Second-lien mortgages to the rescue of the battered mortgage industry. It’s expensive to benefit from your home equity unless you sell the home.

By Wolf Richter for WOLF STREET.

The problem for Wall Street is that homeowners are said to sit on $11 trillion in “tappable” home equity after years of surging home prices.

The actual home equity won’t be known until the homeowner sells the home and pays off the mortgage with the proceeds; the cash that’s left over is the actual home equity. In that situation, the homeowner cashed out and can now use the cash for other things, bet it on cryptos to become a billionaire overnight, buy Treasury bills to earn 5.3% in interest, fund their own startup, or blow it in some other way.

But without a sale, the home equity is a theoretical value that you can turn into cash only by borrowing against it, thereby paying Wall Street interest and fees to get to your own money.

Which is of course the promised land for Wall Street – especially as they can see and smell that $11 trillion in “tappable” home equity in front of them, ripe for exacting their pound of flesh. And now it’s just a matter of promoting this to homeowners — “this” being the opportunity to pay interest and fees to Wall Street in order to get to their own money.

Home equity overall is $16.9 trillion , of which $11 trillion is “tappable” equity (including a 20% equity cushion), according to ICE Mortgage Technology, a subsidiary of Intercontinental Exchange (ICE). About 48 million homeowners have some tappable home equity, it said.

And it’s just so juicy: two-thirds of the tappable home equity is held by homeowners with credit scores of 760 and higher, which make them low-risk borrowers, paying interest and fees to get to their own money.

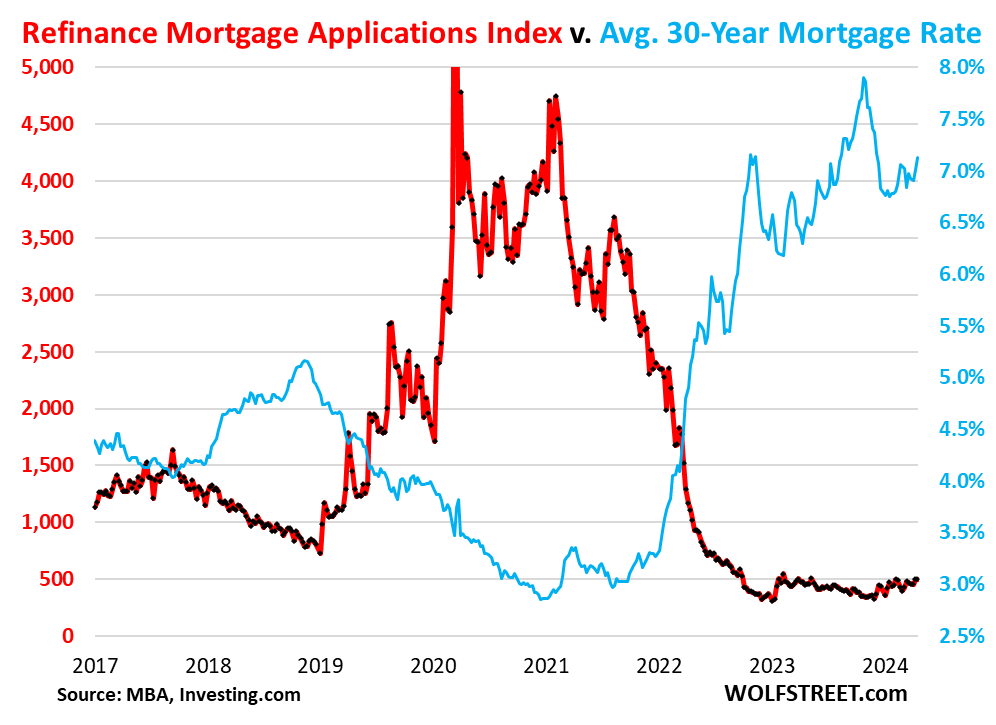

So the mortgage industry is trying to make this the next new thing after it got crushed by the collapse of refinance-mortgage originations – including cash-out refis – starting in late 2021 when mortgage rates began to rise, and homeowners didn’t want to refinance their 3% mortgage into a higher rate mortgage.

HELOCs are rising from the ashes, but the volume is still small. These are lines of credit secured by a second lien on the home, but homeowners with a HELOC only pay interest on the actual balance they withdrew. For now, this is still just small potatoes for Wall Street:

Second-lien mortgages to the rescue.

The mortgage industry has been super-eager to find other avenues to make money off the “tappable” home equity. And so they’re promoting second-lien mortgages, where the borrower takes out a second mortgage on the house, with a fixed payment, to where the borrower now has two mortgage payments to make, instead of one, paying Wall Street interest and fees to get their own money out of their home.

After a lot of pressure from the mortgage industry on the government to get behind this opportunity to get homeowners to pay interest and fees on their own money, Freddie Mac has come out with a proposal to buy second-lien mortgages from mortgage originators – from banks and non-banks alike – in order to securitize them with government guarantees into MBS and sell them to investors.

Banks can carry second-lien mortgages on their balance sheets, and banks have money from their depositors, so they can do that; but non-banks don’t have depositors, they need to borrow the money from somewhere else, and that has been getting in the way of second-lien mortgage originations.

Nonbanks are now the dominant mortgage originators. They can sell their regular conforming mortgages to Fannie Mae, Freddie Mac, the VA, Ginnie Mae, and other government entities, thereby getting those mortgages off their books. But they cannot sell second-lien mortgages so easily. So Freddie Mac is trying to make that easier, and once Freddie Mac pulls this off, the other Government Sponsored Enterprises (GSEs) and government agencies are going to follow, at least that’s the industry hope.

The hope is that being able to offload the second lien mortgages to the government entities and from there to investors will open the floodgates for that $11 trillion in tappable home equity to start generating fees and interest income.

And so this opportunity for homeowners to pay fees and interest to get to their own money has been hyped everywhere, on YouTube, on TikTok, even in the comments here.

For most people, when they think about it, paying fees and interest on their own money is absurd. But it’s hard to get to this money. They’d have to sell the home to get to it; or they can borrow against it, in which case they’re using their own money as collateral and paying interest and fees out of their nose to turn it into cash.

There are few situations where this – paying interest and fees to turn your own money into cash – might be, I don’t know, justifiable? Such as funding your kid’s startup company; funding the down-payment of a rental property; funding a big remodeling project; betting on becoming a billionaire via a big crypto investment, etc. You’re leveraging the house – you’re taking on more risk and more expenses – to accomplish something with it.

Multiple risks for the homeowners.

Homeowners might not be able to maintain their income (due to layoff, etc.) to make those two mortgage payments.

Even in the 12 states with non-recourse mortgages, such as California, where homeowners can walk away from the home and let the lender take the loss if the housing market tanks, second-lien mortgages may be recourse loans, and if homeowners walk away from the home, the lender of the second-lien mortgage can go after them personally for the deficiency. In the 38 recourse states and DC, lenders can go after them personally to collect any deficiency on both mortgages. A second-lien mortgage makes a deficiency more likely when home prices are heading lower.

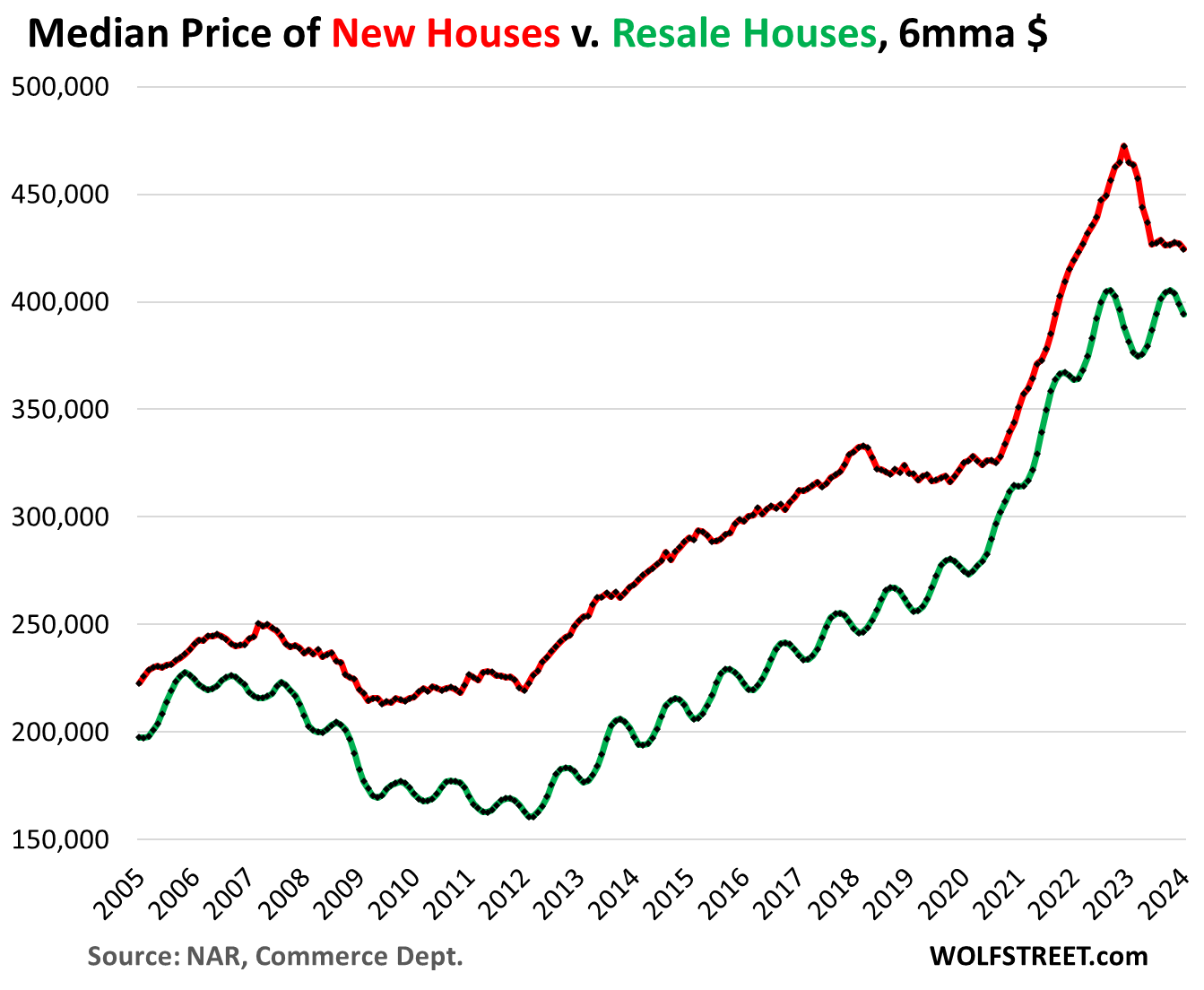

Home prices are already heading lower in many markets, and may head lower in more markets. This overpriced market is primed for a reset. And it’s happening in enough markets already to where, despite prices still heading higher in other markets, prices of existing homes have at least flattened out on a nationwide basis since the high in June 2022 (the national median price is down from the peak in June 2022), and prices of new houses have dropped sharply. Chart shows six-month moving averages of the median price of new single-family houses (red) and existing single-family houses (green):

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Bankers are looting the world. You’re not in the middle of a recession; you’re in the middle of a robbery”.~Frankie Boyle

It’s a general mentality these days: Don’t be happy with what you have; borrow from the future to have more NOW!

Borrowing can be a good thing if the value of what you get is greater than what you pay but the message that goes out is that the value is greater simply because you have it today, and that is dangerous.

Brian – sage advice, but up against the entire advertising ‘industry’s constant R&D’s to find ways to encourage and amplify the dopamine hit of a purchase to the average human…

may we all find a better day.

A bigger problem than most realize, Dustoff.

If advertising weren’t a DAMNED TAX WRITE-OFF, this world would be in better shape. That whole industry wouldn’t have grown so HUGE. Massive social damage, in every aspect of life

Those guys are TOO DAMN GOOD at the psychology of it.

Wolf disagrees with me, but perhaps some kind of a LIMIT to it?

I tried to find a law, but it has always just been assumed.

Was fine assumption when one had a sign and word of mouth….but to is WAY TOO BIG now.

Yep. Banks use to be just banks. Pay 3-4 % interest on savings, charge 7-10% on loans, and get your ass on the golf course by 4:00 PM so as to not get greedy and fuck things up. Now banks are simply casinos funded by their printing press and allowed to continue via bought-and-paid-for political puppets. Too big to fail is even bigger now.

Interesting times.

Big banks like Wells Fargo and Citicorp are criminal syndicates masquerading as money center banks. Sort of like Al Capone, the gangster and thug whose business card listed him as a furniture dealer.

Lucky Luciano – “I joined the wrong mob!”

Don’t forget that very honest, sincere, and handsome Tom Selleck selling reverse mortgages to senile old widows on TV, so she can shop for jewelry for her grandkids.

The money extractors are in total control now….they even advertise all sorts of payday and other brand new bank loans/free money on TV….stuff that used to be mostly in ghettos…..but long ago they ran out of Indians to kill, and then later on other people of color to screw, so it’s been the WASPS filling in since Reagan.

All of them programmed by ex and present Talk Radio hosts. It’s a billionaire’s (and Murdoch’s….and many other’s, in and out of this country) wet dream.

I suppose one justification for this refi would be to get some quick cash together to ransom a kidnapped relative? Depends on whether you want the relative back………

That kidnapped relative can be a cloned voice, courtesy of AI. Or maybe the kid is in on it ….

It’s pathetic to observe supplicants, approaching hat-in-hand, to gain approval for a loan and then disparage the lender as soon as they’re approved and receive the funds.

Looking from the other perspective, as a young person starting out I approached the bank for a small loan to buy furniture, the bank where I had an account, as did the company I worked for just up the street, and was told that I had to have liquid collateral for the amount of the loan. Of course if I had that I wouldn’t require a loan.

So I went to a finance company (the bogeymen typically described as monsters to be hated), received a loan instantly at at a much higher interest rate, and paid it off diligently.

I continued to borrow from them occasionally over the years even though I wasn’t really in need, because I appreciated the service they provided and the trust they demonstrated.

Sorry to say, but they didn’t demonstrate trust. They demonstrated risk vs reward calculations.

My husband and I started our lives with nothing, and by dint of hard work and buying USED everything, we are now are quite comfortable. Quality used furniture and clothing are easily available for a fraction of the original cost. One plus – it’s a treasure hunt. You can find the most amazing things discarded at Goodwill.

Most evil economy in the world, if that is what you’d like to call it.

Where boomers take out a loan based on their overvalued home, thanks to the Fed, to go buy a new corvette, and the speculators on WS skim the top.

Meanwhile the younger generations have to deal with the overwhelming amount of inflation that still hasn’t been rung out of the economy, and the 1/3 loss of buying power since Trump was sworn into office.

It’s amazing that no value is really created in the US, and whatever value is created is siphoned off by WS via fees and interest.

And yet this Ponzi has been going on for multiple decades like this.

I guess thank god for the Great Depression levels of deficit spending by the federal government, or we’d all be screwed.

Millennials and GenZers are now the biggest home-buying cohort. Millennials have been buying homes for a decade. THEY are the ones trying to pull cash out of their homes, not boomers. Boomers did that 20 years ago before the mortgage crisis and got ripped to shreds.

Perhaps this is your best analysis I’ve seen. It does seem that you’re a bit peeved on this. I agree!

Wolf does seem to be out in front of this one (although I think he is focusing too exclusively on Wall Street scummery and not enough on Ye Olde Indispensable Actor – the G, which if it allows Fed insurance on second mortgage lending, will be the beating heart/eager patsy of the latest “stimulative” corruption).

Basically, the engine of all this financialized idiocy (over and over) is the ability of the G to,

1) Print new money without real asset backing,

2) Use said money to perpetually buy fiscal deficit financing Treasuries,

3) Thereby driving down all USD-based interest rates (since essentially all USD lending is priced at a spread to Treasury benchmarks),

**4)** By driving down interest rates artificially, the G can (temporarily, artificially) goose most all asset values (real estate, public equities, everything else…) because the “present value” of assets goes up as interest rates go down, mathematically per the industry standard discounted cash flow formula (DCF),

5) Now the worthies pushing the “G should insure second mortgages” scam want to use the very theoretical, almost certainly inflated valuation of such assets (in this case, residential housing) to goose (again) the stalling economy – at the cost of the G (read taxpayers and USD savers) catching it in the neck when home values inevitably fall.

(5a – Really, somebody/anybody should ask current commercial real estate owners/borrowers just how fictional real estate valuations can be, as office buildings are being written down 80% percent around the country. That “tappable” real estate “equity” turns out to be quite “evaporable”.)

YES! We actually use to let people/corporations get “ripped to shreds”!!! We also use to punished bad behavior and force short sales etc.

Now everyone get a fucking trophy and a BAILOUT.

This is exactly the foundation of all our eCONomic woes!

“Freddie Mac has come out with a proposal to buy second-lien mortgages from mortgage originators – from banks and non-banks alike – in order to securitize them with government guarantees into MBS and sell them to investors.”

I read where this means that the government would issue the 2nd mortgage at the 1st mortgage rate. Does this sound correct? Sorry if I missed this in your article.

If so, then this seems extremely reminiscent of circa 2002-2007 with subprime borrowers. And if you ask me, it’s more evidence that the government has every intention of riding to the rescue with rent & mortgage relief whenever the next recession hits.

It’s all about backstopping everything and pushing the bubble higher and higher with no consequences.

“I read where this means that the government would issue the 2nd mortgage at the 1st mortgage rate.”

That’s incorrect.

1. The government doesn’t issue the mortgages at all. The lender writes the mortgage, hangs on to it for a while to pool it with other mortgages, and then eventually sells the bundle to Freddie Mac. It’s up to the lender to decide what interest rates they can get away with charging the borrower.

2. Under the current proposal, Freddie Mac will only buy the second-lien mortgage if it already holds the first-line mortgage from that borrower. So that’s a huge limitation. If Fannie Mae holds your first-lien mortgage, Freddie Mac will not buy your second-lien mortgage. And Fannie Mae won’t buy it either. The rate of the second-lien mortgage is set by the lender, and has nothing to do with the rate of the first-lien mortgage. Your first-lien mortgage may be 3% and your second-lien mortgage may be 8%.

Wolf,

In aggregate, don’t the government-backed/insured entities (the Macs and Maes) already own/insure a huge percentage of outstanding residential mortgage loans? So how much of a limit will “existing first lien ownership” really be?

And, as you said, if one such entity gets the government insurance for this latest scheme/scam, won’t the others demand equal treatment (in the name of “competitive fairness” – snort)?

(And I don’t think this latest poisoned chalice would be being promoted to the public right now if at least some DC heavy political hitters weren’t already in favor of it).

So this is Freddie Mac only. Not any of the others. Freddie Mac backs $3.28 trillion in mortgages, and the second-lien mortgages would be limited to qualified borrowers of those $3.28 trillion in mortgages.

Total mortgage debt outstanding = $12.3 trillion

cas127 and Wolf,

If Freddie’s experiment works out well, I surmise Fannie will follow suit.

If so, cas127, it will probably not be a big limitation, but to the extent originators currently shop particular loans to either Fannie or Freddie based on minute differences in underwriting criteria, they will be unable to do so with these second mortgages.

Just spitballing, if we got to where Freddie and Fannie both offered these, I really doubt the limitation on shopping around would even reach 25 bps of materiality on average. But I would be surprised if it was really zero bps.

Not to mention that both Millennial and GenZ have higher earnings than the Boomers had at the same age. In fact, they’re doing better than all previous generations. This whole “Boomers are stealing the wealth of the younger generations” line is tiresome nonsense.

https://www.economist.com/cdn-cgi/image/width=360,quality=80,format=auto/content-assets/images/20240420_FNC345.png

It’s adjusted by household size, so it’s also accounting for more dual-earner couples and fewer kids.

The following information was taken directly from the Freddie Mac Proposal for Public Comment:

“Freddie Mac proposes to purchase certain closed-end second mortgage loans from primary market lenders who are approved to sell mortgage loans to Freddie Mac

(Sellers).”

“In the current mortgage interest rate environment, a closed-end second mortgage may provide a more affordable option to homeowners than obtaining a new cash-out refinance or leveraging other consumer debt products. A significant portion of borrowers have low interest rate first mortgages, and the proposal would allow those homeowners to retain this beneficial interest rate on the first mortgage and avoid resetting to a higher rate through a cash-out refinance.”

I could be wrong, but that sounds like Freddie Mac is going to start buying 2nd mortgages where lenders originate the loan at the 1st mortgage rate.

If this is correct, this will be shown to be disastrous and almost as dumb as lending to subprime borrowers.

No, your interpretation is NOT correct. Read it carefully. What this — “the proposal would allow those homeowners to retain this beneficial interest rate on the first mortgage and avoid resetting to a higher rate through a cash-out refinance” — says is that the first mortgage remains intact at the current rate and only the second mortgage has the new higher rate.

So this — the 1st mortgage at 3% and the 2nd mortgage at 7% — is an improvement over a cash-out refi, where the entire new mortgage balance (old mortgage balance plush cash-out) are at 7%.

Amazing headline article and thanks so much for the tidbit of absurdity that these programs bring to light . My house is paid for and when rates hit 3 percent I was tempted to secure either a 1st lien mtg or reverse mtg and arbitrage the cash in tbills that were slightly higher. 2021 time period . However the fees required were quite high at first glance upwards of 2 percent of mtg costs which wipes out most of the arbitrage. This article brings tears of joy to me that I did not bite at the tempting bait on top of the water . Leverage is a banks dream to collect easy fees. My daughter did tap into her home equity she is 30 to build an addition to her home . I told her to make bonus payments with any extra cash but no idea if she does. Up to her

Umm, they are not charging for fees and interest from people using their own money. They are charging this for the loan bank is giving out from bank’s money. Homeowner then still has the house and the cash at the same time. House is a guarantee that the loan will be repaid. This is homeowners equity only when the home is sold. While they have it still, they can only borrow money from the bank.

Has everyone just lost their.mind?

Hudson:

Your example of a Boomer buying a Corvette has nothing to do with feeding inflation unless the younger struggling generation wants to buy a Corvette as well. Buying a Corvette doesn’t raise the price of a house, a Prius, nor does it impact a pound of hamburger. Hocking a house to buy a geezermobile (Geezer habitats include Corvettes and a Harleys) only exposes the borrower to the risk, not the struggling generations.

As Wolf said, Boomers got their heads ripped off stripping equity out of their houses decades ago. The house my daughter bought (at the ripe age of 27) was an example of that phenomena. It was in East Bay (Clayton, CA) and she bought it for $200K+ back of what the prior owner (who lost it to foreclosure) had it hocked for – a 40% haircut. He hocked it to buy a motor home (which also got repopped).

And, by the way, the bulk of the recent loss of buying power occurred since all the stimmies, PPP, etc., a good chunk of which what’s his face had not much to do with. @ $7T+ of it (IIRC) has been since he left town. The new guy has nearly tied the prior guy, with 8 more months to go. On a percentage basis it’s less, but on a $ basis, it’s allegedly nearly the same.

Speaking as one of the horrible Boomers, I am not the problem with inflation. I have enough junk that I don’t need to compete to buy the latest computer, newest gizmo-mobile, house, couch, bigger house, nor 297″ TeeVee. For you to imply that anyone should sell their home for less than market value is naive. There are no participation trophies in real life. Oh, and the “depression level of government spending” will assure that you’re screwed. It may just take awhile.

I have two kids. One owns a home with his wife. They do just fine. Daughter now rents (used the proceeds from the sale of her house to fund a career change) and is doing just fine. From what I can tell, by comparing them to their peers, those young adults who had parents that invested their time in teaching them how to handle money are doing well. Those whose parents spent like drunken sailors are not as they simply don’t know how (or don’t want to learn). My daughter had to teach her roommate about CD’s. That person never had any idea about how to use them as a savings vehicle. Imagine being in your 40’s and not know about a CD…. and keeping all your money in a checking account (what little they had until meeting her) and getting $0.27 per month in interest vs. $100. She taught them to budget, basket money for savings, “mad money”, retirement, and so on. Before that, spending was determined by how much was available without any regard for the “oh, sh!ts” of life.

Excellent comment Katz. My Millenial kids and a z nephew will be inheriting all our assets and should be very well fixed when the dust settles. They have also been raised to be aware of their finances and all are getting ahead on their own. My 13 year old granddaughter has a savings account and saves most of her babysitting money. We just did what we were taught to do, and did without the things many people take for granted these days in order to get ahead. Parents are supposed to pass on ‘life skills’ out of love, caring, and responsibility. Parents…(Boomers)…are on the side of their children for the most part and don’t go through life stuffing themselves at their expense.

@Paul: Many parents either didn’t or couldn’t give their millennial kids a good start financially or knowledge-wise. Many of us started out with no money, no direction and nowhere to go back to. Nobody thinks of putting whatever savings they manage to get in a retirement acccount when the interest rate equals the inflation rate and they’re worried about becoming homeless every time the lease renews.

Some years ago there was a book-length sociological study called “Lost in Transition”, where they did in-depth interviews with a few hundred young millennials, and one of their conclusions was that the adult world had “simply abdicated” their responsibility to teach their kids anything.

MattB this was my experience. You can’t pick your parents unfortunately. There was something uniquely culturally toxic and subversive growing up in the 80s and 90s as ‘that kid’ and more than a few of them grew up bitterly resentful for it. Self included for far too long. But the Gen Wars are a waste of energy. Those parents are now hurting hard and running short on time. Hard to be bitter against those you pity, from a safe distance of course.

While you don’t know what you don’t know, you can turn damage into resource and resilience. Take up a career that’s AI and recession proof. Or sell feet pix. Whatever.

Having climbed out of the victim trap, it feels like there’s a palpable effort to keep an increasing % of the population feeling victimized and defeated. But with so many free online resources these days, the only real challenge is in recognizing the trap and deciding to get out of it.

At my age, in this economy, I assume I’ll be on the Matt Foley Retirement Plan unless I can improve my situation in the next two decades, but these days its actually a pretty sweet deal so bring on the government cheese.

“Hocking a house to buy a geezermobile (Geezer habitats include Corvettes and a Harleys) only exposes the borrower to the risk, not the struggling generations.”

Something similar was said in 2006. Unfortunately, it’s actually the financial system at risk from collective irresponsibility of said borrowers.

Re “actually the financial system at risk from collective irresponsibility of said borrowers.”

That was also said in 2006-2008, and is even more untrue now than it was then. “Systemic Risk” is a euphemism for “the wrong people will bear the costs”, coined by people who were too proud to admit that “Collective irresponsibility” applied to them as LENDERS, as well as to borrowers.

Proper (pre-1990) application of (a) antitrust law and (b) contract law would fix the problems of systemic risk, too-big-to-fail, ad-hoc illegal bailouts, and the consequent collective irresponsibility (formerly known as “moral hazard”).

To be fair, there really wasn’t a good reason to use CD’s until recently. Even now, there isn’t a massive benefit vs. some of the higher-yielding savings accounts out there.

Also, the roommate doesn’t have any money, putting those meager savings in a CD means there’s nothing available if an emergency pops up.

Millennials from 2019 to now have seen the biggest wealth increase in that time frame than any previous generation. I have no idea if this report is correct but it is popping up a lot of places on the internet. It is from CAP and this is from CNBC.

—————————-

Millennials may have ditched their “broke generation” stereotype.

Household wealth among Americans under age 40 — which includes most millennials, who are currently ages 28 to 43, and some Gen Zers, who are currently in their teens and up to age 27 — grew by a whopping 49% between 2019 and 2023, according to a Center for American Progress analysis of Federal Reserve data.

The inflation-adjusted average net worth of households headed by someone age 40 or under was around $174,000 at the end of 2019. That number grew by $85,000 to hit $259,000 by the end of 2023, CAP found.

“Millennials from 2019 to now have seen the biggest wealth increase in that time frame than any previous generation”

The exact same thing was said about home buyers/multiple home pyramiders from 2002 through 2008. Then they were crushed in trash compactors.

Asset valuations (key to any “wealth calculation”) are volatile and driven by the cycling of interest rates and related supply/demand factors.

A snapshot in time is only a snapshot in time – the transient product of ever changing economic fundamentals and perennially manipulated interest rates.

When you start from very low levels, it is easy to grow wealth. Add to that absolution of rent and student loan payments, and deferral of mortgage payments, not to mention sky-high unemployment insurance payments, and of course all that free money is going to be a boon.

Gen-X here, and I wrote a check for my new Vette. Thanks for the concern.

I hope the old boomer buying the Corvette trades in his Grand Marquis – I’m on the lookout.

I don’t know if you made a typo, but the inflation rate in 2020-the END of Trump’s term and the beginning of Biden’s term was 1.2% (according to Bureau of Labor Statistics). The following rates for the following years were 4.7%, 8.0%, and 4.1%. The loss of buying power occurred during Biden’s term.

“ It’s amazing that no value is really created in the US, and whatever value is created is siphoned off by WS via fees and interest.”

I worked for 20+ years in US manufacturing companies that sell products to US agricultural producers, and it’s all still going strong. . So yes real value is being created every day in the US.

Engineering doesn’t have all the college general education of our business colleagues; however, a mandatory class is Engineering Economics, so there is a solid mathematical grounding in all the juicy schemes of the business world. From this perspective, why not split the second mortgage into two parts: Part 1 could use some of that untapped equity to buy down the second mortgage interest to something as appealing as the Federal Reserve’s zero interest days, just set it at like 2.x% (sort of like slot machines with the two cherries 🍒 kicking back a coin). Part 2 then would be the treasure trove of equity ready to be “invested” in sure things in the securities world that again our business colleagues cook up. For the engineers, put down that Quantum Tunneling … book by Liang and join up with these business graduates. PS: The corporate office of an American semiconductor company probably doesn’t know what tunneling is anyway.

“For the engineers, put down that Quantum Tunneling … book by Liang and join up with these business graduates.” Barrier penetration doesn’t leave me feeling dirty like finance does.

I have no idea what quantum tunneling is but will now search the term out

Easy. #1 it is a THEORY.

Academic mathematical worms that make Swiss cheese out of the brains of ONLY those that rise to the top of the physics (among many other disciplines) world? (see Bertolt Brecht)

Might inspire some slightly different kinds of good old trial and error, though, in making CPUs…and give people a way to talk about making them…..probably it’s main value…..but also might set us WAY back in other areas…..look up “receptor theory”….one of my favorite examples. Who cares if it’s based on BS? IT MAKES LOTS OF MONEY!!!

Not sure I understand your logic by stating that they are paying interest and fees on their own money. The money isn’t theirs, the house is. They are borrowing cash from a lender and still retaining full use of their house. If you want use of the house AND the cash, you should pay for it.

The home equity is theirs. The house is theirs. the mortgage is what they owe. So if they sell the house, their home equity becomes their cash, and they can spend it on whatever.

Yes, they’re borrowing cash from a lender, and yes, they should pay for it, you got it!! But they already own the money (home equity), except they’re having trouble turning that money into cash, so they’re paying interest and fees to turn their own money into cash.

There are several points:

1. What’s not to like, if you’re the banker? So if the lenders can talk lots of homeowners into doing this, that’s the hope, interest and fees will rescue the battered mortgage industry, that’s the hope.

2. Homeowners take on the listed risks and expenses to do that.

3. It’s expensive to benefit from home equity unless you sell the house.

It’s truly sad that these borrowings may be bought (enabled) by the federal government. A lot like subsidizing a crack habit. But the reality is that people are responsible and accountable for excessive borrowing. The “bankers” aren’t the evil-doers; they’re more like dance partners.

I just don’t see the knuckleheads as being so innocent. Who ya gonna blame?

The GSEs were one of Franklin Roosevelt’s long-term solutions to the Great Depression. The idea being that coming out of WWII, tens of millions of Americans would be employed building suburbia and the accoutrement that come with it: roads, water infrastructure, cars, appliances, etc… And it worked! The great age of the building of suburbia, the ’50’s and ’60’s is what many older folks look back on as America’s golden age.

But today, private banks can replicate the MBS with their own software. Producing and selling their own products. One of their problems though is trust. Back in the double oughts, the banks couldn’t get enough interest and fees from standard mortgages, so they lowered lending standards to no-doc loans, fraudulently sold that garbage, and crashed the world economy. Big investors haven’t forgotten, so the bankers need the federal government to hide behind, because people have some expectation that the government is more trustworthy than the banks.

So the problem isn’t the federal government enabling ne-er-do-wells, but the evil people spending millions to manipulate those who pull the strings in the government: the bankers and others of their ilk.

:) This is the real issue. Bankers are like the street corner drug dealer. He’s got the product but he’s not putting a gun to your head to buy it. The Junkies… AKA about 50% of US population is used to instant gratification and has no concept of hard work. So the drug dealers flourish. Preaching restraint and fiscal responsibility, while observing neither has become fashionable. Just going to Church on the weekend does not make you a good person.

“The “bankers” aren’t the evil-doers; they’re more like dance partners”

I think the word you are really looking for is…pimps.

Not so much Arthur Murray as Chlamydia Mary.

GSE insurance for second mortgages on vastly inflated SFH values doesn’t just appear…it is the product of a political program pushed by political/financial interests.

Cas127, all professions are built on “borrowing” except for yours, of course, whatever that may be. How many engineers thought up the chain rule on their own. Plumbers, gardeners, welders, and yes, bankers, borrowed; they didn’t invent those jobs. I was a teacher so I can say with some authority that critical thinking is most needed but almost impossible to get across, esp. to those who think in terms black & white, good & evil, and other binaries. Same with conspiracies. “If ya ain’t wit me your agin’ me.” (Ronald Reagan selling his tax cuts for the wealthy to the ninnies – the trickle down thesis.) And some think that there’s something evil in every crevice of the government.

Conspiracies: ya just can’t fix ’em.

@Kent:

The GSEs of today have gone Frankenstein compared to their original incarnations.

Prior to the 2008 crisis MBS were explicitly NOT federal guaranteed, nor eligible for Federal Reserve purchase. When the next crash comes, we’re once again going to deeply rue letting the bankers offload their mistakes onto the taxpayers under the ruse of “making mortgages more affordable”.

At the systemic, holistic level, what makes owning a house affordable isn’t the interest rate, it’s the economic output of the buyer vs. the economic input required to build the house.

Of course I’m pissed that GSEs are considering buying jr. loans. But if it weren’t for GSEs, almost all of us would be renters, not 64% of us in homes.

Mortgages in the 1920s were at most 5 yr loans, interest rates not fixed, interest only payments, and with a 50% down pymt. How about that for starting collateral. Refi every 5 years or you needed to hand the bank a balloon payment of the other 50%. No mercy on foreclosures.

But with huge swaths of the population losing their homes in the depression, and others in bread lines, there was a growing belief among the “haves” that capitalism may be at risk. Hence, GSEs to lube the economy and give some relief, starting in 1933. This was amped-up after WWII by offering tiny down payments for vets.

All was good and the economy did well. Yes, some moral hazard, but worth the cost. Besides, there were the Nelsons, Father knows best, and Leave it to Beaver.

As we all know, the road to hell is paved with good intentions. Now the GSEs are going overboard to stimulate and provide more liquidity. I just do not see this, wrong as it may be, as demonic. They make it up as they go along; they all dance while the music’s playing.

HowNow,

“They make it up as they go along; they all dance while the music’s playing”

That is a very benign view in light of repetitive policy mistakes – affecting tens of millions – over the last 20 years.

These guys ain’t dummies or babes in the woods…this is the industry and these are the dynamics they deal with every minute of every working day for their entire career.

They knew they were taking gross risks in 2002-2008 and they know they are taking gross risks in proposing this now.

It is just a tragedy that the 325 million non-industry participants have to educate themselves (slowly…all too slowly) to protect themselves from this repetitive idiocy/risk-dumping.

We’ve seen this horror movie before…no reason to be forced to watch it again, less than 15 years later.

(“Free the Nubile, Trapped Equity Hiding in the Attic!!”)

Spoiler – The “trapped” equity is the financial equivalent of the demon girl in the well in “The Ring”

Thankfully, not many homeowners got HELOCs or second-lien mortgages. The numbers are tiny.

Another example of our debt based overcunsuming society determined to borrow itself into destruction.

Equity in the house? – let’s borrow it and spend it on some more stuff we don’t need and can’t really afford. Maybe a new pickup, boat, jet ski, atv, vacation, fast fashion. Or let’s be prudent (lol) and pay off our 30% credit cards with a 10% 2nd mortgage!

Dumb consumers who can’t manage their finances and spend and live beyond their means to keep up with the Jones’s

This is also part of our inflation problem.

Agree with the logic but not the style. I don’t think home equity is “money”. It is non liquid wealth. And if you are house rich and cash poor, and a big expense comes along (kids wedding, major uninsured loss, home improvement) tapping home equity is option. I wish there was a lower price tier for people borrowing less than 50% of net equity. That should be much more attractive for investors given that home values might have peaked.

Kevin,

“I don’t think home equity is “money”.

If you have “a lot of money,” it includes the equity you have in your home as well as the equity you have in your other assets, plus whatever else you have. “Money” means a lot of things.

In my Random House Webster’s Unabridged digital dictionary, money has 20 definitions, things like: #7 “capital to be borrowed, loaned, or invested: mortgage money”; and #9 “wealth considered in terms of money: She was brought up with money”; and #11 “property considered with reference to its pecuniary value.”

I tend to agree with Kevin and don’t look at assets as money, I look for ways to get actual money from my assets (that includes selling things I don’t use on a regular basis) but want to let people know that borrowing to pay for a wedding is usually a bad use of money (one of the best weddings I ever went to didn’t cost much money)…

It’s really funny. People just make up their own definition of “money.”

That said, not counting your chickens until they’re hatched it a good and conservative policy.

“That said, not counting your chickens until they’re hatched it a good and conservative policy.”

Especially if the Fed can arbitrarily resize your chickens month to month.

A VERY refreshing answer Wolf. You could also point out that lawyers are trained to use their “special language” to prove Kevin is exactly correct…and then it’s case closed….for a suitable fee.

The Neolithic revolution brought about “civilization” and the division of labor.

Wonder how divided the “labor” is now, and how many special “tickets” exist so that one may engage in a given division?

At least a heloc provides the borrower with the utility of the borrowed cash.

The bigger ripoff is real estate taxes based on unrealized market value, which can fluctuate from year to year, and have no relation to the eventual profit or loss from an eventual sale. You can pay taxes on the inflated value and then sell in a major downturn with no recourse. Been there.

yes, governments benefit hugely from inflated real estate values.

“yes, governments benefit hugely from inflated real estate values.”

And, mirabile dictu, we’ve had 20+ years of government policies (ZIRP) that grossly inflated housing values.

Wolf,

What’s the opposite of opportunity cost? Opportunity benefit? That’s how I look at home equity: if it doesn’t have a mortgage against it, then you’re not accruing interest. That’s a benefit–possibly a big one. It helps you stay in your house, but sadly it doesn’t help repair the house, buy groceries, fill a gas tank, or cover a doctor visit.

Semantics play going on there. Do you believe all assets are money?

Yeah, this is a weird take. If you borrow on margin in a trading account, you are borrowing against “your own money” (the other stocks you own), and for that privilege you will be charged interest. Same for any collateral-backed loan you might get from a bank.

The mortgage company will canvas an area, find a weak spot in the homeowners armor- and shoot them with the stupid arrow.

But…Until “lack of money” becomes a thing, the mortgage companies will have a hard time getting a clean shot on the equity rich homeowner.

Nice image, but the shot of the stupid arrow is self-inflicted.

Actually it’s quite creative and… Very much to the “point”. Been very successful living my life without debt, easy for some, extremely difficult for others.

The stupid arrow shot me long ago, I’m still trying to get the arrow out.

Like you said “self inflicted”. Done shot myself with the stupid arrow.

Starting to see bidding wars on the rental applications Ive been sending out. When they have 40 applicants to each unit they can make us fight for the scraps.

This cant be fixed without bloodshed.

They are “low risk” specifically because they were proper with their money/debts and paid off their mortgage!

“And it’s just so juicy: two-thirds of the tappable home equity is held by homeowners with credit scores of 760 and higher, which make them low-risk borrowers, paying interest and fees to get to their own money.”

Exactly. That’s the subset of the population that isn’t stupid enough to use home equity for a new Harley.

There are lots of folks like me with an 800+ credit score (old retirees).

And I have no W-2 income, have a paid for house, live with a small dog, have an EV, and no debt. But, I don’t need a 2nd mortgage, or any mortgage for that matter.

I’m like Debt-Free-Bubba I guess! LOL

My middle aged daughter doesn’t like debt either, and owns a paid off house.

Those scummy bankers won’t get us roped into their schemes!

Did a ‘scummy banker’ ever help you or your daughter purchase a house? Most of us need a ‘scummy banker’ or we would not own a house. Can you recall?

I too do everything possible to reduce payments to scummy bankers. Why does the mortgage payment start with 99% interest on first payment? – SCUMMY BANKERS.

Bankers don’t want anyone to pay off loans like Anthony A. & DFB and in the last cycle here in the SF Bay Area with super high prices I heard of lots of interest only (1/O 100% of the payment to interest) home loans…

WTF-justabuck: In finance, there is the Rule of 78; 78% of your loan is still owing half way through the loan. The faster you pay the principal, the less interest you owe. Try paying an extra $100 on a mtge pymt and see how quickly your amortization (ie: 30 yr mtge) is reduced

I fondly remember Mr. Drysdale and Mr. Mooney, Miss Hathaway.

wtf-justabuck: the reason your initial mortgage payment is 99% interest (actually 90% on an 8% mortgage, but 77% on a 5% mortgage) is because the monthly payment is a constant for the life of the loan.

This means that initially, when the principle is highest, the interest (which is a fixed percentage of outstanding principle) is also highest, and therefore takes the largest chunk of the payment.

You could alternately structure the payments so that the “interest” percentage was a constant, but then the amount of the monthly payment would decrease through the life of the loan, being a maximal amount at the outset, when the borrower is presumably least financially able to pay.

Having said all this, “interest” vs “principal” is ultimately an accounting fiction. Albeit one enshrined in tax law for some reason. In actual fact, you have an outstanding balance which increases by a fixed percentage (the interest rate) per annum, counteracted by whatever payments are made. If the payments exceed the interest the balance will eventually go to zero. Otherwise it won’t.

GSEs do not need to be purchasing second liens. Let them sit on the banks’ balance sheet. Next up is scrapping the conventional loan limit.

Exactly. Isn’t it in the GSE charter somewhere that their goal is to promote home ownership? How does getting into 2nd lien borrowing do that?

“scrapping the conventional loan limit”

The limit has been so grossly inflated already that it is fairly meaningless as an actual constraint.

Expect inflation to skyrocket, especially in services. No one involved in policy making cares; Well, at least the overwhelming majority of policy makers don’t care.

I had a HELOC from #$% @2.74% for 6 years then had a heart attack. Those people are ruthless, no-good bustards. They called every few hours for their payments. Problem was it wasn’t due for another 8 days, didn’t stop them. After I healed a year later I was determined to pay them off. Pandemic hit and off we go sales exploded. Last march I paid it in full. They tried not to close my line of credit. It took me 6 tries,finally received my satisfaction and they still called me to reopen.I just replied FUCK YOU!!

“A banker is a fellow who lends you his umbrella when the sun is shining and wants it back the minute it begins to rain.”

— Mark Twain,

Today’s bankers just lend you somebody else’s umbrellas and outsource the umbrella repossessions.

And that is just one small division of the bank. (especially big 4…5?)

I just gave my teller today a 10, and they wanted to transfer me to some data collection outfit for further inquiry into her usefulness to them.

No thanks, but I hope she got the 10, anyway.

Robert Frank Walker

Who were the bankers?. I want names.

Their names are Legion.

I didn’t go that far but wanted to… out of curiousity, I filled out request for HELOC pricing at Discover. It came back at 9.50% so of course I just exited. Then I got a barrage of mail (the post office kind as well as email) congratulating me on obtaining the loan. Two points: lenders are not only nasty and relentless, as you say, but also so greedy it makes your teeth hurt. I did write to them via snail mail to say I had NOT applied, just inquired. .

Second, Discover was easily able to find out all kinds of personal info, including who holds the exiting mortgage, current valuation (not Zillow), etc. No privacy at all. Starting to appreciate the conspiracy theorists.

“Second, Discover was easily able to find out all kinds of personal info, including who holds the exiting mortgage, current valuation (not Zillow), etc. No privacy at all. Starting to appreciate the conspiracy theorists.”

Most property records are public info, and your mortgage servicer is probably listed in your credit report.

If you’re concerned about identity theft, you can freeze your credit with the three reporting agencies.

How about letting the financiers put their own money and risk on the line if this is such a great business idea?

Of course not! When there’s an opportunity for passing the risk on the government needs to get involved to make sure that Wall St. can’t lose.

I’m as convinced as ever that the fed gov’t needs to get out of the residential mortgage business altogether. 30-yr fixed rates at ZIRP levels are already going to keep prices inflated for far too long. Housing is a necessity and we can’t pretend that we’re doing anything to help that notion when the ones writing mortgages can have zero skin in the game.

Banks can make their own mortgaged-back securities. So have the federal government get out of the business and pass a simple regulation that says only MBSs that meet minimum standards, say no more than 3 times income or whatever, can be rated A+, and everything else has to be rated B & below. That will cause banks to have to keep their bad mortgages on their own books because they will find it difficult to pass off their garbage onto others.

Sounds nice but it actually won’t work. Banks will use their “personhood” to corrupt Congress to get rid of these needless regulations that stifle American ingenuity.

Ever heard of a corporate lobbyist? Who do you think runs your (programmed general dislike) for OUR democratic government attempt….the people?

My uncle “owned” at least one well known Senator and a collection of lesser government and military players, on behalf of a HUGE defense contractor you probably were invested in.

Money is speech, ya know?

Wonder if that definition of money made Wolf’s Random House dictionary?

Probably not…doesn’t fit a lot of American Myths.

In Canada HELOC debt is still steadily rising. Scotiabank still sticks with the same motto – “you’re richer than you think”, allowing customers to access more credit and take on greater debt. It should be mentioned that federal government’s enjoy the claim of a population’s high net value (bolstered by mythical/ not realized real estate paper gains on an overly inflated market). The consumer debt ratio in Canada has been at risky levels even before covid; they’re even worse now. There’s also the topic of reverse mortgages; pay on the way up – and a deferred compounding payment on the way down (when estate is sold, no inheritance?). The OSFI made it policy last November that regulated lenders will have to comply with a “certain percentage” (number not disclosed publicly) of the lenders entire mortgage portfolio of non insured mortgage loans will need a LTI (loan to income) ratio not exceeding 450%; Seems like the most risk publicly and privately is in insured loans (guessing the government doesn’t want to tighten up mortgage credit – even though they should in order to deflate the bubble).

Scappy Doo: was this a misprint (450% LTI?) Banks traditionally did 35% gross income for mtge payments and a total 43% of gross income for mtge and ALL OTHER DEBTS (credit cards, car loans, etc)

It says 4.5x income when I googled it so it appears that is not a misprint. I assume that the loan total is 4.5 times your yearly income. Seems…..okay?

I agree this housing market is due for a reset. I’m blown away at some of the new tract home prices I’m seeing in the Chicago suburbs. Over $900,000 for a two car garage Pulte home! SMH

The problem is, the housing market has been desperately due for a reset for years now. And the reset never comes.

If its in the Chicago burbs – omg what are the property taxes on a 900k new build? (also – they are only going up)

If you absolutely must build in a Chicago burb, then get it via small one-off builder. Big basement does not count towards prop tax square footage. Buy/bring your own high-end electrical fixtures, etc. not included in purchase price. Disclaimer: this is strictly hypothetical, of course.

My grasp of demographics is shaky, but I’m wondering when the gen-x or the millenial parents will have to figure out how to pay for the kids’ educations and the parents’ medical bills. That might drive a lot of otherwise sensible parents/children to overexpose themselves to debt.

Its all part of a big cycle. Since the turn of the century ( 1900. not 2000) or earlier and the greatest and most dynamic industrial and agricultural economy in History. We literally invented and implemented most of what makes up modern industrial civilization.From the power grid, to assembly line manufacturing, to air conditioning, to machine tools and computers. This resulted in the largest store of wealth and value ever recorded.

Up until about 1980 it was the job of the finance industry to assist, inventors, farmers, miners and manufacturers to develop this wealth that created the worlds largest ( at the time) middle class. But after that, growth in the real economy began to falter so the finance industry reinvented itself to strip-mine all this value that had been created over the years.

They started in on the older industrial companies, picking their bones clean and leaving crumbling smokestacks for the now Pension-less employees to gaze at. They moved on to everything else, culminating in the strip-mining of the homeowner. This latest scheme is probably their final act to pry the last remaining coins from the sofa cushions of what remains of the middle class.

Hubberts – very well-said. (…sounds like the ‘financial industry’, well-before ‘AI’, met its singularity-the tool fancying, and then actually achieving, more importance than the mission of our general citizenry’s national weal (too-often able to deflect real scrutiny with a ‘who knew’ or ‘this time it’s different’ (usually in an elegantly-dressed, stentorian voice) public arm-waving. Can never thank Wolf (and many of the commentators) enough for the dogged devotion to manning one of the scarce, and mercilessly stark, spotlights upon it…).

may we all find a better day.

So well written, HC, but that colossus that you describe as metastasizing from a economic participant into a gargantuan raptor is largely an unfair depiction. (I hate like hell defending finance and their minions, but…) Wherever there’s been currency, or any medium of exchange, there were those who labored in the business of extracting income from that very medium. It was going on long before the birth of Christ. Laws against usury were created to try to rein in the most heartless, but for those who could live off of it, they did.

Making money off the money itself wasn’t limited to the industry of “finance”. Companies that produced goods were finding that financing the sale or use of those goods was an additional way to make money on their own products (e.g. G E Capital, Ford, IBM). Ransom, extortion were just further out on the money for nothing spectrum.

I just can’t demonize people or an industry that “lives off the fat of the land” like financiers do. Unless egregious, isn’t it due to simple jealousy?

But I do think that, in a civil, enlightened society, those who are easily exploited should be protected and the only line of defence is the government.

defense… And the jealousy is us feeling that the financiers are making gobs of money while we get left holding the empty bag.

How – I take your point, my friend, but so much of it amongst management of what were formerly ‘productive’ industries sounds more to me like the old case of: “…if you can’t beat ’em, join ’em…” (…meanwhile the thoughtless looting of the spacecraft’s LSS by the ‘tools’, and the rest of us, continues apace…). Best to you.

may we all find a better day.

Is HELOC interest tax deductible without any use restriction(s)?

HELCO interest is deductable only if used for home improvements.

Re: :tappable” home equity after years of surging home prices”

This topic resonates and connects to my latest hot button, which is the concept of inflation hedging, especially with homes.

In the big picture, finding assets that generate cash in inflationary periods, seems very suspect, because, as an example, after the pandemic hit, obviously house prices exploded to generational fantasy levels, but, with the everything bubble, everything went up.

It seems to me in retrospect that the assets hyped as being inflation hedges, contributed and amplified to the growth of inflation.

I’m not a big fan of Case Shiller inflation adjusted pricing, but at least that’s a measure of how inflation can influence prices on assets.

Nonetheless, all the inflation hedging assets exploded in price, making them all into overvalued assets, which now, seems to have them all at levels that will decrease in value, especially with an impending recession eventually unfolding.

Houses are unique because an owner can rent the asset and generate cash flow, but even that game has changed because of inflation adjusted house prices and the reality that renters can only afford only so much per month.

The doggie asset of gold is now suddenly attractive bait that sucks cash into a pointless black hole, magnetically drawing in suckers who think it’ll protect them from inflation — but speculators buy at inflated high points, once again, making the asset overvalued and likely to devalue.

In terms of cashing in on home equity MEW, same thing, houses exploded and people get conned into robbing themselves and placing themselves into situations that will end up diluting their ownership — especially when there’s repricing of their inflation proof asset.

Inflation plays a unique role in bubbles and one of the main functions it provides is the process of burning up mis-allocated cash.

I’m still trying to figure out what an inflation hedge is…

“I’m still trying to figure out what an inflation hedge is…”

How about taking out a low, fixed-rate loan to buy a solar system that generates 120% of your annual electric use.

By replacing my (variable) monthly electric bill with a (fixed) loan payment, I’ve eliminated my exposure to rising residential electric prices.

“How about taking out a low, fixed-rate loan to buy a solar system that generates 120% of your annual electric use.”

I had to read this three times before I realized you meant a system of solar panels! A “solar system” in other contexts refers to an entire star and all its planets…

Andrew P – I dunno, suspect a large number of us would be attracted to being the master of a small chip of the universe (…apologies to friend MM, I couldn’t resist…).

may we all find a better day.

The only reason a boomer should take out a second mortgage is to help their children or grandchildren buy a home of their own. It can be a struggle to save that 20% down payment for anyone who has student loans. Borrow more than 80 % and you get trapped into that PMI scam.

MW: Roaring Kitty is back, and GameStop stock is rallying. The company still is struggling to make money.

GameStop shares are up 51% after Monday’s opening bell…

Markets (of all kinds) saw the fear in the Fed’s eyes in early 2023, and have been responding appropriately–by rallying–ever since. Nobody should be surprised by any of this.

I bought my first fixer upper home in 1967 and paid about 12% due to my age and the house. Then came Nam and serious inflation.

The young whiners are about to get a taste of the real world and do not have a clue how easy they have it.

Worked hard and made some money! It’s my money and I am going to spend it any way I want it.

Howdy Bear Hunter Fixer upper / Starter home terms are offensive and not used by the youngins.

“The young whiners are about to get a taste of the real world”

My parents, and their parents probably said the same thing about the next generation as Papa ploughed the the lower 40 with the ox, grandma in the kitchen canning some peaches and tomatoes, and mama hanging up clothes to dry on the line, and me, cleaning out the fly infested shitter.

Most youth learn quick when need be, others – like myself – need a 2×4 upside the head.

“the line” – hey kids – want to see a solar clothes dryer!

Bear – …more like: ‘…paying for ‘Nam…’ (we started kiting the financial checks AND cashing the human cost ones well before ’67…

may we all find a better day.

So simple….but it requires the admission that most all the great leaders of the greatest country in the world simply FD up….and extremely badly.

Wolf – Mortgages usually prohibit junior liens. How does the second mortgage industry propose to get around this? Will the first mortgagees routinely give their consent to second mortgages, as they do with HELOCs?

Howdy WB2. In the olden days, you could easily get a HELOC for above your homes value/equity. 10 to 20 % more was common. 2nd and 3 rd liens get 0 if nothing is left after the tax man and the 1st lein.

You do not need to get consent from the first mortgage lender to get a HELOC or second mortgage. The first mortgage is still first in line on claim to the property. You may be thinking of subordination, which happens when you refinance a first mortgage when there is a second mortgage in place already.

“It’s Deja Vu All Over Again”

― Yogi Berra

I think I have seen this before!

Home values go up, some people borrow against their equity…

– some of them finish their basements, put in a pool, build a huge deck.

Home values go down.

Some people lose jobs.

The overleveraged try short sales, then first mortgage holder forecloses and 2nd mortgage holder negotiates down to pennies on the dollar.

That pretty much sums it up. I’m trying to figure out if we’re in inning 4 or 5 of this new game.

Difference now is those of us patiently waiting for the deals are competing with Wall Street during the feeding frenzy

Anyone can print credit by promising to create something of value in the future in exchange for something now. Only performing some unit of work can have real value. There are too many parasites trying to extract value without doing anything. Also, too many people making promises that cannot be kept.

Timely article. Been reading many articles in the past 2 weeks about how this home equity is going to save the world as economy slows. There is even one on the front page of Marketwatch this morning. Cheerleaders out in full force.

Our home equity has always been sacrosanct. There is nothing I need that would cause me to violate that. As health or life stages evolve, that may change. But we don’t need the house equity because we planned for life.

One of the examples above was to borrow against your house for a wedding. Nothing could be more stupid. If your ego is that fragile that you’d risk your future for a one day party, you need to seek help.

ElK – but, by gawd, it’s easy to sell…

may we all find a better day.

My thoughts exactly but i try to practice minimalism.

Home equity loans are retirement suicide. Don’t do it! You will never be able to retire. Your mortgage should be paid off before you retire. Home equity loans extend that payoff time into well after you should retire. Home equity loans are pure evil.

Howdy Homer. Sorry, but not at all for some folks. HELOC s can be $$$$ makers.

Wolf, as usual, is 100% correct.

We had an open HELOC – could draw on it if we needed to do so … but we didn’t (until we sold our house) – so we only paid the annual fee.

When we sold our home and bought a condo we used the HELOC as a ‘bridge’ loan, instead of having to look for one while we in the midst of moving.

And, yes, the bank made us pay interest on our home equity.

Yes that is a great strategy. Can’t tell the HELOC lender you’re selling, though. Disclaimer: this is hypothetical, of course.

Howdy 3 % ers. Now just imagine if all those prisoners started that small business or how about The Lone Wolf telling you MA and Pa love second homes and rent them out. HELOC your way to prosperity? I doubt the youngins have the guts……..

That’s because the young’ins understand that 50% of all small businesses fail in the first year. So if you fail at the business, you also lose your home.

Guts are beside the point. Common sense and an understanding of risk win the day.

Advocating using home equity for a business is reckless.

But then you are a squirrel. I see lots of squirrel roadkill while driving around.

Howdy Outside TB Lots of different road kill everywhere. In Florida the road kill is alligators and crocodiles. Entrepreneurs are few today?????

No guts, no glory.

Wolf,

Does this have 2008 Mortgage Meltdown Part 2– The Sequel! written all over it?

Mortgages don’t melt down until prices melt down. The problem arises when borrowers who have trouble can’t sell the home because the mortgage balance exceeds the home value. We’re far from that for most homeowners.

Seems an odd way of thinking to me. I have a lawn mower worth £70 in my shed but I don’t stare at it in frustration thinking “there’s £70 value in that lawn mower but I can’t get at it.” I either decide to have a lawnmower or £70. As the article says, if the homeowner wants to get access to his equity, he can sell the house :)

Rent out a lawn mower hourly like a cab. Renters can run it 24/7.

That idea has already been had by equipment leasing companies.

Endless credit bubble.

Wolf, There have been numerous articles lately saying prices are not going down. I know you’ve shown that’s not true in all areas esp with new home prices. But their theory is that it’s simple supply and demand. Builders didn’t build during the pandemic and now we have a bigger shortfall. And this latest dramatic price increase is totally different than 2008 for numerous reasons including the types of loans and the creditworthiness of the mortgagees. Can you please address why you think this is wrong? We are trying to figure out whether buying now makes sense. I’ve read many of your prior articles so I know you don’t agree overall. But what do you think about supply and demand argument? And the different kind of loan situation now versus 2008?

Lots of supply already on the market and more coming on the market. Active listings are the highest in years, in terms of existing homes. And inventory of new single-family houses is the highest in 15 years. Homebuilders are out there making deals and buying down mortgage rates. Don’t let this shortage BS get to you. However, prices are too high (though in many markets they’re lower than they were), and that’s the problem.

In terms of your personal life, you do what you need to do to get on with your life. This website is not a personal advice column. This site is about business, finance, and munnnneeee

We’ve talked here a lot about people “trapped in their current houses” by interest rate differences between old & new mortgages. But there’s another “trap”: capital gains taxes on gains > $500K ($250K for singles). The current property bubble has “gifted” a lot of people a hidden tax time bomb. Is there a cottage industry of converting primary homes to rentals to avoid capital gains?

Howdy Bagehot’s G. If the profit is reinvested in another home. Lots of Legal ways to avoid gains.

This second-lien refi thing means that in a year or few, we’ll start getting some fantastic sob stories from low-equity “owners” of higher-end (California…) houses. Some people who are forced to sell in a time of declining equity prices will get a triple-whammy:

1) have to pay the lender in order to sell, due to negative equity after cash-out refi…

2) have to pay significant capital gains tax … due to property value inflation

and 3) forced downsizing due to much higher interest rates and lack of down-payment money.

Wouldn’t that mean these folks are forced to stay and can’t sell?

What could possibly go wrong with the US taxpayer footing the bill on any losses? In 2008, the federal government took control of Fannie Mae and Freddie Mac—leaving taxpayers on the hook for any potential losses.

In order to qualify for one of these second mortgages, the first mortgage must also be a Fannie Freddie loan. How many of the outstanding mortgages are Fannie Freddie? I don’t know.

The bad news is you only need a 580 credit score to qualify for any Fannie Freddie loan in the first place. Funny how taxpayers are on the hook for such high risk loans. So, Llet’s help those sub prime borrrowers tap even more equity to give the economy a much needed boost, since it’s clearly damn sluggish, eh?? lol. Cash outs could fuel more inflation, what do you think Wolf?

I think this is a terrible idea and citizens should be strongly opposed to it. Gov’t backing is partly responsible for housing being too expensive so the USA needs less gov’t backing of mortgages, not more. It’s just another scheme to keep the bubble inflated which messes up the market, making it an even more manipulated, unfree market than it already is.

See latest Planet Money Podcast

Zombie 2nd mortgages are coming back to life

MAY 10, 20246:25 PM ET

10s of thousands of homeowners current on 1st mortgage getting debt collectors calling on 2nd mortgages they thought were forgiven. Investors bought up the bad 2nds during GFC and waited 16 years so houses are above water again and now trying to collect and sometimes foreclose.

I don’t understand the hysteria from many here re these 2nd mortgages. Lenders are providing a service at a risk to allow homeowners to tap some equity within their real estate. And since these 2nd mortgages are presumably subordinate to the primary mortgage, both the lender (of the 2nd) and the homeowner can incur losses if the value of the home drops. So both parties are taking a meaningful risk. But the alternative is excessive regulations… Do we want to be coddled by big government?

You must be one of those rugged individuals like on the naked reality shows. But were you coddled by an entire camera crew?

Or did you have to hit the ground ready to fight with zero help?

I guess there is a sure cure for paying fees and interest to evil lenders on your own “money”. DON’T DO IT.

I can see where this would give these non bank entities an opportunity to market to homeowners, but what advantage would the home owner gain when they can pay no fees to close a HELOC? The rates are similar, so unless you are willing to bet on rising rates, why lock in the rate on a second lien AND pay fees to do it?

No secret here.

The answer lies in the Basel-III regulations for banks (which the banks fought tooth and nail but had to swallow after they misbehaved that badly in 2007/08).

For a HELOC, they’d have to put more capital aside as a risk buffer because after all, it’s a loan.

For a second-lien mortgage, not, because after all, it’s a mortgage, and who the hell doesn’t pay their mortgage (that’s a quote).

There’s your answer.

Both have a second lien on the home, no difference. HELOCs are vastly more popular than second-lien mortgages. The difference is that a HELOC is a line of credit that the borrower may draw on if they want to, and payments vary with the amount borrowed. A second-lien mortgage has fixed payments over a fixed term.

I assume if paying for medical care is the issue, the HELOC is the way most people would go. Given that medical debt is one of the big reasons people go bankrupt, I assume that many are going to tap into their home value if they think they can avoid bankruptcy.

As I understand it : Depending on which State you live in, this might not be a good idea as most states at least shield part of the value of the primary residence in bankruptcy.

Yes, once you start thinking about defaulting on debt, HELOCs complicate the matter. If you take out a HELOC to pay for medical debts, you’re converting an unsecured medical debt into a secured housing debt. Depending on your personal financial situation, this may be a low-risk or high-risk situation.

If I were a first mortgage lender, wouldn’t I have one of my terms limit the borrower’s ability to add second mortgages to the property unless permission granted in writing?

In the event of a HELOC default but first mortgage is OK, what if any rights does the HELOC lender have to foreclose against the collateral?

I would think that this might be a very sensitive subject area for lenders in these times.

This is what it’s called debtor in first possession. Other than the government doing a tax sale, any debtors that come after can’t force a foreclosure until the debtor in first possession no longer has an interest. This is part of what puts second mortgage lenders in a riskier position.

Is the ability of the lenders to know they can sell out to a government backed entity partially causing higher interest rates? They have to make them 2 to 3 percent higher than treasuries in order to make them attractive though to be bought by the government backed entities? I also wonder what happens if you go back to just the bank writing and holding mortgages. I want to say it’s time to bring an end to Fannie and Freddie, but I don’t know exactly what would happen to the market.

The premise of the article is absurd in this and any other context in a non-zero rate environment. If you borrow against your stock portfolio for example, you get charged interest because you still own the shares and you’re pulling cash out at the same time. You still own your home 100% with a mortgage whether you pull money out of it or not, so if you want the cash you’ll pay a bit for the privilege, with the house just serving as collateral.