Amid improved automation and efficiencies, production rises, but employment doesn’t, or only a little.

By Wolf Richter for WOLF STREET.

Manufacturers in the US were on a roll in May, expanding at the fastest rate since May 2022, after months of acceleration, amid surging orders and exploding input costs and soaring output prices, according to the two Purchasing Managers Indices released today, the S&P Global Manufacturing PMI for the US and the ISM Manufacturing PMI. Though they differ substantially, and don’t always agree, both PMIs grew by the fastest rate since May 2022.

But don’t expect a surge in employment: In the US, manufacturing is about improving automation and efficiencies – more production with less labor. And both PMIs showed that.

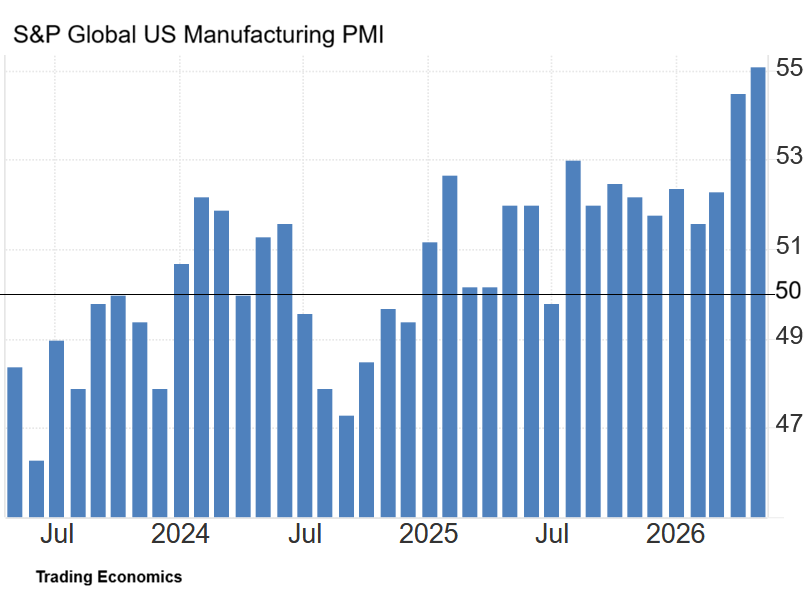

The S&P Global Manufacturing PMI for US manufacturers rose to 55.1 in May, the fastest rate of growth since May 2022, and the third month of accelerating growth (above 50 = growth), as production increased at the fastest rate since April 2022, and as orders increased, “largely driven by client efforts to build stock given expectations of further price rises and supply delays.” Supply chains began to struggle, and supplier delivery times deteriorated by the most since August 2022 (chart via Trading Economics).

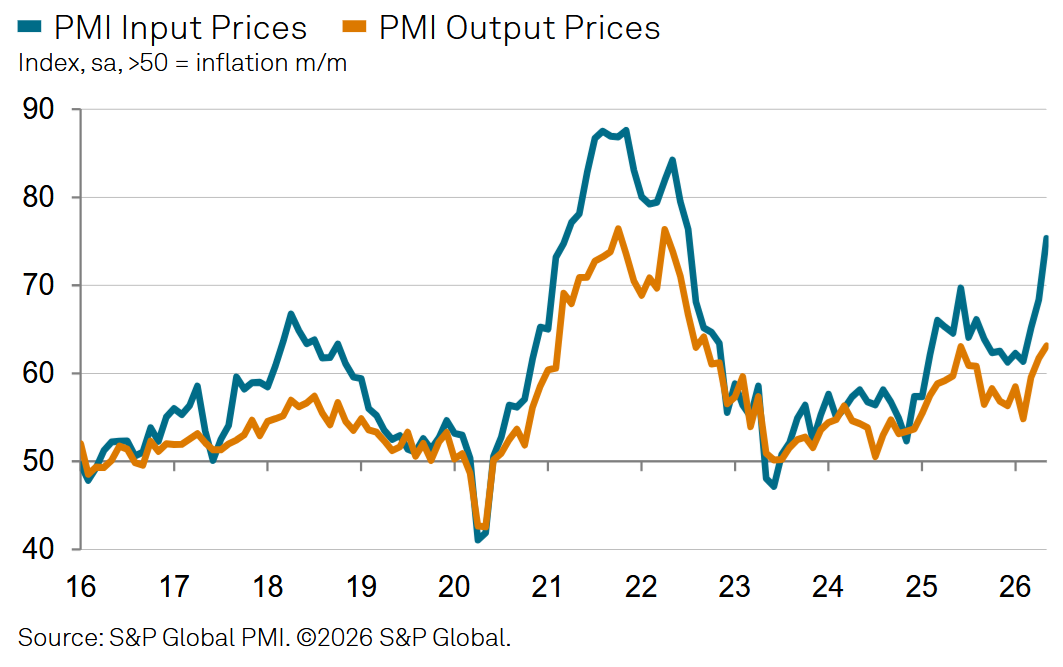

Prices, oh my! Manufacturers’ input cost inflation exploded in May from April, with the index spiking by the most since July 2022 – driven by “raw material prices, particularly for fuel and oil-related products” (blue line in the chart below).

And prices charged by manufacturers soared in May from April by the most since September 2022 (brown line) “as they sought to pass through their own higher expenses to clients wherever possible” (chart by S&P Global Market Intelligence):

Fears of more inflation and supply chain disruptions have begun to cause frontloading of purchases: “Purchasing activity rose solidly since April and was often linked to higher production requirements and efforts to mitigate against further price increases and supply chain disruption.” And so input stocks rose for the second month in a row – “despite difficulties sourcing and receiving inputs amid supply constraints and shipment delays from vendors,” according to S&P Global.

Employment increased in May from April, and “although the rate of job creation was only modest, it was the best for five months,” the report said. “A positive outlook in part helped encourage additional hiring, with manufacturers generally anticipating an increase in sales and output over the coming 12 months.”

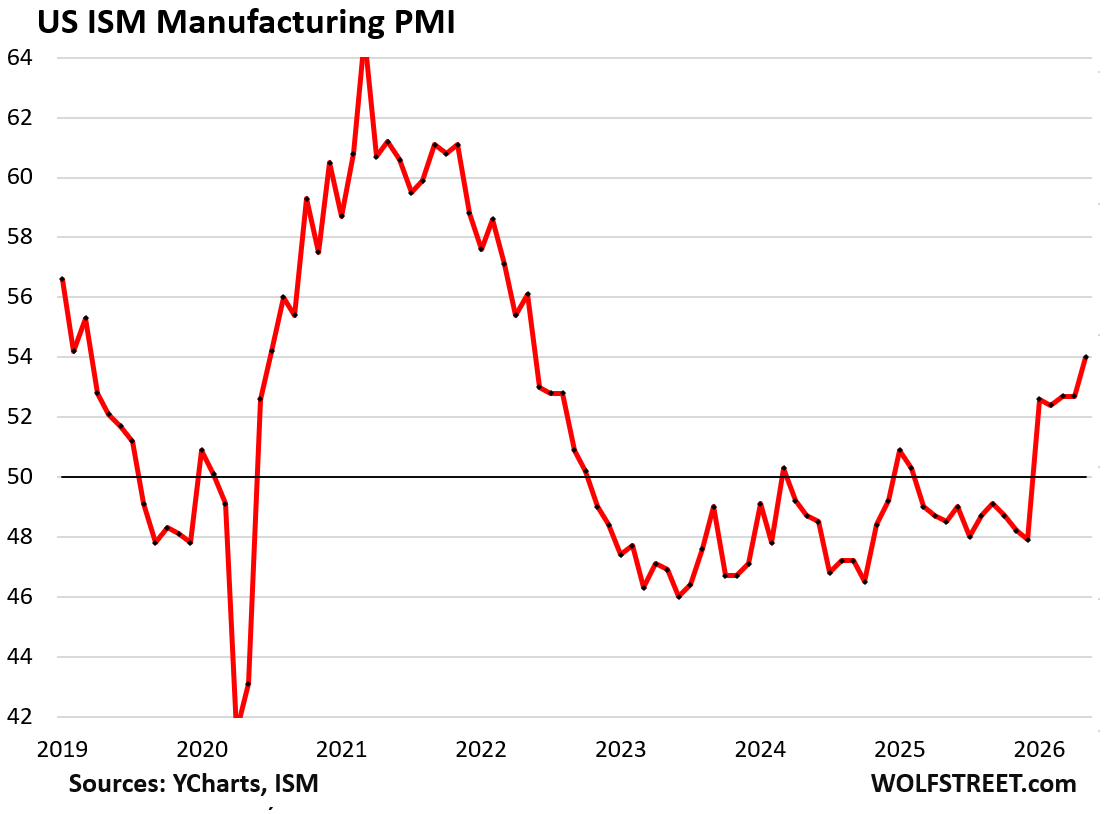

The ISM Manufacturing PMI for May, also released today, expanded for the fifth month in a row. At 54.0%, it was the sharpest growth rate since May 2022, having now emerged from the 2023-2025 doldrums, driven in part by surging new orders.

“Three of four demand indicators (the New Orders, Backlog of Orders, and New Export Orders indexes) were in expansion.” The Customers’ Inventories Index remains in ‘too low’ territory, which is “usually considered positive for future production,” the ISM report said. And Supplier deliveries were slowing for the sixth month in a row.

New orders (56.8%) rose at the second-fastest rate since January 2022, a hair behind only the spike in January. Four of the six largest of the 18 manufacturing industries reported increases, in that order: Computer & Electronic Products; Chemical Products; Transportation Equipment; and Machinery. The New Export Orders Index also rose (50.6%), after a decline in April.

The Production Index rose at an accelerated pace in May from April (54.3%), and in expansion territory for the seventh month in a row. Five of the six largest manufacturing industries reported higher production, in that order: Transportation Equipment; Machinery; Computer & Electronic Products; Food, Beverage & Tobacco Products; and Chemical Products.

The growth of the Backlog of Orders Index accelerated by 0.8 percentage points to 52.2%.

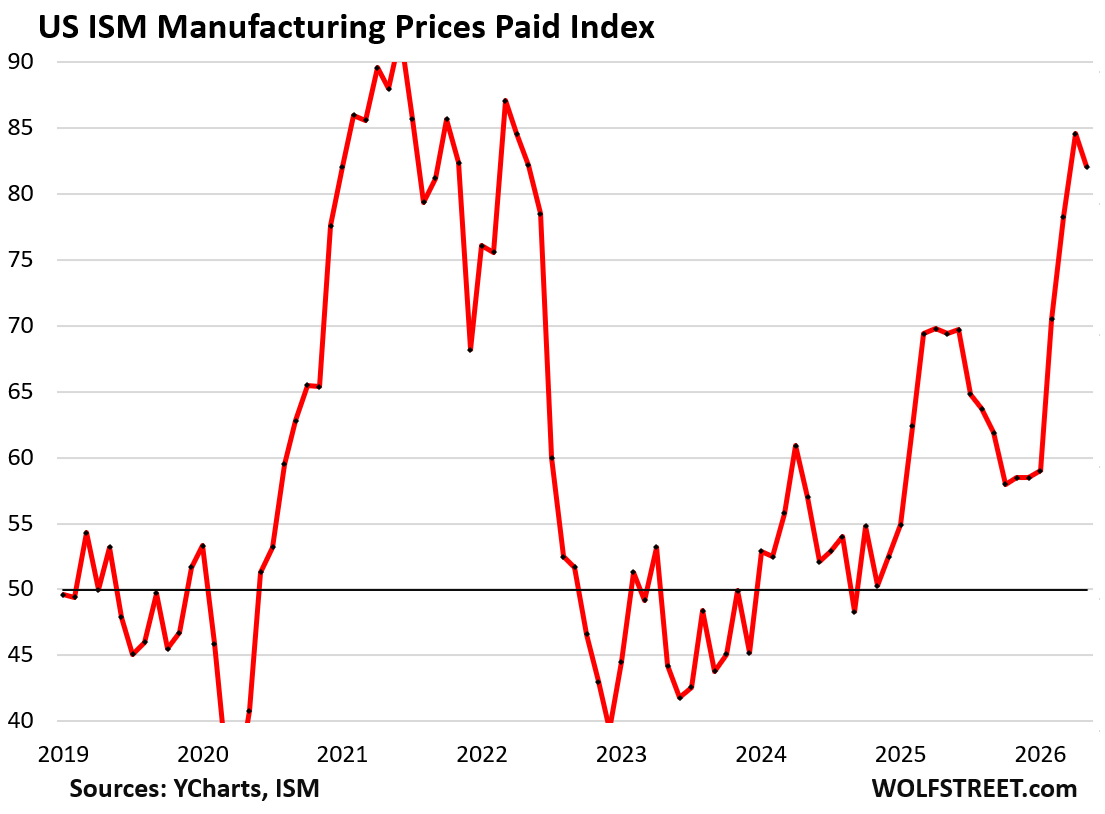

And input prices spiked in May from April (82.1%), but at a slightly slower rate than they’d spiked in April from March (84.6%), which had been the worst since April 2022. 16 of the 18 manufacturing industries reported that prices rose in May from April.

But employment was still in contraction in May from April (48.6%), though at a slower rate than in the month before. Of the 18 industries, half reported growing employment. The rest reported stable or declining employment.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I work in chemical manufacturing and the raw material situation has been and likely will remain pretty dicey for the time being (we use a lot of Petrochemicals). Our sales for the first five months were decent, but the people with the money have us working pretty lean to reduce fixed costs so the increase demand hasn’t actually translated into more hiring on our part. It’s interesting to see that other places may be in the same situation.

US economy is driven by investment the past few years. Kinda like a war economy. It will prosper while the demand is there but the price to pay is massive post war inflation.

Absolutely correct that US economy is being driven by investments rather than consumption.

That said I’m kind of doubtful that you’ll necessarily see massive inflation due to that. Whether or not you do depends on a lot of other factors, like:

Can consumption (ESPECIALLY consumption on credit) fall sufficiently to free up economic resources for investments?

How much additional aggregate supply is the investment adding? Is production merely getting more efficient, or is there more of it?

Will savings rise or fall? Or interest rates?

That said US has a massive investment hole that needs to be filled, so I suspect investment-led growth is going to be the standard for decades to come. Not good for the “little guy” or Wall Street but great for manufacturing build-out and infrastructure investment. So it’ll be good for America and its economic performance as a whole.

MW: As Micron’s stock blows past $1,000, Wall Street sees more gains

All driven by fear of the future, not growth.

There is an established delay between an increase in the ISM Manufacturing Index and actual manufacturing hiring.

Alphabet goes from stock buybacks to stock sales to raise $80 Billion. Trying to beat SpaceX, OpenAI, Anthropic to whatever liqudity is there in the market. They will all start doing it now.

I think it’s awesome and kind of funny but uber-logical that they all start selling newly created shares at super-high prices to mostly retail investors. Companies will at least do something with this money, plow it into the economy, make it work, while retail investors clearly have no use at all for money, as everyone can see, they’re just gambling with it.

Is if really retail investors or retirement funds buying the stocks? Do you have some numbers around showing the percentage of retail investors in the stock market?

I have always wondered why this isn’t a celebrated facet of the boom-bust cycle.

Any somewhat mature company with a PE over 20 should be taking advantage of the free liquidity. As long as it is marketed as accretive or future proofing, i would expect investors to flock to the stock.

Tesla always comes to mind. If they can sell $20bn of new shares to fund a slight reduction in production costs, wouldn’t everyone win?

Agreed. People always refer to investing money in the stock market as “putting money to work.” But trading existing shares around is not benefiting the economy, nor is it doing any “work.”

Only the issuance of new shares that actually raises money for investment can be accurately described that way.

Future Bagholders of the World: Unite!

More proof of what Mr. Wolf has been saying concerning manufacturing employment. It’s been going down for years. More automation and robotics, less people.

And like he says the economy is more in Services and consumer spending.

How can the President give IBM $1000 Million (1 Billion)????????????

The House controls the purse strings. He is pumping the markets, and the indexes (IBM and the Dow 30)

You keep having articles that suggest / show that manufacturing is doing well / expanding.

If I were an invisible boogeyman in the night I would be shouting into the wind in a very spooky tone of voice “In – Flaaaaaayyyy-Shiinnnn.”

That ol’ Inflation Boogeyman sure is a scary fella.

I know Wolf very well may tell me “BS. Read the %#+=!*!!!” Might even call me a moron. But every night I can hear that boogeyman shouting into the wind.

Yeah, but do read the article 🤣 these figures are not dollars, but increases in output (more diesel gensets produced), orders (more diesel gensets ordered), employment (more people hired or not), supplier delivery times (rose by x number of days), etc. etc. real stuff, not money, and therefore inflation doesn’t have anything to do with it.

Wonder what Keynes would think of 2 trillion dollar deficits and a 4.3 percent unemployment rate.