Companies, seeing Higher-for-Longer, take advantage of it to lock in historically narrow spreads and still low yields.

By Wolf Richter for WOLF STREET.

The feverish demand for US corporate bonds, particularly high-yield bonds has been flabbergasting, a sign that financial conditions in most parts of the economy, except in commercial real estate, have become ultra-loose despite the Fed’s efforts to tighten financial conditions.

This week, junk-rated companies have sold over $14 billion in new bonds, the most since late 2021, according to LSEG and FT calculations.

“Bankers and investors highlighted a growing conviction in markets that US interest rates are unlikely to fall steeply this year, prompting companies to meet their funding needs now rather than risking higher borrowing costs while waiting for another opportunity,” the FT explained.

In 2024 through April – so not including the surge in May so far – issuance of corporate bonds of all grades soared by 38% year-over-year, to $752 billion, according to industry association SIFMA.

Of those $752 billion in newly issued bonds this year through April, junk bond issuance nearly doubled. Junk bonds are those with credit ratings of BB+ and below (here’s our corporate bond ratings cheat sheet):

- Investment grade: $635 billion, +31% year-over-year

- Junk bonds: $117 billion, +95% year-over-year.

Hopes for Fed rate cuts and even lower yields are being skuttled, in favor of locking in the historically narrow spreads and still relatively low yields driven by this feverish demand from investors for these securities.

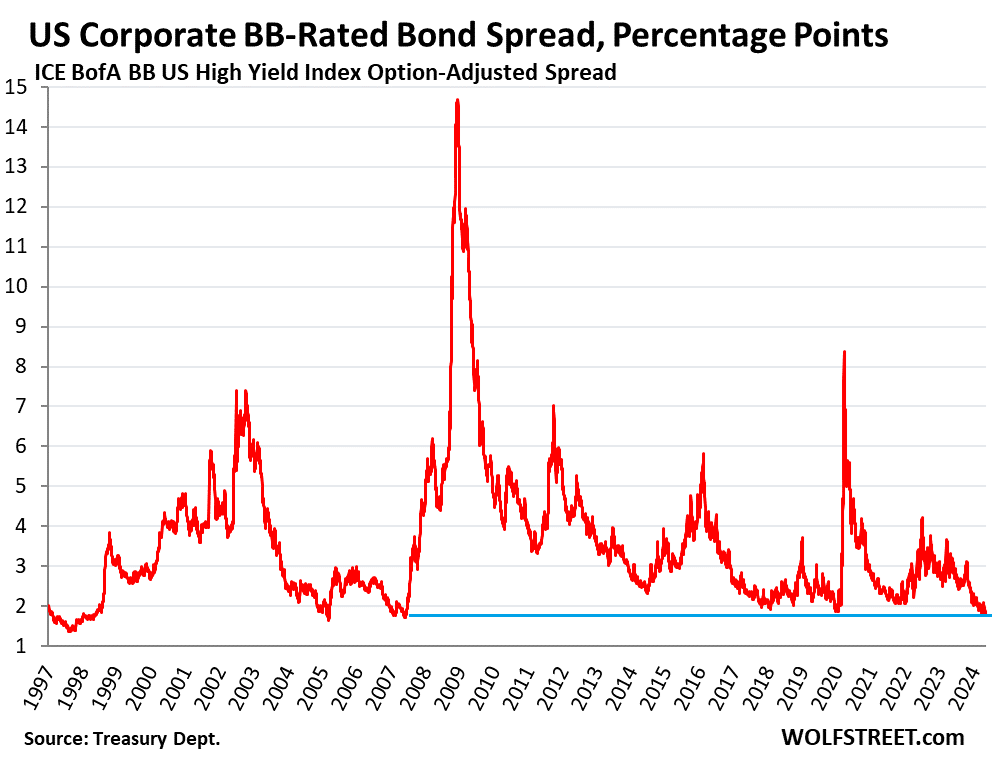

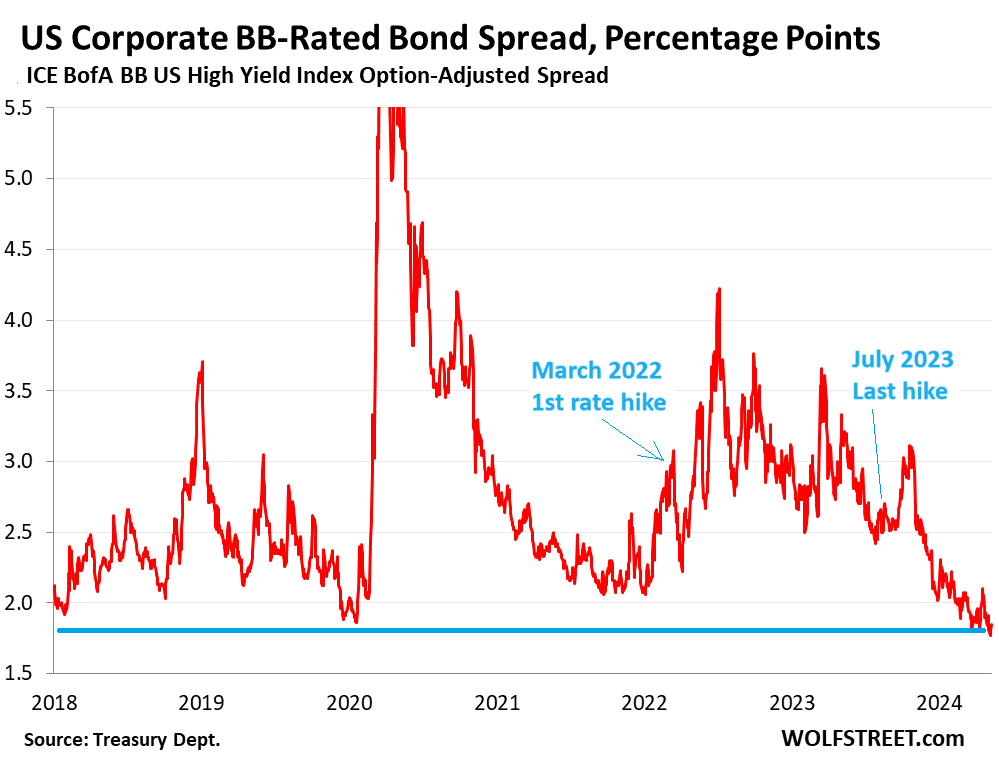

The Fed’s policy rates have remained unchanged at 5.5% at the upper end of the range since July 2023. But financial conditions have loosened since November, and spreads between junk-rated bonds and Treasury securities have narrowed to historically low levels, meaning that investors are being compensated by a historically small amount for the big extra credit risks they’re so eager to take.

The spread of BB-rated corporate bonds to Treasury securities is now down to just 1.85 percentage points. While it has widened a hair over the past six days or so, those spreads are the narrowest since 2007, on the eve of the Financial Crisis:

When the Fed “tightens” by raising interest rates, and by running down its balance sheet via QT, $1.6 trillion in QT so far, it means to tighten financial conditions, which includes widening the spread between Treasury securities and securities with more risk. And that worked at first, and spreads widened substantially, reaching 4.2 percentage points in July 2022.

But then the “Powell was dovish” rhetoric from Wall Street took over, and at each rate-hike meeting – by 75 basis points, no problem – “Powell was dovish.” This narrative took on a whole new magnitude when the Fed suggested in December 2023 that there would be a few rate cuts in 2024, always caveated with “if inflation continued to decline toward the 2% target,” with the median projection in the “dot plot” seeing three cuts. It set off Rate-Cut Mania; markets were suddenly projecting six or seven cuts in 2024.

All this has been walked back now, after three months of nasty inflation data, and the term “rate hike” suddenly started cropping up all over the place. But the spreads haven’t widened more than a hair.

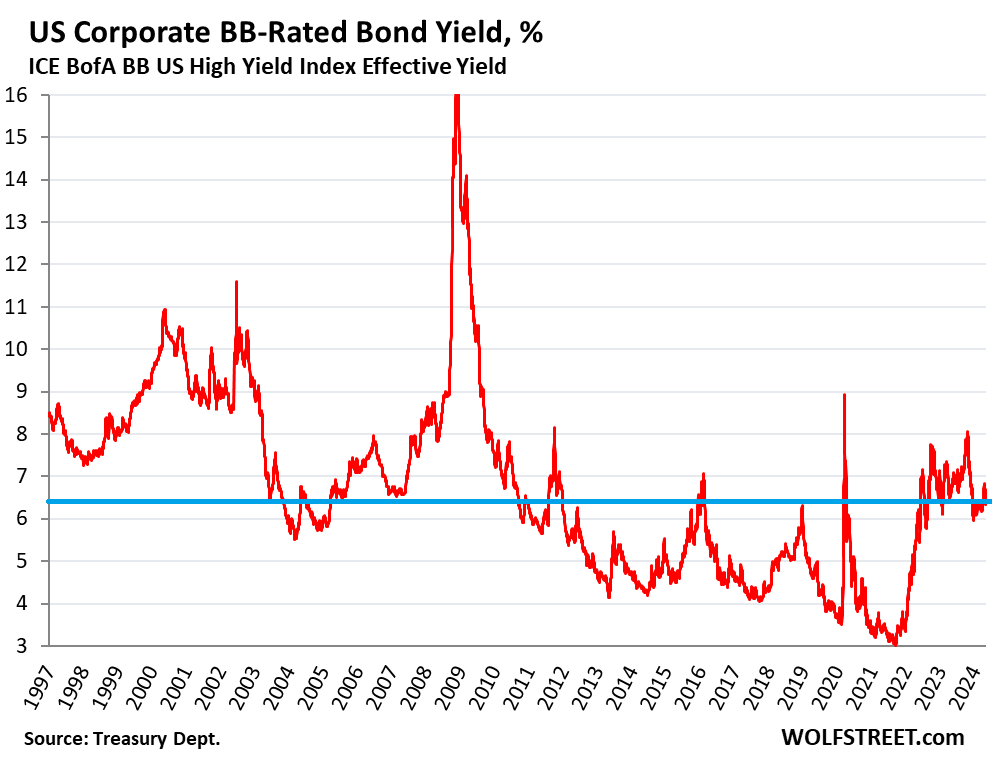

This had the effect – one of the reasons why companies are rushing to sell those bonds – that the average BB-rate bond yields 6.4%, same as in June 2022, at the early phases of the rate-hike cycle.

Back in August 2021, just before the Fed started talking about rate hikes, the BB yield was around 3.2%. By June 2022, when the Fed hiked to 1.75% at the top end, the BB yield rose to 6.4%, and now, with the Fed’s policy rate at 5.5% at the top end, the BB yield is again 6.4%.

So the Fed has hiked by 5.25 percentage points since August 2021, and BB-yields have risen by only 3.2 percentage points. This produces a yield that is low compared to pre-QE times:

So that’s a deal for the junk-rated companies, and they’re jumping all over it, and they’re issuing these bonds hand-over-fist, having largely given up trying to wait for rate cuts. And the investment-grade issuers are doing the same thing. Their bet is that yields will stay higher for longer, and they’re taking advantage of the mania now.

Demand is huge because buyers are betting that the Fed will soon cut rates massively and bring yields back down, and that they will have a winner on their hands by locking in today’s yields, and then selling those bonds in the future at a higher price after yields have dropped back down. That’s the buyers’ bet.

They are accepting historically low compensation to take the associated credit risks. They’re back in la-la-land, another sign of just how loose financial conditions have become. And companies are taking advantage of it.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I know i am seeing what i want, but in the 1990s the fed was still known for fighting inflation and financial condtions respected that belief. Fed has made life much harder on themselves

“Fed has made life much harder on themselves”

Rest assured, James, they are doing just fine.

I think the correct statement should be: ““Fed has made life much harder on Americans””

in mid 90’s we took out our 1st mortgage at 7 7/8%

just paid it off

price was $83k, today same property(due to fed devaluation of fiat $dollar) is more like $283k

rents were $400 now $1,200

that’s how you keep up with inflation(I mean devaluation)

“Inflation hasn’t ruined everything. A dime can still be used as a screwdriver.” ~ H. Jackson Brown, Jr.

While I agree with your assessment I would point out that I think the message is a recipe for disaster.

Business, as we know it, a positive, cannot survive the corruption.

First.

Best financial blog on the internet.

I do think things are eventually going to go to hell in a handbasket but probably longer than many of the bears think.

Thanks Wolf.

The absurdity of the residual monetarist’s folly lingers, as hangovers have a tendency too do. What just last night seemed like a good idea, hell fund the speculate market at the same rate as the US Treasury pays for them.

Seems that risk aversion is being sold cheap. There are several asset bubbles that have yet to decline to the point that my angry children can afford it.

Risk has a way of pooling and the unfolding in some nefarious new way that the existing tools struggle with, also blindsiding many punters all at once. Fortunes will be made by a few, as last time. The usual suspects will be bailed out. The rest of us are the payers for insurance for the top dogs.

– The High Yield ETF called HYG has also been rising “through the roof” since november 2023. NOT a good sign !!!!

– The ratio between the Dow Jones and the Dow Transports (think: Dow Theory) has risine since say august of 2023. Also NOT a good sign.

If what you say is true, that the HYG has been rising. I submit the reason is that the excess liquidity provided by the Federal Reserve is being used as the marginal buyer which determines the market price.

The evidence is that high risk investments are selling like hot cakes.

“The High Yield ETF called HYG has also been rising “through the roof” since november 2023.”

people need to look at a long-term chart of these instruments. There’s nothing “through the roof” – it’s through the floor:

In 2007, HYG was $105. Then it plunged (GFC), recovered partially but not all, then plunged again in 2016 (oil bust), then recovered partially but not all, then it plunged again (pandemic), recovered, and then it plunged again.

In November it was at $71, and now it’s at $76.90, and in 2007, it was $105. That thing continues to lose value, with some rallies in between.

I believe that’s based on price v based on total return where the result is quite high relative to 2007. On StockCharts, the difference is between measuring by ticker _HYG AND HYG. Which is the best measure of comparability ?

Price performance for _HYG = -27% and for HYG = +112%.

True. But something that pays a high dividend and loses in principal value just eats itself up. Yield now is 5.95%. T-bill yield now is 5.3% to 5.5%. T-bills don’t lose principal value.

Wolf: $0.75T in 4 months or $3T for whole year. The FED must be aware of these excesses but still came out and said, QT will be reduced. They also keep assuring that we will see rate cuts late this yeat. Wtf? If they cannot do QT at a faster rate when the economy is great and the financialconditionis loose, when can they do it?

I think there is a big arbitrage going on. Even at 5 to 6%, most companies use that cash to buy back their stocks (Apple withbthe highest buyback in their history). The peasants bid up the stock, but the dilution through SBC is ignored. Why shouldn’t they if their stocks go up 25% every year (for fun, I visit stockwits dot com to read comments on Meme stocks. Their was euphoria in SMCI, the computer case or box maker about making a killing in zero day options. Now the song has changed to about market makers fleecing the retail crowd).

I wonder if we are heading in the same path as 1920’s that lead to depression.

“They also keep assuring that we will see rate cuts late this year.”

That’s your homemade nonsense. Or maybe you’re drinking someone’s Kool-Aide. No one at the Fed, not even the janitor, is “assuring” anyone that there will be rate cuts this year.

What they all say in unison is: “if inflation continues to drop sustainably toward our 2% goal, we may make policy a little less restrictive,” which is of course precisely what inflation has NOT been doing. Now they’re talking about maybe no rate cuts, or maybe even a hike, or maybe a cut if inflation continues to drop sustainably toward out 2% goal.

There’s an interesting thesis – not widely accepted on the street / market consensus – but hinted at by Wolf here and that is that on the one hand rates are “high” and that should dampen economic activity but actually not happening (other than the most rate sensitive sector(s) like real estate) and on the other hand maybe that very policy rate is actually driving inflation itself through consumer spending. You have trillions of dollars in savings now earning 5%+ that more likely than not is getting spent. In tandem you have fiscal spending from the gov acting to accelerate economic activity. In this reality where would the FFR need to be to create tightness in financial conditions? Certainly higher than 5.3 but 5.55? 5.8? And is the FED, politics considered, actually willing to take it there? It seems much more likely that they’ll tolerate inflation of 3-3.5% than risk spreads blowing out. But if inflation spikes further than it’ll get interesting once more.

It appears that during this period of fiscal dominance and deficit spending, the Feds ability to curb inflation is compromised.

I like that understatement……the Fed can’t do much about the REAL problem…..

EXTREME WEALTH INEQUALITY and the fiscal and other “laws” that drive and increase it.

Not that it matters, the planet is likely going to be trashed for large land mammals, especially Hominids.

Dropping QT from 60 billion to 25 billion loosened conditions and brought back animal spirits. The Fed sent the wrong message. The Markets now feel that Fed has our back.

“Dropping QT from 60 billion to 25 billion loosened conditions and brought back animal spirits.”

BS.

1. They didn’t drop “QT from 60 billion to 25 billion”– they dropped the cap of the Treasury roll-off from $60 billion to $25 billion. But the MBS roll-off continues as before, capped at $35 billion. The current pace is around $17 billion a month, and when the housing market unfreezes, this will go toward $35 billion a month. In addition, the BTFP will go to zero by March. Last week, another $10 billion dropped off. $120 billion more to go in 10 months. That will come out of reserves and is straight QT. In addition, there are other things that will come off, for a total of AT LEAST $630 billion by end of May 2025, for an average of AT LEAST $52 billion a month. Add another $10-$25 billion a month in MBS roll-off when the housing market unfreezes, for about $60-$75 billion a month, as explained here at the bottom:

https://wolfstreet.com/2024/05/02/fed-balance-sheet-qt-1-60-trillion-from-peak-to-7-36-trillion-lowest-since-december-2020/

2. Doing QT more slowly is NOT loosening anything; it’s tightening more slowly. Saying otherwise is a manipulative lie.

I dunno, like Wolf said the MBS roll-off is still happening at same pace and it was that portion of the QE that was biggest culprit, in fueling the housing bubble and rest of the Everything Bubble. It was borderline criminally stupid to of done that much QE esp the MBS purchases, a big factor in locking out a generation of Americans from realistic, affordable home ownership and a devastating hit to the country.

But that’s at least one thing JPow does seem to realize seriously and is correcting that mistake by making sure the MBS’s continue to get off the balance sheet like before. As for the QT slow-down itself, it’s still happening while the short-term rates from the Fed stay high, he’s maybe just trying to avoid a 2018 repeat and a disaster forcing a reversal. If anything seems like a way make sure QT keeps going.

“Ultra-loose financial conditions”

Why in the F**K is the FED even TALKING about rate cuts amidst “ultra-loose financial conditions,” in the midst of the biggest everything bubble in the history of mankind, and a resurgence in inflation? That’s the problem, Wolf.

When inflation was raging out of control, they were jabbering about “not even thinking about thinking about raising rates,” and yet when they haven’t even brought inflation down to their target (which is a scam in and of itself), they’re already talking about lower rates.

Everybody sees this. The FED wants bubbles, they want inflation, they want all of this under the guise of “trying to help.” These people are the scourge of society.

Look, inflation has come down a lot and has been well below their policy rates. So back last fall, when inflation looked like it was going even lower, it made sense to talk about rate cuts. If inflation is 2%, you don’t need 5.5% policy rates. But they had two issues: Wall Street hype spun that conversation into Rate Cut Mania; and inflation reared its ugly head again. So far they have not cut. And the Fed has changed its tune. But Wall Street is deaf on that ear.

Since 2008, the Fed has ushered in a semi-MMT-based approach to managing the economy. Unfortunately, they can’t raise taxes to suck liquidity out of the markets. But they can pump QE in bad times, saturating the market with liquidity. Then during periods when the Fed is not purchasing treasuries, this ensures there’ sufficient demand to ensure yields don’t spike. It’s that simple.

In doing so, they’re manipulating financial markets, housing, debt issuance & most importantly creating winners & losers by fueling massive asset bubbles. Personally, I don’t think the Fed should be allowed to purchase treasuries with maturities longer than 7 years or MBS. The long-term bond markets should be free from Fed intervention. What the Fed has done is jumped on the we’ll backstop everything train which is what Congress is doing.

Together, they are ruining America’s financial future which is something we both can agree on. JPowell just needs to come out and admit that, outside of a recession, core PCE inflation isn’t returning to 2% anytime soon. This month-to-month, data driven analysis is not working. Why? Because they’re simply unwilling to raise rates. There should have been a 25-basis point raise in March with Fed talk supporting at least one more increase this year, if needed.

What is needed is a recession with about 5.5% unemployment for about 12 months. The stock market needs to drop about 35% and housing needs to drop at least 20% on top of any new homes price declines over the last 12 months. And the FFR shouldn’t drop below 2.5%. And, most importantly, JPowell needs to put on his big boy pants and tell Congress that it needs to get it’s out of control spending under control.

Depth Charge,

You always seem so angry. I can understand this sincerely since you obviously missed out on the free money binge.

The question is, are you positioning yourself to make out like a bandit on the next free money Fed handout or are you positioning yourself to thrive in higher-for longer? As long as you’re not feeling sorry for yourself and just spending it all using the past boat missed as an excuse not to save and invest. Hopefully your day will come (but it can’t come if the latter of the three scenarios is the one you choose).

Replying to MussSyke…

Made out big for last 10 years because of feds policies but I am angrier than DC for obvious reasons you may not understand.

But with corporate margins and profits and stock prices up, 5%, 6%, even 7% or 8% is still cheap money. It’s not as cheap as 3 or 4%, but if Im clearing 20%+, I’ll borrow at 6% all day long, especially to buy stock AND get myself big stock performance bonuses

I take exception to your characterization of SMCI as a “computer case or box maker.” The stock is overvalued but Super Micro motherboards are the best I have used over the past 30 years.

Same stuff in European markets.

This is a weird bet : if we have disinflation you won’t get a spread contraction, they are already tight. so you will gain barely the same with risk free govies, maybe 1.5% for holding high yield assuming you won’t get any default/restructuring event.

All other scénarii you lose.

It’s the same geniuses who were buying long term treasures at 0.5-1% yield. Most likely Ivy league graduates.

May be it would be far better if the Fed keeps its mouth shut as to what it is going to do. Instead of throwing juicy bones at Wall Street, knowing that it is eager to look at only the juicy part ( rate cut) ignoring the tough end ( if inflation drops sustainably to 2%). Announce whatever it wants to announce, clear the building, take the next flight out.

I agree. Every time Powell gives a press conference the stock market rallies for weeks. It must be a coded message sent out promising that their fortunes will be defended and preserved.

Government policy.

Hi Wolf, do you the percentage of BB-rated bonds that defaulted during the Financial Crisis, say from 2007 until 2014?

High yield default rates by year (Fitch):

2007: 0.5%

2008: 6.8%

2009: 13.7%

2010: 1.3%

recovery rates of defaulted bonds over those years ranged from 34% in 2008 to 57% in 2010.

I wonder how big the HY universe is, in terms of number of issuing parent companies (“issuer” count might be a little hinky since multiple subsidiaries, ringfenced within a single company, might all issue their own debt).

My guess is somewhere in the neighborhood of 1100 just among the publicly traded companies (a number which itself has gone way, way down since 2000).

But that is just a guess.

Then there are the privately held companies issuing junk debt (a smaller universe because there is no tradable equity to prod off the gangplank before even the junk bonds in a bankruptcy…but plenty of privates do issue junk debt).

And there are even some muni special issuers with junk debt.

*And*…we are not even counting the large group of crypto BB companies rated as BBB thanks to rating company generosity (and payola). That BBB versus BB is a big deal distinction since it determines who is allowed to *buy* such debt…significantly affecting required interest rates.

While I agree with your premise that the current market environment seems to be speculative, historically been a bad time too invest in a stock market promising to pay off in 25 years.

Those recovery rates seem pretty high, given that the average unsecured recovery in bankruptcy is around 5%. But then, the universe of high yield may be of higher quality than the general universe which includes a lot of small companies where the recovery rate will be zero.

Also, do you have a sense of the proportion of “covenant lite” loans now vs in the runup to 2008? Covenant lite loans will give the borrowers more of a chance to blow through all of the cash before they formally default.

Much of the defaulted debt is secured in some form. With first lien bonds, for example, the recovery can be close to 100%.

If a company only has unsecured debt, it will have lots of collateral left to pledge and will likely be able to sell secured bonds to raise funds and avoid bankruptcy. It’s when companies run out of collateral that push can come to shove.

If I remember right, the company whose unsecured bonds you bought and held through bankruptcy also had secured debt, and secured loan holders and noteholders got the farm, and there wasn’t much left over for the unsecured noteholders.

Pretty wild stuff with the lack of compensation for the added risk. Another example of animal spirits running wild…. However

Jnk etf looks to be headed down so possibly this trend is nearing an end 🤞

Agreed…getting just 1-2% more for a junk bond vs. A guaranteed repayment Treasury is just nuts (what ZIRP wrought).

And that is reflected in the rapid, huge rate spikes that occur when there is some question about whether or not Mother Fed will print the next trillion to delay the consequences of having printed the previous trillions…

Those spikes are closer to the un-Fed-inflected truth about junk companies than those multi year stretches of 1-2% spreads.

There are a ton of public companies on Fed life support (unZIRP’ed but still artificial rates) notwithstanding the seeming calm and laughable spreads. Plenty of companies are going BK (retailers most publicly) even with the tiny spreads.

UnZIRP got ’em, even though the spreads haven’t expanded yet.

The spreads are as if the riskiest scheme is a sure thing.

Here in the land of dreams.

What to buy when my dreams come true.

First, a trip to the “junk” yard. Some of the best stuff at a discount rate can be found.

Looking under an old torn couch I find what I’m looking for, an old tarnish lamp. Back at home I grab some polish and start to shine my small lamp. Surly theirs a genie in this one.

I bought shock absorbers for my 1960 chev bel aire in the local junk yard an automobile that I had acquired as the verdict in which said vehicle, driven by someone who was proven to be driving while intoxicated, lost the only thing he owned. The 1960 chev bel aire, too my brother. It was the first of several vehicles I bought from my brother including the 68 toyota adorned with bullet holes.

I’ve been wondering for a few months when the cash on companies’ balance sheets would start to create meaningful interest. But if they are borrowing more money now at the rates, then the answer might be never

It’s not the same companies. There are cash-rich companies, and they’re highly rated because they have lots of cash, and that cash is generating interest at today’s T-bill rates or higher. Some like Apple, also have lots of debt, but that debt was issued years ago at very low interest rates, while the investments are in shorter-term securities with 5%-plus yields, so it’s a net benefit. And long-term rates are still lower than short-term rates.

Then there are companies that are junk-rated, and by definition, they have lots of debt and don’t have much cash, and most are cash-flow negative. So they’re just making higher interest payments on their newly issued debt, and they’re not getting much interest income because they have little cash.

In general, I blame Baby Boomers and their excess cash, chasing yields and not understanding what they’re doing.

As Wolf mentioned, investors aren’t being compensated for taking risk, but there’s still this tsunami of buyers that are like drunk sailors in casinos, willing to bet on almost anything labeled risky debt.

Early last year I had been entertained by Hugh Henry, who was pushing his TLT bet, but it never made sense. He’s recently admitted that he got that wrong, but he also uses options and can wait years for his initial bets to pan out.

Additionally, tons of banks like SVB got Treasury bond duration totally wrong a few years back — but, same story as above, bad bets can take years to turn around — duration risk is a huge factor for anything.

Junk bonds are an insane part of casino mentality and there’s an insane amount of people chasing the illusion of yield — and not being compensated is utterly ridiculous.

Here’s a blurb that adds background in terms of the insane demand for “trading sardines”:

“According to data by the Institute of International Finance (IIF) and S&P Global, the debt of non-financial corporations has increased from 75% of total global gross domestic product (GDP) in 2007 to 98% last year (which along with the debt of governments, households and financial corporation brings the total aggregate worldwide debt to a record $300 trillion, a 349% leverage on the gross domestic product).”

“In general, I blame Baby Boomers and their excess cash, chasing yields and not understanding what they’re doing.”

Boomer bashing by ignoramuses never ends???? If the sun doesn’t shine, it’s the boomers’ fault???

Not many retail investors – boomers or otherwise – buy junk bonds. High-yield is owned mostly by institutional investors, such as insurance companies, pension funds, bond funds, PE firms, hedge funds, by companies, by the professionally managed family offices of billionaires, etc. If retail investors want to take risks, they buy stocks.

Sure, any idiot can buy stock-market traded junk-bond ETFs, and young stock-market jockeys are big fans of them because it’s just a trade, and they never look at a long-term chart to see the long-term decline of the price. JNK was 140 in 2007 and now it’s at 94, despite the recent rally. It goes down slowly, then plunges, then recovers partially but not all the way, and then continues to go down slowly, then plunges, then recovers partially, etc. So it’s a trading instrument, after it plunges. If you use it as buy-and-hold, you will watch your money vanish slowly and then suddenly before your eyes.

For retail investors, high-yield bonds are not that easy to buy outright in a targeted way and even harder to sell (and you’ll get ripped off) because they’re fairly illiquid. So if you’re looking to buy BB-rated bonds from a specific company because you have done your homework and think the company will be fine, you might not be able to buy any of them because the fixed-income desk at your broker can’t find those bonds for sale. But you might be able to buy some other junk-rated bonds that your broker shows as for sale. So some people dabble in this stuff, but there is no mass-buying by retail investors to drive down yields.

Exactly, exactly, exactly.

As a Boomer buying bonds since 1999 I have never touched junk bonds and as a retiree I am not rich by any stretch of my imagination having lost a bunch during the GFC and aged out of the workforce in 2016 when I hit 60. Poor me nope I manage and love the current 5 percent no risk yield for the first time in 15 plus years

Sure, the boomers are victims of their environment just like the current young people. IMO, the 60 70 80 90 2000 etc were not particularly pleasant from the perspective that us young people had a leg up. Unemployment was rampant.

Housing was unaffordable because the mortgage interest rate was greater than 14 pct.

…irrespective of age, one can never really know that which they have not experienced themselves…(…that won’t stop us from trying to convey it, anyway…).

may we all find a better day.

If the human race survives, future men will, I suspect, look back on our enlightened epoch as a veritable age of Darkness. They will presumably be able to savour the irony of the situation with more amusement than we can extract from it. The laugh’s on us. They will see that what we call “schizophrenia” was one of the forms in which, often through quite ordinary people, the light began to break through the cracks in our all-too-closed minds.

-R.D. Laing

The truly, very over-leveraged companies are certain, foreign EV makers, already stuck with tens of thousands of poorly-made, hazardous, EV vehicles that they will never sell, who were going to go broke (those not secretly,broke already) no matter how many more ultra low interest loans and subsidies their presitator gave them now, reportedly, facing increased, 100%+ US tariffs, with the EU about to take similar action. I.e., RIP, BYD. LOL

You gotta be a moron to buy junk bonds at this juncture. Being invested in a high yield mutual fund because you are desperate for income is a risky strategy, paying for the capital losses while enjoying the cessation of dividends during bankruptcy proceedings.

Lol your post is pure delusion, BYD is one of the most effectively run companies in the world right now and far better than US companies like Intel, Boeing and whole lot of others (and more and more looking like Tesla itself) that focus on stock buy-backs, gimmicks and hype instead of real productivity or quality improvements. The 100 percent tariff in the US is pure political gimmicks too, BYD has already said it has no interest entering the US market anyway because of Americans preference for huge cars and light trucks–the tariff is just a way of sounding protectionist while not actually doing anything (and not risking more inflation which would be disaster for Americans) and the EU isn’t going to tariff them like that because then VW, BMW and the others would lose their biggest market in turn, So, not going to happen.

It’s cars have been recognized high quality and all pass the stringent EU safety tests with some of the best marks of any maker, there’s a good reason it dominates the EV market and is growing extremely fast with a focus on emerging ones. Lots of cash and little debt. Some wishful thinking in several of these posts but yours here takes the cake, and what does this even have to do with the topic of junk bonds?

BYD just announced plans to build a plant in Mexico, specifically to establish an export hub to the US. So your post is BS.

Wolf doesn’t like links but you can look it up yourself- the story is on Reuters from February 14th.

BYD has been assembling and selling electric buses in the US for years.

Actually, BYD issued bonds which will later go to junk ratings, gets massive subsidies from CCP, does have the “most fires” per wapcar dot my 4/8/24, started in late 2023 to ship dolphin ev to North America, and per the Drive,,the US is pressuring Mexico to exclude EV makers from China from sweet deals. The inadequate, energy infrastructure to make a majority of cars or even a large portion electric in most countries south of Texas is left as homework for discerning readers.

CCP ev makers are _____ed. Hope you do not own their securities. LOL I predicted Evergrande, Country garden, and China’s implosions long ago.

Thank you Wolf for not using the words “investing” and “junk” in the same sentence.

Can history repeat it’s self? Sitting on the Budget And Finance Committee at my local association I saw first hand how this ends like it did in 2008. The wealth manager gave us the bad news as Lehman Brothers collapsed. “Your Investment Grade Bonds have been frozen”. It took around a year for the bonds to free up so we could get out. We had to wait and got full payment but next time we may not be that lucky.

“The spread of BB-rated corporate bonds to Treasury securities is now down to just 1.85 percentage points. While it has widened a hair over the past six days or so, those spreads are the narrowest since 2007, on the eve of the Financial Crisis:“

This paragraph says a lot.

Is there anything to read into the fact prime mortgage rates are the same as junk bonds? Investors see the most qualified borrowers of residential RE as being just as risky as junk companies?

I don’t think this is a valid comparison. Different kinds of investors buy corporate bonds vs mortgages.

Usually 30yrfm are ~3% above the 10-year treasury. The fact that HY is hovering around the same is a coincidence.

Actually, all one has to do is look at the interest rate structure and say too them selves, this doesn’t make sense. By calculation, in order for the 10 year average 4.3 pct would require several years of QE level interest rate suppression.

The inflationary economy carves it’s own future without regard to the past.

As someone who owns a few BB and BB+ bonds, my thesis is NOT rate cuts. Rather, I specifically bought ultra-short (<18 months) maturities based on the idea that recession and defaults are unlikely within that timeframe.

These bonds are yielding between 6.5 and 8% factoring in my buy-in price. With the economy humming along just fine, why not? They're still safer than buying those same companies' stocks.

Good buys !!

Good buys, hope so.

Investors and gamblers do what they are “good”at, for the last 10, 15 years they have sharpened their skill. They enjoy it for good reason, it’s fun, exhilarating and they are successfully, it’s what they do.

But the party is over, the easy money bunny is cold and dead.

That doesn’t matter to the skill sharpened investor, this is now a way of life, it’s part of the being. The entertainment value can not be denied.

Using an bad analogy: Watching the skilled fisherman waiting for the perfect time to pull the net and swoop up all the little fishies.

My apologies,

I’m a little behind on my writing skills.

Risk often seems acceptable like not having home insurance.

Its less risky than buying equity in these same companies. I’m holding all these bonds till maturity, so as long as the companies don’t go bankrupt before then, I’m fine.

This is an excellent distillation of JPow’s dovish buffoonery at the press conferences and how it completely undermines his otherwise (semi) hawkish rate hikes. It’s like yes we hiked rates but don’t worry, they’ll be back down again in no time! No need to worry about anything, ever again!

“But though he’s not a spaceman, famous or re-knowned,

He’s just a guy that’s down to earth, with both feet on the ground,

It’s all imagination, he’ll never learn to fly,

His words are like a fireball, a fireball,

Everytime he says those rate may go sky high.

Fireball! Fireball!

Ev’rytime he says those rates may go sky high.”

While all the while, it seems, every time he speaks, the money flows pumping the Fed’s pet projects, the asset bubble valuations.

In my eyes, the cause of inflation. In their eyes, an artifact of inflation.

The Federal Reserve may be increasing interest rates, not that it would matter much at all to anyone.

Is there some form of implicit guarantee by the Fed for people (meaning hedge funds, pension funds, insurance companies, etc.) that causes these outfits to buy this crap at these prices?

None of this makes any logical sense whatsoever at these credit spreads.

LOL Keep dreaming. Hedge funds blow up routinely and go to hell. No problem. But big diversified hedge funds will not be taken down by junk-bond bets. What they’re doing is buying defaulted or nearly defaulted junk bonds for a few cents on the dollar (small investment at risk) and then with a majority of control of those bonds, they have a big seat at the bankruptcy or restructuring table and can steer the outcome, and they end up getting either new debt at a huge gain (Carvana), or a big part of the restructured company (Hertz). This is what “distressed debt investors do.” It’s hugely profitable. Sometimes it doesn’t work, and the funds lose some money, but not much because they will nearly aways get some recovery on their bonds, even if it’s small; if they bought at 10 cents on the dollar, and they get only a 10% recovery (of face value), they’re even. And if they only get a 5% recovery, they lose half of their investment, which they had bought at 10 cents on the dollar, and that’s close to the worst-case scenario.

This issuance blurb from FT kinda makes sense, as to why there’s an increase in activities.

As for plumbing, a strong dollar and inflation add uncertainty to future value. Retaliatory tariffs and tax cuts, mixed with sticky inflation seems messy, what do I know…

““I think what most companies are thinking — particularly frequent issuers — is ‘let’s get the majority of our funding done in the first half of 2024’,” said Morgan Stanley’s Hodgson. “[Then] if we go through the election, and the market response is positive for whatever reason, we’ll use the back end of the year to get a head start on 2025.”

““I think what most companies are thinking…”

Read that out loud a couple of times and see if there is anything credible in what follows. It was just another theory pulled out of thin air by some guy that had to say something on the spot.

They are called ‘junk bonds’ for a reason: they are JUNK with huge risk.

Thanks WR for this article showing how loose the financial conditions have become.

Iirc in 2022 when thr markets were tanking.. Powell mentioned that tighter finance condition are doing thr job of rate hike.

I wonder if he would come out of his hoke and state the opposite now 🤔..

I’m one of the few retail investors who buys junk bonds. Or at least I have in the past. Waiting for much better spreads. Check back in a few decades. LoL.

Actually comparing risk to return, eh? I guess they’ll have to sell these junk bonds to Japanese banks.

“Ultra-loose financial conditions”

The FED blew it by pausing. They should have continued to raise rates another 100-150 basis points. Even worse, they started talking about rate cuts instead of saying “we’re not even thinking about thinking about rate cuts.”

The FED is an arsonist in firefighter garb. They caused this inflation along with CONgress, yet they tiptoe around and placate wealthy insiders while absolutely destroying the bottom 50%. I’d like to see Jerome Powell and his day-trading buddies in a cold prison cell.

Couldn’t agree more!

Absolutely no reason to project three rate cuts at the December meeting.

Impossible to know how much of the recent inflation trend has been caused by that one meeting but I’m sure it’s worth a few nips.

This world has been destroyed by greed l, led by the mighty USA, and that greed has lead to the insanely high prices for the basic human needs.

No wonder population growth projections are WAY down. It’s too expensive to have kids plus who wants to bring another poor soul into this downward spiral of a society

American dream- is dead and gone?

“Who wants to bring another poor soul into this downward spiral of a society”

Just when you think all is lost, cousin Ivan pops out of the bushes with a bottle of vodka and 2 Russian hookers.

The birds are content, the fish the plants, insects, even the flies are content.

Be like a fly, find a dead cat and multiply.

If not, shoot your wad on some junk bonds….show some spirit.

The sky is always falling with you Chicken Littles. I have nine grandchildren with another on the way. Thank God someone can imagine the future – it’s going to happen with or without you!

Living in a bubble but it’s not reality you’ve got to have a look outside-eiffel 65 lol

You should feel fortunate for your situation.

Birth rates have been trending down for almost 20 years and there’s plenty of reasons why… Most not positive ones.

FED and Powell are living in Denial from Dec 2023. They keep saying Monetary policy works through the Financial conditions. If that’s case look at Financial conditions from Dec 2023 and see for yourself. 10 yr rate came down from 4.75 to 3.6 in that time-frame. That’s like 25% drop.

FED never guaranteed any rate cuts in 2024. But they started this narrative. 3 rate cuts in Dec 2024 SEP was high hope. But keeping same 3 cuts in March SEP was blunder. Sure. We can say its was very close call. That is seen in dot plot 10 vs 9. But in April, Powell kept on saying Financial conditions are tighter now at Stanford event. In May meeting Press Conference too, he was hinting Financial conditions are tight. Which Planet he is living on? The Statement still has easing bias. “Next move will be Hike is Very Unlikely doesn’t help either.”

From June onward, slowing down QT means less pressure on Financial conditions. Even this move they started very early. Slowing down QT is needed but no so early.

If Institutional Investors are buying bonds at such thing spread, good luck to them. Let them loose money. Who cares? If they lose, they deserve it.

What I want is FED to do its job. Stay vigil and get the inflation down to 2%. Nowadays that another narrative by Media. 3% Inflation is new reality. Such a BS! FED did not increase rates for almost 6 years because Inflation was 1.7%. That’s below their 2% Target. They continued to ZIRP and QE. So now 3% is still way higher than 2% target.

We will see how they put Jun SEP dot plot. My respect to Boastic and Bowmen. Boastic put only one rate cut only in Dec and March SEP. That’s way before hot inflation data came in. Bowmen keep repeating hike is not off the table and might be needed if inflation data is not good.

Im still trying to figure out the price on the insurance that is credit default swaps on that there high yield debt is going off at. To me thats where the rubber meets the road.

Keep in mind, with a credit default swap, if there is a default event, the seller of the CDS loses and the buyer wins, and the net is a wash. If there is no default, the seller wins because they pocket the fixed payments. Much of it is gamblers betting against each other to make some money for a moment, which has led to some strange results.

What ever happened to;

“He who sells what isn’t his’n, pays it back or goes to prison”

Guess that was from long before ‘Too big to fail’ and “too big to jail”?

Hi Wolf , as always thanks for the insightful analysis. Would be excellent if you can provide your view on why the financial conditions ( Chicago Fed’s NFCI for example ) have been easing science mid of 2023 despite the FED holding interest rate and contouring QT.

They’ve been easing because everyone and their dog has been going after risky assets to chase yield, thereby pushing down risky yields, thereby narrowing the spread between risky and risk-free assets. There are all kinds of risky instruments, and spreads, not just junk bonds, that are going through this, and there is a huge appetite for newly issued risky assets, all of which are signs that financial conditions have eased.

The big exception is CRE, where financial conditions are tight.

“They’ve been easing because everyone and their dog has been going after risky assets to chase yield, thereby pushing down risky yields, thereby narrowing the spread between risky and risk-free assets.”

Because there’s way too much liquidity in the system, because the FED paused too soon and encouraged the speculative mania to continue. This is the biggest everything bubble/credit bubble in world history. Nothing even remotely compares.

The fact of the matter is that the FED does not G A F if house prices stay at these levels or increase, they only want the rate of inflation to go down so they can say they did their job. They actively state their policies and actions had nothing to do with house price increases. The FED is a cancer upon society at this point.

I agree whole heartedly with DC on this.

The loosening financial condition is a slap on FED’s face ( or may be not ).

The question is: Why investors are running towards these JNK bonds pushing yields down. I think it is because of these reasons:

1. The FED would cut rates sooner or later.

2. Too much liquidity in the system. Also evident by price of BTC and other bs coins.

@DC: I think middle class ( people who don’t own homes, or kids who don’t get homes from their parents ) are priced out of homes for ever. Not the America I know for sure.

You don’t need to look at what Powell says .. because it can be interpreted in many way. Just look at how market reacts to it.

“I think middle class ( people who don’t own homes, or kids who don’t get homes from their parents ) are priced out of homes for ever.”

As incomes rise and home prices fall, even if slowly, homes become more affordable over time.

Millennials and GenZers are already the largest home-buying cohort. They’re out there buying homes even as we speak, trying to drive up prices further, LOL

DM: Tallest building in Texas city sells for astonishingly low price… amid fears empty office blocks are going to sink the US economy

The tallest building in a Texas city has sold for a mammoth price drop. Burnett Plaza was purchased in a foreclosure auction for three years after it was sold for more than $137.5million. The 40-story building was bought by Pinnacle Bank Texas during the auction at the Tarrant County courthouse on Tuesday. According to public records, Pinnacle claimed that the building’s previous owner, Burnett Cherry Street LLC, an affiliate of New York-based Opal Holdings LLC, failed to pay a loan that was used to buy the tower in 2021.

Corporate Interest Expenses Are Expected to Increase Further

Kansas Fed Feb 2024

However, most firms have healthy interest coverage ratios, suggesting they can likely weather higher debt servicing costs as long as their earnings remain stable.

Party on dudes, nothing but good times ahead

Congrats Wolf! A mention in the NYTimes today. You’re the new king of all media! Well done.

Found it by googling. Thanks.

https://www.nytimes.com/2024/05/13/briefing/a-new-rent-versus-buy-calculator.html

“Developers are more likely to cut a deal. They lose money when homes sit empty, and many have cut the price of newly built homes, as the financial writer Wolf Richter has noted.”

Can’t read Times, but Congrats to you and the media empire you built.

Single handedly!!