Cut the price, and they will buy. Dealing with the affordability crisis. Sales volume is up, but shares have plunged by nearly 50%.

By Wolf Richter for WOLF STREET.

Lennar, one of the largest homebuilders in the US, reported Q2 earnings this evening. In terms of the travails of the housing market, they’re revealing. Lennar targets the mass market and sales volume. In this “affordability crisis,” as it’s often called – where no homeowner wants their home to become affordable – Lennar has been cutting sales prices and piling on incentives to boost its unit sales in a very tough market.

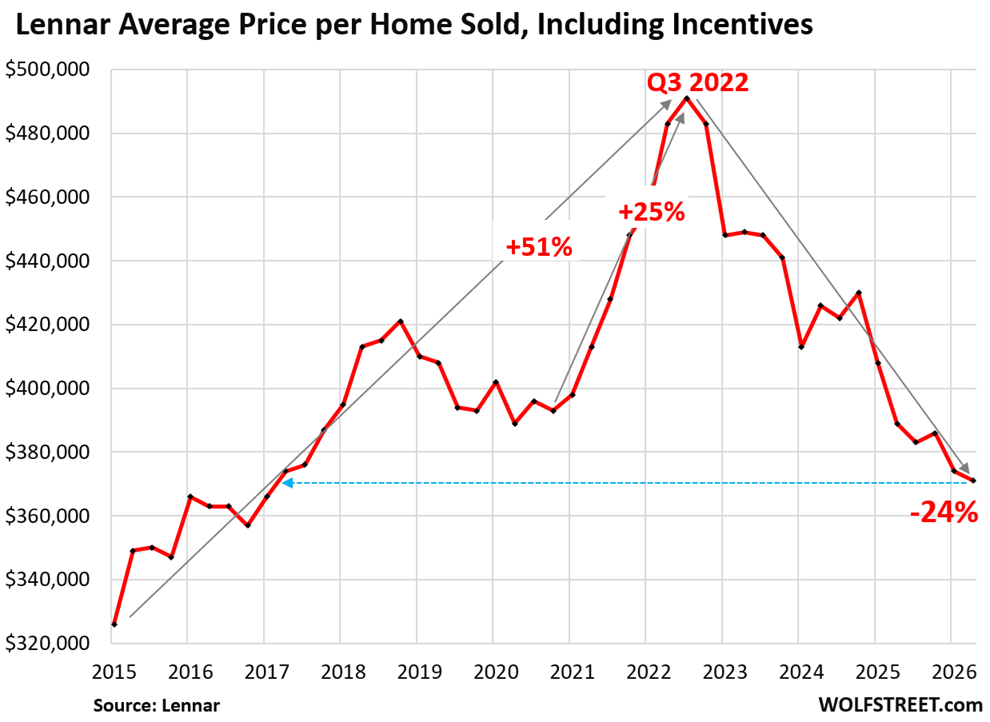

The average sales price, including incentives, fell further, both per home sold and per square foot. It largely came at the expense of gross margin, which fell to 15.6%, from 17.8% a year ago, and from 29.5% in Q2 2022, at the FOMO peak. Efforts to whittle down construction costs – they declined by “13% over the last several years,” it said – also helped. But land prices rose.

The average price per home delivered in Q2 fell by 4.6% year-over-year to $371,000, “primarily due to continued weakness in the market” and “reflecting approximately 12.9% in incentives, along with base price adjustments necessary to sustain volume in a market where affordability remains the defining constant,” the company said. That price is back where it had first been in 2017 and is down by 24.4% from Q3 2022.

But that decline in the average sales price comes after massive price increases, including 25% in less than two years, when homebuyers were eager to pay whatever, and Lennar let them.

lower prices do the trick in a tough market amid the “affordability crisis” where no homeowner wants their home to become affordable: Lennar’s deliveries rose by 2% to 20,519 homes, though its revenues from homebuilding fell by 3% due to the lower sales prices.

“Our strategy consistently has been to execute around the affordability challenge rather than wait it out. We have prioritized volume to create durable scale advantages, to deliver that volume at lower prices, and ultimately improve margins,” the company said.

“Our costs are down materially over the past two years, volume is holding, our asset-light balance sheet is functioning extremely well and improving, and our technology initiatives are defining a new Lennar,” the company said.

“We remain deeply committed to building the homes America needs, at prices families can afford, and to generating the returns our shareholders deserve,” it said in the earnings report, and we’ll get to those returns that shareholders deserve in a moment.

“Gross margins decreased primarily due to lower revenue per square foot and higher land costs year over year, which were partially offset by a decrease in construction costs, reflecting the Company’s continued focus on cost-saving initiatives,” it said.

“Our construction costs improved another 2% sequentially and 13% over the last several years. Our cycle time reached a new record low of 121 days, down from 122 days last quarter and 132 days a year ago. We reduced our inventory to 2.1 homes per community from 3 homes per community last quarter, and our inventory turn stands at 2.5 times,” it said.

To return to its phrase, “generating the returns our shareholders deserve”:

- Operating earnings from homebuilding plunged by 32% year-over-year to $489 million.

- Net income plunged by 36% year-over-year to $305 million. Compared to Q2 2022 ($1.32 billion), net income plunged by 77%.

- Earnings per share dropped by 31% to $1.24. Compared to Q2 2022 ($4.50), EPS plunged by 72%.

Lennar has been giving up a big portion of its gross profits, net profits, and earnings per share by offering lower prices to gain market share in a tough market steeped in the affordability crisis, and it has been working on bringing its construction costs down to mitigate the effects of those lower prices.

In terms of sales volume in a tough market, where home prices are too high, this strategy has been successful. Lower the price, and they will buy. This is exactly what today’s affordability-wrecked frozen housing market needs. Bring on the affordable supply.

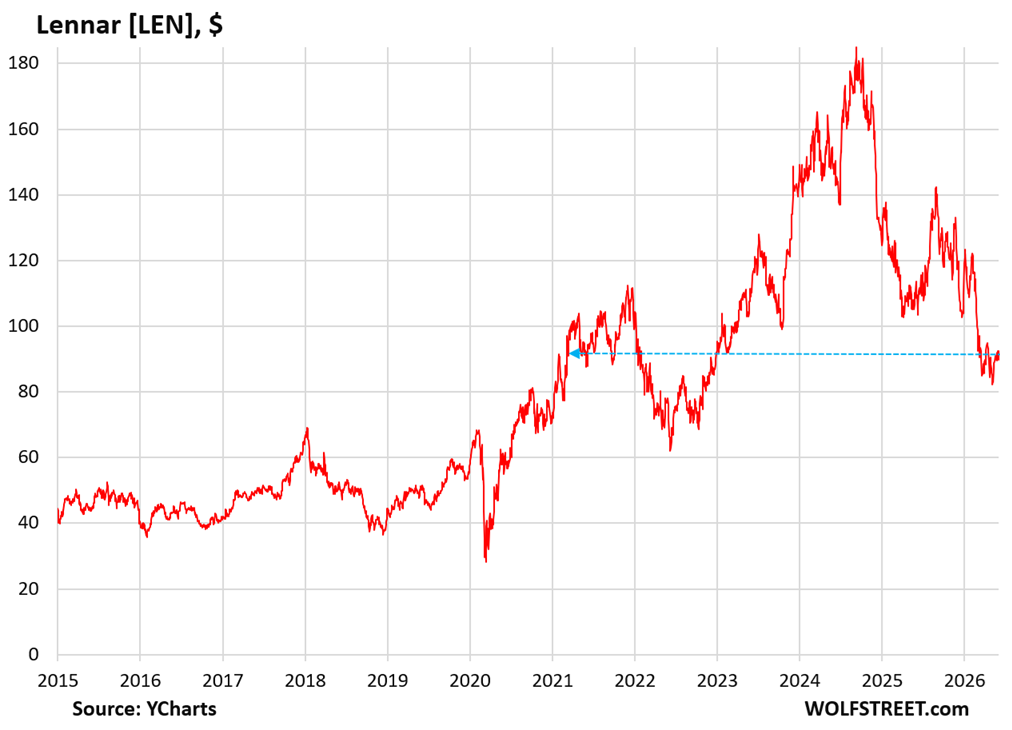

But the price of Lennar’s shares [LEN] has plunged by 49% from the peak in September 2024, to $92.43 currently, including today’s after-hours drop of 2.6%, and are back where they’d first been in March 2021 (data via YCharts).

In case you missed it: Supply of Existing Single-Family Homes at 10-Year High, Condo Supply at 12-Year High, Sales still in Freezer

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks for the research. I’m waiting for an entry opportunity to buy/ build a new home.

I bought at the market top in 2007, and never regretted it. I couldn’t stand being a renter any longer.

I imagine that around 2012 you were feeling regret that has since dissipated…

Have you considered the performance of other assets after the GFC?

A house is, of course, more than just another discretionary asset. We all need a place to live, we don’t all need to own stocks at any given time.

When junk houses (resales) are asking and getting $500,000 sales will not stabilize and become affordable. (SE Pennsylvania). A lot of money is needed to cover down payments and closing costs.

Junk ?

I bought a second home in 2023, that was 24 years old, and there haven’t been any problems.

People find so many reasons to be perpetual renters.

Looking to buy my first house in SE PA in the next 2-2.5 years when student loans are taken care of. Its bleak, unless you want to live in Norristown.

likely more pain ahead for the homebuilders

Yep, especially when TX counties stop issuing so many building permits.

That’s not allowed in Texas.

All attempts by citizens to prevent building of those huge data centers have failed.

Lennar is a low quality, low dollar-high volume builder with an aggressive financing component. They are over saturating Fredericksburg, TX.

You have no idea how tone-deaf this sounds amid the affordability crisis. People here gripe all the time about the sky-high home prices, and here you are griping about affordable homes getting built for young families?

Houses are eventually worth zero and will be torn down, including yours. Only land has enduring value.

You must be proud of automakers, such as Ford, that have abandoned their lower-cost models (including their sedans) and moved upscale so that many people cannot even afford a new Ford anymore.

Good point, but here in New England, some old houses are still standing and have great value!

Some from the early 18th century and many from the 19th!

I did get your point and fully agree, though.

I wouldn’t necessarily argue that “old homes are a good value”.

Cleveland’s inner suburbs (Shaker, Cleveland Heights, Lakewood) have a large number of homes built in the early 1900s – 1930s.

“They have character!” is the common refrain.

They also have significant deferred maintenance/updates that can cost many multiples of the original purchase price to implement.

Anyone who has owned an older home will attest to the very costly nature of their upkeep, especially if located in a “historic neighborhood” or saddled with a strict building code which mandates certain features be maintained (copper gutters, as is common in The Heights).

Young buyers concerned about affordability don’t benefit from these older homes with attractive lower purchase prices due to the immense investment necessary.

*anecdote from myself: 1,750 sq. ft. 1920 colonial. I purchased in 2005 for $117,000. I have easily invested 2x that over the years, and if I decide to stay, will easily invest another $175k on a replacement garage, driveway, and remodeled 3rd floor attic conversion.

Surprise – anything that we buy now would be between $500k-$600k….roughly the amount I will have invested in the current property.

I live in a sfr in socal and sick and tired of spending $$ on upkeep and maintenance for basic things

Always need to send $$ on something ..

Renting definitely is much much cheaper

My home is valued at 1.5 mill and I can rent the same hone for 5k per month

You do the math if it is smarter to rent or purchase

On top of this the home value is going down little bit every month

Yes, sellers need to remember they’re competing with resales AND new builders, who may be lower quality, but are very attractive at times.

Example, a family member just closed on their first home with Lennar in the Orlando, FL area, got a good price compared to resale and 3.95% fixed mortgage thru Lennar.

“Houses are eventually worth zero and will be torn down, including yours. Only land has enduring value.”

How true, My home is over 75 years old and everyone wants to tear it down already. I get a solicitations from junkyard dog builders and Realtors every week. One of them said they have a nice couple who wants to buy the home. Total BS.

Agree completely, but I read here low QUALITY is the complaint. I work at a big box hardware retailer and often hear complaints about how cheaply new homes (and cars) are built. Like they take the second most inexpensive model and reduce the quality 40% and the cost 10% so people are getting less for their money but still buy because it’s the cheapest (in the short run anyway). Buying the cheapest is usually risky and it’s hard to put a price tag on risk. Risk is always there but it’s often easiest to ignore, for a while.

Old homes are the worst. You pay $400,000 to buy it and $200,000 over the years to fix that old building. Total cost $600,000, and it’s still an old building that will be torn down eventually. The ultimate value of a building is zero. Only land has enduring value. Your hardware store is making a killing on people in old homes. People take HUGE risks buying an old home, and they face huge expenses, and they have no idea what they’re getting into when they buy it, but since your hardware store is getting rich off them, you diss new homes.

Lennar is part of the solution to the affordability crisis by building affordable supply. You people spreading falsehoods about affordable supply to keep other people from buying lower-cost homes and to keep builders from building them are part of the problem.

Doesn’t that description apply to most houses built post war (and maybe prewar?).

I’ve lived in/been to a lot of places throughout the US. Housing quality seems… mostly good enough. Even in expensive places, lots of fairly crappy houses and apartments. It’s ok, people make it work (except the lead piping, obviously that’s bad news).

What clearly doesn’t work is housing that doesn’t exist.

I wonder what people who bought a Lennar home in 2022 think about this. That’s especially a problem for a first-time buyer that scraped together a deposit and is now facing negative equity.

They need to quit looking on Zillow every day and instead relax in their home, and enjoy living there with their family and be happy, and do things they love doing, and make their mortgage payments, and after 20 years, if they want to sell, they can sell and walk away with some money, essentially no matter what.

In the long run we are all dead yes sir Wolf completly agree.

Amen! Well put Wolf. A primary residence should be looked at as a HOME first and as an investment second.

Well most don’t sell for frivolous reasons. Most buy a home to live near their work and house their family. Roughly 20% of sales are driven by either the employment or family dissolving, and a much higher share in prime working age.

Buy a house. Pay it off before retirement. Live in it. Enjoy it. Sell it when you are too old to take care of it and move into a smaller place. This is the “circle of life”. You don’t want a mortgage when you are retired.

They should also not look at the stock market for the next 20 years, for what they could have bought for their $4,000 mortgage payment.

Probably in nominal terms they’ll make a gain.

They probably think “lesson learned.”

Every normal person has many experiences of buying something at not-rock-bottom prices. We can either be happy we got what we bargained for, or we can be bitter about failing to predict the future.

Good point

Either we bought at the right time or not wrle all die one day

So lets enjoy the present moment and what we have

That still might be better than renting over the last 4 years. What is the cost of renting over that time ?

“What is the cost of renting over that time?”

According to Zillow. 3 bed 2 bath near my office, Just a regular house, nothing “nice” for 4 years.

$321,072 buy

$190,848 Rent

I’m my area of Eastside Seattle:

3 years owning – $430,000

3 years renting – $155,000

Same house.

Three-year Home price appreciation per Redfin – $0

Our first house was a new-build. After a while, we rented it out so that we could go to work in Turkey for 18 months. We drove from London to Ankara and back again via Geneva (we wanted to see the bank where our salaries had been paid into). We could pay off the morgage when we returned home. The point is that negative equity is not necessarily a trap if you have a way of earning more money elsewhere.

Yeah, but you also have to factor in the mortgage rate. The sticker price of the home may have declined, but the mortgage rate has skyrocketed. So your actual monthly payment can very well be lower than were you to rebuy at market mortgage rates.

Percentages going up have different implications compared to percentages going down. For example, a house could double in value (up 100%), and then more than double again some years later (say up another 130%). But if the house value later declines 100%, the house is then worth zero.

Deflation can be more painful than inflation if you are a forced seller. However, If you’ve made your mind up to buy a house or condo then get in the game, don’t worry about the starting price, but be smart about it. If a seller won’t negotiate down close to your price then walk away. Once you own it, falling prices have no effect than on your paper balance sheet. Banks can’t call loans because the value dropped. Over the long-term, 5+ years, you’ll be above water. Home RE is the only asset out there that we can leverage 90%. Is this a great country or what? Watching RE prices fall is like watching multiple slow motion train wrecks. By the way, there has been a big uptick in train wrecks the last couple of years. Wolf, any correlation between train wrecks in the US and home prices?

My accountant told me years ago that regardless of what real estate does, you never sell your primary residence; rental properties yes, if you need or want to. Real estate moves in cycles and once you own a home it doesn’t matter what it does. If you sell at the top, you’ll buy at the top to replace it. If real estate goes down, you’ll buy lower also.

My friend in san Diego sold his primary home for 1.8m in 2022

Rented similar home f9r 6k per month

Now he is buying a better updated home but similar for 1.4mill.

He did it and did great i wont have done it

I have been looking in flyover to escape the California, $1,000,000 “fixer upper” plantation, and everywhere I look homes have doubled since 2020. Nothing makes any sense in the RE market.

Out here in flyover housing cost increases are minor compared to land value increases.

Well, move to OKC .

A house is to live in not to live for !!!

Amen to this.

I saw the light in 2018 and downsized from a 2700 sf minor mansion to a 1300 sf bungalow. It was, in hindsight, the worst possible timing, but with one decision to live more simply I deleted 15 years of mortgage payments.

A house is to live in not to live for and this is what gets a lot of people into trouble !!!

My recently passed father in law who had an awesome home on the ocean always said, “I love this house and love living here. But remember, a house doesn’t love you back”.

Good WSJ article on US housing market recently, headline “Berkshire Hathaway and Japanese Builders See the Same Opportunity in U.S. Housing”.

The downturn in homebuilding companies is now deep enough that capital is starting to view the companies as acquisition targets.

Interesting excerpt: “Innovation in building techniques might be the next lever they can pull. According to UBS housing analyst John Lovallo, 15% of homes in Japan are built using modular construction, where parts of the home such as the walls are made in a factory and transported to a building site, where they are assembled into a new home.

More widespread adoption of modular construction, which is only used in 3% of new U.S. homes today, could be a way to protect profit margins, or make homes more affordable for buyers. A UBS study found that switching from traditional stick-built walls to modular open wall panels can cut waste by 20% and could increase operating profit by $6,175 per home. “

I used to do IT for a company that was based out of California’s Central Valley that did something similar. The company was called Entekra and they prefabbed trusses for houses getting built.

For whatever it didn’t panel out but they were ahead of their time.

Sears kit homes were popular in Chicago way back in the 1920s. What’s old is new I guess.

Personally, I have my eye on 3d house printing. They’ve done some model projects down south already. Should cut build times and costs by quite a bit once they work out the kinks and scale.

Renting isn’t necessarily bad. I’m very happy renting. Have a great house and good landlord. I don’t need to worry about repairs, property taxes etc. My coat of housing is about 40% lower than it would be if I were to buy something similar, and I’m banking the difference and investing in other things.

I may buy if the market corrects and the numbers make sense, but for now the numbers are better for renting, at least for me in PNW.

I liked the comment: houses are eventually worth zero and will be torn down. Only land has enduring value.

Something has changed here. Perhaps houses are being built the way cars and other products are in the world today. They only last a while, the shorter the better, before being “torn down”. The quicker you have to replace them the stronger the demand for new ones. The stronger the demand the higher the price, the more the manufacturer makes, etc.

We now live on a “disposable” economy. Start thinking of new homes like new cars, they do not last forever. Taken to it extreme this means you have to start saving for your next home soon after you bought the last one. Do you really want this?

Love the statement from Lennar about increasing land prices when the builders/developers are the ones who really drove it up in my neck of the woods.

I wonder, I just wonder how people would be feeling right now if the housing market were truly a free market and were allowed to find true price discovery. It would be one major economic hangover. The illusory wealth effect would vanish. The drunken sailors would in fact be destitute and hopeless. The economic edifice would appear more like a dilapidated shack.

Can someone explain to me why SpaceX is worth $2.2 trillion?

I think we will see some reasoning in Wolf’s future article about Trillionaires. Did I spell it right?

I just heard this on the radio:

One Million Seconds: This equals roughly 11.5 days.

One Billion Seconds: This equals roughly 31.7 years.

One Trillion Seconds: This equals roughly 31,709 years.

There just is not a lot of places to put your savings except stocks. Much of the world is buying US stocks. 20% of stocks are now owned by foreign entities. This is up from 8% in 2000.

What are alternatives:

– FED funds is below inflation rates

– Housing is flat maybe going down. Why invest in a a flat or dropping investment class. Very few want a 2nd job managing rental investment properties.

– Cryptos helped suck up some retirement savings but no growth compared to Stocks and AI going forward.

I keep asking a friend who is 65 and retiring if he is worried about current valuations. He understands cash is losing value due to printing. Bonds funds are not keeping up with inflation. He said, where else can I put my 401k besides stocks?

He said, 10 to 15 years ago he used to worry about a 20% dip in the stock market and how it would affect his retirement. Now he says he does not care. A 20% drop and he will still be up 150% then he was 10 years ago.

He said the trick is to stay invested. Every 20% drop the past 10 years has been bought. So he is staying in equities…no bonds.

Fair point, but that doesn’t really answer the question about SpaceX specifically. It also shows how ill prepared the world is for a long-term downturn.

There’s smart money and there’s dumb money investors. The smart money investors just cashed out of Space X (owners) and the dumb money (most of the retail investors who believe the story) paid for it. There’s about $3.0 Tril sitting in retail MM funds at the end of May. A lot of institutions who bought in the primary market today did so to resell to retail investors in secondary market over the ensuing weeks.

I have to add a funny follow-up. This friend is a risk estimator for an insurance company. For 30 years he has been generating underwriting reports after investigating manufacturing plants to define the analyze the risk for accidents and thus the future price of an annual insurance premium. One of the most risk aversion people I know.

We went on a vacation to Vegas a few years ago for 3 days. 1st day we were gambling at Black jack. After 1 hour he was up $9. Cashed out and refused to gamble the rest of the 3 day trip because he knew the odds were against him and he wanted to leave as a winner.

I hope this gives people some idea the faith people have in the FED and the stock market. He is all in on stocks.

This guy has a screw loose (if he actually exists). He spends all this money to go to Las Vegas to gamble, and then he gambles only 1 hour and stops when he makes $9, and twiddles his thumbs the rest of the 3 days, after having wasted all this money to go there to gamble. If he didn’t want to gamble at least for the fun of it, he should have skipped Las Vegas and go hiking instead. There is nothing to learn from a guy with a twisted brain like this.

Because Musk walks on water.

Sure seems like it. People are willing to throw money at whatever nonsense Musk attaches his name to.

That guy who went to Vegas is brilliant. “He gambles only 1 hour and stops when he makes $9, and twiddles his thumbs.” He decided he’d lose a lot less with high-dollar call girls and have 100 times more fun. 🤩

It’s like buying lots on the moon but you never take possession of them because they’re on the moon and you’re on earth. The same type of reasoning.

Lennar wants $300.00 per month for 30 years in Haines City FL. as a community development fee. This is on new builds

Crazy amount.

What was a scary price for us ($440K) for a tiny (1000 sq.ft.) 1930-home in 1990 in Silicon Valley has become a valuable plot of land. Soon after purchase there was a 5-year downturn that forced us into mortgage insurance. The house value dropped 20%! Luckily, we kept our jobs and were able to make the payments to keep the house. Now, 7 years post-retirement, we are beginning to make plans to sell. We bought the house to live in. In terms of investment, the S&P 500 would have been better (not including rental cost).

@Freddy the S&P 500 has outperformed CA real estate since 1990 up over 20x vs less than 10x. That means that anyone that put $440K in a house and let it sit empty for the past 36 would have WAY less than someone who put $440K in the S&P 500 (the guy that rented it and invested the net profit would do a lot better). For people that made a 20% down payment in Santa Clara County in 1990 saw close to a 100% equity wipe out by 1995, but then the 5x leverage kicked in and the ROI went nuts. By the time dotcom boom rent spikes kicked in by the year 2000 most SV “homeowners” were paying less (PITI) than renters were paying rent and if they started investing this extra money (plus all the money after paying off the home) the return will be lot closer (higher for some and lower for others). To be fair you should also back out the cost of moving a few times (since few SV homes have been rentals since 1990). As Wolf says people should “quit looking on Zillow every day and instead relax in their home, and enjoy living there with their family and be happy,” You can do fine if you buy or rent a home and there are pros and cons of both. SF Peninsula parents get mad at me when I tell their kids who want to buy that unless they are super rich buying a home for $3.6mm near the home they grew up in that their parents bought for $360K 30 years ago is a bad idea (if they work for Space X and have $10mm and stock options they are fine buying a $3mm home)…

Wolf – this article really piqued my interest, especially the chart of the average price of new homes sold. “The average price per home delivered in Q2 fell by 4.6% year-over-year to $371,000.” I was in massive disbelief over this, so I went to Lennar’s website. In Texas, you CAN indeed get a very decent home for $350K; even a basic home for $250K. In California, you can almost TRIPLE that price! Yes, TRIPLE. There are a few crappy homes in crappy places (of Cali) for $450-$500, but a decent or nice home is $650 to $900K! Now, I realize you or some people will say, ‘oh, it’s the jobs’, or ‘not enough housing’. I call BS on all of it ‼️ The sad fact is that ‘officials’ are SCREWING US and MAKING home prices high. It’s total bull crap and it’s unacceptable. This is a manufactured insanity. Manufactured.

End of story.

Wasn’t Cali going to build tiny homes?

How did that turn out? In line with Lennars cost per ft2

Midterms coming up. Libertarian is the only party on the ballot for a balanced budget so people have the opportunity to vote out officials they think aren’t doing things right.

The main problem to consider when buying a new “affordable” house is that the entire country has an extreme shortage of skilled workers. It will be interesting to see what the life span will be of these Lenar discounted houses.

Include skilled (experienced) inspectors.

The trend is to use more manufactured components that are mass-produced with automation in a factory and trucked to the site, rather than building everything by hand from scratch on site. Homebuilding has been stuck in the 1800s for too long.

Home prices today? As a nation the folks in DC will keep the money system going as long as they can make money. Inflate or Die ! I remember in 1967 a Ford Mustang Fastback cost me $2500.00

Census Bureau on 1967 income: “Median income of white families was about $8,300 and nonwhite families, $5,100.”

So that Fastback was bout 1/2 a year’s income for a nonwhite family and about 1/3 a year’s income for a white family.

Today, median household income is about $83,000. So a car costing $42,000 or $27,000 would be about the same as athat $2,500 Fastback in ’67.

Lennar may be bottom-tier in quality, but there is no arguing that they are responding to the market signals. I have seen listings for their tiny 2-3 bed homes in the 1000-1300 square feet range in North Texas. These are funny-looking little boxes in 1/10th of an acre plots. These are priced in the $200-250K range. For a family making median income who are looking for a starter home, these are good enough.

Buyers Market Returns – Notably, buyers in the $750,000-$2 million range might have the most leverage, the Realtor analysis finds. After seeing a greater number of bidding wars than average during 2022, the height of the pandemic rush, the final sales numbers for homes in those price points are the furthest below asking. Who cut their throat to blow their nose in 2022, lowering higher prices paid to get in, now to get out. February 2021 I locked 2.65% refinance for the next 30 years P&I $1045/mo. I will never leave, not sure if the wife will stay. Newly built Lennar 2400 square ft home purchased in 2014 $335K now valued at $660K. 12 years later and I would buy another Lennar Home in a heartbeat, as we have had zero problems to report. A Man only needs a place to Shit, Shave, and Shower in this world. The inflation termites are winning war since March 2020.