QE hangover a little less atrocious after years of QT and lower interest rates.

By Wolf Richter for WOLF STREET.

The Fed disclosed in its audited annual financial report today that its results in 2025 were less atrocious than in 2024, which had been less atrocious than peak-atrociousness in 2023 when the hangover from its prior monetary policies of ultra-low interest rates and QE had set in.

This is the consolidated report of the Federal Reserve System consisting of the Federal Reserve Board of Governors – a self-funded federal agency whose governors and chair are nominated by the President and confirmed by the Senate – and the 12 regional Federal Reserve Banks, such as the New York Fed, the San Francisco Fed, the Boston Fed, the Dallas Fed, etc., which are private companies whose shares are held by the largest financial institutions in their districts. The financial report was audited by KPMG.

Today, the Fed disclosed two types of losses:

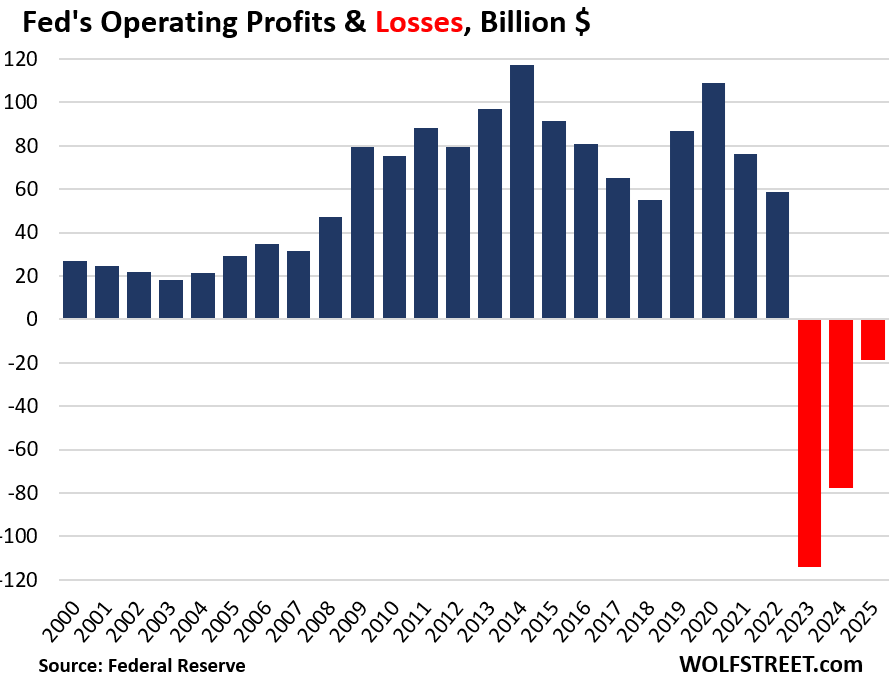

- An operating loss of $18.7 billion, compared to operating losses of $77.6 billion 2024, and $114 billion in 2023 (red columns in the chart).

- Cumulative “unrealized losses” of $844 billion at the end of 2025, an improvement from the $1.06 trillion at the end of 2024, on its holdings of Treasury securities and MBS.

What happens to the income and losses: The Fed creates its own money and therefore cannot become insolvent. But these losses matter to the Treasury Department – and the taxpayer.

The Fed has to remit nearly all of its operating income to the Treasury Department (similar to a 100% income tax). From 2008 through September 2022, the Fed remitted $1.36 trillion (blue columns in the chart above). At Treasury, these funds became part of the tax receipts. Those remittances stopped with operating losses in September 2022.

The Fed’s income:

- $155.3 billion interest income from its securities portfolio: $106.6 billion from Treasury securities and $48.0 billion from MBS, mostly purchased before 2022. The Fed’s QT reduced its holdings by $2.4 trillion from peak-balance-sheet in mid-2022.

- $3.1 billion in other income, including: $1.6 billion in “foreign currency translation gains”; $0.5 billion from services it provides to banks; and $0.9 billion from “reimbursable services” it provides to government agencies.

The Fed’s interest expenses: $167.4 billion, of which:

- $147.7 billion paid to banks on their Reserve Balances (cash they deposited in their accounts at the Fed, just under $3 trillion at the end of 2025)

- $19.7 billion paid to its counterparties, mostly money market funds, on their overnight reverse repurchase agreements (ON RRP) balances at the Fed, which dwindled to near $0 in 2025.

The interest rate that the Fed pays on reserve balances and the interest rate that the Fed pays ON RRPs are part of the Fed’s five policy rates, respectively 3.65% and 3.50% since the last rate cut in December.

The Fed started hiking its policy rates in March 2022, and on a quarterly basis started booking operating losses in Q4 2022, after years of huge gains. And these rate hikes continued through mid-2023, so its interest expenses ballooned with the rate hikes. In September 2024, the Fed started cutting its interest rates, and its interest expenses began to decline.

At the same time, the Fed began unwinding part of its Treasury and MBS holdings under its QT program. This liquidity drain had the effect of reducing reserve balances and ON RRPs. By the end of 2024, ON RRP balances were near $0, having dropped by over $2 trillion from their peak in 2021. By the end of 2025, reserve balances had fallen just below $3 trillion. And so the dollar amounts the Fed was paying interest on got smaller.

The rate cuts combined with the reduction in ON RRPs and reserve balances reduced the Fed’s interest expense to $167.4 billion in 2025, from the peak of $281 billion in 2023.

The Fed’s operating expenses: $9.8 billion, of which:

- $4.4 billion in salaries at the Federal Reserve Board of Governors and the 12 regional Federal Reserve Banks. By comparison: JP Morgan Chase compensation expenses: $54.5 billion. Truist Financial, a much smaller regional bank: $2.2 billion.

- $2.7 billion in operating expenses of the Federal Reserve Board of Governors including printing and managing the Federal Reserve Notes (the paper dollars)

- Smaller expense items include: $577 million for pension service costs; $352 million for occupancy; $286 million for equipment; $245 million for the Consumer Financial Protection Bureau, which is funded by the Fed.

The “unrealized losses”: $844 billion.

The Fed’s cumulative “unrealized losses” on its holdings of Treasury securities and MBS declined to $844 billion at the end of 2025, from $1.06 trillion at the end of 2024, and from $948 billion at the end of 2023.

Unrealized losses represent the theoretical losses the Fed would have incurred if it had sold all its $6.47 trillion in securities at market prices on December 31, 2025.

These cumulative unrealized losses are the difference between the securities’ amortized cost (which will be equal to face value by the time the security matures) and their market value at the end of the year:

- Securities at amortized cost: $6.47 trillion ($4.39 trillion of Treasuries, $2.08 trillion of MBS)

- Market value at year-end: $5.63 trillion

- Cumulative unrealized loss: $844 billion.

The Fed bought most of these securities years ago when yields were far lower, and therefore market prices a lot higher, than at year-end 2025. As yields on Treasury securities and MBS soared from very low levels starting in late 2020, their market values declined.

For example, at the low point in August 2020, the 10-year Treasury yield had dropped to a silly low of 0.5%, when the hype in the markets was that it would soon turn negative. In October 2023, the 10-year yield briefly kissed 5.0%. That was fun.

The Fed’s unrealized losses declined in 2025 largely because longer-term yields declined modestly between the end of 2024 and the end of 2025, which means that prices of those securities rose. For example, the 10-year Treasury yield declined to 4.18% at the end of 2025, from 4.55% at the end of 2024.

The Fed’s unrealized losses also declined because securities holders get paid face value when the securities mature, and as they get closer to their maturity date, their market value approaches face value, and the unrealized losses diminish and eventually vanish.

MBS are paid back mostly via passthrough principal payments at face value as the underlying mortgages are paid off when the home is sold or refinanced, and as regular mortgage principal payments are made. Even though QT stopped in November 2025, the Fed continues to shed its MBS at the pace of those passthrough principal payments and replaces them with Treasury bills.

Dividend paid: $1.69 billion, up from $1.62 billion in the prior year. Despite the losses, the Fed paid the statutory dividend, as required by the Federal Reserve Act (FRA), to the shareholders of the 12 Federal Reserve Banks, namely the largest financial institutions in their districts.

The largest shareholders got paid a rate equal to the 10-year Treasury yield at the auction just before the dividend payment was made, on the amount of their paid-in capital. Smaller shareholders got paid 6% on their paid-in capital. The dividend rate is capped at 6% for all shareholders, which kicks in when the 10-year Treasury yield rises above 6%, which used to be normal, but hasn’t happened in decades.

The annual report describes the formula laid out in the FRA for how the dividends are calculated.

“The FRA requires each Reserve Bank to pay each member bank an annual dividend based on the amount of the member bank’s paid-in capital stock and a rate determined by the member bank’s total consolidated assets. Member banks with total consolidated assets in excess of a threshold established in the FRA receive a dividend equal to the smaller of 6 percent or the rate equal to the high yield of the 10-year Treasury note auctioned at the last auction held prior to the payment of the dividend. Member banks with total consolidated assets equal to or less than the threshold receive a dividend of 6 percent. The threshold for total consolidated assets was $12.8 billion and $12.5 billion for the years ended December 31, 2025 and 2024, respectively.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Auction today of the five year treasury was almost 4%!

“ $577 million for pension service costs” – so Janet Yellens retirement? Does George Akerloff really need such a cushy home? lol just kidding around.

It’s neat how open all this info is, in light of well uhhh some people not being open about things as a strategy.

I can’t help being frustrated and sick to my stomach as a small business owner also with rental property and the government forced me to utilize and extend all my credit lines to survive while also telling my renters they didn’t have to pay rent. And these jackholes write their own rules and print their own money. The deck is stacked

“And these jackholes write their own rules and print their own money.”

That is basically the crux of the problem.

It would be one thing if government policy performance (over decades) somehow justified using the Fed as money print confiscator (of last/first resort) – the argument being that market failures/national emergencies justified occasional (read permanent) use of the Fed’s inherently questionable money print powers.

(For all the hind leg pontificating of both parties, the truth is that Fed money printing acts as a flat(ish) tax on every USD holder/saver in existence – that is its appeal to the political class and its toxic effect upon everyone else).

But when this sort of thing goes on for decades and DC fiscal course correction (either through making the hard political case for increased taxation or the seemingly inconceivable act of effectively policing political spending) becomes more and more of a distant/quasi-mythical memory, it becomes harder and harder (at this point, close to impossible) to say that the inherently inflationary act of using Fed money printing to substitute for remote fiscal discipline is not a sign of societal collapse.

The Paycheck Protection Program loans to business owners were forgiven.

That didn’t help a small landlord without employees.

Unless it was a Somalian Learing Center.

Sole proprietors and self-employed individuals were eligible. You didn’t have to have additional employees.

“Unless it was a Somalian Learing Center”

How you can tell that time, the internet, and sufficient ruin are (slowly, oh so slowly) changing America –

High profile *Dems* are proposing a “waste/fraud/abuse” commission – perhaps more than anything, that suggests that the “money print fix” string may be played out – the explicit inflationary impact finally having become too toxic in political impact.

Even if it is a charade…it is a charade that could have been retailed for 50+ years – and wasn’t.

But *now* it is.

The fact that it is today (50+ years after the underlying problem became serious) suggests that something fundamental may have changed.

Otherwise, even trial balloons like this never get launched.

Yep. Personally, I have found sorority girls to be the best tenants. They occasionally make frivolous call to squish a bug or change a light bulb, but their parent all co-sign and put up the deposits. Their rent is always on time and if they like your rentals they tell their friends and every year when the older girls (juniors and seniors) leave the sorority house you have more customers. Only had to deal with one eviction in the last ten years when I noticed some girls had been in a unit for 8 years. Apparently they were not very “academic” and had found a more lucrative means of making a living. The additional male traffic, new Mercedes, and occasional drug dealer tipped me off. We recorded all this with external cameras and gave the girls the opportunity to leave or face prosecution for their other behaviors…

There is nothing immoral in this:

“The Fed creates its own money and therefore cannot become insolvent. But these losses matter to the Treasury Department – and the taxpayer.”

One of the key points in the Communist Manifesto is the call for the centralization of credit in the hands of the state, which includes the establishment of a national bank with state capital and an exclusive monopoly.

Communism always ends with one dude offing all his competition.

Wasn’t it the Germans who put Lenin in place in the first place?

Hence China’s success.

All of the world’s 196 or so countries have central banks.

“All of the world’s 196 or so countries have central banks.”

But while that may speak to the Oneness of Man…what does it actually say about Man?

Theft is a universal reality as well – but I don’t know if that says anything good.

In the end, the money printer is the State’s non-pointy-guns final “march in” power – how somebody feels about that is going to reflect whether they view the State as the source or solution to societal toxicity.

By all means, move to China. Not sure I’d say that’s a great life for the average person. The path to their current state was also not an easy one. That government has executed many citizens, as typical of the communist governments. It’s all about balance IMO. Regardless, the best systems seem to reward good behavior and actually punish bad behavior or, at the very least, allow bad ideas, bad behavior, and bad management to FAIL.

2007/2008 should have been the wake-up call that America is now more communist than China…

Interesting times.

Also if you disagree or are of an ethnicity that even has a hint of resistance or tries maintain cultural heritage, you get a free all paid extended stay at one of their lovely camps where you will get a free hair cut, work experience, and education that will allow you to see the beauty of the CCP.

Sorry I forgot to add the fact that this is sarcasm

I admit that my understanding of all this is poor. However, when Wolf Richter writes about Fed debt, whether unrealized or not, in the high billions and low trillions it doesn’t give me great confidence in our future in the USA. I can imagine disaster looming if our government can’t stop throwing money all over the world and into their own pockets.

Same. With regard to throwing the money all over and impending disasters…

If the so-called hyperscalers are slow-crashing (e.g. Google is down 20% in two months), will the still spend $700 Billion on Nvidia chips over the next three years? Does that $700B even exist?

I am not trying to take one side or the other, but where do the building renovation costs fall in this? Are they “operating costs” that the Fed creates money to pay for?

I’m not an accountant, but I would think building renovation costs would be capitalized assets that would go under “Bank premises and equipment, net” on the balance sheet and then depreciation and maintenance costs in future years would be expenses on the income statement.

Any accountants here who can confirm how this works?

Renovating a building is an investment. In terms of accounting, that investment is added to an asset account (“capitalized”). In the Fed’s case, this asset account is called “Other Federal Reserve assets”; it contains $36 billion in assets, including all the land and buildings that the Federal Reserve Board of Governors and the 12 regional Federal Reserve Banks own, and including the Fed’s accounts receivables and accrued interest on its bond holdings.

Office buildings are depreciated to zero over a 39-year period. This depreciation enters into the expenses of the Fed. Land is not depreciated. So the renovations will show up as an expense when depreciation starts.

Would love to hear your analysis of primary dealer takedown rates, tails, and bid to cover ratios at recent treasury auctions.

Are treasury auctions really starting to fail….ie primary dealers taking a larger than normal percentage of treasuries and tails exceeding historical norms? If so, what does it portend?

Higher yields.

would be hreat to see % of dealer activity in auctions

Bit to cover (BTC) percentages are listed on the Treasury department’s data site. You can create a custom view that just shows the term, BTC, and other attributes in a chart on the site. and you can calculate takedown rates. But they don’t show you the “when-issued (WI) yield” which is a cleaner metric of demand (weak or strong) but only available via bloomberg and CME. The 2 year that Wolf mentioned and then the 5yr and 7yr in the days following all showed unexpected weak demand. Now today the 10 yr is spiking….it’s would be nice to see the WI on these things moving forward but que sera, sera.

We certainly seem to be heading towards higher rates and with all the rollover debt schedule in 2026 + new debt I think the Fed is going to have to get involved later this year with some QE (damn inflation) and save the economy….and they better make the QE they deliver the biggest we’ve ever seen!! Brace yourselves

I buy at auctions, and I watch them, and I’m cynical about them. Their sole purpose is to allow the government to borrow for as low a cost as possible. That has always been that way. The primary dealers’ job is to make that happen; they’re by design arm-twisted into making that happen.

So for example, the 2-year yesterday was offered at a too-low coupon (3.875%), and there was not a lot of demand at that coupon interest rate. There was demand at a higher yield, but then primary dealers had to step in to keep the yield from going there all the way. So in the end, the note, with a coupon interest rate of 3.875%, was sold at a discount (for 99.883 cents on the dollar) which brought the yield up to 3.936%.

If the government had offered the 2-year with a coupon interest rate of 4.0%, there would have been huge demand for it, and dealers wouldn’t have gotten hardly anything, and the note would have sold at a premium, which might have brought they yield to 3.95% or so. But the purpose is to sell this stuff at the lowest possible cost to the government. The purpose is NOT to give investors a good deal. And most investors that buy at auction know that’s how it is.

The whole setup, including arm-twisting primary dealers into buying at a yield that is too low for where demand is, is designed to push down yields and let the government borrow at the lowest cost possible. From a taxpayer’s point of view, that’s good. From an investor’s point of view, it’s not ideal.

Mr Wolf

I was surprised to see the Federal Reserve board designated a Federal agency

As for the Fed paying 6% to smaller banks on their stock, curious the Fed never cuts that rate

It seems the Feds foray into the long end was a new and expensive exercise

Your comments on banking regulations being adjusted/slackend to allow banks to compete with private lending operations…as banks still have no required reserves. Dangerous?

Thanks

The dividend and the formula of how it is paid was enshrined by Congress into law (the Federal Reserve Act), and the Fed cannot change anything. To change it, you need to lobby Congress to amend the FRA.

Bank regulations are so vast and so complex and so difficult to deal with that they give everyone a headache. There are a lot of unintended consequences in those regulations, including that a lot of lending was pushed from highly regulated banks to unregulated nonbanks that acted like cowboys and became what is now in the headlines, Private Credit. In theory, the regulations that caused this should probably be re-looked at. I agree with much.

$147.7 billion paid to banks not to lend. What a stupid credit control device.

So I read an article this morning that was titled something like “Retail firms warning of price hikes if Iran war continues,” and had a realization. Often whether or not events like the Iran war, or tariffs, actually SHOULD have an effect on pricing, businesses set the seeds for it before the hikes actually occur. What they’re doing is trying to get the inflationary mindset in motion before the hikes, so when the hikes happen, people just sigh, say “Ehh, it’s because of X factor, what are you gonna do,” and just pay it.

OECD just stated they expect US inflation rate to be 4.2% this year.

You can find the quotes on CNBC website, up top and dead center.

Of course some here will dispute their forecast as it does not fit into their narrative.

That “up to” inflation projection of 4.2% for the US and 4.0% for the G20 (includes Canada) seems possible to me. But the OECD has a horrid record with its projections.

Correct. They’re making the announcements in advance so that 1. all retailers follow and do the same thing without being tried for collusion; and 2. to manipulate the consumers into thinking that they will just have to pay higher prices, rather than fighting price increases by shopping around, or not buying, or buying less.

every single time a CEO opens their mouth, it’s to manipulate someone (investors, government, consumers, other businesses, etc.)

The great German poet and playwright Bertolt Brecht would have agreed and once said it was “easier to rob by setting up a bank than by holding up (one).”

As Willie Sutton said: his reason for robbing banks is ‘That’s where the money is’.

Thomas Jefferson’s my favorite: “I sincerely believe the banking institutions having the issuing power of money are more dangerous to liberty than standing armies.”

Stock indexes are down as oil and bond yields climb

SPX -1.11% DJIA -0.75% COMP -1.49% CL00 +5.33%

BX:TMUBMUSD10Y 4.406%