todd,while I agree especially if you had a good relationship with parents do not do it(care for them) to a point you ignore your own family or personal life.

Tis why multi family homes were a good thing,folks taking care of each other multi generation.

Short of that perhaps in law units and perhaps free room and board for someone who can help out with said care,tis a tough path,traveled it and it sucked in many ways/was nice in many ways.

I will check meself out when unable to reasonably care for meself,will not be a weight on others or a prisoner in a care facility.

I bought the house across the street with the idea I could rent to someone who could help in my dotage. It already came in handy when I broke my ankle and needed someone to wheel me to the loo and pop bagels in the toaster for breakfast.

Mid boomer here and hopefully a few more years before dementia or permanent incapacitation hits.

@ James

Many say that but few do. My neighbours are 91 and 99. Both can hardly walk. We look after many of their maintenance and upkeep issues and have rescued them with their occasional falls and broken bones. Food comes twice per week as ordered by computer. They waited too long to confront aging and have held out for a particular placement. I finally made them finalise a more firm plan, but it is a slow moving disaster to be honest. Rural here, neighbours help neighbours but this won’t end well. Sad, as they are like family for the past 25 years.

A few years ago I had to force my friend and tenant to take a placement in a ‘facility’. It was okay for him for a couple of years, then one day poof, he died. He had talked about killing himself in my rental so I went into his closet and removed his guns and buried them with my backhoe. Then he had falls and seizures over a few years so I got to deal with the hospital discharge team and ‘system’. A freaking nightmare. But the facility was okay…..beer fridge in room, tunes and tv, the occasional takeout, an old work buddy down the hall. He paid 80% of his $2600 per month income for this. The leftover 20% went for extras etc. Treats. Clothing. Rec.

The way it works here (BC Canada) is if you are rich you can pay whatever for wherever. If you are not flush a Govt controlled facility inspected and run with well paid unionised labour, takes 80% of monthly income with tax payers paying for the rest. Every facility, and many are private, have the same size and outfitted rooms, washrooms, bathing facilities, recreation stuff, food selections….all are pretty much the same and quite nice, actually. Dining room for food. Workers are paid for full time and must have full time shifts so they are not forced to work part time at more than one facility….just to make a wage. There is a full time nurse 24/7 for each floor and an assigned GP that can come in as needed. A nurse does all the meds twice per day. This is important…… resident’s assets are left alone….the 80% fee is only income based. If someone had a house the family can sell it and distribute. It is not estate so the funds are considered to be a ‘gift’ and left untaxed.

The problem is everyone needs a plan and/or an advocate, preferably both from the getgo. Aging is hard enough and just saying you’ll check out before is not a plan. No one ever does this unless they have a terrible disease. No one, and I have dealt with this stuff for over 20 years now with parents and friends.

When my buddy died the facility business manager contacted me with a full spreadsheet of expenses and refunds was done by cheque to the ‘estate’. In fact, as executor I just finished doing all disbursements two weeks ago. Pretty seamless, actually.

But a plan is needed. A real plan. Even pre paid funeral expenses would be a help for the executor plus disperse all funds before real decline sets in.

Go out naked like you came in…..with a smile.

regards

Don’t know where you got the idea that, ”nobody does it” with regards to folx choosing to off themself P, but I can testify that both one parent and one grandparent did so,,, clumsily in both cases, when they were confronted with major ”trauma”,,, and with their spouse already gone from dis=ease,,, and their ”quality of life” clearly gone down below their choices…

Fact is that in ALL the world ,some folx get to the point of no likely hood of any rational and reasonable life choices and would prefer to have a non violent way out of their life.

That this choice is made to seem bad is another anachronism based on way out of date ”need for cannon fodder.”

” To each their own” sooner or later MUST be the way and when all of us old farters get to choose our peaceful demise.

…and don’t ask follow up questions, they’re not gonna know the answer and it just frustrates them. Let them talk, nod your head, smile, and say, “I remember that too”, whether you do or not.

It is not difficult to stay healthy. My wife and I, in our mid 60s, have not had prescription medication, dental care, or contact with a physician in 17 years. We eat whole foods, mostly plants, exercise, drink modestly, only, and have a spiritual bent. We are both at our high school/college weight, without trying. I tried to get my in-laws — good folks, but who are adamant Fox News and sports watchers — now 92 and 93 and largely immobile (one incontinent), to eat as my wife and I do. Heck, when I volunteered to prepare all of my FIL’s meals for a week a few years ago, he was able to get off his blood pressure medication, which he had been on for 65 years. But, he did not like the food and asked to return to his normal fare. I understand duty, having raised children and helping my wife run the inherited family business after I retired. But, I am irritated that my in-laws remain brainwashed about the importance of eating good food, exercise, sunlight, etc., and have pushed the burden for their care (overseeing hired caregivers who are onsite 12 hours per day, seven days per week, at my in-laws’ expense, taking them to physician visits, buying their groceries, etc.) onto my wife and me, without getting our buy-in. From my in-laws, I have learned that I clearly do not want to be a burden to my wife, kids, grandkids, etc. Oh well, we plod along…

@John in San Diego We are about the same age (and your in-laws are about the same age as my parents). After 60 about half my friends have already lost a parent and not many parents are left, but if I can give you advice don’t waste any time trying to change the diet of someone over 80. My Dad would have never made it to 80 with his diet but “he” was the one that wanted to change his diet after a stroke in his 70’s. He now eats less sugar and drinks less than I do. Like you I have had a stable weight for decades (never getting more than 5lbs. over my college weight). My wife is actually 5 pounds “below” her college weight since she is eating better and going to the advanced Pilates class three mornings a week. Here in CA Prop 19 has allows older (over 55) people to “downsize” and keep the low Prop 13 tax basis, but I don’t see many people taking advantage of it. It seems like most people are like me and if they like their home want to stay in it until they die – I finally installed a lift in the garage so I don’t have to crawl under the cars when I get “old” when I work on them.

Ha, ha, yep, I learned my lesson (again) that you can lead a horse to water…

I feel you John. I too don’t like having the responsibility of taking care of parents that neglected their mental and physical health. We didn’t ask for it but it happens to a lot of us. I will never place the burden of my care onto someone else. I feel pretty confident that I will live a long healthy life, so I’m not to worried about that.

They would not have had these issues if they would not have been watching Fox news. LOL ( reply to John in San Diego )

One can only delay the inevitable. Sooner or later we will all become someone’s burden. George Burns outlived Jack Lalanne, so one can never be too sure how things will play out. Yeah, good old Fox News, if nothing else it is for identifying TDS among our fellow posters, that have to bring politics into every conversation.

Todd….

Well said

I really don’t feel the need to defend the scenario, but I’ll just say that the in-laws are a bunch of hippy-types, who partied their way through their entire lives, always expecting a handout/bailout, and never taking any personal responsibility. Any money they got was squandered with zero thought to the future. They also treated their kids (which includes my wife) like $#@!, whom they still gaslight and manipulate to this day. It’s a miracle my wife turned out as intellectual and well-adjusted as she is, mostly by raising herself.

The wife and I will be damned before we’re taking on the cost burden of their care at the expense of our own family and retirement.

I could written this myself. Word. For. Word.

Been there and done that and al I can say is a big AMEN!

Thank you Todd.

It’s sad that it even needs to be said.

We are a hollowed out nation if this

Is no longer the norm.

Howdy Folks. Love the last paragraph about our Prisoners…HEE HEE

Wanna Get Away??? You can t.

I don’t see the ALF as a prison. Dad and SM were able to get to their farm most every weekend where step brother and his sons lived. I’m going to hire someone to take me to the mountains every couple of weeks where I can sit by a stream. Suppose I anticipate being mentally incapacitated before being physically incapable.

But even when I broke my ankle I still got people to take me to the woods. When we saw a bear I told my friend: you don’t have to outrun the bear, you just have to outrun me!

Guess it’s the SNF that is more like a prison. And when the government is paying the bill they don’t want you galavanting around.

Bubba

It depends on circumstances…

It makes sense sometimes, For instance I refied with the credit union that held my loan.

Because it was an in house refi…. The cost was negligible.

If I recall correctly I was only out of pocket for an appraisal and some small fees for $1,200

Looking at the Amortization schedule, it saved me $30,000 over the life of the loan. Not pinched, just trying to be smart….

Smart is a big word for me though….haha

We closed our purchase in the CA Central Valley last month and moved last weekend. Rate wasn’t a factor in the least, retirement was the factor as was exiting SoCal. Orange County house will hit the market in two weeks and we expect to take a small price hit due to market conditions, but better than waiting another 2-3 years for this administration to start two more wars or the AI bubble to collapse and leave a lot of people feeling less wealthy.

Did you sell to a corporation?

1) They havent sold yet.

2) A corporation is ultimately just a group of individuals acting in unison.

3) Their recent purchase was likely at 20-40% over what it should be for the housing market to recover and be affordable.

Realtors are dropping like flies and letting their licenses expire because of the frozen RE market. Over 3,000 Realtors out of 40K+ dropped out in Maryland in 2025. 2026 will be worse. Many of the required courses to renew licenses are being cancelled because of lack of attendance. The market here is dead and frozen. This will not change for at least another decade. The only affordable houses in the Swamp are in neighborhoods that are riddled with crime and foreclosures.

It’s also something that AI can easily do. I have a friend who sold a few startups and about two years ago he invested in startup that would essentially replace real estate agents. There’s a lot of regulatory issues to deal with, but in the next 5 years I think having a real estate agent becomes a premium service for wealthy or out of state clients only.

I’m old and I remember when you could buy a new pick-up truck for $2000. I remember when a bottle of coke in a machine was 5 cents. I remember when dental appointments and filings were less than $10. I bought a 12-room house in Manchester, NH and my mortgage and real estate tax payments was less than $300 a month. We’ve had a lot of inflation; we’ve had government manipulation; we’ve got 12 political appointees setting the price of borrowed money. They’ve corrupted the money, interest rates and the economy. I went to an Ivy League University and it was $2000 a year. I never thought I’d live to see what’s now happened to America, with $40 trillion in federal debt going to $60 trillion in less than 10 years. We’re screwed and AI could make it worse with millions of layoffs.

How old are you? Ivy League tuitions were about $4-5k per year in the 70s, so you must have graduated in the 60s.

Buy some gold and a farm before it is too late

If you wait a while, you might get a better deal on gold 🤣

I’m older middle-aged. When I was a little kid, people older than my parents would say that when they were kids, the could buy a Coke for a nickel.

There is a strange tenderness in the desire to age in place.

It is not merely about refusing change. It is about recognizing that, as life narrows, the familiar becomes more important. The old chair matters. The view out the kitchen window matters. The way the light hits the hallway in the morning matters. These are small things until they are not small anymore.

When parents are gone, friends are passing, and the world feels less populated by people who knew you when, home becomes more than shelter. It becomes witness. It remembers the earlier chapters. It holds the ordinary evidence that a life was lived there.

That is why leaving can feel so violent, even when everyone calls it practical. A move late in life is not just a move. It can feel like being peeled away from one’s own history.

“Aging in place” sounds clinical, like something from a planning document. But underneath it is a very human plea:

Let me remain where I still know who I am.

Those are nice words. I wish they could apply to everyone. There is a fork in the road and not everyone is better off staying isolated in their home. My wealthy mom refused to leave when pressured, and lucked into a very kind (but illegal) caregiver. Having the time of her life. Had that not happened she likely would have been better off with the social contact of AL. This is a very expensive route, so unfortunately for the heirs, she is no longer wealthy!

A thoughtful way to look at it. Sometimes people have to be along in years to appreciate the simple things.

When President Trump is able to finally lower the mortgage interest rates, we will see the real estate market take off like a rocket! Lets wish him success on this endever like what he has been successful at in other things.

You’re kidding right? This administration (and the prior two) is doing just about everything it can to support the most self entitled generation to ever exist while telling the future generations to get bent.

Once you lot lose power there won’t be any allies in the millennial or A generations to save you. Pulled the ladder up after you did little to get yours. Enjoy rotting in the PE Home.

Kevin Warsh’s undisclosed wealth leaves a $100 million mystery atop the Federal Reserve

He disclosed his personal wealth per law, but as all of these disclosures by officials, they don’t give precise figures per asset held, but a range. That range is $135 million to over $226 million. His wife, Jane Lauder is an Estée Lauder heir and as such is super-wealthy (there’s probably an iron-clad prenup there).

You forgot the sarcasm tag. This is the internet, you need to tell people when you are joking.

Mortgage interest rates are keyed off the yields (interest rates) for 10 year US Treasuries which are set by the enormous free US Treasuries markets and are not in any way subject to political control by the White House. Mortgage rates are typically about 3% higher than 10 year US Treasury yields and I really don’t see those declining at all ahead.

I’m assuming this is sarcasm…

Big wheels keep on turning

Carry me home to see my kin

Singing songs about the Southland

I miss Alabamy once again and I think it’s a sin, yes

Well, I heard Mister Young sing about her (southern man)

Well, I heard ol’ Neil put her down

Well, I hope Neil Young will remember

A southern man don’t need him around, anyhow

Sweet home Alabama

Where the skies are so blue

Sweet home Alabama

Lord, I’m coming home to you

Probably a very smart move. I would recommend a move to Alabama to anyone complaining that housing is unaffordable. For $200k you can live like a king!

How exactly does a king live in Alabama though?

This really highlights something overlooked at the macro level–there is an increasingly smaller return to money over time.

The world’s richest man, from what I gather, spends a lot of time playing video games and ranting on internet message boards, combining the worst habits of millennials and boomers.

Everything is cheap now. Food, clothing, travel, entertainment, gadgets have all shrunk as costs. The only things still creating meaningful social differentiation by being expensive are housing, health care, and higher education. AI is already set to take big chunks out of two of those, and you I think we can assume that depopulation will take out the third. I often find myself asking, “saving for what?”

Since Covid inflation was world-wide, even in economies which did not pursue easy money policy, and in some cases was higher in countries (e.g., Brazil) which actually tightened credit, how much inflation (outside housing) is really attributable to the Fed?

And the comparatively robust state of the U.S. economy during and after Covid, compared to others with less aggressive easing (or austerity), had no benefits for working people?

That’s revisionist nonsense. In 2020, the central bank of Brazil had cut its policy rates to a record low 2%, from 17% in 2017 and from 6.5% in 2019. Mexico had cut to near-record low of 4% in 2020. That was hugely stimulative. All central banks or major countries went haywire with easing during that time – that coordinated easing was a global phenomenon.

In late 2020, inflation began to explode in Brazil, Mexico, and other countries as result of this easing and the huge amounts of stimulus through mid-2022 (it also exploded in the US). By October 2021, inflation in Brazil was 10.7%, and it was 7.4% in Mexico. While the Fed refused to tighten, Brazil and Mexico began tightening in the second half of 2021. I discussed this at the time (article from Dec 2021 inflation charts and policy rates for both countries):

https://wolfstreet.com/2021/12/09/central-banks-in-latin-americas-largest-economies-grapple-with-raging-inflation-brazil-with-shock-and-awe-mexico-with-an-eye-on-the-fed/

He’s just going to not post any comments that don’t support his boomerist debt-panic views. He knows where his bread is buttered.

First time commenting for me! (Hi Wolf, remember me from TN?).

I appreciate all the perspectives on this topic as it is on my radar, being 64, empty nester and divorced. With 3 grown children, I start to play out the different possible scenarios as I age – such a balancing act: plan and control what you can, accept what you can’t, remain grateful.

TN? Not sure what that is. Maybe “TP”?

Tennessee!

Ah-ha!!! Thanks. Welcome back.

Tennessee – we had 2 phone consults – 2023.

Alice

Congrats on your divorce!

I’m seeing more foreclosure articles in my feed, this may break the deadlock if it turns into a significant trend. This or job losses are the only things that will break this housing deadlock. Something that makes owners sell.

Foreclosures are coming up from near zero during the era of foreclosure moratorium and mortgage forbearance to the very low pre-covid levels. In percentage terms, they spiked by hundreds of percent from near zero to very low levels. Q1 update coming next week. This chart is through Q4:

@Wolf Typo: as been back -> has been back

The housing bubble is simply reflecting the fact that there is no way to avoid the final collapse of a boom engineered by credit expansion.

The average household is not sitting on piles of cash, so in markets like housing, the availability of credit has a greater impact.

DUH.

The young folks have it rough in finding affordable housing, but many of them are doing OK despite what you read.

One key to success is being employable with skills people are willing to pay for.

There has been an oversupply of people with education but limited demonstrable skills that can be turned into a good salary. These folks will have a more difficult time as AI and automation continue to expand.

Finally, if these folks who have marketable skills bank a reasonable percentage of their take-home pay and have a 401 (k), they will be OK.

No one is locked in by a 3% mortgage per se. However if folks delay selling because of low mortgage payments, they may find their equity wiped out by falling real estate prices. At that point they would be truly locked in, not by the low interest rate, but by the high loan balance.

^^^This everyone is holding thinking things will go up. Not realizing it’s probably flat to down for the next 5 years. The demographics are shifting back to what they were pre COVID

– consolidation, i.e. people have roommates again

– travel returning to normal levels and many airbnbs struggling

– no more mass immigration both international or from other states to the sunbelt

– lots of new apt supply driving down rental demand

– normal interest rates

Would it be fair to say that the housing market is broken broken beyond repair? I’d say so! Interesting that new home sales are up 1.6% in March over last year, but you say (in previous aricle) that existing home sales are down 22% (from March 2019, it seems).

Recently saw a video of a fairly young man saying he is starting to realize that he will NEVER be able to afford a home. Made me want to cry. Broken beyond repair.

And btw – it says above that the AVERAGE price of a new home built by Lennar is $374K ??? !!!

Show me a home for $374K in California and I’ll buy four of them! Makes me think of the MC Hammer song ‘You can’t touch this!’ (For $374K).

Maybe they’re selling in Texas and Alabama at that price.

And finally for a little humor, the best way to trigger Wolf is by saying that the new homes being built are of such poor quality. 😁😊

If you want a new $375,000 house from Lennar, or even a new $200,000 house from Lennar, look in Texas, not San Diego or San Francisco.

In San Francisco, Lennar will sell you a new condo for around $400,000 in the brand-new San Francisco Shipyard, which has a beautiful brand-new park right by the Bay that I love to walk through on my way back from the Mission Bay doctor’s office.

We just bought a 2000 sqft home for $375k in central CA. Plenty more here. The coastal areas are what is expensive.

Why is it so hard to believe a home can cost less elsewhere? Think of it as going to a different country. I can go to Mexico and eat breakfast, lunch and dinner off the beaten path for about $25. Does that sound crazy? Does that make me a liar? Does that make sense to someone in San Francisco? It absolutely should not be mind boggling. But when it comes to housing, people’s brains melt. “Not possible, that’s not real.”

4913 N Diana St, Fresno, CA 93726 is currently listed for $374,000. You’re welcome, send me my 3% for finding your home.

I wish the SF housing market would go down. But just keeps reaching all time highs :(

Hopefully Wolf will be right one day with his bearish predictions.

All you have to do is read these articles that I publish so you don’t have to post such BS here. Only your first sentence isn’t BS. Sentence #2 is BS because see charts below. Sentence #3 is BS because I don’t predict home prices, I show actual home prices in the past, including recent past, most recently for March.

About half of the sales in SF are condo sales. Prices of mid-tier condos have been rising recently but are still at 2015 levels, and down 12% from the peak in May 2022:

Prices of mid-tier single-family homes are still down 14% from the peak in mid-2022 though they have risen recently. They’re now where they’d first been in May 2021:

It really feels like affordability has become the biggest issue in the housing market right now. Even when inventory starts improving, high mortgage rates and elevated prices are still keeping a lot of buyers on the sidelines. The “lock-in effect” mentioned in the article is something people underestimate too. Interesting analysis overall, especially compared with some of the more overly optimistic housing headlines lately.