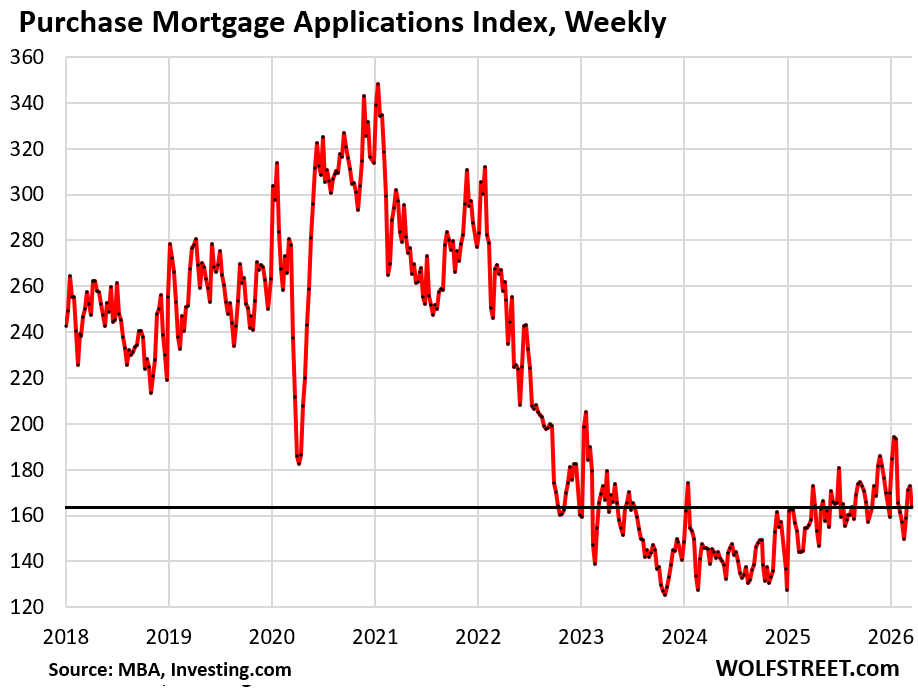

Mortgage purchase applications are down by 35% from the same period in 2019 in a housing market that remains frozen.

By Wolf Richter for WOLF STREET.

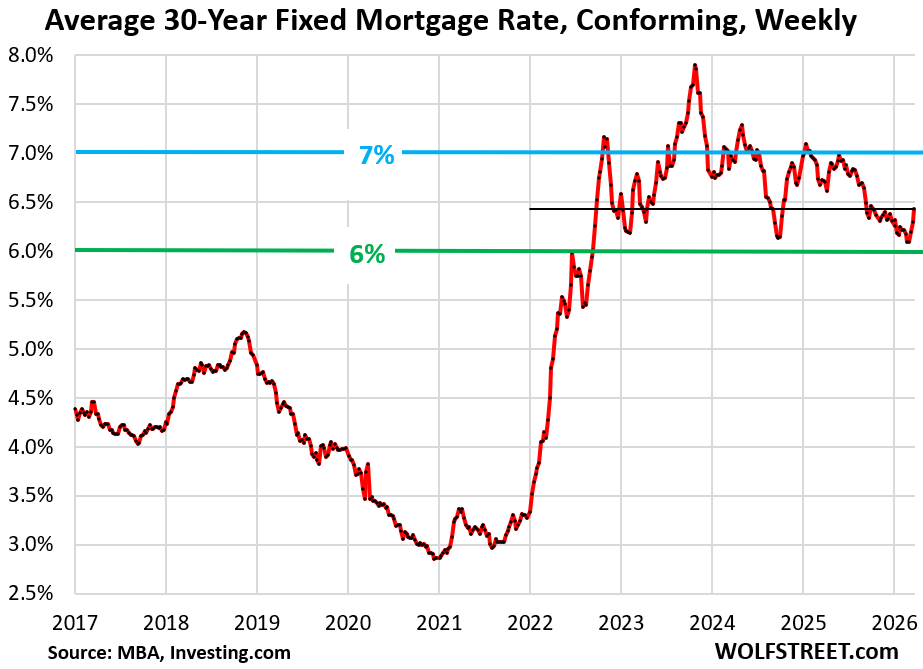

The average weekly mortgage rate for conforming 30-year fixed mortgages rose to 6.43%, the highest since October 2025, according to the Mortgage Bankers Association today.

This weekly measure of mortgage rates is once again solidly in the middle of the 6% to 7% range that has prevailed since mid-2022, and that before 2008 was considered relatively low to normal.

It’s just that the Fed’s QE, which included the purchase of trillions of dollars of mortgage-backed securities, had repressed overall interest rates, and specifically mortgage rates, to recklessly low levels – 30-year mortgage rates below 3% even as inflation was shooting toward 9% – which had triggered the fantastical home-price explosion through mid-2022 that left prices beyond where they make economic sense.

And so annual home resales have plunged by 23% from 2019 in each of the past three years, mortgage applications to purchase a home have collapsed by 35% from the same period in 2019, the industry has been decimated, and the housing market has been frozen, now in its fourth year, while supply of resale single-family homes surged to the highest in 9 years and inventories of new completed single-family homes reached the highest since 2009.

And the much hoped-for and hyped spring selling season, on the expectations of miraculously lower mortgage rates, is already turning into a dud once again.

Mortgage applications to purchase a home fell in the current survey week for a miserably low beginning of the year and remain near rock-bottom levels, down by 35% from the same period in 2019.

That drop of roughly 35% from the same period in 2019 has prevailed in February and March, after a slight improvement late last year and into January.

Purchase mortgage applications are a measure of demand for homes that may become actual home sales in the future and are therefore a forward-looking indicator of home sales. And it’s not looking good for the spring selling season.

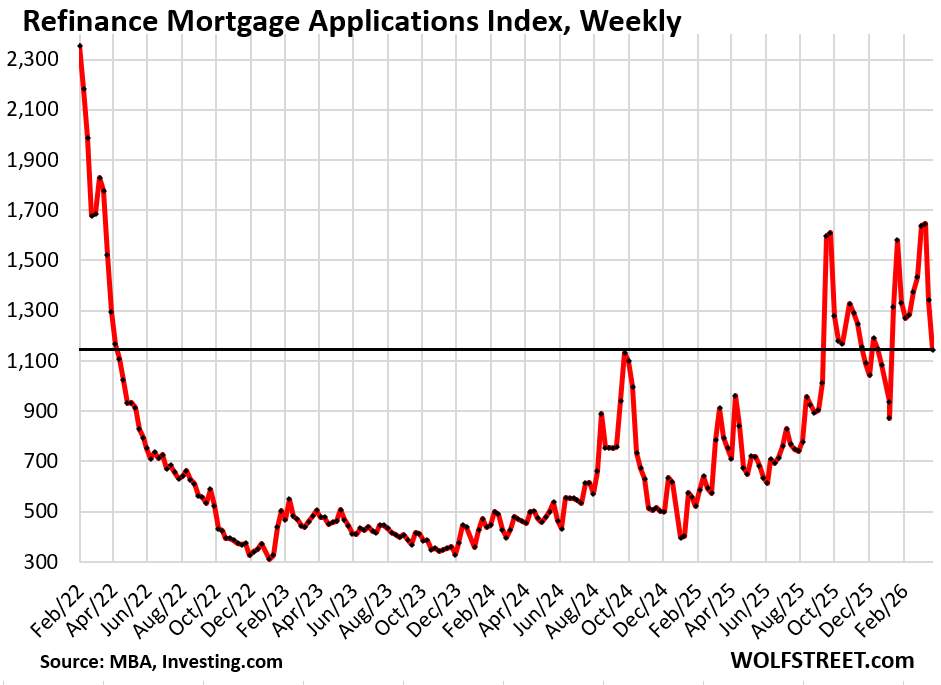

Mortgage applications to refinance a home plunged for the past two weeks from their spike in early March, as mortgage rates have risen.

When mortgage rates dropped even a little, refi applications spiked as if homeowners were sitting at their screens, just waiting for the right second to pull the trigger. This process has been repeated several times since October 2024. Any dip in mortgage rates brings out new waves of homeowners that pounce on refinancing a mortgage at a lower rate, or to pull out some cash. And when mortgage rates bounce off that dip, demand fizzles.

Refinancing a mortgage is not free. There are up-front fees to be paid by homeowners when they refinance a mortgage – typically 1% of the mortgage balance – and those fees are then added to the loan amount and increase the payment, which reduces the advantage of lower mortgage rates. Homeowners who want to refi a mortgage to lower their payment do a breakeven analysis with online calculators or through brokers and mortgage lenders, to see if refinancing the existing mortgage is even worth it. When results tilt their way, they pounce, creating these brief spikes in refis.

Mortgages also count as refis when homeowners that no longer have a mortgage get a mortgage to take that amount of cash out of the home they own.

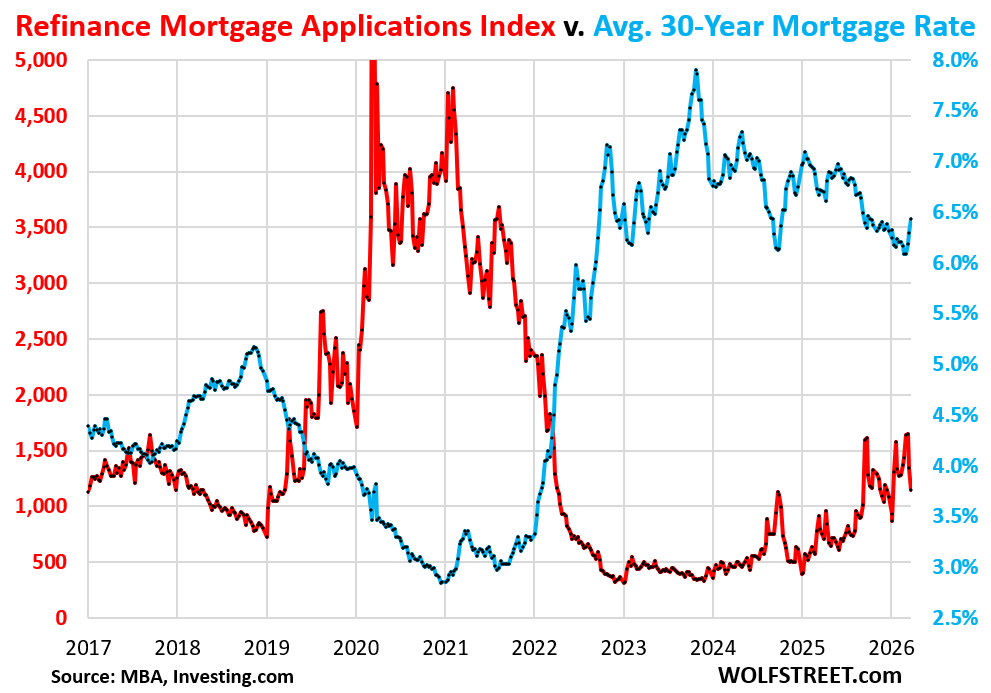

But even the highest refi activity this year was relatively low compared to the refi boom of 2019-2021.

This decade-long view shows the tight inverse relationship between mortgage rates (blue) and refi applications (red):

In case you missed it: Whatever it takes to sell lots of homes in this frozen market? Homebuilder Lennar Cuts Average Selling Price by 24% to 2017 Level.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

– I see a releationship between the closure of the Strait of Hormuz and these rising interest rates. When the oil stops “flowing” then it undermines the PetroDollar system.

– I am still not too worried. I still think long term rates will / could go down in the near future.

There is no “petrodollar” system. It died years ago. the US has become a net-exporter of crude oil and petroleum products and has a massive trade surplus in the energy trade, and there are no petrodollars to recycle. Instead the US is bringing dollars back to the US with its energy trade surplus.

Indeed. Add Guyana with, if they secure it beyond the initial effects of president poaching, Venezuela, to the US energy sphere and there’s going to be a a deep well of dollars over many years.

Maybe enough for the odd game of middle eastern whack-a-mole or other disruptuon of Mackinder’s heartland.

And Argentina with vaca muerta.

There is a reason every gulf country is desperately seeking to shift their economy from oil exports.

China has significant potential via fracking–supposedly greater than the US.

Do tell more. All kinds of Bechtel, KBR, Fluor, Wood, Hyundai, and Samsung activity when the dust settles. Tops off now on open insider trading. NG $$ for US consumers is up over 30+% and just starting. Western US is gonna be tinder dry on 2026.

Is this satire on what you think Keynes would say or your opinion? Tom Lehrer claimed satire was obsolete after Kissinger won the Nobel peace prize. Just saying

There was never any such thing as the ‘petrodollar’ and oil has always been used as a purchase of less than 5% of US dollars.

“I see a relationship between oil flowing and these rates”

Thanks captain obvious! /s 😉 hehe jk

Timberrr !!!!

For housing prices that is.

My guess is the Iran war is the biggest reason.

Depends on the neighborhood. Higher end is going to get considerable more expensive. Lots of dollars are coming home, at least for the upper 1-5%.

“Darling, tell our butler to hire himself a butler.”

‘Coming home’ from WHERE?

I take it you have never had an offshore bank account…

…not surprising.

LMFAO!

I have been anticipating a general housing bubble pop since 2004 based on mortgage rates exploding higher and plunging sales.

Except for a few specific markets, it has been the wrong call.

2026 may be the year!

Depends on the market. For many markets, the top was in mid-2022, and price have plunged since then, including Austin, Oakland, New Orleans,

https://wolfstreet.com/2026/03/17/the-most-splendid-housing-bubbles-in-america-price-drops-gains-in-33-big-expensive-cities-february-2026/

New Orleans has a stagnant economy but the biggest hit came from the rapid rise in homeowners insurance following Hurricane Ida in 2021 and the premium increases on flood insurance due to federal reforms which primarily affect new policies. A modest home in south Louisiana, inside flood protection, will pay $400 per month in homeowners and $250 per month in flood insurance before PIT. This killed plenty of sales since 2023.

Coming soon to a neighborhood near you.

Imagine if coastal California homeowners were required by the GSEs to purchase earthquake insurance.

Insurance is a VERY TINY part of the cost in owning properties.

New Orleans may be on the verge of becoming uninhabitable. This is from a recent article from nola dot com about the 100+ year old tap water infrastructure. I have no idea how this will ever be addressed.

“In 2003, a consulting firm delivered a 565-page document with a soup-to-nuts assessment of the water system’s condition, along with a prioritized list of projects, timelines and cost estimates. The price tag: $2.8 billion over 20 years.

While the 2003 plan from consulting firm MWH is now well out of date, it offers a sense of how arduous, and costly, the challenge ahead is for the S&WB. Even then, large chunks of the system were at the end of their useful life and hundreds of miles of pipes needed to be replaced across the city’s neighborhoods. More than twenty years later, the S&WB is farther behind.”

It’s like the bubble is giving us the middle finger.

Aside from some subtle differences, I feel like this is almost exactly what I could’ve written.

I called the 2008 crash, but I’ve been mostly wrong ever since! 😀

Since 2004? Did you fall asleep at the wheel during 2008-2012?

Did you fall asleep at the wheel again during 2020-2021 when money was free?

Long overdue. However, lots of dollars coming back to the U.S. and wealthy people often will park money in real estate, so good rentals or nice vacation properties will not see much of a price decline. Mid and low-end housing will definitely drop in price.

But Wolf has already documented some of the once hottest markets already crashed in price by 25% from its peak.

The problem with this analysis is timescale. In 2010 I bought an ex-urban Austin condo for $66k. Sold in 2015 for $100k. Peak 2021 it sold for $235k and now listed for $190k. Sure for the 2021 buyer it sucks (though less with the 3% fixed mortgage), but that’s a small share of the owner population and most have seen enormous gains over the last couple decades.

Those sitting on gains will only benefit if they sell before prices in Austin fall more…

True, though lots of that appreciation value washes away unless these homeowners either downsize or relocate to a more affordable market. Certainly possible, but not an option in everyone’s cards.

Personally, I wish shelter hadn’t become such a focus of investment and speculation. We should buy homes for the value they provide, not as a money making endeavor. Such is the world we’re in now I guess, but I find it unfortunate all the same for the broader society as a whole. And I say this as a homeowner with beneficial appreciation value in my own home.

I live in a “vacation” area. After contesting my property taxes last year with another appraisal and comps, apparently a Midwest wealthy person overpaid for my neighbor’s house by over 40% for a smaller house.

I don’t think I have a leg to stand on for contesting taxes on my forever home next year.

Wish me well as my property taxes increase while my income decreases during retirement. However, don’t shed a tear for me while I am the wealthiest house poor person in the area. Maybe I’ll move to Tulsa.

Tulsa is down now but with Middle East oil bottlenecked, maybe it is a good time to buy and make sure to sell before the next oil crash. I’ll be an itinerant retiree going between data centers, oil centers, and Amazon warehouses.

We need a good stock market crash like 2008.

The wealthy people won’t invest in RE in my hood because they lost it all and fear will rule both stock and RE markets. I don’t know where all of the gold, silver, and BTC bugs are going. That concerns me.

This sounds greedy because I’ve been mostly in safe ST bonds for the last year. I hate speculative unstable markets with money I intend to live on.

My biggest fear is safe US bonds will become less safe in my lifetime. The Bankruptcy King is in charge.

The good news is Tulsa is in the semi=finals of the NIT !

Saul Goodman’s best line:

Jesse has no money but owns a large brick home in Sante fe NM

“You’re house poor!”

😂

“Wish me well as my property taxes increase while my income decreases during retirement.”

Just sell it for the 40%+ and move. What’s the issue?

But my dream was to live the rest of my life in my payed-off Golden Sarcophagus(while wrapped in bandages from having too much fun mountain biking and skiing).

Isn’t this the American Dream to work 30+ years to pay off a 30 year mortgage and retire with a payed-off fully owned house? The house is never yours while taxes exist and can go up 40% per year. Despite its faults, Prop 13 in CA allowed this for my parents. I see a wave of new Prop 13’s in other states.

Coming home from where? Are you a real estate agent?

There’s no money parked overseas. Last I talked to a wealth manager friend people were cashing out of airbnbs as investments.

“There’s no money parked overseas.”

Are you serious? Ireland. Luxembourg. Gulf. How many liberal upper-middle class liberal Americans have moved abroad over Trump 1.0+2.0? How many “digital nomads” and “crypto bros” are out there? How many Chinese are desperately trying to get assets out (see precious metal prices)? How many upper-income Europeans, Canadians, Australians are trying to get their assets to low-tax US destinations?

No money oversee? LMFAO. Lots of high net wealth individuals selling many assets around the world. Also they already have cash in many accounts. Lots of island nations with tremendous wealth, gee I wonder why…

High end and multi-family (revenue generating asset) are on sale, Wake up.

Another $30m home sold at Kukio yesterday. Corporate grifters seemed unconcerned.

….and a $9m front row lot at Kohanaiki today

File under “cash in those stock options!”

Tech firms are growing – but the use Claude / Codex. These tools dont require a house to stay

Yeah they require a nuclear power plant and to vaporize our rivers for cooling the GPU AI chips.

No biggie!

Just need to double YOUR power bill. Thanks citizen!!

You’ll take it like a good citizen.

If you can achieve that productivity enhancement with merely the cost of doubling US consumer electricity bills, this is a huge win-win.

The housing market it so overvalued much like everything else. Unfortunately, those with low mortgage rates who bought at the peaks are unwilling to take a real loss unless absolutely necessary. Those with equity are unwilling to sell at lower prices because they perceive their home as more valuable than it actually is. Then when you factor in higher property taxes, insurance, and HOA, smart buyers will just wait. Maybe there are those flush with AI money willing to buy, but they think the good times will never end. It’s going to take a recession with job losses to get this market moving.

Mortgage rates are in the normal range and look set to stay there. Perhaps house prices will follow…

The bubble remains, only very slightly deflated. Will not change until there is forced selling (job losses), we build more houses, or a demographic change. No relief in sight for popular-to-live-in areas.

Interest rates are rising for multiple reasons. It’s not just the Iran war, there’s the crisis in Private Credit, the excesses of the AI Boom coming home to roost, and of course the perpetual profligacy of Federal deficits.

Who wants to buy a new home anyway, when they are built so cheaply?! 😂😂😂😂😂😂

Is there any way, Wolf, that you can move my comment to the very top of the line? I came late to the party!

Only God can move your comment to the top. But I don’t think He has a history of doing that.

Alternatively you can reply to one the comments at the top.

But you’re not late to the party. I posted this article just a few hours ago.

“Only God can move your comment to the top. ”

Does God visit here and does God post,if so,I have been remiss in not visiting more!?

God,could you please convince home sellers see the light and drop their prices…..,thank you for your attention in this matter!

RP: NONENSE!!!

as a ”worker” at the lowest levels starting in the 1950s and continuing into the late ”oughts” when I became embarrasing to the young folx working in the field and was ”promoted” to the office to the extent of ”PM” ( paper monger!!) and so forth, I can testify with total confidence that today-s constructions, at ALL levels, including from basic residential to ”bestest” industrial and institutional are WAAAAY better in all structural and resistance to environmental challenges…

MOST relevant/important reason to support Wolf is his continuing efforts to stop the BS at all levels!!!

This is probably a larger conversation we should have else where, but to someone who doesn’t know much about home construction (me), what would you point to to show that these little boxes on a hilltop are better built? I hear the rhetoric all the time that these new houses are ‘cheap’, usually pointing at lazy craftsmanship if I had to do a word bubble.

Craftsmanship and build quality are very much dependent on the builder’s choices at the time of construction. I agree with VintageVNvet that average component quality is generally improving, but … there have clearly been time periods in our area (Northern California) where the builders tend to economize vs. others when they build solidly. So some older houses are in fact higher quality than some newer houses.

What I realized in buying dream house back in 2005 was that at that time our local market didn’t care about anything other than (a) square footage and (b) lot size.

So you could buy a higher quality house for the same price as a lower-quality one of the same square footage.

One of the houses we toured had dimmer switches that were so bad you nearly burned your hand touching the wall plate. Doors so flimsy that they echoed when you tapped them. And so on.

We bought a sturdy well-built place that was a bit older, but has stood the tests of time much better!

Vintage,I have personally seen as a most times remodel carpenter/fix a issue or two guy most newer homes in last 30 years not that good,not saying all but many build out developements for single family really kind of junk in comparison to older homes.

I will say higher spec houses and custom builds very nice for most part but maybe about 20% of the homes I am talking about,that said,this is in the north east.

I have a friend in Co. and the townhouses/condos there for last 20 years garbage in my opinion due to the sudden influx of west coasters and the boom in housing building,could live there and work till the day I die fixing bullshit that never should have happened.

My how the glory days from March 2020 through July 2022 have fizzled out. $FOMO to $YOLO. The moratorium on paying your mortgage and paying your student loans. Car manufacturers running out of inventory, prices skyrocketing, overbidding on homes sight unseen. PPP loans for politicians and criminals with LLC’s. Those were the good old days, paper towels and toilet tissue hoarding. Everyone bought a Peloton treadmill. I think we need the next man made crisis to start the printer again. Meanwhile there just seems to be no appetite in the housing market for the common folk. “You can’t Always get what you want” U might find “ Get what need” – Rolling Stones

> “I think we need the next man made crisis to start the printer again.”

There are at least two happening right now: The fast moving kind (Iran War) and the slow moving kind (climate change).

According to Trump it’s not a war it’s a ‘Military Operation.’ Sound familiar?

I thought it was an Excursion?

More like target practice. Attrition is boring and ugly, but the math is compelling…

We just got threatened to get a VA appraisal case out early before the 10 days required. The lender said the buyer would face a gigantic rate increase if we didn’t. So we had to stay up till 3AM in the morning and sent it out without any proof reading or spelling checks etc. It went out all right but upon further review, it looks like it was written by a 6th grader just learning to read and write. Lenders have lowered their standards to rock bottom just to make deal. We are looking at a repeat of 2007/2008.

“Given this period of increasing mortgage rates and diminishing refinance incentives, refinance applications decreased 15% as applications across all loan types declined,” said Joel Kan, MBA’s deputy chief economist.

Rising rates have “shaken buyer confidence,” Kara Ng, senior economist at Zillow Home Loans, said in a statement.

“The bulk of home activity typically happens between March and October,” Ng added. “The longer it takes for the rate shock to resolve, the more likely transactions would be delayed to next season, offering a repeat of 2025.”

FYI, we just got an appraisal using active listings as comps. SMH! Underwriting approved it.

I guess TARP didn’t “fix” appraisal fraud after all.

TNX has broken 4.4 today. Tomorrow looks to be interesting.

“The bulk of home activity typically happens between March and October,” Ng added. “The longer it takes for the rate shock to resolve, the more likely transactions would be delayed to next season, offering a repeat of 2025.”

May be a lot of astute and forced seller would reduce price. There is always buyer out there for the right price at a given rate.

Rates are historically normal ( 7% ) but homes are priced for 3% mortgage rates.

Rates are not the problem, but high home prices are.

Homes also have high carrying cost.

no doubt “climate change ” will be an in issue in about 10,000 years ( like its always been ) ! LOL

In my opinion, mortgage rates are too low because we shouldnt adding more US govt debt, which is already way too high and shouldnt have used money printing (and should never do QE again) to push down rates. I think that these suppressed rates have caused what many feel is the big long lasting issue of prices being too high. Houses could get back to reasonable prices and therefore sales could come back just fine if the govt would quit manipulating rates. And thats also why property tax, home insurance, HOA fees, etc. have all gone way up. And this mortgage rate manipulation is done by both the major political parties. Why keep voting for them if they never change these bad policies hurting the country? I think part of the reason is a lot of people arent feeling the damage being done because its being temporarily hidden by massive deficit spending, but that can’t continue forever. And there IS an alternative that has been on the ballot a long time and will be again for midterms, Libertarian, the only choice for balanced budget. Unfortunately might take even more inflation for people to start feeling it enough to start seeing through the fake culture war propaganda and question what *both* major parties (who both appoint the fed, which should be abolished for their part in enabling the massive debt and devaluing the dollar) are doing.