There’s no indication the bond market is better now in figuring future inflation; its expectation of 2.4% average annual CPI over 10 years seems woefully low.

By Wolf Richter for WOLF STREET.

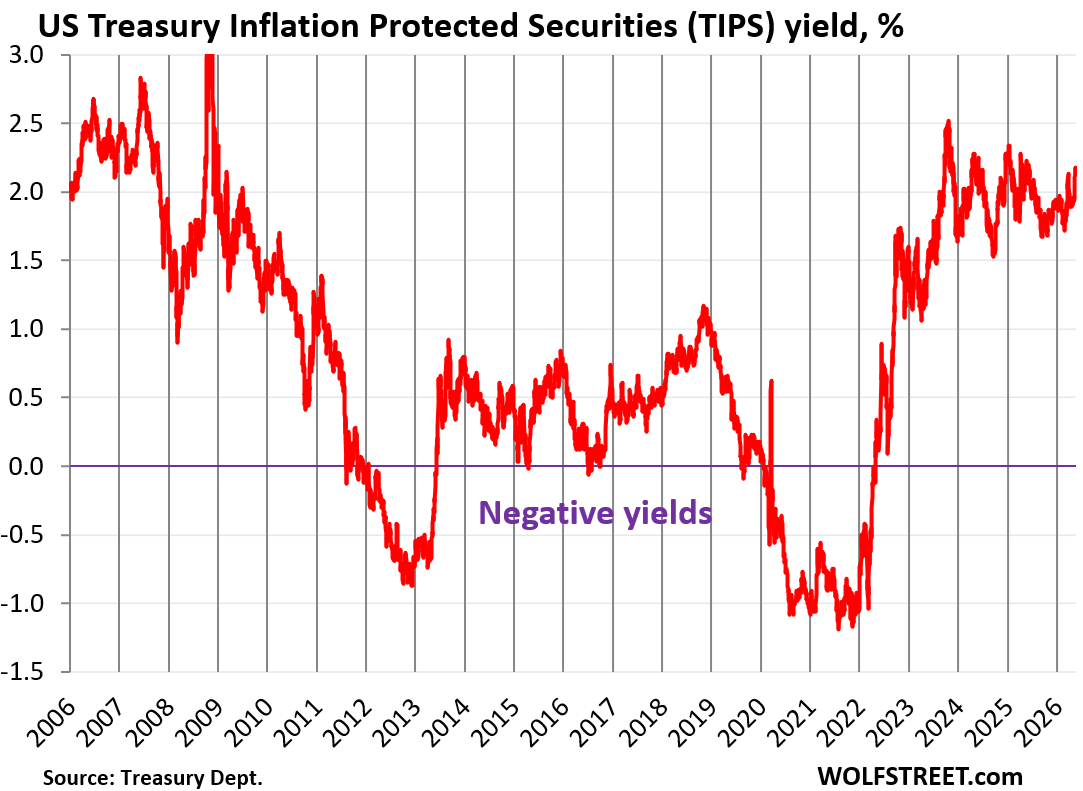

The US government sold $19 billion of 10-year Treasury Inflation Protected Securities (TIPS) on Thursday at a yield of 2.169%. The 10-year TIPS auctions occur every other month, six auctions per year. In secondary market trading, the 10-year TIPS yield ended on Friday at 2.16%.

This TIPS yield is paid in addition to the CPI-based inflation protection that TIPS holders receive and that is added to the principal and is paid when the TIPS mature. So the principal of the TIPS grows over time with CPI. The interest rate (the percentage is fixed for the term of the TIPS) is applied to the entire principal, including the inflation protection. As the principal grows over time with CPI, the interest payments increase, though the interest rate remains fixed.

If CPI inflation averages 3.5% per year over the next 10 years, these TIPS buyers will get a combined yield of about 5.66%. If inflation averages 2.0% over the next 10 years, the TIPS buyers will get a combined yield of 4.17%. You can see where this is headed: the bond market’s delusional “inflation expectations.”

The chart above shows that the TIPS yields went negative during QE when the Fed’s heavy-handed purchases of TIPS dominated the TIPS market.

The TIPS market is relatively small and not very liquid, with only $2.1 trillion in TIPS of all maturities outstanding, spread over 5-year, 10-year, leftover 20-year (issuance was discontinued in 2009), and 30-year TIPS. In this thin market, the Fed’s purchases of TIPS during QE pushed the TIPS yields deeply into the negative.

The bond market’s “inflation expectation” is the difference between the regular 10-year Treasury yield (4.56% on Friday) and the 10-year TIPS yield (2.16% on Friday).

If the bond market thought on Friday that average CPI inflation over the next 10 years would be 3.5% per year, the regular 10-year Treasury yield would have been 5.66% (inflation-protected yield of 2.16% plus average CPI inflation of 3.50% per year over the next 10 years).

But that’s not what happened. On Friday, the bond market figured that 10-year average CPI inflation would be 2.40% (regular 10-year Treasury yield of 4.56% minus the 10-year TIPS yield of 2.16%).

If the past is any indication, the bond market is delusional about future inflation.

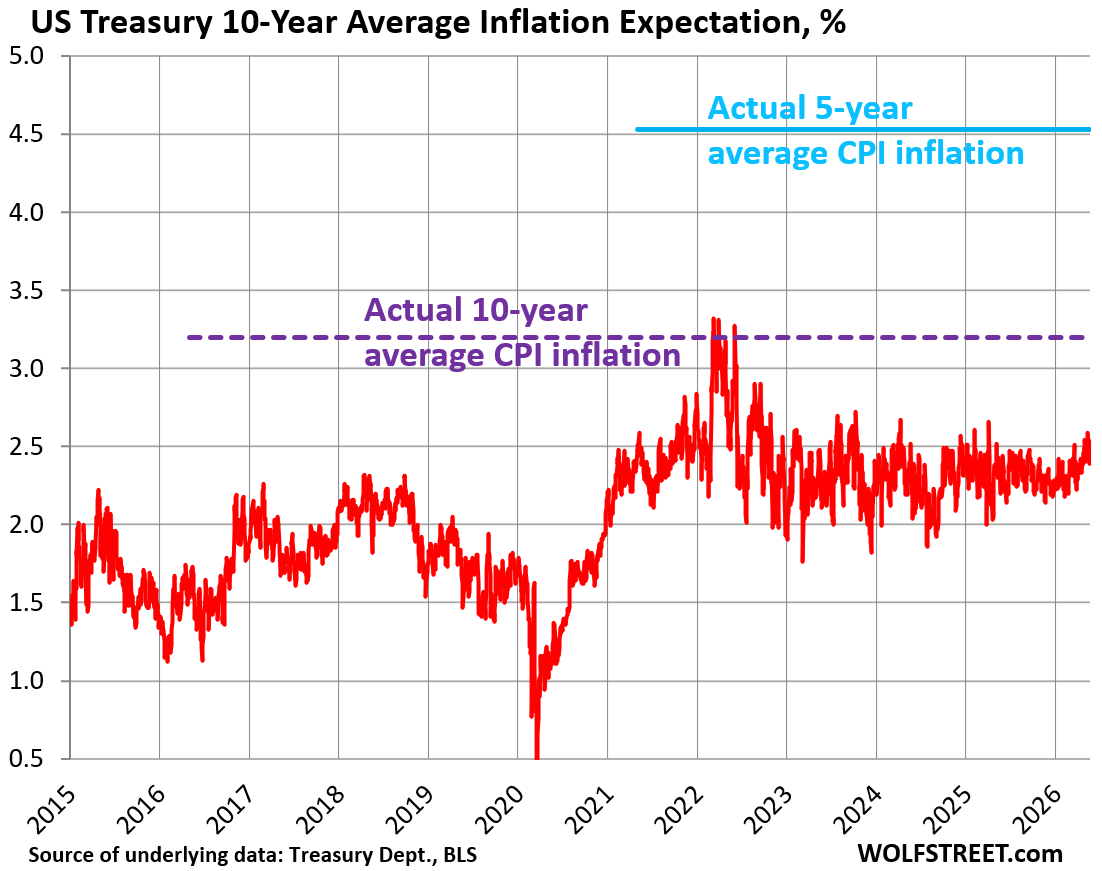

In May 2016, the bond market figured that over the next 10 years, CPI inflation would average about 1.8% per year. As we know now, as these 10 years are up, actual CPI inflation over those 10 years averaged 3.2% per year (dotted purple line in the chart below).

In May 2021, after inflation had already begun to rage, the bond market still thought that over the next 10 years, CPI inflation would average about 2.4%. But over the first 5 of those 10 years, actual CPI inflation has averaged 4.5% per year, nearly double (light-blue line).

In fact, the bond market has been totally delusional about how high actual CPI inflation would be.

Buyers of regular 10-year Treasury securities totally underestimated actual future CPI inflation, and yields ended up being way too low compared to TIPS and way too low compared to actual CPI inflation, and those good folks got ripped off.

And there is no indication whatsoever that the bond market is any better now in estimating what future inflation will be, and its current estimate of 2.4% average CPI inflation per year over the next 10 years seems woefully low.

Which is why this observer is not touching 10-year Treasury securities at these yields – not even with a 10-foot pole.

The insidious effect of the Fed’s TIPS QE.

The Fed’s QE – when the Fed buys massive amounts of longer-term Treasury securities and MBS to push down longer-term yields and mortgage rates – is by definition a strong-arm method of outright, explicit, and much-hyped market manipulation.

But the Fed’s purchases of TIPS added an especially insidious side to QE. The Fed’s purchases of TIPS pushed down TIPS yields into the negative and created the deceptive perception that the market’s “inflation expectations” were “anchored” at very low levels – below 2% through 2021 – which Powell touted at his insidious press conferences in the first half of 2021 as rationalization why there was no need to end mega-QE or to raise rates, though inflation had begun to rage.

In other words, the Fed’s QE manipulated down the Fed’s very yardstick that it used to defend QE and ZIRP despite raging inflation. This was one of the factors that made it the most reckless Fed ever in 2021 (Google that phrase), and Powell was the architect of it.

But QT ended that eventually. And now there is no longer any excuse for the bond market to be this delusional about inflation.

Pouring a bucket of ice water on TIPS.

TIPS have nasty tax consequences. The inflation protection counts as taxable income. Each year, the inflation protection that was added to the principal during the year will show up on the 1099-INT for that year. And the coupon interest payments also show up on the 1099-INT. So TIPS trigger a tax liability every year for the inflation protection that won’t actually be paid until maturity, in addition to triggering a tax liability for the coupon payments that were actually paid, which is why TIPS remain unpopular.

And as is the case with other longer-term Treasuries, when yields rise, TIPS market prices decline, but due to the relatively low liquidity in the TIPS market, selling TIPS, especially in a hurry, might come with a nice haircut.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Best explanation of what tips really are

Tips aren’t that bad.

Look if you think inflation is going to go Crazy, which we all do right?

I mean Warsh just basically said he will never raise rates. And he has tons of pressure Not to. So someone else will clean that up later, maybe?

So tips pay you, quite well, if inflation is high.

Pretty simple.

Interestingly, 10 year TIPS have outperformed regular treasuries by ~1% per year over the last 30 years.

Which makes sense because as Wolf shows, the current TIPS yield underestimates inflation by about that much, and since the advantage of TIPS is that you win if inflation is higher than everyone expects, the difference between expected inflation and actual inflation should equal the amount TIPS outperform regular Treasuries.

TIPS return likely higher because of both the tax penalty problem, as well as the “market can’t predict inflation” problems that Wolf noted.

If you want inflation protection and are either in a really low tax bracket or have a nice tax-deferred account, TIPS can make a lot of sense.

If you don’t want to buy individual TIPS (and even 5 years can feel like a long time), The VTIP ETF is shorter in duration (2 years) than any other TIPS ETF, and therefore won’t lose you much if you turn out to be wrong.

No, we don’t all think inflation is going to “go crazy”.

AI should be one of the most massively deflationary technologies in history, having its initial impact in sectors that have shown the highest CPI growth over recent decades such as education and medicine.

Already you see teenagers (and their parents) saying college isn’t worth it alongside universities lowering tuition and closing. You see similar poor performance in managed health stocks (United Healthcare, etc) as people send the photo of the spot on their arm to AI for initial assessment. Over the medium term this will begin to impact every sector.

If the AI timeline is off, the negative return on AI infrastructure build out will cause a massive recession and force the Fed cut rates dramatically to stimulate. Remember, without AI infrastructure spending, we’re already in recession and have been for years.

The great wealth transfer will be in full swing over the next couple decades, and that’s hard to model as it’s never happened before, but I tend to think that will dramatically lower housing prices when combined with below-replacement fertility rates.

Of course, politically we’ve got a guy who wants to cut rates into inflation, and expectations for that kind of behavior have bled into the stock market and the wealth effect, but his movement does seem truly dead.

ZIRP was around far longer that the recent COVID-19 inflation, and it makes sense that this is the new baseline over the long term.

Tips are just another government scam. Just like 401ks and IRAs where it grabs your gains at ordinary tax rates vs capital gain rates upon withdrawal by forced RMDS. And the next serial scam is adding IRMMA as a tax on your income.

Throw in the Fed manipulation and guess what and who wins?

Sunrise is also a government scam because it makes you go to work and earn money and pay part of it to the government.

Well, there is the “Sunshine Tax” — though that is purely a state-level thing and not Federal.

Seriously though, as I’m approaching retirement and learning about IRMMA I have to agree with a that it pretty much is a scam. Not the idea that those of higher means should be forced to pay more into Medicare so much as the way it is structured with the hard cliffs — $1 over and you’re screwed for a year — as well as the 2-year lookback. It takes very careful strategizing and constant monitoring of your MAGI throughout the year to avoid the trap.

Unless you work the night shift….!

Somehow preferential Capita Gains rates are the natural order of the world, completely originating outside of Federal Government remit.

Let me tell you, given the political winds, you might want to realize some of those preferentially treated capital gains in the near term.

The consumer is a conspirator as well in the outlook for inflation, when it comes to prediction

The consumer price inflation expectation, calculated by the Federal Reserve Bank of New York, is coincident with announced inflation , indicating there is little connection between the present and what is actually coming in the future

Forecasting future outcomes tend to be based on extrapolation , where the current becomes the future, not a result of the past

Great depth here. Thank you. Why is the bond market delusional? What’s driving this? I’m inclined to say it’s the market structure. My take is that large asset managers act as quasi-agents for policy goals because their incentives align accordingly. Not conspiratorial, just the reality of the role of government in their businesses. I suspect that such disconnects as you observe only happen in one direction: lower yields. Thx.

Good start Ken,,, but the actually proven facts, by any kind of rational analyses, is that the FED IS,,, and always has been a servant of the rich and richer.

And to be more clear, those folx who continue to want to be the ”rulers” or kings of our financial world, and be clear that it is now acknowledged as THE entire global world, have utilized the micro and macro management of the financial parts of our global economy to control any and perhaps all of the gains of the worker folx who somehow continue to make USA and many other nations keep operating… Keep operating in spite of the vast devaluations of USD and other currencies kept by workers, etc., and also in spite of the vast and continuing attacks at all levels by the clearly deranged folx thinking that a low level incident will change policy, which, so far, clearly those attacks do not change anything…

Good justification for NOT playing “just the tip”.

Most reckless Fed ever, indeed. Gross manipulation and deception, and we’re going to pay for it for a generation.

I thought that Wolf’s article captured the apparent grift between the official report of the rate of inflation versus the actual rate of inflation

Then as I was driving to the remote mine where I was working

I thought I was imagining what my eyes were looking at was an alien vehicle that appeared to be shaped like a hoagy roll two football fields in length

levitating silently at a slow rate as if in first gear, speeding up as it drifted over the top of the truck and then instantly vanishing without a sound

That’s why you buy tips in a IRA.

Yes, IRAs and SEP IRAs are the places to buy TIPS. But make sure you don’t load up on too much of TIPS when you get closer to 73 because you have to make RMDs, and you don’t want to have to sell TIPS to meet your RMD requirements.

Roth MAYBE, depending on the state you claim residency in. But I’m not so sure about buying them in a trad IRA. The coupon pmnts and inflation protection portion of TIPS are both protected from state income tax when held in a taxable account. Buying them in a trad IRA exposes both fully to state income tax. So you lose one of the benefits of ownership. I don’t put any of my money in trad IRAs because I never want to be in a lower tax bracket than I am now (read as: I never want to have less income than I have now), and my flexibility to absorb the impact of taxation is far greater while I’m still working than it will be when I stop working. Tax rates have never been much lower than they are now and our debt is as high as it was when tax rates were at their highest ever. Every other time in our short little history as a country that war has resulted in massive debt run up, Congress has eventually answers by raising tax rates. So why would you want to postpone taxation into the future? They don’t call trad IRAs tax postponed accounts because tax deferred is far more marketable, but postponement is what they actually do. The government will keep pulling the dollar devaluation levers before they raise tax rates until that lever breaks, but eventually, tax rates have to go up or this whole thing turns to shit. Yes, spending cuts would help too, and frankly, I think we’re going to need all three to right the ship. If marginal rates went back up to WWII levels (the last time our debt was where it is now) I’d consider postponing taxation into some of my income. But not now. And I’ll probably never buy TIPS anyway because I don’t trust the central banks not to manipulate their pricing.

“A tax delayed is a tax not paid “

unless you’re an heir.

Excellent observations, particularly that trad IRAs are just a tax-timing device. Just to add a few comments. As a retiree, yes, the RMD tax is significant. Though I’m lucky as a Florida resident not to pay state tax on my RMDs. Also, I can do a qualified charitable distribution with my RMDs, so there’s some additional tax flexibility there. And the annual income on my IRA is generally more than my tax on the year’s RMD, so there is some IRA growth in that respect, separate from any appreciation growth.

You may not have that much control over future income.

IRA is a form of insurance for harder times. You can’t easily save enough in it (pre-tax) to retire with a truly high income anyway. Compounding helps but a million bucks just ain’t what it used to be!

If all goes well, you’ll leave most of the IRA to your kids – and if you raise them right, odds are good they’ll be happy to have that inheritance, even with the tax hit.

In Britain I’m tempted to buy an ETF of TIPS within a tax shelter called an ISA (Individual Savings Account) – no income tax, no capital gains tax, and I can hold hedged into GBP.

Though how long ISAs will survive on such generous terms, God knows.

But would a diversified ETF of international index-linked bonds be a better bet?

Wolf, what are your thoughts on Series I bonds? Better than TIPS for the little guy?

I bonds have great tax advantages (tax deferred income until you cash them in). And you can sell I bonds back to the government at face value, after 5 years without penalty. That’s great when yields rise. And worthless when yields fall.

But the base rate on current I bonds is only 0.9% compared to the 2.16% TIPS yields. The base rate needs to be higher before I bonds become attractive IMHO.

I am uncertain about the real protection that TIPs offer during inflation, and welcome balanced perspectives.

TIPs appear to provide protection against inflation by accounting for CPI

However, interest rates normally rise when inflation hits. TIPS do not seem to protect against the rise in interest rates as result of inflation.

Look forward to your views

When yields rise, market values decline for bonds that are still years away from maturity. The closer bonds get to maturity, the closer market value gets to face value. When you hold to maturity, you receive face value. So if you hold to maturity, market value (up or down) doesn’t matter to you. Bonds are not like stocks. Stocks don’t mature, and you have to sell them to get your money out. Bonds mature on a specific date, which is when you get your money out automatically at face value.

This was an outstanding explanation and article.

Thanks!

Agree with you 100%. Learned a lot.

The government is constantly trying to Jerry rig the system to get more spendable money out of it. This has become the Treasuries/feds job! Next it will become AI job at the Treasury/FED/government/whatever.

Paper money will have less and less true value, assets will appreciate more and more in terms of paper money. The government will tax assets more and more as inflation drives up asset prices. Do not forget that asset prices do not all rise at one time, home prices might drop and grocery prices might go up, but they all appreciate eventually.

Great explanation. It seems this is exactly why one SHOULD consider TIPS (in an IRA, etc) in preference to the regular Treasury notes.

Re: The insidious effect of the Fed’s TIPS QE.

I’m not sure I see your logic in this paragraph? The implied inflation rate is the 10-yr Treasury less the 10-yr TIPS. If the Fed were buying TIPS heavily, then it would depress the yield on the TIPS and *increase* the implied inflation rate. The reverse would happen if they were supporting the 10-yr Treasury.

A good read, though. I absolutely agree that the implied inflation rate here is far too low.

For the average investor at this moment in time, I don’t see the point of buying treasuries longer than 2Y notes. Ideally, you stay in bills for now. Warsh is going to have a very interesting 2.5 years under Trump.

And when a recession arrives, it will be very interesting as to the root causes. For now, nothing appears to be lining up as a good bet it will arrive in the next 12 months.

In addition, the Fed appears to be very willing to let the economy run hot. The question is what temp provokes them into raising rates. I don’t think words like “transitory” are going to cut it nowadays.

Given the closure of the Strait of Hormuz, and the threat of supply disruptions, yes, anticipatory hoarding could well produce a spike in inflation, but the subsequent recession/depression will be marked by a collapse of demand, and resulting deflation (particularly in housing). In such a scenario, the current TIPS rate might not be underestimating average long term inflation, yes?

The subsequent recession/ depression will cause demand destruction.

What will cause this economic downturn and associated demand destruction? This has been the question for a decade and a half!

The last “recession” was mandated, and accompanied by subsequent “pent up demand,” all paid for by pennies from heaven!

I don’t think I will lose my appetite. Many of the services in this service-driven economy are actually mandatory and/or mandated. Home and insurance services come to top of mind. Others become required by the growing number of people who have too few skills to “self-serve” their needs or desires.

Yes, mass unemployment can destroy demand. What will destroy the jobs? (AI? -too soon, War? -Not yet on American soil, Demand destruction? -self fulfilling prophecy?).

Economists have predicted 38 of the last 3 recessions!

Read more of Wolf’s stuff.

Inflation is in services and has been ramping up for a long time. The recent business in Hormuz is just a kicker.

Also, personally I don’t think the Persian Gulf settles down anytime soon… talking years, not weeks. That hornet’s nest has been poked too much. If in fact a lasting peace is achieved I’ll be amazed.

Wolf,

You have long warned us about the hazards of TIPS. Thank you for providing the details in this post. The clarity of your presentation is greatly appreciated.

Except he’s not saying TIPS are hazardous. He’s saying nominal long bonds are hazardous because the market is underestimating what the future inflation rate will be and nominal bonds are therefore too expensive (or, equivalently, their yields are too low). TIPS don’t have that problem. You get >2% real (after inflation) return on your investment, which is guaranteed if you hold the TIPS to maturity.

It’s pretty clear (at least imho) that Wolf is saying TIPS are hazardous if you’re not certain you can hold a TIPS till maturity.

If you Can hold a Treasury bond until maturity, I’m not sure if he’s saying a TIPS is inferior or superior to the equivalent length regular Treasury bond.

Google AI says:

” Choose a regular Treasury if you believe inflation will be lower than the market’s implied break-even rate (10 yr Treasury minus 10 yr TIPS). Choose a TIPS if you believe inflation will be higher than the market’s implied break-even rate.”

The trouble with this is that Wolf makes a pretty convincing case that the break-even inflation rate underestimates actual inflation. But he stops short of saying that a TIPS is preferred if you’re certain to hold to maturity, so I’m not sure if he has an opinion on conventional Treas bond vs TIPS.

Some further clarification on TIPS and inflation expectations:

Yes, the market is not particularly good at predicting inflation over long periods. In fact, bond markets have historically underestimated realized inflation over time.

When people talk about “market inflation expectations,” they are usually referring to the difference between nominal Treasury yields and TIPS real yields — commonly called the “breakeven” inflation rate.

For example:

5-year Treasury yield = 4.0%

5-year TIPS real yield = 1.5%

→ 5-year breakeven inflation = 2.5%

That does NOT mean inflation will definitely average 2.5%. It is simply the inflation rate at which investors would be indifferent between owning nominal Treasuries and TIPS.

Also, most professionals focus more on the 2- to 5-year part of the curve rather than the 10-year breakeven, since shorter maturities tend to be more sensitive to actual inflation trends, energy prices, Fed policy, and economic data.

Importantly, these are traded market securities. Breakevens move daily and can be heavily influenced by headlines, positioning, liquidity, oil prices, and risk sentiment — not just “true” inflation expectations.

A lot of people online talk about breakevens like they’re some crystal ball for future inflation, but that’s not really how they work. They’re better thought of as a pricing signal from the bond market at a specific moment in time. Markets can be wrong, emotional, early, late, or reacting to things that have nothing to do with long-term inflation.

So in practice, breakevens are often used more as a relative value tool:

• If you believe inflation over the next 5 years will average ABOVE the breakeven rate, TIPS are likely the better investment.

• If you believe inflation will average BELOW the breakeven rate, nominal Treasuries are likely more attractive.

That said, TIPS are not a perfect inflation hedge. They can still lose money in the short run when real yields rise, liquidity dries up, or risk markets become stressed. Breakevens themselves can also move sharply based on sentiment and positioning.

But over time, TIPS do help investors keep up with CPI inflation because the principal adjusts with the CPI index. For investors looking for a U.S. government-backed security tied directly to inflation, TIPS are probably the best tool currently available.

Beyond inflation views, TIPS can also serve as a useful diversification tool, particularly in long-term or tax-deferred portfolios.

That explains it well, thank you very much!

Thanks for the nice description for TIPS.

It would seem that a Roth would be the ideal place for TIPs.

But perhaps they too might be subject to risk if the published CPI numbers become manipulated. Is that far fetched or considered a legitimate risk?

I also don’t understand the bond market and the underlying calculus of future inflation. Is it possible that market participants have drank the index ETF Kool Aid so much that demand is too low to reflect future CPI? It’s clear that the short term yields are so low that it pushes money into other investment vehicles. And with the bubble brewing (CAPE Ratio ~ 42, Buffett Index @230), what’s an investor to do?

Sounds like you’re finally questioning the official narrative on inflation and the reliability of stats like cpi as well, Wolf.

That’s not AT ALL what I’m saying. You may have to re-read the article.

It really never ends well for those who try to interpret what you’re saying. It’s much better if they make up their own BS that’s not trying to restate your point(s).

It’s like that Far Side cartoon about what dogs hear. Blah, blah, blah, conspiracy, blah, blah, [hyper]inflation, blah, blah, question.

“Apes don’t read philosophy”

“Yes they do, Otto, they just don’t understand it”

Trust the “official” numbers or not: they are driving the bus.

Knowing what the numbers are communicating opens the door to taking a rational approach to finance and economy.

This type of comment makes me think of Wolf’s occasional articles featuring dot plots and spaghetti graphs. “Market expectations” are notoriously wrong! As are most predictions about the future.

If timing doesn’t matter, then following a futurist is interesting (not really actionable advice).

If you’re wanting to know what drives policy? Look at official numbers.

Rose tinted glasses that FRB stamped on in 2021/22 were not fit to be put back on one’s head.

Even a novice like me who lost ~ 10% on their ‘defensive’ slice of their pie the lesson was learnt quickly. Short dated held to maturity outside an open ended fund, or don’t bother (I’m uk so thinking gilts and usd debt)

I wouldn’t bother on 10yr until the yield was 8-10%

Thanks Wolf for “The insidious effect of the Fed’s TIPS QE.” part.

Thank God Powell is out now as FED Chair. Trump bogus criticism and charges gave Powell people’s sympathy. Sure, he defended FED’s independence.

But he led the FED to take ALL Asset prices to ATH. He is to be blamed for all relaxed monetary policy and all inflation not coming back. Now also he wants to look through the inflation surge.

Balance sheet at 6.7T is as good as Treason.

“But QT ended that eventually. And now there is no longer any excuse for the bond market to be this delusional about inflation.”

You meant QE? I assume the Fed is no longer buying tips.

No, the sentence is correct. You may have misread it.

Good article Wolf … that last chart is mind boggling. I’m sure glad that inflation is transitory! lmao

Trump paused beyond: FIFA, the 250Y jubilee and midterm election. FIFA might be a bust. Oil extraction shifted to Americas:

Argentina, Brazil, Venezuela, Guyana, the US and Canada. We export

more LNG than any other country. Oil tankers cost: barrels x distance. After opening the Hormuz more tankers entered the market.

NVDA CUDA.X , Omniverse and Dassault can build oil tankers,

cars, engines, missiles and planes. We can increase productivity with a system which predicts physical reality. We can test robots in virtual reality. Virtual reality female partners can teach engineers and high school kids working in factories, real estate agents, home builders and designers. We might deflate. Demand for highly skilled and skilled workers will rise. We need a lot of them. Their real income will rise.

Tips never were an enticement. Atlanta gdpnow is at 4.3%. Inflation over 3%. N-gDp too high.

In 2020 the Fed sucked liquidity first before charging 9%, instead of 18% or 20%. Home cooking is healthier. When u eat at home TIPS are negative.

After opening the Hormuz straight lower oil prices reduce inflation. Along with Dassault and NVDA CUDA X, which increase productivity, the Fed will have to cut rates and stay low for years.

So, an open straight gets us back to 4%?

Treasury rout tests Washington’s tolerance for higher borrowing costs

I think of TIPS as a tool for maintaining wealth, not building wealth. I retired early and built a TIPS ladder in my Traditional IRAs to bridge me to taking SS at 70. I would not use my Roth IRAs for that. I want to spend down my Traditional IRA before touching my ROTH IRAs. My TIPS and Social Security are my safe bucket of money (both inflations protected) to pay for the basics: keeping the lights on and the refrigerator full. I own VT (Vanguard Total World Stock Index Fund ETF Shares) in my Roth and those are the funds I hope to grow my wealth with. Could I earn more by putting my TIPS money into a broad market index ETF, probably. But tips can help you sleep at night. I don’t loose sleep over what our crazy president will do next. As William Bernstein says, “When you’ve won the retirement game, stop playing it” — specifically with the money you need for basic living expenses like rent and groceries.

Thank you Wolf and readers for educating me.

Actual headline tonight “Hassett says ending Iran war may create room for rate cut”

They won’t stop until they kill it all.

That’s copy-and-paste of what he’s been saying for two months.

I’m not surprised. He only says two things and Wall Street really really wants him to keep saying them

Thank you Wolf for the articles and your measured responses.

Yes, thanks to The Fed there is no true pricing of risk or inflation in the bond market. The knock on affect is no fiscal discipline in congress.

So does this mean that TIPS cause an understatement or under-reporting of national debt, since the excess inflation-related interest is added to the principal of each issuance? Probably not a big deal if TIPS are only $2 trillion out of almost $40 trillion. But does the reported national debt include the accruing interest related to TIPS.

Also, I have noticed that various news outlets have shifted to only reporting the U.S. debt held by the public. That seems new and also seems misleading.

“So does this mean that TIPS cause an understatement or under-reporting of national debt, since the excess inflation-related interest is added to the principal of each issuance”

No, it does not understate the national debt because the added inflation protection is added to the total balance of TIPS outstanding (currently $2.1 trillion).

It’s fun to watch all this. The stock market recently started having a larger market cap than the federal bond market, but there’s another $1T in debt coming soon. It’s like watching a horse race to see who’s winning. Liquidity is coming out of the housing market, crypto has Michael Saylor talking about selling BTC, but stocks and bonds only have the moon in front of them. It’s so exciting, lol.

It would appear that the 5-10 yr part of the cure isn’t a good judge of actual inflation and only goes as far as pricing in an amount of inflation close to what the Feds target for inflation expectations are. 30 year nom yields vs last ng Tips tells a better story so use those inflation expectations and apply to 10 yr relative value Tips/Treas to judge rich or cheap.

Seems to me most have on here have an illusion about “absolute real wealth”. Money – be it dollars, equities, bonds, gold or other assets have no other value but to buy human work/time.

But the demographic cliff is real: In the future there will be a lot of more older folks competing for services and products from much less younger folks, and the only means they will have left to compete for those services of the younger generations will be assets, for which their will be less demand than their is now….

Is it possible the Fed will change CPI to be trimmed mean CPI like the Dallas Fed? To me they might decide to change how things are measured by getting rid of the extremes.

There is no such thing as you describe.

1. The Fed’s preferred inflation measure is not CPI, but the PCE Price index.

2. What Warsh said is that

— current inflation indices are flawed and old-fashioned in their methodology, and that he wants an improved index that tracks “a billion prices.” And that’s probably a good idea.

— that he would look at ALL inflation indices to see the trends of underlying inflation (cooling v accelerating), including the Dallas Fed’s trimmed mean index. And that’s probably a good idea too. But the Fed already does that, obviously, so that’s not new.

3. What Warsh did NOT say is that he would switch the Fed’s measure of inflation from the PCE price index to the Dallas Fed’s trimmed mean index… he didn’t even suggest that. If he tries to do that, it would be a bad idea. But he didn’t say anything like that.

and one tunes into the financial shows (stock market infomercials) and hear such as

* It will be tough for the Fed to raise rates

or

* There probably will only be one rate cut later in the year.

There really are no rules for the Fed, apparently. Prices over target, prices rising over the pegged Fed Funds. Stock markets new highs each day (irrational exuberance anyone?)