They partied most at Restaurants & Bars, and at ecommerce retailers. If I hear one more time consumers are “tapped out,” I’m going to scream.

By Wolf Richter for WOLF STREET.

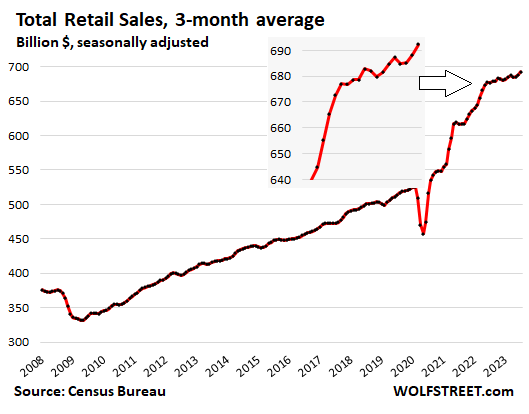

Retail sales, including at food services and drinking places, jumped 0.7% in July from June, after the upwardly revised 0.3% increase in June, and the 0.7% increase in May. Compared to a year ago, retail sales rose 3.2%, seasonally adjusted. Not adjusted, retail sales were $703 billion in July.

The growth in retail sales came despite a sharp decline of inflation in the goods that retailers sell, such as motor vehicles, gasoline, electronics, etc., with some actual price declines. And it came despite the shift of spending from goods – which is what the retailers here sell – to services.

This growth in July from June was driven by the huge growth rates among the #2 and #3 largest categories of retailers:

- Nonstore retailers (mostly ecommerce): + 1.9%

- Food services & drinking places: +1.4%.

Retail sales are not a measure of consumer spending. They’re a measure of how well retailers are doing. We track consumer spending separately, which also includes services, which retailers don’t sell, and it’s adjusted for inflation.

The charts below show the three-month moving average to squash the artificial drama of the monthly ups and downs that can obscure the trends.

The three-month moving average of retail sales rose 0.6% from the prior month and was up 2.3% year-over-year:

Retail sales by category, 3-month moving average, seasonally adjusted.

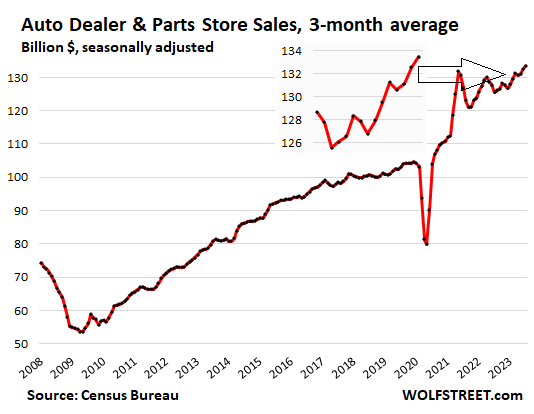

New and Used Vehicle and Parts Dealers (20% of total retail sales):

- Sales: $133 billion

- From prior month: +0.7%

- Year-over-year: +6.3%

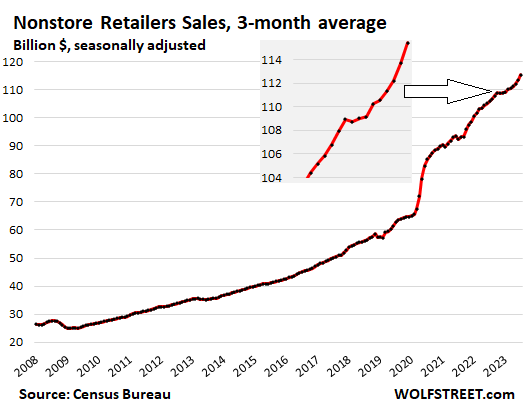

Ecommerce and other “nonstore retailers” (17% of total retail sales), ecommerce retailers, ecommerce operations of brick-and-mortar retailers, and stalls and markets:

- Sales: $115 billion

- From prior month: +1.5%

- Year-over-year: +9.0%

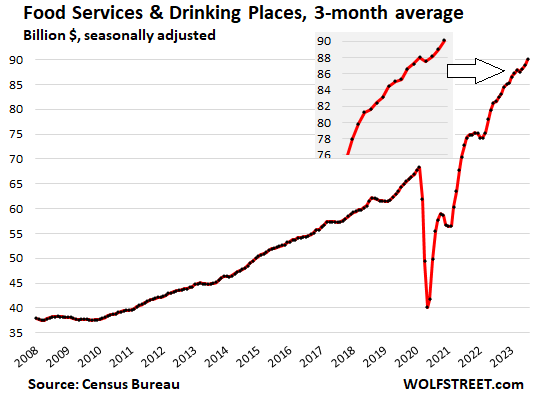

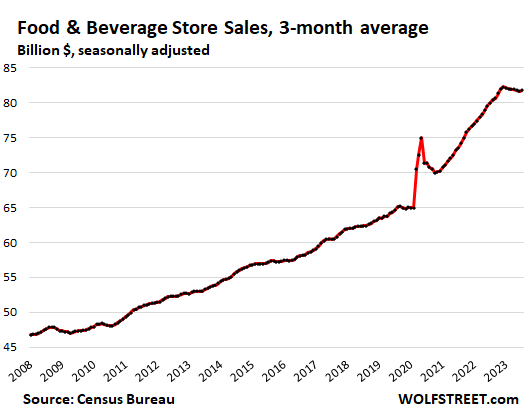

Food services and drinking places (13% of total retail), includes restaurants, cafeterias, bars, etc. Americans are spending more here ($90 billion in July) than at grocery & beverage stores ($82 billion, next chart down):

- Sales: $90 billion

- From prior month: +1.2%

- Year-over-year: +10.4%

Food and Beverage Stores (12% of total retail). Sales leveled off as grocery prices leveled off at high levels in recent months:

- Sales: $82 billion

- From prior month: +0.2%

- Year-over-year: +2.2%

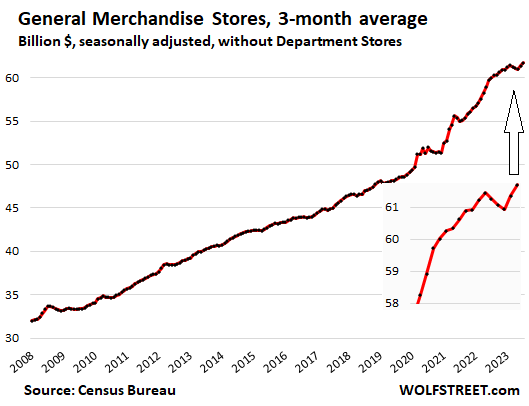

General merchandise stores, without department stores (9% of total retail):

- Sales: $62 billion

- From prior month: +0.5%

- Year-over-year: +2.8%

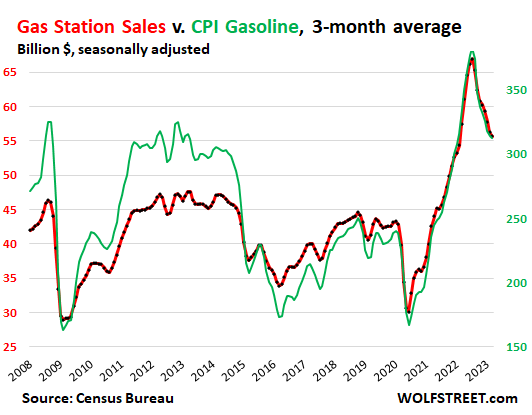

Gas stations (8% of retail):

- Sales: $52 billion

- From prior month: -1.3%

- Year-over-year: -21.7%

This chart shows the CPI for gasoline (green, right axis) and sales in billions of dollars at gas stations, including other merchandise that gas stations sell (red, left axis). Changes in sales are mostly driven by price changes, not because people drive more or less:

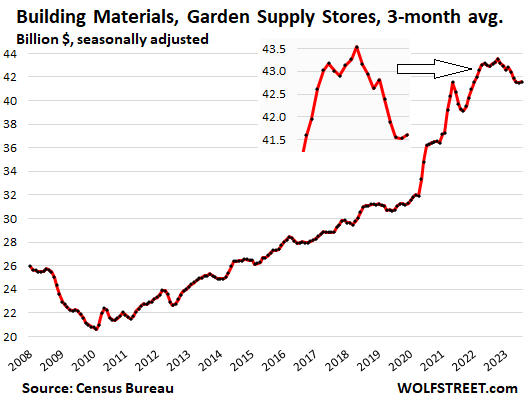

Building materials, garden supply and equipment stores (6% of total retail):

- Sales: $42 billion

- From prior month: +0.2%

- Year-over-year: -3.0%

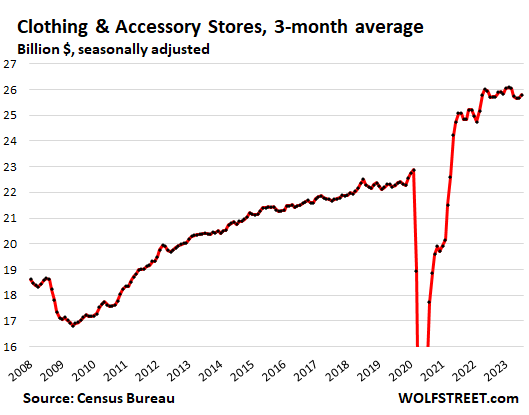

Clothing and accessory stores (3.7% of retail):

- Sales: $26 billion

- From prior month: +0.4%

- Year-over-year: +0.4%

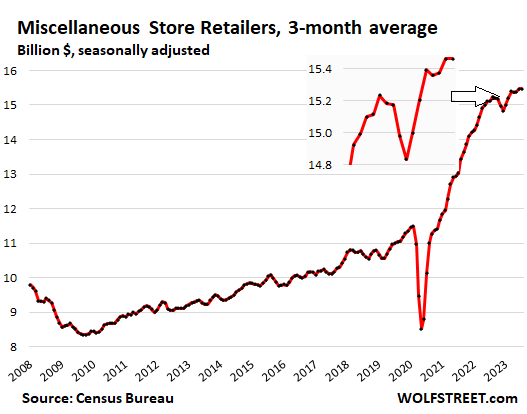

Miscellaneous store retailers, includes cannabis stores (2.2% of total retail): Specialty stores, from art-supply stores to wine-making supply stores.

- Sales: $15.5 billion

- Month over month: +0 %.

- Year-over-year: +2.3%

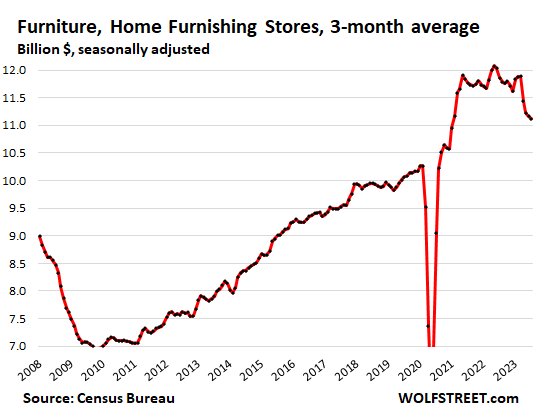

Furniture and home furnishing stores (1.6% of total retail):

- Sales: $11.1 billion

- From prior month: -0.4%

- Year-over-year: -6.2%

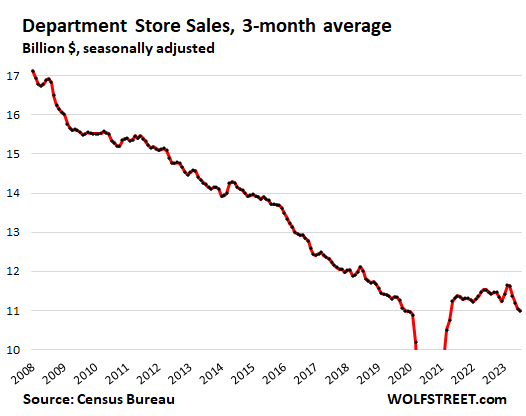

Department stores (1.6% of total retail sales, down from around 10% in the 1990s). Online sales by department store chains are included in the ecommerce retail sales chart above.

- Sales: $11.0 billion

- From prior month: -0.4%

- Year-over-year: -4.1%

- From peak in 2001: -40% despite 21 years of inflation.

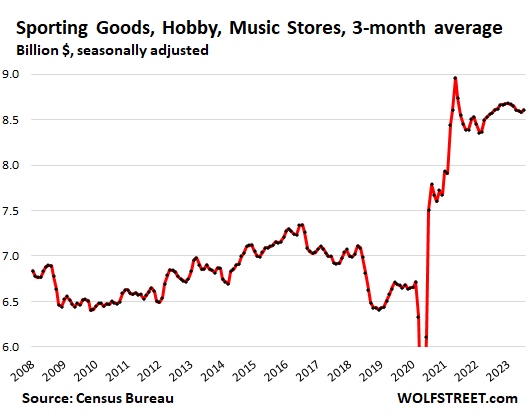

Sporting goods, hobby, book and music stores (1.2% of retail):

- Sales: $8.6 billion

- Month over month: +0.4%

- Year-over-year: +0.4%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Here is what is one of the reasons causing inflation.

“

Digger Dave

Aug 15, 2023 at 7:07 am

The people who are sitting around with $300,000 in savings, after previously earning zilch for far too long, are not awash in inflated earning. This is not PPP money or any other pandemic stimulus – it is a reversion to mean for people that live and save conservatively. Yes, after waiting many years of having no spending power, surely some are spending this interest income.

Sure some of it is from sales of inflated assets, but people who played that game are largely not conservative financially – it’s hard to imagine that they are just sitting on this money in insured accounts en masse. Plenty of them are full of themselves and vision themselves as great investors, so they continue plowing on and paying slightly less inflated prices for new assets.

Wolf hits on the fact that a lot of inflation is driven by mindset, such as FOMO. You can’t believe that a decade and a half of very loose monetary policy and the effects of that policy will suddenly turn reckless people into savers.“

Another interesting tidbit which is causing inflation. I spoke with several people living in US and Europe, who echoed the same thing that they have grown up kids, some even engaged or married, but live with them, because the rent is too high, or/and they cannot afford to buy a house at these prices and interest rates And their only chance to have a house is inheriting it from their parents, so these people are also spending a lot as they do not see an opportunity to buy a house in the income/price/interest rates which they have, so why save, might as well spend and enjoy.

.

There parents are irresponsible,should charge them rent in proportion to there income ,then in 5 years or when it is feasible have them buy a house .At which time parents give them rent money back .

That’s what we do, it gives them some financial responsibility, but you have to be strong to enforce it and send a monthly ledger. We don’t tell them that they will get it back later either.

Something tells me the purchasing power of folks living with their parents due to soaring rents is an inconsequential driver of inflation relative to, you know, soaring rents.

My wife in the 60s paid rent to her parents and our daughter paid rent to us in the 90s. Anything less is a disservice to all concerned.

Why is this what you believe?

I grew up dirt poor in the coal fields of western Pennsylvania and was the youngest of 6 kids. We all graduated high school and buy the 4th of July we were all out of the house and on our own. My Dad said his job was to get through school and after that our life was our own. Four boys and two girls we all did ok in life. Our lives was a walk in the park compared to theirs.

But the real question is….are they incurring credit card debt in order to.spend. What about student loan payments?

lol. Repayment of student loans is the running joke here on wolfstreet.

“…so these people are also spending a lot as they do not see an opportunity to buy a house in the income/price/interest rates which they have, so why save, might as well spend and enjoy“

here we go again … all of these people growing up getting participation trophies and never having to really compete. ‘life is just so hard, and i’m feeling sorry for myself and won’t even try’.

that’s a great way to think for anyone who wants to spend their life as wolf food. hey enjoy being a sheep.

Agree with this partially and certainly for t he ones who are doing what Digger Dave mentioned, ie. just throwing up their hands and spending with abandon without saving. Problem is we’re also seeing a lot of financially responsible Millennials and Zoomers–more than almost any Boomer we’ve grown up knowing–who work very hard (with side jobs), are well educated and trained and saved, but still can’t afford homes or rent because the inflation and costs are just so outrageously high, even outside of major markets.

The reality is that home and rental costs in 2023 are proportionally much higher relative to income than they ever were for Boomers, so even professional, hard working and more frugal young people are being locked out. If we want these people to move out and buy their own homes, and this is a goal we should support, then it’s simple, this outrageous housing bubble has to pop and homes and rents need to become more affordable relative to actual incomes. Yes some young people have been profligate and that’s a problem, but others have worked and saved, and here, it’s incompetent Fed policy with ZIRP and QE (and loose monetary policy for several decades) that’s the problem.

You completely missed his point. Congrats. It has absolutely nothing to do with participation trophies.

It has to do with the fact that there has been a shift in cultural attitudes and spending. How much of this is due to crazy housing costs is certainly debatable, but I am quite sure that housing costs have had more of an effect than participation trophies (LOL)

Just yell at the kids to get off your lawn.

I wonder what percentage of retirees will discover that the interest income pushes them from drawing their social security tax free to it being taxed. You can get into a zone that every $1.00 of income it nets out $.50 – $60. Its a convoluted calculation, but it is roughly $50K – $70K gross income zone for a single person.

How is this different from Feudalism? We have an extractive Rentier class who has pulled the ladder up and everyone now must pay them for anything.

Why have kids if they will be a burden and will have a worse life than their parents?

Things must change, or else!

I don’t know where you’re seeing “cooling inflation”.

Scream at me if you want, I can take it, but I am having a tough time reconciling all this. Can you post another article like this? They used to be regular. Someone else mentioned this and I added a request, but do not know how to search this successful ongoing book notion of yours.

https://wolfstreet.com/2022/12/21/fed-tightening-reduces-horrendous-wealth-disparity-that-qe-and-interest-rate-repression-have-wrought-fed-data/

Yes wealth inequality is my obsession, just like climate change, yes I understand why “criminals are criminals” in this society, and I know little to NO economics….the only place I care to get a picture of things in the Econ world view is HERE…..along with some sociology on med high net worth (high middle, upper middle, class and a bit above?) No way to tell except reading comments and interpolating…..a shaky methodology to be sure. Kaplan in “Methodology of Inquiry”, said you cannot avoid bias, best you can do is admit what you are aware of. Took a damn long time to do it, too, but how much can you sell aphorisms for, unless you have a mass of them, like Nietzsche?

Hmmm your failure to reconcile is on you and your inability to overcome your biases. Not Wolf.

I think his words are fairly clear and easy to understand.

Of course you posted on an earlier article about rising insurance rates being the fault of democrats, just proving you have lots of biases preventing you from seeing things as they are.

Hmmmm……(is that the code for hard/clear/unbiased thinking?

You must be a modern day polymath.

Anyway, yeah, and I continue to believe health care and health insurance is supported by democrats because of donors, (ACA instead of single payer when they easily had the power to do it? Think!), like I believe fossil fuel and chemicals are GOP donors which they therefore support.

I try harder to see “things as the are” than you do, that’s for damned sure.

Let’s hear YOUR present world view……or is your function just to admonish “failures”like me?

I don’t know why I even answered a poorly designed insult.

hot dang…guess that SOB Pow Pow is going to pull off no landing scenario..who would have thought…maybe he is one of the best Fed chairman yet in the last 3 decades

Did u forget TRANSITORY. Best lie in history,

Error. Not a lie, an error. Being wrong is not the same as being malicious.

EXACTLY!

“Error” my ass!

No one’s perfect. Present company included. You don’t manage the largest economy in the world without making misstatements and under/over-reacting from time to time. But as Phoenix stated, he’s done a pretty damn good job of not sinking this economy which is more than can be said of our previous few Fed presidents.

i dont think you caught the massive *SARC* in phoenix’s post..

and he hasnt sunk the economy.. yet.

it remains to be seen what the ultimate results will be.

and what is this about ‘managing the largest economy in the world”?

this isnt the USSR. the fed ‘manages’ monetary policy, not economic policy, like.. say, how many automobiles get produced in a year.

the combination of monetary and fiscal policy are what cause the economy to expand or contract. you are attributing too much power to a single entity (the fed) and a single individual (the chairman) he is not a dictator.

I am pleased by Powell and the Fed. I wonder if the ‘transitory’ wasn’t just so they could be certain the economy got going and didn’t slip back.

BlackRock’s basecase from here is full employment stagflation for the next year. They also prefer to call this a structural change and not an economic cycle because of the shrinking labor force.

what we see ourselves and what we hear from friends and neighbors is its “balls to the walls ‘ spending !- with extreme spending applied to travel including europe and vacation homes – its FUN out there no end in sight! enjoy !

(Looking at my mortgage origination pipeline)

(sighing)

They sure aren’t buying houses, that’s a fact.

I have a friend who has been an LO for 23 years. He’s been working other jobs all year long. He said the top 10% of LOs with deep relationships with the top 10% of producing realtors are eating all the pie that’s available right now for home sales. He seems to think it will be late ’24 or early ’25 for some normalcy to come back to originating.

A 50% correction in real estate prices would bring back some normalcy in both transactions and lending

Yes, there’s too much whining from some of the wonky types about dreaded deflation when talk about lowering home prices and rents comes up, forgetting that this would be on heels of massive inflation for 2 years. Even with a major drop in real estate prices there’d still be overall inflation, it’s fine to have some deflation specific to sectors that are in bubble territory and it’s a needed correction.

We can’t afford the damn houses. So we console ourselves with spending on other crap, I guess.

Sadly, the days when skipping the avocado toast and coffee out would make any meaningful difference are long gone.

We put our lives on hold for three years. We’re now tapping all available resources to try to make up for lost time, recover some of what we lost, and have some feeling that our lives back to normal. If it costs more to do that, the attitude is basically, f*** it. Life is short and sucked for far too long. We see things are still not fully back to normal, but we’re tired of waiting. Sell assets, borrow, pay whatever it takes. We’re done. We’ll do it until we can’t and cross our fingers. Plus, it may ultimately be someone else’s problem. If/when it is, the Fed will bail everyone out anyway.

You forgot “WAGES.” The Biggie!! Record number of people working, making record amounts of money, and getting the biggest pay increases in 40 years. That’s where this money comes from.

People always pooh-pooh the employment data from the jobs report, unemployment claims, JOLTS, ADP, from whatever, and they say they’re all fake, and the labor market is in a deep depression, and then they’re stunned when they see that consumers are spending these huge amounts of money, and they wonder where it came from. Well, it came from the employment numbers these folks pooh-pooh every day 🤣

Normally these increased wages would be spent on getting a bigger house and a bigger mortgage. But that market is frozen. So the money gets spent on travel, goods, and services. And it prevents people from gambling on that asset class so you have the decrease in mortgage delinquency. No mysteries here.

Yes, this is one of the longer term costs of dumb and short sighted ZIRP and QE policy by the Fed (with the criminal negligent purchases of MBS’s) and fiscal over-spending to fuel consumption, even before the pandemic. A real estate market so distorted that even good earning young professionals are stuck living at family homes because the rent and home prices are so outrageously distorted by the flood of over-printed money and inflation.

All while the US life expectancy nose dives more and the US birth rate falls to the ground. We know a lot of very successful American young professionals in this situation, did all the right things but still can’t afford homes due to the Everything Bubble compared to their Boomer parents who could afford a decently nice 2 or 3-BR starter home on one high school dropout’s salary working on an assembly line. The cost of homes relative to income actually made sense back then. And I’d bet this is a huge source of the resentment boiling over for young Americans these days.

America is a whole new paradigm compared to Canada.

15-year-old teenage burger flippers get paid USD$20/hr, while thousands of middle-aged finance and IT professionals send resumes for CAD$15 (USD$12) job positions requiring a few years’ experience.

Those teenage burger flippers still face soaring rent prices in the US though that they can barely (if at all) afford. And plenty of cases of American IT professionals in the same boat, a lot of companies putting out ridiculous job descriptions requiring 5 years experiences with COBOL or other programming languages not really used in decades for entry level positions. A nice ploy to shrug their shoulders and cry “we couldn’t find any qualified Americans” to then turn around and try to hire cheap labor on an H1B from abroad.

One thing I’m having trouble reconciling is yes, there are wage increases, but at what pace are they beating or keeping up with inflation or not? Do you have charts here that I missed? Just curious. I was under the impression that yes, there is wage growth, but due to inflation I was thinking most people are at best breaking-even with their increased earnings or perhaps even falling behind somewhat. Ultimately it is true that they are spending more, but how much of that is due to everything… well… costing more. Thoughts welcome.

Raging inflation did eat wage increases until this year. In Q2 Nonfarm Real Hourly Compensation for All Workers rose by 2.7%.

Got to watch out for that “wage growth”. Not seeing that either.

Because you closed your eyes so that you don’t have to see it because you don’t want to see it? Common practice.

I hear your point, but no one except for the most crazy among us put their lives on hold for three years. It was morel like one year. Most people I knew (across a wide range of types of people) were back to normal by April of May of 2021, after the vaccines came out.

The problem was, even if we wanted to return to normal once the vaccines came out, not everyone did. That continued to throw a wrench into things. Some things were happening. Others still weren’t. It was hard to get into a groove with one’s life. Also, the supply side and workers still weren’t there. So, many places had limited hours, availability, etc. We’re still struggling with that some. Because of all this prices are higher now, but we’re tired of waiting. So we’re just paying up and saying, screw it. Wages may be up, too. But because prices are up as much or more than prices, the net result is purchasing power not really up. So, we’re borrowing, cashing in assets, whatever it takes and not waiting around anymore. Besides, if one waits, prices will probably be even higher tomorrow.

I understand completely. I do. But patience is more than a virtue, it’s a strategy. The worm always turns.

“I hear your point, but no one except for the most crazy among us put their lives on hold for three years.”

It depends on your definition of “put their lives on hold.” I have been waiting more than 3 years to purchase a vehicle while the prices continued to increase to stupid levels.

Used car prices aren’t going down much for another year or so. They might even go up for a while, at least on a seasonal basis.

Supply of near-new units is gonna stagnate at or near current levels (-20% vs. pre pandemic) for about another year while the 2020-2022 production slump works through the system.

When I saw that sales at restaurants was $8 billion higher than sales at supermarkets I thought the exact same thing! Revenge travel now has a partner called revenge dining out.

Department stores. Wow, talk about a dying industry!

Your charts definitely say Home Cheapo is getting kicked in the coconuts.

Prices are down quite a bit on lumber and gypsum at my local store.

Romex 12-2wg 250’electrical cable was $160 less than a year ago, now $108. Twenty rolls for a custom house rough-in that’s a thousand dollars saved. PVC fittings and boxes and Mexican breakers are still hit and miss.

Does the $90 bil for bars and restaurants include the $5 bil or so collected in sales taxes?

No, sales taxes are not included. These are retailer “revenues.” Sales taxes are not part of revenues. They’re just collected by the shop and passed on.

Thanks Wolf, I’ve been wondering about that for a long time. Your a fountain of knowledge.

Finally, I understand. I agree spend away and let the fed bail us out again. Free college tuition, can’t afford a house, so go drinking, buy a fancy vehicle, addicted to ecommerce shopping and yes that is what my adulting kids are doing now. I’m not able to because I’m still paying their bills – no more.

Consumers are tapped out………

🤣❤

Where is the scream? Might play well on your YT channel of you screaming. lol

Howdy Folks and Mr Wolf.

Consumers are tapped out. Just kiddin Sir. We have a long way to go folks. Trillions and trillions still out there. The old folks like me are probably spending every bit of the interest income too….. Waited a lifetime to spend some money and enjoy……

Interesting… American spent ~1/2 on restaurants/bar vs ~1/2 on grocery (90B/82B). Total about 170B/month (?), average is about $500/month for each man/woman/child. For a family of 4, that is about $2K/month.

Holy cow! That is a lot! No wonder a lot of folks are having a hard time. Our bill for a family of 4 is about $1K/month for grocery alone. So if people eating out once/week then definitely this will hit $2K/month.

I do find these numbers shocking, that $280 is spent per month per American on bars/restaurants. That said, I suspect there’s a huge range between the classes.

Consumption data would be a lot more interesting if they could somehow be broken down by age, and by income. But these data are retail sales, which do reflect consumption, but I doubt if there is any hope of getting an age/income breakdown with retail sales. Maybe look at Nordstrom and Neiman Marcus and compare change in retail sales to Walmart and Target.

In any case, the economy keeps plugging along, much to the chagrin of Chairman Powell.

Notdstrom needs to go to membership only after those gangs keep hitting them for 100-250k in losses. That way it could be like a Costco. Chain link fence and a member checker for the first 30 yards into the store.

And the middle class customers could feel good knowing they “belong”.

If you use a Pareto distribution, the average for the bottom 80% would be ~$70 per month per person, while the top 20% would be spending ~$1100 per month per person.

McDonald’s is like $10 now for a basic meal, mid-range dining $15-30 range, and fine dining in the $150-$200 range. So the numbers make somewhat more sense.

Still, every person in every class would have to eat out at least once or twice a week for these numbers to add up.

What would skew this are the abstainers. I rarely eat out, so someone else is definitely eating out more than their share!

Most people definitely eat out twice a week if you include working people grabbing lunch.

I remember in the ‘80s some booze hounds I knew from the South Side of Chicago would bring a flask of hard liquor with them like W.C. Fields when they went to upscale clubs downtown to save money.

I eat 90% organic, cook every meal myself and shop for it all (which is good exercise! Try it.). My groceries for one month per person are prob $750. I try to follow several nutritionists who base their recommendations on health studies.

It’s a lot of high quality protein, fiber, carbs, superfoods, etc. etc.

This way paying zero tips. Zero to drivers. Zero to store shoppers and zero to corporate excess. And I shop all the sales. Lately the coupon apps like Ibotta and coupons.com have been terrible. They offer almost nothing. I guess the manufacturers wised up and their numbers are good enough not to offer discounts atm.

Anything that you can get coupons for is generally processed crap.

Eggs, dairy, meat, fruit/veggies don’t generally have coupons.

We are pretty similar, rarely eat out, but cost per person monthly is much lower, probably 250$ per person.

That’s a very large grocery designated budgetar amount per month. Wow! I could spend that much easily too as I love eating healthy and organic.

I’m spending approximately $200/month or less if possible as one individual.

You’re probably one of the fortune wage earners experiencing “wage growth” month over month or year over year.

Zard,

We’re certainly doing out part, us drunken sailors, gotta keep that economy pumped up to piss off JPow.

Are you kidding? Weimar Powell loves it.

LOL

I wish you could live in a Weimar situation. Only then would you realize how stupid it is thinking the U.S. is there now.

The total retail sales graph goes from 680 to 690 billion for the 3 month period; that could be accounted by credit card debt. It would seem interesting to match the retail sales graph with an overlay of consumer credit card debt as there might be an increasing trend. The automotive part might be a problem as car loans are separate, but auto parts etc would be cash or credit.

LOL. No. Read my articles about credit card debt. What does it say??? Here is an excerpt:

https://wolfstreet.com/2023/08/08/our-drunken-sailors-still-not-getting-in-trouble-with-their-credit-cards/

The most important thing about credit card balances is that they’re largely a measure of spending – rather than borrowing. Credit cards are the dominant consumer payments method in the US. About $5 trillion in spending was paid for by credit cards in 2021, according to the Federal Reserve’s most recent payments study. The amount would be much higher in 2023 because prices have gone up, spending overall has increased, and people have gone on a travelling binge, and nearly all travel expenses are run through credit cards.

Most of these balances get paid off the next month and never accrue interest. Only a small portion gets stuck as interest-bearing debt. But the data doesn’t split out interest-accruing credit-card balances from balances that are paid off in full on due date and never accrue interest.

And only about 28% of households have interest-bearing credit card debts. Here is the data:

https://wolfstreet.com/2023/08/19/how-many-americans-have-interest-bearing-credit-card-debt/

60%+ of drunken sailors got dishonorably discharged from the Navy for not owning stocks and houses and contributing ponzi paper wealth profits to Washingtons economic all is well coverup divert from inflation wipe out of the lower classes. These top 30% are so drunk with paper wealth they could spend double and not blink and just might and fill up those charts. With so much doomy news why not before “something breaks”. Now I live and work near Disneyland and drive by it everyday almost and dont see many people around ever and this is busy season. Never saw that in summer for 50 years. You would always see the streets crowded, families walking around at the corner of Harbor and Katella. I see more for rent/for lease signs every week everywhere. More and more homeless everywhere and brazen smash and grabs with 50 to a mob now just this week, again. China mfg slowdown, RE problems? Impossible. UK warning? Inflation has done a good job(of wealth transfer) at least from what i see, not read. Everyone looking at drunken sailors’ spending, jobs and travel. I look too but Im not listening. I’m looking at tax receipts, for rent signs, jobs that are part time, homeless, mfg data, sentiments on certain business and good/ bad time to buy a house sentiment. Im looking at CRE liquidity concerns and bank risks, deposits fleeing to treasuries. I’m looking at interest rates at bubble everything valuations. I’m looking at debts, business and personal and especially sovereign debts like ours with vertical increasing deficit debt to infinity since it dont matter. Im also looking at anything that reflects reality collectively. I see the Fed trying to lower its balance sheet like its trying to save itself and its own credibity if it even has any left because it knows Washington is bankrupt without recourse except to default which it probably will do,(unwillingly) as there is no other option left. I look at the end game here of inflation which would be the end of our money, the Fed and our Government as we know it. When I try to put it all together and make sense of it all moving forward I come to this conclusion: I have no comment other than I am sure glad that I don’t drink.

pleasure to read, thanks Steve!

In terms of Disney, they’ve got a problem, a company problem, and not an economic problem, and their stock has plunged by over 50% since March 2021

is it a problem?

what looks like a problem to you, may not look like a problem to tim cook, for example.. it may look like a 50% discount on one of the most valuable brands in the world..

in that case, it isnt a ‘problem’, its the opportunity of a lifetime.

The stock price is NOT the problem, it’s the symptom. The problems Disney has are explained in its earnings reports, including a $460 million loss in the last quarter. As a result of these ongoing problems, the stock dropped 50%.

I’m buying a lot of stuff through mail order catalogs. I use snail mail to mail the order and charge it to my gift credit card. I’m spending about $500/month this way. Just bought some cargo shorts and some shoes this way. Saved going to the mall and wasting gas.

I’m wondering if Wolf or anyone else would clue me in on where this form of sales shows up in the consumer sales data, or if it even shows up at all.

Why on earth are you mailing orders in through snail mail?

LL bean maybe?

Einhal

My e-mail (Earthlink.net) and Internet with Comcast is not secure (not encrypted) and has been hacked a half a dozen times. My credit card has been stolen with on-line purchases. Snail mail is safer.

I sincerely doubt your credit card number was stolen by someone hacking data from Comcast. It’s much more likely that it was stolen from a retailer’s database (which you can’t control, even if you send in your order snail mail).

The only two times I have had a credit card compromise are with cards used for in-person transactions. I know this because I have cards that I only use for online and ones I never do.

Obviously you have to do what makes you happy, but I doubt there’s much science that says your way is safer.

Einhal

Agree, the retailer’s database is the primary culprit. Amazon was definetely penetrated by bad actors. I’ve solved some of these hacks by not leaving my credit card on file with vendors.

I have a sacrificial lamb card I use all over. When that one gets taken (like the movie! ;) ) I use one of the others. Waiting that 2 weeks for the new card is painful.

A lot of gas stations near me have issues with C.C. Fraud.

“These top 30% are so drunk with paper wealth they could spend double and not blink and just might and fill up those charts.” Absolutely. You don’t unwind nearly 30 years of bubble-generated wealth in a year, especially when rate hikes started at 0% (or negative in some places). Plus, many people actually have interest income now. So, even more money to spend. So many people are richer than they could have ever imagined. They’ve just come through three years of putting life on hold, and they’re not getting any younger. Their kids are only going to be around the house for a short while and at key ages once. Same with grandkids. So, they’re going to be pretty willing to spend now and tap resources or borrow if necessary to stop missing out on life.

Wolf, do automatic gratuities and services charges factor into the “Food Services and Drinking Places” data?

There are a lot more of those charges lately, and some careless drunken customers don’t even seem to notice them and just pay them.

The creep in locations is getting really out of control. I ran into one the other day at the cash register of a convenience store! I’ve also noticed they’re playing games with the format, things like putting the highest value on the left instead of the right where it would traditionally go, and that the lowest value seems to have shifted from 10-12% to 18% or more being common.

Thing is, if you don’t pay them, it definitely gets noticed and you often get treated accordingly.

It’s getting to the point it needs regulating. Want the default to be your customers pay the shortfall from your employees wages? Fine, but then your price list should have to include that full default price.

That’s an interesting question. In the old days, when people paid in cash, including the tip, the restaurant never saw the tip, and it didn’t become part of their revenues. Now customers pay by credit card, and the restaurant is supposed to pay the entire tip to the staff. So logically, it would seem that restaurants do not consider tips passed on to the staff as revenues, but I’m not sure how they do it. I should ask one my accounting buddies.

Service charges other than tips should be part of the revenues.

Wolf,

From the few contacts I have in the restaurant industry, tips are NOT included in revenues. Revenue is the amount of the bill. Rips on credit cards are immediately paid out to workers and not included in any restaurant measure.

I trust the two sources I discussed this with, but it is all second hand and I will fully admit I am not an expert in restaurant cash flows. So use whatever amount of salt you require.

Appreciate the charts. They only go back 15 years but need to go back 17-18 years to give the full picture

They include the financial crisis. They’re already too long because all the details get lost and I have to put in the inserts so you can see the details. It’s like every time you want to look at a stock chart, you insist that it goes back to Adam and Eve, which is bullshit. If you want to study history, study history. I have already shortened the time scale over the years, and I will shorten it further soon, and then it won’t even have the Financial Crisis on it. And you can howl at the moon.

“If I hear one more time consumers are “tapped out,” I’m going to scream.”

Conversely, the constant tales of the robustness of the US consumer-driven economy and all the extravagance of its gluttonous shopaholics are bordering on emetic.

People who close their eyes to it will never understand inflation and why this economy isn’t slowing down. You can wallow in BS all day long, but if you want to understand what happens in this economy, you’ve got to pay attention.

No no — I totally get it. Americans are out there being fabulous — shopping & partying and globetrotting. Everything is awesome.

Yeah, some of the consumers in the USA are spending like drunken idiots, but others aren’t and those are the ones in the lower socioeconomic levels.

Too bad dope isn’t included in retail sales as that would probably have a huge increase in spending over the past couple of years.

After all things go better with coke…

“Too bad dope isn’t included in retail sales…”

Cannabis is included. Sales by cannabis retailers are included in “Miscellaneous store retailers.” I pointed this out, see chart above. So here is again, for your convenience, so you don’t have to scroll up.

Also note that cannabis is one of the products whose prices actually dropped sharply late last year and earlier this year, and dropping prices hit the dollar-sales amounts, though may have increased the quantities sold.

Miscellaneous store retailers, includes cannabis stores (2.2% of total retail): Specialty stores, from art-supply stores to wine-making supply stores.

FYI pot isn’t coke, it isn’t included in retail sales and it isn’t legal either.

The coke market is about the same size as the pot market and as a result of the difference in price between the two those who tend to be regular users are quite different.

Dope seriously?

I am constantly amazed at the crazy tales people will spin for themselves in order to avoid changing their views.

I haven’t heard anyone say that consumers are “tapped” out. The wealthy and top of the middle class is doing fine. The poor and lower middle class are quickly going paycheck to paycheck and are “maxxed” out, referring to their personal credit cards. No, not all of them but anecdotally and even reading into some of the charts within articles on this site it can be reasonably inferred.

Drunken sailors are still partying on the top deck but the minions rowing the ship are petering out.

In terms of credit cards, read this:

https://wolfstreet.com/2023/08/08/our-drunken-sailors-still-not-getting-in-trouble-with-their-credit-cards/

And this — only 28% of US adults have credit cards with interest-accruing balances:

https://wolfstreet.com/2023/08/19/how-many-americans-have-interest-bearing-credit-card-debt/

The poor are always living paycheck to paycheck. They are poor.

This isn’t Lake Woebegon where everyone is above average and has tons of money in the bank.

A leading indicator of fewer drunken sailors seems to be evident with temporary help, whoever they are, but one can assume they are currently spending less in this epic recovery, as they work far fewer hours… however, the soft landing of the helicopter appears to be exactly where it needs to be for 2024 election cycle.

Take a look at that graph for Music Stores !

Lots of people fiddling while Rome burns.

There are several truisms here that time will tell if they remain true:

Warren Buffet says something along the lines that bubbles are like sex; feels best just before its over.

Yield curve being inverted for a long time predicts recession every time.

Stocks require a significant risk premium over risk free assets to compensate investor.

The Fed never sees a recession coming.

All I see is more and more Warning signs.

1. Not sure if I’d use Buffett to obtain sexual truths, LOL.

2. Everything predicts a recession over time because there is always a recession eventually. The fact that I dropped a hammer today on my toe predicts a recession. We just don’t know when.

3. yes

4. The Fed saw the recession coming this year that isn’t coming, LOL. Earlier this year, it said we’d have a recession in the second half. That projection has now been scuttled.

I thought buying a home when rates were very low in early 22 would be a mistake. I waited for rates to go higher. Everyone was saying prices would tumble when rates went up. Everyone except socaljim. He was saying everyone was wrong. His point was home prices would rise if inflation is high. I wish I would have bought in early 22 because I could qualify. Prices are even high now and rates are high making the payment very high and I am priced out forever. I used to use zillow to look for homes for sale. Now I use zillow to find home for rent.

Prices ARE down. They’re down a LOT in some cities, including in the SF Bay Area. The national median price is down year-over-year. Lots of cities have lower home prices now than a year ago. The national median price will fall further in the second half. But you gotta be patient. RE is not crypto. Also some cities had big price increases, such as Tulsa, LOL, still el-cheapo though. Why don’t you buy a house in Tulsa?

Maybe the reason prices are so cheap is that Tulsa has been featured in the A & E homicide series First 48. They’ve had over a dozen episodes. Watched a few of the episodes myself. Looks like the city has become a human hellhole.

I’m seeing a lot of older people come back into the workforce. Publix is really

scouting the nursing homes for cashiers

and baggers. Whether they are working because they have to, or because the pay

has risen enough to make it worthwhile,

I don’t know.

They’re working because finally someone is wanting them to work and is paying them adequately. Age discrimination is a thing, it’s very frustrating, and after getting blown off so many times, people stop looking. Now it has changed, this is just a really strong job market, and employers are bending over backwards to hire, especially in these lower-level jobs.

Yes. I see that as well. It’s a phenomenon indeed. Probably and likely need to supplement their “social security” and would likely lose what they have if not for that fact.

When you get older, working is the best thing you can do to stay active, keep your brain stimulated, learn new things, meet people, feel useful and appreciated, and make extra income.

Paul, your and Sporkfed’s comments reek of age discrimination in your brains: You don’t want to see older people when you buy something? Older people should stay out of sight?

About a week ago The Chief on the Stocks & Jocks podcast in Chicago was saying that the front of his office and the block on south Wells Street was overloaded with young homeless people lying on the sidewalk in sleeping bags and tarps. He said it turned out that they were actually idiots from the ‘burbs waiting to get into Lollapalooza the next day.

Just picking through the bones, but:

Re: New and Used Vehicle and Parts Dealers (20% of total retail sales):

The YTD gain isn’t exactly impressive, which indicates drunken sailors aren’t totally exuberant and probably showing signs of greater hesitation.

The YOY of6.3% doesn’t reflect the decline that’s occurring…

I’ll go eat a bar of soap and hide under the bed.

I am very guilty of not really paying attention to how much I’m being charged. Every once in a while something penetrates the fog and I’m left thinking something like “hang on, this is a *McDonalds*. How the hell is the bill this much?”

That extrapolates to pretty much our whole spending, except of course many things aren’t frequent enough purchases for me to have any real memory of what’s normal.

Our habits haven’t yet changed, and I suspect it’s because we haven’t really sat down and realised what the current tally is. I confess, we are drunken sailors.

I think there’s a lot of us in the same boat. It’s easy not to pay close attention when you have enough to comfortably cover day to day life, but the main big ticket item – your own house – is out of reach.

Wolf, your charts are great! Much better than words in most cases.

Then I love your ‘moderated’ comments. It’s nice to hear other intelligent people’s views about what is going on.

Your ‘moderation’ is beautiful. It keeps the crazy and mean tamped down!

Thanks!

Without reading Wolf, I would have thought folks tapped out, recession looming…..but I do read Wolf! I have made my business projections 4th quarter, and 1st quarter 2024 (Christmas thru Valentines ) to be dynamic. I believe spending will be huge. I see a slow down in 2nd quarter 2024. Still not a recession. Wolf has been statistically correct. I love reading the comments. It shows folks believe what they want to believe, and don’t change opinions based on facts. Its hard to change beliefs, even when shown the facts don’t back us up. That is why, Wolf, is the most valuable source of fact based measures in our economy. Certainly worth a donation this fall!

Atlanta GDPNow predicts 5.8% growth for the third quarter. Way to many bears for this market. I am buying as the market falls.

It’s too early in the quarter to pay a lot of attention to the GDPNow. It only has a few Q3 data points so far, and it’s likely to come down as more Q3 data arrives.

But so far, the data has been very strong, including these retail sales here, which is why the GDPNow is so high.

Big Short guru Michael Burry has bet the farm on a market crash. He’s just put 1.6 billion of his company’s money leveraged 100 to 1 on the S&P taking a massive nosedive. Unlike 2007 he’s not singling out the housing sector, but betting on an across the board crash of the entire stock market especially the NASDAQ.

Wolf, what is the name of the new and “used” home price indexes on FRED you use? There are many different ones and it is a bit confusing. Thanks.

Its official name is “Existing Home Sales.” Not sure if it’s in the FRED database. I don’t get the data from there.

It’s not party hard thing