Keeping an eye on them because some day enough of them will get in trouble to move the needle. But not yet.

By Wolf Richter for WOLF STREET.

The most important thing about credit card balances is that they’re largely a measure of spending – rather than borrowing. Credit cards are the dominant consumer payments method in the US. About $5 trillion in spending was paid for by credit cards in 2021, according to the Federal Reserve’s most recent payments study. The amount would be much higher in 2023 because prices have gone up, spending overall has increased, and people have gone on a travelling binge, and nearly all travel expenses are run through credit cards.

Most of these balances get paid off the next month and never accrue interest. Only a small portion gets stuck as interest-bearing debt. But the data doesn’t split out interest-accruing credit-card balances from balances that are paid off in full on due date and never accrue interest.

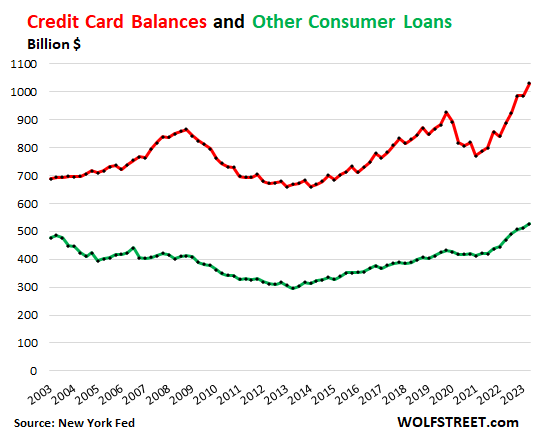

Credit card balances in Q2 rose by $45 billion from Q1, to $1.03 trillion, after having been flat in the prior quarter, according to the New York Fed’s Household Debt and Credit report today.

Year-over-year, credit card balances rose 16.2% on higher prices and increased spending particularly on services such as travels, restaurants, and entertainment (red in the chart below).

“Other” consumer loans, such as personal loans, payday loans, and Buy-Now-Pay-Later (BNPL) loans, ticked up by $15 billion in Q2 from Q1, to $527 billion. Unlike credit card balances, most of these “other” balances are interest bearing, but not all. BNPL loans are interest-free for the consumer and are subsidized by participating retailers (typically the customer pays 25% down and makes four weekly installments).

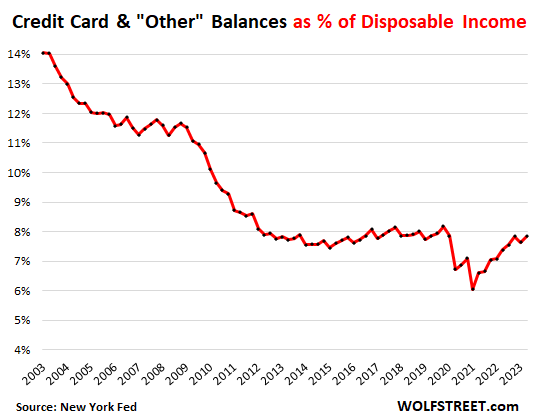

The burden of credit-card balances is low.

Credit card balances and “other” consumer debt combined in Q2 of $1.56 trillion amounted to 7.8% of disposable income, right back in the Good Times range before the pandemic. The spike in disposable income during the stimulus era caused the ratio to plunge to record lows (disposable income = income from all sources except capital gains, minus taxes and social insurance payments).

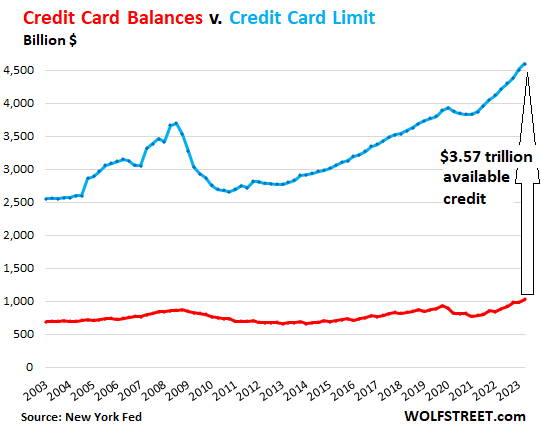

$3.57 trillion in available unused credit.

Consumers with subprime credit ratings might encounter tightening credit. But overall, there are no signs that consumers with halfway decent credit are running into a “credit crunch.”

Banks have raised the aggregate credit limits on credit cards to a record $4.6 trillion. With only $1.03 trillion in credit card balances outstanding, the total available unused credit rose to a record $3.57 trillion.

Note how much faster the aggregate credit limit rose in dollar terms: +$379 billion year-over-year; compared to credit card balances: +$144 billion year-over-year (the-sky-is-the-limit-blue = credit card limits; red = credit card balances).

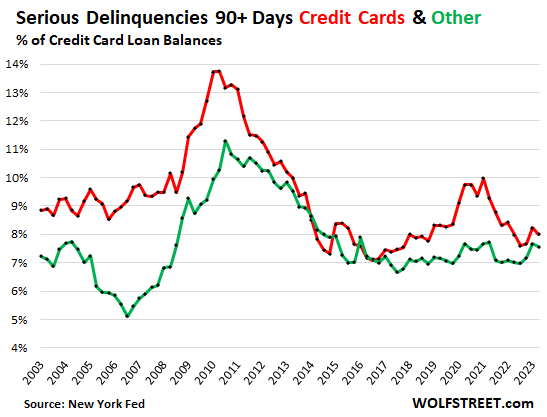

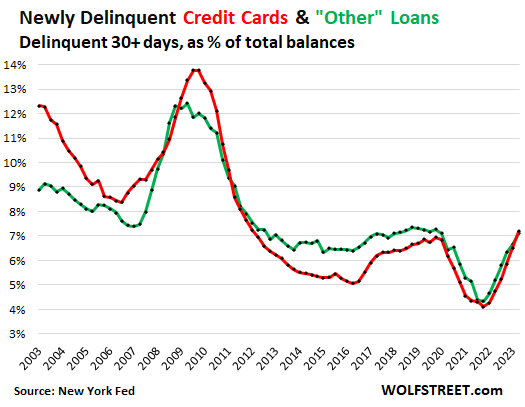

Delinquencies normalize.

The gamut of stimulus monies, forbearance of all kinds, and eviction bans during the pandemic allowed consumers that were behind to get caught up, and it had a big impact on delinquencies. But that era has passed, and consumers are going back to normal.

Serious delinquencies for credit cards ticked down to 8.0% of total balances in Q2, below where they’d been in 2019 and level with 2018 (red). For “other” loans, they ticked down to 7.6%. These are balances that are 90 days or more past due.

You can see the strain on cardholders in 2020, with serious delinquencies surging, that were then getting cured in 2021.

Transition into delinquency – balances that just went 30 days past due – shows that people are falling behind at a level about equal to before the pandemic, with newly delinquent balances for credit cards rising to 7.2% and for “other” to 7.1%. These newly delinquent credit card balances fell to record lows during the stimulus-money era. They have now normalized. If they continue rising, it would indicate added strain. And we’ll watch that.

But as the 90-day delinquency chart shows, they’re mostly still able to cure the delinquency and get caught up before it’s 90 days past due.

But wait, it didn’t really go up.

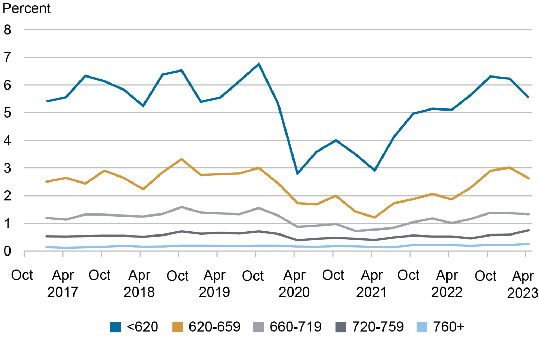

The New York Fed in a blog post disaggregated the transitions into delinquency by the credit score at issuance. And it says, “Note that these rates differ from the transition rate calculated in our Quarterly Report because they are unsmoothed and use more detailed data.”

Based on this more detailed data, the transition into delinquencies actually dipped, and dipped particularly for subprime borrowers (below 620 credit score), near-subprime borrowers (620-659 credit score), and middle-of-the-roaders (660-719 credit score). Disaggregated, the chart from the New York Fed also shows that the vast majority of the delinquent balances are in the subprime category.

Transition into delinquency (30 days+) by credit score. Chart by New York Fed. Source: New York Fed Consumer Credit Panel / Equifax (Philadelphia Fed Credit Card Detail); Credit scores are Equifax Risk Score 3.0.

A word about banks and credit cards.

Banks incentivize the use of cards as payment method by offering 1% or 2% cash-back on card spending, frequent flier miles, and other benefits. Banks collect percentage-fees from merchants for every dollar paid for with a card, and these fees have become big profit centers for banks. So banks are aggressively marketing these cash-back cards to people that may never borrow and incur interest with these cards, but will run large amounts through them, and pay them off every month, and collect 1% or 2% cash-back, and the bank cashes in on the fees it charges the merchant.

Banks, by charging huge interest rates, are essentially discouraging the use of cards as a borrowing method. And a majority of people don’t use their cards to borrow, but pay off their credit cards every month to avoid interest charges, or they borrow only briefly to finance a major purchase, such as some furniture, and then they hustle to pay off the balance quickly. But the people that don’t pay off their credit cards monthly, and who carry a balance every month, pay huge amounts in interest, and they’re the ones that show up in the delinquency data when they fall behind.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Transition into delinquency…people are falling behind at a level about equal to before the pandemic”

But they sure have gotten back to “normal” delinquency pretty quickly, eh? The rate of increase in delinquencies is pretty close to the time period leading up to the GFC peak. It will be interesting to see what this chart looks like in a year and again in 2 years. Will that ascent stay steep? I suspect the answer is yes, especially now that debt servicing actually costs something again. Can’t escape delinquency by rolling old debt into even cheaper new debt anymore.

1. “But they sure have gotten back to “normal” delinquency pretty quickly, eh?”

Normal is the Good Times normal before the pandemic.

2. “The rate of increase in delinquencies is pretty close to the time period leading up to the GFC peak.”

BS statement.

3. “Will that ascent stay steep?”

BS question. Because look at the descent! It didn’t “stay steep either.” BS questions lead to BS answers, which you provided. Look at the NYFed chart. OK, here it is again. Transition into delinquency by credit score:

These gravity defying, massively over inflated bubbles are primarily the result of three mistakes:

Near ZIRP policies by the Fed much, much longer than necessary

Massive government stimulus that continues unabated

And MOST IMPORTANTLY rent & mortgage relief

Is anyone surprised that it’s taking the treasury so long into July to update its fiscal data website for the running FY23 annual deficit? I’m not. When it drops, it’s going to be ugly.

We are on an unsustainable fiscal path that’s accelerating. I don’t see how this doesn’t end badly in the next 24 months or so. Our annual budget deficit is single-handedly keeping us out a recession.

Thanks, Wolf!

I hope so. I hate so much what modern America has become that I want it to fail so it can be reset. I see it as a modern Sodom and Gomorrah.

People have said we are running unsustainable deficits since Reagan was President, 40 years ago. No one is willing to say how high they have to go to cause the great reset. And maybe, as Dick Cheney said, they just don’t matter.

Massive government stimulus that continues unabated

And MOST IMPORTANTLY rent & mortgage relief

cause with so many other takers like illegals, homeless

we need lots more of those ole stimi $dollars

what is interesting to me is how starting at the 2008 financial crisis, the credit card borrowing as % of disposable income just fell to a new level and then stabilized. any reason for this? did credit card interest rates rise? was it due to restricted credit limits on subprime borrowers that permanently reduce over-spending? or was this really just a societal-level change in borrowing habits?

my guess is that it was the differential between borrowing rates for credit cards and other forms of borrowing (main mortgage debt).

i think that despite these seemingly “normal” metrics, most people on this board feel that the current economic performance is simply unsustainable government stimulus measures in the form of 1) moratoriums on the repayment of student loans 2) propping up the mortgage market with 2.5 trillion of Fed MBS purchases 3) massive fiscal deficit spending each year 4) local governments in some states not yet acknowledging their growing budget crisis 5) wealth effect from stock market gains and housing equity gains 6) massive propping up of the asset bubbles with 6 trillion of bond purchases by Fed.

When people deny that this is all just a big bubble created by government, I want to ask one simple question. If this isnt all just a by-product of unsustainable government programs, then why cant they just immediately normalize the budget deficit and Fed balance sheet? Sell off 2-3 trillion of assets from the Fed balance sheet at the same pace they purchased the stuff back during COVID? and cut the deficit spending to zero by either raising taxes or cutting spending.

why not? if the economy is so strong, why not?

we all know the answer. our economy would be plunged into the most dire of circumstances.

the reason we are all so pessimistic is that we arent dumb. this economy is NOT normal, even if the core metrics of employment and spending look normal for now.

it is all just borrowing from the future.

I have about 1,100 clients who pay weekly. We mow the lawn and then charge the cards. In my 21st year of this (DFW). Normally, in good times, I’d have to call 10 to 15 clients a week on declines. This year it’s been around 30 per week. Bed debt write off is thru the roof too, compared with “good times.”

You CAN escape delinquency by rolling your balance into a 0% card! Many cards still offer this option for “21 months.”

The presence of these offers (still widely available!) os a sign that credit issuers are still chasing. What choice do they have?

As Wolf stated: they’re after a margin of total commerce. They offer 1-2% “rewards” and charge 3% fees.

They bet on some amount of accrued interest and some amount of default.

Capital One has made a living off subprime, gotten burned and done it again.

Watch the 1/4erly chart of BAC. Showing the break below trend for the second time in 20 years? Maybe so, maybe a red flag.

My credit card is the best 30 day free loan anywhere . Thanks banks and no annual fee

^^^^^^^^^^^^^

This guy gets it.

The credit rating specific chart is all you need to know.

If you absolutely refuse to pay annual fees, you often come out behind. For example, I have a Chase Sapphire Reserve with a $250 effective annual fee. I get way more than $250 worth of benefits every year beyond what I could get from a no-annual fee card.

Recent Clark Howard recommendation.

Clark says the Capital One Venture X Rewards Credit Card and Chase Sapphire Reserve® are two of his favorite choices because they allow you to be a “free agent” when shopping for travel and still receive really great rewards in the process.

At $395 and $550, respectively, both of these travel rewards cards have what most would consider expensive annual fees.

It’s not really $550. It comes with a $300 travel credit that basically refunds the first $300 in hotel/parking/airfare/bus spending. It’s basically impossible not to use it. I don’t think I’ve ever made it past February without using it in full.

Their probably selling your financial data to help provide the service.

When I go to Goodwill or buy beer I pay cash, and leave the cell phone at home.

Goodwill stores now have liquor licenses – awesome!

I don’t take cell phone anywhere,I can monitor myself . About to go phoneless

Cuz the aliens might know huh?

I have spent more in the expectation of higher and higher prices. The bankers’ (not) “Federal’ Reserve (which is only as “Federal” as Los Angeles judges are “honorable”) is not serious about taming inflation. Only foreign economic and weather disasters may reduce it.

Automotive loan balances are now at $1.58 trillion in the second quarter and rose by $20 billion in the 2nd quarter of 2023.

Will be interesting to see the coming negative effects higher borrowing costs have on mortgages, on auto loan rates, on credit card payments, etc.

At some point in the next few months these added costs will inhibit spending in other areas and drastically slow growth. Prepare for higher delinquencies, job losses, and yet another bust after the Fed’s boom.

Always difficult to put a timeframe on when the music stops, but it took only about a year at 5% FFR in 2006 before the Fed figured out they once again went too far and had to start slashing interest rates.

For anyone that hasn’t seen this great PBS documentary yet, it’s free on YT now:

Interest rates have little impact on new vehicle sales automakers will offer 1.9% financing, as Ford does on F-150s now, if they need to move the iron. They can also offer $10,000 cash, or whatever. Incentives and the captives’ special rates are what’s driving sales. And sales are way up from last year because now there is inventory and the incentives are coming out of the woodwork.

What will happen with the subsidization of gasoline by the government since electric vehicles are gaining ground?

Will they subsidize electricity more?

I’m watching to see how the renewed repayment of student loans beginning in October will effect consumer spending and borrowing. I read recently that there are 45 million individuals with student loans. Biden’s “on ramp” program will allow a one year grace period, but interest will accrue starting September 1, and outstanding balances will grow. Some retail outlets are expecting this could significantly decrease sales.

I stopped considering government student loans as “loans” until I actually see borrowers making payments in large numbers.

I know a guy hoping to get 450k in student loans written off!

If not, he will have to make $3500 payments.

Insane.

I think there are plans that limit payments to 10% of your discretionary income.

I doubt if the student loan payment would ever start ..

Stealth welfare working as intended. Beneficiaries are the ivory tower statistical studies clowns and their myriad careerist administrators. Science!

student loans started out only being for science degrees that were needed for our country to compete. i think we need to go back to the idea that for the government to fund something, it needs to provide a societal benefit to everyone, not just a special interest benefit to a few people.

and yes, government funding of the education industry is primarily a benefit to that industry, not students. our corrupt educational industry has managed to push the price of a college education up to 80K a year, which really hits the middle class who dont qualify for needs based financial aid but are not rich enough that 300K is meaningless to them.

Household Debt to GDP for United States, looking stronger everyday, the consumers are invincible if not unstoppable!

Just don’t make them diet. That would stop this economy dead in its tracks.

“No more McDonald’s Mr. Smith!”

Mr Smith: “well I’m going on strike!”

The Canadian Walmart clerks keep badgering me for a store credit card. I don’t have ID on me? No problem, we can use your (Ontario) health card lol.

I already have a store credit card and mainly use it for cash back points. If it goes above $500 on a given week, I do my best to get rid of the balance like a news reporter does to a zit which popped up before show time.

On the contrary, the parking lots of the 24H Money Marts and Cash Money always seem to have cars, even at 3 am in the middle of winter. You borrow $300, and you end up paying $150 in interest and fees within a week.

Gen Z, freeze your credit with the major credit agencies (Equifax, TransUnion, and Experian) and you won’t have that problem again. I froze mine after the credit breech of 2017.

A couple of months ago, I was badgered by a Home Depot customer service rep about opening a Home Depot credit card. I kept telling her I didn’t want one but she kept on and on about it. Finally, I said “ok, fine, open one up”.

A few minutes after starting the credit application process she looked at me and told me my credit was frozen. I said, “yep” and then promptly left the store.

Thanks HotTub.

There are Canadians who really need a good credit score to remain employed in the public sector, and there are Canadians who want to take as many loans, file bankruptcy, and either stay low for 7 years, or flee the country with tens of thousands of dollars in loan money.

I thought spending like drunken sailors only applied to Congress.

I see my Comcast (internet provider) and T-Mobile (cell phone) now will only let me keep their deals if I stop payment by credit card, and allow them to take the monthly bill directly from my bank account. Seems like actions like this will hurt Visa and Mastercard profits eventually.

Yes. They’re using ACH, which is a lot cheaper than credit card fees.

There are services, including Zelle (bank owned), that are totally free, and I don’t know why companies don’t use them.

Our payment system in the US is horrible, 20 years behind the times. But banks fight tooth and nail that it stays that way because they make a lot of money on it. Banks have been fighting FedNow for 10 years, and now that it’s here, few banks are using it (something like 43 banks are on it). It would provide for free and instant payment, with the Fed as the central clearing point. But the banks would lose billions of dollars in fees.

WL & Wolf

I use Verizon as they also offer a bank card with rewards to pay the invoice. Stock dividends almost pays it each month anyway.

I also use ACH for almost all other bills except the guy who prints my checks, he simply ACHs the bank for the cost. All others I pay each month from the bank via ACH.

This seems to keep everybody honest and on their toes.

I began this computer game in the mid 80s and try to keep up with the scams.

The ACH network is governed by NACHA which is a private organization (most funds through the network actually clear through the Fed). They actually have a very good set of rules in place and the banks are audited to ensure they are following the rules. There are a lot of regulations built into the system that make it easy to resolve errors in payments and thus incredibly safe. They came out with same-day ACH around 2016, but they phased it in super slowly and I was never able to get a straight answer on why it wasn’t just the standard and mandatory at least for small dollar amounts.

Zelle is instant. As far as can tell, ACH is still next day, and if you make the payment on Friday, next day means Monday. I have no idea why it’s not 24/7 … that should be easy to do. And why they cannot make it instant.

I think it boils down to the simple fact that banks refuse to give up the “float” — the day or two of free money they get by sitting on a gazillion transfers every day.

ACH between my broker and bank is always one day. For example, I tell the broker to suck the money out of my bank on Monday, and it is in the broker’s cash account on Tuesday.

I can actually play the float using the the three day settlement for Treasuries. One reason I like 4 month T-bills is that there is a weekend between purchase and settlement date, giving me 4 or 5 days of double interest (from my bank and from my T-bill). It isn’t much money, but fun to do. If I had billions, I would only buy 4-month T-bills.

The issue with Zelle is many smaller banks & credit unions don’t use it.

I have memberships with two credit unions, either of which participate in the Zelle network.

It otherwise seems like a great alternative to ACH/debit/Paypal etc.

ACH sucks. Recently had my entire Wells Fargo account stolen from Post Office criminals. Opened a new one with same bank and the ACH transfers went over to my new account and stole additional money out of there. The only solution was to close out my entire checking account with Wells Fargo. Putting ACH transfers on your checking account is like playing Russian Roulette.

Wells Fargo. ‘Nuff said.

A small bank we do business with has a check writing service that’s *free*…. drawn against your account but they produce the check and mail it. That check has a blind account number on it. The thieves can wash it all they want. There’s nothing in that account until the check is presented and, if the amount doesn’t match their records…. it bounces.

Howdy Folks. The Banksters have had this figured out long ago. Legalized loan sharking, at high interest rates. Meanwhile savers earned less than 1 % for over a decade…….. Mr Wolfs reports, in my opinion, continue proving, higher for longer, is here to stay…………

DM: America’s savings rate divide – Only a third of middle-income earners have moved their cash into higher-yield accounts – despite big banks stiffing savers with ‘pitiful’ 0.01% interest while tech firms offer ‘deals’ above 4%

Despite inflation concerns and aggressive interest rate hikes by the Federal Reserve, only 32 percent of middle-income Americans have moved their funds since March, according to a new survey.

@SoCalBeach…

I looked into the top banks data (From sources such as S&P Global) during the Signature/SVB/etc collapse wave:

For the top 50 banks in the US as of 1Q23, Deposits are ONLY 60% of assets for banks. 40% of assets come from “wholesale” sources

like:

•Federal Funds Market (“Fed Funds”)

•Repurchase Agreements

•Federal Reserve Banks

•Advances from Federal Home Loan Bank

•Negotiable Certificates of Deposit

•Commercial Paper Market

•Eurocurrency Deposit market

•Long-Term Nondeposit Funds Sources

etc.

Further, WITHIN the deposits category,…..ONLY ~30% of deposits at the top banks are classified as balances of $250K or less! 70% of deposits are….yuuuge…likely NOT mom and pop / average american! Consider the average individual American’s savings… and likely the average is well well below $250K…maybe more like 50K!

It’s not “our” money in there that matters. Its’ not people that they care about!

Howdy SoCal… Maybe they can t move the $$$?? Tax issues and such…

SoCal, I’m one of those middle income earners you mention who have moved cash into higher yielding accounts.

The backstory:

I came across a website called WeissRatings a couple of months ago. It gave my credit union a D- rating. I promptly opened new accounts at a different credit union that Weiss rated as a B+.

After my direct deposits successfully appeared in my new credit union accounts, I then closed all my accounts at the former credit union.

My former credit union paid the pitiful 0.01% on my savings account; the new credit union pays 2.127%, which is better.

But then I found TreasuryDirect, which is paying almost 5.5% on four week and longer T-Bills. I’m hoping those rates continue to go higher.

Now I’m buying those instead and I’ve been quite pleased with my decision to move my money.

HotTub. Thanks for the link. I wonder if they also rate insurance companies? Now I just need to figure out how to navigate the site.

Bauer Financial has a similar rating site for both credit unions and banks. I use it when I evaluate the financial institutions offering the brokered CD’s on our brokers’ sites.

In India credit cards are also hugely pushed on the middle class. Debit cards are around quite long: you can’t go negative on those. Now cardless payment and even ATM cash withdrawal are coming up fast utilizing your mobile phone camera as QR code scanner.

Cashless society will never happen here: the majority of voters will turn against you. Local groups of known people (~20-50) organized their own cash loan / savings network, call chit, since centuries.

But why are your trains so bad?

Fix the trains. Choo choo

MW: Bank ETFs slide after credit downgrades, warnings rattle sector

Interesting to see limits growing at a faster pace then balances.

Thinking this might have to do with higher income levels. In my experience the higher stated income for a credit card app the higher the limit offered.

If that’s the case that tells me this inflationary environment will linger longer as it’ll take a while to go through all that available credit

“I think it boils down to the simple fact that banks refuse to give up the ‘float’ — the day or two of free money they get by sitting on a gazillion transfers every day.”

This is why you’re one of the best financial reporters on the internet. What a simple explanation for institutionalized greed. I always wondered, in this day in age where ones and zeros fly by in an instant… the money takes days and days to get into a different account.

In Canada(*), a lawsuit has broken the CC terms that forbid different prices based on payment methods. This, merchants are now free to pass on the surcharge to customers right on the bill(**) if they pay with Visa, MC, etc. Not all will, of course, but I suspect it’ll become more and more common because it’ll allow lower sticker/advertised prices and competition will encourage that. Using your debit card may save you 2-4% right at the sale.

Wolf, I’m curious about your thoughts on the effect this will have, if any.

*) Canada… except Quebec… where i happen to live.

We in Massachusetts can not add the fees to purchases. However, we can offer discounts for cash. This effectively raises prices to cover fees, and so many no longer use cash!

An investigation into the Employee Retention Credit (ERC) that has been extended into 2025 may reveal a rather large source of money still being pumped into the economy.

A recent article in the NYT, among other sources, claim that a cottage industry of thousands of financial service advisor tax credit “mills” has fueled a run for this money. The “advisors” are pushing these credits on businesses and charging up to 25% for their service fee. The article states that “these guys are preying on people and promising them the moon.”

By in large, my understanding, is that most recipients are not eligible for the credits. However, the IRS rules are complicated and it would take an audit by the IRS to discover the fraud and claw back the money. So, the strategy appears to be grab the money and run. If audited, deal with the fall out then. Of course, the “advisor” would have already taken its 25%. Good luck with getting that back.

This new “cesspool of fraud” as it has been called is “the worse kept secret of corporate America and fiscal authorities.” It has been reported that in June $29 billion has gone out to these mostly bogus claims. In July $33 billion.

If this trend continues it is estimated on an annual basis up to $400 billion by the end of the year. That would be 1.5% of GDP all on its own.

The IRS has now started to aggressively investigate these ERC scams, and that’s easy to do. It’s not complicated to nail these entities for fraud. We’ll see a bunch of fraud charges brought against them.

I get 3 to 4 calls, plus emails each week. They always open with the line “the IRS has mandated that you receive credit”. One look at the IRS website will clarify what is required to claim any credit. In reviewing, wasn’t worth the bookkeeping/accountant fees. Plus, remember, it is taxable income!

Interestingly in other news the feds are pursuing PPP loan fraud and they are not going to criminally charge these people.

They do not have the resources, so they will be seeking civil penalties. And civil penalties can recoup 2-3x the original amount stolen with fines.

Article in the NYT about it

Your comment on these reports not breaking out balances of the monthly paid with no interest vs those that carry interest bearing balances is spot on in my opinion.

I have zero debt and two credit cards. In the past year, we switched from checks, and a bank debit card to virtually all purchases and payments are made via these two cards and they are paid in full montly.

Once a month I pay them off electronically. I guess I contributed to that “increase in CC balances” just by switching to 99% of my transactions now via my existing CCs. Is that true?

We write zero checks anymore. All bills are paid by credit card. We get 2% back and, where there’s a CC surcharge, the 2% usually offsets it. The two credit cards we use are paid by ACH.

With all the check washing fraud (USPS even announced they couldn’t guarantee the safety of your check in the mail), it’s just not worth the potential risk.

El Katz

There is a massive check fraud ring operating here in the Washington DC Metro area as we speak. Checks are stolen out of the Post office, washed and cashed at banks by insiders in the bank. I had the cops out here the other day and she said she gets 3 calls a day for the same crime. Banks are in on it. They launder the stolen checks. They are so incompetent that I believe they are making money on all the fraud. Note, most banks post your account number on your monthly statements and anyone can read it and start charging vendor purchases.

Remedy, I have one checking account for paying bills and keep the balance less than 1K, so that’s all the crooks can get. The rest of my money is locked up in savings accounts and CDs.

Just make sure you don’t have overdraft protection on that checking account. Otherwise, your other accounts could be tapped to avoid “overdraft fees” on a check that you didn’t write. Our accounts are isolated just for that reason.

Yes, everyone I know is that way. No one I know carries interest-accruing balances on their credit cards.

The situation that might cause their kids to borrow on their credit cards is after they buy a house and have to furnish it. They’re house poor and will struggle for a few months to pay that off. And then they get it behind them.

AS ALWAYS CONFUSED,

I keep reviewing data and article that state 401K companies are seeing a large increase in hardship loans requests because consumers are cash strapped. The chart states we are at 8% (rounded up) of credit card debt as a % of disposable income.

I feel the pinch on purchasing groceries for my family even on a credit card. It is still very expensive and my disposable income has not kept up with inflation.

I still haven’t purchased a vehicle – driving my old 2014 – because vehicle prices and home prices are very high.

How is the consumer not cash strapped? What am I missing Wolf? I only see Drunken Sailors?

Since you’re “confused,” let me help you clear this up. Seems you’ve never had a 401k.

1. You have to distinguish between “loans” and “hardship distributions,” which is not a loan. And I will do that here.

2. Average 401k balance in Q2 jumped by $7,250 from year end, to $82,300.

3. In 2Q, more participants increased vs. decreased their contribution rate: 10.2% increases their contributions vs. 2.2% decrease their contributions. The increases were led by Generation Z and Millennials.

4. So there’s that… account balances are growing, and contributions are growing.

5. Number of participants taking a “hardship distribution” during 2Q = 0.5% of all participants, which is minuscule, but it was up from an even more minuscule 0.4% in Q4. Average amount of distribution fell to $5,050 from $5,400 a year ago.

6. Much more common are “loans” from your 401k (not all plans allow them). Friend of mine did that years ago for a down-payment of a house, which is very common, free (the interest you pay goes back to your account), and easy to do. People use it also for down-payments on a car, to buy furniture for their new house, etc. You have to pay it back, though, or else there are tax consequences.

People would be nuts borrowing at 7% to buy a car or borrowing at 7% for a down-payment of a house, if they can borrow from themselves at 0% (the interest you pay goes back to your own account). People squirrel away a big part of their income in these accounts, because it saves a lot of taxes, and because of company matching, and if they need a big pile of cash to pay for something, they borrow from themselves at 0%.

Number of people taking out regular loans from their 401K was 2.5% of all participants, up from 1.9%. average amount of $8,550, roughly unchanged.

BofA tracks the data on 401k:

https://business.bofa.com/content/dam/flagship/workplace-benefits/id20_0905/documents/Participant-Pulse.pdf

Thanks Wolf, always helpful! These headline articles are so misleading.

I’m sort of cash strapped as well. So don’t feel too bad they’re Mr. Confused. Groceries are insane! I only shop the sales, sometimes going twice in a week to double up the pantry with what’s on sale. That way you can have 6 months worth of the sale item at sale prices. And not have to grab 1 or 2 items at non sale prices. Cook at home too, never get delivery and stay off of the tip merry go round.

I have no idea when the Vice on some of our wallets will let up.

///

Is it possible to see credit card balances vs. credit scores (the first chart broken down by credit score class)? Though the delinquencies are most frequent, I would not expect the lowest credit score group to have the most debt incurred.

///

Credit card balances are a function of paying for stuff, because credit cards are a universal payment method. In 2021, $5 trillion was paid for with credit cards in the US, and very little got stuck as interest-accruing debt. I made a big deal out of this in the article.

So what you should ask: the balances of “interest-accruing credit-card debt” by credit score.

But we don’t even get balances of interest-accruing credit card debt at all. This is not broken out in the monthly and quarterly data. So we don’t know the balances of interest-accruing credit card debt, neither overall nor by credit score. I would love to have this data!

Wolf,

How do you know that “most” credit card balances never incur an interest charge? I’m asking because I recently got into an argument with a YouTube host who takes the contrary position. Thanks.

The short answer: only about 28% of adult consumers (18 and over) have one or more credit cards that accrue interest:

The long answer in detail:

https://wolfstreet.com/2023/08/19/how-many-americans-have-interest-bearing-credit-card-debt/