Those ultra-low mortgages wrecked the housing market, but homeowners had nevertheless been paying them off steadily – until now.

By Wolf Richter for WOLF STREET.

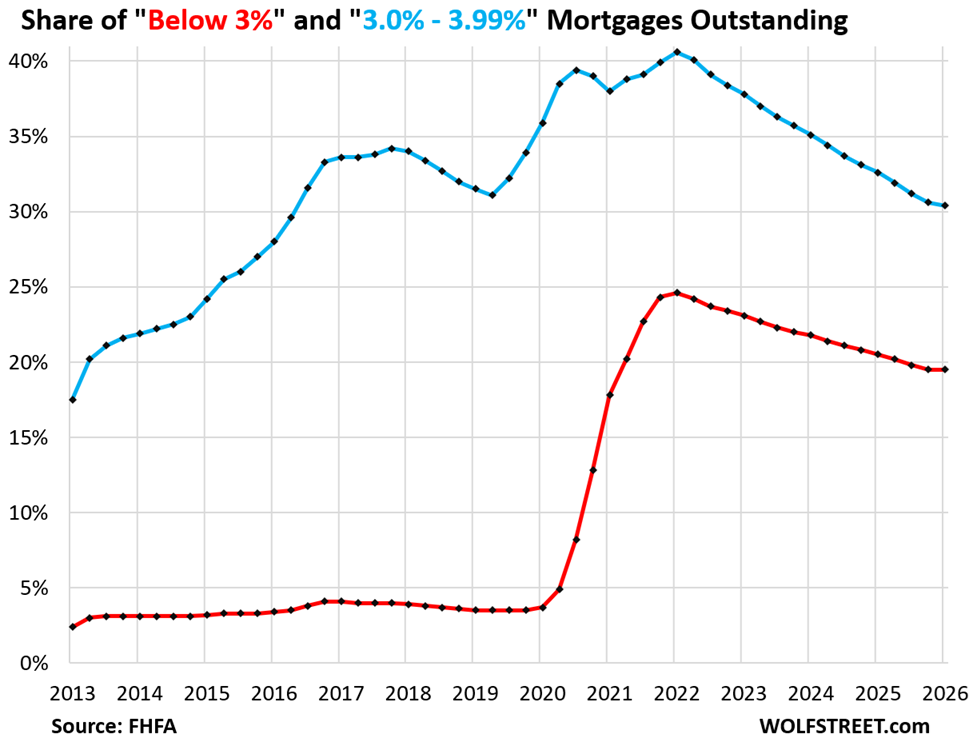

Progress in resolving the “lock-in effect” has suddenly stalled: The share of below-3% mortgages outstanding, by number of mortgages, remained unchanged at 19.5% of all mortgages outstanding in Q1, after declining steadily since the peak in Q1 2021 of 24.6% (red in the chart).

The share of 3% to 3.99% mortgages edged down by just 20 basis points in Q1 from Q4, the smallest quarter-to-quarter decline since their share started to decline in 2022, to a share of 30.4% of all mortgages (blue), according to data by the Federal Housing Finance Agency (FHFA).

Combined, the share of below 4%-mortgages edged down only 20 basis points in Q1 from Q4, by far the smallest quarter-to-quarter decline since the share began to decline in 2022.

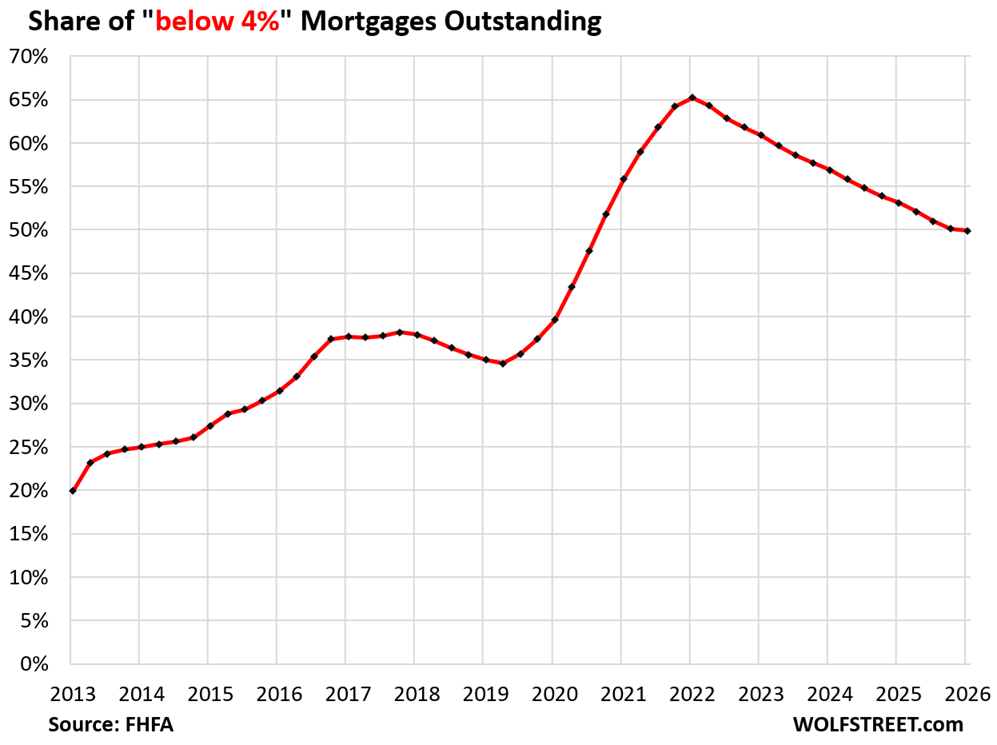

The combined share in Q1 of 49.9% of all mortgages outstanding marks the first time since Q3 2020 that the share of these ultralow-rate mortgages accounted for less than half of all mortgages outstanding, down from over 65% at the peak in Q1 2022.

From early 2020 through Q1 2022, the Fed’s interest rate repression via 0% policy rates and trillions of dollars of asset purchases, including mortgage-backed securities (MBS), had pushed mortgage rates to historic lows, which had created a tsunami of homeowners refinancing their homes into mortgages with these new ultra-low interest rates. And those low-rate mortgages have since then frozen up the housing market.

The share of these ultra-low mortgages declined since early 2022 because homeowners had to deal with changes in life that pushed them to give up those ultra-low-rate mortgages, either by selling the home or refinancing the mortgage: a new job in a different city, divorce, growing family, bad neighbors, death, financial issues, etc.

But now this trend has stalled. The stall of that decline in Q1 could be a blip, or it could turn into a larger trend of the housing market remaining frozen for even longer:

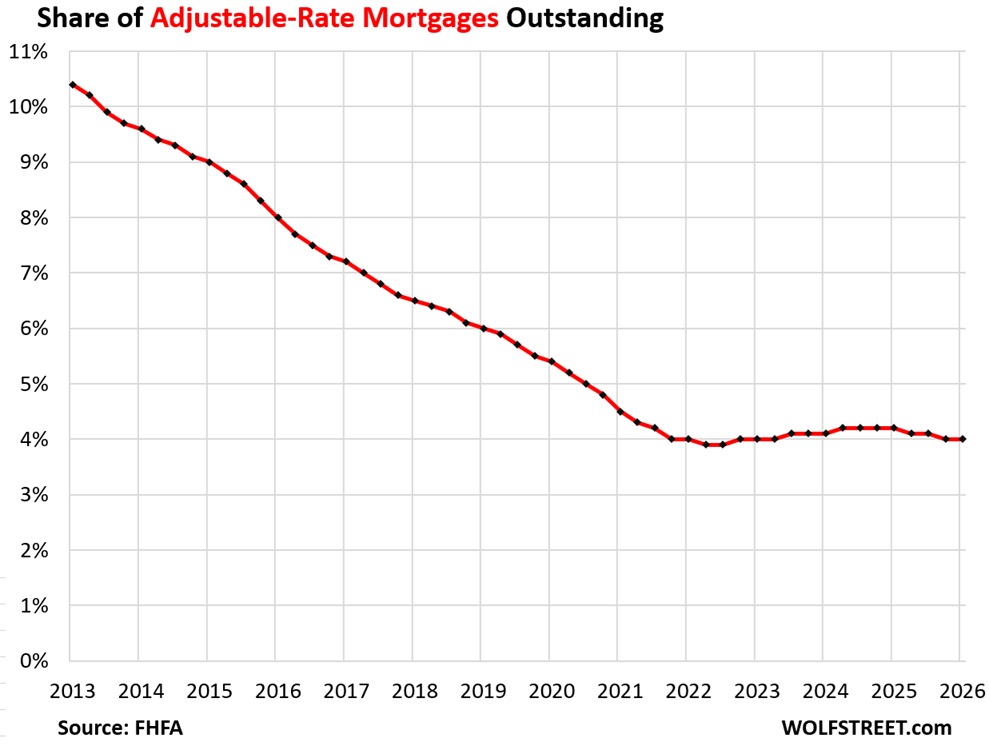

All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Adjustable-Rate Mortgages.

The share of Adjustable-Rate Mortgages remained unchanged in Q1 at 4.0% of all mortgages outstanding, and has hovered at these low levels since 2021, down from over 10% in 2013, the extent of the FHFA data.

Some ARMs had rates below 3% even before 2020, which is one of the reasons the share of below-3% mortgages was above zero even before 2020.

Homeowners with ARMs that were originated when rates were ultra-low experienced payment shock when their mortgage rates adjusted to the higher rates that began in 2022. But in 2020 to 2021, the share of ARMs continued to decline, and was very low when rates began to rise; so only a relatively small number of homeowners were affected by payment shocks.

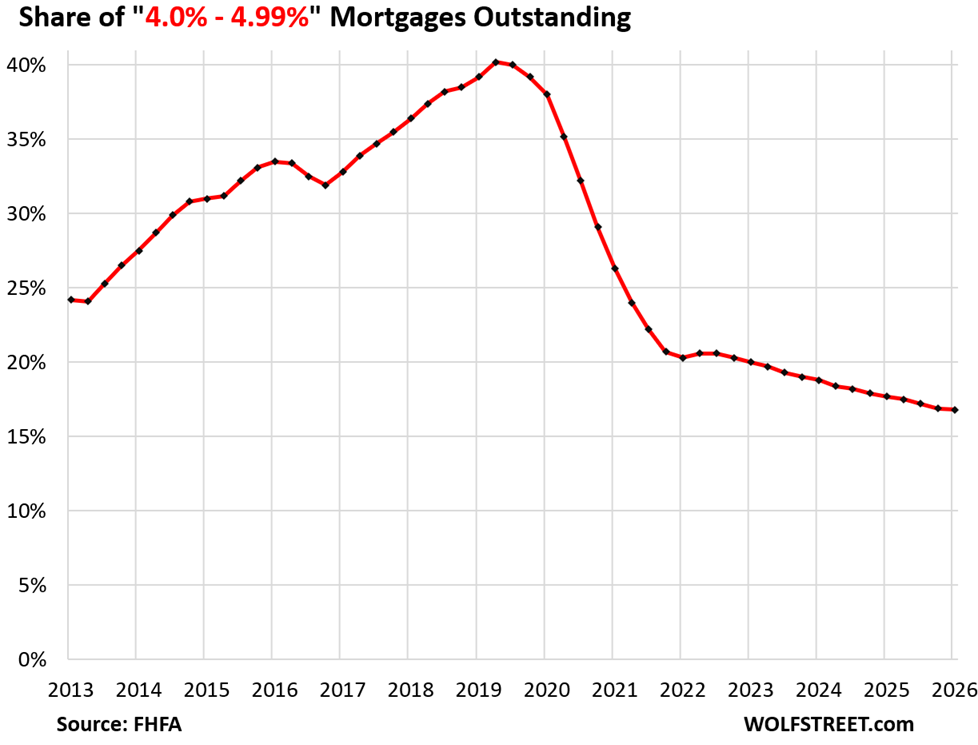

The share of 4.0% to 4.99% mortgages edged down by just 10 basis points to 16.8%, the lowest share in the FHFA’s data going back to 2013, and down from the peak in 2019 of 40%.

When the tsunami of homeowners refinanced their mortgages in 2020-2022 into lower-rate mortgages, not everyone could get a below-4% mortgage.

Homeowners who’d qualified for mortgage rates between 4.0% and 4.99% before 2020 refinanced into the lowest-rate categories, including below 3%, thereby refinancing out of this range.

But a much smaller number of homeowners who had 6% or 7% mortgages before 2020, due perhaps to a tarnished FICO score, also refinanced, but the lowest rates they might have had available were in this 4% to 5% range, and they refinanced into this range.

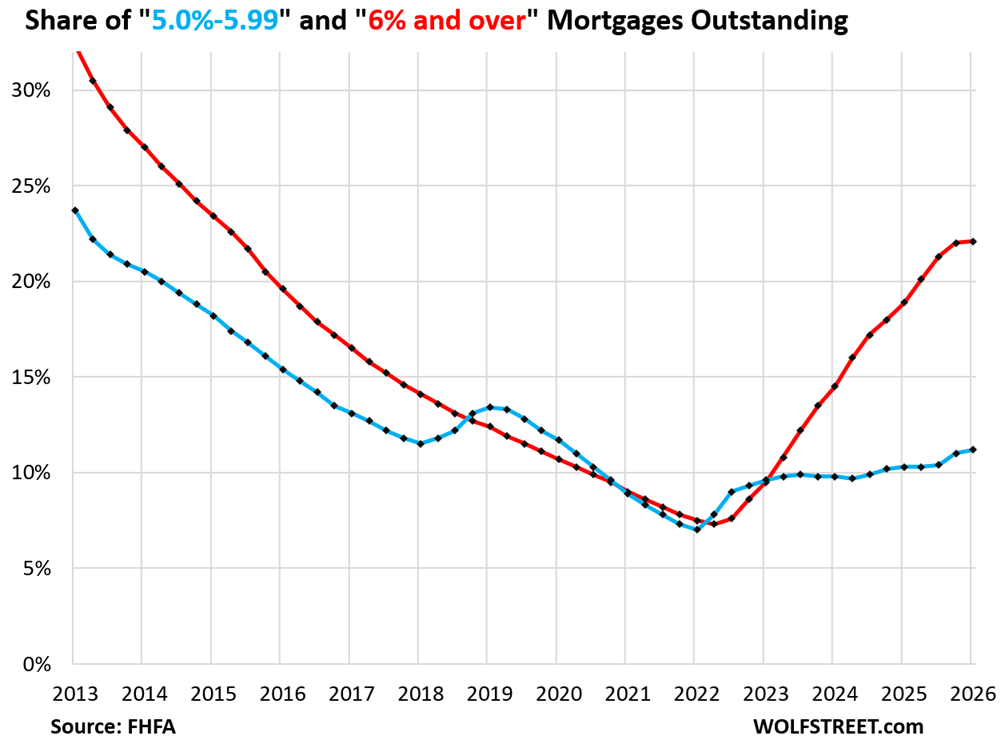

The share of 5.0% to 5.99% mortgages increased to 11.2% of all mortgages outstanding, the highest since Q1 2020 (blue in the chart below).

There are currently fixed-rate mortgages offered in this range. For example, the interest rate of the average conforming 15-year mortgage was 5.84% in the latest week – compared to the average 30-year mortgage rate of 6.49% — according to Freddie Mac. But 15-year mortgages, though they save large amounts of interest over the life of the mortgage, are not popular. Mortgage brokers and bankers don’t even propose them, and borrowers aren’t looking for them, because they come with higher monthly payments, and everyone is chasing after the lowest monthly payments – not the lowest amount of total interest paid over the life of the mortgage.

The share of 6%-plus mortgages edged up a hair to 22.1% of all mortgages, the highest since Q2 2015, up from a share of 7.3% at the low point in Q2 2022 (red in the chart). The bulk of 30-year mortgages originated currently fall into this category.

Combined, these 5%-plus mortgages now account for 33.3% of all mortgages outstanding, the largest share since Q1 2016 (not shown in the chart).

“Locked in” by Free Money.

People know when they get a generationally good deal, and they protect it. Below 3%-mortgages are free money in real terms because inflation is currently running well above 3% (CPI inflation in May was 4.2%). If the cost of borrowing money (the interest rate) runs below the rate of inflation, borrowers face essentially no “real” borrowing cost after inflation.

This gift didn’t fall from the sky but was the result of the Fed’s reckless monetary policies that caused home prices to explode in many markets by 50% and much more in just two years through mid-2022 and that helped trigger the worst inflation in 40 years.

Those ultra-low-interest-rate mortgages and the too-high home prices have chilled part of the housing market: those homeowners are now not selling and therefore are not buying either because they don’t want to finance a much more expensive home with a much higher interest rate.

The real estate brokerage and lending industry has called this the “lock-in effect,” and they loathe it because this effect has dramatically reduced commissions, fees, jobs, and stock prices in the industry.

But homeowners with these low mortgage rates don’t feel “locked in.” They’re just trying to hang on for as long as possible to one of the best deals ever: lower-than-inflation fixed mortgage rates.

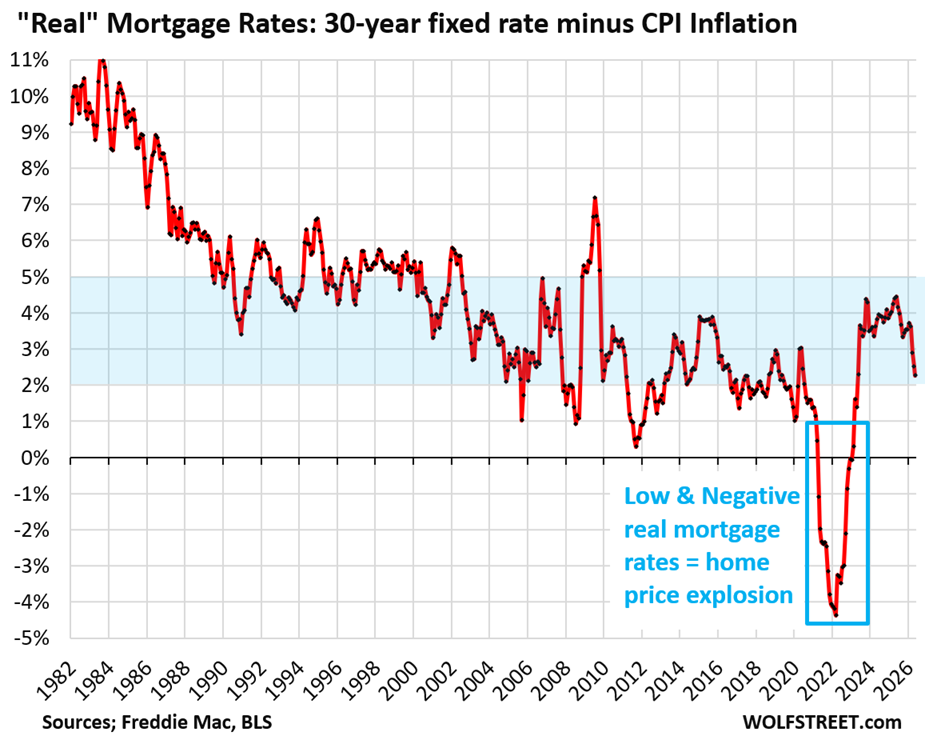

Between early 2021 through 2022, the average 30-year fixed mortgage rate was below CPI inflation – negative “real” mortgage rates.

At the peak of the Fed’s recklessness, “real” mortgage rates were 4 percentage points below CPI inflation, with the average 30-year fixed mortgage rate below 3% and CPI inflation exceeding 7%. This is what wrecked the housing market.

Also note how low these “real” mortgage rates currently are. It shows that mortgage rates today are not too high; if anything, they’re too low, compared to inflation:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Good analysis. It explains the housing market in one straightforward read.

Owner-occupied homes: About 60% have a mortgage.

All U.S. housing units: About 40% have a mortgage.

Therefore:

Approximately 40% of owner-occupied homes have a mortgage with an interest rate below 5%.

Approximately 25% of all U.S. housing units have a mortgage with an interest rate below 5%.

From my perspective, this means that roughly 25–40% of the U.S. housing stock has effectively been locked off the market. Millions of homeowners are financially trapped in ultra-low-rate mortgages and have little incentive to move.

This housing lock-in is, in my view, one of the most damaging consequences of Jerome Powell’s Federal Reserve. The rapid rate hikes may have helped curb inflation, but they also froze housing mobility, constrained supply, and made affordability even worse for buyers.

Thanks, Jerome.

What froze housing mobility was ZIRP and QE. Powell was acting redponsibly.

You can be upset with Powell, but be upset with the free money programs – NOT the fact that they were ended.

💯

Free money drove prices into the stratosphere.

you all miss real culprit

grifters in CONSgress who keep on spending OPM

remember we’d have BALANCED BUDGET if we could eliminate the TRILLIONS OF FRAUD annually

protected by uniparty system

Lol Brian Murphy. You complain about rate hikes without even realizing why they had to hike in the first place. The rates were too low thanks to Jerome Powell who kept saying that inflation is “transitory”. Its not.

Rates need to remain high so that people like these take the time to educate them instead of repeating mindless slogans like rates are too high, housing only goes in in the long run, date the rate marry the house etc. I don’t own a home yet, but I’d like to see some sense driven into people’s heads lest housing continues to get even more unaffordable.

@Brian Murphy

You are assuming you know everyone’s situation. We were already “locked-in” before COVID, not because of our mortgage but because we really like our house and location. We had no plans to move (and still don’t), so we refied when the opportunity presented itself. We are no more locked-in than if we hadn’t refied. We might be less locked-in, financially, because we took the opportunity to shorten our loan term and accumulate equity faster, rather than reduce our payments. I assume our situation is not unique. Are some folks locked-in? Absolutely. I’m saying that your calculation makes an assumption that leaves out folks in my situation.

While always keeping a eye out still on “buyers strike”,this will prolong said strike.

we’re planning on downsizing(we have 3.35% loan)

but we’re taking different path

selling rental after remodel, waiting for year(because of 1031 laws)

then moving into and selling our place and paying off said mortgage

oh, our rentals have total of $0 of mortgages

They always said the cure for high prices is high prices.

I marvel at what garbage people spend their money on.

I just need a cottage in fly over country, not a mansion on the coast

The ability to borrow MORE money on the same house AND get a lower interest rate while doing it??? Realtors and mortgage brokers can badmouth these homeowners all they want but as that last graph shows… this really was the financial deal of a lifetime.

Just another gift and legacy of Bernanke’s and Yellen’s Federal Reserve’s ZIRP and QE. Negative real rates. Who won? Wall Street and its bankers.

Who lost? We are living it.

I and a lot of other mortgage holders won. I’m at 2.65% with no plan to sell unless circumstances force me too.

I feel blessed, not locked-in.

Agreed. My 3% mortgage is great.

ZIRP was stupid but no one was stupid for taking advantage of it.

Ever heard of a Faustian bargain?

Nah, there wasn’t no Foostian bargain. It is sickening how far behind those not holding assets have been positioned, but this has nothing to do with moral integrity. Lots of people went all in betting on the crash before covid and did not hold assets. Now claiming some moral high ground for losing the bet is just coping.

“Now claiming some moral high ground for losing the bet is just coping.”

So cheating is acceptable as long as you win the bet? And when what goes around comes around, i’m sure you’ll still feel that way.

The lack of wisdom is astounding. Cheat for short term gain and power, end up with a french revolution, but it was worth it, i swear!

Mr.House can you explain why its a Faustian bargain ? As much as I don’t like the housing situation, i can’t blame people for not taking advantage of it. I only became financially aware too late which is why I am behind. But thats ok. Hopefully, my time will come too. Maybe sooner than expected, if some of these people have to sell in distress.

@Mr. House,

Taking a good deal from my local friendly megabank, a deal they offered everyone with good credit, is cheating? Or do you mean something else?

I think reverse-mortgages of all types are going to become an upward trend soon. IMO more people will staying put and need money for maintenance, medical, etc..

There is much stagnation in housing now. Can’t afford to buy, demand goes down, putting a ceiling on prices, and elevated sense of what a house will sell for, even if it won’t sell now that puts a floor on prices. Which side will bend or break first? Downsizing is a financial wash or worse for most.

IMO, living in place , however it can be done, will become an ever more viable option, as long as the owners can ambulate and are lucid. I would rather die in my home than in an assisted living/retirement home. Nobody gets out of here alive.

Getting a “reverse mortgage” means getting a new mortgage: you pay off your old 3% mortgage and get a new mortgage under much worse conditions. Reverse mortgages can be ruinous, and you might lose the home and all the equity you had in it and end up with nothing when you’re very old.

Absolutely agree.

However, keep in mind that desperate people do desperate things. We shall see what % of home owners, at all levels of income, will fall into this category for a myriad of reasons going forward.

I have 3 separate older friends and family who reverse mortgaged their homes.

They asked my opinion, and I encouraged them not to, but they did anyway.

All 3 regretted it very quickly. For all 3 of them it was a very financially harmful product.

In my opinion many companies who offer these products are very predatory, and prey on those less financially savvy and in the lower income brackets. The products were not even close to being as advertised, borderline/ probably criminal.

Fortunately, one of the elderly couples was able to get out, but it was very costly. Almost ruined them.

What exactly were the problem each encountered?

I’m in the mortgage space and I used to do reverse mortgages on occasion for certain clients if they came around. The reality is only about 2,000 per month are created and of those about 15% of them are refinances of a reverse mortgage. With rates at their current levels it’s not very advantageous to get one and the fees you incur to get one you better really need it.

One of my friends took out a reverse mortgage. She was not of sound mind and had no business signing the papers.

But she did. And, long story short, she lost the house.

Howdy there, AZSlim

Long time no see! Still riding that bike around the neighborhood?

Seems that a cash-out refinance may make better sense. Even for someone who has paid off their mortgage.

Don’t listen to Magnum PI and reverse mortgage your home !!

For most, there are far better options.

Can I know some alternatives? serious question.

I used to sell and believe in reverse mtges. I’ve seen the 80+y.o. literally eating cat food so they don’t touch their very large equity, so kids have some inheritance.

The kids likely won’t have an inheritance with a reverse mortgage as the entire mortgage must be repaid in full when the owner dies, and that usually happens via a sale of the home. That mortgage gets bigger every month as payments are made and as interest compounds. It is eating the equity at a rapid pace. And unless the kids have enough cash to pay off the entire huge mortgage, there won’t be a house for the kids to inherit.

There are lots of reasonable ways to deal with a home that has lots of equity, whose elderly owners want to supplement their retirement income. A reverse mortgage is probably the worst most expensive way.

Many of the burdensome regulations affecting the sale and financing of homes has been carried over from the Biden administration and the corrupt Powell Federal Reserve. Trump never got rid of them. We are the victims of these regulations and lost our jobs Appraising RE Properties along with 30% (soon to be 50%) of those in our profession. So in addition to the lock in affect cited above, look for a crisis in the ability to close on financing as there will be no one left to complete the massive paperwork that has been added. These new regulations are slated to go into affect this November.

Good news then for cash buyers.

…….and the historic context is, reverse mortgages were first “regulated” by Republican majority Congress during the Bush administration. Let’s give the banksters all the cards in the deck. A snowball becomes an avalanche with time and incentive. Both Bush 1 and Ob ama dealt with Banks deregulation! The bailouts supported the banksters first and foremost.

The Republican politicians in Congress have been whores for the banks.

I say that as a Republican voters.

Is the US the only country offering 30y fixed rate? I think I could maybe get 7y or 10y at best but with higher %. Those 30y fixed rate mortgages are nice, though rate hikes end up having a dampened effect if homeowners aren’t forced to refinance

The low interest rate for a 30 year is only beneficial if one rides out entire mortgage or the house appreciated significantly because the majority of the payments for the first ten to fifteen years is interest.

Not true.

My 2.5% 30 year mortgage was barely above 50% interest on the first payment. By month 28 I was 50/50.

With a 6% loan the 50/50 month is Month 222!

And a faster way to pay less interest is to pay mtges bi weekly rather than monthly. Makes a difference of some five years in mtge payments

Another aspect not explicitly mentioned is that these ultra-low rates massively benefited anyone getting a mortgage in those years. The people left out were those not in a position to buy a home in that period, disproportionately younger and poorer people, who now have difficulty buying a home at current prices and interest rates. This also spills into higher rental prices. This government-created separation of the haves and have-nots is, in my opinion, helping create the political radicalization we are seeing in recent elections.

Actually, the ultra low rates managed to benefit people simply refinancing their homes rather than buying new (or replacement) homes. That is because of the massive spike in home prices during that same time frame. So the people left out out (disproportionately younger and poorer people) really were NOT hurt by the ZIRP phenomena since they have instead benefitted by the massive drop in housing prices in the past five years.

It is more a case of the “rich get richer” than of the poor getting poorer since the poor weren’t in a position to take advantage of a once in a lifetime good deal. There is no doubt a knock-on effect of fewer houses being on the market so home prices are still elevated beyond what they should be…

Massive drop in housing prices in the past 5 years? In some places, like Austin (you can go to Wolf’s charts and get the specific cities), but in many places, prices have leveled out or dropped a little bit. And in others, prices have continued going up.

One thing to keep in mind is that the principal may be falling vs the total value of the home (as perceived.) If one has a 3% mortgage with 80% LTV it’s more attractive to hang onto it. If one has a 3% mortgage with 50% LTV then the other 50% is dead money that could be invested in NFTs (just kidding!)

But the return does have to take in the opportunity cost and the math may have changed in the last half decade. It certainly has in my case, making me feel much more “meh” about my low interest mortgages… still not enough to act on getting out, but enough to not quite be whistling zippity doo dah out of my nether regions.

Welcome back Wolf, good to see the fresh meat on the page!

When market rates exceed a homeowner’s mortgage rate, the probability of sale drops sharply — by 18.1% for each percentage point spread. IOW, those with 3% in moribund markets are squeezing the last drops of juice from the lemon in terms of tax advantage. Rationally choosing to retain cheap debt rather than pay off a depreciating asset — effectively extracting the last remaining financial advantage from local structurally weak housing environments.

To this foreigner the US mortgage system looks bonkers. I suppose the US taxpayer must be subsidising it – might it be wiser to try free market capitalism instead?

dearieme – You speak the truth! Unfortunately, the transition would cause total anarchy when the value of homes suddenly drops 50%. The dependent would need to be slowly weaned off the government teat.

Also, the self-righteous would have to admit they are actually living like welfare queens!

It doesn’t just drop 50% because in other countries people get out their crystal ball and look at either getting an ARM, 3 year term, or 5 year term. There is not a collapse surge because people don’t lock in for so long. I have done mortgages a few times over my life. On the ARM you can instantly lock in to any of the others at any time….you aren’t just stuck with it and then get the shaft. This option is negotiated. Plus, a 15 year or 20 year mortgage is considered max and folks often pay bi-weekly or double up a mortgage payment at the end of each month. On the yearly anniversary date you can also do an additional bulk payment off the principal, usually 10%, but some mortgages allow more.

How are the double ups possible for Joe Shmo? You start by buying in an affordable area rather than some over priced place you just have to live in. You pick a career that makes this possible. Live within your means and never never add on extra payments for anything at the time of mortgage renewal. This means no car loans folded into the mortgage and probably entails no car loan at all, rather, drive junk, bike, walk, or transit. While you are buying and paying off a house vacations are modest and dining out is reserved for events or as a special treat.

Furthermore, the 30 year fixed screws the market as we all know. It freezes it up.

I do want to address the assumption of housing being overpriced. Yes, in many markets it is, However, and I speak as someone who is still building strong at age 71, materials, permits, code, furnishings, and labour have all produced a new build at $450/sq ft in my area. In US dollars and prices maybe $350-400 per sq ft. A 1500 sq foot home price is simple math. If you want to then go smaller, why then the land prices in many places are too high to justify it all.

I’m going to suggest that wages (and expectations) have simply not kept up to costs in all sectors, not just RE. The Dream is dead/dying because the dream is now priced as unrealistic. I also think slow and steady can still win this race. You remember the old arborite and shag carpet starters from the 70s? It was cheap. California stucco on donacona….cheap. 65 amp service….cheap. Remember folks saying, “Put on a sweater”. They probably grew up in the Great Depression.

The 30 year should be phased out and people need to adjust expectations. Needs and wants. Needs and wants. Make a plan then stick to it.

My 43 year old ex tenant just bought her first home. It closed June 10th. She ditched the Thailand and Mexico vacations for the down payment. It took her a few years. She operates heavy equipment at northern gold mine for her employment, 2 weeks on and 2 off. She bought a 1 year old modular on a small lot and very proudly sent me photos. It looks very very nice. I am making her some planters for a house warming gift. :-)

regards

There is a similar problem with Australia’s Superannuation system. Basically, in Australia, a person can use their home like an American would use an asset in their 401k. This has led to a run-up in prices which has make Aussie housing utterly unaffordable. In addition, rising prices attract even more investment so Australians and foreigners are basically bidding up the price of anything and everything on the greater fool theory. But when greater fool theory is supported by government policy, it seems a lot more sustainable.

But, as you note, fixing the system would involve popping a bubble and depriving most voters of a whole lot of home equity.

For young people, the solution is not to play the Boomers’ game. DO NOT buy a house. Rents are the only thing set by the free market and if that’s cheaper, pay rent and apply your savings elsewhere.

I would like to see a system closer to the five year term of Canadian mortgages. I don’t know how else their process differs but it would certainly make people think more if they had to refinance to a different rate every 5 years. I’m getting pretty tired of being the ant while the grasshopper plays.

I love reading the comments from this well-informed subscriber base!

The only people locked in are those who bought MBS yielding 3%. Sadly that includes all Americans since the Federal Reserve overpaid for MBS to try and prop up the COVID economy.

People who bought in ~2022 paid the absolute highest price for what they got. They financed that debt with low rate mortgages but it will be a long time before someone else is willing to pay what they paid. Enjoy the low mortgage rate while you wait.

The fact that people have given up trying to sell for a profit and are just holding on now is good. That means prices will not be going anywhere until the housing market is truly healed – the Fed’s MBS pile is essentially gone, rates are in the healthy 5-7% range (10-year slowly getting there), and people have completely stopped thinking of houses as speculative investments. I give it 6-8 more years.

Back in the 80’s when the S and L blew up for corrupt lending 800 bankers went to Jail and Assets were sold off in bankruptcy. In 2008 corrupt lending resulted in one arrest and Federal bailouts as too big to fail banks were saved by interest manipulation and no mark to market accounting. In 2020 covid money dumping the Fed thought money going to the people would not cause inflation as had been the case in 2008 when money went to the banks. Big Surprise now we get to live with it.

Voters told politicians to make the economy go back up.

An engineering tradeoff was made.

The reason everyone around you can spend like drunken sailors is they were gifted a house by the government. Then gifted all their student loans back by the government. And if they did the PPP scam, got gifted a few tens of thousands of dollars on top of it as a treat.

Meanwhile if you’re a sucker who paid your way through college, works a job, pays taxes and pays your rent on time every month – you’ll never get anything. Because the Government hates you.

Beta, to be clear, GUVMINT does not hate us, it just ignores us IMVHO…

Mainly because WE, in this case the WE the People who save and pay off every debt on time and usually without interest or ”fee s” will also bee those voters who will NOT vote ”the party line”,,, but will and DO vote for the best person representing the best choices for us and for all folx…

Time and enough for USA to get our, repeat OUR, vast debt paid off and behind us, if for no other reason than so as to NOT burden our children and grand children with the very clear results of that debt…

I did not refi my current 5.125,just paid in down to almost nothing. I think that was the better deal when all that free money was flying around. No closing costs to deal with,closing costs are a killer when you have a 3 % mortgage. They either get you in the front or the back.Either way nothing is free as we all can see now.

I was fortunate to refi from a 30 yr to a 15 yr at 2.5%. I now only have 9 years and 5 months remaining. At the time, I could have paid 1 point for a 2% rate. Crazy, huh?

Off topic: No Sen. McConnell sighting since June 14th. His staff say that he is conducting the people’s business and not to worry. Is this Washington D.C., “Auto-Pen 2.0?” Maybe “Week-end at Bernie’s!” lol

Well, exchanging liquidity for leverage isn’t a free lunch, but better to be the debitor than the creditor for these loans – both with the inflation angle and potential loss of collateral value if the borrower defaults for the newer loans.

A return to the times that supported valuations seems unlikely. We’re a 3-5% inflation rate nation that claims a 2% target. So inflation and new supply will have to fix things I guess.

Another factor in that market is going to be what people do from here on. Thus far, you were told to buy a home. That is just “what you just did” like smoking back in the day and so on.

Bu I’ve seen stats from NY finance types that show half of US folks won’t ever have gotten married by the time 2050 rolls around. And you look at large American cities and they ain’t planning suburbs any longer.

So the housing people in the US housing lots (a nice way to put it) might not have the same base they once did in the future which will cause a lot of changes if so.

Yea what’s missing from the criticism of reverse mortgages is that the kids will absolutely NOT need a way of life that is unaffordable.

They’ll be single, divorced, or single parents, so they won’t need 3BR/2BA and bigger family sized homes. They need 1-2 BRs and they don’t need to be tied to one location when the job market is dynamic.

Also, those family sized homes were never built to a quality standard that we should expect to last for multiple generations. All the plumbing is rusted, the plastic coating on the wires is deteriorating and flaking, the asphalt roof only lasts 20 good years, the drywall is moldy, the HVAC is only good for 10-12 years at a time between five-figure replacements, and the sticks have probably attracted termites in a few places. A typical American home, by the time it turns 50, is on borrowed time before it needs to be gutted and rebuilt for some six-figure amount.

And then what do you have? A long commute, a bunch of yard work, and an isolating social environment that makes people crazy. Just like it did your parents.

You must be the life of the party.

This data really highlights the irrationality of the ‘lock-in’ label. It’s not that these homeowners are ‘locked in’ they are just acting in their own best interest by holding onto an asset that is essentially outperforming inflation. When the cost of borrowing stays below the rate of CPI, it’s a rational financial move to stay put, not a mistake. We shouldn’t expect significant inventory shifts until the spread between current market rates and these legacy rates narrows significantly

The top Realtor here in the Swamp stopped putting out 4th of July American Flags on everyone’s lawn like in previous years. Reason was mostly likely there is no business to be had. No one is buying and no one is selling. Realtors are SOL (S$it out of luck) and are the first casualty of the lock in affect. They are dropping like flies out of the profession, and have few skills that are portable to other jobs. You can thank J Powell who destroyed lives and careers, and markets with his bankrupt policies.

Re “” They are dropping like flies out of the profession, and have few skills that are portable to other jobs””

Not sure that I would agree. IMHO (not a broker) they ability to search for “saleable property”, find potential customers and close a deal . with all the red tape involved .. can and will be useful in any number of professions that involve dealing with people and selling things.

Love .. Jenny (singapore)

Wolf,

Are you aware of any data on the actual balance of these mortgages <4%. The absolute number is helpful, but the balance info I think would paint a clearer picture.

It’s easy. The unpaid principal balance of all mortgages that the FHFA has in its data is $12.3 trillion. The below-4% mortgages account for 49.9% of that, or about $6.15 trillion of unpaid principal balance.

People gripe about whatever they don’t like and have zero gratitude for all the things that do go right.

JPow and crew may have been slow to react to inflation in 2021-2022, but look at what DIDN’T happen:

-They didn’t keep rates too high during the 2020 economic crisis, as the unemployment rate was skyrocketing and tens of thousands were dying each month. Unemployment peaked at 14.8% in April 2020 and started going back down as liquidity flooded the market and allowed businesses to resume operations*. Had those rate cuts, QE, and fiscal-side interventions not been announced around this time, things would have gotten much worse and stayed much worse for a longer time.

-They didn’t raise rates by 500bp in one meeting in late 2021 like the critics imply they should have done, because that would have raised the unemployment rate to >20% overnight, led to waves of bank collapses or the insolvency of the FDIC, and caused asset prices to collapse. The result would have been a depression. If you’ve had assets appreciate or held down a job over the past 5 years, consider sending former FOMC members a thank you card.

-They stopped the rate-hiking at 5.25%, even though inflation had just been higher than that. This was a risky move, but it proved to be the correct thing to do when there was disinflation and no recession in 2023-2024. The Fed had threaded the needle.

-They prevented the banking system from collapsing, save for a couple of bad actors in 2023. Special lending windows were established to help banks maintain liquidity. Had the banking system collapsed, again, we would be living through a depression right now instead of 4.2% unemployment. Housing would be cheap, but only because nobody could afford anything, just like in the 1930s. Do you really yearn for that life?

-We always talk about how inflation and home prices are bad.. blah blah. But do we ever talk about earnings? Indexed to the start of the COVID recession, hourly earnings for private sector employees are now 31.9% HIGHER than they were in February, 2020**. So people not living off of treasury dividends should be able to afford much higher home prices. If we graph hourly earnings next to CPI, and index both to 2/2020, we see that the two lines overlap. The average worker has the same purchasing power now as they did before, and that’s an amazing accomplishment considering the scale of that crisis. What more could we have realistically asked for five years ago?

Finally, the haters don’t even get their dates right. JPow wasn’t a rate cutter, on net. He was installed in February 2018 amid a rate hiking campaign that continued for another +100bp. He then oversaw the cutting of rates by before and during the COVID crisis by -225bp, only to then raise them +525bp. Then he oversaw -175bp of rate cuts in 2024 and 2025. Do the math or just look at a chart and find that JPow oversaw a net +225bp of rate increases during his tenure.

So this was the big tradeoff everyone is grouching about? Rates 225bp higher in exchange for dodging a severe, generation-defining economic depression with widespread unemployment, poverty, and assets/RE that can’t be sold except at a steep loss?

Imagine the complaining if the Fed had instead errored in its approach and we actually experienced another Great Depression instead of a series of boom years!

Sorry to hurt some feelings here, but if you’re complaining about the Federal Reserve because economic growth boosted asset prices, then you really need to read a book about how people lived on one can of beans per day back in the Great Depression. Then learn to cultivate some friggin gratitude that you haven’t had to live through such deprivations (yet). Finally, read up on Andrew Mellon’s populist “liquidate everything” approach, before spouting the same nonsense prescriptions that were debunked by the Depression.

Bottom line: The politically independent Fed has proven the value of its approach over the past decade. By all rights we should have been in a 2nd Great Depression by now, but moves by the Fed have prevented that from happening (so far). Have some gratitude.

*https://fred.stlouisfed.org/series/UNRATE

**https://fred.stlouisfed.org/series/CES0500000003#