AI investment mania and the second wave of semiconductor plants.

By Wolf Richter for WOLF STREET.

Of the trillions of dollars to be sunk into the AI-related capital expenditure mania – nearly $3 trillion through 2028, per a research report by PitchBook today – only a small portion is going to the actual construction costs of data centers, which is what we track here, but they nevertheless show the trend of the AI spending mania.

The vast majority of data-center costs is going to AI servers and related equipment in those data centers, and to equipment to supply the servers with power, and to the equipment and infrastructure to connect the data centers to the internet, none of which are included in construction costs here.

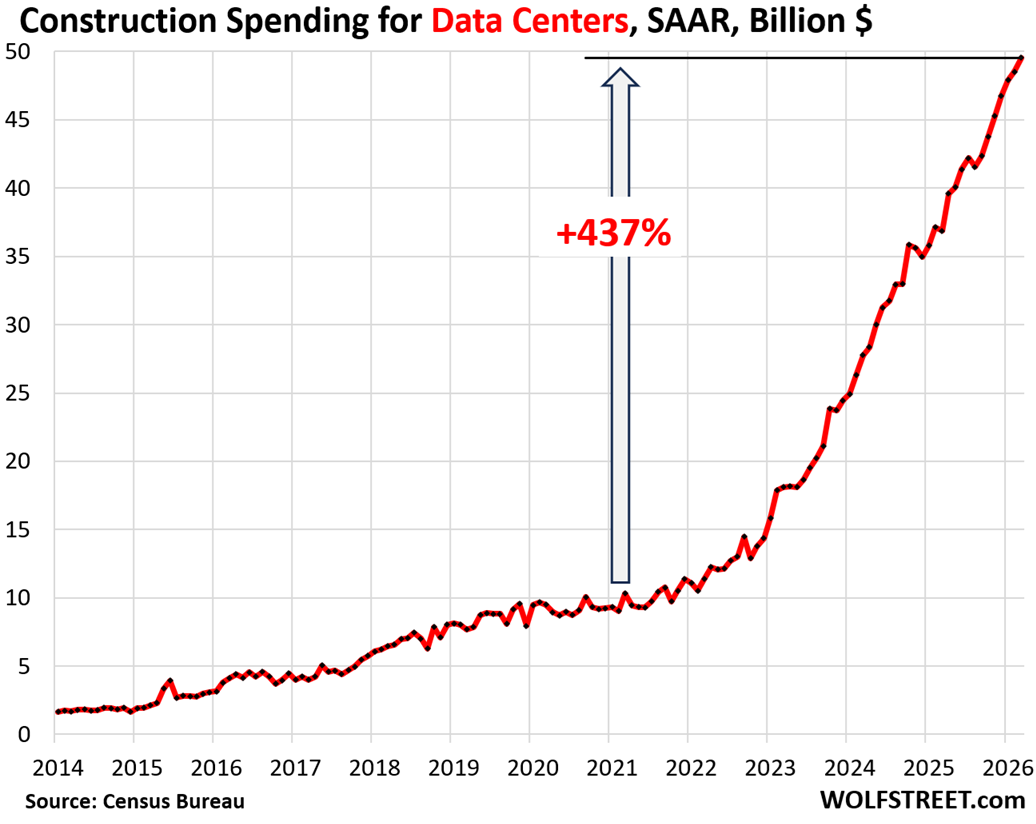

Construction spending on data centers soared by 34% year-over-year in March to a seasonally adjusted annual rate (SAAR) of $50 billion, up by 437% since the beginning of 2021 and up by 688% since the beginning of 2018, according to data from the Census Bureau today. It takes years to plan, permit, and build data centers – now amid growing local opposition – and the spending today was originally planned some time ago.

This boom in data-center construction activity has triggered various supply constraints and bottlenecks, ranging from labor, such as electricians, to electrical equipment, including on-site power-generation equipment when grid power is insufficient. No one was prepared for this kind of explosion of concentrated investment.

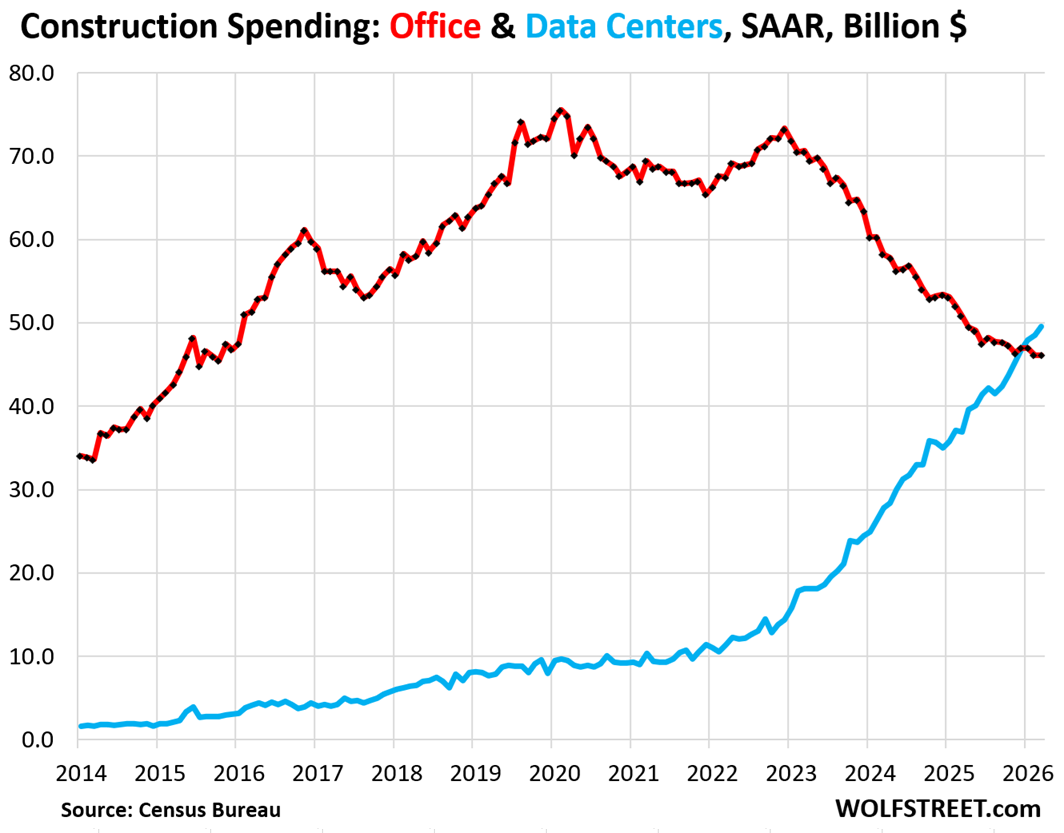

Office construction spending fell by 9% year-over-year in March, to a seasonally adjusted annual rate of $46 billion, the lowest since 2015, amid the severe problems in the office sector of commercial real estate.

Spending on data center construction (blue line) exceeded spending on office construction (red line) for the first time ever in January. Boom and bust:

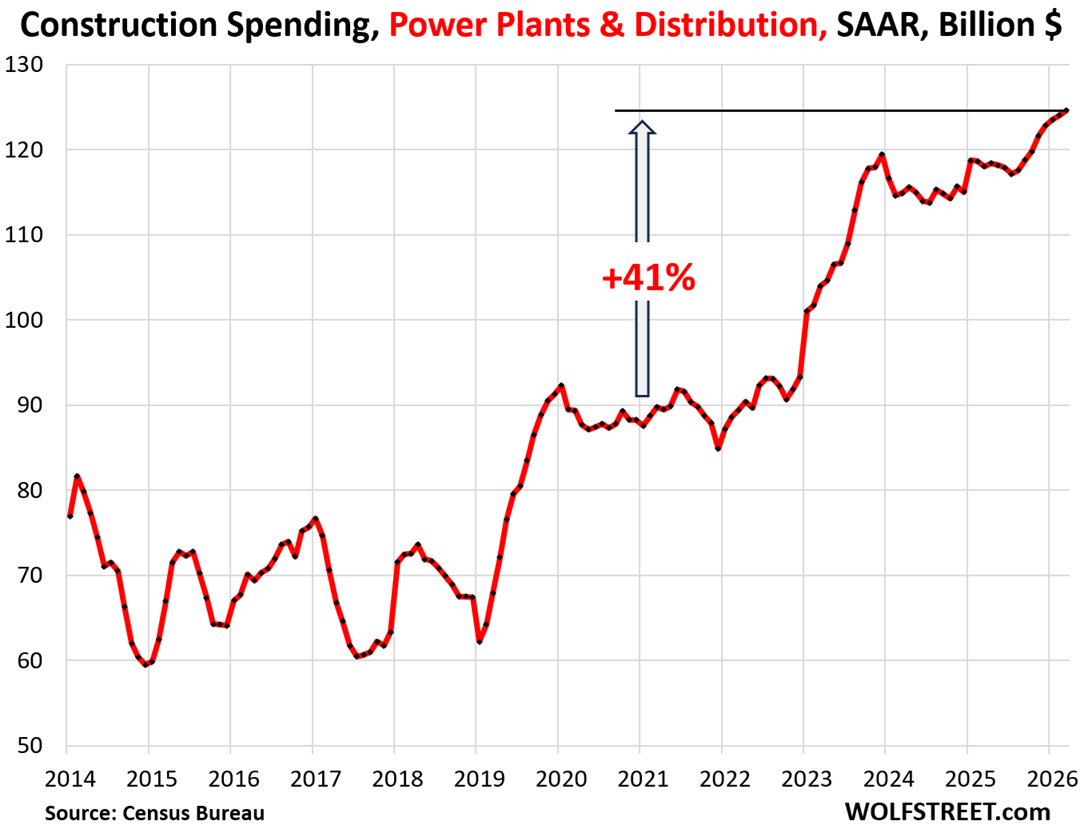

Spending on Power Plants & Distribution rose by 5.5% year-over-year to a seasonally adjusted annual rate of $125 billion, up by 41% since the beginning of 2021. This includes construction spending on power plants and transmission infrastructure.

It takes years to plan and build a power plant, including regulatory approvals. That process lags far behind what data centers need. In addition, utilities and power generators are worried about an untimely end of the AI investment mania that might leave them with newly-built stranded assets when the investment bubble implodes, and they’ve been proceeding with some care.

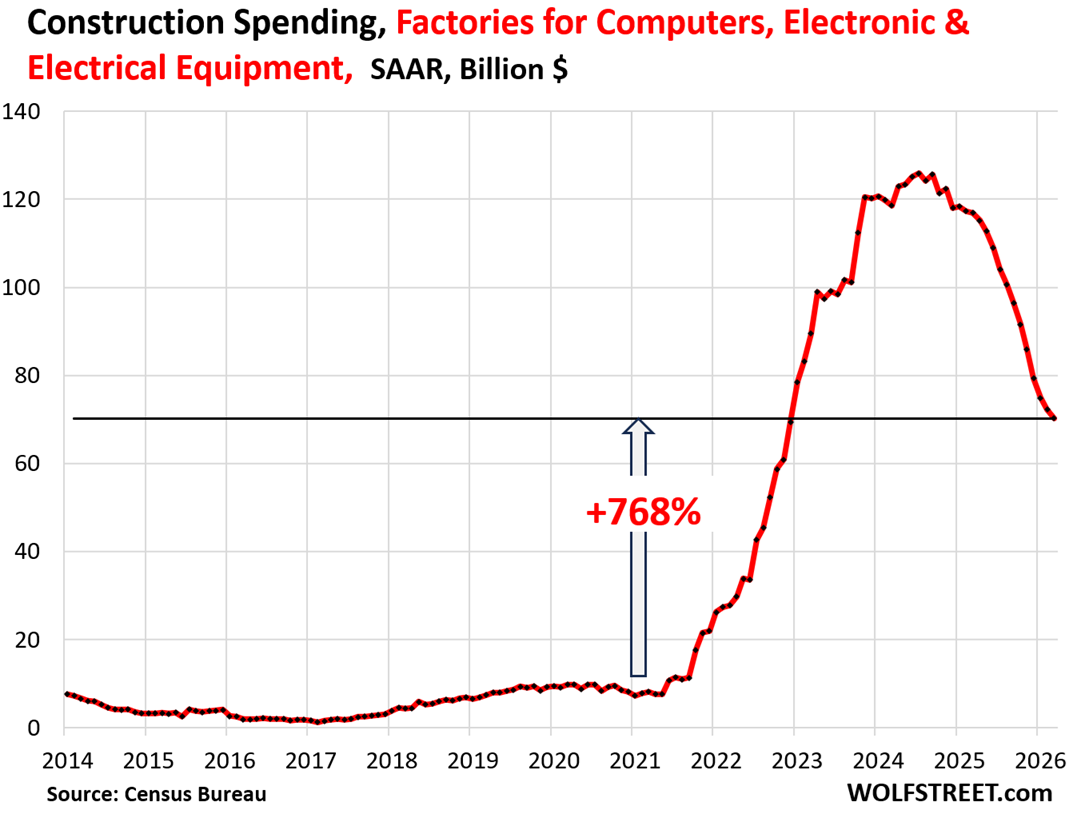

Construction spending on factories.

Semiconductor plants are included in the category of factories for computers, electronic & electrical equipment factories. At the peak, this category accounted for roughly half of total factory construction spending.

Construction spending on those factories dropped to an annual rate of $70 billion in March, down sharply from the peak in 2024, but still up by a huge 768% from early 2021.

And there is a second wave of semiconductor plants getting lined up, including SpaceX’s Terafab facility in Grimes County, Texas, with an estimated capital investment of $55 billion for the first phase, and total capital investment, “if additional phases are constructed,” of $119 billion, according to a Grime County public hearing notice.

The construction phase of some of the plants that were started a few years ago is now finished, and the equipment is getting installed, and in some, production is getting ramped up. But these data here are just the construction costs of the buildings and do not include the cost of the production equipment in the building that dwarf the costs of the building.

What’s important for the US economy is the future production at these plants after they ramp up — decades of production interlaced with further investments. Construction spending is just an indicator of how much production capacity is getting added at a point in time to the US manufacturing base.

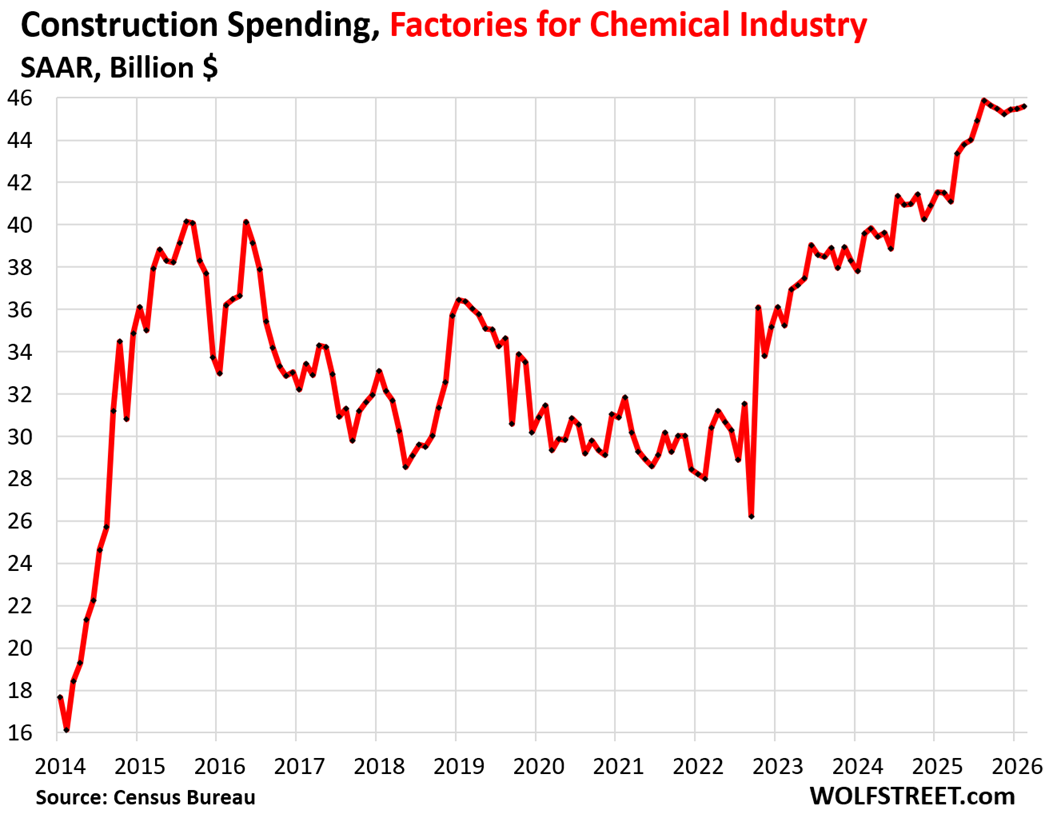

Construction spending on factories for chemical products, the second-largest category of factory construction, jumped by 9.9% year-over-year to a seasonally adjusted annual rate of $46 billion in March, up by 57% from the beginning of 2021.

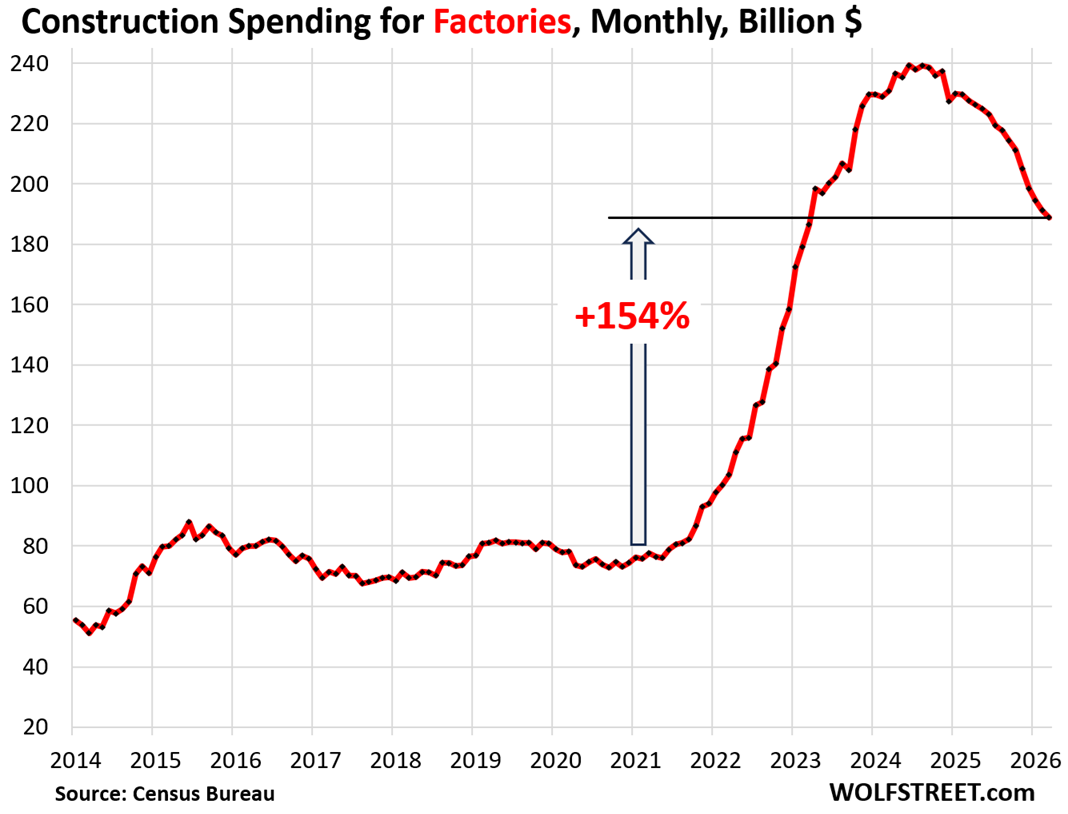

Overall spending on factory construction in March dropped to an annual rate of $189 billion, that was still up by 154% from the beginning of 2021, still a massive increase in spending on factories compared to a few years ago.

All these factories will be highly automated plants with relatively little low-skilled manual labor. No one is building a sweatshop factory in the US as labor is too expensive, and there won’t be a surge of low-skilled manual labor coming with these factories. But industrial robots cost the same anywhere in the world; they’re the great equalizer.

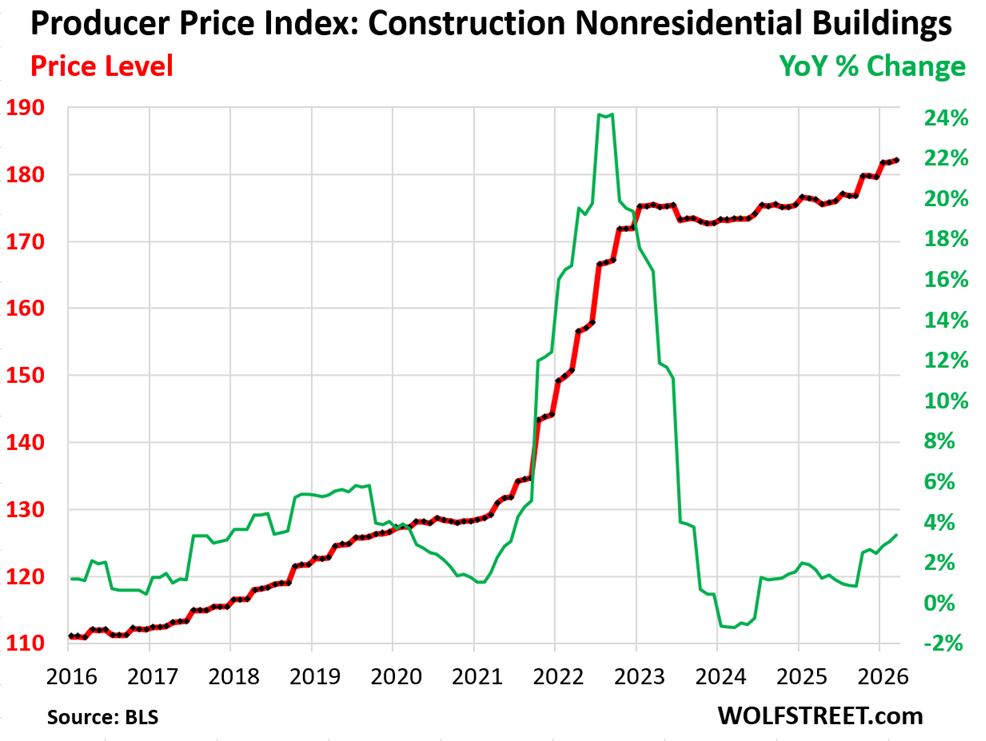

How much of this growth is inflation? Construction cost inflation for nonresidential buildings has started to accelerate over the past three months and in March rose by 3.3% year-over-year, according to the Producer Price Index for Construction of Nonresidential Buildings.

The big spike of construction cost inflation occurred in 2020 through 2022 (+36% in two years). In 2023 and 2024, costs remained relatively flat, with inflation near 0% over those two years. Then in the second half of 2025, construction costs began rising again.

By comparison: Year-over-year, the PPI for construction costs is up by 3.3%, while spending on data-center construction is up by 34%; since January 2021, the PPI is up by 36%, while spending on data-center construction by 437%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I’m assuming the Electronics graph includes the CHIPS act funding from a couple of years ago?

The actual disbursements of the CHIPS Act started in Dec 2024, when Intel got its first lump, and continued in 2025 and 2026 under Trump. Intel also got a big cash infusion under Trump through a share sale to the government. The data here is “spending” – no matter where the cash came from that got spent.

Construction on data centers reached $50B. The data centers are options. Investors aren’t fully committed. They can change their mind. Since most customers are aren’t happy with them investment might stop, before losses accumulate.

This is actual spending, cash out the door, not options to spend.

If anyone is interested, here is a fun stock ETF to watch– SOXL. It is a bullish TRIPLE leveraged semiconductor ETF. It performs 3X whatever the SOXX does in either direction. It has quadrupled since March 30th amid the current AI chips mania. Now, if at ANY time the SOXX were to fall by 35%, SOXL would go to ZERO. It doesn’t matter how high it goes, since it replicates 3X the performance of SOXX, it would go to ZERO. Well, it probably wouldn’t go to ZERO, it would do a huge reverse split so it could keep trading, but it would get totally obliterated.

My old-fashioned non-leveraged semiconductor index fund XSD has increased 250% since Mar 30, so if your triple-leveraged SOXL has increased only 400%, doesn’t seem like they’re very good at it.

You guys forgot to add the year. You are talking about “since Mar 30, 2025” not “since Mar 30, 2026.”

Since Mar 30, 2026, the XSD increased by about 80%. This is still a HUGE GIGANTIC parabolic increase for a six-week period, but not 250%.

The $50G spent on data centers construction is a small down payment for multi trillions co. It’s smaller than spending on

powerplant, factories and LNG terminals. The war with Iran might

last a long time. Higher oil prices are here to stay. It will affect data centers. The US exports: oil, jet fuel, diesel and LNG. SPX reached 7,400 in order to distribute the mag7 to the weak hands. Those multi trillions co are raising cash. Capex avoidance is on !

There is a committed 1.1 trillion from the MAG 7 in capex for next year. 1.1 TRILLION DOLLARS IN ONE YEAR! No one is hoarding cash- they are raising cash via bond sales, equity and FCF.

I have no idea what the S&P will do next year, but your thesis is verifiably terribly horribly incorrect.

Crying won’t help you, praying won’t do you no good

No, crying won’t help you, praying won’t do you no good

When the levee breaks, mama, you got to move, ooh…

I am predicting a resurgence of Blues music…

Challenging as most have to buy NVIDIA chips well in advance. By the time the data centers are built and ready, NVIDIA will be 2 generations down the road, which will require brand new racks. I suppose lots of hardly used GPUs will flood the market at some point although buyer beware. It isn’t like the .com boom didn’t build out but the reality is the scale and cost are not even ballpark comparable so hard to buy this will play out similar. Everything is different as winners and losers today very close to being decided.

NVIDIA chips are bought like crazy. But somehow their (Nvidias) inventory keeps rising. The thing is that ordering chips is a lot faster then building data centers and getting a power connection up and running.

1. Inventory keeps rising when prices (cost of goods sold) keep rising. The new Blackwell system is far more costly and complex to produce than the prior generation.

2. Inventory is not what Nvidia has in stock in a warehouse somewhere waiting for a sale. Nvidia doesn’t operate that way. It’s the amount that they have been invoiced for by their contract manufacturers and suppliers, such as TSMC, but that hasn’t been delivered yet by these contract manufacturers and suppliers, or that is in transit between them: so raw materials, work-in-progress, and finished goods — which will come out of Nvidia’s inventory when it’s finished by its contract manufacturers and suppliers and delivered to Nvidia’s customers.

From everything I’ve reviewed, the US has already lost the AI competition with China. They have the power….now…and certainly have the technical expertise (and lots of it) to power ahead of the US. In many areas, they already have.

I guess what the US builds in AI can be used here at home, but I would not expect the US to be the king of AI in the world by any stretch.

Expect construction cost inflation to accelerate in the US due to the obvious shortage of qualified and willing workers to build this stuff. A shortage across the board from the data center construction, to all the specialized stuff needed to build the data centers as well as the electric system buildout needed to power this stuff. Regional utilities are already proposing 15% rate hikes for next couple of years, and that is likely only the beginnning.

You are reading the wrong materials- The US is ahead in AI race and very likely to stay that way

Such a hideous waste of natural resources, all in the name of making the already fantastically wealthy OBSCENELY wealthy, with the byproduct being massive inflation for the masses.

The AI grift. AI is just a fancy search engine that can photoshop audio, visual, and written data. I use it to make myself more efficient when trying to find solutions to problems. AI is a a misnomer for for what has been developed, it is a tool that can build on itself. We are the actual ai, since we are the only biological life form on this planet that is self aware.

I use AI for tech support to deal with the tech that’s behind this site (I’m not a tech guy). And the AI tech support from the vendors that I use is amazing. Human tech support had been universally awful, time-consuming, aggravating, and often useless. Humans are terrible. They don’t have a brain, or if they have one, they cannot use it. I’ve been using AI tech support for two years. It’s constantly getting better and easier to use. A few days ago, one of them offered to actually FIX the issues it found, rather than just telling me how to fix them. It implemented the fix in one minute what would have taken me an hour-plus of headache-inducing work, and if I screwed something up, it would have taken down the site. Every time that I have to use AI tech support, I thank God that it exists, and that I don’t have to deal with humans.

Many call center folks seem to lack a facile grasp of the English language.

Tough break for any chip makers. Helium seems to be in the process of becoming unobtainium. Asked a dollar store cashier if the price of party balloons had gone up. She said no helium available hence no party.

Tough break for those wags that like to huff helium and talk in a high pitched voice to entertain their friends. May have to go to shady dark web dealers to score your “H”.

Thanks Donald.

The US is the largest helium producer in the world, and the largest helium exporter in the world, and it can ramp up production further, and is already doing so. There won’t be any shortage of helium in the US. But there may be in some other countries.